ACCT20075: Auditing & Assurance Report for Technology One Company

VerifiedAdded on 2023/06/07

|11

|2272

|205

Report

AI Summary

This report provides an audit and assurance analysis of Technology One Company, focusing on materiality, analytical review, and audit procedures as per the ACCT20075 course requirements. It assesses the company's financial statements, including the statement of cash flow, and reviews the auditor's report, highlighting key financial ratios, business risks, and audit assertions. The analysis covers the company's revenue growth, business expansion strategies, and potential financial risks, such as high cash outflow from investing and financial activities. The report concludes that Technology One's financial performance is generally positive, but emphasizes the need for balanced financial leverage and harmonization of reporting frameworks. Desklib offers a wide array of similar solved assignments and past papers to aid students in their studies.

TEchnologey one (TNE) Company

Auditing reporting and assurance

Auditing and assurance

Name of the Author

University Name-

Auditing reporting and assurance

Auditing and assurance

Name of the Author

University Name-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.................................................................................................................................2

Answer to section-1...............................................................................................................................2

Answer to section- 2..............................................................................................................................3

Answer to section- 3..............................................................................................................................7

REVIEW OF STATEMENT OF CASH FLOW...............................................................................7

REVIEW OF AUDIT REPORT........................................................................................................8

Conclusion.............................................................................................................................................8

REFERENCES......................................................................................................................................9

1

INTRODUCTION.................................................................................................................................2

Answer to section-1...............................................................................................................................2

Answer to section- 2..............................................................................................................................3

Answer to section- 3..............................................................................................................................7

REVIEW OF STATEMENT OF CASH FLOW...............................................................................7

REVIEW OF AUDIT REPORT........................................................................................................8

Conclusion.............................................................................................................................................8

REFERENCES......................................................................................................................................9

1

INTRODUCTION

Auditing and assurance is the key aspect of strengthen the true and fair view of the

assets and liabilities recorded in the financial statements of company. The main objective of

the audit and assurance program is to increase the transparency of reported financial

statements of organization. In this report, different three sections have been answered by

undertaking the proper methods and auditing assertion test. The audit and assurance program

have been undertaken for the company Technology one which has been operating its business

on international level. In the starting Materiality concept have been explained after that

review of the financial statement of Technology one and audit assertion test have been

analyzed. Afterward, in the end, analysis of the cash flow statement, financial and non-

financial activities of the company have been taken into consideration to determine the

highest and lowest activity of the cash flow.

Answer to section-1

Materiality could be defined as evaluating the quantifiable financial data to identify

the internet risk such as misstatement, omission and errors in the prepared financial

statements of company. As per ASA 320 , the concept of materiality is discussed with

reference to the preparation and presentation of the financial report which analaysi the

ommmision and problems in the financial statements. In this regard, the misstatements are

considered to be material if they individually or in the aggregate impact the decision taken by

the users with regards to financial statements. Materiality in planning and performing audit

focuses on the auditor’s responsibilities to determine the materiality for the financial

statements. Each and every auditor while auditing the financial statement of company set the

materiality level to analysis the inherent risk and viability of the prepared financial

statements. This set materiality level is determined on the basis of performance materiality

concepts which emphasis upon the viability of the set parameters in the particular time

period. For instance, performance materiality may be fixed such as 1% of the revenue, 10%

of revenue, .5% of revenue and 5% to 10% of revenue. This will allow auditors to determine

the viability of the overall turnover shown in the financial statements while preparing the

audit report without any disclaimer. It is analyzed that there could other parameters as well

which could be used by auditors while setting the performance parameters such as net

income, gross profit and total turnover of company (Jelinek, 2015).

2

Auditing and assurance is the key aspect of strengthen the true and fair view of the

assets and liabilities recorded in the financial statements of company. The main objective of

the audit and assurance program is to increase the transparency of reported financial

statements of organization. In this report, different three sections have been answered by

undertaking the proper methods and auditing assertion test. The audit and assurance program

have been undertaken for the company Technology one which has been operating its business

on international level. In the starting Materiality concept have been explained after that

review of the financial statement of Technology one and audit assertion test have been

analyzed. Afterward, in the end, analysis of the cash flow statement, financial and non-

financial activities of the company have been taken into consideration to determine the

highest and lowest activity of the cash flow.

