Time-Driven Activity-Based Costing Report for Business Management

VerifiedAdded on 2020/05/28

|13

|2504

|129

Report

AI Summary

This report examines Time-Driven Activity-Based Costing (TDABC) and its application within private organizations, using BHP Billiton as a case study. The report begins by defining TDABC and its advantages over traditional costing methods like Activity-Based Costing (ABC), highlighting its simplicity and ease of implementation. It then details the features of TDABC, including capacity cost and time estimation, and differentiates it from other costing models. The report analyzes how TDABC can address cost management challenges faced by companies like BHP Billiton, such as reducing operational costs and improving resource allocation. The report concludes by emphasizing TDABC's effectiveness in providing accurate cost information, streamlining operations, and enhancing decision-making in complex business environments. The structure of this report includes the discussion on suitability of TDABC on private organization operated in Australia. This report is referred to the client named BHP Billiton Plc. and it includes the brief information about the client, introduction of TDABC and its features, reliability of TDABC for client.

Running Head: Business Management 1

Business Management

Business Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Management 2

Executive summary:

This paper defines the meaning and other aspects of the time-driven activity based costing, and it

further states the reliability of this method of costing in the private organizations. For preparing

this report and for analyzing the reliability of this costing technique, we use BHP Billiton as the

case study. It is the simple technique which helps the organization in achieving its target in more

effective manner by removing the necessity of surveys and interviews for distributing the cost

related to resources to the activities. This technique of costing removes the faults of the original

model of activity based costing and also allocating the cost related to resources directly to the

object of the costs.

Executive summary:

This paper defines the meaning and other aspects of the time-driven activity based costing, and it

further states the reliability of this method of costing in the private organizations. For preparing

this report and for analyzing the reliability of this costing technique, we use BHP Billiton as the

case study. It is the simple technique which helps the organization in achieving its target in more

effective manner by removing the necessity of surveys and interviews for distributing the cost

related to resources to the activities. This technique of costing removes the faults of the original

model of activity based costing and also allocating the cost related to resources directly to the

object of the costs.

Business Management 3

Contents

Introduction:...............................................................................................................................................3

Client Information:......................................................................................................................................4

About TDABC:..............................................................................................................................................5

Features of TDABC:..................................................................................................................................5

Differences between TDABC & other costing models:.................................................................................6

TDABC & ABC:..........................................................................................................................................6

Traditional costing system & TDABC:.......................................................................................................7

TDABC for Client:.........................................................................................................................................8

Conclusion:..................................................................................................................................................9

Contents

Introduction:...............................................................................................................................................3

Client Information:......................................................................................................................................4

About TDABC:..............................................................................................................................................5

Features of TDABC:..................................................................................................................................5

Differences between TDABC & other costing models:.................................................................................6

TDABC & ABC:..........................................................................................................................................6

Traditional costing system & TDABC:.......................................................................................................7

TDABC for Client:.........................................................................................................................................8

Conclusion:..................................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Management 4

Introduction:

There are number of elements which creates unnecessary burden for the business units

such as providing quality of goods and services at lower cost to the consumers. These elements

includes high cost related to information, high demand in context of services related to digital,

economic slowdown, etc.. It becomes necessary for the management of the organization to

understand the aspects related to costs and other participation of costs in the organization for

evaluating the role of these elements in the organization and use these elements in the favor of

the organization (Kaplan & Anderson, 2003).

Cost management introduces various techniques, and one of the most reliable techniques

of the cost management is the Time-Driven Activity-Based Costing (TDABC). TDABC is

considered as important technique of the cost management because it helps the business

organization in the development of the exact cost information related to various activities

performed in the business unit. TDABC is not a new technique but it is the improved version of

the original model of the costing that is Activity based costing (ABC). Business organizations

required this improved version because of the shortcomings of the original ABC model. It

becomes difficult for the management to apply this traditional model of costing in their

organizations as it involves the high cost in context of interviews and surveys of the people.

Introduction:

There are number of elements which creates unnecessary burden for the business units

such as providing quality of goods and services at lower cost to the consumers. These elements

includes high cost related to information, high demand in context of services related to digital,

economic slowdown, etc.. It becomes necessary for the management of the organization to

understand the aspects related to costs and other participation of costs in the organization for

evaluating the role of these elements in the organization and use these elements in the favor of

the organization (Kaplan & Anderson, 2003).

