AASB 138 Application: Technology Enterprises Ltd Case Study Report

VerifiedAdded on 2020/10/22

|9

|2648

|415

Case Study

AI Summary

This case study report examines the application of AASB 138, the Australian Accounting Standards Board standard for intangible assets, within the context of Technology Enterprises Ltd. The company is engaged in a research and development project related to battery recharging technology. The report details the accounting standards relevant to the preparation of financial statements, specifically focusing on the recognition and measurement of internally generated intangible assets like patents. It analyzes the impact of AASB 138's restrictions on the comparability of financial statements and provides recommendations for Technology Enterprises Ltd to improve investor understanding of its financial reporting, including enhanced communication of key information and clear disclosure of accounting policies. The report also discusses the classification of R&D expenditure into research and development phases, and the costs associated with intangible assets. The report concludes by emphasizing the importance of compliance with relevant business laws and regulations to ensure the accuracy and reliability of financial statements.

Case Study Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The Australian Accounting Standards Board 138 is considered as a Commenwealth Government

Body which is governing all the accounting standards by laying down principles or standards

company, public sector enterprises or not profit business organisation has to comply. This report is

based on Technology Enterprises Ltd which has been engaged in a research and development

project related to modification in process related to the recharging of batteries of its own products.

This report further discuss about the Accounting standard necessary to be followed for preparation

of the financial statement.

The Australian Accounting Standards Board 138 is considered as a Commenwealth Government

Body which is governing all the accounting standards by laying down principles or standards

company, public sector enterprises or not profit business organisation has to comply. This report is

based on Technology Enterprises Ltd which has been engaged in a research and development

project related to modification in process related to the recharging of batteries of its own products.

This report further discuss about the Accounting standard necessary to be followed for preparation

of the financial statement.

Table of Contents

EXECUTIVE SUMMARY..................................................................................................................2

INTRODUCTION................................................................................................................................4

MAIN BODY.......................................................................................................................................4

1. Accounting standard AASB 138 & its application for formulation of financial statement.........4

2. AASB 138 restrictions impacting the comparability features of financial statements................6

3. Recommendation related to concern of investor interpretation of financial statements..............7

CONCLUSION....................................................................................................................................8

REFERENCES.....................................................................................................................................9

EXECUTIVE SUMMARY..................................................................................................................2

INTRODUCTION................................................................................................................................4

MAIN BODY.......................................................................................................................................4

1. Accounting standard AASB 138 & its application for formulation of financial statement.........4

2. AASB 138 restrictions impacting the comparability features of financial statements................6

3. Recommendation related to concern of investor interpretation of financial statements..............7

CONCLUSION....................................................................................................................................8

REFERENCES.....................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

AASB and IAS are the accounting standard which has to be followed by every business

organisation for preparation of its financial statements. The present report is based on case of

Technology Enterprises Ltd which has initiated a process of Research and Development in context

of bringing modification in the manner of recharging of batteries implanted in its own products and

goods. The report will show application use of AASB 138 in preparation of financial statements of

Technology Enterprises Ltd for the year ended 30 June 2018. Further it will streamline about the

AASB 138 rules and restrictions which results in reducing the comparability features of financial

statements. At last, it will recommend measures to be taken by Technology Enterprise Limited so as

to mitigate the problems related to interpretation of Financial Statements by the investors and other

stakeholders of the company.

MAIN BODY

1. Accounting standard AASB 138 & its application for formulation of financial statement.

The term Australian Accounting Standards Board (AASB) is a Commenwealth Government

Body which helps in regulating accounting standards by defining requirements which has to be

followed by every company, public sector entities as well as not for profit organisation on which it

is applicable. The Australian Accounting Standards Board helps in developments of standards,

procedures and methodology which assist companies in successful preparation of financial

statements for a particular period of time.

These accounting standards also helps in making proper and accurate interpretations which

defines the accounting mechanism to be adopted for completing of a particular transaction, activities

or events of the business that are creating impact on the preparation of the financial statements of

the company (Steenkamp and Steenkamp, 2016). All the information provided with the help of

financial statements as per the requirements of accounting standards provides transparency of

business operations and transaction taken place throughout the accounting year.

