A Comprehensive Report on Management Accounting Systems and Techniques

VerifiedAdded on 2020/11/23

|17

|5234

|63

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within Tech (UK) Ltd. It begins by defining management accounting and exploring various management accounting systems, including inventory management and cost accounting systems like actual, normal, and standard costing, job costing. The report then delves into different methods used for management accounting reporting, such as budgeting, cash flow, production, accounts receivable, and sales reports, highlighting their significance in minimizing losses, developing budgets, improving understanding, and enhancing financial returns. The advantages of management accounting systems are discussed, including price optimization and job costing systems. Furthermore, the report establishes the integration between management accounting reports and organizational processes, using examples like accounts receivable aging reports and job cost reports. The report also covers cost analysis techniques, including marginal and absorption costing, to prepare income statements. Finally, the advantages and disadvantages of different planning tools are examined, along with how management accounting systems can respond to financial problems, concluding with a summary of key findings and recommendations for Tech (UK) Ltd.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and different types of management accounting systems..........1

P2 Different methods used for management accounting reporting........................................4

M1 Benefits of management accounting systems and their applications...............................5

D1 Management accounting systems and management accounting reporting is integrated. .6

TASK 2............................................................................................................................................6

P3 Techniques of cost analysis to prepare an income statement of marginal and absorption

costing.....................................................................................................................................6

M2 Management accounting techniques and financial reporting documents........................8

D2 Financial reports that accurately apply and interpret data................................................8

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different types of planning tools.................................9

M3 Different planning tools and their applications..............................................................11

D3 Planning tools for accounting respond appropriately to solving financial problems.....11

TASK 4..........................................................................................................................................11

P5 Management accounting systems to respond to financial problems...............................11

M4 Responding to financial problems, management accounting........................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

.......................................................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and different types of management accounting systems..........1

P2 Different methods used for management accounting reporting........................................4

M1 Benefits of management accounting systems and their applications...............................5

D1 Management accounting systems and management accounting reporting is integrated. .6

TASK 2............................................................................................................................................6

P3 Techniques of cost analysis to prepare an income statement of marginal and absorption

costing.....................................................................................................................................6

M2 Management accounting techniques and financial reporting documents........................8

D2 Financial reports that accurately apply and interpret data................................................8

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different types of planning tools.................................9

M3 Different planning tools and their applications..............................................................11

D3 Planning tools for accounting respond appropriately to solving financial problems.....11

TASK 4..........................................................................................................................................11

P5 Management accounting systems to respond to financial problems...............................11

M4 Responding to financial problems, management accounting........................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

.......................................................................................................................................................15

INTRODUCTION

Management accounting refers to provision of financial advice and advice to an

organisation for using in company as well as development of business. It is a procedure of

making the management accounts and also reports which give timely and accurate financial

information needed through employers to make daily operations as well as short term decisions

(Arroyo, 2012). It is a necessary profession that contribute in monitoring, planning, controlling

and decision making of functions of company. Management accounting is wider concept that

involves costing provisions and helpful in developing better coordination between various

departmental functions. It aids management in order to achieve more flexibility in its structure

and also make better strategies which aids in attaining objectives of company. This report is

based on Tech (UK) Ltd. that manufactures the special chargers for the retailers. Under this

mention report discuss about the management accounting and provide necessary needs of various

kinds of management accounting systems. Advantages and limitations of various kinds of

planning tools which are used for budgetary control will also be mentioned in it. In order to

respond to the financial problems, firms adopting the effective management accounting systems.

TASK 1

P1 Management accounting and different types of management accounting systems

From: Management accounting officer

To: General manager of Tech (UK)

Sub: Management accounting system

Management accounting refers to a process that consists regards evaluate, interpretation,

identification and also presenting accounting information achieved through manager with the

help of cost accounting related techniques as well as management accounting. It is helpful in

decision making. It is helpful for management n develop along with execution of better strategies

in better or effective manner (Boyns and Edwards, 2013). There are various functions of

management accounting such as control, monitor, plan and also increasing employees

performance by make improvement of understand regarding various functions of departments.

Definitions of management accounting

1

Management accounting refers to provision of financial advice and advice to an

organisation for using in company as well as development of business. It is a procedure of

making the management accounts and also reports which give timely and accurate financial

information needed through employers to make daily operations as well as short term decisions

(Arroyo, 2012). It is a necessary profession that contribute in monitoring, planning, controlling

and decision making of functions of company. Management accounting is wider concept that

involves costing provisions and helpful in developing better coordination between various

departmental functions. It aids management in order to achieve more flexibility in its structure

and also make better strategies which aids in attaining objectives of company. This report is

based on Tech (UK) Ltd. that manufactures the special chargers for the retailers. Under this

mention report discuss about the management accounting and provide necessary needs of various

kinds of management accounting systems. Advantages and limitations of various kinds of

planning tools which are used for budgetary control will also be mentioned in it. In order to

respond to the financial problems, firms adopting the effective management accounting systems.

