Tech (UK) Limited: Management Accounting and Financial Performance

VerifiedAdded on 2024/05/21

|17

|4310

|340

Report

AI Summary

This management accounting report analyzes the financial performance of Tech (UK) Limited, covering various aspects such as cost accounting systems, inventory management, job costing, and the presentation of financial information. It distinguishes between management and financial accounting, highlighting the importance of management accounting as a decision-making tool. The report includes an income statement prepared using both absorption and marginal costing methods, along with a discussion on budgeting advantages, disadvantages, and the preparation process. Finally, it recommends the balanced scorecard approach for a comprehensive analysis of the company's financial health, offering insights into improving financial strategies and operational efficiency. Desklib provides access to similar solved assignments and study resources for students.

MANAGEMENT ACCOUNTING

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The reports of management accounting have been prepared on taking the data on monthly basis.

Management accounting involves the devising planning, decision making, and performance

measurement system. This also provides expertise in financial reporting and also assists the

management to implement and formulate the organization's strategy. A brief analysis of different

types of budgets and costing system can be used in any type of the organization has been

discussed. The small business like Tech (UK) Limited the business owner generally focuses on

giving marketing effort. In order to evaluate the decisions, the accounting managers examine the

costs.

2

The reports of management accounting have been prepared on taking the data on monthly basis.

Management accounting involves the devising planning, decision making, and performance

measurement system. This also provides expertise in financial reporting and also assists the

management to implement and formulate the organization's strategy. A brief analysis of different

types of budgets and costing system can be used in any type of the organization has been

discussed. The small business like Tech (UK) Limited the business owner generally focuses on

giving marketing effort. In order to evaluate the decisions, the accounting managers examine the

costs.

2

Table of Contents

Introduction......................................................................................................................................4

Task 1.............................................................................................................................................5

A. Explanation of management accounting.................................................................................5

I. Distinguishing the management accounting from financial accounting...............................5

II. Importance of management accounting as a decision-making tool.....................................5

III. Cost accounting system......................................................................................................6

IV. Inventory Management System..........................................................................................7

V. Job Costing System.............................................................................................................7

B. Presentation of Financial information.....................................................................................8

I. Types of managerial accounting reports...............................................................................8

II. Importance of the information to be presented....................................................................9

Task 2...............................................................................................................................................9

Income Statement.........................................................................................................................9

I. Absorption costing methods..................................................................................................9

II. Marginal costing methods..................................................................................................11

Task 3.............................................................................................................................................13

A. Budget advantages and disadvantages..................................................................................13

B. Budget preparation process...................................................................................................14

C. Importance of budget.............................................................................................................14

Task 4.............................................................................................................................................15

Balanced Scorecard approach....................................................................................................15

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

3

Introduction......................................................................................................................................4

Task 1.............................................................................................................................................5

A. Explanation of management accounting.................................................................................5

I. Distinguishing the management accounting from financial accounting...............................5

II. Importance of management accounting as a decision-making tool.....................................5

III. Cost accounting system......................................................................................................6

IV. Inventory Management System..........................................................................................7

V. Job Costing System.............................................................................................................7

B. Presentation of Financial information.....................................................................................8

I. Types of managerial accounting reports...............................................................................8

II. Importance of the information to be presented....................................................................9

Task 2...............................................................................................................................................9

Income Statement.........................................................................................................................9

I. Absorption costing methods..................................................................................................9

II. Marginal costing methods..................................................................................................11

Task 3.............................................................................................................................................13

A. Budget advantages and disadvantages..................................................................................13

B. Budget preparation process...................................................................................................14

C. Importance of budget.............................................................................................................14

Task 4.............................................................................................................................................15

Balanced Scorecard approach....................................................................................................15

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Management accounting is a process of analyzing the business costs and business operations to

prepare the internal financial records, reports and also aids the decisions of the managerial

people. This development of the accounting system helps in terms of achieving the business

goals. Management accounting system measures and defines the financial performance of the

business industries. In this report, a brief analysis on the Tech (UK) Limited has been taken for

financial study. Finally, the balanced scorecard has been recommended for the organization to

make an analysis of the financial health.

Task 1

A. Explanation of management accounting

Management accounting helps in providing the timely statistical and financial information to the

business managers. This system helps to prepare the financial reports and the managers of the

organization will be able to make short-term managerial decisions in day to day activities.

Maintenance of solid accounting practices is essential for the business growth (Andre et al. 2016,

p.150).

I. Distinguishing the management accounting from financial accounting

Managerial accounting is also named as cost or managerial accounting system and that generally

differs from the financial accounting. Management accounting produces the business reports for

the internal stakeholders of the company as opposed to the external stakeholders. The results

derived from the management accounting are termed as periodic reports for the managers and

CEO of the organization. Management accounting system generally includes the details of

organizations cash, generated sales revenue, accounts payables and receivables.

