Financial Report Analysis: Contemporary Accounting Issues in Australia

VerifiedAdded on 2020/03/04

|15

|2708

|90

Report

AI Summary

This report provides a comparative analysis of the accounting practices of Telstra Corporation and Amaysim Australia Limited, focusing on their compliance with the IFRS and AASB conceptual frameworks. The analysis includes a review of their annual reports, treatment of assets (tangible and intangible), depreciation methods, and the content of their Annual General Meeting (AGM) and Director's reports. The report highlights key differences in asset valuation, depreciation policies, and financial reporting practices between the two companies. It also addresses specific issues related to the application of IFRS and AASB standards in their accounting practices, including the challenges and limitations of these frameworks, providing a comprehensive overview of their financial reporting strategies and the implications for stakeholders. The report uses financial data from 2015 and 2016 to illustrate the differences in financial performance and asset management between the two companies.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary issues in accounting

Name of the student

Name of the university

Author note

Contemporary issues in accounting

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CONTEMPORARY ISSUES IN ACCOUNTING

Executive summary

This report will focus on the importance of IFRS and AASB conceptual framework on the

accounting and financial statement of Telstra Corporation and Amaysim Australia Limited. It

will also focus on the treatment of assets, method of depreciation of the company. Further,

the report will concentrate on the AGM of the companies, Director’s reports of the companies

and the issue associated with the IFRS and AASB in accounting.

Executive summary

This report will focus on the importance of IFRS and AASB conceptual framework on the

accounting and financial statement of Telstra Corporation and Amaysim Australia Limited. It

will also focus on the treatment of assets, method of depreciation of the company. Further,

the report will concentrate on the AGM of the companies, Director’s reports of the companies

and the issue associated with the IFRS and AASB in accounting.

2CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Analysis......................................................................................................................................4

Annual reports and its compliance with AASB conceptual framework....................................4

Total assets.................................................................................................................................5

Tangible asset.............................................................................................................................5

Intangible assets.........................................................................................................................6

Treatment of assets.....................................................................................................................7

Depreciation...............................................................................................................................8

Treatment of assets.....................................................................................................................8

Depreciation...............................................................................................................................9

AGM report..............................................................................................................................10

Director’s report and closing statements..................................................................................10

Issues in accounting with regard to IFRS and AASB..............................................................11

Conclusion................................................................................................................................12

Reference..................................................................................................................................13

Table of Contents

Introduction................................................................................................................................3

Analysis......................................................................................................................................4

Annual reports and its compliance with AASB conceptual framework....................................4

Total assets.................................................................................................................................5

Tangible asset.............................................................................................................................5

Intangible assets.........................................................................................................................6

Treatment of assets.....................................................................................................................7

Depreciation...............................................................................................................................8

Treatment of assets.....................................................................................................................8

Depreciation...............................................................................................................................9

AGM report..............................................................................................................................10

Director’s report and closing statements..................................................................................10

Issues in accounting with regard to IFRS and AASB..............................................................11

Conclusion................................................................................................................................12

Reference..................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

Telstra is one of the leading technologies and Telecommunication Company from

Australia that offers full range of services related to telecommunication sector and competes

with all the other telecommunication companies. They deliver services to more than 17

million mobile services, 3.5 million retail services for broadband and 6.8 million services to

fixed voices. They believe that more the people are connected, more opportunities they will

have. Therefore, they are assisting in creating the exceptional connectivity for everyone.

They believe in content and technology solutions which are easy and simple to use and are

valued by the customers. They always focus on serving and knowing the preference of the

customers better as compared to others. As the leading information and Telecommunication

Company from Australia, Telstra always provides a helping hand towards their customer to

improve their living standard through better connectivity (Telstra.com.au, 2017).

On the other hand, Amaysim is the telecommunication company that is focussed on

providing the telecommunication services and make the home internet and mobile experience

of the customers with exceptionally simple through solving the unnecessary issues and letting

the customers to get the superfast speed at pocket-friendly price. They believe in providing

the services in such a way that the customers will have minimum number of complaints with

regard to the telecommunication services. They are confident that at least 93% of their

customers will tell their loved ones or mate regarding the exceptional good services of the

company. Further, they believe in no lock-in contacts that mean if the customers with

Amaysim it is just because they want to be with the company and not because they are forced

to be with the company (Amaysim.com.au, 2017).

Introduction

Telstra is one of the leading technologies and Telecommunication Company from

Australia that offers full range of services related to telecommunication sector and competes

with all the other telecommunication companies. They deliver services to more than 17

million mobile services, 3.5 million retail services for broadband and 6.8 million services to

fixed voices. They believe that more the people are connected, more opportunities they will

have. Therefore, they are assisting in creating the exceptional connectivity for everyone.

They believe in content and technology solutions which are easy and simple to use and are

valued by the customers. They always focus on serving and knowing the preference of the

customers better as compared to others. As the leading information and Telecommunication

Company from Australia, Telstra always provides a helping hand towards their customer to

improve their living standard through better connectivity (Telstra.com.au, 2017).