TASK 1

P1 Management accounting and different types of management accounting systems

From: Management accounting officer

To: General manager of Tech (UK)

Sub: Management accounting system

Management accounting refers to a process that consists regards evaluate, interpretation,

identification and also presenting accounting information achieved through manager with the

help of cost accounting related techniques as well as management accounting. It is helpful in

decision making. It is helpful for management n develop along with execution of better strategies

in better or effective manner (Boyns and Edwards, 2013). There are various functions of

management accounting such as control, monitor, plan and also increasing employees

performance by make improvement of understand regarding various functions of departments.

Definitions of management accounting

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the basis of CIMA, Management accounting involves determination, measuring,

interaction and interpretation of necessary information by which management can develop better

plan for proper utilisation of resources in order to achieve set objectives.

According to IMA, Management accounting is a wider concept that helps in process of

decision making, performance and planning of the management systems.

Significance of management accounting

There are many advantages which are related with management accounting applications

in an organisation (Cadez and Guilding, 2012). It is helpful in giving various kinds of

management accounting information that is helpful for management of Tech (UK) Ltd. It is used

as a decision making tools related to various aspects. Some importance of management

accounting mention below:

Identification of Aim- According to information and data available, management

accounting is helpful in identify its set aims and also try to search the better method by which it

can achieve its targets in easy manner.

Performance measurement- Budgetary control standard costing is an effective

techniques that enable performance measurement. In context to standard costing, these are

identified once and also actual cost compare with the standard cost. Under this, it able

management to search all deviation among actual and standard cost. The budgetary control

system is helpful in analysing effectiveness of staff members.

Give better management control- Management accounting tools are helpful for

management in coordination, planning and controlling business activities, standard getting and

also assess the actual performance continuously able management to “management through

exception”.

Decision making- Management accounting system is helpful in make improvement in the

decision making of internal parties in order to get the high outcomes (Chiarini, 2012).

Make or buy- Under this, management accounting is helpful for owners of small

organisations which goods and services they should in manufacturing unit in first place. Cost

accounting system gives better opportunities to take better decisions related to outsourcing as

well as production. It is helpful in make improvement of profit of company.

Presentation of financial statement- Management accounting is helpful in gathering

various data and information which shows financial position of company. Various data and

2

interaction and interpretation of necessary information by which management can develop better

plan for proper utilisation of resources in order to achieve set objectives.

According to IMA, Management accounting is a wider concept that helps in process of

decision making, performance and planning of the management systems.

Significance of management accounting

There are many advantages which are related with management accounting applications

in an organisation (Cadez and Guilding, 2012). It is helpful in giving various kinds of

management accounting information that is helpful for management of Tech (UK) Ltd. It is used

as a decision making tools related to various aspects. Some importance of management

accounting mention below:

Identification of Aim- According to information and data available, management

accounting is helpful in identify its set aims and also try to search the better method by which it

can achieve its targets in easy manner.

Performance measurement- Budgetary control standard costing is an effective

techniques that enable performance measurement. In context to standard costing, these are

identified once and also actual cost compare with the standard cost. Under this, it able

management to search all deviation among actual and standard cost. The budgetary control

system is helpful in analysing effectiveness of staff members.

Give better management control- Management accounting tools are helpful for

management in coordination, planning and controlling business activities, standard getting and

also assess the actual performance continuously able management to “management through

exception”.

Decision making- Management accounting system is helpful in make improvement in the

decision making of internal parties in order to get the high outcomes (Chiarini, 2012).

Make or buy- Under this, management accounting is helpful for owners of small

organisations which goods and services they should in manufacturing unit in first place. Cost

accounting system gives better opportunities to take better decisions related to outsourcing as

well as production. It is helpful in make improvement of profit of company.

Presentation of financial statement- Management accounting is helpful in gathering

various data and information which shows financial position of company. Various data and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information related with finance and cost are helpful in prepare better financial reports that

contribute in the decision making.

Different kinds of management accounting systems

Inventory management- It is a supervision of the stock items as well as inventory. It is a

combination of the processes as well as technology which oversee maintenance and monitor

stocked goods whether those are raw materials, supplies,company assets, finished goods and

ready to send to end consumers or vendors (DRURY, 2013).

Cost accounting systems- It is helpful for management to estimate the product cost for

evaluation purpose of profit level, cost control and also inventory. Under this included process

and job order costing. Under this, it can be classified in actual, normal and standard costing.

Actual costing- It is a procedure of record cost of goods, actual cost of labour, overhead

and material.