Management accounting and financial accounting generally differs from the information

available inside it in the number of ways. The reports of financial accounting generally based on

the historical data, whereas the management reports are primarily focused on looking forward

(Anelli and Puglisi, 2015, p.409). Financial accounting reports and statements are publicly

reported whereas the management accounting systems are used for internal use only and also

kept confidential in the organization.

4

Management accounting is a process of analyzing the business costs and business operations to

prepare the internal financial records, reports and also aids the decisions of the managerial

people. This development of the accounting system helps in terms of achieving the business

goals. Management accounting system measures and defines the financial performance of the

business industries. In this report, a brief analysis on the Tech (UK) Limited has been taken for

financial study. Finally, the balanced scorecard has been recommended for the organization to

make an analysis of the financial health.

Task 1

A. Explanation of management accounting

Management accounting helps in providing the timely statistical and financial information to the

business managers. This system helps to prepare the financial reports and the managers of the

organization will be able to make short-term managerial decisions in day to day activities.

Maintenance of solid accounting practices is essential for the business growth (Andre et al. 2016,

p.150).

I. Distinguishing the management accounting from financial accounting

Managerial accounting is also named as cost or managerial accounting system and that generally

differs from the financial accounting. Management accounting produces the business reports for

the internal stakeholders of the company as opposed to the external stakeholders. The results

derived from the management accounting are termed as periodic reports for the managers and

CEO of the organization. Management accounting system generally includes the details of

organizations cash, generated sales revenue, accounts payables and receivables.

Management accounting and financial accounting generally differs from the information

available inside it in the number of ways. The reports of financial accounting generally based on

the historical data, whereas the management reports are primarily focused on looking forward

(Anelli and Puglisi, 2015, p.409). Financial accounting reports and statements are publicly

reported whereas the management accounting systems are used for internal use only and also

kept confidential in the organization.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

II. Importance of management accounting as a decision-making tool

Small businesses like Tech (UK) Limited managers are facing countless decisions on day to day

activities. Management accounting system generally uses the information from the business

operations in order to produce the reports. These produced business reports provide ongoing

insight into the performance of the business (Avenali et al. 2017, p.130). Labor utilization and

profit margins are some of the business resulted in activities from the end of the management

accounting systems decisions. The managers of the Tech (UK) Limited must have the data-

driven inputs to make valuable decisions. As per the comment of Cooper et al. (2017, p.995), the

decision-making process generally helps the enterprise to achieve higher profitability and to gain

competitive advantages. There are various activities to be performed by the managerial people

using decision-making tool in management accounting.

Relevant cost analysis: management accounting system helps the organization to make

decisions related to what needs to be sold and how to sell the organizational products and

services into the market. This process has been involved in the management accounting. Based

on the decision making the discontinuity and adding the product line into the business operations

also judged and decided.

Making buy analysis: managerial accounting system provides the basic information related to

manufacturing the products. The make and buy analysis determines the most profitable products

selected for the organization.

Utilizing the data:

Management accounting system provides the valuable data for the balanced scorecard, financial

statements projections and budget statements. This in term helps the organization to guide for

future. Based on this information the managers can make decisions to aim for continuous

improvement.

Analyzing activity-based costing techniques:

As per the comment of Flannery (2016, p.16), the activity based business technique determines

the business needs and whom to sell the products. This is a part of management accounting

system that in term helps to make decisions on determining the product line. This helps in

deciding who the potential customers for the business firm are. The less profitability form the

business will allow the managers to take decisions on paying more attention to the advertising

media and promotional channels.

5

Small businesses like Tech (UK) Limited managers are facing countless decisions on day to day

activities. Management accounting system generally uses the information from the business

operations in order to produce the reports. These produced business reports provide ongoing

insight into the performance of the business (Avenali et al. 2017, p.130). Labor utilization and

profit margins are some of the business resulted in activities from the end of the management

accounting systems decisions. The managers of the Tech (UK) Limited must have the data-

driven inputs to make valuable decisions. As per the comment of Cooper et al. (2017, p.995), the

decision-making process generally helps the enterprise to achieve higher profitability and to gain

competitive advantages. There are various activities to be performed by the managerial people

using decision-making tool in management accounting.

Relevant cost analysis: management accounting system helps the organization to make

decisions related to what needs to be sold and how to sell the organizational products and

services into the market. This process has been involved in the management accounting. Based

on the decision making the discontinuity and adding the product line into the business operations

also judged and decided.

Making buy analysis: managerial accounting system provides the basic information related to

manufacturing the products. The make and buy analysis determines the most profitable products

selected for the organization.

Utilizing the data:

Management accounting system provides the valuable data for the balanced scorecard, financial

statements projections and budget statements. This in term helps the organization to guide for

future. Based on this information the managers can make decisions to aim for continuous

improvement.

