Technology Enterprises Ltd: Intangible Assets and Financial Statements

VerifiedAdded on 2020/10/23

|9

|2417

|191

Report

AI Summary

This report examines Technology Enterprises Ltd's accounting practices concerning a new battery design project. It analyzes the application of AASB 138 and IAS 38 to the company's intangible assets, including research and development costs. The report details how the project should be accounted for in the financial statements, specifically focusing on the treatment of expenses and the valuation of the new design. It also explores the extent to which the rules and regulations of AASB 138 and IAS 38 may impact the comparability of financial statements. Furthermore, the report provides recommendations to the CEO of Technology Enterprises Ltd. on mitigating concerns regarding investor interpretation of the financial information, suggesting the use of the efficient market hypothesis to aid stakeholders in their analysis. The report highlights the importance of complying with accounting standards for accurate and transparent financial reporting.

Research Individual

Project

Project

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Present report is based upon a company Technology Enterprises Ltd. which is planning to

replace its design of charging batteries. Research and development activities are conducted by

organisation and accountants does not have any idea of the way in which information should be

recorded in financial accounts. For this purpose they have analysed different accounting

standards including AASB 138 and IAS 38. Recommendation regarding interpreting information

to investors is also provided to Technology Enterprises Ltd. in which CEO is recommended to

follow AASB 138 and use efficient market hypothesis.

Present report is based upon a company Technology Enterprises Ltd. which is planning to

replace its design of charging batteries. Research and development activities are conducted by

organisation and accountants does not have any idea of the way in which information should be

recorded in financial accounts. For this purpose they have analysed different accounting

standards including AASB 138 and IAS 38. Recommendation regarding interpreting information

to investors is also provided to Technology Enterprises Ltd. in which CEO is recommended to

follow AASB 138 and use efficient market hypothesis.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Way in which project should be accounted in financial statements for year ended 30 June

2018..............................................................................................................................................1

2. Extent where rules and regulations in AASB 138/ IAS 38 may reduce comparability of

financial statements......................................................................................................................4

3. Recommendation to the CEO regarding the way in which organisation can mitigate its

concern regarding investor's interpretation of information..........................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Way in which project should be accounted in financial statements for year ended 30 June

2018..............................................................................................................................................1

2. Extent where rules and regulations in AASB 138/ IAS 38 may reduce comparability of

financial statements......................................................................................................................4

3. Recommendation to the CEO regarding the way in which organisation can mitigate its

concern regarding investor's interpretation of information..........................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

All the business entities have some assets which could not be touched and all of them are

known as intangible assets. It is vital for companies to follow appropriate accounting standards

while trying to record them in the books or financial statements. If companies are not able to

comply with all of them then it can result negatively or legal authorities may take strict actions

against enterprise (Hussey and Ong, 2017). Organisation which is selected for this report is

technology enterprises Ltd which is a listed company and planning to modify all its products.

This assignment covers various topics such as they way in which a new project is being

accounted in final accounts, extent to which rules or restrictions in AASB 138/ IAS 38 may

reduce comparability of financial statements etc. Apart from this, recommendation to the CEO of

the company is also provided regarding interpretation of the information reported in financial

statements.

MAIN BODY

1. Way in which project should be accounted in financial statements for year ended 30 June 2018

An organisation named Technology Enterprises Ltd. which is listed on ASX (Australian

Stock Exchange) commenced a research and development activity in mid of year 2017 for the

purpose of modifying methods of itself which were used by it to change batteries used in

business projects. The whole project was completed in mid of 2018 and top executives applied a

patent for the new design. It has been planned by the entity to modify all the products in next two

years and incorporate this plan in financial budget. It has been analysed that the new design will

provide economic benefits to the company in next ten years (Sugiyama and Islam, 2016).

Accountants of the company do not have any idea of the way in which all the expenses should be

accounted which are related to the new project. From the time sheet of engineers it various

expenses are identified which are as followed:

$100000 for the time which is being spent by engineers to search and evaluate alternative

materials.

$700000 for time which is being spend by them on designing models, constructing and

testing prototypes.

$200000 for the time which is spent by engineers to train maintenance workers to use

new design to change batteries.

1

All the business entities have some assets which could not be touched and all of them are

known as intangible assets. It is vital for companies to follow appropriate accounting standards

while trying to record them in the books or financial statements. If companies are not able to

comply with all of them then it can result negatively or legal authorities may take strict actions

against enterprise (Hussey and Ong, 2017). Organisation which is selected for this report is

technology enterprises Ltd which is a listed company and planning to modify all its products.

