University of Delhi MBA Project: Automobile Sector Technology Analysis

VerifiedAdded on 2023/04/22

|34

|8415

|325

Project

AI Summary

This MBA project report, submitted to the Faculty of Management Studies, University of Delhi, analyzes the threats and opportunities presented by technology in the automobile sector. The report begins with an executive summary, literature review covering management of technology, technology forecasting, and technology intelligence. It then introduces the global and Indian automobile sectors, highlighting market trends, sales figures, and the impact of fuel emission standards. The study focuses on technology maturity in the Indian automobile sector, assessing the impact of ACES (Automated-Connected-Electrified-Shared) technologies. The report provides recommendations based on the analysis, aiming to offer a third-party perspective on the sector's future, considering factors like environmental enablement, marketplace forces, and the growth of electric and autonomous vehicles. The research examines three segments of the Indian automobile market: premium, middle segment, and economy segment. The project also acknowledges the contributions of various research studies and papers to support the findings.

Threat and Opportunity

Analysis of Technology in

the Automobile Sector

A Project Report Submitted for the partial fulfilment of the award of degree of

Master of Business Administration (M.B.A.)

Under the Guidance of

Prof. Soma Dey

Submitted by-

Shreya Kashyap

F-350, MBA (FT) – 2017-2019

Area Code: SBM

Faculty of Management Studies

University of Delhi

February 2019

Analysis of Technology in

the Automobile Sector

A Project Report Submitted for the partial fulfilment of the award of degree of

Master of Business Administration (M.B.A.)

Under the Guidance of

Prof. Soma Dey

Submitted by-

Shreya Kashyap

F-350, MBA (FT) – 2017-2019

Area Code: SBM

Faculty of Management Studies

University of Delhi

February 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CERTIFICATE

This is to certify that the project titled, “Threat and Opportunity Analysis of Technology in

the Automobile Sector” submitted in partial fulfilment of the requirements for the Degree

of Master of Business Administration is a record of original research work carried out by

myself. Any material borrowed or referred to is duly acknowledged.

Student

Shreya Kashyap

Roll No. F-350

MBA(FT)-2017-19

This is to certify that the above-mentioned project titled, “Threat and Opportunity Analysis

of Technology in the Automobile Sector” submitted by Shreya Kashyap, MBA(FT) Batch of

2019, Roll No. 350 has been carried out under my supervision.

Project Guide

Prof. Soma Dey

Faculty of Management Studies

University of Delhi

This is to certify that the project titled, “Threat and Opportunity Analysis of Technology in

the Automobile Sector” submitted in partial fulfilment of the requirements for the Degree

of Master of Business Administration is a record of original research work carried out by

myself. Any material borrowed or referred to is duly acknowledged.

Student

Shreya Kashyap

Roll No. F-350

MBA(FT)-2017-19

This is to certify that the above-mentioned project titled, “Threat and Opportunity Analysis

of Technology in the Automobile Sector” submitted by Shreya Kashyap, MBA(FT) Batch of

2019, Roll No. 350 has been carried out under my supervision.

Project Guide

Prof. Soma Dey

Faculty of Management Studies

University of Delhi

ACKNOWLEDGEMENT

I would like to express my heartfelt gratitude to my guide Dr. Soma Dey for providing me the

opportunity to work under her guidance. Ma’am provided me with constant help and

support throughout the duration of this project. Pursuing a project in such a vast and

dynamic field would not have been possible without her encouragement.

Apart from the project work, I would also like to hereby thank Dr. Soma Dey for being a

faculty member who has always laid strong emphasis on creative thinking and always been

there for her students whenever they needed her support and guidance.

I would also like to thank the entire faculty at FMS, Delhi for providing me with an enriching

and I have learnt from several articles, research studies and papers from national and

international entities. I acknowledge the value I have received from these bodies of

knowledge.

Last but not the least, I would like to thank my colleagues and friends for their support and

words of motivation during the project tenure.

Shreya Kashyap

Faculty of Management Studies

University of Delhi

February 2018

I would like to express my heartfelt gratitude to my guide Dr. Soma Dey for providing me the

opportunity to work under her guidance. Ma’am provided me with constant help and

support throughout the duration of this project. Pursuing a project in such a vast and

dynamic field would not have been possible without her encouragement.

Apart from the project work, I would also like to hereby thank Dr. Soma Dey for being a

faculty member who has always laid strong emphasis on creative thinking and always been

there for her students whenever they needed her support and guidance.

I would also like to thank the entire faculty at FMS, Delhi for providing me with an enriching

and I have learnt from several articles, research studies and papers from national and

international entities. I acknowledge the value I have received from these bodies of

knowledge.

Last but not the least, I would like to thank my colleagues and friends for their support and

words of motivation during the project tenure.

Shreya Kashyap

Faculty of Management Studies

University of Delhi

February 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INDEX

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The automobile sector is at an interesting crossroad today. Over the past few years, the

explosion of digital and the introduction of smart technologies have pushed this sector into

the next stage of its growth trajectory. Clean fuels and climate change concerns have put

great pressure on this industry to innovate. This makes it important to optimise the impact

of technological developments on the business and avoid threats that come from both

within and outside the sector/industry.

