Management Accounting Report: Strategic Decisions for Tech (UK) Ltd

VerifiedAdded on 2024/05/17

|25

|4052

|316

Report

AI Summary

This management accounting report provides a detailed analysis of Tech (UK) Limited's financial performance, covering various aspects such as the differences between management and financial accounting, cost accounting systems, and inventory management. It includes an examination of managerial accounting reports, focusing on budget reports, job cost reports, and inventory/manufacturing reports, highlighting the benefits of management accounting systems like increased efficiency and cost transparency. The report also presents income statements using marginal and absorption costing methods, reconciles the differences between them, and discusses the importance of budgeting for planning and control, outlining the process for preparing a budget and its advantages and disadvantages. This comprehensive analysis aims to support strategic decision-making within the organization.

Management Accounting report for Tech (UK) Limited

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction.................................................................................................................................................3

TASK 1.......................................................................................................................................................4

TASK 2.......................................................................................................................................................9

TASK 3.....................................................................................................................................................12

Introduction...........................................................................................................................................12

Content..................................................................................................................................................13

Conclusion.............................................................................................................................................18

TASK 4.....................................................................................................................................................19

Conclusion.................................................................................................................................................23

REFERENCES..........................................................................................................................................24

2

Introduction.................................................................................................................................................3

TASK 1.......................................................................................................................................................4

TASK 2.......................................................................................................................................................9

TASK 3.....................................................................................................................................................12

Introduction...........................................................................................................................................12

Content..................................................................................................................................................13

Conclusion.............................................................................................................................................18

TASK 4.....................................................................................................................................................19

Conclusion.................................................................................................................................................23

REFERENCES..........................................................................................................................................24

2

Introduction

This report deals with the various fundamentals of management accounting which can apply to

the organisation so as to solve the financial problems and attain sustainable success. The

importance of the management accounting has been explained which can be used by the

managers for taking the strategic decisions in the organisation. Also, how the management

accounting is different from the financial accounting has been identified. The income statements

using the marginal and absorption cost has been prepared to evaluate the performance of the

organisation. With the benefits and limitations of the budget the proper procedure of preparing

the budget has also been highlighted.

3

This report deals with the various fundamentals of management accounting which can apply to

the organisation so as to solve the financial problems and attain sustainable success. The

importance of the management accounting has been explained which can be used by the

managers for taking the strategic decisions in the organisation. Also, how the management

accounting is different from the financial accounting has been identified. The income statements

using the marginal and absorption cost has been prepared to evaluate the performance of the

organisation. With the benefits and limitations of the budget the proper procedure of preparing

the budget has also been highlighted.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

A) Management accounting is the procedure of analyzing the cost and operations of the

business so as to prepare the internal financial reports which helps the managers of Tech

(UK) Ltd in taking the strategic decisions (Accounting Tools, 2017). Financial

accounting means analyzing the financial reports of the company to track the financial

tractions.

I)

Point of Distinction Management Accounting Financial Accounting

Focus It focuses on the decisions

which are to be made for the

future.

It focuses on the past to take

the decisions.

Scope The scope of the management

accounting is narrow.

Its scope is wide.

Primary Users Internal audience like

managers.

External audience like

investors.

Regulations GAAP and IFRS None

II) Management accounting information is the crucial part in the organisation for taking the

appropriate decisions. The results which arise from analyzing these statements will provide the

managers of the Tech (UK) Ltd an idea to plan their resources and profit margins accordingly

(Butterfield, 2016). Collecting the data from the various departments and then comparing those

with the actual or the budget one will help the organisation to enhance their performance

(Butterfield, 2016). The analyses of the reports can be done through various tools and techniques

some of which includes Key Performance Indicators (KPI’s), Benchmarks and balanced

Scorecard. The evaluation of the performance also helps in achieving the growth (Butterfield,

2016).

III) Cost accounting systems are a framework which is used by the organizations for analyzing

the cost of the products so as to predict the profit and valuate the stock. There are three cost

accounting systems:

4

A) Management accounting is the procedure of analyzing the cost and operations of the

business so as to prepare the internal financial reports which helps the managers of Tech

(UK) Ltd in taking the strategic decisions (Accounting Tools, 2017). Financial

accounting means analyzing the financial reports of the company to track the financial

tractions.