Analyzing activity-based costing techniques:

As per the comment of Flannery (2016, p.16), the activity based business technique determines

the business needs and whom to sell the products. This is a part of management accounting

system that in term helps to make decisions on determining the product line. This helps in

deciding who the potential customers for the business firm are. The less profitability form the

business will allow the managers to take decisions on paying more attention to the advertising

media and promotional channels.

5

III. Cost accounting system

As stated by Fürst et al. (2014, p.1440), the cost accounting system is used by the enterprise to

record the production activities using the perpetual inventory system. Cost accounting systems

are generally designed to track the flow of inventory in a continuous manner following the

various stages of production.

Actual Costing

Actual costing system records the product cost based on the actual cost of labor, material and

incurred costs allocated to the firm. This costing system takes a longer time to evaluate the cost

of sold goods and ending inventory as all the actual costs need to compile for study.

Normal Costing

Normal costing technique is used to tally the manufactured products with the actual material

costs and the actual direct labor costs and the manufactured overhead rate based on the

manufacturing overhead. The cost associated with the normal costing is referred to as the product

costs and also used for inventory evaluation and cost of goods sold. The difference is referred as

variance in case there is any presence of difference among the overhead costs actually incurred

to the overhead cost assigned to the products.

Standard Costing

Standard costing is generally related to the manufacturing costs with predetermined material

costs, direct labor cost and manufacturing overhead cost. In case the actual cost varies slightly

significant from the standard cost the variances will be assigned to the cost of sold goods.

IV. Inventory Management System

Inventory management system in an organization tracks available goods through a portion of the

prepared business and from the entire supply chain involved in the operation. This in term covers

warehousing to shipping, production to retail and form the movement of stocks to the market.

The business firm is able to see moving parts from the operation to market through the different

supply chain. Inventory management system acts as a key component in the supply chain and

also facilitates the point of sales. The inventory management system of Tech (UK) Limited

tracks the products volume and also makes aware the enterprise regarding supply chain

management system status.

6

As stated by Fürst et al. (2014, p.1440), the cost accounting system is used by the enterprise to

record the production activities using the perpetual inventory system. Cost accounting systems

are generally designed to track the flow of inventory in a continuous manner following the

various stages of production.

Actual Costing

Actual costing system records the product cost based on the actual cost of labor, material and

incurred costs allocated to the firm. This costing system takes a longer time to evaluate the cost

of sold goods and ending inventory as all the actual costs need to compile for study.

Normal Costing

Normal costing technique is used to tally the manufactured products with the actual material

costs and the actual direct labor costs and the manufactured overhead rate based on the

manufacturing overhead. The cost associated with the normal costing is referred to as the product

costs and also used for inventory evaluation and cost of goods sold. The difference is referred as

variance in case there is any presence of difference among the overhead costs actually incurred

to the overhead cost assigned to the products.

Standard Costing

Standard costing is generally related to the manufacturing costs with predetermined material

costs, direct labor cost and manufacturing overhead cost. In case the actual cost varies slightly

significant from the standard cost the variances will be assigned to the cost of sold goods.

IV. Inventory Management System

Inventory management system in an organization tracks available goods through a portion of the

prepared business and from the entire supply chain involved in the operation. This in term covers

warehousing to shipping, production to retail and form the movement of stocks to the market.

The business firm is able to see moving parts from the operation to market through the different

supply chain. Inventory management system acts as a key component in the supply chain and

also facilitates the point of sales. The inventory management system of Tech (UK) Limited

tracks the products volume and also makes aware the enterprise regarding supply chain

management system status.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

V. Job Costing System

Job costing system is a process of accumulating the cost associated with specific products and on

services. Job costing is an accounting system for budget rates and manufacturing overheads. Job

cost record has been produced while taking the special order into account. In case of Tech (UK)

Limited, the job order costing has been used for manufacturing the mobile devices. The job

costing system in Tech (UK) Limited records the document costs in inventory process, finished

goods inventory and cost of sold goods from the enterprise.

B. Presentation of Financial information

I. Types of managerial accounting reports

Managerial accounting reports are the tools which help to analyze the business performance

quantitatively (Weygandt et al. 2015, p.10). Traditional accounting reports are generally

prepared for tax purposes whereas the managerial reporting has been sued for making a

collection of different types of data about the company's operation. Managerial accounting

reports can be following types which will be useful for the Tech (UK) Limited for improving the

financial health.

Budget Report

Using the budget reports the managers are able to analyze the control costs and departments

performance. Estimated budget in a target period of time is generally recorded in this report

based on the actual expenses occurs. This also has been used by the managers to provide an

incentive to their respective employees.