In this project, using a technology planning support function, the technology maturity of the

automobile sector in India will be estimated. This function highlights possible threats and so

helps planners and decision makers in making the right decision before the anticipated

problem occurs. Based on the function output estimates and prediction of the future

landscape, recommendations will be provided for the automobile sector in India.

This research is aimed to provide a 3rd party analysis of the sector, a view that is different

from individuals working in this sector currently. Apart from technology readiness,

environmental enablement through policy and regulations along with marketplace forces

play an important role in the success of an industry.

The automobile sector is at an interesting crossroad today. Over the past few years, the

explosion of digital and the introduction of smart technologies have pushed this sector into

the next stage of its growth trajectory. Clean fuels and climate change concerns have put

great pressure on this industry to innovate. This makes it important to optimise the impact

of technological developments on the business and avoid threats that come from both

within and outside the sector/industry.

In this project, using a technology planning support function, the technology maturity of the

automobile sector in India will be estimated. This function highlights possible threats and so

helps planners and decision makers in making the right decision before the anticipated

problem occurs. Based on the function output estimates and prediction of the future

landscape, recommendations will be provided for the automobile sector in India.

This research is aimed to provide a 3rd party analysis of the sector, a view that is different

from individuals working in this sector currently. Apart from technology readiness,

environmental enablement through policy and regulations along with marketplace forces

play an important role in the success of an industry.

LITERATURE REVIEW

1 MANAGEMENT OF TECHNOLOGY

The term technology refers “not only to physical items (e.g. machines or tools), but also to methods,

techniques, or software that humans require in order to solve a problem or gain achievement. The

term technology has evolved more so with the managerial concept compared to any other concept.

When technology is defined in the literature, it is described as applied knowledge focusing on the

know- how of the organisation. Technology management is a process, which includes planning,

directing, controlling, developing and implementing technological capabilities to shape and

accomplish the strategic and operational objectives of an organization. Irrespective of what is

managed, management involves concerns about the future. In technology management a decision

must be made by managers today that will affect the organisation’s future. This decision process

needs accurate inputs to support technology managers in anticipating the future. This could be using

technology forecasting, which is further discussed.”

2 TECHNOLOGY FORECASTING

Technology is responsible for many changes. The decision-making process can be greatly improved

by technology forecasting due to greater accuracy of the future. “A technological forecast includes

four elements: the time of the forecast or the future date when the forecast is to be realised, the

technology being forecast, the characteristics of the technology or the functional capabilities of the

technology, and a statement about probability. The greater part of the technological forecasting

literature since the 1960s has been devoted to structured judgmental approaches such as Delphi

surveys and cross impact matrices. There are few real industrial applications of technology

forecasting and most of the tools are described only in theoretical terms. Therefore, there is a need

for a systematic process that can generate dynamic support for technology planning and can use

simple and useful tools.”

3 TECHNOLOGY INTELLIGENCE (TI)

Most strategic managers claim that their companies keep up-to-date in their field but they do not

have a systematic way to capture the important elements of technology changes from the general

information around them. In today’s world, an arbitrary process is insufficient. “Methods and tools,

primarily in the technology intelligence field such as those described in are needed to offer actions

to cope with threats that are not necessarily obvious to detect. Such a threat, in the form of an

emerging technology or new technological innovation, product or service, may replace the existing

dominant technology in the market, despite the fact that it may initially perform worse in terms of

the measures used by the current market leaders; this concept is referred to as disruptive

technology. The activity of collecting and evaluating information on technology developments is

called technology intelligence (TI) or technology watch. Literature on technology intelligence

describes many processes. TI is an important subject matter in this dissertation in helping to develop

technology watch (TW) framework that will work as a tool for monitoring; identifying and assessing

the technologies that emerge and could disrupt the business by affecting or replacing the existing

technologies which comprise the bottom line of the company.”

1 MANAGEMENT OF TECHNOLOGY

The term technology refers “not only to physical items (e.g. machines or tools), but also to methods,

techniques, or software that humans require in order to solve a problem or gain achievement. The

term technology has evolved more so with the managerial concept compared to any other concept.

When technology is defined in the literature, it is described as applied knowledge focusing on the

know- how of the organisation. Technology management is a process, which includes planning,

directing, controlling, developing and implementing technological capabilities to shape and

accomplish the strategic and operational objectives of an organization. Irrespective of what is

managed, management involves concerns about the future. In technology management a decision

must be made by managers today that will affect the organisation’s future. This decision process

needs accurate inputs to support technology managers in anticipating the future. This could be using

technology forecasting, which is further discussed.”