I)

Point of Distinction Management Accounting Financial Accounting

Focus It focuses on the decisions

which are to be made for the

future.

It focuses on the past to take

the decisions.

Scope The scope of the management

accounting is narrow.

Its scope is wide.

Primary Users Internal audience like

managers.

External audience like

investors.

Regulations GAAP and IFRS None

II) Management accounting information is the crucial part in the organisation for taking the

appropriate decisions. The results which arise from analyzing these statements will provide the

managers of the Tech (UK) Ltd an idea to plan their resources and profit margins accordingly

(Butterfield, 2016). Collecting the data from the various departments and then comparing those

with the actual or the budget one will help the organisation to enhance their performance

(Butterfield, 2016). The analyses of the reports can be done through various tools and techniques

some of which includes Key Performance Indicators (KPI’s), Benchmarks and balanced

Scorecard. The evaluation of the performance also helps in achieving the growth (Butterfield,

2016).

III) Cost accounting systems are a framework which is used by the organizations for analyzing

the cost of the products so as to predict the profit and valuate the stock. There are three cost

accounting systems:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Actual Costing: It means recording the actual cost of the products which includes actual cost of

material, labor and overhead incurred during the allocation of the resources (Ryckman, M. L.,

2018).

Normal Costing: It is the cost analysis tool which assigns the cost to the product including the

cost of the material, labor and overheads (Ryckman, 2018).

Standard Costing: It is the technique for analyzing the expected cost for an actual cost and then

analyzing the variance between both the costs (Business Dictionary, 2018).

IV) Inventory management system is the basic instrument for all the organizations which helps

in analyzing the inventory of tangible goods. This tool is basically used by the organizations that

manufactures and sells the finished and semi-finished goods in order to prepare work order and

other related documents (Kontus and Kastav, 2014). Inventory management system is basically

used by the large scale industries as this system is quite expensive and costly so the small scale

industries cannot afford it. This tool is used by the mangers in the organisation as it is highly

optimized and effective for the overall success of the business (Kontus and Kastav, 2014).

V) Job costing is an accounting method of tracking the cost for manufacturing the particular

product. Through job costing systems the accountant can keep a track on the cost of the goods

which are under production and can maintain the data which is relevant to the business

operations. The job costing forms includes the direct labor, direct material and direct overheads.

The projects such as construction use this tool widely to analyze and determine the cost. This

analysis is important for the company to determine the accuracy in the estimating system of the

organization which allows achieving the reasonable profits (Wilkinson, 2013).

5

material, labor and overhead incurred during the allocation of the resources (Ryckman, M. L.,

2018).

Normal Costing: It is the cost analysis tool which assigns the cost to the product including the

cost of the material, labor and overheads (Ryckman, 2018).

Standard Costing: It is the technique for analyzing the expected cost for an actual cost and then

analyzing the variance between both the costs (Business Dictionary, 2018).

IV) Inventory management system is the basic instrument for all the organizations which helps

in analyzing the inventory of tangible goods. This tool is basically used by the organizations that

manufactures and sells the finished and semi-finished goods in order to prepare work order and

other related documents (Kontus and Kastav, 2014). Inventory management system is basically

used by the large scale industries as this system is quite expensive and costly so the small scale

industries cannot afford it. This tool is used by the mangers in the organisation as it is highly

optimized and effective for the overall success of the business (Kontus and Kastav, 2014).

V) Job costing is an accounting method of tracking the cost for manufacturing the particular

product. Through job costing systems the accountant can keep a track on the cost of the goods

which are under production and can maintain the data which is relevant to the business

operations. The job costing forms includes the direct labor, direct material and direct overheads.

The projects such as construction use this tool widely to analyze and determine the cost. This

analysis is important for the company to determine the accuracy in the estimating system of the

organization which allows achieving the reasonable profits (Wilkinson, 2013).

