Economics Report: Market Structure of Telecom Industry Analysis

VerifiedAdded on 2022/08/16

|17

|2739

|25

Report

AI Summary

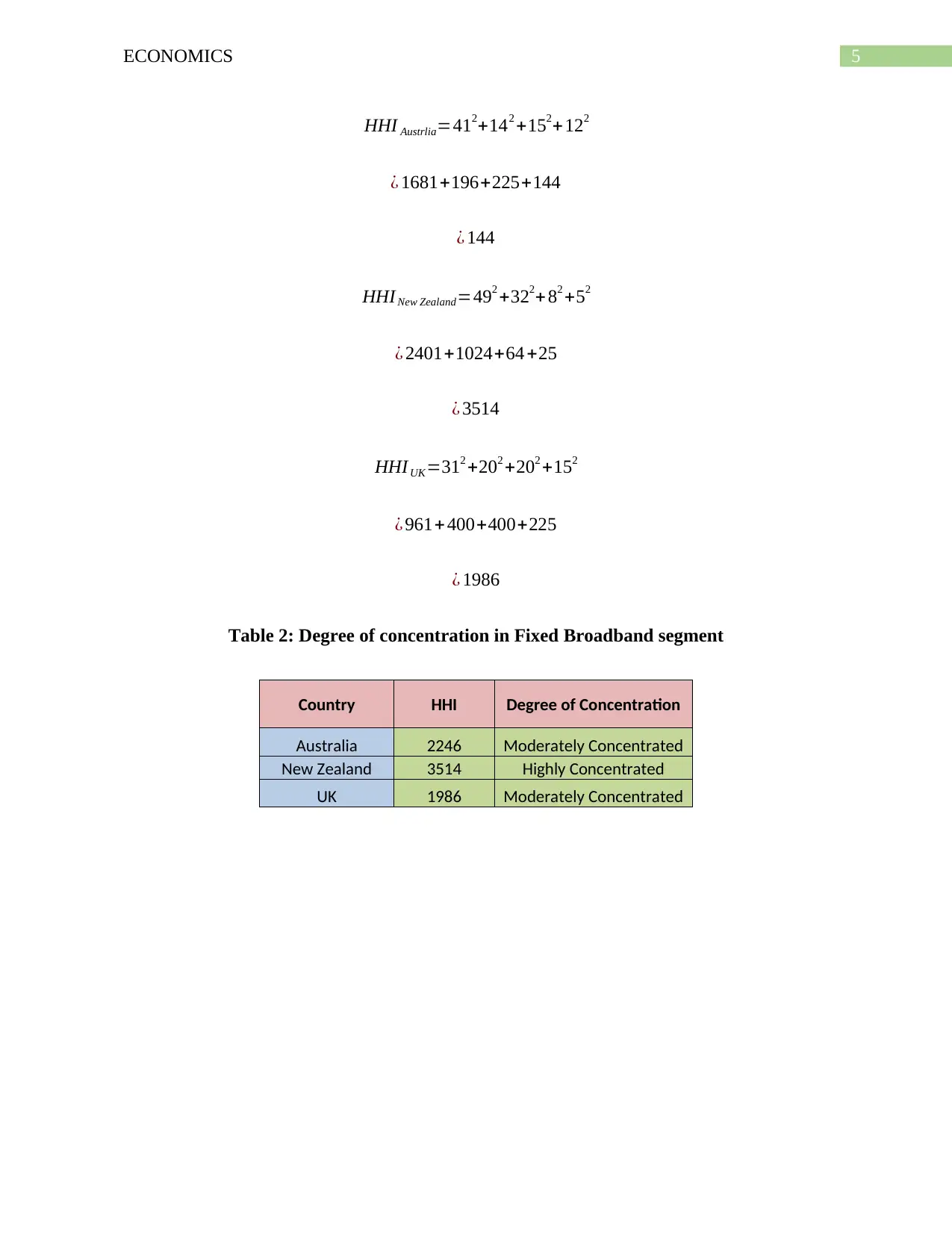

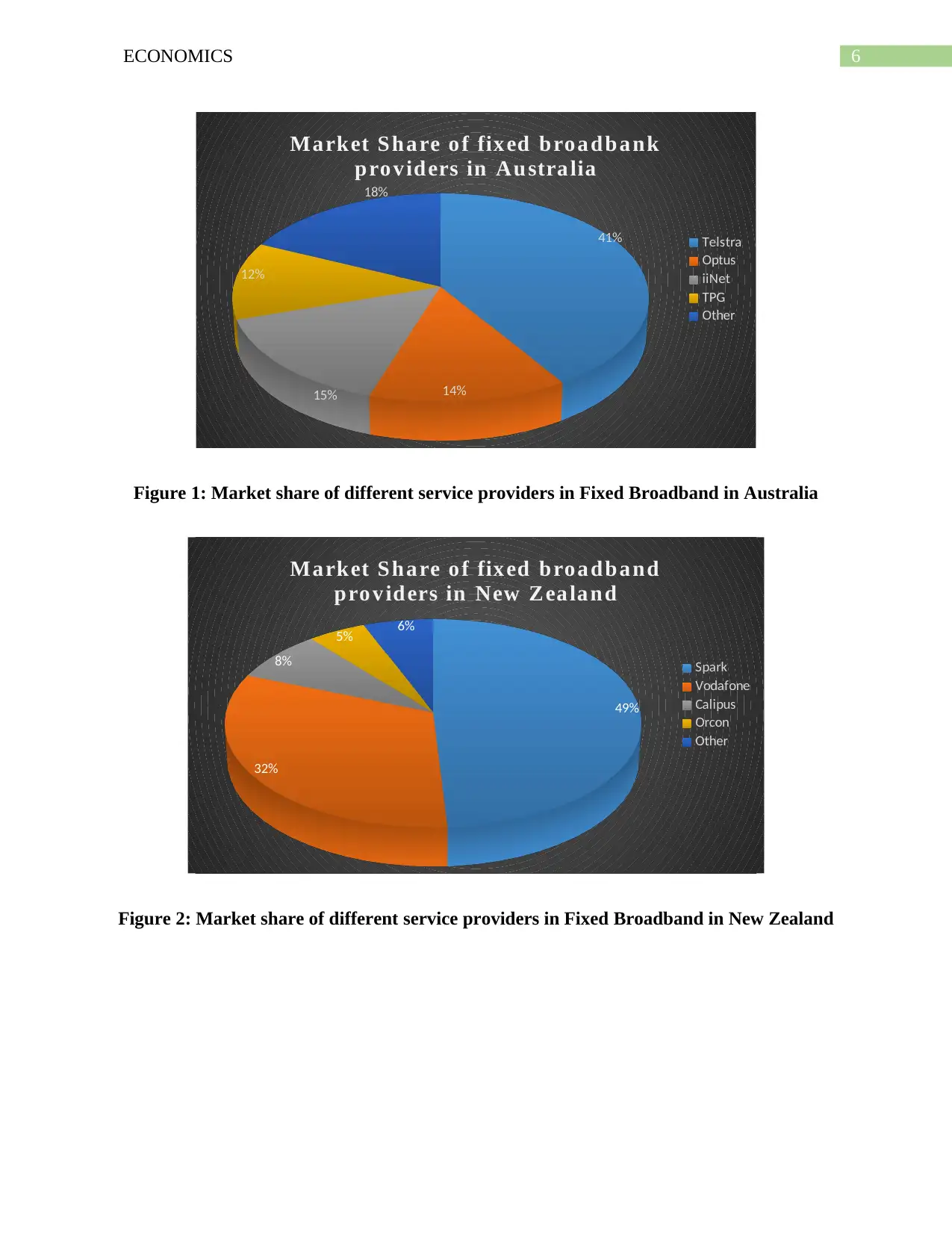