Cost management introduces various techniques, and one of the most reliable techniques

of the cost management is the Time-Driven Activity-Based Costing (TDABC). TDABC is

considered as important technique of the cost management because it helps the business

organization in the development of the exact cost information related to various activities

performed in the business unit. TDABC is not a new technique but it is the improved version of

the original model of the costing that is Activity based costing (ABC). Business organizations

required this improved version because of the shortcomings of the original ABC model. It

becomes difficult for the management to apply this traditional model of costing in their

organizations as it involves the high cost in context of interviews and surveys of the people.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Management 5

Implementation of the traditional model of ABC is challenging for the organization

because of the complication level of this model. As stated above, TDABC is the improved

version of the original ABC model, and this version is based on the two factors that are unit cost

related to capacity of supplying and required time for conducting any activity or operation

(Basuki & Riediensyaf, 2014).

Structure of this report includes the discussion on suitability of TDABC on private

organization operated in Australia. This report is referred to the client named BHP Billiton Plc.

and it includes the brief information about the client, introduction of TDABC and its features,

reliability of TDABC for client. After all this discussion, report is concluded with brief

conclusion which summarizes all the important points.

Client Information:

BHP Billiton holds the position of top resource company across the globe, which is

involved in mining and handling of minerals, oil and gas. BHP employed 6000 workers and

employees mainly in countries like Australia and USA. Company sells its products and services

across the globe. Melbourne, Australia is the place where BHP established its main headquarter.

This company opts for Dual Listed Company structure which involves two parent companies that

are BHP Billiton Limited and BHP Billiton Plc. (BHP, n.d.).

About TDABC:

Generally, it is expected from the management of the business organizations that they

understand the cost behavior and manage the business accordingly. However, management can

only implement the cost model in effective manner if such model is easy to understand and if

Implementation of the traditional model of ABC is challenging for the organization

because of the complication level of this model. As stated above, TDABC is the improved

version of the original ABC model, and this version is based on the two factors that are unit cost

related to capacity of supplying and required time for conducting any activity or operation

(Basuki & Riediensyaf, 2014).

Structure of this report includes the discussion on suitability of TDABC on private

organization operated in Australia. This report is referred to the client named BHP Billiton Plc.

and it includes the brief information about the client, introduction of TDABC and its features,

reliability of TDABC for client. After all this discussion, report is concluded with brief

conclusion which summarizes all the important points.

Client Information:

BHP Billiton holds the position of top resource company across the globe, which is

involved in mining and handling of minerals, oil and gas. BHP employed 6000 workers and

employees mainly in countries like Australia and USA. Company sells its products and services

across the globe. Melbourne, Australia is the place where BHP established its main headquarter.

This company opts for Dual Listed Company structure which involves two parent companies that

are BHP Billiton Limited and BHP Billiton Plc. (BHP, n.d.).

About TDABC:

Generally, it is expected from the management of the business organizations that they

understand the cost behavior and manage the business accordingly. However, management can

only implement the cost model in effective manner if such model is easy to understand and if

Business Management 6

such model shows the changes occurred in the business on time. Traditionally, business

organizations used the original activity-based costing (OABC) for understanding the cost

behavior of the firm, but because of the shortcomings of this model organization required new

model. Latter, improved version of OABC is introduced by the experts and this new version

eliminates all the shortcomings of the OABC as it is completely different from the OABC.

However, it must be noted that OABC is considered as strong model of costing which is different

from products and services, but TDABC shows more differentiation and complexity in context of

products and services offered by company.

TDABC is the model which is simple in nature and easy to understand. It is easy for

management to understand and implement this model because it facilitates the high quality

information by eliminating the issues created by OABC (Stout & Propi, 2011).

Features of TDABC:

Presently, this model is considered as effective and efficient cost model for business

organization because it is possible to change the parameters of this model with changing business

environment. Two elements are considered by the TDABC, and these two elements are unit cost

related to capacity of supplying and required time for conducting any activity or operation. Both

the parameters are discussed in detail:

Capacity cost- TDABC initiates its working by recognizing various classes of resources

related to performance of activities in the organization. Measuring of capacity related to

resources is done on the basis of time availability and time-driven approach. This parameter is

calculated by using the formula stated below:

Capacity cost rate- Cost of capacity supplied/ practical capacity of resources supplied.

such model shows the changes occurred in the business on time. Traditionally, business

organizations used the original activity-based costing (OABC) for understanding the cost

behavior of the firm, but because of the shortcomings of this model organization required new

model. Latter, improved version of OABC is introduced by the experts and this new version

eliminates all the shortcomings of the OABC as it is completely different from the OABC.