AASB 138 – The Australian Accounting Standards Board 138 provides the definition in relation

with Intangible Asset. This accounting standard defines:

1. How to make recognition of an Intangible Asset.

2. The way measurement of an Intangible Asset can be made

3. Provides requirements related to the disclosure of an Intangible Asset.

In case of Technology Enterprises Ltd, company has started in July 2017 a research and

development project with the aim of bringing modification in the process of charging of all the

batteries which are used in by its own company products. After successful completion of research

and development project in June 2018, company has applied for undertaking of Patent right for its

new modified design. Patent is considered as one of the intangible asset which provides a monopoly

AASB and IAS are the accounting standard which has to be followed by every business

organisation for preparation of its financial statements. The present report is based on case of

Technology Enterprises Ltd which has initiated a process of Research and Development in context

of bringing modification in the manner of recharging of batteries implanted in its own products and

goods. The report will show application use of AASB 138 in preparation of financial statements of

Technology Enterprises Ltd for the year ended 30 June 2018. Further it will streamline about the

AASB 138 rules and restrictions which results in reducing the comparability features of financial

statements. At last, it will recommend measures to be taken by Technology Enterprise Limited so as

to mitigate the problems related to interpretation of Financial Statements by the investors and other

stakeholders of the company.

MAIN BODY

1. Accounting standard AASB 138 & its application for formulation of financial statement.

The term Australian Accounting Standards Board (AASB) is a Commenwealth Government

Body which helps in regulating accounting standards by defining requirements which has to be

followed by every company, public sector entities as well as not for profit organisation on which it

is applicable. The Australian Accounting Standards Board helps in developments of standards,

procedures and methodology which assist companies in successful preparation of financial

statements for a particular period of time.

These accounting standards also helps in making proper and accurate interpretations which

defines the accounting mechanism to be adopted for completing of a particular transaction, activities

or events of the business that are creating impact on the preparation of the financial statements of

the company (Steenkamp and Steenkamp, 2016). All the information provided with the help of

financial statements as per the requirements of accounting standards provides transparency of

business operations and transaction taken place throughout the accounting year.

AASB 138 – The Australian Accounting Standards Board 138 provides the definition in relation

with Intangible Asset. This accounting standard defines:

1. How to make recognition of an Intangible Asset.

2. The way measurement of an Intangible Asset can be made

3. Provides requirements related to the disclosure of an Intangible Asset.

In case of Technology Enterprises Ltd, company has started in July 2017 a research and

development project with the aim of bringing modification in the process of charging of all the

batteries which are used in by its own company products. After successful completion of research

and development project in June 2018, company has applied for undertaking of Patent right for its

new modified design. Patent is considered as one of the intangible asset which provides a monopoly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

right in form of government authority or license of making, selling, utilising or developing the

invention made. Patent is provided by applying to the patent office under the applicable act.

As per AASB 138, Patent is considered as internally generated Intangible asset of which

recognition and measurement has to be done under the rules, regulations and norms as applicable

(Bond, Govendir and Wells, 2016). First intangible asset generated has to be identified that whether

such asset is meeting the criteria for recognition under the research phase and development phase.

1. Research Phase – If intangible asset is developing during research phase, then no

recognition will be provided. Patent is an intangible asset for which Technology Enterprise

Ltd has applied. All the expenditure incurred by Technology on conducting research will be

recognised as expense as and when it will be incurred properly

2. Development Phase - Intangible asset arising during conduct of development process, then

recognition will be provided for technical feasibility of completing intangible asset for

assessing its future use or sale. Also, the intention of completing intangible asset and its

ability to use or sell is meaningful. Recognition is provided when availability of financial,

technical and other resources for completing such development and its use and sell option

has been made. Ability of measuring the amount of expenditure taking place in case of

development of such intangible asset (Bodle and et.al., 2018).

Cost associated with an Intangible asset generated internally - Technology Enterprises Ltd

has incurred cost expenditure in conducting of research and development of project is as follows:

The cost of an Intangible asset which is generated internally during the research and development

process is calculated as taking sum of all the expenditure which are incurred from that date when

intangible asset has first meet the criteria of recognition. The cost calculation for Technology

Enterprises Ltd of its internally generated intangible asset i.e. Patent design includes all the cost

which are directly attributable as well as necessary for creating, producing and preparing the asset

so as to make it capable of operating in manner which is specified and required by the management

of the company.