Answer to section-1

Materiality could be defined as evaluating the quantifiable financial data to identify

the internet risk such as misstatement, omission and errors in the prepared financial

statements of company. As per ASA 320 , the concept of materiality is discussed with

reference to the preparation and presentation of the financial report which analaysi the

ommmision and problems in the financial statements. In this regard, the misstatements are

considered to be material if they individually or in the aggregate impact the decision taken by

the users with regards to financial statements. Materiality in planning and performing audit

focuses on the auditor’s responsibilities to determine the materiality for the financial

statements. Each and every auditor while auditing the financial statement of company set the

materiality level to analysis the inherent risk and viability of the prepared financial

statements. This set materiality level is determined on the basis of performance materiality

concepts which emphasis upon the viability of the set parameters in the particular time

period. For instance, performance materiality may be fixed such as 1% of the revenue, 10%

of revenue, .5% of revenue and 5% to 10% of revenue. This will allow auditors to determine

the viability of the overall turnover shown in the financial statements while preparing the

audit report without any disclaimer. It is analyzed that there could other parameters as well

which could be used by auditors while setting the performance parameters such as net

income, gross profit and total turnover of company (Jelinek, 2015).

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

After analysing the annual report of company, it is analyzed that Technology one

company increased its revenue to AUD $ 271.61 million in 2017 which is 15% higher as

compared to last year data. However, the figured detailed given have been adjusted for the

tax computation. The overall turnover could be used to set up the materiality level which

could be between AUD 25 million to 30 million. The main disclosure made by the

Technology one company is related to its business expansion in other market segment and

diversified business functioning. It will allow organization to strengthen its overall sales. In

addition to this, merger strategy has also allowed company to increase its overall market

share in given time period (Mock, Ragothaman, & Srivastava, 2018).

Answer to section- 2

Audit and assurance process checks the viability of the financial statements and errors

and issues in the books of account of company. The preliminary analytical review is the

beginning stage which is adopted by the auditors reviews the reporting financial statements.

In ASA 450 , the auditors evaluate the effect of misstatements on the audit and the impact of

uncorrected misstatements on the financial statements.. As per ASA 1031It also influences

the discharge of accountability by the governing authority or the management As per the

ASA 300, it is analyzd that review of thefinanical statemetn by the auditros is very much

required to assess the risk asociated with the finanical statements. This analysis allows

auditros to identify the relation between the financial and non-finanical information

(Louwers, et al. 2015).

KEY RATIOS 2014 2015 2016 2017

CURRENT

RATIO

1.1 1.56 1.25 1.65

3

company increased its revenue to AUD $ 271.61 million in 2017 which is 15% higher as

compared to last year data. However, the figured detailed given have been adjusted for the

tax computation. The overall turnover could be used to set up the materiality level which

could be between AUD 25 million to 30 million. The main disclosure made by the

Technology one company is related to its business expansion in other market segment and

diversified business functioning. It will allow organization to strengthen its overall sales. In

addition to this, merger strategy has also allowed company to increase its overall market

share in given time period (Mock, Ragothaman, & Srivastava, 2018).

Answer to section- 2

Audit and assurance process checks the viability of the financial statements and errors

and issues in the books of account of company. The preliminary analytical review is the

beginning stage which is adopted by the auditors reviews the reporting financial statements.

In ASA 450 , the auditors evaluate the effect of misstatements on the audit and the impact of

uncorrected misstatements on the financial statements.. As per ASA 1031It also influences

the discharge of accountability by the governing authority or the management As per the

ASA 300, it is analyzd that review of thefinanical statemetn by the auditros is very much

required to assess the risk asociated with the finanical statements. This analysis allows

auditros to identify the relation between the financial and non-finanical information

(Louwers, et al. 2015).