Job cost reports

These reports show expenses incurred on the assigned specific projects. Job cost reports are

matched with the estimated revenue in order to tally the profitability of the job. Higher earning

areas in the firm can be identified through this report. This report also helps in analyzing the

expense occurred while the project is in progress mode. The managers can be able to correct and

rectify the errors and areas of waste occur during the execution before the cost escalates.

Inventory and Manufacturing

Companies like Tech (UK) Limited must use the inventory managerial accounting report for

making the manufacturing process more efficient. These reports include the inventory wastes,

per unit overhead cost and hourly labor costs. The managers are responsible for comparing the

7

Job costing system is a process of accumulating the cost associated with specific products and on

services. Job costing is an accounting system for budget rates and manufacturing overheads. Job

cost record has been produced while taking the special order into account. In case of Tech (UK)

Limited, the job order costing has been used for manufacturing the mobile devices. The job

costing system in Tech (UK) Limited records the document costs in inventory process, finished

goods inventory and cost of sold goods from the enterprise.

B. Presentation of Financial information

I. Types of managerial accounting reports

Managerial accounting reports are the tools which help to analyze the business performance

quantitatively (Weygandt et al. 2015, p.10). Traditional accounting reports are generally

prepared for tax purposes whereas the managerial reporting has been sued for making a

collection of different types of data about the company's operation. Managerial accounting

reports can be following types which will be useful for the Tech (UK) Limited for improving the

financial health.

Budget Report

Using the budget reports the managers are able to analyze the control costs and departments

performance. Estimated budget in a target period of time is generally recorded in this report

based on the actual expenses occurs. This also has been used by the managers to provide an

incentive to their respective employees.

Job cost reports

These reports show expenses incurred on the assigned specific projects. Job cost reports are

matched with the estimated revenue in order to tally the profitability of the job. Higher earning

areas in the firm can be identified through this report. This report also helps in analyzing the

expense occurred while the project is in progress mode. The managers can be able to correct and

rectify the errors and areas of waste occur during the execution before the cost escalates.

Inventory and Manufacturing

Companies like Tech (UK) Limited must use the inventory managerial accounting report for

making the manufacturing process more efficient. These reports include the inventory wastes,

per unit overhead cost and hourly labor costs. The managers are responsible for comparing the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

different assembly lines within the targeted company and also able to analyze the business

process where it needs to be improved.

Accounts Receivable Aging

In order to manage the cash flow of the companies the Tech (UK) Limited must go for

undertaking the accounts receivable aging reports which extend the credit to customers.

Customer’s balances have been broken down into this report via calculating the number of days

owned (Sparks and Bradley, 2017, p.720). The aging report generally includes the invoices

columns of 30 days or 90 days or more time period. Analyzing this report the manager can be

able to pay the balances and also tightens the credit policies. Old debts can be overlooked

following this report analysis.

II. Importance of the information to be presented

The information present in the above report s must be recorded in an understandable manner.

This in terms helps the organization to make analyze the data at any point in time. In case the

managerial get replaced this understandable format helps other managers to get aware about the

information required to run the business process.

Task 2

Income Statement

An income statement is a form of a financial statement that in term reports the company's

financial performance over given period of time. The Tech (UK) Limited has been taken into

consideration in this report for making income statement analysis.

I. Absorption costing methods

As per the comment of Hackett and Hand (2016, p. 340), absorption costing method includes the

overall manufacturing costs like variable cost and fixed cost and the production cost has been

added to operating expenses. In case there is a constant change in variable cost then the total

production cost also gets vary while bringing change in the operational activity. The cost of the

sold good is calculated through adding the direct labor, operating overhead and direct material.

The variable manufacturing cost includes direct labor and direct material.