Particulars Cost (in $)

Cost related to the time spent on searching and

evaluating alternative materials

100 000

Cost incurred in respect of time taken for designing

models, constructing and testing of prototypes

700 000

Cost of time incurred on imparting training and

maintenance of worker for new design

200 000

Estimated present value of design 4000 000

Fair Value of design 3000 000

invention made. Patent is provided by applying to the patent office under the applicable act.

As per AASB 138, Patent is considered as internally generated Intangible asset of which

recognition and measurement has to be done under the rules, regulations and norms as applicable

(Bond, Govendir and Wells, 2016). First intangible asset generated has to be identified that whether

such asset is meeting the criteria for recognition under the research phase and development phase.

1. Research Phase – If intangible asset is developing during research phase, then no

recognition will be provided. Patent is an intangible asset for which Technology Enterprise

Ltd has applied. All the expenditure incurred by Technology on conducting research will be

recognised as expense as and when it will be incurred properly

2. Development Phase - Intangible asset arising during conduct of development process, then

recognition will be provided for technical feasibility of completing intangible asset for

assessing its future use or sale. Also, the intention of completing intangible asset and its

ability to use or sell is meaningful. Recognition is provided when availability of financial,

technical and other resources for completing such development and its use and sell option

has been made. Ability of measuring the amount of expenditure taking place in case of

development of such intangible asset (Bodle and et.al., 2018).

Cost associated with an Intangible asset generated internally - Technology Enterprises Ltd

has incurred cost expenditure in conducting of research and development of project is as follows:

The cost of an Intangible asset which is generated internally during the research and development

process is calculated as taking sum of all the expenditure which are incurred from that date when

intangible asset has first meet the criteria of recognition. The cost calculation for Technology

Enterprises Ltd of its internally generated intangible asset i.e. Patent design includes all the cost

which are directly attributable as well as necessary for creating, producing and preparing the asset

so as to make it capable of operating in manner which is specified and required by the management

of the company.

Particulars Cost (in $)