On the other hand, Amaysim is the telecommunication company that is focussed on

providing the telecommunication services and make the home internet and mobile experience

of the customers with exceptionally simple through solving the unnecessary issues and letting

the customers to get the superfast speed at pocket-friendly price. They believe in providing

the services in such a way that the customers will have minimum number of complaints with

regard to the telecommunication services. They are confident that at least 93% of their

customers will tell their loved ones or mate regarding the exceptional good services of the

company. Further, they believe in no lock-in contacts that mean if the customers with

Amaysim it is just because they want to be with the company and not because they are forced

to be with the company (Amaysim.com.au, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CONTEMPORARY ISSUES IN ACCOUNTING

Analysis

Annual reports and its compliance with AASB conceptual framework

From the Financial statement of Telstra it is recognised that the financial report of the

company is a general purpose financial report and is prepared by the profit entity as per the

requirements of the Australian Corporation Act 2001, the Accounting Standards those are

applicable in Australia and other conceptual framework and interpretation of AASB

(Australian Accounting Standard Board) and also complies with the IFRS (International

Financial Reporting Standards) and the interpretations issued by the IASB (International

Accounting Standards Board) (Kober, Lee & Ng, 2013). Further, the report is prepared in

Australian Dollars unless it is stated otherwise and the value are rounded off to nearest

million dollars ($m) under the available option of ASIC. The historical balue approach is

used for preparation of the statements except for some financial instruments those are

transacted at fair values.

On the other hand, in the way like Telstra, Amysim’s financial report is also a general

purpose financial report that is prepared by the profit entity as per the requirements of the

Australian Corporation Act 2001, the Accounting Standards those are applicable in Australia

and other conceptual framework and interpretation of AASB (Australian Accounting

Standard Board) and also complies with the IFRS (International Financial Reporting

Standards) and the interpretations issued by the IASB (International Accounting Standards

Board). Further, the report is prepared in Australian Dollars unless it is stated otherwise and

the value are rounded off to nearest thousand dollars ($’000) under the available option of

ASIC. The historical value approach is used for preparation of the statements except for some

financial instruments those are transacted at fair values.

Analysis

Annual reports and its compliance with AASB conceptual framework

From the Financial statement of Telstra it is recognised that the financial report of the

company is a general purpose financial report and is prepared by the profit entity as per the

requirements of the Australian Corporation Act 2001, the Accounting Standards those are

applicable in Australia and other conceptual framework and interpretation of AASB

(Australian Accounting Standard Board) and also complies with the IFRS (International

Financial Reporting Standards) and the interpretations issued by the IASB (International

Accounting Standards Board) (Kober, Lee & Ng, 2013). Further, the report is prepared in

Australian Dollars unless it is stated otherwise and the value are rounded off to nearest

million dollars ($m) under the available option of ASIC. The historical balue approach is

used for preparation of the statements except for some financial instruments those are

transacted at fair values.

On the other hand, in the way like Telstra, Amysim’s financial report is also a general

purpose financial report that is prepared by the profit entity as per the requirements of the

Australian Corporation Act 2001, the Accounting Standards those are applicable in Australia

and other conceptual framework and interpretation of AASB (Australian Accounting

Standard Board) and also complies with the IFRS (International Financial Reporting

Standards) and the interpretations issued by the IASB (International Accounting Standards

Board). Further, the report is prepared in Australian Dollars unless it is stated otherwise and

the value are rounded off to nearest thousand dollars ($’000) under the available option of

ASIC. The historical value approach is used for preparation of the statements except for some

financial instruments those are transacted at fair values.