5

B) I) There are various types of managerial accounting reports which are used by the

managers for analyzing the company’s performance (Sullivan, 2018). Some of which are:

Image: Types of managerial Accounting Reports

Source: By Author, 2018

Budget Report: This report reveals the actual performance of the company by defining

the variance between the actual and the predicted cost.

Job cost Reports: This report shows the expenses of the particular project. It identifies

the areas where the higher earnings can be achieved in order to gain profits (Sullivan,

2018).

Inventory and Manufacturing: These reports are used by the companies for making

their manufacturing process more efficient as this includes the wasted inventory, labor

cost and the overhead cost (Sullivan, 2018).

II) The information should be presented in the manner it should be understandable as it is

the evidence through which the analyses of the financial performance is measured by the

top level managers of the company. The information which is depicted by the financial

accounts is first measured with the actual performance and then the variance is

calculated. This variance shows the path to organizations for achieving the desired

objectives. If the information is not presented in the understandable form so it will be

difficult for the organizations to evaluate it take the decisions accordingly.

6

B u d g e t R e p o r t

J o b C o s t R e p o r t s

I n v e n t o r y a n d

M a n u f a c t u r i n g

managers for analyzing the company’s performance (Sullivan, 2018). Some of which are:

Image: Types of managerial Accounting Reports

Source: By Author, 2018

Budget Report: This report reveals the actual performance of the company by defining

the variance between the actual and the predicted cost.

Job cost Reports: This report shows the expenses of the particular project. It identifies

the areas where the higher earnings can be achieved in order to gain profits (Sullivan,

2018).

Inventory and Manufacturing: These reports are used by the companies for making

their manufacturing process more efficient as this includes the wasted inventory, labor

cost and the overhead cost (Sullivan, 2018).

II) The information should be presented in the manner it should be understandable as it is

the evidence through which the analyses of the financial performance is measured by the

top level managers of the company. The information which is depicted by the financial

accounts is first measured with the actual performance and then the variance is

calculated. This variance shows the path to organizations for achieving the desired

objectives. If the information is not presented in the understandable form so it will be

difficult for the organizations to evaluate it take the decisions accordingly.

6

B u d g e t R e p o r t

J o b C o s t R e p o r t s

I n v e n t o r y a n d

M a n u f a c t u r i n g

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1) There are various benefits of management accounting systems which includes:

Image: Benefits of management accounting systems

Source: By Author, 2018

Increase Efficiency: The efficiency of the company can be achieved by comparing and

analyzing the financial accounts (Reddy, 2018). Tech (UK) Ltd. can evaluate its performance by

keeping the check on the cost and selecting the ways in which the revenue of the company can

increase this will help to compete with the external environment.

Cost transparency: There are various costs which are to be considered by the company while

taking the strategic decisions. These decisions will help to ensure that the results are occurred

according to the pre-determined budgets in the organisation (Reddy, 2018). If the results are

achieved according to the set standards then the transparency of the cost is maintained.

Simplifies Decision Making: Management accounting systems simplifies the decision making

process of the company as the decisions related to the financial accounts are taken keeping the

common perspective. For these accountants of the Tech (UK) Ltd. creates a specified reports to

make interpretation simpler.

7

Increase

Efficiency

Cost

Transparency

Simplifies

Decision

Making

Flexibility

Image: Benefits of management accounting systems

Source: By Author, 2018

Increase Efficiency: The efficiency of the company can be achieved by comparing and

analyzing the financial accounts (Reddy, 2018). Tech (UK) Ltd. can evaluate its performance by

keeping the check on the cost and selecting the ways in which the revenue of the company can

increase this will help to compete with the external environment.

Cost transparency: There are various costs which are to be considered by the company while

taking the strategic decisions. These decisions will help to ensure that the results are occurred

according to the pre-determined budgets in the organisation (Reddy, 2018). If the results are

achieved according to the set standards then the transparency of the cost is maintained.

Simplifies Decision Making: Management accounting systems simplifies the decision making

process of the company as the decisions related to the financial accounts are taken keeping the

common perspective. For these accountants of the Tech (UK) Ltd. creates a specified reports to

make interpretation simpler.