Cost related to the time spent on searching and

evaluating alternative materials

100 000

Cost incurred in respect of time taken for designing

models, constructing and testing of prototypes

700 000

Cost of time incurred on imparting training and

maintenance of worker for new design

200 000

Estimated present value of design 4000 000

Fair Value of design 3000 000

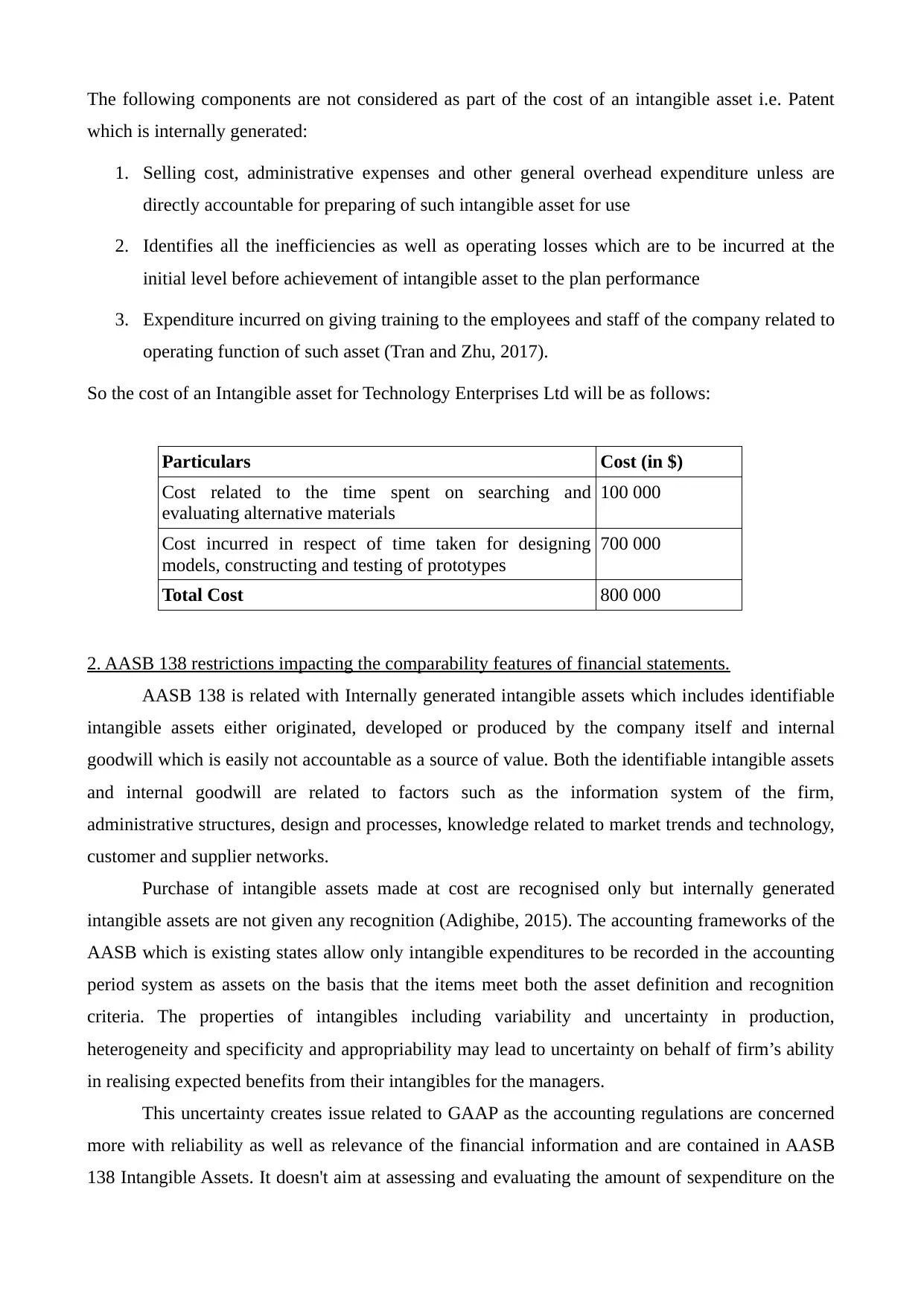

The following components are not considered as part of the cost of an intangible asset i.e. Patent

which is internally generated:

1. Selling cost, administrative expenses and other general overhead expenditure unless are

directly accountable for preparing of such intangible asset for use

2. Identifies all the inefficiencies as well as operating losses which are to be incurred at the

initial level before achievement of intangible asset to the plan performance

3. Expenditure incurred on giving training to the employees and staff of the company related to

operating function of such asset (Tran and Zhu, 2017).

So the cost of an Intangible asset for Technology Enterprises Ltd will be as follows:

Particulars Cost (in $)

Cost related to the time spent on searching and

evaluating alternative materials

100 000

Cost incurred in respect of time taken for designing

models, constructing and testing of prototypes

700 000

Total Cost 800 000

2. AASB 138 restrictions impacting the comparability features of financial statements.

AASB 138 is related with Internally generated intangible assets which includes identifiable

intangible assets either originated, developed or produced by the company itself and internal

goodwill which is easily not accountable as a source of value. Both the identifiable intangible assets

and internal goodwill are related to factors such as the information system of the firm,

administrative structures, design and processes, knowledge related to market trends and technology,

customer and supplier networks.

Purchase of intangible assets made at cost are recognised only but internally generated

intangible assets are not given any recognition (Adighibe, 2015). The accounting frameworks of the

AASB which is existing states allow only intangible expenditures to be recorded in the accounting

period system as assets on the basis that the items meet both the asset definition and recognition

criteria. The properties of intangibles including variability and uncertainty in production,

heterogeneity and specificity and appropriability may lead to uncertainty on behalf of firm’s ability

in realising expected benefits from their intangibles for the managers.