2 TECHNOLOGY FORECASTING

Technology is responsible for many changes. The decision-making process can be greatly improved

by technology forecasting due to greater accuracy of the future. “A technological forecast includes

four elements: the time of the forecast or the future date when the forecast is to be realised, the

technology being forecast, the characteristics of the technology or the functional capabilities of the

technology, and a statement about probability. The greater part of the technological forecasting

literature since the 1960s has been devoted to structured judgmental approaches such as Delphi

surveys and cross impact matrices. There are few real industrial applications of technology

forecasting and most of the tools are described only in theoretical terms. Therefore, there is a need

for a systematic process that can generate dynamic support for technology planning and can use

simple and useful tools.”

3 TECHNOLOGY INTELLIGENCE (TI)

Most strategic managers claim that their companies keep up-to-date in their field but they do not

have a systematic way to capture the important elements of technology changes from the general

information around them. In today’s world, an arbitrary process is insufficient. “Methods and tools,

primarily in the technology intelligence field such as those described in are needed to offer actions

to cope with threats that are not necessarily obvious to detect. Such a threat, in the form of an

emerging technology or new technological innovation, product or service, may replace the existing

dominant technology in the market, despite the fact that it may initially perform worse in terms of

the measures used by the current market leaders; this concept is referred to as disruptive

technology. The activity of collecting and evaluating information on technology developments is

called technology intelligence (TI) or technology watch. Literature on technology intelligence

describes many processes. TI is an important subject matter in this dissertation in helping to develop

technology watch (TW) framework that will work as a tool for monitoring; identifying and assessing

the technologies that emerge and could disrupt the business by affecting or replacing the existing

technologies which comprise the bottom line of the company.”

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CHAPTER 1: INTRODUCTION

Globalisation of competition and the accelerating rate of technology change have created

difficult challenges for advanced technology-based industries in this new millennium.

Companies in these industries must now continually reduce costs and develop better

products and services in order to maintain a competitive advantage in an environment that

is constantly changing.

High costs for research and development (R&D) force high technology companies to choose

which technologies to invest in more carefully. Technologies are introduced into a company

in order to make a positive contribution to its products and services. Companies need

technology planning in order to make better decisions with regard to strategic corporate

planning, R&D management, product development, production and marketing.

The automobile sector has long been at the forefront of embracing new-age technology.

The technology future of this industry is ACES (Automated-Connected-Electrified-Shared). As

the automotive sector keeps innovating and the competition intensifies alongside, the risks

associated with extensive R&D in one field can have a detrimental impact on market share

and bottom line. Unpredictability of results and secrecy involving competitor R&D

investments makes technology planning and forecasting extremely important for a company

in this sector.

As the developing countries’ gross incomes rise, more and more people in these countries

are willing to make investments in the auto industry; buy cars for personal travel, trucks for

transporting goods or tractors for field work or even put in money for further avenues of

income generation. Since level of transportation and the GDP of any country are inter-

linked, improved GDPs of developing countries like BRICS (Brazil, Russia, India, China and

South Africa) indicate greater scope for automobile sector growth and penetration within

these countries. New technologies bring in benefits of greater cost to scale, improved

efficiency, increased comfort to end consumers and at times, a competitive advantage to

companies.

India is expected to emerge as the world’s 3rd largest passenger market by 2021 and also a

leader in shared mobility by 2030. It is expected to be at the forefront of electric and

autonomous vehicles in the years to come. With the benefits of growing demand due to

rising incomes of the middle class and young population, improving regulatory processes in

FDI and FII and a fairly competitive marketplace, India becomes an interesting geography for

this study.

As Uber and Ola are changing marketplace dynamics in the shared mobility space, Indian

government is going ambitious with its Electric Vehicles Plan, it is important to understand

the opportunities and threats that come with such developments. Understanding India’s

maturity in accepting these factors as well their feasibility of implementation are important

considerations for this study. Indian automobile companies in three segments will be

analysed using this model – Premium, Middle Segment and the Economy Segment. Before

delving into that, a background is provided in the initial segments of this report.

Globalisation of competition and the accelerating rate of technology change have created

difficult challenges for advanced technology-based industries in this new millennium.

Companies in these industries must now continually reduce costs and develop better

products and services in order to maintain a competitive advantage in an environment that

is constantly changing.

High costs for research and development (R&D) force high technology companies to choose

which technologies to invest in more carefully. Technologies are introduced into a company

in order to make a positive contribution to its products and services. Companies need

technology planning in order to make better decisions with regard to strategic corporate

planning, R&D management, product development, production and marketing.

The automobile sector has long been at the forefront of embracing new-age technology.

The technology future of this industry is ACES (Automated-Connected-Electrified-Shared). As

the automotive sector keeps innovating and the competition intensifies alongside, the risks

associated with extensive R&D in one field can have a detrimental impact on market share

and bottom line. Unpredictability of results and secrecy involving competitor R&D

investments makes technology planning and forecasting extremely important for a company

in this sector.