However, it must be noted that OABC is considered as strong model of costing which is different

from products and services, but TDABC shows more differentiation and complexity in context of

products and services offered by company.

TDABC is the model which is simple in nature and easy to understand. It is easy for

management to understand and implement this model because it facilitates the high quality

information by eliminating the issues created by OABC (Stout & Propi, 2011).

Features of TDABC:

Presently, this model is considered as effective and efficient cost model for business

organization because it is possible to change the parameters of this model with changing business

environment. Two elements are considered by the TDABC, and these two elements are unit cost

related to capacity of supplying and required time for conducting any activity or operation. Both

the parameters are discussed in detail:

Capacity cost- TDABC initiates its working by recognizing various classes of resources

related to performance of activities in the organization. Measuring of capacity related to

resources is done on the basis of time availability and time-driven approach. This parameter is

calculated by using the formula stated below:

Capacity cost rate- Cost of capacity supplied/ practical capacity of resources supplied.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Management 7

Estimation of Time- in this organization determines the time required for performing any

particular activity, and there is no need to calculate the exact time, organization can determine

the close estimation of time.

As define, TDABC is the new and better model in comparison of OABC, and some of the

advantages of this model are stated below:

1. TDABC is the model which is less complex in nature, and easy to understand and

implement.

2. This model provides high quality data, and integrates with the organization data in easy

manner.

3. Less expansive and very low cost is required to maintain and update this model Garvais,

Levant & Ducrocq 2010).

Differences between TDABC & other costing models:

This section of the report is divided into two parts; first part defines the difference

between the TDABC and original model of ABC. On the other hand, second part of this section

defines the difference between TDABC and other traditional costing techniques.

TDABC & ABC:

Original model of ABC is the costing method which provides various facilities to the

business organization at initial stage, but after sometime it is noted that this model is not suitable

for large scale operations. OABC is the model which provides reliable option to the management

of the organization by distributing the costs to the consumers and products related to the services

of departments. This model also possesses some other disadvantages such as it is an expensive

Estimation of Time- in this organization determines the time required for performing any

particular activity, and there is no need to calculate the exact time, organization can determine

the close estimation of time.

As define, TDABC is the new and better model in comparison of OABC, and some of the

advantages of this model are stated below:

1. TDABC is the model which is less complex in nature, and easy to understand and

implement.

2. This model provides high quality data, and integrates with the organization data in easy

manner.

3. Less expansive and very low cost is required to maintain and update this model Garvais,

Levant & Ducrocq 2010).

Differences between TDABC & other costing models:

This section of the report is divided into two parts; first part defines the difference

between the TDABC and original model of ABC. On the other hand, second part of this section

defines the difference between TDABC and other traditional costing techniques.

TDABC & ABC:

Original model of ABC is the costing method which provides various facilities to the

business organization at initial stage, but after sometime it is noted that this model is not suitable

for large scale operations. OABC is the model which provides reliable option to the management

of the organization by distributing the costs to the consumers and products related to the services

of departments. This model also possesses some other disadvantages such as it is an expensive

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Management 8

model and complex in nature. Elimination of OABC is not an option for the organizations

because concept of this model is useful and strong, and it provides huge potential for companies

in context of large scale operations. Later, simple approach of this model is developed by the

experts and this approach is known as the time-driven ABC. Difference between the OABC and

TDABC is stated below:

TDABC ABC

It is easy to maintain and update this system,

because maintaining and installation of this

model is not costly.

OABC model is an expensive model which

involves high maintenance cost.

Management applied and understands this

model easily.

This model is complex in nature.

Duration cost drivers is the parameter which is

used by the TDABC.

Transaction cost drivers is the method which is

used by OABC (Hayden, n.d.).

Traditional costing system & TDABC:

Traditional costing techniques used the application of indirect cost on products and this

cost is based on the preset overhead rate. In this overhead cost is considered on the basis of

single group which directly relates with indirect cost. It is suitable in the organizations where

indirect cost is low in comparison of direct costs. Various parameters are used by these methods

such as identification of indirect cost, estimation of that cost for specific time, selection of cost

driver, estimation of cost driver amount, etc. (Accounting Tools, 2015).

model and complex in nature. Elimination of OABC is not an option for the organizations

because concept of this model is useful and strong, and it provides huge potential for companies

in context of large scale operations. Later, simple approach of this model is developed by the

experts and this approach is known as the time-driven ABC. Difference between the OABC and

TDABC is stated below:

TDABC ABC

It is easy to maintain and update this system,

because maintaining and installation of this

model is not costly.