This uncertainty creates issue related to GAAP as the accounting regulations are concerned

more with reliability as well as relevance of the financial information and are contained in AASB

138 Intangible Assets. It doesn't aim at assessing and evaluating the amount of sexpenditure on the

which is internally generated:

1. Selling cost, administrative expenses and other general overhead expenditure unless are

directly accountable for preparing of such intangible asset for use

2. Identifies all the inefficiencies as well as operating losses which are to be incurred at the

initial level before achievement of intangible asset to the plan performance

3. Expenditure incurred on giving training to the employees and staff of the company related to

operating function of such asset (Tran and Zhu, 2017).

So the cost of an Intangible asset for Technology Enterprises Ltd will be as follows:

Particulars Cost (in $)

Cost related to the time spent on searching and

evaluating alternative materials

100 000

Cost incurred in respect of time taken for designing

models, constructing and testing of prototypes

700 000

Total Cost 800 000

2. AASB 138 restrictions impacting the comparability features of financial statements.

AASB 138 is related with Internally generated intangible assets which includes identifiable

intangible assets either originated, developed or produced by the company itself and internal

goodwill which is easily not accountable as a source of value. Both the identifiable intangible assets

and internal goodwill are related to factors such as the information system of the firm,

administrative structures, design and processes, knowledge related to market trends and technology,

customer and supplier networks.

Purchase of intangible assets made at cost are recognised only but internally generated

intangible assets are not given any recognition (Adighibe, 2015). The accounting frameworks of the

AASB which is existing states allow only intangible expenditures to be recorded in the accounting

period system as assets on the basis that the items meet both the asset definition and recognition

criteria. The properties of intangibles including variability and uncertainty in production,

heterogeneity and specificity and appropriability may lead to uncertainty on behalf of firm’s ability

in realising expected benefits from their intangibles for the managers.

This uncertainty creates issue related to GAAP as the accounting regulations are concerned

more with reliability as well as relevance of the financial information and are contained in AASB

138 Intangible Assets. It doesn't aim at assessing and evaluating the amount of sexpenditure on the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

intangible assets. Instead, objectives of standard is to allow recording of only those intangible assets

which is bearing a price from an exchange business transaction. Also, on the basis of mode of

acquisition accounting standard differentiates accounting methods for expenditure on intangibles

(Hussey and Ong, 2017). Items which has been excluded from recognition as an intangible asset

include brands names, mastheads, publishing titles, customer software etc. But these items can be

recognized as an intangible asset if purchase has been made.

The Intangible Assets consist of the three basic themes as follows:

1. All the expenditure made on purchased of intangibles (either separately acquired or as part

of an acquisition) which has met the definition of an intangible asset are deemed to be

recognisable as intangible assets.

2. All the other expenditure related to intangibles will come under the heading of internally

generated intangible asset provisions which are further classifiable only as either Research

or Development.

3. Out of expenditure incurred on the research and development, only development expenditure

meeting definition of intangible asset, recognition standards or rules plus the six tests in

AASB 138 Intangible Assets are recognisable as an intangible asset.

3. Recommendation related to concern of investor interpretation of financial statements.

Business transaction and activities taking place in an accounting year is recorded and

summarised in an accurate and correctly manner by every company in its financial statements every

year. Technology Enterprise Limited by considering following recommendation can mitigate its

concern related to the interpretation of the financial statements made by investors are as follows:

1. Technology Enterprise Limited should enhance the manner and method of communicating

of all the important and relevant information related to business in its financial statements by

determining the key themes and terminology. It will help the investors and other

stakeholders of the company in making better and clear understanding of financial

statements (Paruchuri and Misangyi, 2015).

2. By using the keywords, themes or terminology it provides an ease to company as well. With

the help of this terminology or themes, Technology Enterprise Limited can reordered its

disclosures and frame grouped related notes under headings such as “Debt and Equity”,

“Working Capital”, “Investments”, “Financial Risk Management ” etc. All these changes can

be made visible in the new structure of notes.

3. Any changes made during the accounting period in conducting of its business operations and

activities by the company, then it is necessary on behalf of Technology Enterprise Limited to

which is bearing a price from an exchange business transaction. Also, on the basis of mode of

acquisition accounting standard differentiates accounting methods for expenditure on intangibles

(Hussey and Ong, 2017). Items which has been excluded from recognition as an intangible asset

include brands names, mastheads, publishing titles, customer software etc. But these items can be

recognized as an intangible asset if purchase has been made.