5CONTEMPORARY ISSUES IN ACCOUNTING

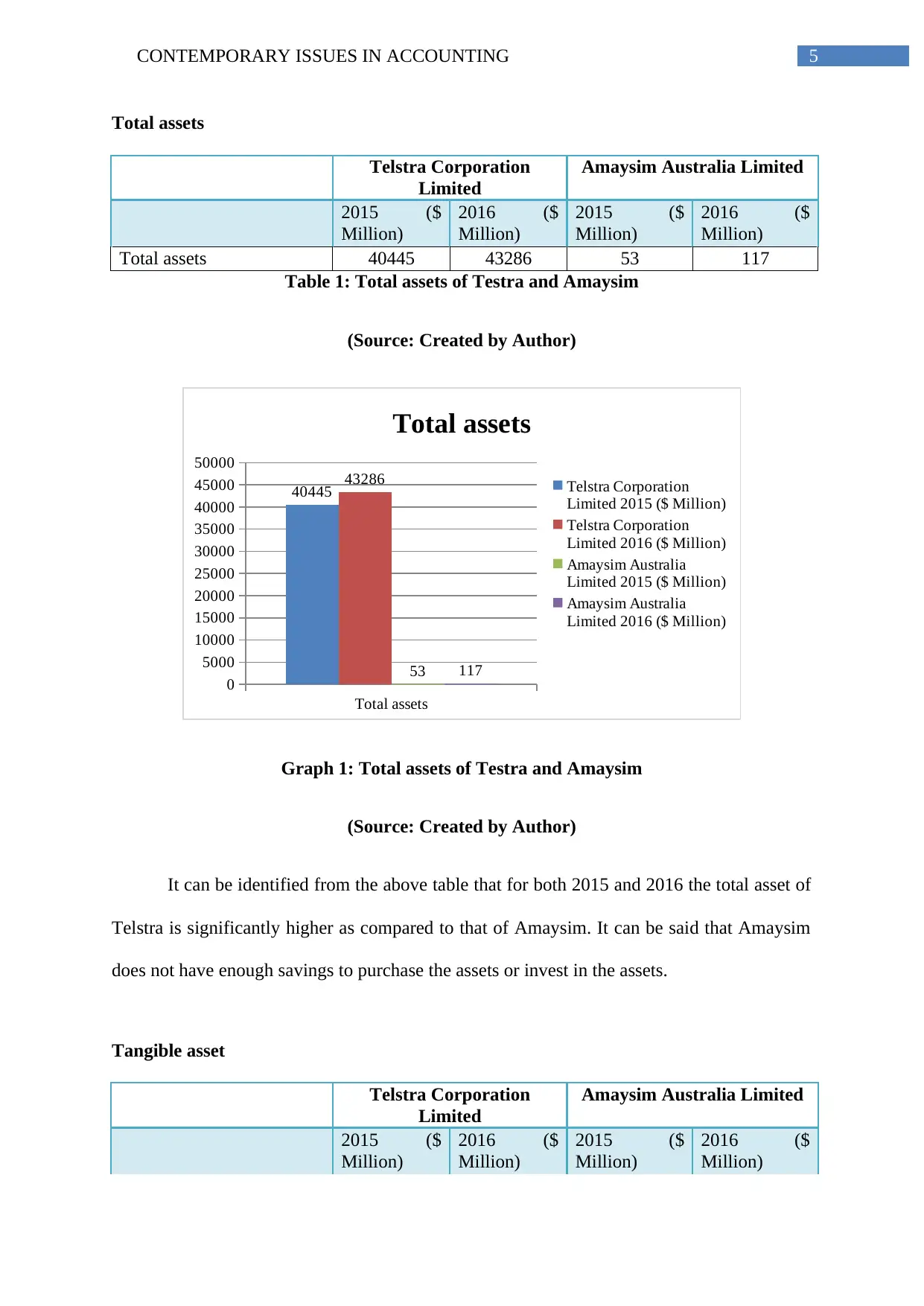

Total assets

Telstra Corporation

Limited

Amaysim Australia Limited

2015 ($

Million)

2016 ($

Million)

2015 ($

Million)

2016 ($

Million)

Total assets 40445 43286 53 117

Table 1: Total assets of Testra and Amaysim

(Source: Created by Author)

Total assets

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

40445 43286

53 117

Total assets

Telstra Corporation

Limited 2015 ($ Million)

Telstra Corporation

Limited 2016 ($ Million)

Amaysim Australia

Limited 2015 ($ Million)

Amaysim Australia

Limited 2016 ($ Million)

Graph 1: Total assets of Testra and Amaysim

(Source: Created by Author)

It can be identified from the above table that for both 2015 and 2016 the total asset of

Telstra is significantly higher as compared to that of Amaysim. It can be said that Amaysim

does not have enough savings to purchase the assets or invest in the assets.

Tangible asset

Telstra Corporation

Limited

Amaysim Australia Limited

2015 ($

Million)

2016 ($

Million)

2015 ($

Million)

2016 ($

Million)

Total assets

Telstra Corporation

Limited

Amaysim Australia Limited

2015 ($

Million)

2016 ($

Million)

2015 ($

Million)

2016 ($

Million)

Total assets 40445 43286 53 117

Table 1: Total assets of Testra and Amaysim

(Source: Created by Author)

Total assets

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

40445 43286

53 117

Total assets

Telstra Corporation

Limited 2015 ($ Million)

Telstra Corporation

Limited 2016 ($ Million)

Amaysim Australia

Limited 2015 ($ Million)

Amaysim Australia

Limited 2016 ($ Million)

Graph 1: Total assets of Testra and Amaysim

(Source: Created by Author)

It can be identified from the above table that for both 2015 and 2016 the total asset of

Telstra is significantly higher as compared to that of Amaysim. It can be said that Amaysim

does not have enough savings to purchase the assets or invest in the assets.