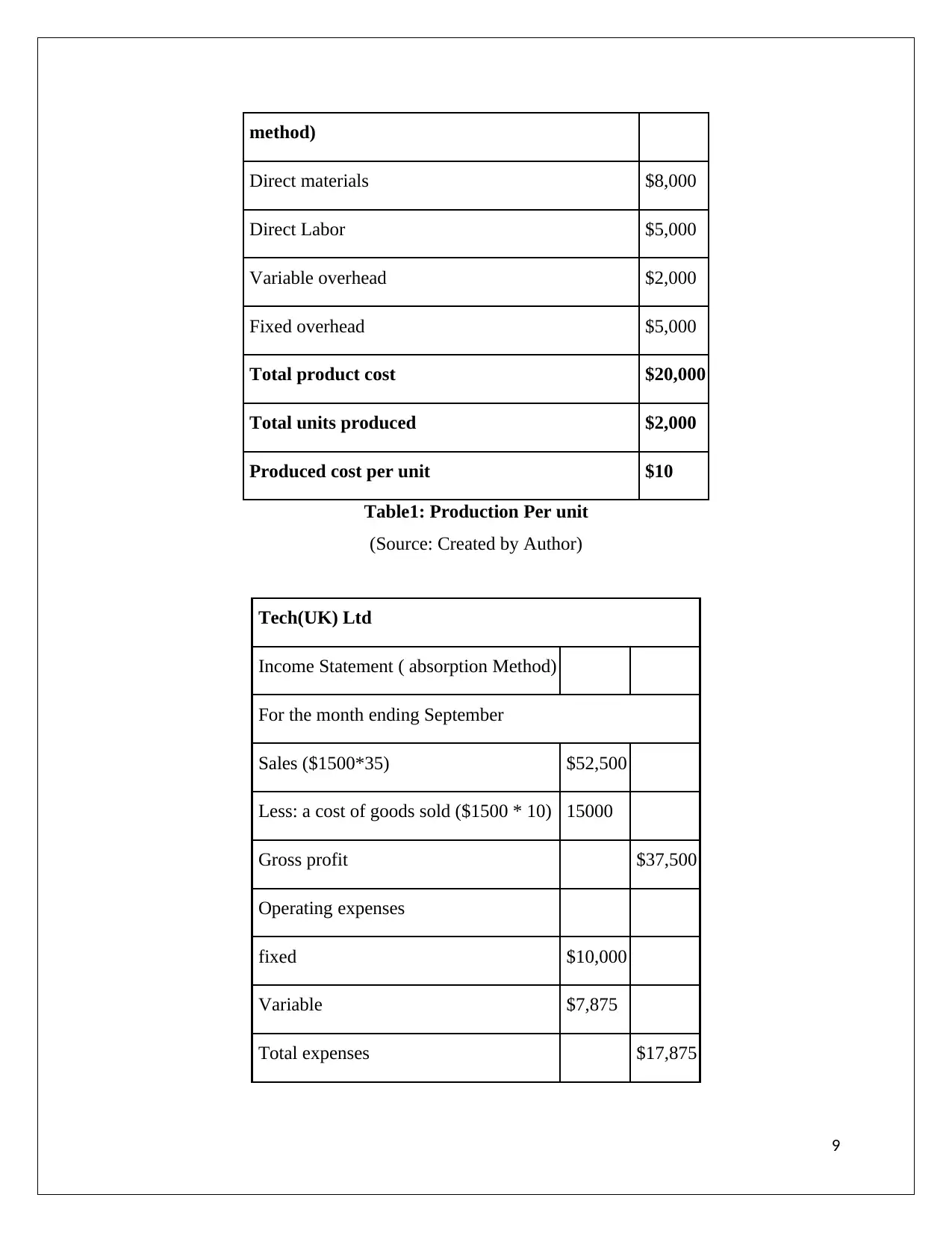

The production per unit for Tech (UK) Limited has been calculated in below manner.

Production per unit (absorption costing

8

process where it needs to be improved.

Accounts Receivable Aging

In order to manage the cash flow of the companies the Tech (UK) Limited must go for

undertaking the accounts receivable aging reports which extend the credit to customers.

Customer’s balances have been broken down into this report via calculating the number of days

owned (Sparks and Bradley, 2017, p.720). The aging report generally includes the invoices

columns of 30 days or 90 days or more time period. Analyzing this report the manager can be

able to pay the balances and also tightens the credit policies. Old debts can be overlooked

following this report analysis.

II. Importance of the information to be presented

The information present in the above report s must be recorded in an understandable manner.

This in terms helps the organization to make analyze the data at any point in time. In case the

managerial get replaced this understandable format helps other managers to get aware about the

information required to run the business process.

Task 2

Income Statement

An income statement is a form of a financial statement that in term reports the company's

financial performance over given period of time. The Tech (UK) Limited has been taken into

consideration in this report for making income statement analysis.

I. Absorption costing methods

As per the comment of Hackett and Hand (2016, p. 340), absorption costing method includes the

overall manufacturing costs like variable cost and fixed cost and the production cost has been

added to operating expenses. In case there is a constant change in variable cost then the total

production cost also gets vary while bringing change in the operational activity. The cost of the

sold good is calculated through adding the direct labor, operating overhead and direct material.

The variable manufacturing cost includes direct labor and direct material.

The production per unit for Tech (UK) Limited has been calculated in below manner.

