BBAC601: Audit Strategy and Risk Assessment for Telstra Corp

VerifiedAdded on 2023/04/19

|16

|4373

|138

Report

AI Summary

This report outlines an audit strategy for Telstra Corporation Limited for the 2017-2018 financial year, developed in accordance with Australian Standard on Auditing (ASA) 315. It includes a detailed analysis of the client, covering information about Telstra, its industry, regulatory environment, nature of operations, and accounting policies. The report also examines related party transactions, changes in accounting policies, preliminary analytical procedures, financial performance measurement, and business objectives and strategies, assessing their impacts on future audit work. The aim is to provide a comprehensive understanding of Telstra to facilitate effective audit planning. Desklib provides a platform to explore similar solved assignments and past papers for students.

Running head: AUDIT STRATEGY

Audit Strategy

Name of the Student

Name of the University

Author’s Note

Audit Strategy

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT STRATEGY

Table of Contents

1. Introduction............................................................................................................................2

Part A: The Client......................................................................................................................2

2.1 Information about the Client............................................................................................2

2.2 Industry, Regulatory and Other External Factors............................................................3

2.3 Nature of the Client..........................................................................................................3

2.4 Accounting Policy............................................................................................................4

2.5 Related Parties and Transaction with Related Parties......................................................5

Part B: Analysis of the Client and Impacts on the Future Audit Works....................................8

2.6 Changes in Accounting Policies and the Impact of Changes...........................................8

2.7 Preliminary Analytical Procedures..................................................................................9

2.8 Measurement and Review of Financial Performance....................................................10

2.9 Objectives, Strategies and Related Business Risks........................................................11

3. Conclusion............................................................................................................................11

References................................................................................................................................13

Table of Contents

1. Introduction............................................................................................................................2

Part A: The Client......................................................................................................................2

2.1 Information about the Client............................................................................................2

2.2 Industry, Regulatory and Other External Factors............................................................3

2.3 Nature of the Client..........................................................................................................3

2.4 Accounting Policy............................................................................................................4

2.5 Related Parties and Transaction with Related Parties......................................................5

Part B: Analysis of the Client and Impacts on the Future Audit Works....................................8

2.6 Changes in Accounting Policies and the Impact of Changes...........................................8

2.7 Preliminary Analytical Procedures..................................................................................9

2.8 Measurement and Review of Financial Performance....................................................10

2.9 Objectives, Strategies and Related Business Risks........................................................11

3. Conclusion............................................................................................................................11

References................................................................................................................................13

2AUDIT STRATEGY

1. Introduction

Auditing is considered as the systematic and methodical process of inspecting as well

as examining the financial statements of the companies in order to make sure that there is not

any material misstatements in them (Louwers et al. 2015). Before commencing the audit

works, it is needed for the auditors to chalk out the audit strategy in detailed manner. An

Audit Strategy sets the direction, timing as well as scope of the audit work and the auditors

use the audit strategy as a parameter for the development of audit plan (Knechel and Salterio

2016). For this reason, the auditors are needed to include the key decision required in the

audit strategy document for effective planning of auditing. At the time to develop the audit

strategy, an auditor is needed to consider the methodical analysis of the audit client that

includes the analysis and evaluation of business, industry, external factors, nature, accounting

policies, change in accounting policies, objectives, strategies and business risks of the audit

client. Information about all these aspects provides the auditor with the necessary direction to

plan the audit procedures (Byrnes et al. 2018). The main aim of this report is to gain

understanding about the audit client that is Telstra Corporation Limited (Telstra) so that

effective audit strategy can be developed for the company for the 2017 to 2018 financial year.

Part A: The Client

2.1 Information about the Client

Name: Telstra Corporation Limited

Address: 242 Exhibition Street, Level 41, Melbourne, VIC 3000, Australia

Year of Establishment: 1901

Field of Operations: Telstra Corporation Limited is the provider is the provider of

telecommunication services to businesses, governments, communities and individuals in

Australia as well as internationally. The company has operations in four segments; they are

Telstra Consumer and Small Businesses, Telstra Operations, Telstra Enterprise and Telstra

Wholesale. Telstra provides their customers with telecommunication products, services as

well as solutions through mobiles, telephones, broadband services and others.