As the developing countries’ gross incomes rise, more and more people in these countries

are willing to make investments in the auto industry; buy cars for personal travel, trucks for

transporting goods or tractors for field work or even put in money for further avenues of

income generation. Since level of transportation and the GDP of any country are inter-

linked, improved GDPs of developing countries like BRICS (Brazil, Russia, India, China and

South Africa) indicate greater scope for automobile sector growth and penetration within

these countries. New technologies bring in benefits of greater cost to scale, improved

efficiency, increased comfort to end consumers and at times, a competitive advantage to

companies.

India is expected to emerge as the world’s 3rd largest passenger market by 2021 and also a

leader in shared mobility by 2030. It is expected to be at the forefront of electric and

autonomous vehicles in the years to come. With the benefits of growing demand due to

rising incomes of the middle class and young population, improving regulatory processes in

FDI and FII and a fairly competitive marketplace, India becomes an interesting geography for

this study.

As Uber and Ola are changing marketplace dynamics in the shared mobility space, Indian

government is going ambitious with its Electric Vehicles Plan, it is important to understand

the opportunities and threats that come with such developments. Understanding India’s

maturity in accepting these factors as well their feasibility of implementation are important

considerations for this study. Indian automobile companies in three segments will be

analysed using this model – Premium, Middle Segment and the Economy Segment. Before

delving into that, a background is provided in the initial segments of this report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.1 WORLDWIDE AUTOMOBILE SECTOR AT A GLANCE

The global economy is transforming dramatically, triggered by the accelerated increase in

new technologies, development in emerging markets like India, policies towards

sustainability and evolving consumer preferences with respect to ownership. The mobility of

people and goods has also witnessed a considerable transition over the last century. As

claimed by the experts, the automobile industry is at the cusp of disruptive in the last

decade. For instance, the sale of new passenger vehicles1 has grown at a CAGR of 3.15%2 as

shown in exhibit 1.

2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7 2 0 1 8

74.9

78.2

82.1

85.6

88.3

89.7

93.9

96.8

99.1

Glo b a l T r en d s i N P A S S en g er Veh i c l e S a l es

Year

Sales in Millions

While the automobile industry is primarily dominated by manufacturers based out of

Germany, US and Japan as highlighted in exhibit 2, their new profits is likely to come from

emerging markets of BRICS countries, whereas the growth in US, Europe, Japan and South

Korea is expected to remain stagnant in terms of profitability.

Toyota Motor

Volkswagen

Daimler

General Motors

Ford Motor

Honda Motor

Fiat (FCA)

SAIC Motor

BMW Group

Nissan Motor

0 50 100 150 200 250 300

265.4

261.1

185.4

160

158

140.1

133.7

130.4

112.3

109.8

Revenue of the leading automotive manufacturers worldwide

in FY 2018 (in billion U.S. dollars)

3

1 Passenger vehicles

2 Taken from Statista

3 Statista

The global economy is transforming dramatically, triggered by the accelerated increase in

new technologies, development in emerging markets like India, policies towards

sustainability and evolving consumer preferences with respect to ownership. The mobility of

people and goods has also witnessed a considerable transition over the last century. As

claimed by the experts, the automobile industry is at the cusp of disruptive in the last

decade. For instance, the sale of new passenger vehicles1 has grown at a CAGR of 3.15%2 as

shown in exhibit 1.

2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7 2 0 1 8

74.9

78.2

82.1

85.6

88.3

89.7

93.9

96.8

99.1

Glo b a l T r en d s i N P A S S en g er Veh i c l e S a l es

Year

Sales in Millions

While the automobile industry is primarily dominated by manufacturers based out of

Germany, US and Japan as highlighted in exhibit 2, their new profits is likely to come from

emerging markets of BRICS countries, whereas the growth in US, Europe, Japan and South

Korea is expected to remain stagnant in terms of profitability.

Toyota Motor

Volkswagen

Daimler

General Motors

Ford Motor

Honda Motor

Fiat (FCA)

SAIC Motor

BMW Group

Nissan Motor

0 50 100 150 200 250 300

265.4

261.1

185.4

160

158

140.1

133.7

130.4

112.3

109.8

Revenue of the leading automotive manufacturers worldwide

in FY 2018 (in billion U.S. dollars)