Tangible asset

Telstra Corporation

Limited

Amaysim Australia Limited

2015 ($

Million)

2016 ($

Million)

2015 ($

Million)

2016 ($

Million)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CONTEMPORARY ISSUES IN ACCOUNTING

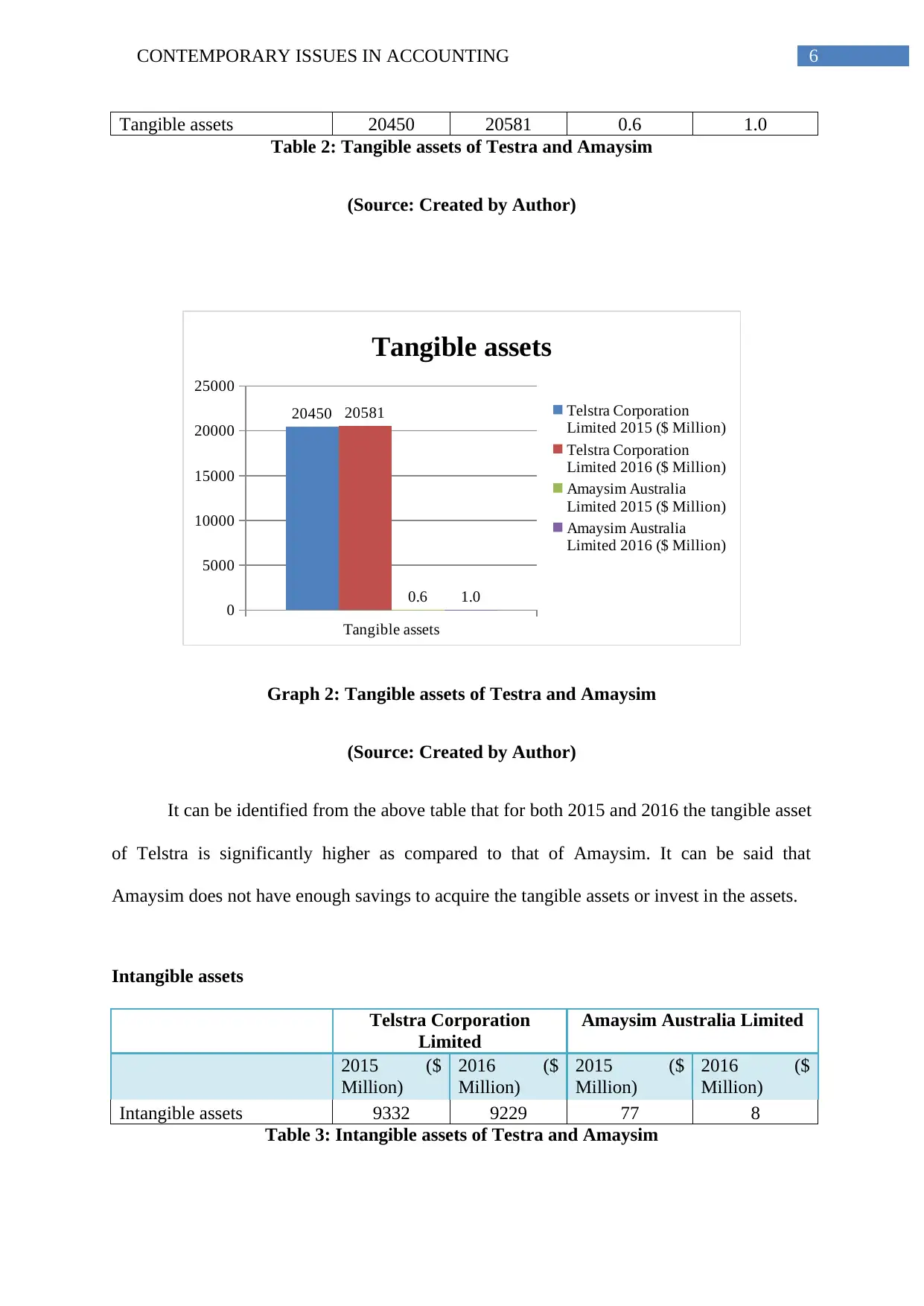

Tangible assets 20450 20581 0.6 1.0

Table 2: Tangible assets of Testra and Amaysim

(Source: Created by Author)

Tangible assets

0

5000

10000

15000

20000

25000

20450 20581

0.6 1.0

Tangible assets

Telstra Corporation

Limited 2015 ($ Million)

Telstra Corporation

Limited 2016 ($ Million)

Amaysim Australia

Limited 2015 ($ Million)

Amaysim Australia

Limited 2016 ($ Million)

Graph 2: Tangible assets of Testra and Amaysim

(Source: Created by Author)

It can be identified from the above table that for both 2015 and 2016 the tangible asset

of Telstra is significantly higher as compared to that of Amaysim. It can be said that

Amaysim does not have enough savings to acquire the tangible assets or invest in the assets.

Intangible assets

Telstra Corporation

Limited

Amaysim Australia Limited

2015 ($

Million)

2016 ($

Million)

2015 ($

Million)

2016 ($

Million)

Intangible assets 9332 9229 77 8

Table 3: Intangible assets of Testra and Amaysim

Tangible assets 20450 20581 0.6 1.0

Table 2: Tangible assets of Testra and Amaysim

(Source: Created by Author)

Tangible assets

0

5000

10000

15000

20000

25000

20450 20581

0.6 1.0

Tangible assets

Telstra Corporation

Limited 2015 ($ Million)

Telstra Corporation

Limited 2016 ($ Million)

Amaysim Australia

Limited 2015 ($ Million)

Amaysim Australia

Limited 2016 ($ Million)

Graph 2: Tangible assets of Testra and Amaysim

(Source: Created by Author)

It can be identified from the above table that for both 2015 and 2016 the tangible asset

of Telstra is significantly higher as compared to that of Amaysim. It can be said that

Amaysim does not have enough savings to acquire the tangible assets or invest in the assets.