7

Increase

Efficiency

Cost

Transparency

Simplifies

Decision

Making

Flexibility

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Flexibility: Management accounting systems of the organization should be flexible in nature.

These accounts are prepared on the annually basis so the accountants get enough time to prepare

the reports (Reddy, 2018).

D1) Management accounting systems and management accounting reporting are integrated

within the organization as it provides companies with both qualitative and quantitative

information about the financial reports. These financial reports help the organisation in achieving

the growth in the market. The integration of the management reports with the management

systems activities of the Tech (UK) Ltd. will make efforts towards the timely collection policies

for ensuring flexibility and accuracy. The integration between the processes will provide better

management of inventory and cost in the organization. These all the reports will ensure that the

decisions in the organisation are taken according to the appropriate situations.

8

These accounts are prepared on the annually basis so the accountants get enough time to prepare

the reports (Reddy, 2018).

D1) Management accounting systems and management accounting reporting are integrated

within the organization as it provides companies with both qualitative and quantitative

information about the financial reports. These financial reports help the organisation in achieving

the growth in the market. The integration of the management reports with the management

systems activities of the Tech (UK) Ltd. will make efforts towards the timely collection policies

for ensuring flexibility and accuracy. The integration between the processes will provide better

management of inventory and cost in the organization. These all the reports will ensure that the

decisions in the organisation are taken according to the appropriate situations.