The Intangible Assets consist of the three basic themes as follows:

1. All the expenditure made on purchased of intangibles (either separately acquired or as part

of an acquisition) which has met the definition of an intangible asset are deemed to be

recognisable as intangible assets.

2. All the other expenditure related to intangibles will come under the heading of internally

generated intangible asset provisions which are further classifiable only as either Research

or Development.

3. Out of expenditure incurred on the research and development, only development expenditure

meeting definition of intangible asset, recognition standards or rules plus the six tests in

AASB 138 Intangible Assets are recognisable as an intangible asset.

3. Recommendation related to concern of investor interpretation of financial statements.

Business transaction and activities taking place in an accounting year is recorded and

summarised in an accurate and correctly manner by every company in its financial statements every

year. Technology Enterprise Limited by considering following recommendation can mitigate its

concern related to the interpretation of the financial statements made by investors are as follows:

1. Technology Enterprise Limited should enhance the manner and method of communicating

of all the important and relevant information related to business in its financial statements by

determining the key themes and terminology. It will help the investors and other

stakeholders of the company in making better and clear understanding of financial

statements (Paruchuri and Misangyi, 2015).

2. By using the keywords, themes or terminology it provides an ease to company as well. With

the help of this terminology or themes, Technology Enterprise Limited can reordered its

disclosures and frame grouped related notes under headings such as “Debt and Equity”,

“Working Capital”, “Investments”, “Financial Risk Management ” etc. All these changes can

be made visible in the new structure of notes.

3. Any changes made during the accounting period in conducting of its business operations and

activities by the company, then it is necessary on behalf of Technology Enterprise Limited to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

highlight all the relevant matters and information. Also, communicating the same relevant

information to the investors and stakeholders in a clear and concise manner should be done.

4. For better interpretation of financial statement by the investor of Technology Enterprise

Limited, it is good on behalf of company to make description of all the significant and

necessary accounting policies, procedures, estimates and judgements made in a specific

note.

5. It is better recommended to the management of Technology Enterprise Limited to take into

consideration both the quantitative and qualitative factors when determining whether the

nature of information is material or relevant and should become part of financial statement

or not (Brazel and et.al., 2015).

6. Technology Enterprise Limited should covers all the information and matters of relevant and

material importance in its books of accounts and financials, of which the investors and other

stakeholders such as creditors, government, competitors can find important in their decision

making process.

7. The financial statement, books of accounts of the relevant accounting year should be

prepared by complying with all the requisite business laws, rules and provisions as specified

by the Company Act so as to reduce the chance of error which can be occurred while

recording of business transaction.

CONCLUSION

From the above report it has been concluded that, AASB 138 is a term which basically deals with

the Intangible Assets of the company. The AASB 138 is an accounting standard which helps

Technology Enterprises Limited in providing recognition to its intangible asset in form of patent

which has been developed during the research and development process conducted. Also, the report

has made disclosures related to the issues faced by the investors while making interpretation of

financial statements of the company because of unclear concept and non disclosure of material

information about the company. Further, report has defined measures which has help the company

in mitigating all the risk associated with the investor's interpretation and understanding. Technology

Enterprises Limited should focus on preparation of its financial statements in an accurate and

correct manner which contains the every detail of company which is crucial from the investor

points. It is very important from the investor perspective of Technology Enterprise Limited to

consider both the qualitative as well as quantitative factors while preparing the financial statements.

information to the investors and stakeholders in a clear and concise manner should be done.

4. For better interpretation of financial statement by the investor of Technology Enterprise

Limited, it is good on behalf of company to make description of all the significant and

necessary accounting policies, procedures, estimates and judgements made in a specific

note.

5. It is better recommended to the management of Technology Enterprise Limited to take into

consideration both the quantitative and qualitative factors when determining whether the

nature of information is material or relevant and should become part of financial statement

or not (Brazel and et.al., 2015).

6. Technology Enterprise Limited should covers all the information and matters of relevant and

material importance in its books of accounts and financials, of which the investors and other

stakeholders such as creditors, government, competitors can find important in their decision

making process.