Intangible assets

Telstra Corporation

Limited

Amaysim Australia Limited

2015 ($

Million)

2016 ($

Million)

2015 ($

Million)

2016 ($

Million)

Intangible assets 9332 9229 77 8

Table 3: Intangible assets of Testra and Amaysim

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY ISSUES IN ACCOUNTING

(Source: Created by Author)

Intangible assets

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000 9332 9229

77 8

Intangible assets

Telstra Corporation

Limited 2015 ($ Million)

Telstra Corporation

Limited 2016 ($ Million)

Amaysim Australia

Limited 2015 ($ Million)

Amaysim Australia

Limited 2016 ($ Million)

Table 3: Intangible assets of Testra and Amaysim

(Source: Created by Author)

It can be identified from the above table that for both 2015 and 2016 the intangible

asset of Telstra is significantly higher as compared to that of Amaysim. It can be said that

Amaysim does not have enough savings to acquire the intangible assets or invest in the

assets.

Treatment of assets

The assets of Telstra like plant property and equipments including the the construction

under progress are transacted at cost after deducting the impairment and depreciation.

Further, the cost involves the purchase costs and the costs that are directly attributable for

bringing the assets to the condition and location required for the intended use (Kent and

Zunker, 2015). The borrowing costs are capitalised that are attributable to production,

(Source: Created by Author)

Intangible assets

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000 9332 9229

77 8

Intangible assets

Telstra Corporation

Limited 2015 ($ Million)

Telstra Corporation

Limited 2016 ($ Million)

Amaysim Australia

Limited 2015 ($ Million)

Amaysim Australia

Limited 2016 ($ Million)

Table 3: Intangible assets of Testra and Amaysim

(Source: Created by Author)

It can be identified from the above table that for both 2015 and 2016 the intangible

asset of Telstra is significantly higher as compared to that of Amaysim. It can be said that

Amaysim does not have enough savings to acquire the intangible assets or invest in the

assets.

Treatment of assets

The assets of Telstra like plant property and equipments including the the construction

under progress are transacted at cost after deducting the impairment and depreciation.

Further, the cost involves the purchase costs and the costs that are directly attributable for

bringing the assets to the condition and location required for the intended use (Kent and

Zunker, 2015). The borrowing costs are capitalised that are attributable to production,

8CONTEMPORARY ISSUES IN ACCOUNTING

acquisition or construction directly. All the other borrowing costs are identified as the

expenses under the income statement at the time of incurring.