8

TASK 2

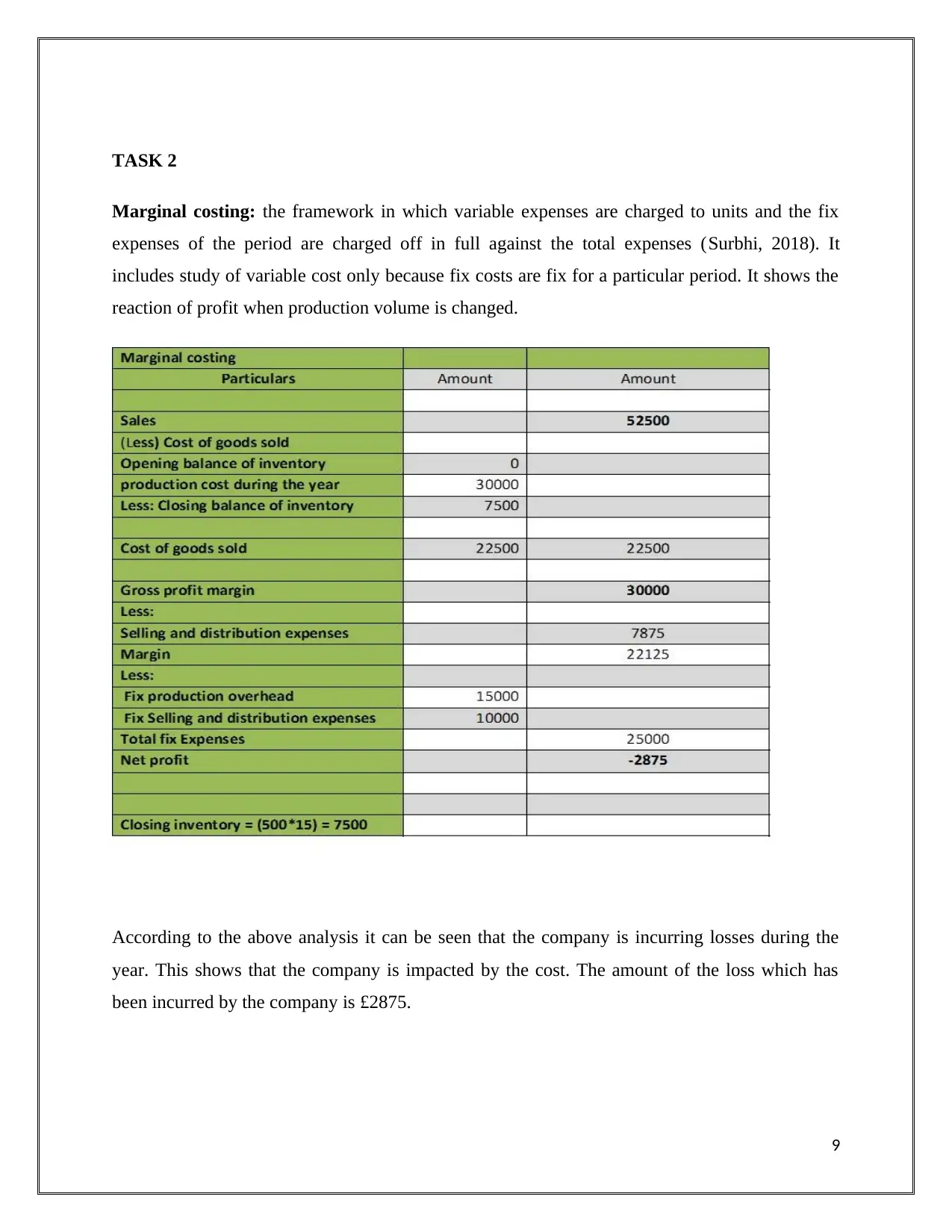

Marginal costing: the framework in which variable expenses are charged to units and the fix

expenses of the period are charged off in full against the total expenses (Surbhi, 2018). It

includes study of variable cost only because fix costs are fix for a particular period. It shows the

reaction of profit when production volume is changed.

According to the above analysis it can be seen that the company is incurring losses during the

year. This shows that the company is impacted by the cost. The amount of the loss which has

been incurred by the company is £2875.

9

Marginal costing: the framework in which variable expenses are charged to units and the fix

expenses of the period are charged off in full against the total expenses (Surbhi, 2018). It

includes study of variable cost only because fix costs are fix for a particular period. It shows the

reaction of profit when production volume is changed.

According to the above analysis it can be seen that the company is incurring losses during the

year. This shows that the company is impacted by the cost. The amount of the loss which has

been incurred by the company is £2875.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