3

1 Passenger vehicles

2 Taken from Statista

3 Statista

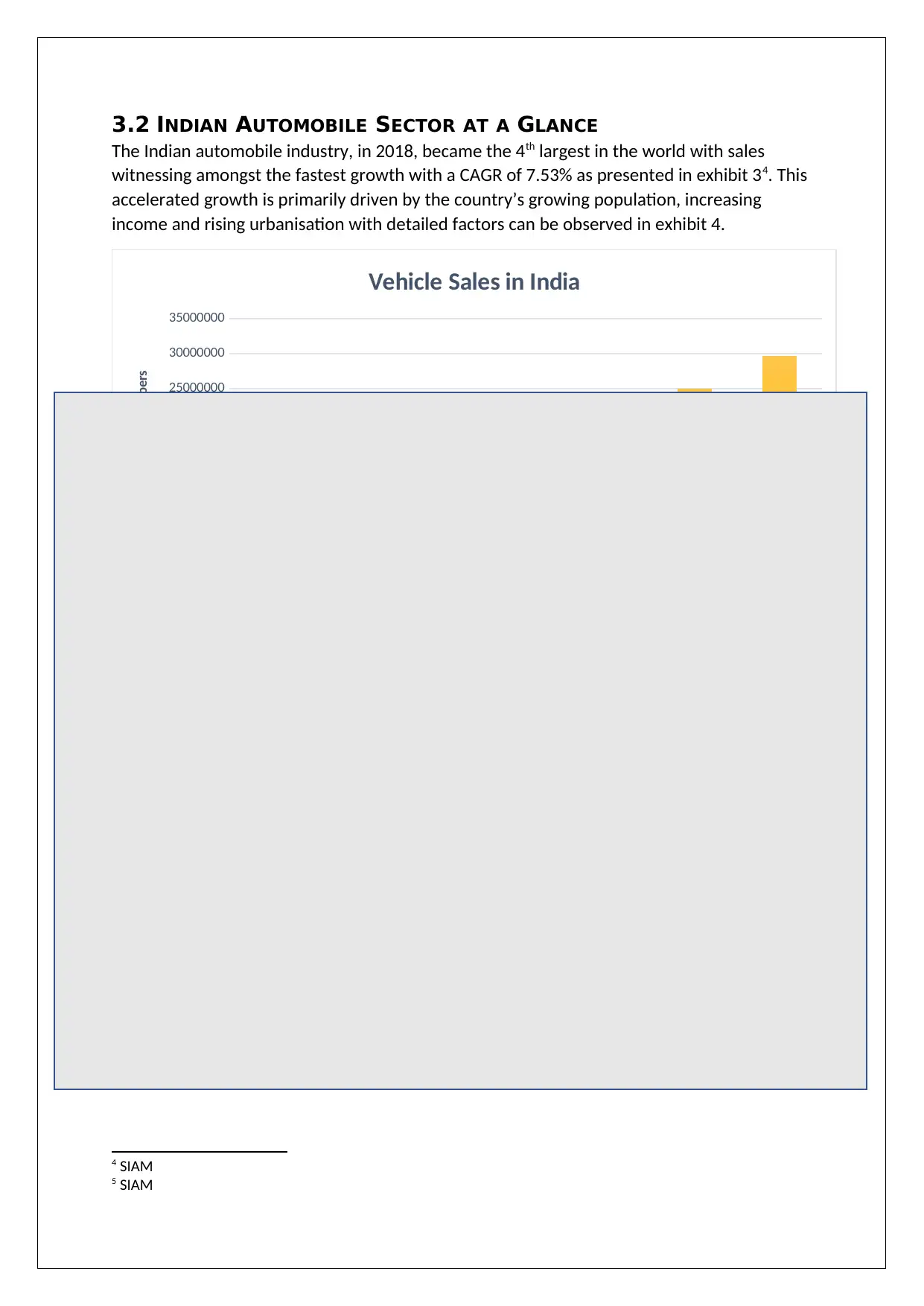

3.2 INDIAN AUTOMOBILE SECTOR AT A GLANCE

The Indian automobile industry, in 2018, became the 4th largest in the world with sales

witnessing amongst the fastest growth with a CAGR of 7.53% as presented in exhibit 34. This

accelerated growth is primarily driven by the country’s growing population, increasing

income and rising urbanisation with detailed factors can be observed in exhibit 4.

2012 2013 2014 2015 2016 2017 2018

0

5000000

10000000

15000000

20000000

25000000

30000000

35000000

Vehicle Sales in India

Passenger Vehicles Commercial Vehicles Three Wheelers Two Wheelers

Year

Sales in Absolute Numbers

The two wheelers have the maximum market share in sales volume as can be observed in Exhibit 45.

While the sales of passenger vehicles in India have constituted to about 2.9%-3.5% of the world’s

share, the Indian market has emerged as the biggest market for two and three-wheelers. This

growth is attributed to the massive spending by the Indian Government in rural programmes and

large road-construction, leading to an accelerated pick up sales volume in smaller towns and villages.

12 3 2

83

Percentage Share of Vehicle Sales in 2018

Passenger Vehicles Commercial Vehicles

Three Wheelers Two Wheelers

4 SIAM

5 SIAM

The Indian automobile industry, in 2018, became the 4th largest in the world with sales

witnessing amongst the fastest growth with a CAGR of 7.53% as presented in exhibit 34. This

accelerated growth is primarily driven by the country’s growing population, increasing

income and rising urbanisation with detailed factors can be observed in exhibit 4.

2012 2013 2014 2015 2016 2017 2018

0

5000000

10000000

15000000

20000000

25000000

30000000

35000000

Vehicle Sales in India

Passenger Vehicles Commercial Vehicles Three Wheelers Two Wheelers

Year

Sales in Absolute Numbers

The two wheelers have the maximum market share in sales volume as can be observed in Exhibit 45.