KEY RATIOS 2014 2015 2016 2017

CURRENT

RATIO

1.1 1.56 1.25 1.65

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

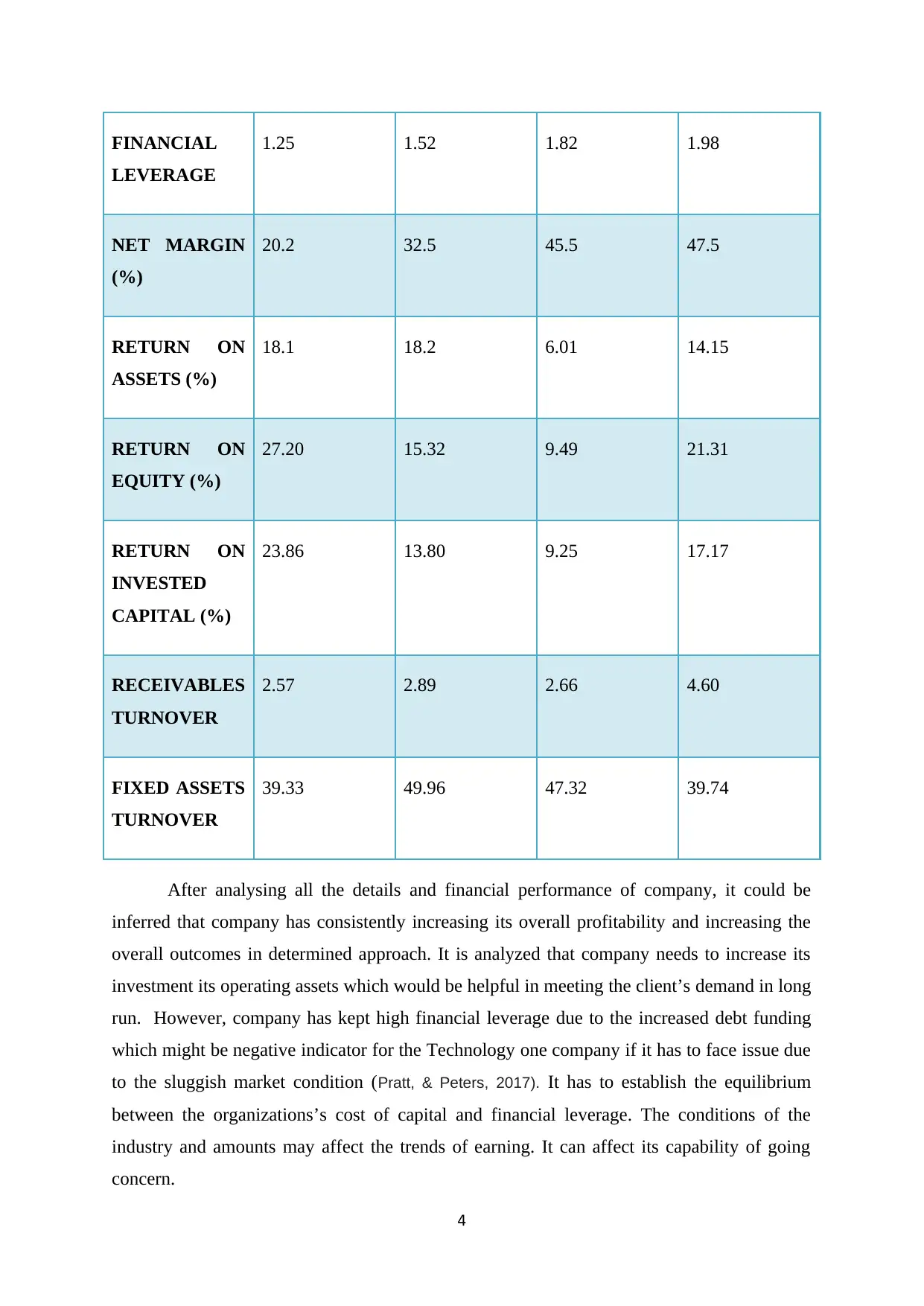

FINANCIAL

LEVERAGE

1.25 1.52 1.82 1.98

NET MARGIN

(%)

20.2 32.5 45.5 47.5

RETURN ON

ASSETS (%)

18.1 18.2 6.01 14.15

RETURN ON

EQUITY (%)

27.20 15.32 9.49 21.31

RETURN ON

INVESTED

CAPITAL (%)

23.86 13.80 9.25 17.17

RECEIVABLES

TURNOVER

2.57 2.89 2.66 4.60

FIXED ASSETS

TURNOVER

39.33 49.96 47.32 39.74

After analysing all the details and financial performance of company, it could be

inferred that company has consistently increasing its overall profitability and increasing the

overall outcomes in determined approach. It is analyzed that company needs to increase its

investment its operating assets which would be helpful in meeting the client’s demand in long

run. However, company has kept high financial leverage due to the increased debt funding

which might be negative indicator for the Technology one company if it has to face issue due

to the sluggish market condition (Pratt, & Peters, 2017). It has to establish the equilibrium

between the organizations’s cost of capital and financial leverage. The conditions of the

industry and amounts may affect the trends of earning. It can affect its capability of going

concern.