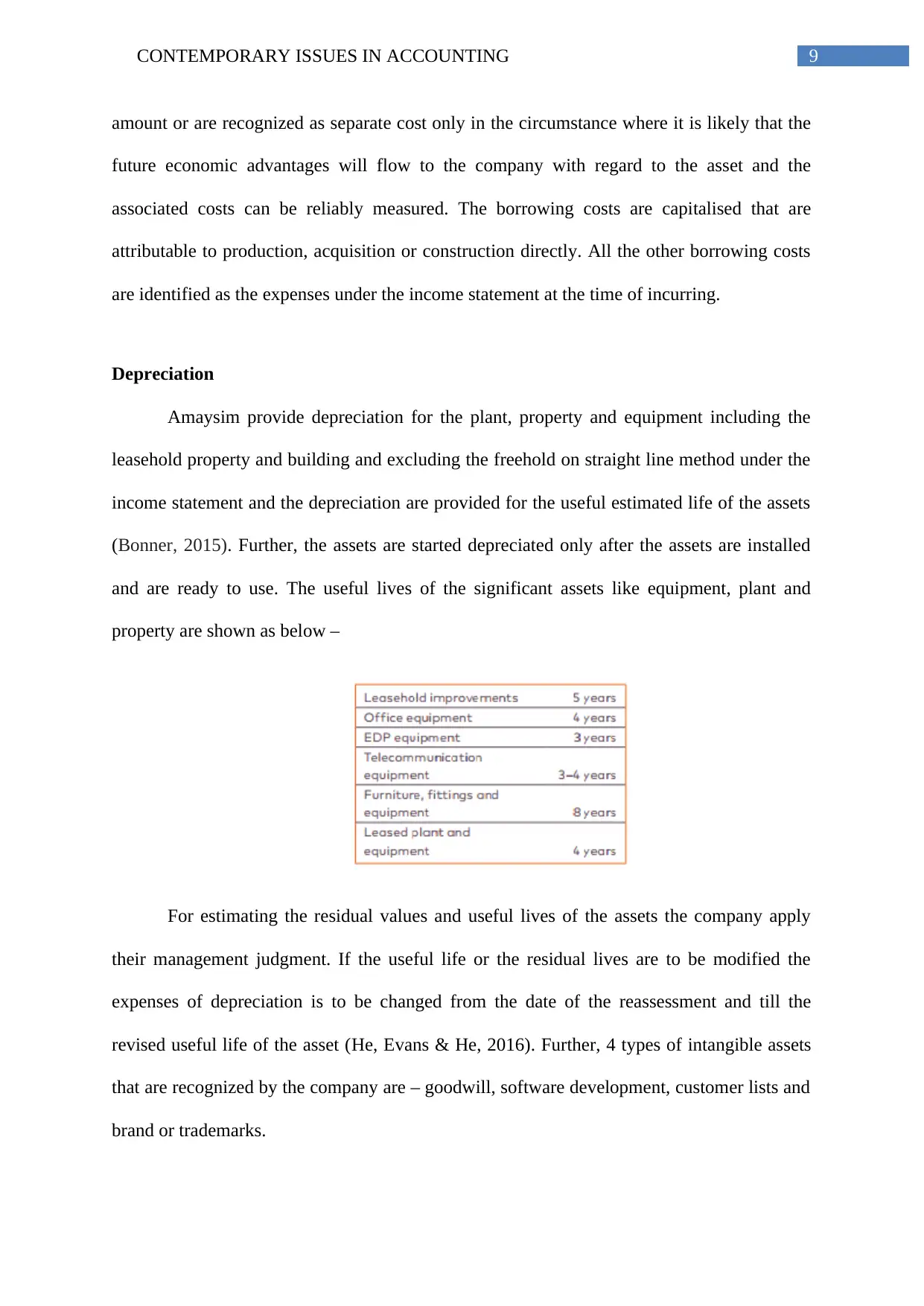

Depreciation

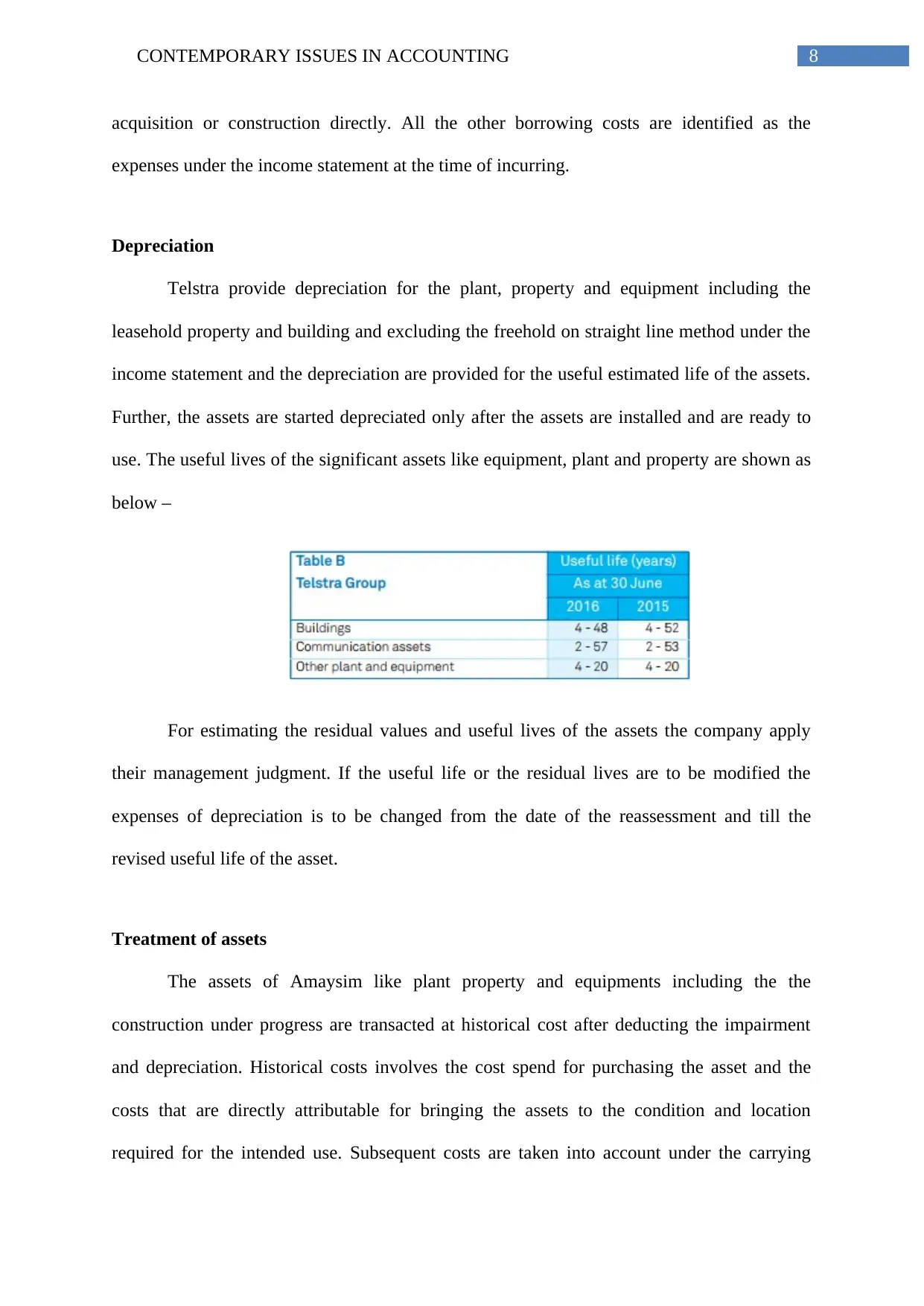

Telstra provide depreciation for the plant, property and equipment including the

leasehold property and building and excluding the freehold on straight line method under the

income statement and the depreciation are provided for the useful estimated life of the assets.