OABC model is an expensive model which

involves high maintenance cost.

Management applied and understands this

model easily.

This model is complex in nature.

Duration cost drivers is the parameter which is

used by the TDABC.

Transaction cost drivers is the method which is

used by OABC (Hayden, n.d.).

Traditional costing system & TDABC:

Traditional costing techniques used the application of indirect cost on products and this

cost is based on the preset overhead rate. In this overhead cost is considered on the basis of

single group which directly relates with indirect cost. It is suitable in the organizations where

indirect cost is low in comparison of direct costs. Various parameters are used by these methods

such as identification of indirect cost, estimation of that cost for specific time, selection of cost

driver, estimation of cost driver amount, etc. (Accounting Tools, 2015).

Business Management 9

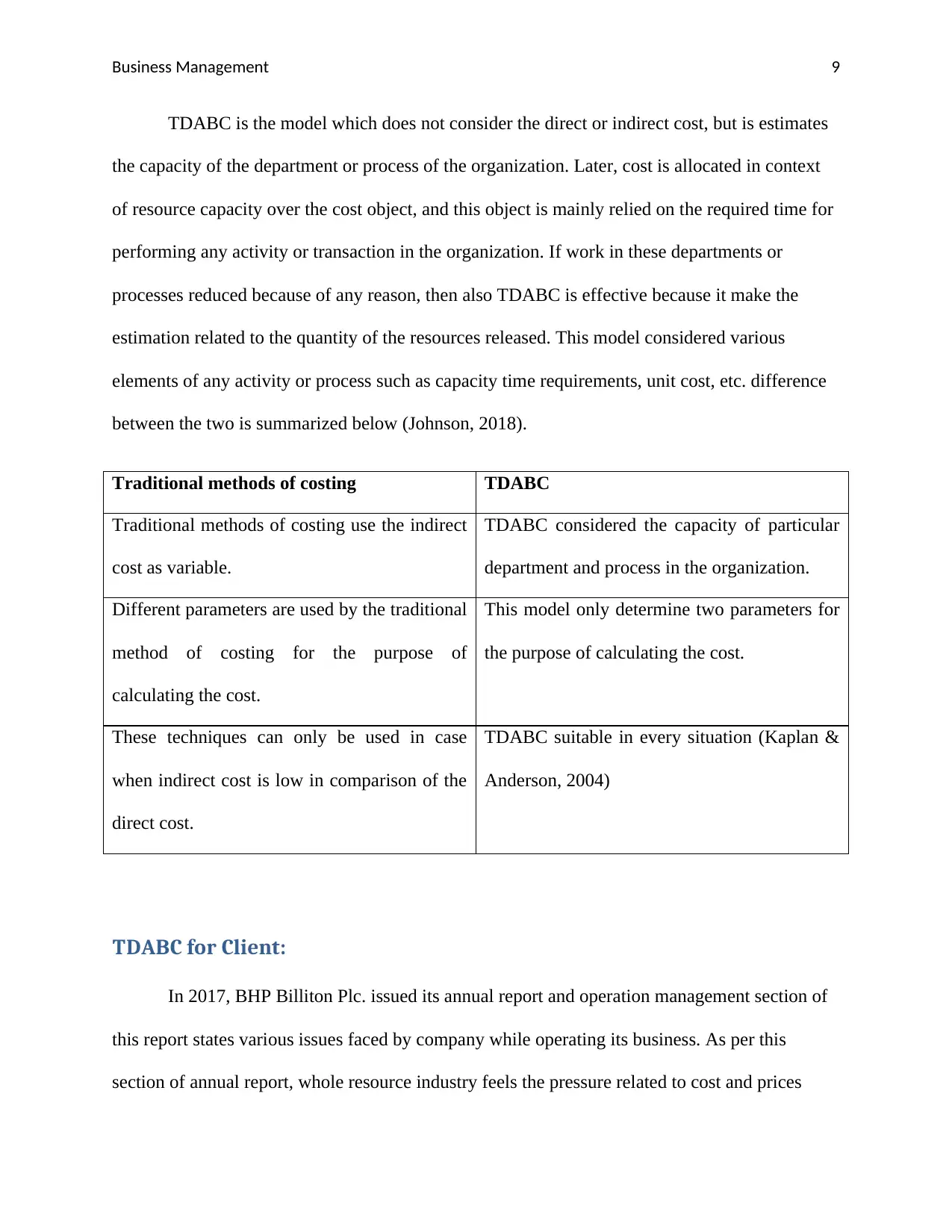

TDABC is the model which does not consider the direct or indirect cost, but is estimates