Period of Financial Report Period under Consideration: 1st July 2017 to 30th June 2018

Types of Financial Report: Consolidated

1. Introduction

Auditing is considered as the systematic and methodical process of inspecting as well

as examining the financial statements of the companies in order to make sure that there is not

any material misstatements in them (Louwers et al. 2015). Before commencing the audit

works, it is needed for the auditors to chalk out the audit strategy in detailed manner. An

Audit Strategy sets the direction, timing as well as scope of the audit work and the auditors

use the audit strategy as a parameter for the development of audit plan (Knechel and Salterio

2016). For this reason, the auditors are needed to include the key decision required in the

audit strategy document for effective planning of auditing. At the time to develop the audit

strategy, an auditor is needed to consider the methodical analysis of the audit client that

includes the analysis and evaluation of business, industry, external factors, nature, accounting

policies, change in accounting policies, objectives, strategies and business risks of the audit

client. Information about all these aspects provides the auditor with the necessary direction to

plan the audit procedures (Byrnes et al. 2018). The main aim of this report is to gain

understanding about the audit client that is Telstra Corporation Limited (Telstra) so that

effective audit strategy can be developed for the company for the 2017 to 2018 financial year.

Part A: The Client

2.1 Information about the Client

Name: Telstra Corporation Limited

Address: 242 Exhibition Street, Level 41, Melbourne, VIC 3000, Australia

Year of Establishment: 1901

Field of Operations: Telstra Corporation Limited is the provider is the provider of

telecommunication services to businesses, governments, communities and individuals in

Australia as well as internationally. The company has operations in four segments; they are

Telstra Consumer and Small Businesses, Telstra Operations, Telstra Enterprise and Telstra

Wholesale. Telstra provides their customers with telecommunication products, services as

well as solutions through mobiles, telephones, broadband services and others.

Period of Financial Report Period under Consideration: 1st July 2017 to 30th June 2018

Types of Financial Report: Consolidated

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT STRATEGY

2.2 Industry, Regulatory and Other External Factors

The Australian economy has taken an upturn on in the fourth quarter of the last year

after an unsatisfactory third quarter and it is expected that this robust growth is expected to

continue in the coming year. After that, the Australian telecommunication industry is

expected to grow in the next five years. Other key developments are decline in fixed-line

DSL broadband, growth in second tier market, slow growth in mobile subscriptions and

others (focus-economics.com 2019).

The laws and regulations applicable to Telstra are industry specific competition

regulation, consumer protection regulation and industry codes and standards under a self-

regulatory regime. Telstra is needed to comply with all the regulations introduced by The

Communication Minister and the Communication Minister’s Department.

Increase in competition can be seen in the Australian telecommunication industry due

to the deregulation of the industry in 1997, but Telstra has been able in maintaining their

dominant position in the industry. The major competitors of Telstra are Optus, AAPT,

Primus, Orange and Vodafone.

The Australian government provides funding support to the Australian

telecommunication industry for their overall growth. At the same time, the Australian

government also supports the telecommunication industry in the policy making process

(communications.gov.au 2019).

Increase in revenue from wireless services can be seen in the Australian

telecommunication industry due to the rise in consumption volume of mobile data along with

improved mobile connectivity. However, decrease in demand can be seen in fixed line

services (ibisworld.com.au 2019).

Even after the deregulation of the Australian telecommunication industry, there are

certain entry barriers for the new companies. The new entrants need to bear huge set-up cost

for the new business in this industry that need huge capital. After that, new companies are

needed to invest hugely for the adoption of new technologies for their business (Fontagné and

Mitaritonna 2013).