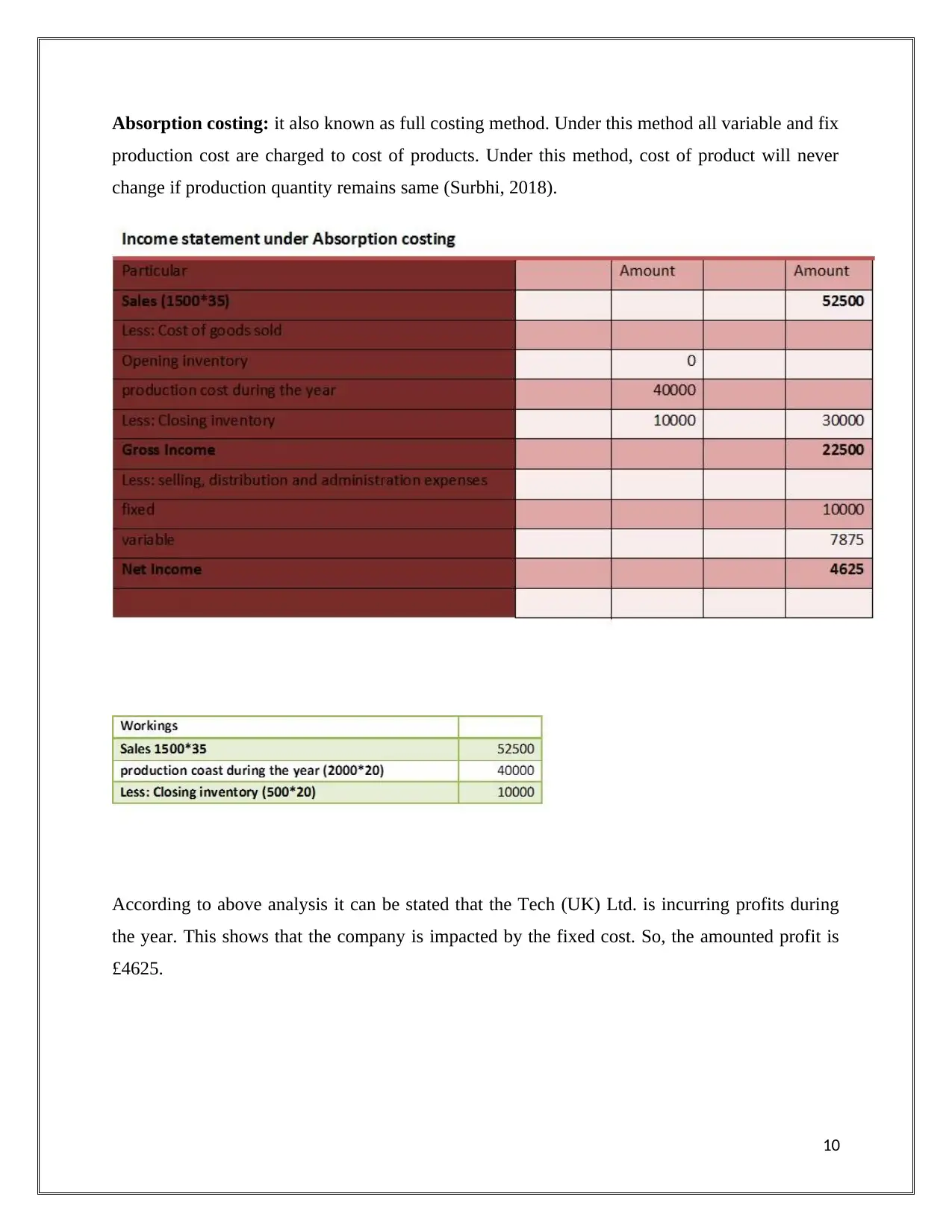

Absorption costing: it also known as full costing method. Under this method all variable and fix

production cost are charged to cost of products. Under this method, cost of product will never

change if production quantity remains same (Surbhi, 2018).

According to above analysis it can be stated that the Tech (UK) Ltd. is incurring profits during

the year. This shows that the company is impacted by the fixed cost. So, the amounted profit is

£4625.

10

production cost are charged to cost of products. Under this method, cost of product will never

change if production quantity remains same (Surbhi, 2018).

According to above analysis it can be stated that the Tech (UK) Ltd. is incurring profits during

the year. This shows that the company is impacted by the fixed cost. So, the amounted profit is