4

LEVERAGE

1.25 1.52 1.82 1.98

NET MARGIN

(%)

20.2 32.5 45.5 47.5

RETURN ON

ASSETS (%)

18.1 18.2 6.01 14.15

RETURN ON

EQUITY (%)

27.20 15.32 9.49 21.31

RETURN ON

INVESTED

CAPITAL (%)

23.86 13.80 9.25 17.17

RECEIVABLES

TURNOVER

2.57 2.89 2.66 4.60

FIXED ASSETS

TURNOVER

39.33 49.96 47.32 39.74

After analysing all the details and financial performance of company, it could be

inferred that company has consistently increasing its overall profitability and increasing the

overall outcomes in determined approach. It is analyzed that company needs to increase its

investment its operating assets which would be helpful in meeting the client’s demand in long

run. However, company has kept high financial leverage due to the increased debt funding

which might be negative indicator for the Technology one company if it has to face issue due

to the sluggish market condition (Pratt, & Peters, 2017). It has to establish the equilibrium

between the organizations’s cost of capital and financial leverage. The conditions of the

industry and amounts may affect the trends of earning. It can affect its capability of going

concern.

4

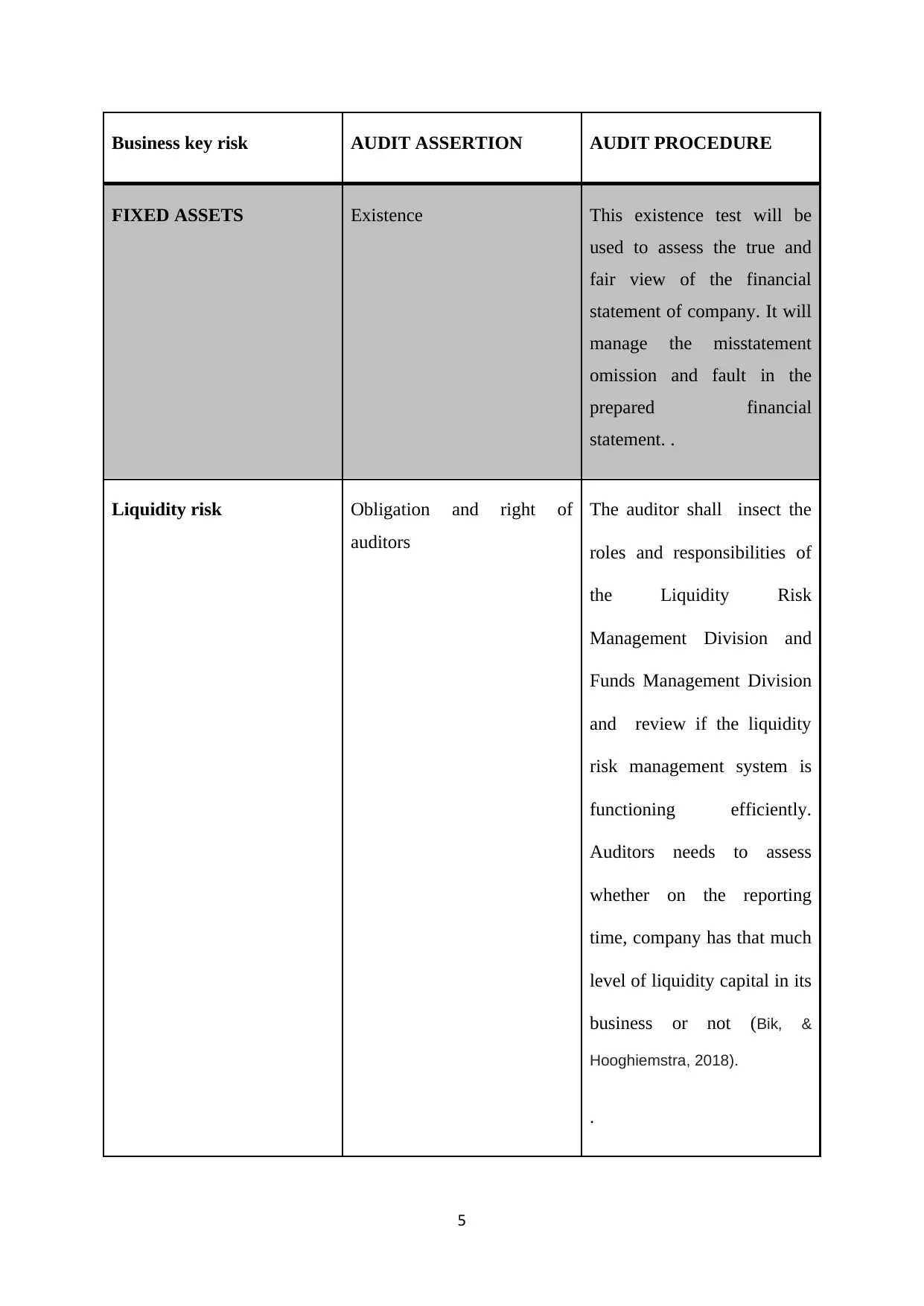

Business key risk AUDIT ASSERTION AUDIT PROCEDURE

FIXED ASSETS Existence This existence test will be

used to assess the true and

fair view of the financial

statement of company. It will

manage the misstatement

omission and fault in the

prepared financial

statement. .

Liquidity risk Obligation and right of

auditors

The auditor shall insect the

roles and responsibilities of

the Liquidity Risk

Management Division and

Funds Management Division

and review if the liquidity

risk management system is

functioning efficiently.

Auditors needs to assess

whether on the reporting

time, company has that much

level of liquidity capital in its

business or not (Bik, &

Hooghiemstra, 2018).

.

5

FIXED ASSETS Existence This existence test will be

used to assess the true and

fair view of the financial

statement of company. It will

manage the misstatement

omission and fault in the

prepared financial

statement. .

Liquidity risk Obligation and right of

auditors

The auditor shall insect the

roles and responsibilities of

the Liquidity Risk

Management Division and

Funds Management Division

and review if the liquidity

risk management system is

functioning efficiently.

Auditors needs to assess

whether on the reporting

time, company has that much

level of liquidity capital in its

business or not (Bik, &

Hooghiemstra, 2018).