7. The financial statement, books of accounts of the relevant accounting year should be

prepared by complying with all the requisite business laws, rules and provisions as specified

by the Company Act so as to reduce the chance of error which can be occurred while

recording of business transaction.

CONCLUSION

From the above report it has been concluded that, AASB 138 is a term which basically deals with

the Intangible Assets of the company. The AASB 138 is an accounting standard which helps

Technology Enterprises Limited in providing recognition to its intangible asset in form of patent

which has been developed during the research and development process conducted. Also, the report

has made disclosures related to the issues faced by the investors while making interpretation of

financial statements of the company because of unclear concept and non disclosure of material

information about the company. Further, report has defined measures which has help the company

in mitigating all the risk associated with the investor's interpretation and understanding. Technology

Enterprises Limited should focus on preparation of its financial statements in an accurate and

correct manner which contains the every detail of company which is crucial from the investor

points. It is very important from the investor perspective of Technology Enterprise Limited to

consider both the qualitative as well as quantitative factors while preparing the financial statements.

REFERENCES

Books and Journals

Adighibe, C. N., 2015. Public private partnership infrastructure delivery: benefits and costs for

society (Doctoral dissertation, Queensland University of Technology).

Bodle, K. and et.al., 2018. Critical success factors in managing sustainable indigenous businesses in

Australia. Pacific Accounting Review. 30(1). pp.35-51.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairment decisions by

Australian firms and whether this was impacted by AASB 136.

Brazel, J. F. and et.al., 2015. Understanding investor perceptions of financial statement fraud and

their use of red flags: Evidence from the field. Review of Accounting Studies. 20(4). pp.1373-

1406.

Hussey, R. and Ong, A., 2017. Corporate Financial Reporting. Macmillan International Higher

Education.

Paruchuri, S. and Misangyi, V. F., 2015. Investor perceptions of financial misconduct: The

heterogeneous contamination of bystander firms. Academy of Management Journal. 58(1).

pp.169-194.

Steenkamp, N. and Steenkamp, S., 2016. AASB 138: catalyst for managerial decisions reducing

R&D spending?. Journal of Financial Reporting and Accounting. 14(1). pp.116-130.

Tran, A. and Zhu, Y. H., 2017. The impact of adopting IFRS on corporate ETR and book-tax income

gap. Austl. Tax F. 32. p.757.

Online

AASB 138. 2019. [Online]. Available through: <https://legalvision.com.au/aasb-138-intangible-

assets-summary-for-businesses/>.

Revenue recognition principle. 2018. [Online]. Available through:

<https://www.accountingtools.com/articles/2017/5/15/the-revenue-recognition-principle>.

Books and Journals

Adighibe, C. N., 2015. Public private partnership infrastructure delivery: benefits and costs for

society (Doctoral dissertation, Queensland University of Technology).

Bodle, K. and et.al., 2018. Critical success factors in managing sustainable indigenous businesses in

Australia. Pacific Accounting Review. 30(1). pp.35-51.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairment decisions by

Australian firms and whether this was impacted by AASB 136.

Brazel, J. F. and et.al., 2015. Understanding investor perceptions of financial statement fraud and

their use of red flags: Evidence from the field. Review of Accounting Studies. 20(4). pp.1373-

1406.

Hussey, R. and Ong, A., 2017. Corporate Financial Reporting. Macmillan International Higher

Education.

Paruchuri, S. and Misangyi, V. F., 2015. Investor perceptions of financial misconduct: The

heterogeneous contamination of bystander firms. Academy of Management Journal. 58(1).

pp.169-194.

Steenkamp, N. and Steenkamp, S., 2016. AASB 138: catalyst for managerial decisions reducing

R&D spending?. Journal of Financial Reporting and Accounting. 14(1). pp.116-130.

Tran, A. and Zhu, Y. H., 2017. The impact of adopting IFRS on corporate ETR and book-tax income

gap. Austl. Tax F. 32. p.757.

Online

AASB 138. 2019. [Online]. Available through: <https://legalvision.com.au/aasb-138-intangible-

assets-summary-for-businesses/>.

Revenue recognition principle. 2018. [Online]. Available through:

<https://www.accountingtools.com/articles/2017/5/15/the-revenue-recognition-principle>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.