£4625.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

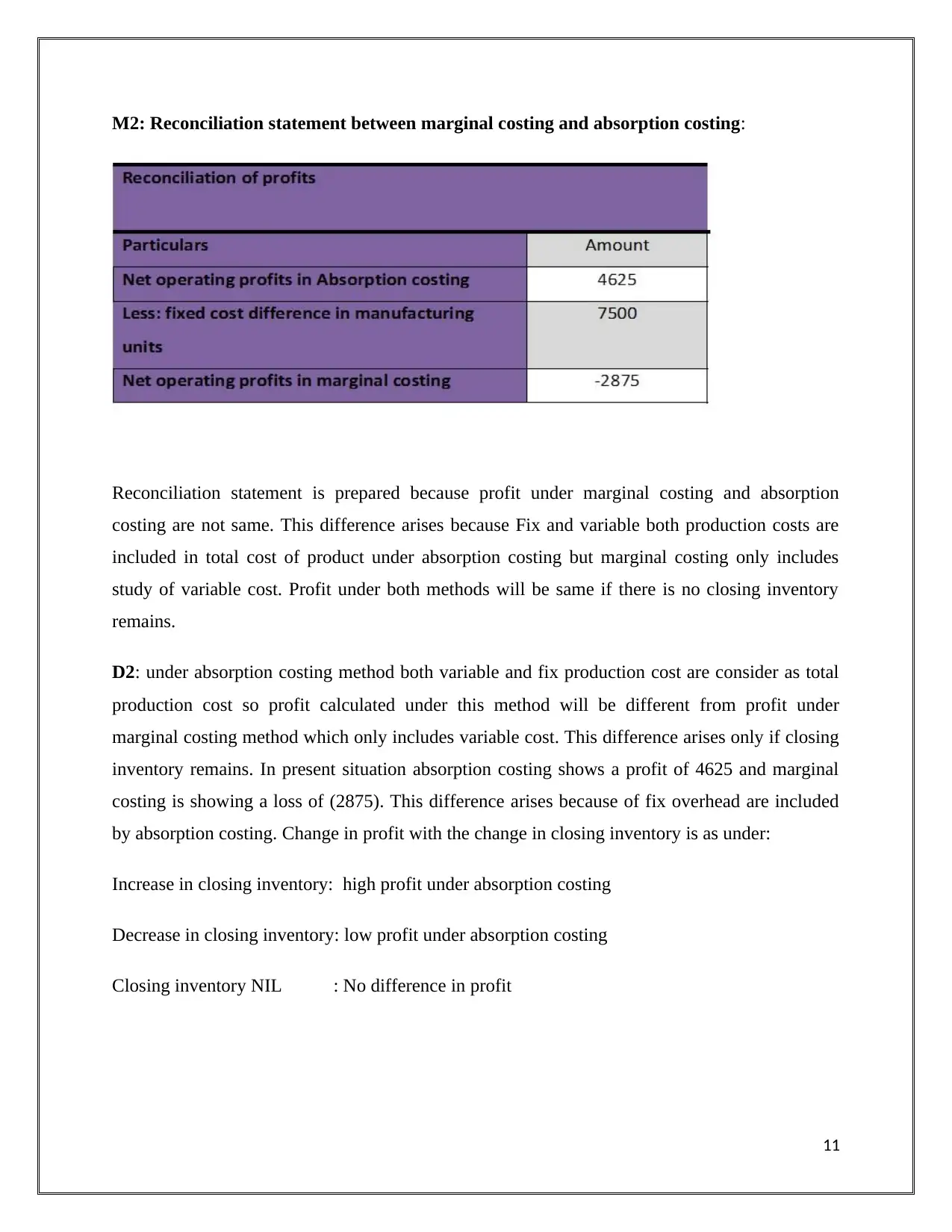

M2: Reconciliation statement between marginal costing and absorption costing:

Reconciliation statement is prepared because profit under marginal costing and absorption

costing are not same. This difference arises because Fix and variable both production costs are

included in total cost of product under absorption costing but marginal costing only includes

study of variable cost. Profit under both methods will be same if there is no closing inventory

remains.

D2: under absorption costing method both variable and fix production cost are consider as total

production cost so profit calculated under this method will be different from profit under

marginal costing method which only includes variable cost. This difference arises only if closing

inventory remains. In present situation absorption costing shows a profit of 4625 and marginal

costing is showing a loss of (2875). This difference arises because of fix overhead are included

by absorption costing. Change in profit with the change in closing inventory is as under:

Increase in closing inventory: high profit under absorption costing

Decrease in closing inventory: low profit under absorption costing

Closing inventory NIL : No difference in profit

11

Reconciliation statement is prepared because profit under marginal costing and absorption

costing are not same. This difference arises because Fix and variable both production costs are

included in total cost of product under absorption costing but marginal costing only includes

study of variable cost. Profit under both methods will be same if there is no closing inventory

remains.

D2: under absorption costing method both variable and fix production cost are consider as total

production cost so profit calculated under this method will be different from profit under

marginal costing method which only includes variable cost. This difference arises only if closing

inventory remains. In present situation absorption costing shows a profit of 4625 and marginal

costing is showing a loss of (2875). This difference arises because of fix overhead are included

by absorption costing. Change in profit with the change in closing inventory is as under:

Increase in closing inventory: high profit under absorption costing

Decrease in closing inventory: low profit under absorption costing

Closing inventory NIL : No difference in profit

11

TASK 3

Introduction

This report depicts the various types of the budget which are been used by the organisation while

taking the strategic decisions for the organization. The importance of the budget for planning and

control has also been explained. With these two factors the procedure for preparing the budget

has also been highlighted so as to determine the price.

12

Introduction

This report depicts the various types of the budget which are been used by the organisation while

taking the strategic decisions for the organization. The importance of the budget for planning and

control has also been explained. With these two factors the procedure for preparing the budget

has also been highlighted so as to determine the price.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.