.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

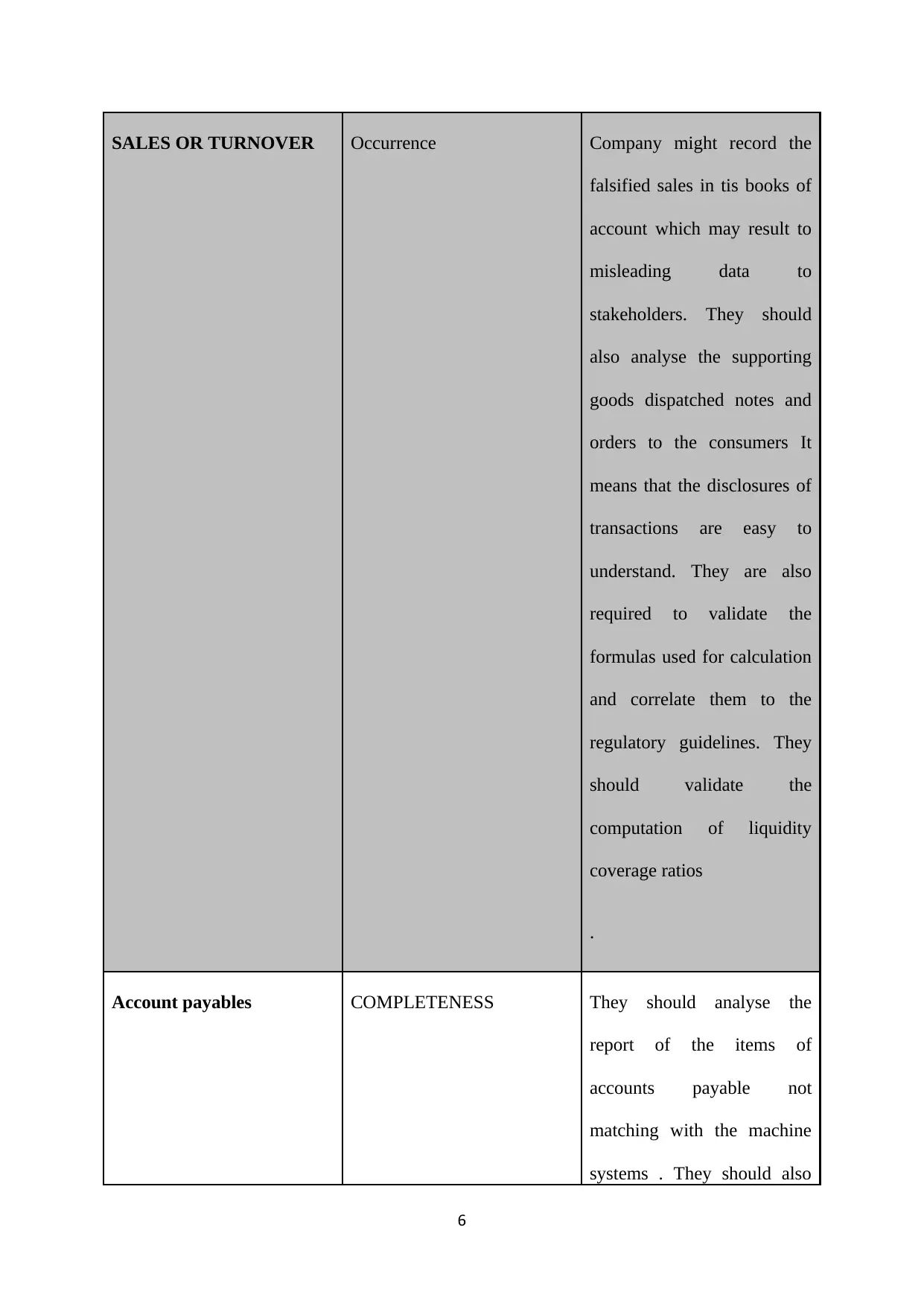

SALES OR TURNOVER Occurrence Company might record the

falsified sales in tis books of

account which may result to

misleading data to

stakeholders. They should

also analyse the supporting

goods dispatched notes and

orders to the consumers It

means that the disclosures of

transactions are easy to

understand. They are also

required to validate the

formulas used for calculation

and correlate them to the

regulatory guidelines. They

should validate the

computation of liquidity

coverage ratios

.

Account payables COMPLETENESS They should analyse the

report of the items of

accounts payable not

matching with the machine

systems . They should also

6

falsified sales in tis books of

account which may result to

misleading data to

stakeholders. They should

also analyse the supporting

goods dispatched notes and

orders to the consumers It

means that the disclosures of

transactions are easy to

understand. They are also

required to validate the

formulas used for calculation

and correlate them to the

regulatory guidelines. They

should validate the

computation of liquidity

coverage ratios

.

Account payables COMPLETENESS They should analyse the

report of the items of

accounts payable not

matching with the machine

systems . They should also

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

use the software to prepare

the role of debit to account

payable other than the

payment made to the

vendors. The role of auditors,

in this case, is to assess the

risks in the acquisition cycle.

They should focus on

payments made to the

vendors and review the files

of accounts payable

( Fuhrmann, Ott, Looks, &

Guenther, 2017).

Answer to section- 3

REVIEW OF STATEMENT OF CASH FLOW

The cash flow statement of Technology one company has reflected that company has

high cash outflow from its investing and financial activities. It is analyzed that investing

activities of the cash flow statement of company reflects AUD $ 113 million of cash outflow.

