Tech UK Limited: Management Accounting, Costing, Budgeting Report

VerifiedAdded on 2024/05/31

|18

|3386

|339

Report

AI Summary

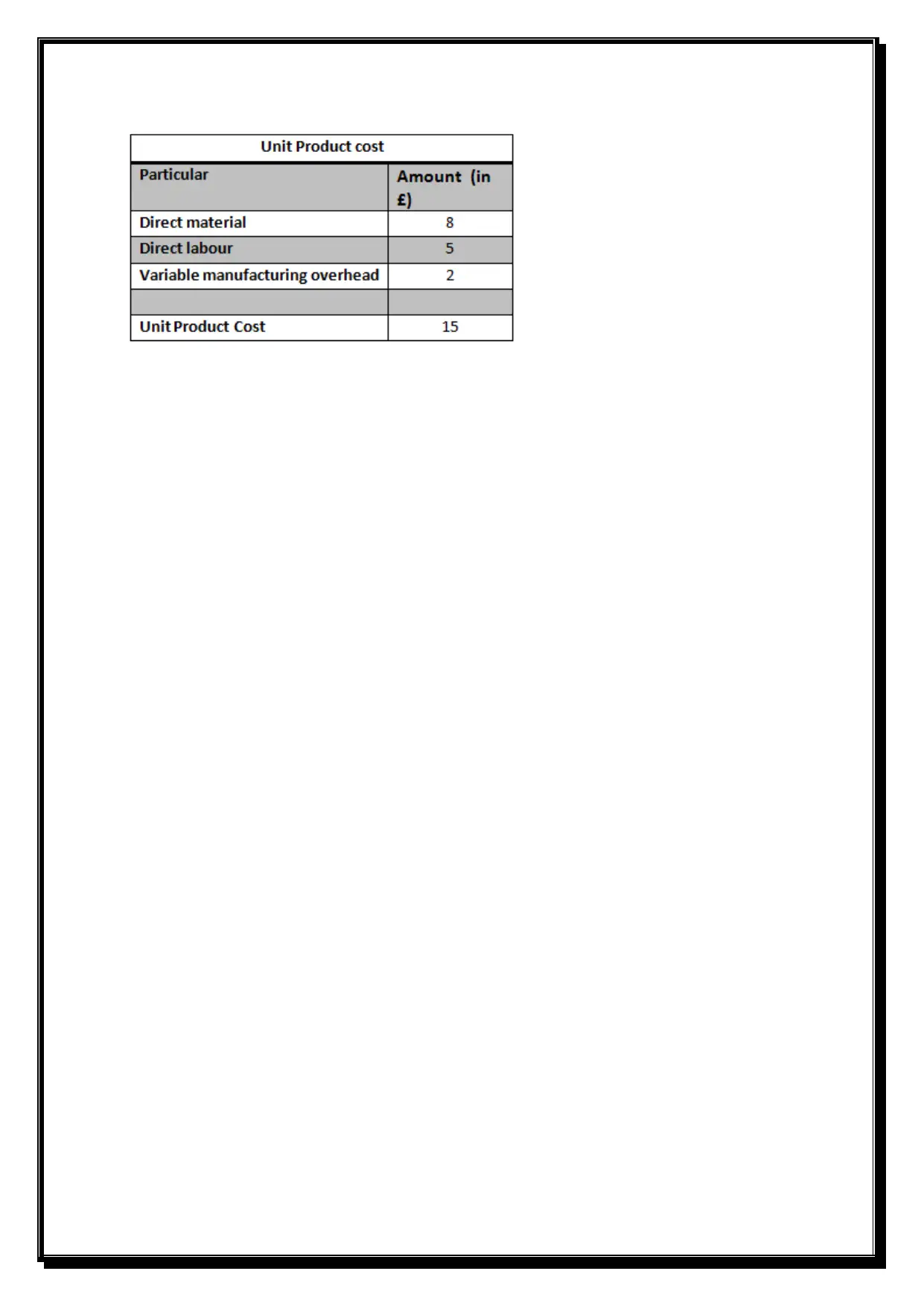

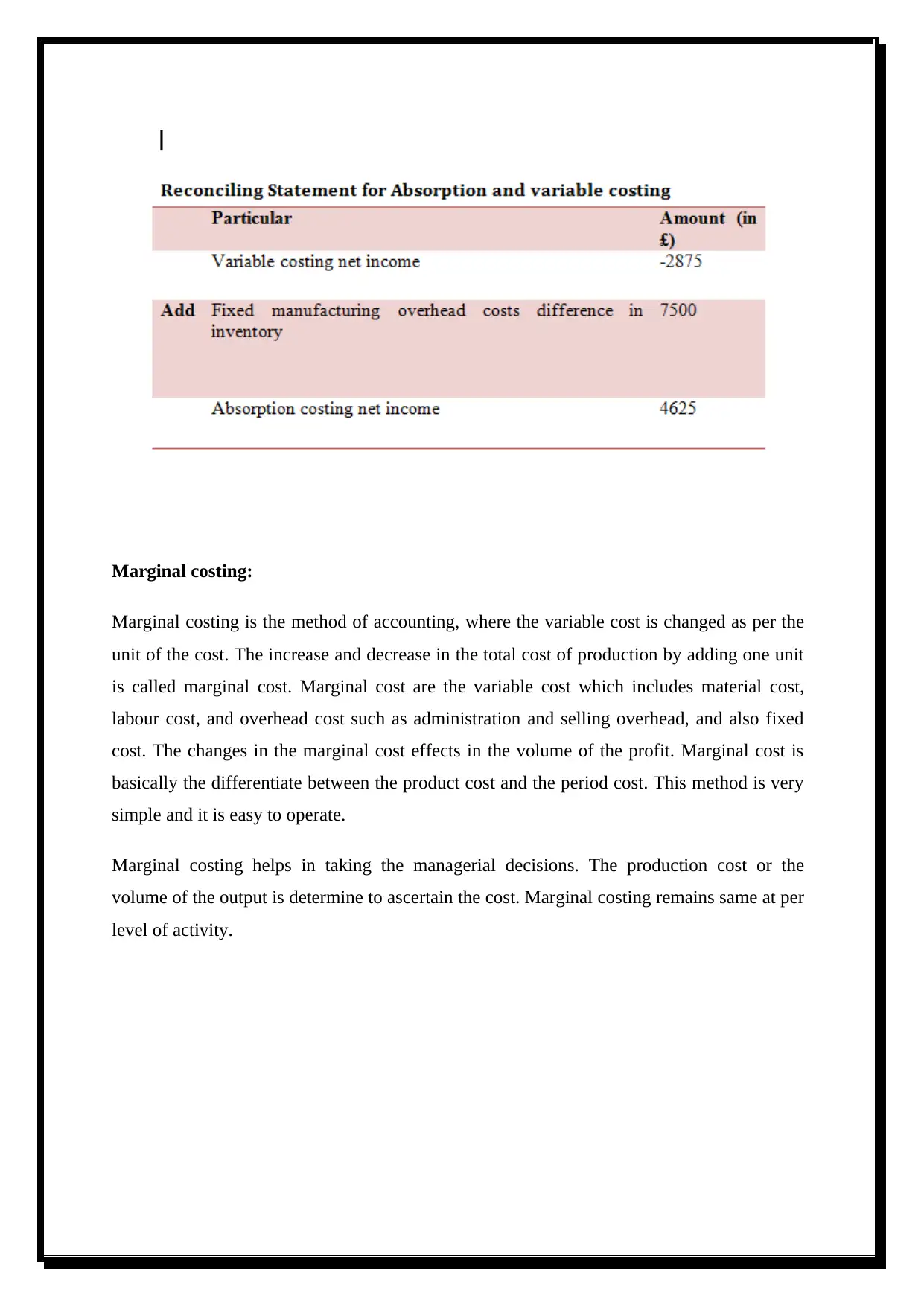

This management accounting report delves into various aspects of financial management within Tech (UK) Limited, a mobile charger and gadget retailer. It covers the functions of management accounting systems, including inventory and cost accounting, differentiating it from financial accounting. The report highlights the importance of management accounting as a decision-making tool, exploring cost accounting systems (actual, normal, and standard), inventory management systems (FIFO, LIFO, Average), and job costing systems. It also presents different types of managerial accounting reports and emphasizes the importance of accurate financial information presentation. Furthermore, the report discusses absorption and marginal costing methods, comparing their impact. Finally, it examines different kinds of budgets (master, financial, cash flow, static), along with their advantages and disadvantages, and outlines the budget preparation process, including pricing and costing considerations, providing a comprehensive overview of management accounting practices.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.