Normal costing- It is used to produce goods on the basis of labour, overhead cost of

production and also actual material according to the predetermined production overhead rate.

Standard costing- It is regarded as the predetermined cost that incurred in manufacturing

of services and products.

Job costing- It is used for producing the multiple goods. It is helpful in cost allocation to

every product it gives better opportunity in order to track actual expenses those are incurred on

product manufacturing (Fullerton, Kennedy and Widener, 2013).

Difference among management and financial accounting

Management Accounting Financial Accounting

It is basically developed for the internal

parties.

It is basically used through the external

stakeholders.

It aids in analyse operational as well as

financial performance of Tech (UK) Ltd.

By use of accounting information provisions

, financial data is to be analysed.

Information and also data is used for the future

planning.

IT is based on the previous reports.

3

contribute in the decision making.

Different kinds of management accounting systems

Inventory management- It is a supervision of the stock items as well as inventory. It is a

combination of the processes as well as technology which oversee maintenance and monitor

stocked goods whether those are raw materials, supplies,company assets, finished goods and

ready to send to end consumers or vendors (DRURY, 2013).

Cost accounting systems- It is helpful for management to estimate the product cost for

evaluation purpose of profit level, cost control and also inventory. Under this included process

and job order costing. Under this, it can be classified in actual, normal and standard costing.

Actual costing- It is a procedure of record cost of goods, actual cost of labour, overhead

and material.

Normal costing- It is used to produce goods on the basis of labour, overhead cost of

production and also actual material according to the predetermined production overhead rate.

Standard costing- It is regarded as the predetermined cost that incurred in manufacturing

of services and products.

Job costing- It is used for producing the multiple goods. It is helpful in cost allocation to

every product it gives better opportunity in order to track actual expenses those are incurred on

product manufacturing (Fullerton, Kennedy and Widener, 2013).

Difference among management and financial accounting

Management Accounting Financial Accounting

It is basically developed for the internal

parties.

It is basically used through the external

stakeholders.

It aids in analyse operational as well as

financial performance of Tech (UK) Ltd.

By use of accounting information provisions

, financial data is to be analysed.

Information and also data is used for the future

planning.

IT is based on the previous reports.

3

Scope of management accounting is narrow

and also depends on deportments (Håkansson,

Kraus and Lind, 2010).

IT has wider scope and also cover all

transactions of full organisations.

P2 Different methods used for management accounting reporting

From: Management accounting officer

To: General manager of Tech (UK)

Sub: Management accounting system

Report is document that contain information and data related to necessary aspects those

are used through management for the future planning as well as achieve set objectives., on

context to Tech (UK)Ltd., in various types of reports involves accounts receivable, performance,

job costing, budgeting etc.

Significance of management accounting reports

Minimize loss- Various types of reports include different data or information which

which all problems are measured in order to minimize the future loss (Herzig and et. al. 2012).

For an example- Accounts receivable reports are helpful in determine outstanding debts

amounts. In this, correction in the policies are helpful in liquidity maintenance in firm.

Budgets Development- Various types of reports give information and data by which Tech

(UK) firm developed better budgets in order to guide staff members. Budgets are work as

standards that gives better opportunity to make improvement in performance and achieve targets

with in specific period of time.

Improvement in understanding- This type of management report plays a necessary role

to improve understanding among the activities of different departments. It is helpful in gain

support and also attain the common goals.

Enhanced financial returns- Job costing related reports are helpful in determination of

profitable project aspect. It is helpful for manager to use its whole efforts to improve necessary

areas. In addition to this, various reports provides better advantages to Tech (UK) Ltd. Firm.

Various kinds of management reports

Budgeting reports- It gives better standards as well as plans those are used to examine

organisational performance by comparison with the actual performance of various departments

(Hopwood, Unerman and Fries, 2010). In this, it aids in identify problems those are related with

functions and helpful in cost controlling. On the basis of this, incentive report is developed

4

and also depends on deportments (Håkansson,

Kraus and Lind, 2010).

IT has wider scope and also cover all

transactions of full organisations.

P2 Different methods used for management accounting reporting

From: Management accounting officer

To: General manager of Tech (UK)

Sub: Management accounting system

Report is document that contain information and data related to necessary aspects those

are used through management for the future planning as well as achieve set objectives., on

context to Tech (UK)Ltd., in various types of reports involves accounts receivable, performance,

job costing, budgeting etc.

Significance of management accounting reports

Minimize loss- Various types of reports include different data or information which

which all problems are measured in order to minimize the future loss (Herzig and et. al. 2012).

For an example- Accounts receivable reports are helpful in determine outstanding debts

amounts. In this, correction in the policies are helpful in liquidity maintenance in firm.