Production per unit (absorption costing

8

method)

Direct materials $8,000

Direct Labor $5,000

Variable overhead $2,000

Fixed overhead $5,000

Total product cost $20,000

Total units produced $2,000

Produced cost per unit $10

Table1: Production Per unit

(Source: Created by Author)

Tech(UK) Ltd

Income Statement ( absorption Method)

For the month ending September

Sales ($1500*35) $52,500

Less: a cost of goods sold ($1500 * 10) 15000

Gross profit $37,500

Operating expenses

fixed $10,000

Variable $7,875

Total expenses $17,875

9

Direct materials $8,000

Direct Labor $5,000

Variable overhead $2,000

Fixed overhead $5,000

Total product cost $20,000

Total units produced $2,000

Produced cost per unit $10

Table1: Production Per unit

(Source: Created by Author)

Tech(UK) Ltd

Income Statement ( absorption Method)

For the month ending September

Sales ($1500*35) $52,500

Less: a cost of goods sold ($1500 * 10) 15000

Gross profit $37,500

Operating expenses

fixed $10,000

Variable $7,875

Total expenses $17,875

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

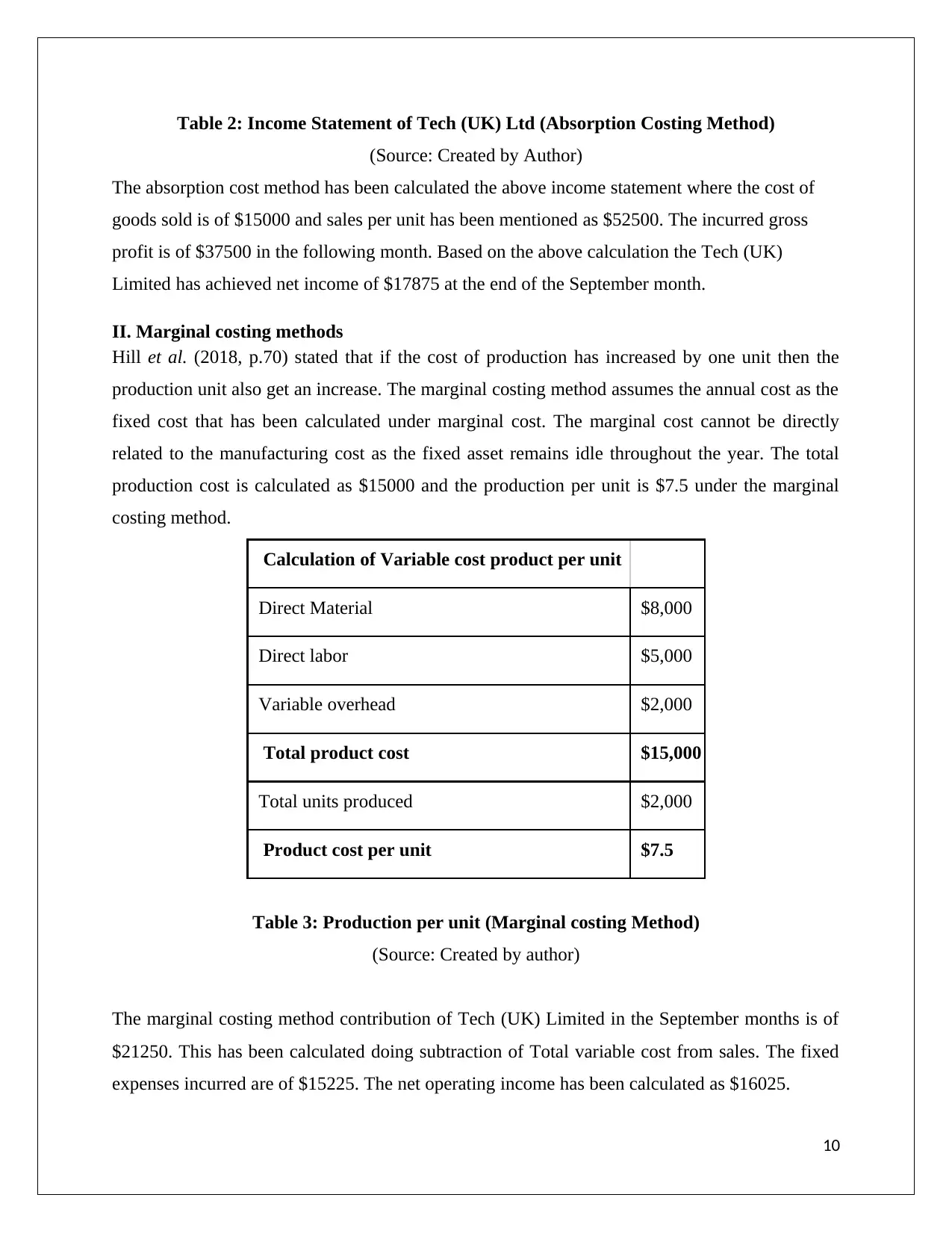

Table 2: Income Statement of Tech (UK) Ltd (Absorption Costing Method)

(Source: Created by Author)

The absorption cost method has been calculated the above income statement where the cost of

goods sold is of $15000 and sales per unit has been mentioned as $52500. The incurred gross

profit is of $37500 in the following month. Based on the above calculation the Tech (UK)

Limited has achieved net income of $17875 at the end of the September month.