2.3 Nature of the Client

Telstra Corporation Limited is the provider is the provider of telecommunication

services to businesses, governments, communities and individuals in Australia as well as

2.2 Industry, Regulatory and Other External Factors

The Australian economy has taken an upturn on in the fourth quarter of the last year

after an unsatisfactory third quarter and it is expected that this robust growth is expected to

continue in the coming year. After that, the Australian telecommunication industry is

expected to grow in the next five years. Other key developments are decline in fixed-line

DSL broadband, growth in second tier market, slow growth in mobile subscriptions and

others (focus-economics.com 2019).

The laws and regulations applicable to Telstra are industry specific competition

regulation, consumer protection regulation and industry codes and standards under a self-

regulatory regime. Telstra is needed to comply with all the regulations introduced by The

Communication Minister and the Communication Minister’s Department.

Increase in competition can be seen in the Australian telecommunication industry due

to the deregulation of the industry in 1997, but Telstra has been able in maintaining their

dominant position in the industry. The major competitors of Telstra are Optus, AAPT,

Primus, Orange and Vodafone.

The Australian government provides funding support to the Australian

telecommunication industry for their overall growth. At the same time, the Australian

government also supports the telecommunication industry in the policy making process

(communications.gov.au 2019).

Increase in revenue from wireless services can be seen in the Australian

telecommunication industry due to the rise in consumption volume of mobile data along with

improved mobile connectivity. However, decrease in demand can be seen in fixed line

services (ibisworld.com.au 2019).

Even after the deregulation of the Australian telecommunication industry, there are

certain entry barriers for the new companies. The new entrants need to bear huge set-up cost

for the new business in this industry that need huge capital. After that, new companies are

needed to invest hugely for the adoption of new technologies for their business (Fontagné and

Mitaritonna 2013).

2.3 Nature of the Client

Telstra Corporation Limited is the provider is the provider of telecommunication

services to businesses, governments, communities and individuals in Australia as well as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT STRATEGY

internationally. The company has operations in four segments; they are Telstra Consumer and

Small Businesses, Telstra Operations, Telstra Enterprise and Telstra Wholesale. Telstra

provides their customers with telecommunication products, services as well as solutions

through mobiles, telephones, broadband services and others (telstra.com.au 2019).

It needs to be mentioned that Telstra has a large customer base and the company has

segregated their customer base in a well manner. In Australia, Telstra has 17.7 million

customers for the retail mobile service, 4.9 million customers for retail fixed voice services

and 3.6 million customers for retail fixed broadband services (telstra.com.au 2019).

It can be seen from the above that Telstra has certain increased dependency on the

customers for the retail mobile services as it consists of the majority portion of the customer

base.

Telstra has certain major suppliers who supply the company with many things like

office equipment to uniform, coffee to stationary, cables of buildings along with servers to

satellite capacity. For this reason, the major suppliers of Telstra are businesses across

Australia and overseas that includes small companies, companies from remote areas and large

corporations (telstra.com.au 2019).

As per the ownership structure, Telstra falls under Corporation. Telstra adheres to the

third edition of the ASX Corporate Governance Council’s Corporate Governance Principles

and Recommendations (ASX Recommendations) for the purpose of corporate governance.

The board size of Telstra is 11. The company has four committees; they are Board Charter,

Audit and Risk Committee Charter, Remuneration Committee Charter and Nomination

Committee Charter (telstra.com.au 2019).

Telstra has a total of 360 retail stores across the regions of Australia. In addition, the

company has retail stores in many other countries like United States, United Kingdom,

Indonesia, Singapore, Malaysia, Philippines, India, China, Taiwan, Hong Kong and others

(telstra.com.au 2019).

2.4 Accounting Policy

Property, Plant and Equipment: As per the accounting policies of Telstra, the company has

reported and recorded the property, plant and equipment at cost less accumulated

depreciation. Hence, the company has adopted the cost model (telstra.com.au 2019).

internationally. The company has operations in four segments; they are Telstra Consumer and

Small Businesses, Telstra Operations, Telstra Enterprise and Telstra Wholesale. Telstra

provides their customers with telecommunication products, services as well as solutions

through mobiles, telephones, broadband services and others (telstra.com.au 2019).