Further, the assets are started depreciated only after the assets are installed and are ready to

use. The useful lives of the significant assets like equipment, plant and property are shown as

below –

For estimating the residual values and useful lives of the assets the company apply

their management judgment. If the useful life or the residual lives are to be modified the

expenses of depreciation is to be changed from the date of the reassessment and till the

revised useful life of the asset.

Treatment of assets

The assets of Amaysim like plant property and equipments including the the

construction under progress are transacted at historical cost after deducting the impairment

and depreciation. Historical costs involves the cost spend for purchasing the asset and the

costs that are directly attributable for bringing the assets to the condition and location

required for the intended use. Subsequent costs are taken into account under the carrying

acquisition or construction directly. All the other borrowing costs are identified as the

expenses under the income statement at the time of incurring.

Depreciation

Telstra provide depreciation for the plant, property and equipment including the

leasehold property and building and excluding the freehold on straight line method under the

income statement and the depreciation are provided for the useful estimated life of the assets.

Further, the assets are started depreciated only after the assets are installed and are ready to

use. The useful lives of the significant assets like equipment, plant and property are shown as

below –

For estimating the residual values and useful lives of the assets the company apply

their management judgment. If the useful life or the residual lives are to be modified the

expenses of depreciation is to be changed from the date of the reassessment and till the

revised useful life of the asset.

Treatment of assets

The assets of Amaysim like plant property and equipments including the the

construction under progress are transacted at historical cost after deducting the impairment

and depreciation. Historical costs involves the cost spend for purchasing the asset and the

costs that are directly attributable for bringing the assets to the condition and location

required for the intended use. Subsequent costs are taken into account under the carrying

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CONTEMPORARY ISSUES IN ACCOUNTING

amount or are recognized as separate cost only in the circumstance where it is likely that the

future economic advantages will flow to the company with regard to the asset and the

associated costs can be reliably measured. The borrowing costs are capitalised that are

attributable to production, acquisition or construction directly. All the other borrowing costs

are identified as the expenses under the income statement at the time of incurring.

Depreciation

Amaysim provide depreciation for the plant, property and equipment including the

leasehold property and building and excluding the freehold on straight line method under the

income statement and the depreciation are provided for the useful estimated life of the assets

(Bonner, 2015). Further, the assets are started depreciated only after the assets are installed

and are ready to use. The useful lives of the significant assets like equipment, plant and

property are shown as below –

For estimating the residual values and useful lives of the assets the company apply

their management judgment. If the useful life or the residual lives are to be modified the

expenses of depreciation is to be changed from the date of the reassessment and till the

revised useful life of the asset (He, Evans & He, 2016). Further, 4 types of intangible assets

that are recognized by the company are – goodwill, software development, customer lists and

brand or trademarks.

amount or are recognized as separate cost only in the circumstance where it is likely that the

future economic advantages will flow to the company with regard to the asset and the

associated costs can be reliably measured. The borrowing costs are capitalised that are

attributable to production, acquisition or construction directly. All the other borrowing costs

are identified as the expenses under the income statement at the time of incurring.

Depreciation

Amaysim provide depreciation for the plant, property and equipment including the

leasehold property and building and excluding the freehold on straight line method under the

income statement and the depreciation are provided for the useful estimated life of the assets

(Bonner, 2015). Further, the assets are started depreciated only after the assets are installed

and are ready to use. The useful lives of the significant assets like equipment, plant and

property are shown as below –

For estimating the residual values and useful lives of the assets the company apply

their management judgment. If the useful life or the residual lives are to be modified the

expenses of depreciation is to be changed from the date of the reassessment and till the

revised useful life of the asset (He, Evans & He, 2016). Further, 4 types of intangible assets

that are recognized by the company are – goodwill, software development, customer lists and

brand or trademarks.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CONTEMPORARY ISSUES IN ACCOUNTING

AGM report

The AGM of Telstra for the year 2016 was held on 11th October 2016, Tuesday at

Grand Ballroom, Four Points By Sheraton (Darling Harbour), 161 Sussex Street, Sydney

NSW. The meeting was held as per the listing Rule of 3.13.2 and the section 251AA (2) of

Corporation Act. At the AGM o the company the following points were discussed –

Re-election and election of the directors

Grant for performance rights

Adoption of remuneration report

On the other hand, the AGM of Amaysim was held on 17th November 2016 at the

Market Announcement Office, Australian Securities Exchange, 20 Bridge Street, Sydney

NSW 2000. The meeting was held as per the listing Rule of 3.13.2 and the section 251AA (2)

of Corporation Act. At the AGM o the company the following points were discussed –

Summarize the performance of the company for the financial year 2016

Provide the overview for their strategies and the business model and to explain the

reasons that setting them apart from their competitors

Highlight the priorities for future years including their entry into broadband market.