The cash outflow from the financial activities of company reflects cash outflow of AUD $

171 million. However, there are several primary financial activities of the Technology one

company such as sale or maturity of investments, proceeds from the convertible bonds, and

proceeds from the issue of shares and income from the consolidated funding. On the other

hand, primary cash payment of company would include purchase of property, net cash paid,

payment to shareholder to dividend and rest payment to stakeholders for the investment

purpose. There are other non-cash financial activity which needs to be managed such as

7

the role of debit to account

payable other than the

payment made to the

vendors. The role of auditors,

in this case, is to assess the

risks in the acquisition cycle.

They should focus on

payments made to the

vendors and review the files

of accounts payable

( Fuhrmann, Ott, Looks, &

Guenther, 2017).

Answer to section- 3

REVIEW OF STATEMENT OF CASH FLOW

The cash flow statement of Technology one company has reflected that company has

high cash outflow from its investing and financial activities. It is analyzed that investing

activities of the cash flow statement of company reflects AUD $ 113 million of cash outflow.

The cash outflow from the financial activities of company reflects cash outflow of AUD $

171 million. However, there are several primary financial activities of the Technology one

company such as sale or maturity of investments, proceeds from the convertible bonds, and

proceeds from the issue of shares and income from the consolidated funding. On the other

hand, primary cash payment of company would include purchase of property, net cash paid,

payment to shareholder to dividend and rest payment to stakeholders for the investment

purpose. There are other non-cash financial activity which needs to be managed such as

7

investing in buying new assets, convertible bonds and hedge funding investment (Mala, &

Chand, 2015).

The main risk company is facing is related to going concern if it failed to manage the

proper flow of cash funding for its business. The financial activities of Technology one is

comparatively high which reflects that company might face issue related to increased cash

risk. The Auditors of company has also faced the issue related to the maternity level and cash

risk in its business.

The cash transactions in the cash flow statement of company include payment to

shareholders as dividend, issue of shares and payment for the investment. On the other hand,

non-cash transactions include depreciation, impairment loss and charge created on the assets

of company. This has shown that company might face issue related to the sustainable

business practice and may increase business risk which might negatively impact the business

growth of Technology Company (Legoria, Melendrez, & Reynolds, 2013).

REVIEW OF AUDIT REPORT

The opinion of the auditors for the financial statement of the Technology one company is

favourable. They centralize their visibility and policy setting regarding the risks of increasing

commodity price. Auditors of company have given in its report that it shall have counterparty

credit policies. Judgments regarding materiality are made in the context of surrounding

circumstances and they are influenced by the nature or size of the misstatements. The

determination of materiality is a matter of professional judgment and it is often influenced by

their perception. As the percentage of materiality varies from industry to industry, but it also

depends upon the perception of the auditors. Auditors have passed non-qualified audit report

which reflects that company has complied with the all applicable laws and regulations in

preparation of the financial statements. The unqualified audit report of the auditor reflects

that company has complied with the applicable rules and regulation in effective manner

(Choudhary, Merkley, & Schipper, 2018).

Conclusion

The annual report of technology one company has been assessed and it is analyzed

that auditors has set up their materiality performance ranging from 5% to 10% that reflects

the viability of the changes in its overall turnover. Auditing and assurance undertaken in this

8

Chand, 2015).

The main risk company is facing is related to going concern if it failed to manage the

proper flow of cash funding for its business. The financial activities of Technology one is

comparatively high which reflects that company might face issue related to increased cash

risk. The Auditors of company has also faced the issue related to the maternity level and cash

risk in its business.

The cash transactions in the cash flow statement of company include payment to

shareholders as dividend, issue of shares and payment for the investment. On the other hand,

non-cash transactions include depreciation, impairment loss and charge created on the assets

of company. This has shown that company might face issue related to the sustainable

business practice and may increase business risk which might negatively impact the business

growth of Technology Company (Legoria, Melendrez, & Reynolds, 2013).

REVIEW OF AUDIT REPORT

The opinion of the auditors for the financial statement of the Technology one company is

favourable. They centralize their visibility and policy setting regarding the risks of increasing

commodity price. Auditors of company have given in its report that it shall have counterparty

credit policies. Judgments regarding materiality are made in the context of surrounding

circumstances and they are influenced by the nature or size of the misstatements. The

determination of materiality is a matter of professional judgment and it is often influenced by

their perception. As the percentage of materiality varies from industry to industry, but it also

depends upon the perception of the auditors. Auditors have passed non-qualified audit report

which reflects that company has complied with the all applicable laws and regulations in

preparation of the financial statements. The unqualified audit report of the auditor reflects

that company has complied with the applicable rules and regulation in effective manner

(Choudhary, Merkley, & Schipper, 2018).