II. Marginal costing methods

Hill et al. (2018, p.70) stated that if the cost of production has increased by one unit then the

production unit also get an increase. The marginal costing method assumes the annual cost as the

fixed cost that has been calculated under marginal cost. The marginal cost cannot be directly

related to the manufacturing cost as the fixed asset remains idle throughout the year. The total

production cost is calculated as $15000 and the production per unit is $7.5 under the marginal

costing method.

Calculation of Variable cost product per unit

Direct Material $8,000

Direct labor $5,000

Variable overhead $2,000

Total product cost $15,000

Total units produced $2,000

Product cost per unit $7.5

Table 3: Production per unit (Marginal costing Method)

(Source: Created by author)

The marginal costing method contribution of Tech (UK) Limited in the September months is of

$21250. This has been calculated doing subtraction of Total variable cost from sales. The fixed

expenses incurred are of $15225. The net operating income has been calculated as $16025.

10

(Source: Created by Author)

The absorption cost method has been calculated the above income statement where the cost of

goods sold is of $15000 and sales per unit has been mentioned as $52500. The incurred gross

profit is of $37500 in the following month. Based on the above calculation the Tech (UK)

Limited has achieved net income of $17875 at the end of the September month.

II. Marginal costing methods

Hill et al. (2018, p.70) stated that if the cost of production has increased by one unit then the

production unit also get an increase. The marginal costing method assumes the annual cost as the

fixed cost that has been calculated under marginal cost. The marginal cost cannot be directly

related to the manufacturing cost as the fixed asset remains idle throughout the year. The total

production cost is calculated as $15000 and the production per unit is $7.5 under the marginal

costing method.

Calculation of Variable cost product per unit

Direct Material $8,000

Direct labor $5,000

Variable overhead $2,000

Total product cost $15,000

Total units produced $2,000

Product cost per unit $7.5

Table 3: Production per unit (Marginal costing Method)

(Source: Created by author)

The marginal costing method contribution of Tech (UK) Limited in the September months is of

$21250. This has been calculated doing subtraction of Total variable cost from sales. The fixed

expenses incurred are of $15225. The net operating income has been calculated as $16025.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