Budgets Development- Various types of reports give information and data by which Tech

(UK) firm developed better budgets in order to guide staff members. Budgets are work as

standards that gives better opportunity to make improvement in performance and achieve targets

with in specific period of time.

Improvement in understanding- This type of management report plays a necessary role

to improve understanding among the activities of different departments. It is helpful in gain

support and also attain the common goals.

Enhanced financial returns- Job costing related reports are helpful in determination of

profitable project aspect. It is helpful for manager to use its whole efforts to improve necessary

areas. In addition to this, various reports provides better advantages to Tech (UK) Ltd. Firm.

Various kinds of management reports

Budgeting reports- It gives better standards as well as plans those are used to examine

organisational performance by comparison with the actual performance of various departments

(Hopwood, Unerman and Fries, 2010). In this, it aids in identify problems those are related with

functions and helpful in cost controlling. On the basis of this, incentive report is developed

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

through management of various employees those contribute towards improving passion towards

work.

Cash flow report- It is necessary document that is helpful in better management in an

organisation. In addition to this, it gives accurate information related to outflow as well as inflow

of cash at the time of particular time period. It is helpful in maintaining liquidity in business

firm.

Production report- IT provides information related to products those are necessary to

manufacture for fulfil demands or needs of various consumers (Islam and Hu, 2012). It is helpful

in achieve targets to Tech (UK) firm.

Accounts receivable report- It contains information or data related to amount that is due

from the debtors. In context to this, for better management, there is a requirement to debtors to

invoice segmentation according of particular time period. It is helpful in assessing problems

those are present in process of collection, it increase decision making regarding current credit

policies and also make modifications in better or effective manner, it gives opportunities related

to minimising old debts amounts and also maintain liquidity that aids in better performance of

daily basis functions.

Sales report- It gives information related to sales amount those are necessary in order to

achieve providence of functions of business. It is used for guidance of staff members to give its

functions on the basis of needs.

Conclusion

It has been concluded from the above report that Tech (UK) Ltd. Needs to develop

various reporting methods due t the different functions (Kokubu and Kitada, 2015). Cash flow

statement related report is helpful in measure business solvency. Under this studied about the

different type of management accounting reports.

M1 Benefits of management accounting systems and their applications

There are several advantages those are related with the management accounting system

used through accountant of the Tech (UK) Ltd. Organisation in order to improve performance.

Advantages of various types of systems given below:

Price optimisation system

It is helpful in identify purchasing behaviour of consumers at various pricing levels.

It gives better opportunities related to increase profit by choosing better costs.

5

work.

Cash flow report- It is necessary document that is helpful in better management in an

organisation. In addition to this, it gives accurate information related to outflow as well as inflow

of cash at the time of particular time period. It is helpful in maintaining liquidity in business

firm.

Production report- IT provides information related to products those are necessary to

manufacture for fulfil demands or needs of various consumers (Islam and Hu, 2012). It is helpful

in achieve targets to Tech (UK) firm.

Accounts receivable report- It contains information or data related to amount that is due

from the debtors. In context to this, for better management, there is a requirement to debtors to

invoice segmentation according of particular time period. It is helpful in assessing problems

those are present in process of collection, it increase decision making regarding current credit

policies and also make modifications in better or effective manner, it gives opportunities related

to minimising old debts amounts and also maintain liquidity that aids in better performance of

daily basis functions.

Sales report- It gives information related to sales amount those are necessary in order to

achieve providence of functions of business. It is used for guidance of staff members to give its

functions on the basis of needs.

Conclusion

It has been concluded from the above report that Tech (UK) Ltd. Needs to develop

various reporting methods due t the different functions (Kokubu and Kitada, 2015). Cash flow

statement related report is helpful in measure business solvency. Under this studied about the

different type of management accounting reports.

M1 Benefits of management accounting systems and their applications

There are several advantages those are related with the management accounting system

used through accountant of the Tech (UK) Ltd. Organisation in order to improve performance.

Advantages of various types of systems given below:

Price optimisation system

It is helpful in identify purchasing behaviour of consumers at various pricing levels.

It gives better opportunities related to increase profit by choosing better costs.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing system

It is helpful in assessment of qualitative work which assign through company.

It aids in eliminate duplication of tasks as well as activities (Kotas, 2014).

Helps in identify all kinds of costs which are related with process of production.

D1 Management accounting systems and management accounting reporting is integrated

There is a relation established among management accounting reports and also

organisational process helpful in finish tasks in an effective or manner manner.

Type of reporting Integration with organisational process

Accounts receivable ageing reports An integration among function of report with

process of company that is ascertain according

timely gathering of outstanding amount and

also make some modification credit policies.

Job cost reports An integration is among process of company

and reports are helpful in achieving the cost

objectives as well as develop better pricing

strategies in significant manner.