the capacity of the department or process of the organization. Later, cost is allocated in context

of resource capacity over the cost object, and this object is mainly relied on the required time for

performing any activity or transaction in the organization. If work in these departments or

processes reduced because of any reason, then also TDABC is effective because it make the

estimation related to the quantity of the resources released. This model considered various

elements of any activity or process such as capacity time requirements, unit cost, etc. difference

between the two is summarized below (Johnson, 2018).

Traditional methods of costing TDABC

Traditional methods of costing use the indirect

cost as variable.

TDABC considered the capacity of particular

department and process in the organization.

Different parameters are used by the traditional

method of costing for the purpose of

calculating the cost.

This model only determine two parameters for

the purpose of calculating the cost.

These techniques can only be used in case

when indirect cost is low in comparison of the

direct cost.

TDABC suitable in every situation (Kaplan &

Anderson, 2004)

TDABC for Client:

In 2017, BHP Billiton Plc. issued its annual report and operation management section of

this report states various issues faced by company while operating its business. As per this

section of annual report, whole resource industry feels the pressure related to cost and prices

TDABC is the model which does not consider the direct or indirect cost, but is estimates

the capacity of the department or process of the organization. Later, cost is allocated in context

of resource capacity over the cost object, and this object is mainly relied on the required time for

performing any activity or transaction in the organization. If work in these departments or

processes reduced because of any reason, then also TDABC is effective because it make the

estimation related to the quantity of the resources released. This model considered various

elements of any activity or process such as capacity time requirements, unit cost, etc. difference

between the two is summarized below (Johnson, 2018).

Traditional methods of costing TDABC

Traditional methods of costing use the indirect

cost as variable.

TDABC considered the capacity of particular

department and process in the organization.

Different parameters are used by the traditional

method of costing for the purpose of

calculating the cost.

This model only determine two parameters for

the purpose of calculating the cost.

These techniques can only be used in case

when indirect cost is low in comparison of the

direct cost.

TDABC suitable in every situation (Kaplan &

Anderson, 2004)

TDABC for Client:

In 2017, BHP Billiton Plc. issued its annual report and operation management section of

this report states various issues faced by company while operating its business. As per this

section of annual report, whole resource industry feels the pressure related to cost and prices

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Management 10

related to products are calculated by considering the commodity markets across the globe. It is

not possible for organization to eliminate this pressure of cost by increasing the price of the

product which ultimately results in adverse impact on the organization productivity. Various

efforts are made by the organization for decreasing their cost, but because of the direct

connection between the costs inputs made it impossible for organization to decrease their cost

and required time. It must be noted that cost related issues affect the operating margins of the

company (BHP, 2017).

It is possible for organization to solve these issues by adopting the costing technique

named as time-driven activity-based costing, as it helps the organization by improving the

capacity of resources group and by allocating the resources in adequate manner. Some of the

usage of TDABC in BHP Billiton is stated below:

It eliminates the need of interviews and surveys among the organization for determining

the define resources pools.

Model of TDABC facilitates the accuracy in accounts by using the time equations which

help the organization in dealing with complex issues related to business transaction. This

model help the organization in determining the accurate time for any activity and it also

remove the need to monitor the activities on continuous basis.

Processing times is decreased if organization use this model and this can be done by

using feeds related to data from ERP systems.

Complexity level of this model is low in compared to other cost techniques and it easy to

maintain and update this model.

related to products are calculated by considering the commodity markets across the globe. It is

not possible for organization to eliminate this pressure of cost by increasing the price of the

product which ultimately results in adverse impact on the organization productivity. Various

efforts are made by the organization for decreasing their cost, but because of the direct

connection between the costs inputs made it impossible for organization to decrease their cost

and required time. It must be noted that cost related issues affect the operating margins of the

company (BHP, 2017).