Director’s report and closing statements

Under the director’s report of Telstra it is mentioned that that Telstra Entity falls

under the category of company as mentioned in Australian Securities and Investment

Commission Corporations (Rounding under Director’s or Financial Reports/) instrument

2016/191 that is dated on 24th March 2016 and the issued pursuant with regard to the section

341(1) of Corporation Act 2001. Owing to this, the amounts under the director’s report and

that are mentioned in the attached financial report are rounded off to nearest million dollars

AGM report

The AGM of Telstra for the year 2016 was held on 11th October 2016, Tuesday at

Grand Ballroom, Four Points By Sheraton (Darling Harbour), 161 Sussex Street, Sydney

NSW. The meeting was held as per the listing Rule of 3.13.2 and the section 251AA (2) of

Corporation Act. At the AGM o the company the following points were discussed –

Re-election and election of the directors

Grant for performance rights

Adoption of remuneration report

On the other hand, the AGM of Amaysim was held on 17th November 2016 at the

Market Announcement Office, Australian Securities Exchange, 20 Bridge Street, Sydney

NSW 2000. The meeting was held as per the listing Rule of 3.13.2 and the section 251AA (2)

of Corporation Act. At the AGM o the company the following points were discussed –

Summarize the performance of the company for the financial year 2016

Provide the overview for their strategies and the business model and to explain the

reasons that setting them apart from their competitors

Highlight the priorities for future years including their entry into broadband market.

Director’s report and closing statements

Under the director’s report of Telstra it is mentioned that that Telstra Entity falls

under the category of company as mentioned in Australian Securities and Investment

Commission Corporations (Rounding under Director’s or Financial Reports/) instrument

2016/191 that is dated on 24th March 2016 and the issued pursuant with regard to the section

341(1) of Corporation Act 2001. Owing to this, the amounts under the director’s report and

that are mentioned in the attached financial report are rounded off to nearest million dollars

11CONTEMPORARY ISSUES IN ACCOUNTING

($m), except where mentioned otherwise. Further, the report was made on 11th August 2016

as per the resolution of the directors (James & Prout, 2015).

On the other hand, under the director’s report of Amaysim it is mentioned that the

company’s board are committed for demonstrating and achieving the highest standards under

the corporate governance. They have reviewed the practices of corporate governance against

the recommendations and principles issued by ASX Corporate Governance Council (Bhimani

2015). Further, it is mentioned that the company falls under the category of company as

mentioned in Australian Securities and Investment Commission Corporations (Rounding

under Director’s or Financial Reports/) instrument 2016/191 that is dated on 24th March 2016

and the issued pursuant with regard to the section 341(1) of Corporation Act 2001. Owing to

this, the amounts under the director’s report and that are mentioned in the attached financial

report are rounded off to nearest thousand dollars ($’000), except where mentioned

otherwise.

Issues in accounting with regard to IFRS and AASB

Various issues that are associated with the IFRS and AASb for accounting are as

follows –

IFRS interpretations are written only for for-profit companies

IFRS do not consider the non-exchange transactions like taxes, donations and grants

and also do not deal with the non-cash generating activities like infrastructure assets

and heritage assets (Beaver, 2014)

Consolidation of GBEs into Government’s financial statement may entail the

alignment of the accounting policies (Williams, 2014)

It also have issue with related party disclosures, emission trading schemes,

disaggregated disclosures and reporting of service performance

($m), except where mentioned otherwise. Further, the report was made on 11th August 2016

as per the resolution of the directors (James & Prout, 2015).

On the other hand, under the director’s report of Amaysim it is mentioned that the

company’s board are committed for demonstrating and achieving the highest standards under

the corporate governance. They have reviewed the practices of corporate governance against

the recommendations and principles issued by ASX Corporate Governance Council (Bhimani

2015). Further, it is mentioned that the company falls under the category of company as

mentioned in Australian Securities and Investment Commission Corporations (Rounding

under Director’s or Financial Reports/) instrument 2016/191 that is dated on 24th March 2016

and the issued pursuant with regard to the section 341(1) of Corporation Act 2001. Owing to

this, the amounts under the director’s report and that are mentioned in the attached financial

report are rounded off to nearest thousand dollars ($’000), except where mentioned

otherwise.

Issues in accounting with regard to IFRS and AASB

Various issues that are associated with the IFRS and AASb for accounting are as

follows –

IFRS interpretations are written only for for-profit companies

IFRS do not consider the non-exchange transactions like taxes, donations and grants

and also do not deal with the non-cash generating activities like infrastructure assets

and heritage assets (Beaver, 2014)

Consolidation of GBEs into Government’s financial statement may entail the

alignment of the accounting policies (Williams, 2014)

It also have issue with related party disclosures, emission trading schemes,

disaggregated disclosures and reporting of service performance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.