TASK 2

P3 Techniques of cost analysis to prepare an income statement of marginal and absorption

costing

Cost is incurred through business firm at the time of manufacturing services and

products. It consist the paid off through firm at the time of process of manufacturing. All cost

are incurred through firms in order to accrued business operations with out any kind of

interruptions as well as achieve aims with in particular time period (Lukka and Modell, 2010). It

is a responsibility of finance department is to determine costs on the basis to allocated funds to

various departments. The cost of Tech (UK) Ltd. products is not much high. This company

works on minimising unnecessary cost for some segment of consumers. It is helpful in develop

positive affect on profit level along with productivity of company. In addition to this, there are

various kinds of costing and these are mention below as above:

6

It is helpful in assessment of qualitative work which assign through company.

It aids in eliminate duplication of tasks as well as activities (Kotas, 2014).

Helps in identify all kinds of costs which are related with process of production.

D1 Management accounting systems and management accounting reporting is integrated

There is a relation established among management accounting reports and also

organisational process helpful in finish tasks in an effective or manner manner.

Type of reporting Integration with organisational process

Accounts receivable ageing reports An integration among function of report with

process of company that is ascertain according

timely gathering of outstanding amount and

also make some modification credit policies.

Job cost reports An integration is among process of company

and reports are helpful in achieving the cost

objectives as well as develop better pricing

strategies in significant manner.

TASK 2

P3 Techniques of cost analysis to prepare an income statement of marginal and absorption

costing

Cost is incurred through business firm at the time of manufacturing services and

products. It consist the paid off through firm at the time of process of manufacturing. All cost

are incurred through firms in order to accrued business operations with out any kind of

interruptions as well as achieve aims with in particular time period (Lukka and Modell, 2010). It

is a responsibility of finance department is to determine costs on the basis to allocated funds to

various departments. The cost of Tech (UK) Ltd. products is not much high. This company

works on minimising unnecessary cost for some segment of consumers. It is helpful in develop

positive affect on profit level along with productivity of company. In addition to this, there are

various kinds of costing and these are mention below as above:

6

Marginal costing- It used the variable costs for costs calculation. On the basis of this

method provision, variable costs is charged towards the cost units bit the fixed cost is write off.

Under this costing includes cost determination, stock valuation, cost segregation in to variable

and fixed costs and also ascertain the profit level.

Absorption costing- It is an effective method of calculate cost of services and firm

through taking in to an account the indirect expensed along with the direct costs (Macintosh and

Quattrone, 2010). It is a method under which all variable as well as fixed costs are related to the

cost centres where they mostly accounted for the purpose of using the absorption rates. This

method is helpful in assure that incurred costs are to be recovered from selling cost of service

and products. Various items which involve at the tome of calculating cost are direct labour,

variable over head costs, direct, material and fixed overhead cost.