It is possible for organization to solve these issues by adopting the costing technique

named as time-driven activity-based costing, as it helps the organization by improving the

capacity of resources group and by allocating the resources in adequate manner. Some of the

usage of TDABC in BHP Billiton is stated below:

It eliminates the need of interviews and surveys among the organization for determining

the define resources pools.

Model of TDABC facilitates the accuracy in accounts by using the time equations which

help the organization in dealing with complex issues related to business transaction. This

model help the organization in determining the accurate time for any activity and it also

remove the need to monitor the activities on continuous basis.

Processing times is decreased if organization use this model and this can be done by

using feeds related to data from ERP systems.

Complexity level of this model is low in compared to other cost techniques and it easy to

maintain and update this model.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Management 11

BHP Billiton faces various issues while using the other costing techniques such as

overestimation of cost as it decrease the capacity usage of the resources. TDABC model is

suitable for the BHP as it helps the organization in increasing its productivity.

Conclusion:

This report highlights various significant aspects of the TDABC model in present

environment of the business and it also states the suitability of this model in the private

organizations like BHP Billiton Plc. it helps the organization in estimating the cost allocated to

each department and resources group of the organization, and it also help the management in

conducting their operations in planned manner. TDABC shows more differentiation and

complexity in context of products and services offered by company.

TDABC is the model which is simple in nature and easy to understand. It is easy for

management to understand and implement this model because it facilitates the high quality

information by eliminating the issues created by OABC.

BHP Billiton faces various issues while using the other costing techniques such as

overestimation of cost as it decrease the capacity usage of the resources. TDABC model is

suitable for the BHP as it helps the organization in increasing its productivity.

Conclusion:

This report highlights various significant aspects of the TDABC model in present

environment of the business and it also states the suitability of this model in the private

organizations like BHP Billiton Plc. it helps the organization in estimating the cost allocated to

each department and resources group of the organization, and it also help the management in

conducting their operations in planned manner. TDABC shows more differentiation and

complexity in context of products and services offered by company.

TDABC is the model which is simple in nature and easy to understand. It is easy for

management to understand and implement this model because it facilitates the high quality

information by eliminating the issues created by OABC.

Business Management 12

References:

Accounting Tools, (2015). Traditional Costing. Retrieved on 19th January 2018 from:

https://www.accountingtools.com/articles/what-is-traditional-costing.html.

Basuki, B. & Riediensyaf, M. (2014). The Application of Time-Driven Activity-Based Costing In

the Hospitality Industry: An Exploratory Case Study. JAMAR, Volume 12(1).

BHP, (2017). BHP Annual report 2017. Retrieved on 19th January 2018 from:

https://www.bhp.com/-/media/documents/investors/annual-reports/2017/

bhpannualreport2017.pdf.

BHP. About Us. Retrieved on 19th January 2018 from: https://www.bhp.com/our-approach/our-

company/about-us.

Garvais, M. Levant, Y. & Ducrocq, C. (2010). Time-Driven Activity-Based Costing (TDABC):

An Initial Appraisal through a Longitudinal Case Study. JAMAR, Volume 8(2).

Hayden, A. Activity-Based vs. Traditional Costing. Retrieved on 19th January 2018 from:

https://quickbooks.intuit.com/r/pricing-strategy/activity-based-vs-traditional-costing/.

References:

Accounting Tools, (2015). Traditional Costing. Retrieved on 19th January 2018 from:

https://www.accountingtools.com/articles/what-is-traditional-costing.html.

Basuki, B. & Riediensyaf, M. (2014). The Application of Time-Driven Activity-Based Costing In

the Hospitality Industry: An Exploratory Case Study. JAMAR, Volume 12(1).

BHP, (2017). BHP Annual report 2017. Retrieved on 19th January 2018 from:

https://www.bhp.com/-/media/documents/investors/annual-reports/2017/

bhpannualreport2017.pdf.

BHP. About Us. Retrieved on 19th January 2018 from: https://www.bhp.com/our-approach/our-

company/about-us.

Garvais, M. Levant, Y. & Ducrocq, C. (2010). Time-Driven Activity-Based Costing (TDABC):

An Initial Appraisal through a Longitudinal Case Study. JAMAR, Volume 8(2).

Hayden, A. Activity-Based vs. Traditional Costing. Retrieved on 19th January 2018 from:

https://quickbooks.intuit.com/r/pricing-strategy/activity-based-vs-traditional-costing/.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.