This assignment covers various topics such as they way in which a new project is being

accounted in final accounts, extent to which rules or restrictions in AASB 138/ IAS 38 may

reduce comparability of financial statements etc. Apart from this, recommendation to the CEO of

the company is also provided regarding interpretation of the information reported in financial

statements.

MAIN BODY

1. Way in which project should be accounted in financial statements for year ended 30 June 2018

An organisation named Technology Enterprises Ltd. which is listed on ASX (Australian

Stock Exchange) commenced a research and development activity in mid of year 2017 for the

purpose of modifying methods of itself which were used by it to change batteries used in

business projects. The whole project was completed in mid of 2018 and top executives applied a

patent for the new design. It has been planned by the entity to modify all the products in next two

years and incorporate this plan in financial budget. It has been analysed that the new design will

provide economic benefits to the company in next ten years (Sugiyama and Islam, 2016).

Accountants of the company do not have any idea of the way in which all the expenses should be

accounted which are related to the new project. From the time sheet of engineers it various

expenses are identified which are as followed:

$100000 for the time which is being spent by engineers to search and evaluate alternative

materials.

$700000 for time which is being spend by them on designing models, constructing and

testing prototypes.

$200000 for the time which is spent by engineers to train maintenance workers to use

new design to change batteries.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

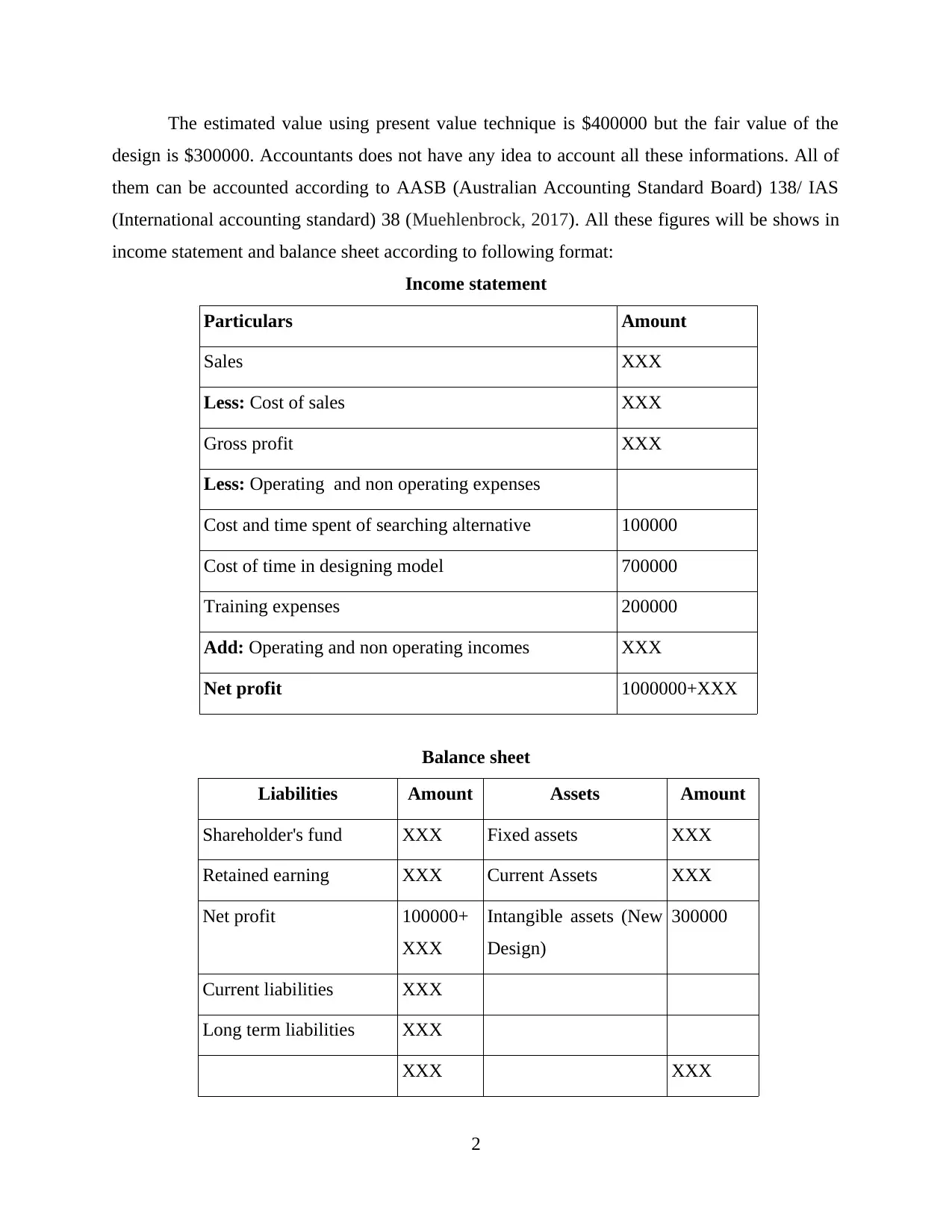

The estimated value using present value technique is $400000 but the fair value of the

design is $300000. Accountants does not have any idea to account all these informations. All of

them can be accounted according to AASB (Australian Accounting Standard Board) 138/ IAS