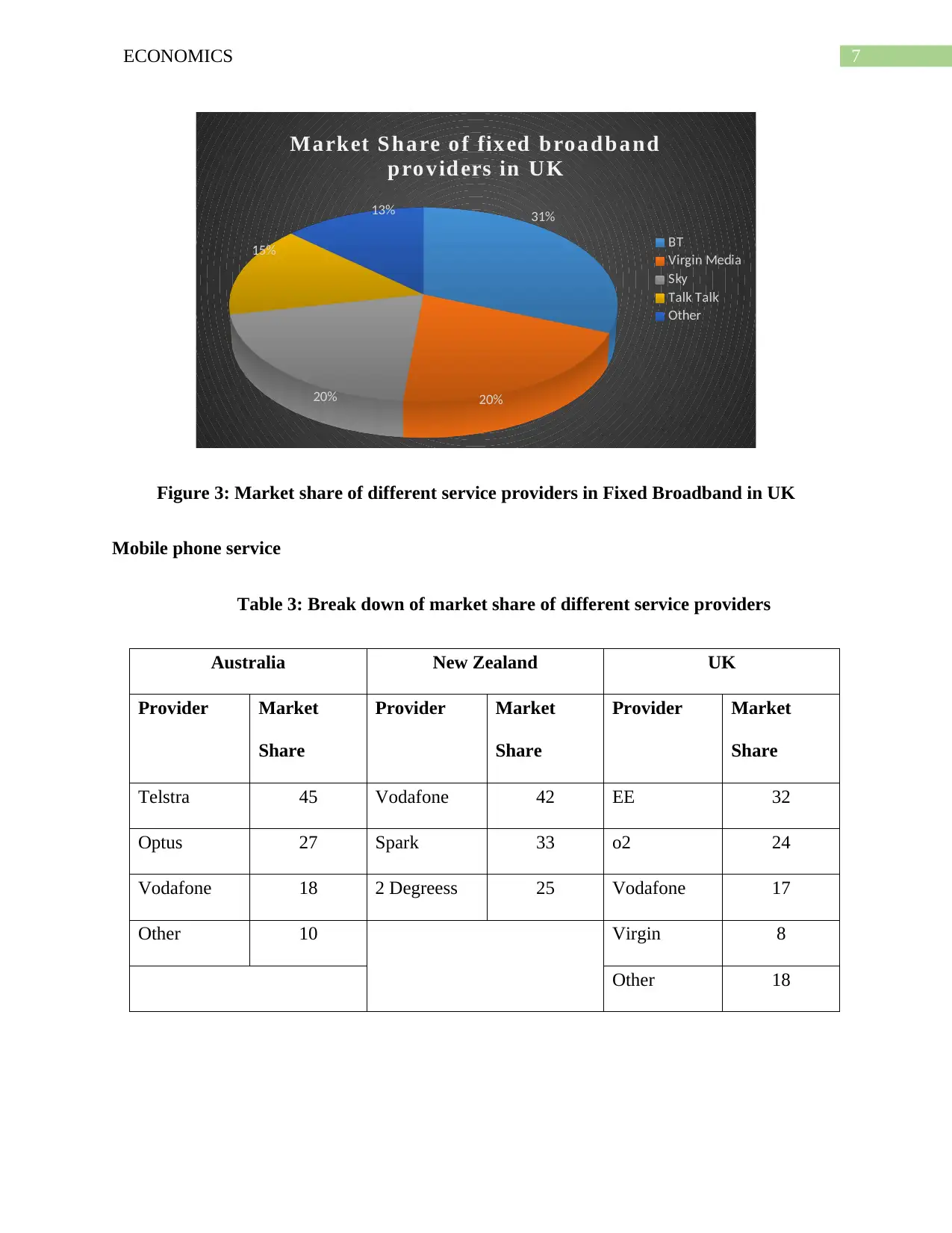

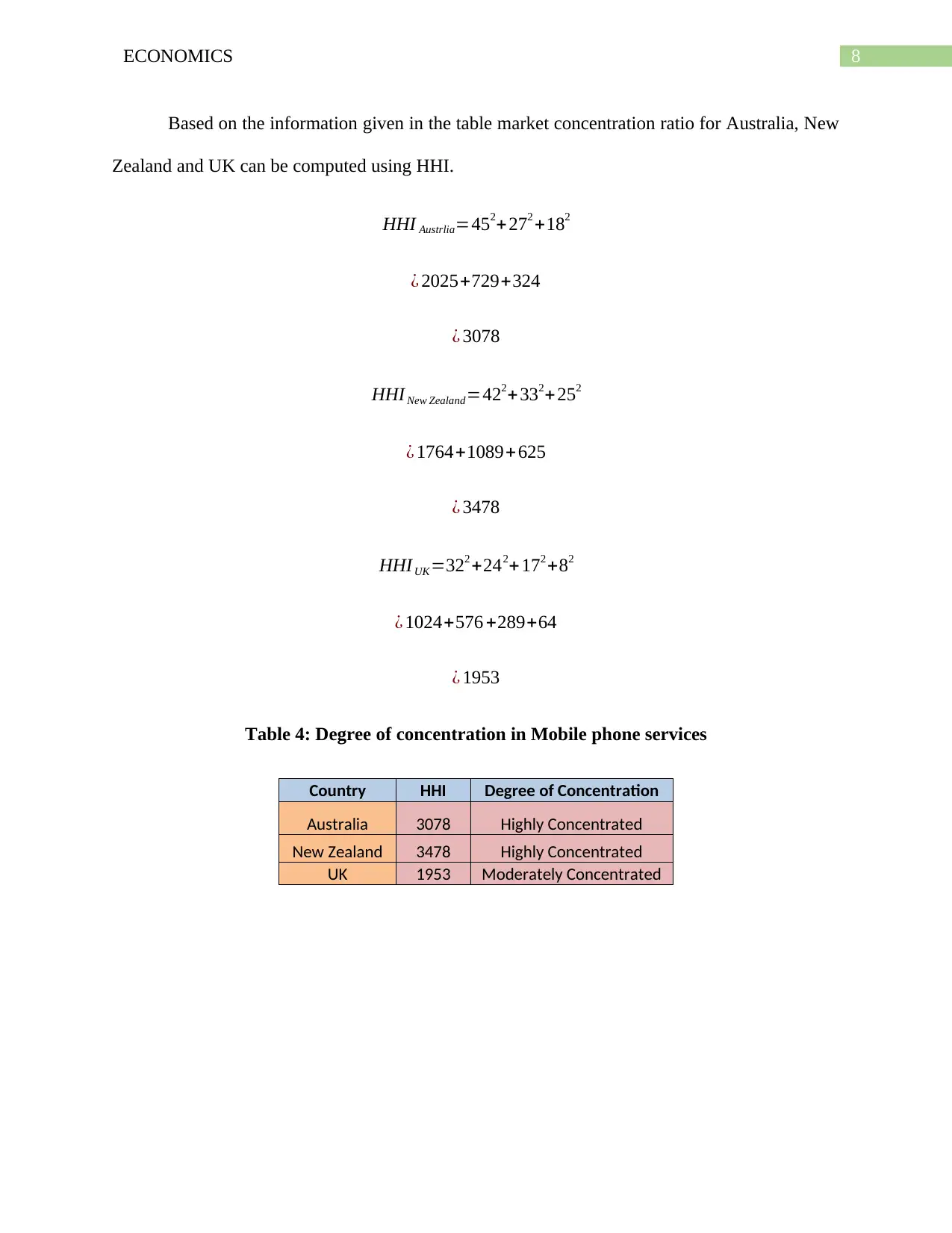

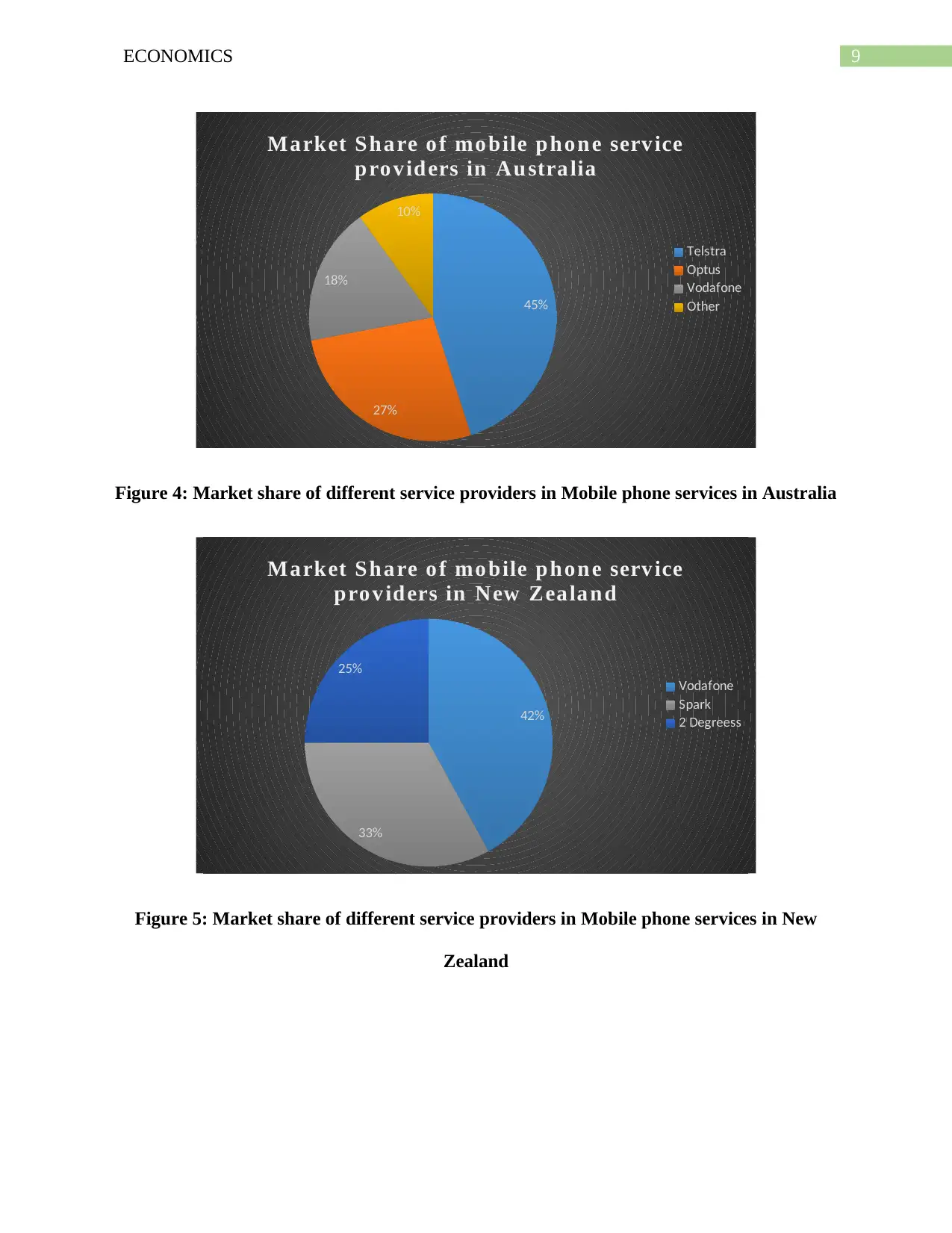

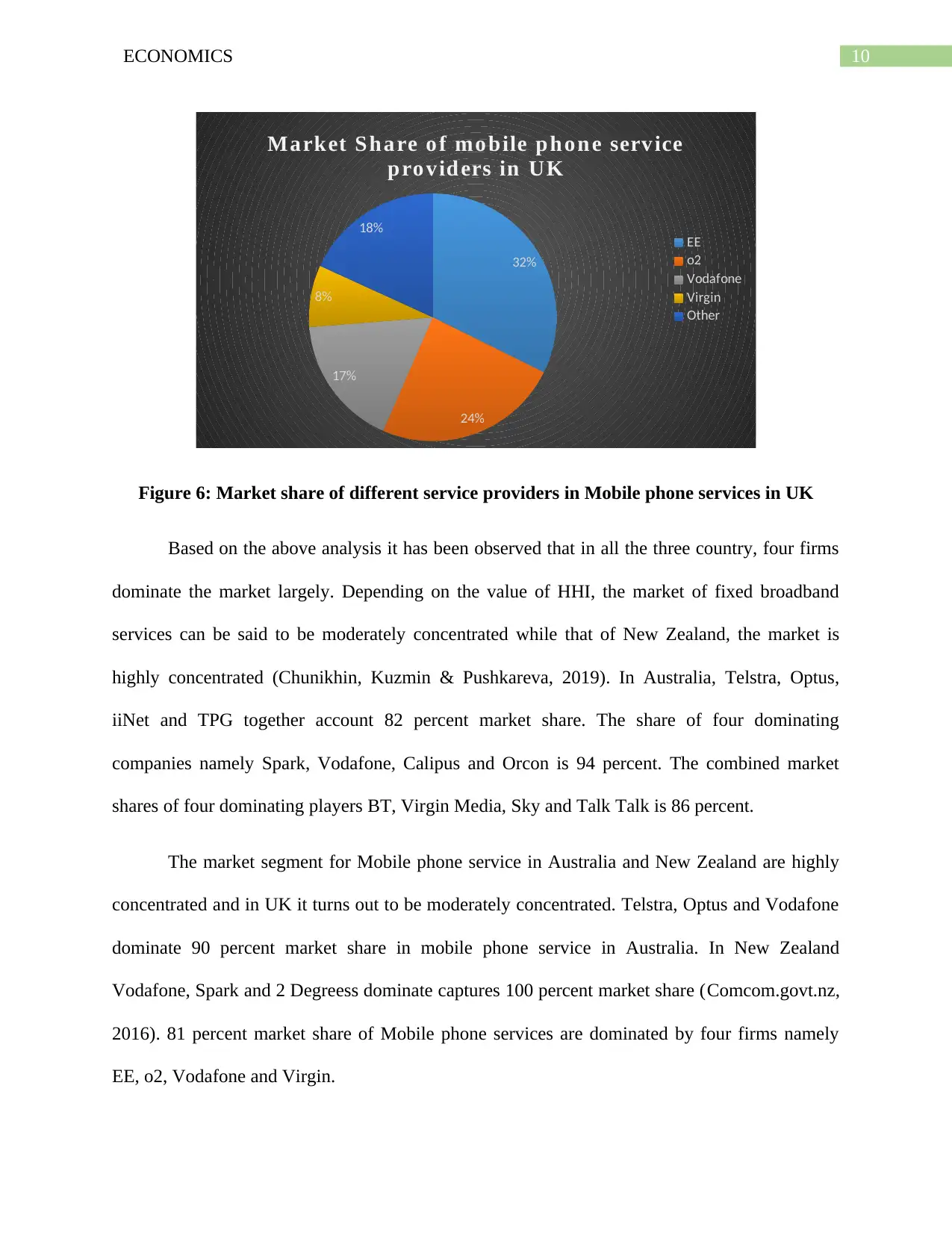

This report analyzes the market structure of the telecommunications industry in Australia, New Zealand, and the UK. It examines market concentration for fixed broadband and mobile phone services using the Herfindahl-Hirschman Index (HHI), revealing an oligopoly market structure dominated by a few firms. The report discusses the potential for price premiums charged by these dominant players and their impact on consumers. Furthermore, it explores government strategies to boost competition, reduce prices, and improve consumer welfare within the telecommunications sector. The analysis includes detailed market share breakdowns, HHI calculations, and a discussion of premium pricing strategies, concluding with recommendations for fostering a more competitive market environment.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.