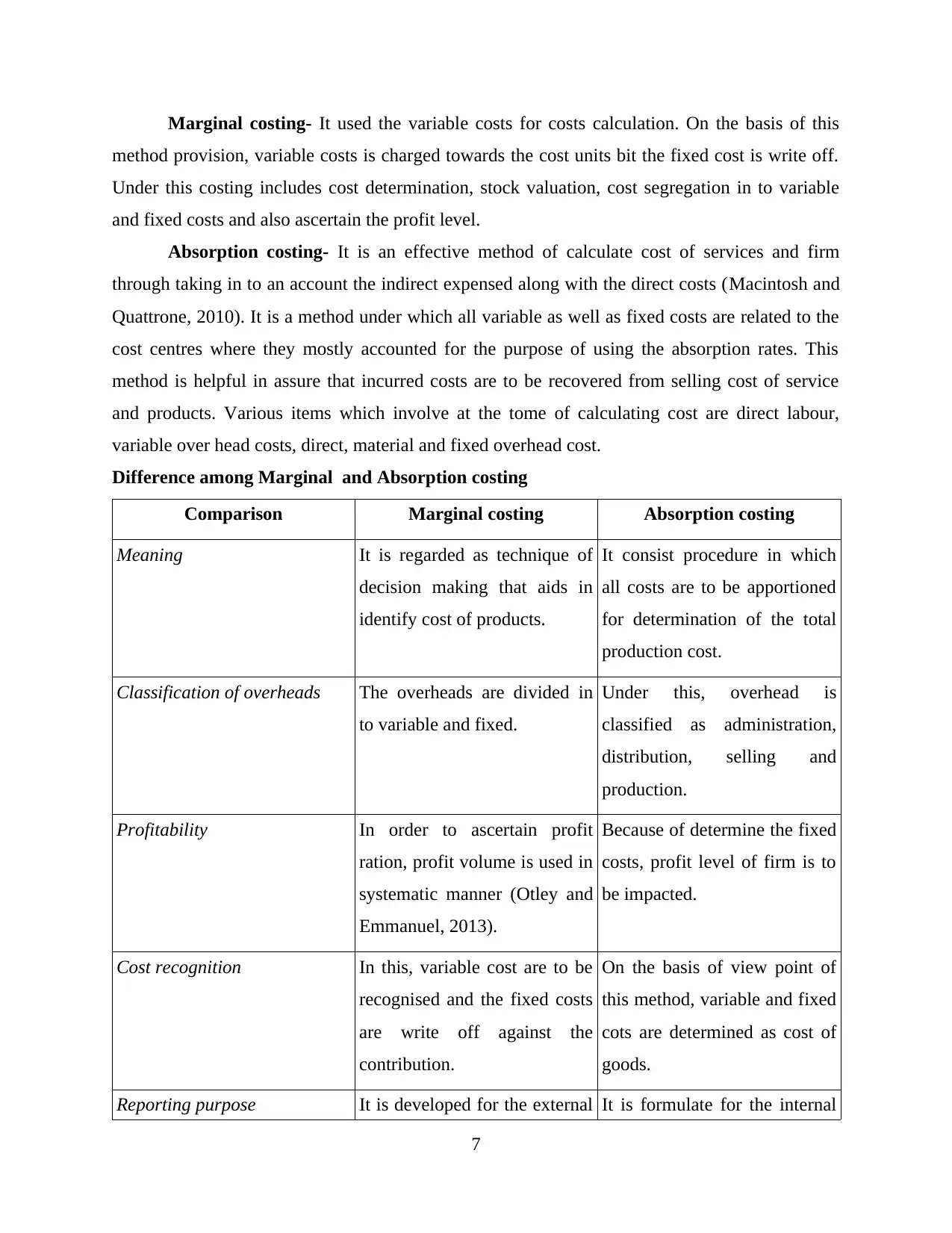

Difference among Marginal and Absorption costing

Comparison Marginal costing Absorption costing

Meaning It is regarded as technique of

decision making that aids in

identify cost of products.

It consist procedure in which

all costs are to be apportioned

for determination of the total

production cost.

Classification of overheads The overheads are divided in

to variable and fixed.

Under this, overhead is

classified as administration,

distribution, selling and

production.

Profitability In order to ascertain profit

ration, profit volume is used in

systematic manner (Otley and

Emmanuel, 2013).

Because of determine the fixed

costs, profit level of firm is to

be impacted.

Cost recognition In this, variable cost are to be

recognised and the fixed costs

are write off against the

contribution.

On the basis of view point of

this method, variable and fixed

cots are determined as cost of

goods.

Reporting purpose It is developed for the external It is formulate for the internal

7

method provision, variable costs is charged towards the cost units bit the fixed cost is write off.

Under this costing includes cost determination, stock valuation, cost segregation in to variable

and fixed costs and also ascertain the profit level.

Absorption costing- It is an effective method of calculate cost of services and firm

through taking in to an account the indirect expensed along with the direct costs (Macintosh and

Quattrone, 2010). It is a method under which all variable as well as fixed costs are related to the

cost centres where they mostly accounted for the purpose of using the absorption rates. This

method is helpful in assure that incurred costs are to be recovered from selling cost of service

and products. Various items which involve at the tome of calculating cost are direct labour,

variable over head costs, direct, material and fixed overhead cost.

Difference among Marginal and Absorption costing

Comparison Marginal costing Absorption costing

Meaning It is regarded as technique of

decision making that aids in

identify cost of products.

It consist procedure in which

all costs are to be apportioned

for determination of the total

production cost.

Classification of overheads The overheads are divided in

to variable and fixed.

Under this, overhead is

classified as administration,

distribution, selling and

production.

Profitability In order to ascertain profit

ration, profit volume is used in

systematic manner (Otley and

Emmanuel, 2013).

Because of determine the fixed

costs, profit level of firm is to

be impacted.

Cost recognition In this, variable cost are to be

recognised and the fixed costs

are write off against the

contribution.

On the basis of view point of

this method, variable and fixed

cots are determined as cost of

goods.

Reporting purpose It is developed for the external It is formulate for the internal

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reporting. reporting.