Conclusion

The annual report of technology one company has been assessed and it is analyzed

that auditors has set up their materiality performance ranging from 5% to 10% that reflects

the viability of the changes in its overall turnover. Auditing and assurance undertaken in this

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

report reflects that audit process helps in of company The financial performance of company

is also increasing and strengthening the true and fair view of the assets and liabilities

recorded in the financial statements reflecting the positive indicator for the future growth and

business outcomes in long run. Now in the end, it could be inferred that company should

establish the harmonization in its domestic and international reporting frameworks for

preparing the financial statements.

9

is also increasing and strengthening the true and fair view of the assets and liabilities

recorded in the financial statements reflecting the positive indicator for the future growth and

business outcomes in long run. Now in the end, it could be inferred that company should

establish the harmonization in its domestic and international reporting frameworks for

preparing the financial statements.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Bik, O., & Hooghiemstra, R. (2018). Cultural Differences in Auditors' Compliance with

Audit Firm Policy on Fraud Risk Assessment Procedures. Auditing: A Journal of

Practice and Theory.

Choudhary, P., Merkley, K. J., & Schipper, K. (2018). Auditors’ Quantitative Materiality

Judgments: Properties and Implications for Financial Reporting Reliability. 28(2), 44-

82

Fuhrmann, S., Ott, C., Looks, E., & Guenther, T. W. (2017). The contents of assurance

statements for sustainability reports and information asymmetry. Accounting and

Business Research, 47(4), 369-400.

Jelinek, K. (2015). The auditing profession: Accounting for some things. Business

Horizons, 5(58), 483-484.

Legoria, J., Melendrez, K. D., & Reynolds, J. K. (2013). Qualitative audit materiality and

earnings management. Review of Accounting Studies, 18(2), 414-442.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Mala, R., & Chand, P. (2015). Judgment and Decision‐Making Research in Auditing and

Accounting: Future Research Implications of Person, Task, and Environment

Perspective. Accounting Perspectives, 14(1), 1-50.

Mock, T. J., Ragothaman, S. C., & Srivastava, R. P. (2018). Using Evidential Reasoning

Technology to Enhance the Audit Quality Assurance Inspection Process. Journal of

Emerging Technologies in Accounting, 15(1), 29-43.

Pratt, S., & Peters, E. (2017). Internal audit: Raising the bar in auditing financial crime

risk. Journal of Financial Compliance, 1(3), 237-244.

10

Bik, O., & Hooghiemstra, R. (2018). Cultural Differences in Auditors' Compliance with

Audit Firm Policy on Fraud Risk Assessment Procedures. Auditing: A Journal of

Practice and Theory.

Choudhary, P., Merkley, K. J., & Schipper, K. (2018). Auditors’ Quantitative Materiality

Judgments: Properties and Implications for Financial Reporting Reliability. 28(2), 44-

82

Fuhrmann, S., Ott, C., Looks, E., & Guenther, T. W. (2017). The contents of assurance

statements for sustainability reports and information asymmetry. Accounting and

Business Research, 47(4), 369-400.

Jelinek, K. (2015). The auditing profession: Accounting for some things. Business

Horizons, 5(58), 483-484.

Legoria, J., Melendrez, K. D., & Reynolds, J. K. (2013). Qualitative audit materiality and

earnings management. Review of Accounting Studies, 18(2), 414-442.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Mala, R., & Chand, P. (2015). Judgment and Decision‐Making Research in Auditing and

Accounting: Future Research Implications of Person, Task, and Environment

Perspective. Accounting Perspectives, 14(1), 1-50.

Mock, T. J., Ragothaman, S. C., & Srivastava, R. P. (2018). Using Evidential Reasoning

Technology to Enhance the Audit Quality Assurance Inspection Process. Journal of

Emerging Technologies in Accounting, 15(1), 29-43.

Pratt, S., & Peters, E. (2017). Internal audit: Raising the bar in auditing financial crime

risk. Journal of Financial Compliance, 1(3), 237-244.

10

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.