While the sales of passenger vehicles in India have constituted to about 2.9%-3.5% of the world’s

share, the Indian market has emerged as the biggest market for two and three-wheelers. This

growth is attributed to the massive spending by the Indian Government in rural programmes and

large road-construction, leading to an accelerated pick up sales volume in smaller towns and villages.

12 3 2

83

Percentage Share of Vehicle Sales in 2018

Passenger Vehicles Commercial Vehicles

Three Wheelers Two Wheelers

4 SIAM

5 SIAM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3.2.1 Fuel Emission Standards

The Indian Government regulations and safety, among other standards, have pushed

automobile manufacturers to make greener and safer vehicles. This can be observed with

the notification from the Ministry of Road, Transport and Highways (MoRTH) to enforce

Bharat Stage VI (BS VI) emission regime nationwide from April 2020. This rachet-up of

emission standards is in continuation to the implementation of BS IV emission standards in

2017. The implementation of BS VI mandates a 68% reduction in NOx and 87% reduction in

particulate matter (PM) for diesel vehicles as compared to BS IV standards, whereas the

vehicles based on gasoline fuel are mandated for a reduction of 25% reduction of NOx.

While it is worth noting the Government’s decision to leapfrog from BS IV to BS VI bypassing

BS V standards, the transition is expected to increase the vehicle costs by 12-20%6.

3.2.2 Electric Vehicles

The electric vehicles market was unregulated until in 2013-14, the country saw the

burgeoning of electric rickshaws in various parts of the country. Tripura, though a small

state, was the first to regulate the EV market, with a policy titled “Tripura Battery Operated

Rickshaw Rules 2014”, under which the registration of electric rickshaws was made

compulsory7. Simultaneously, the Indian Government unveiled the National Electric Mobility

Mission Plan 2020 (NEPMP) with a target to add 6-7 million new full range electric vehicles

including an estimated 4-5 million two-wheelers by 2020. This was brought in the context of

national energy security wherein petroleum products are primarily imported, environmental

change mitigation and promote domestic manufacturing8.

The major push for EVs came when the Faster Adoption and Manufacturing of (Hybrid &)

Electric Vehicles (FAME) scheme was launched in April 2015. The scheme offered incentives

for adoption in form of rebates and lower taxes. Depending on the vehicle, battery

technology (hybrid or full electric) subsidies were fixed. It ranged from INR 29,000 for 2-

6 CSE Report

7 http://agartalacity.tripura.gov.in/act/AMC_Battery.pdf (Retrieved on 20th February 2019)

8 http://www.pib.nic.in/newsite/erelease.aspx?relid=91444 (Retrieved on 20th February 2019)

The Indian Government regulations and safety, among other standards, have pushed

automobile manufacturers to make greener and safer vehicles. This can be observed with

the notification from the Ministry of Road, Transport and Highways (MoRTH) to enforce

Bharat Stage VI (BS VI) emission regime nationwide from April 2020. This rachet-up of

emission standards is in continuation to the implementation of BS IV emission standards in

2017. The implementation of BS VI mandates a 68% reduction in NOx and 87% reduction in

particulate matter (PM) for diesel vehicles as compared to BS IV standards, whereas the

vehicles based on gasoline fuel are mandated for a reduction of 25% reduction of NOx.

While it is worth noting the Government’s decision to leapfrog from BS IV to BS VI bypassing

BS V standards, the transition is expected to increase the vehicle costs by 12-20%6.

3.2.2 Electric Vehicles

The electric vehicles market was unregulated until in 2013-14, the country saw the

burgeoning of electric rickshaws in various parts of the country. Tripura, though a small

state, was the first to regulate the EV market, with a policy titled “Tripura Battery Operated

Rickshaw Rules 2014”, under which the registration of electric rickshaws was made

compulsory7. Simultaneously, the Indian Government unveiled the National Electric Mobility

Mission Plan 2020 (NEPMP) with a target to add 6-7 million new full range electric vehicles

including an estimated 4-5 million two-wheelers by 2020. This was brought in the context of

national energy security wherein petroleum products are primarily imported, environmental

change mitigation and promote domestic manufacturing8.

The major push for EVs came when the Faster Adoption and Manufacturing of (Hybrid &)

Electric Vehicles (FAME) scheme was launched in April 2015. The scheme offered incentives

for adoption in form of rebates and lower taxes. Depending on the vehicle, battery

technology (hybrid or full electric) subsidies were fixed. It ranged from INR 29,000 for 2-

6 CSE Report

7 http://agartalacity.tripura.gov.in/act/AMC_Battery.pdf (Retrieved on 20th February 2019)

8 http://www.pib.nic.in/newsite/erelease.aspx?relid=91444 (Retrieved on 20th February 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

wheelers to INR 138,000 for 4-wheelers. Phase 1 of the scheme, initially slated to continue

for just 2 years, was extended until March 2018. Of the INR 1.27 billion spent through the

FAME scheme till June 2017, around 60 % of the funds were used to support the purchase of

mild hybrid vehicles20. In March 2017, the FAME scheme was amended to exclude mild

hybrids from the demand-based incentives since most of the funds were used by them, with

the government feeling that mild hybrids were not significantly accelerating the path to the

development of full range EVs. This impacted the sales of Maruti Suzuki’s Ciaz and

Mahindra’s Scorpio which were the best-selling models under the mild hybrid category9.