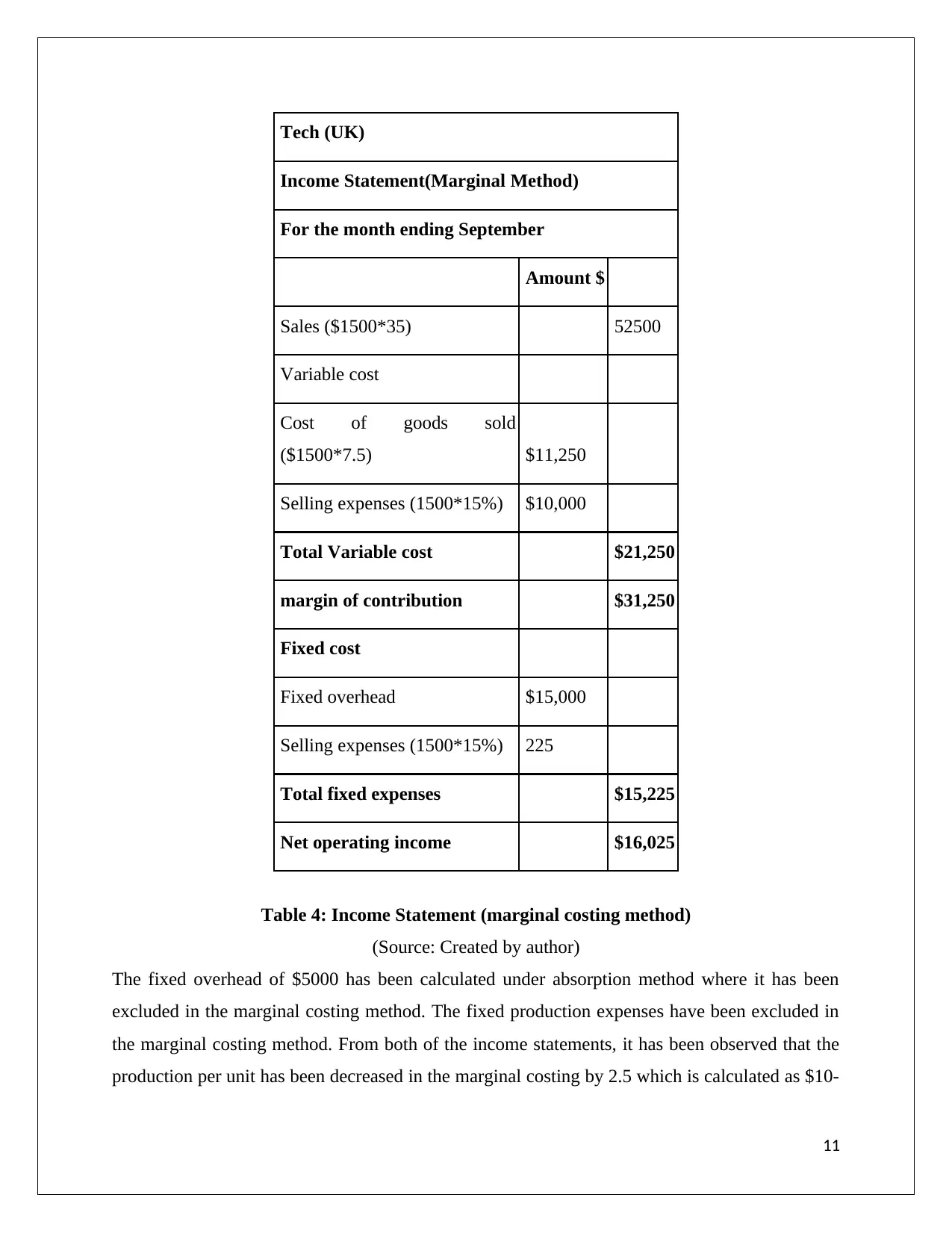

Tech (UK)

Income Statement(Marginal Method)

For the month ending September

Amount $

Sales ($1500*35) 52500

Variable cost

Cost of goods sold

($1500*7.5) $11,250

Selling expenses (1500*15%) $10,000

Total Variable cost $21,250

margin of contribution $31,250

Fixed cost

Fixed overhead $15,000

Selling expenses (1500*15%) 225

Total fixed expenses $15,225

Net operating income $16,025

Table 4: Income Statement (marginal costing method)

(Source: Created by author)

The fixed overhead of $5000 has been calculated under absorption method where it has been

excluded in the marginal costing method. The fixed production expenses have been excluded in

the marginal costing method. From both of the income statements, it has been observed that the

production per unit has been decreased in the marginal costing by 2.5 which is calculated as $10-

11

Income Statement(Marginal Method)

For the month ending September

Amount $

Sales ($1500*35) 52500

Variable cost

Cost of goods sold

($1500*7.5) $11,250

Selling expenses (1500*15%) $10,000

Total Variable cost $21,250

margin of contribution $31,250

Fixed cost

Fixed overhead $15,000

Selling expenses (1500*15%) 225

Total fixed expenses $15,225

Net operating income $16,025

Table 4: Income Statement (marginal costing method)

(Source: Created by author)

The fixed overhead of $5000 has been calculated under absorption method where it has been

excluded in the marginal costing method. The fixed production expenses have been excluded in

the marginal costing method. From both of the income statements, it has been observed that the

production per unit has been decreased in the marginal costing by 2.5 which is calculated as $10-

11

$7.5 compared to absorption costing. The net operating income also varied from $17875 to

$16025.

Absorption costing method has been recommended for Tech (UK) Limited for preparing the

annual income statement. In the inventory, the fixed cost can be carry forwarded as it remains

idle throughout the month.

Task 3

A. Budget advantages and disadvantages

Static budget

The static budget remains unchanged after changing the input units of the budget. A constant

drop in the sales may not impact the budget allocation and rise also may not have any impact.

Advantage:

Consistency

The bills of the Tech (UK) Limited has been planned to be paid in time.

Disadvantage:

Market stagnation not considered into account.

Cash Flow Budget

This budget manages working capital of enterprises.

Advantage:

Ensures cash inflow timely and regularly.

Disadvantage:

Inaccuracy in estimation.

Financial Budget

Ensures right type funds are available at the time of requirement.

Advantage:

Evaluates firm’s performance.

Disadvantage:

Time-consuming

Operating budget

Involves the cost related to the various operating activities of the business firms.

Advantage:

12

$16025.

Absorption costing method has been recommended for Tech (UK) Limited for preparing the

annual income statement. In the inventory, the fixed cost can be carry forwarded as it remains

idle throughout the month.

Task 3

A. Budget advantages and disadvantages

Static budget

The static budget remains unchanged after changing the input units of the budget. A constant

drop in the sales may not impact the budget allocation and rise also may not have any impact.

Advantage:

Consistency

The bills of the Tech (UK) Limited has been planned to be paid in time.

Disadvantage:

Market stagnation not considered into account.

Cash Flow Budget

This budget manages working capital of enterprises.

Advantage:

Ensures cash inflow timely and regularly.

Disadvantage:

Inaccuracy in estimation.

Financial Budget

Ensures right type funds are available at the time of requirement.

Advantage:

Evaluates firm’s performance.

Disadvantage:

Time-consuming

Operating budget

Involves the cost related to the various operating activities of the business firms.

Advantage:

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.