It needs to be mentioned that Telstra has a large customer base and the company has

segregated their customer base in a well manner. In Australia, Telstra has 17.7 million

customers for the retail mobile service, 4.9 million customers for retail fixed voice services

and 3.6 million customers for retail fixed broadband services (telstra.com.au 2019).

It can be seen from the above that Telstra has certain increased dependency on the

customers for the retail mobile services as it consists of the majority portion of the customer

base.

Telstra has certain major suppliers who supply the company with many things like

office equipment to uniform, coffee to stationary, cables of buildings along with servers to

satellite capacity. For this reason, the major suppliers of Telstra are businesses across

Australia and overseas that includes small companies, companies from remote areas and large

corporations (telstra.com.au 2019).

As per the ownership structure, Telstra falls under Corporation. Telstra adheres to the

third edition of the ASX Corporate Governance Council’s Corporate Governance Principles

and Recommendations (ASX Recommendations) for the purpose of corporate governance.

The board size of Telstra is 11. The company has four committees; they are Board Charter,

Audit and Risk Committee Charter, Remuneration Committee Charter and Nomination

Committee Charter (telstra.com.au 2019).

Telstra has a total of 360 retail stores across the regions of Australia. In addition, the

company has retail stores in many other countries like United States, United Kingdom,

Indonesia, Singapore, Malaysia, Philippines, India, China, Taiwan, Hong Kong and others

(telstra.com.au 2019).

2.4 Accounting Policy

Property, Plant and Equipment: As per the accounting policies of Telstra, the company has

reported and recorded the property, plant and equipment at cost less accumulated

depreciation. Hence, the company has adopted the cost model (telstra.com.au 2019).

5AUDIT STRATEGY

Inventory: As per the 2018 Annual Report of Telstra, the company has valued their inventory

at the lower of cost and net realizable value. For the majority items of the inventory, Telstra

assigns cost by using the weighted average cost basis. Hence, the company has adopted

average basis for inventory (telstra.com.au 2019).

Accounts Receivable: Telstra considers accounts receivable as financial assets. As per the

accounting policies, the company measures them on the basis of fair value and they are

subsequently measures at amortized costs with the use of effective interest method. Hence,

the company used fair value method for the measurement of accounts receivable

(telstra.com.au 2019).

Financial Instrument: As per the 2018 Annual Report of Telstra, the company has complied

with the principles and regulations of AASB 9 Financial Instrument. Hence, Telstra

recognizes a financial asset or financial liability in the balance sheet when the company

becomes party to the promised provision of the instrument (aasb.gov.au 2019).

Intangible Assets: Telstra measures their goodwill at the cost basis. After that, the company

amortizes their internally generated intangible assets on the basis of straight-line over their

useful life. After that, Telstra records their acquired intangible assets on the basis of fair value

at the date of acquisition (telstra.com.au 2019).

Revenue Recognition: The main sources of revenue in Telstra are revenue from rendering of

services, sales of goods, construction contracts, lease income, grants from government and

interest income. In Telstra, revenue characterises the fair value of the received consideration

or receivable. The company records the revenue net of sales return, trade allowance, sales

incentives, discounts, taxes and duties (telstra.com.au 2019).

2.5 Related Parties and Transaction with Related Parties

It can be seen from the 2018 Annual Report of Telstra that the company has certain

controlled entities with certain percentage of financial benefits; it can be seen in below:

Inventory: As per the 2018 Annual Report of Telstra, the company has valued their inventory

at the lower of cost and net realizable value. For the majority items of the inventory, Telstra

assigns cost by using the weighted average cost basis. Hence, the company has adopted

average basis for inventory (telstra.com.au 2019).