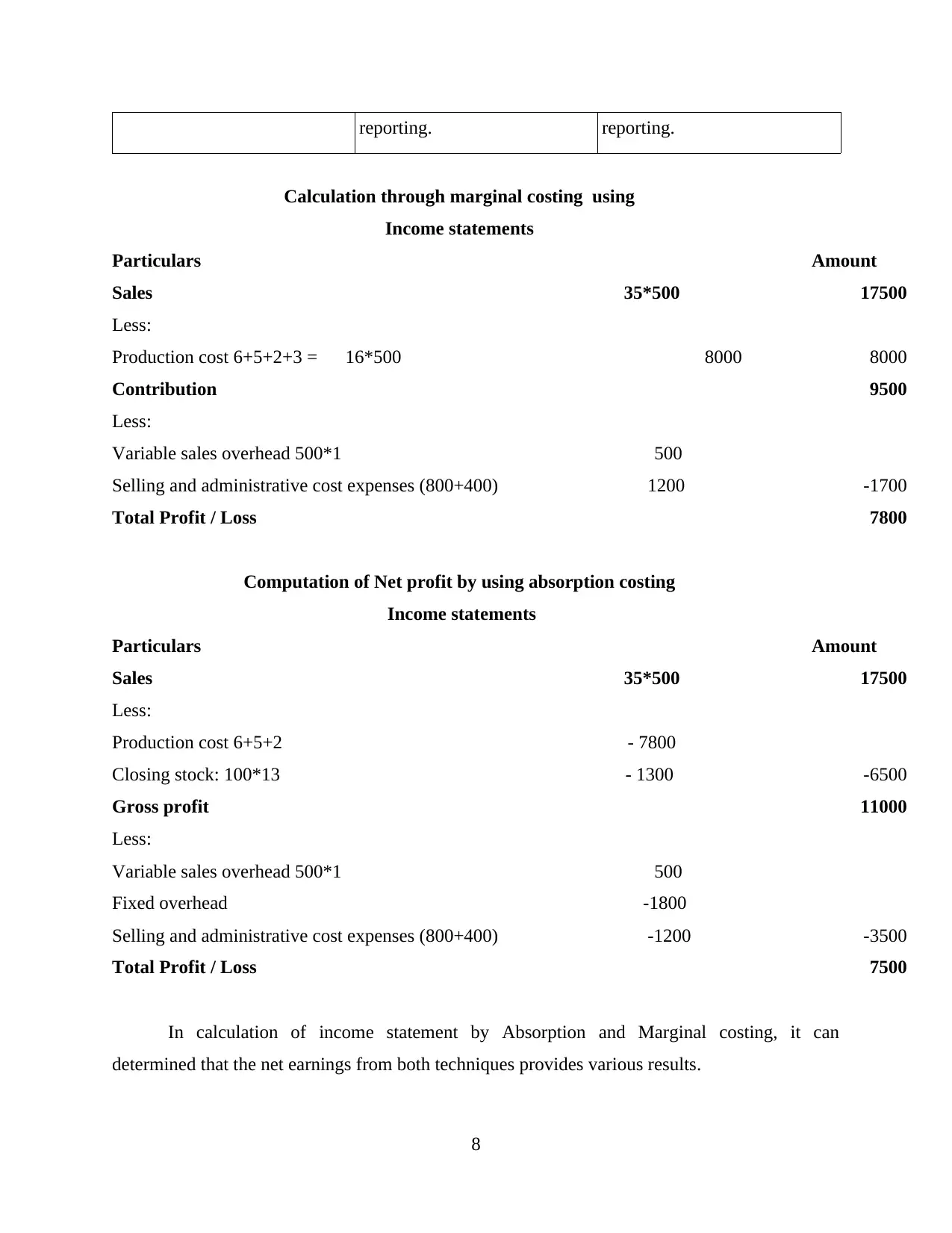

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500 8000 8000

Contribution 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Computation of Net profit by using absorption costing

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Gross profit 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

In calculation of income statement by Absorption and Marginal costing, it can

determined that the net earnings from both techniques provides various results.

8

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500 8000 8000

Contribution 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Computation of Net profit by using absorption costing

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Gross profit 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

In calculation of income statement by Absorption and Marginal costing, it can

determined that the net earnings from both techniques provides various results.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2 Management accounting techniques and financial reporting documents

Management accounting technique plays a necessary role that gives effective

opportunities related to preparing better financial documents. It is a duty of management to

develop better plan for future operations,it gives better chance to assess estimated expensed as

well as cost (Parker, 2012). In context to this, there is a requirement to management of Tech(UK)

Ltd. To use better tools which help in improving profit level of firm. Conservatism techniques is

helpful to manage risk as well as additional cost to manage all resources in an effective way.

D2 Financial reports that accurately apply and interpret data

There are two various techniques used for profit and loss calculation of Tech (UK) Ltd.

And these are absorption and marginal costing. In addition to this, profit that is ascertained

through firm, provision application of these both methods is varied from the each other. With the

help of using absorption cost, profit is 7500 and on the other hand, from marginal costing profit

is 7800. Difference in profit arise because of non- consideration of the fixed assets in method of

absorption costing.