(International accounting standard) 38 (Muehlenbrock, 2017). All these figures will be shows in

income statement and balance sheet according to following format:

Income statement

Particulars Amount

Sales XXX

Less: Cost of sales XXX

Gross profit XXX

Less: Operating and non operating expenses

Cost and time spent of searching alternative 100000

Cost of time in designing model 700000

Training expenses 200000

Add: Operating and non operating incomes XXX

Net profit 1000000+XXX

Balance sheet

Liabilities Amount Assets Amount

Shareholder's fund XXX Fixed assets XXX

Retained earning XXX Current Assets XXX

Net profit 100000+

XXX

Intangible assets (New

Design)

300000

Current liabilities XXX

Long term liabilities XXX

XXX XXX

2

design is $300000. Accountants does not have any idea to account all these informations. All of

them can be accounted according to AASB (Australian Accounting Standard Board) 138/ IAS

(International accounting standard) 38 (Muehlenbrock, 2017). All these figures will be shows in

income statement and balance sheet according to following format:

Income statement

Particulars Amount

Sales XXX

Less: Cost of sales XXX

Gross profit XXX

Less: Operating and non operating expenses

Cost and time spent of searching alternative 100000

Cost of time in designing model 700000

Training expenses 200000

Add: Operating and non operating incomes XXX

Net profit 1000000+XXX

Balance sheet

Liabilities Amount Assets Amount

Shareholder's fund XXX Fixed assets XXX

Retained earning XXX Current Assets XXX

Net profit 100000+

XXX

Intangible assets (New

Design)

300000

Current liabilities XXX

Long term liabilities XXX

XXX XXX

2

According to accounting standards all the expenses which takes place while working on a

new business project are recorded in income statement as all of them are treated as operating

expenses. So the expenses which are costing $100000, $700000 and $200000 are recorded in

income statement of the company. All of them are deducted from gross profit in order to

calculate net income. The amount which is being received as net profit is shown in balance sheet

and new design is recorded on the cost of $300000 which is fair value for it. According to AASB

138/ IAS 38 it is vital for companies to record intangible asset on fair price rather than present

value.

During preparation of various financial statements by companies various issues are faced by

them. This arises due to lack of information about rules and regulations that changes according to

time and introduce by different legal organisations as per the various conditions exist in market.

AASB were imposed by IASB to direct Australian organisations to keep all financial data in

final accounts in appropriate manner. AASB 138 deal with intangible assets of organisation.

Following are the requirements that should be consider an asset intangible in nature:

An organisation require to be a distinct one if it wants to treat an asset an intangible one.

Further that asset should be originated from variety of written agreement.

Assets that can be plumbed in monetary terms cannot be considered as intangible assets

as organisations cannot buy it from any other place (Negri, 2016).

That asset require to not have any tangible characteristic in which organisation is required

to make sure that asset is not touchable.

Proper control is require in order to declare a asset an intangible one. If an enterprise take

decision related with use of its design and logo then company has to control its asset that

can be treated as an intangible one.

If company can sale that asset in future and can acquire some economic benefits then it

fulfil all the requirements of AASB (Requirements of AASB 138, 2019).

All these are the major requirements that are fulfilled by Technology Enterprise Ltd. for new

design of its batteries that are used in its various projects. Present value of design is $400000 and

fair value is $300000 and if company achieve success in sale the same that company will acquire

the economic benefits of $100000. Company has adequate control over its asset so it can sell it to

other parties. After purchase of that buyer can do necessary modifications in the design as per the

3

new business project are recorded in income statement as all of them are treated as operating

expenses. So the expenses which are costing $100000, $700000 and $200000 are recorded in

income statement of the company. All of them are deducted from gross profit in order to

calculate net income. The amount which is being received as net profit is shown in balance sheet

and new design is recorded on the cost of $300000 which is fair value for it. According to AASB

138/ IAS 38 it is vital for companies to record intangible asset on fair price rather than present

value.