As of November 2017, the FAME scheme had been extended to support the purchase of

163,997 vehicles10. Also, under the FAME scheme, support for research and development of

batteries stands at INR 0.3 billion, with INR 2.4 million allocated for Non-Ferrous Materials

Technology Development Centre, Hyderabad and INR 6.1 million allocated to IIT Kanpur11.

The push for electric mobility charging stations will first be rolled out in cities with a

population of greater than 4 million residents i.e. Mumbai, Delhi, Bangalore, Hyderabad,

Ahmedabad, Chennai, Kolkata, Surat and Pune. The rollout means that after much waiting

and uncertainty, India will finally have public electric charging stations as a reality rather

than just a pipe dream. The Indian government has already recently announced additional

benefits to electric car owners such as special green number plates.

9 http://www.autocarpro.in/news-national/government-subsidy-mild-hybrids-fame-scheme-withdrawn-24206 (Retrieved on 20th

February 2019)

10 http://www.newindianexpress.com/business/2017/dec/28/focus-on-e-mobility-in-public-transport-via-fame-scheme-government-

1738961.html (Retrieved on 20th February 2019)

11 http://www.autocarpro.in/news-national/government-spent-rs-crore-research-development-ev-battery-27566 (Retrieved on

February 20th 2019)

for just 2 years, was extended until March 2018. Of the INR 1.27 billion spent through the

FAME scheme till June 2017, around 60 % of the funds were used to support the purchase of

mild hybrid vehicles20. In March 2017, the FAME scheme was amended to exclude mild

hybrids from the demand-based incentives since most of the funds were used by them, with

the government feeling that mild hybrids were not significantly accelerating the path to the

development of full range EVs. This impacted the sales of Maruti Suzuki’s Ciaz and

Mahindra’s Scorpio which were the best-selling models under the mild hybrid category9.

As of November 2017, the FAME scheme had been extended to support the purchase of

163,997 vehicles10. Also, under the FAME scheme, support for research and development of

batteries stands at INR 0.3 billion, with INR 2.4 million allocated for Non-Ferrous Materials

Technology Development Centre, Hyderabad and INR 6.1 million allocated to IIT Kanpur11.

The push for electric mobility charging stations will first be rolled out in cities with a

population of greater than 4 million residents i.e. Mumbai, Delhi, Bangalore, Hyderabad,

Ahmedabad, Chennai, Kolkata, Surat and Pune. The rollout means that after much waiting

and uncertainty, India will finally have public electric charging stations as a reality rather

than just a pipe dream. The Indian government has already recently announced additional

benefits to electric car owners such as special green number plates.

9 http://www.autocarpro.in/news-national/government-subsidy-mild-hybrids-fame-scheme-withdrawn-24206 (Retrieved on 20th

February 2019)

10 http://www.newindianexpress.com/business/2017/dec/28/focus-on-e-mobility-in-public-transport-via-fame-scheme-government-

1738961.html (Retrieved on 20th February 2019)

11 http://www.autocarpro.in/news-national/government-spent-rs-crore-research-development-ev-battery-27566 (Retrieved on

February 20th 2019)

3.3 AUTOMOBILE TECHNOLOGICAL INNOVATIONS OVER THE YEARS

3.3.1 The Steam Engine

The steam engine was, undoubtedly, the most important innovation in automobile

engineering. The first reliable engine was developed by James Watt in 1775.

Steam engines would initially lead to the development of locomotives and ship propulsion

but would later be refined for use in early cars in the late 1800's to early 1900's. The steam

car became popular at this time, especially as roads improved. Fuel was relatively cheap as

well.

The fate of the steam engine car was sealed when Henry Ford fully developed his mass

production process. Electrical starters for internal combustion engines also removed the

need for hand crank engine starting but internal combustion engine driven cars would

ultimately win out as they were much cheaper to buy.