Accounts Receivable: Telstra considers accounts receivable as financial assets. As per the

accounting policies, the company measures them on the basis of fair value and they are

subsequently measures at amortized costs with the use of effective interest method. Hence,

the company used fair value method for the measurement of accounts receivable

(telstra.com.au 2019).

Financial Instrument: As per the 2018 Annual Report of Telstra, the company has complied

with the principles and regulations of AASB 9 Financial Instrument. Hence, Telstra

recognizes a financial asset or financial liability in the balance sheet when the company

becomes party to the promised provision of the instrument (aasb.gov.au 2019).

Intangible Assets: Telstra measures their goodwill at the cost basis. After that, the company

amortizes their internally generated intangible assets on the basis of straight-line over their

useful life. After that, Telstra records their acquired intangible assets on the basis of fair value

at the date of acquisition (telstra.com.au 2019).

Revenue Recognition: The main sources of revenue in Telstra are revenue from rendering of

services, sales of goods, construction contracts, lease income, grants from government and

interest income. In Telstra, revenue characterises the fair value of the received consideration

or receivable. The company records the revenue net of sales return, trade allowance, sales

incentives, discounts, taxes and duties (telstra.com.au 2019).

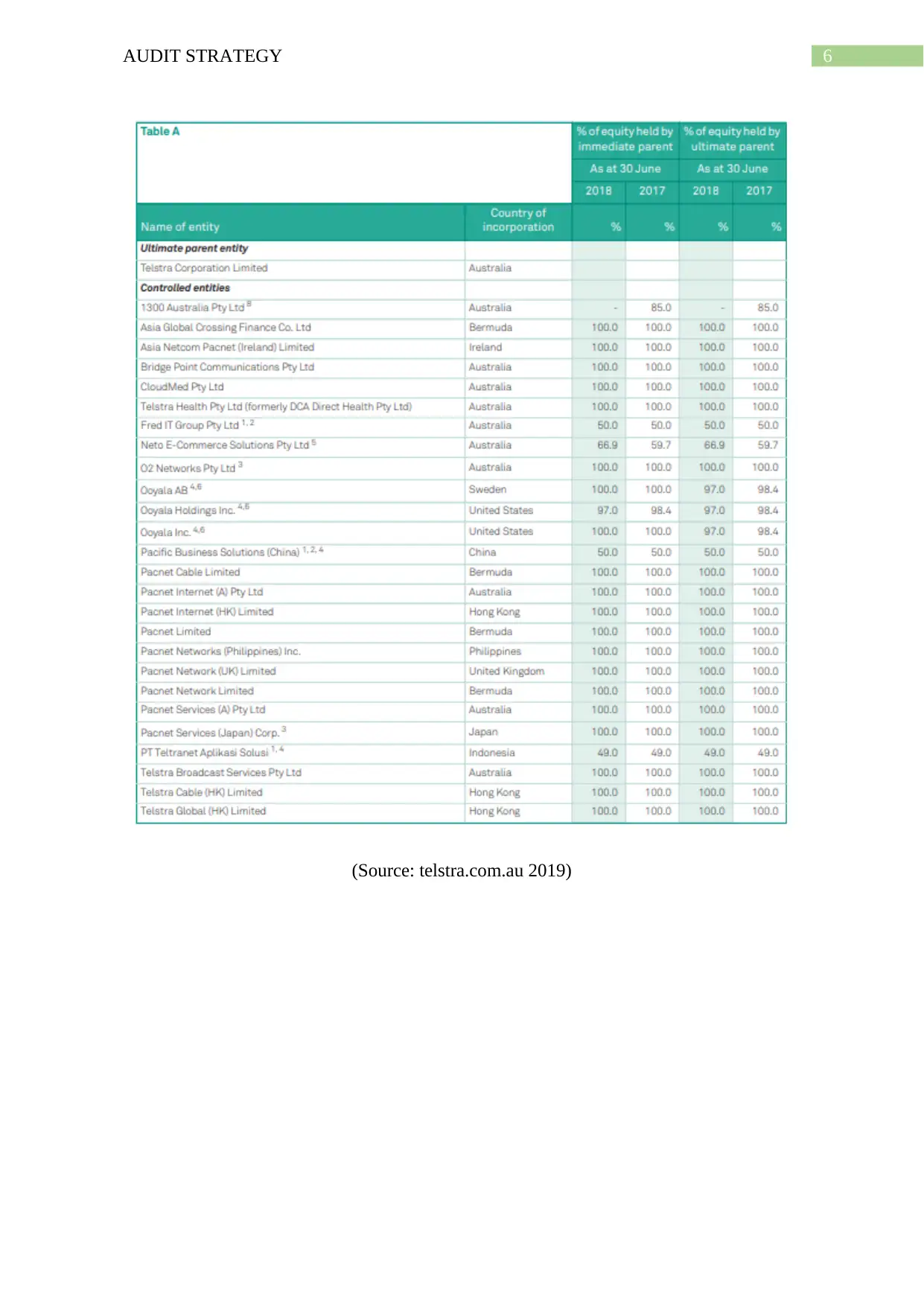

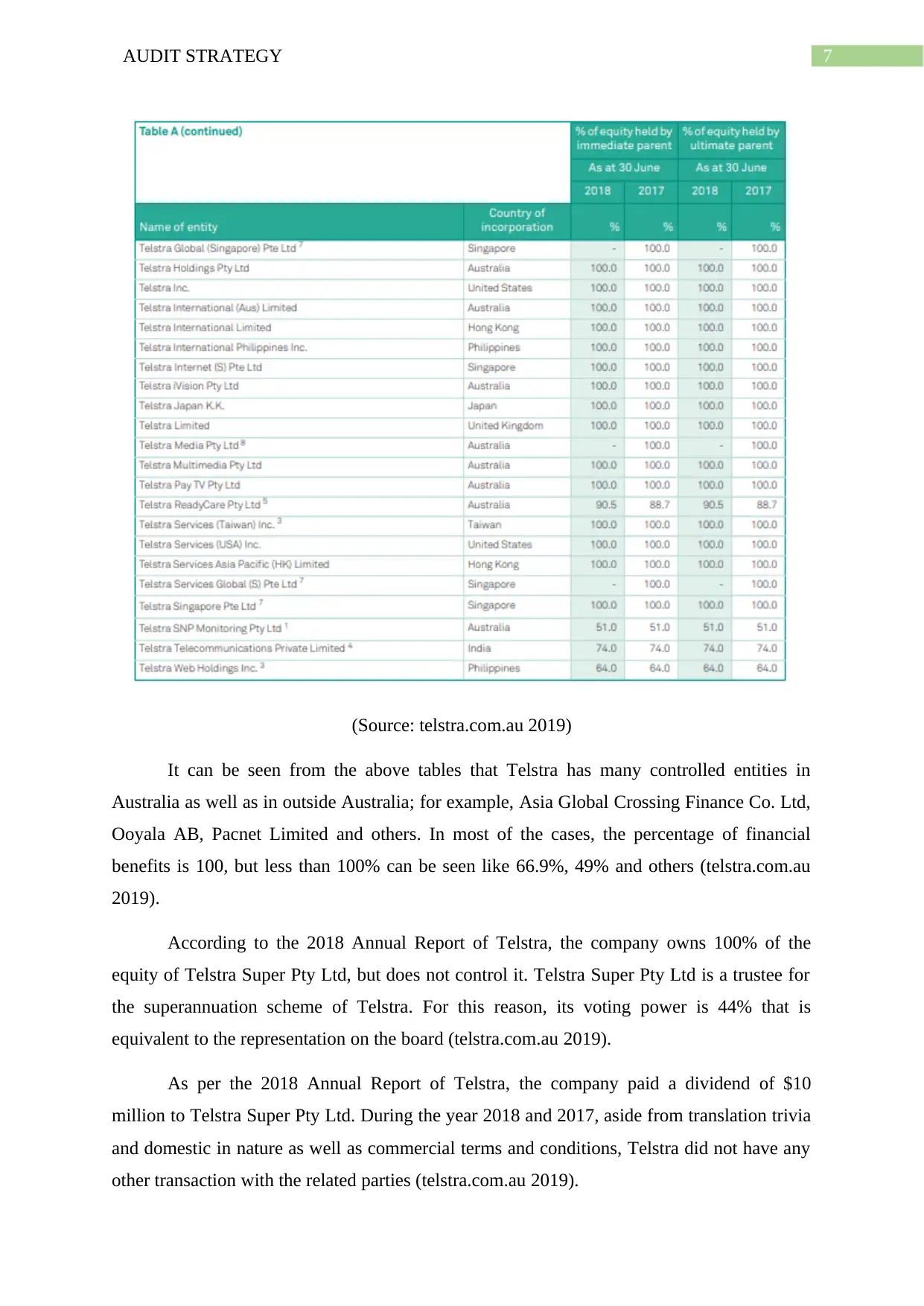

2.5 Related Parties and Transaction with Related Parties

It can be seen from the 2018 Annual Report of Telstra that the company has certain

controlled entities with certain percentage of financial benefits; it can be seen in below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT STRATEGY

(Source: telstra.com.au 2019)

(Source: telstra.com.au 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT STRATEGY

(Source: telstra.com.au 2019)

It can be seen from the above tables that Telstra has many controlled entities in

Australia as well as in outside Australia; for example, Asia Global Crossing Finance Co. Ltd,

Ooyala AB, Pacnet Limited and others. In most of the cases, the percentage of financial

benefits is 100, but less than 100% can be seen like 66.9%, 49% and others (telstra.com.au

2019).

According to the 2018 Annual Report of Telstra, the company owns 100% of the

equity of Telstra Super Pty Ltd, but does not control it. Telstra Super Pty Ltd is a trustee for

the superannuation scheme of Telstra. For this reason, its voting power is 44% that is

equivalent to the representation on the board (telstra.com.au 2019).

As per the 2018 Annual Report of Telstra, the company paid a dividend of $10

million to Telstra Super Pty Ltd. During the year 2018 and 2017, aside from translation trivia

and domestic in nature as well as commercial terms and conditions, Telstra did not have any