During preparation of various financial statements by companies various issues are faced by

them. This arises due to lack of information about rules and regulations that changes according to

time and introduce by different legal organisations as per the various conditions exist in market.

AASB were imposed by IASB to direct Australian organisations to keep all financial data in

final accounts in appropriate manner. AASB 138 deal with intangible assets of organisation.

Following are the requirements that should be consider an asset intangible in nature:

An organisation require to be a distinct one if it wants to treat an asset an intangible one.

Further that asset should be originated from variety of written agreement.

Assets that can be plumbed in monetary terms cannot be considered as intangible assets

as organisations cannot buy it from any other place (Negri, 2016).

That asset require to not have any tangible characteristic in which organisation is required

to make sure that asset is not touchable.

Proper control is require in order to declare a asset an intangible one. If an enterprise take

decision related with use of its design and logo then company has to control its asset that

can be treated as an intangible one.

If company can sale that asset in future and can acquire some economic benefits then it

fulfil all the requirements of AASB (Requirements of AASB 138, 2019).

All these are the major requirements that are fulfilled by Technology Enterprise Ltd. for new

design of its batteries that are used in its various projects. Present value of design is $400000 and

fair value is $300000 and if company achieve success in sale the same that company will acquire

the economic benefits of $100000. Company has adequate control over its asset so it can sell it to

other parties. After purchase of that buyer can do necessary modifications in the design as per the

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

needs and requirements. This is one of the main reason why new design is come under the

category of tangible assets.

2. Extent where rules and regulations in AASB 138/ IAS 38 may reduce comparability of

financial statements

AASB 138 stands for The Australian Accounting Standard Board that is commenced in year

2004 on 15th July under 334 amendment of Corporation act 2001. One of the main motive of this

accounting treatment is to reflect the accounting treatment for an enterprise to all its intangible

assets as these are not deal with any other standard. Therefore, it support a company to identify

all its intangible assets but under one condition which is when some specific conditions are

fulfilled. Further, it assist companies in measure the amount of intangible assets and also direct

how to disclose the same (Nobes, 2014). but in context to financial statement, this standard doe

not apply to following:

The assets which are related to deferred tax then it will not be able to apply AASB under

AASB 112.

Further assets that rise from workers benefits are also not covered in this according to

AASB 119 which related to employee benefits.

All the leases which are fulfilling requirements of AASB 117 which is related to lease.

So it is essential for organisations, to apply AASB 138 standard with all their reporting

periods that starts from 1st January 2009 and after 1st January 2005 (AASB 138, 2019).

From all the above points it has been analysed that AASB leaves impact upon

organisation's comparability of financial statements. For all the Australian companies it is vital to

comply with AASB while recording information in final accounts as it help to analyse nature of

different assets. As AASB 138 help to record intangible assets if company pass criteria of the

standard. If company is following all the standards than it can help to enhance compatibility

because the recorded data will be accurate, transparent and relevant then it brings comparability

in the statements (Zhang, 2018).

3. Recommendation to the CEO regarding the way in which organisation can mitigate its concern

regarding investor's interpretation of information

According to CEO of Technology Enterprises Ltd. can show the value of new design

which is $400000 in balance sheet and can show profits of $300000. But it is not legal according

4

category of tangible assets.

2. Extent where rules and regulations in AASB 138/ IAS 38 may reduce comparability of

financial statements

AASB 138 stands for The Australian Accounting Standard Board that is commenced in year

2004 on 15th July under 334 amendment of Corporation act 2001. One of the main motive of this

accounting treatment is to reflect the accounting treatment for an enterprise to all its intangible

assets as these are not deal with any other standard. Therefore, it support a company to identify

all its intangible assets but under one condition which is when some specific conditions are

fulfilled. Further, it assist companies in measure the amount of intangible assets and also direct

how to disclose the same (Nobes, 2014). but in context to financial statement, this standard doe

not apply to following:

The assets which are related to deferred tax then it will not be able to apply AASB under

AASB 112.

Further assets that rise from workers benefits are also not covered in this according to

AASB 119 which related to employee benefits.

All the leases which are fulfilling requirements of AASB 117 which is related to lease.

So it is essential for organisations, to apply AASB 138 standard with all their reporting

periods that starts from 1st January 2009 and after 1st January 2005 (AASB 138, 2019).

From all the above points it has been analysed that AASB leaves impact upon

organisation's comparability of financial statements. For all the Australian companies it is vital to

comply with AASB while recording information in final accounts as it help to analyse nature of

different assets. As AASB 138 help to record intangible assets if company pass criteria of the

standard. If company is following all the standards than it can help to enhance compatibility

because the recorded data will be accurate, transparent and relevant then it brings comparability

in the statements (Zhang, 2018).