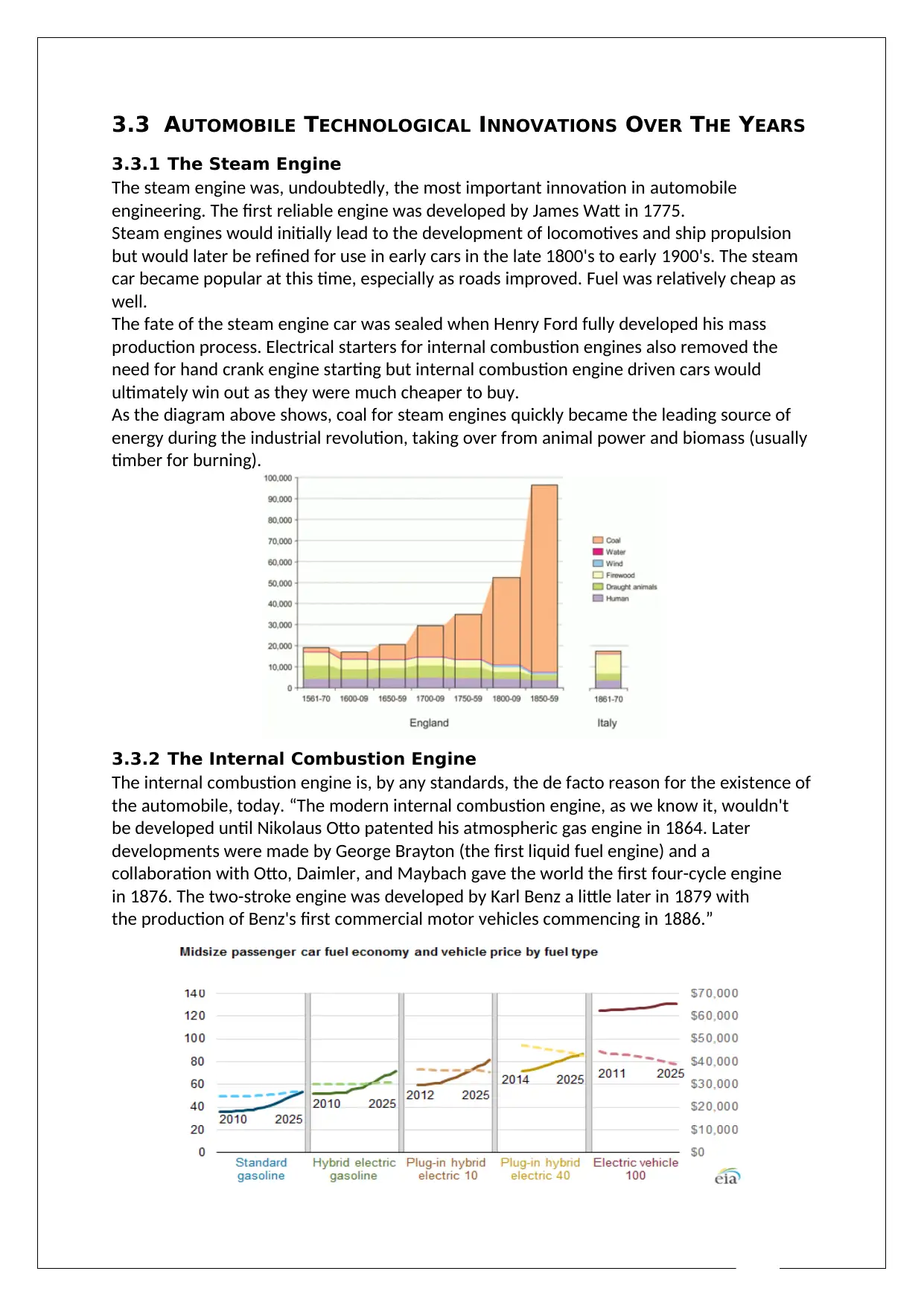

As the diagram above shows, coal for steam engines quickly became the leading source of

energy during the industrial revolution, taking over from animal power and biomass (usually

timber for burning).

3.3.2 The Internal Combustion Engine

The internal combustion engine is, by any standards, the de facto reason for the existence of

the automobile, today. “The modern internal combustion engine, as we know it, wouldn't

be developed until Nikolaus Otto patented his atmospheric gas engine in 1864. Later

developments were made by George Brayton (the first liquid fuel engine) and a

collaboration with Otto, Daimler, and Maybach gave the world the first four-cycle engine

in 1876. The two-stroke engine was developed by Karl Benz a little later in 1879 with

the production of Benz's first commercial motor vehicles commencing in 1886.”

3.3.1 The Steam Engine

The steam engine was, undoubtedly, the most important innovation in automobile

engineering. The first reliable engine was developed by James Watt in 1775.

Steam engines would initially lead to the development of locomotives and ship propulsion

but would later be refined for use in early cars in the late 1800's to early 1900's. The steam

car became popular at this time, especially as roads improved. Fuel was relatively cheap as

well.

The fate of the steam engine car was sealed when Henry Ford fully developed his mass

production process. Electrical starters for internal combustion engines also removed the

need for hand crank engine starting but internal combustion engine driven cars would

ultimately win out as they were much cheaper to buy.

As the diagram above shows, coal for steam engines quickly became the leading source of

energy during the industrial revolution, taking over from animal power and biomass (usually

timber for burning).

3.3.2 The Internal Combustion Engine

The internal combustion engine is, by any standards, the de facto reason for the existence of

the automobile, today. “The modern internal combustion engine, as we know it, wouldn't

be developed until Nikolaus Otto patented his atmospheric gas engine in 1864. Later

developments were made by George Brayton (the first liquid fuel engine) and a

collaboration with Otto, Daimler, and Maybach gave the world the first four-cycle engine

in 1876. The two-stroke engine was developed by Karl Benz a little later in 1879 with

the production of Benz's first commercial motor vehicles commencing in 1886.”

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.