other transaction with the related parties (telstra.com.au 2019).

(Source: telstra.com.au 2019)

It can be seen from the above tables that Telstra has many controlled entities in

Australia as well as in outside Australia; for example, Asia Global Crossing Finance Co. Ltd,

Ooyala AB, Pacnet Limited and others. In most of the cases, the percentage of financial

benefits is 100, but less than 100% can be seen like 66.9%, 49% and others (telstra.com.au

2019).

According to the 2018 Annual Report of Telstra, the company owns 100% of the

equity of Telstra Super Pty Ltd, but does not control it. Telstra Super Pty Ltd is a trustee for

the superannuation scheme of Telstra. For this reason, its voting power is 44% that is

equivalent to the representation on the board (telstra.com.au 2019).

As per the 2018 Annual Report of Telstra, the company paid a dividend of $10

million to Telstra Super Pty Ltd. During the year 2018 and 2017, aside from translation trivia

and domestic in nature as well as commercial terms and conditions, Telstra did not have any

other transaction with the related parties (telstra.com.au 2019).

8AUDIT STRATEGY

Part B: Analysis of the Client and Impacts on the Future Audit Works

2.6 Changes in Accounting Policies and the Impact of Changes

According to the 2018 Annual Report of Telstra, there are certain changes in the

accounting policies that can have impact on the financial reporting. AASB has issued the

final version of AASB 9 Financial Instruments (AASB 9 (2014)) (telstra.com.au 2019).