3. Recommendation to the CEO regarding the way in which organisation can mitigate its concern

regarding investor's interpretation of information

According to CEO of Technology Enterprises Ltd. can show the value of new design

which is $400000 in balance sheet and can show profits of $300000. But it is not legal according

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to accounting standards as AASB 138 indicate that all the intangible assets should be recorded in

final accounts on their fair value. It can help to analyse and measure the economic benefit which

is being raised by the company in a specific time period. It is essential for enterprise to measure

all its assets initially when their actual nature is recognised according of Australian and

International standards imposed by IASB (International Accounting Standard Board). According

to AASB it is very important for Technology Enterprises Ltd. to show detailed information

regarding all the intangible assets in order to meet requirements of AASB 138. If it is not

possible for Technology Enterprises Ltd. to disclose elaborated data regarding its assets then it

can result in strict actions of legal parties, decreased profits and increased taxation for company.

As main issue of CEO is to mitigate the concern to interpret information of organisation which is

recorded in financial statements (Riccardi, 2016). This challenge can be resolved with the help of

Efficient market hypothesis which is a type of investment theory that helps to show detailed

information regarding share price of company. With the help of it stakeholders can estimate

possible return which could be acquired them in future by making investment decision. If this

hypothesis is formulated by the company then it will resolve problem of CEO of interpreting

information with investors as it can guide them to analyse all the data by themselves. When they

find any issue in performance of Technology Enterprises Ltd. then invested money can be

withdrawn by them in order to ignore situation of loss of funding.

Recommendation: As CEO of the company has a concern to show financial information

to investors. In order to decrease the concern following recommendations are provided to CEO:

CEO should enhance information regarding accounting standards that are required to be

complied in order to show accurate financial statements to the investors.

In order to mitigate concern about interpretation to investors efficient market hypothesis

could be formed by the company which will be beneficial for them to analyse business's

information by themselves (Stadler and Nobes, 2018).

CONCLUSION

From the above given information, it can be summarised that legal organisation form

various different type of rules and regulations and every organisation remain responsible to

comply with those in order to carry all commercial activities in proper and adequate manner.

AASB 138 is one of them and this cover various amendments made by IASB in IAS 38. This

mainly deals with treatment of intangible assets hold by different organisation operate in market.

5

final accounts on their fair value. It can help to analyse and measure the economic benefit which

is being raised by the company in a specific time period. It is essential for enterprise to measure

all its assets initially when their actual nature is recognised according of Australian and

International standards imposed by IASB (International Accounting Standard Board). According

to AASB it is very important for Technology Enterprises Ltd. to show detailed information

regarding all the intangible assets in order to meet requirements of AASB 138. If it is not

possible for Technology Enterprises Ltd. to disclose elaborated data regarding its assets then it

can result in strict actions of legal parties, decreased profits and increased taxation for company.

As main issue of CEO is to mitigate the concern to interpret information of organisation which is

recorded in financial statements (Riccardi, 2016). This challenge can be resolved with the help of

Efficient market hypothesis which is a type of investment theory that helps to show detailed

information regarding share price of company. With the help of it stakeholders can estimate

possible return which could be acquired them in future by making investment decision. If this

hypothesis is formulated by the company then it will resolve problem of CEO of interpreting

information with investors as it can guide them to analyse all the data by themselves. When they

find any issue in performance of Technology Enterprises Ltd. then invested money can be

withdrawn by them in order to ignore situation of loss of funding.

Recommendation: As CEO of the company has a concern to show financial information

to investors. In order to decrease the concern following recommendations are provided to CEO:

CEO should enhance information regarding accounting standards that are required to be

complied in order to show accurate financial statements to the investors.

In order to mitigate concern about interpretation to investors efficient market hypothesis

could be formed by the company which will be beneficial for them to analyse business's

information by themselves (Stadler and Nobes, 2018).

CONCLUSION

From the above given information, it can be summarised that legal organisation form

various different type of rules and regulations and every organisation remain responsible to

comply with those in order to carry all commercial activities in proper and adequate manner.

AASB 138 is one of them and this cover various amendments made by IASB in IAS 38. This

mainly deals with treatment of intangible assets hold by different organisation operate in market.

5

This direct them to fulfil all the requirements that are essential to consider an asset as an

intangible one. In case when organisations fail to comply with AASB 138 and other standards

then that enterprise is not allowed to record any asset under intangible asset.

6

intangible one. In case when organisations fail to comply with AASB 138 and other standards

then that enterprise is not allowed to record any asset under intangible asset.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.