TASK 3

P4 Advantages and disadvantages of different types of planning tools

Budget: It mainly concern with a plan which is prepare for a limited period of time as

well as it give various informations about all the companies functions. They had consider the

guidelines as well as directions to their workers about specific objectives and aims in an effective

way. It involve operating as well as finance budgets that support in proper use of funds within

various functions for managing use of available resources in an adequate way.

Budgetary control: It is an effective as well as important strategies of budgeting which is

beneficial for Tech UK. Organisation is performing their activities in an proper manner like as

analysis, coordination and planning (Fullerton, Kennedy and Widener, 2013). It also considered

the centre of budget where they are divided within various sections. They support in giving

various opportunities to supervisor of Tech UK in enhancing volume of sales as well as making

higher profits.

Process of budgetary control

Consultation with managers: It is an main phase, where supervisor have to

consult with others department manager.

9

Management accounting technique plays a necessary role that gives effective

opportunities related to preparing better financial documents. It is a duty of management to

develop better plan for future operations,it gives better chance to assess estimated expensed as

well as cost (Parker, 2012). In context to this, there is a requirement to management of Tech(UK)

Ltd. To use better tools which help in improving profit level of firm. Conservatism techniques is

helpful to manage risk as well as additional cost to manage all resources in an effective way.

D2 Financial reports that accurately apply and interpret data

There are two various techniques used for profit and loss calculation of Tech (UK) Ltd.

And these are absorption and marginal costing. In addition to this, profit that is ascertained

through firm, provision application of these both methods is varied from the each other. With the

help of using absorption cost, profit is 7500 and on the other hand, from marginal costing profit

is 7800. Difference in profit arise because of non- consideration of the fixed assets in method of

absorption costing.

TASK 3

P4 Advantages and disadvantages of different types of planning tools

Budget: It mainly concern with a plan which is prepare for a limited period of time as

well as it give various informations about all the companies functions. They had consider the

guidelines as well as directions to their workers about specific objectives and aims in an effective

way. It involve operating as well as finance budgets that support in proper use of funds within

various functions for managing use of available resources in an adequate way.

Budgetary control: It is an effective as well as important strategies of budgeting which is

beneficial for Tech UK. Organisation is performing their activities in an proper manner like as

analysis, coordination and planning (Fullerton, Kennedy and Widener, 2013). It also considered

the centre of budget where they are divided within various sections. They support in giving

various opportunities to supervisor of Tech UK in enhancing volume of sales as well as making

higher profits.

Process of budgetary control

Consultation with managers: It is an main phase, where supervisor have to

consult with others department manager.

9

Effective assumption: Tech UK capabilities and abilities shows that how

company is interpreting data and informations are getting while discussions with

another department managers.

Fixing of corporation- al information regarding budgets : It contributes the

process of gathering information and data in term of various divisions so that

objectives of business can be achieved (Macintosh and Quattrone, 2010).

Measuring actual data : It is essential for employees of Tech UK to analyse the

collected of information and data is right or not.

Review analysis : It is involved as final stage where every procedure can be

analysed once so that it can decided that task in a perfect track.

Forecasting tool : The strategies of predicting things for forecasting the things of coming days.

In order to this it refer business which consider existing facts as well as records so that effective

decision can be made.

Advantages

From previews figures, organisation get an idea that what they have to do.

Easy to apply (Hopwood, Unerman and Fries, 2010).

It required skilled employees.

Disadvantage

Forecasting tool is not always perfect.

It is very costly within nature.

Scenario tools : Therefore alternative strategies can be implemented by Tech UK as per

previous conditions.

Advantages

Offers increase the chance of planning and entire management.

Could be changed in particular case.

Disadvantages

It consumes time.

Sometimes perfect data is not needed from the same.

Different planning tools

10

company is interpreting data and informations are getting while discussions with

another department managers.

Fixing of corporation- al information regarding budgets : It contributes the

process of gathering information and data in term of various divisions so that

objectives of business can be achieved (Macintosh and Quattrone, 2010).

Measuring actual data : It is essential for employees of Tech UK to analyse the

collected of information and data is right or not.

Review analysis : It is involved as final stage where every procedure can be

analysed once so that it can decided that task in a perfect track.

Forecasting tool : The strategies of predicting things for forecasting the things of coming days.

In order to this it refer business which consider existing facts as well as records so that effective

decision can be made.

Advantages

From previews figures, organisation get an idea that what they have to do.

Easy to apply (Hopwood, Unerman and Fries, 2010).

It required skilled employees.

Disadvantage

Forecasting tool is not always perfect.

It is very costly within nature.

Scenario tools : Therefore alternative strategies can be implemented by Tech UK as per

previous conditions.

Advantages

Offers increase the chance of planning and entire management.

Could be changed in particular case.

Disadvantages

It consumes time.

Sometimes perfect data is not needed from the same.

Different planning tools

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.