Telstra early adopted the old version of this standards that is AASB 9 (2013), but now they

are needed to adopt AASB 9 (2014). The absence of impairment section can be seen in the

new version that replaces the model of incurred loss impairment with an expected credit loss

(telstra.com.au 2019). As an impact, Telstra will need to record expected credit loss on the

financial assets. After that, Telstra will have to apply the new revenue recognition standard of

AASB 15 Revenue from Contracts with Customers (telstra.com.au 2019). As an impact of

this, Telstra will be needed to recognize the revenue in such a way that portrays the promised

goods transfer to a customer and an amount reflecting the expected consideration to be

received. After that, Telstra will be needed to adopt AASB 16 Leases in the place of AASB

117 Leases; and as the effect, Telstra will be needed to recognize the lease liabilities and

right-to-use assets in the financial statements (telstra.com.au 2019). Lastly, Telstra will be

needed to adopt the revised Conceptual Framework for Financial Reporting issued by the

International Accounting Standards Board as the old one did not cover some of the crucial

areas of financial reporting.

The main aim of AASB and IASB behind bringing these changes in the above-

mentioned accounting standards is to cover the areas that were uncovered by the previous

accounting standards. For this reason, these changes in accounting policies will strengthen the

accounting standards in future by improving the crucial areas of financial reporting. For this,

the users will be able in gaining more accurate financial information of the companies

(Henderson et al. 2015).

These changes in the accounting policies will increase the work of the auditors due to

the fact that the auditors will be needed to analyse certain more elements of financial

reporting. For example, for the introduction of AASB 16, it will be needed for the auditors to

analyse whether the companies have recognized their lease liabilities and right-to-use assets

in the balance sheet. After that, with the adoption of AASB 9 (2014), the auditors will be

needed to analyse whether the companies have reported expected credit loss for their assets.

Hence, these will affect the future audit work (Okolie 2014).

Part B: Analysis of the Client and Impacts on the Future Audit Works

2.6 Changes in Accounting Policies and the Impact of Changes

According to the 2018 Annual Report of Telstra, there are certain changes in the

accounting policies that can have impact on the financial reporting. AASB has issued the

final version of AASB 9 Financial Instruments (AASB 9 (2014)) (telstra.com.au 2019).

Telstra early adopted the old version of this standards that is AASB 9 (2013), but now they

are needed to adopt AASB 9 (2014). The absence of impairment section can be seen in the

new version that replaces the model of incurred loss impairment with an expected credit loss

(telstra.com.au 2019). As an impact, Telstra will need to record expected credit loss on the

financial assets. After that, Telstra will have to apply the new revenue recognition standard of

AASB 15 Revenue from Contracts with Customers (telstra.com.au 2019). As an impact of

this, Telstra will be needed to recognize the revenue in such a way that portrays the promised

goods transfer to a customer and an amount reflecting the expected consideration to be

received. After that, Telstra will be needed to adopt AASB 16 Leases in the place of AASB

117 Leases; and as the effect, Telstra will be needed to recognize the lease liabilities and

right-to-use assets in the financial statements (telstra.com.au 2019). Lastly, Telstra will be

needed to adopt the revised Conceptual Framework for Financial Reporting issued by the

International Accounting Standards Board as the old one did not cover some of the crucial

areas of financial reporting.

The main aim of AASB and IASB behind bringing these changes in the above-

mentioned accounting standards is to cover the areas that were uncovered by the previous

accounting standards. For this reason, these changes in accounting policies will strengthen the

accounting standards in future by improving the crucial areas of financial reporting. For this,

the users will be able in gaining more accurate financial information of the companies

(Henderson et al. 2015).

These changes in the accounting policies will increase the work of the auditors due to

the fact that the auditors will be needed to analyse certain more elements of financial

reporting. For example, for the introduction of AASB 16, it will be needed for the auditors to

analyse whether the companies have recognized their lease liabilities and right-to-use assets

in the balance sheet. After that, with the adoption of AASB 9 (2014), the auditors will be

needed to analyse whether the companies have reported expected credit loss for their assets.

Hence, these will affect the future audit work (Okolie 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT STRATEGY

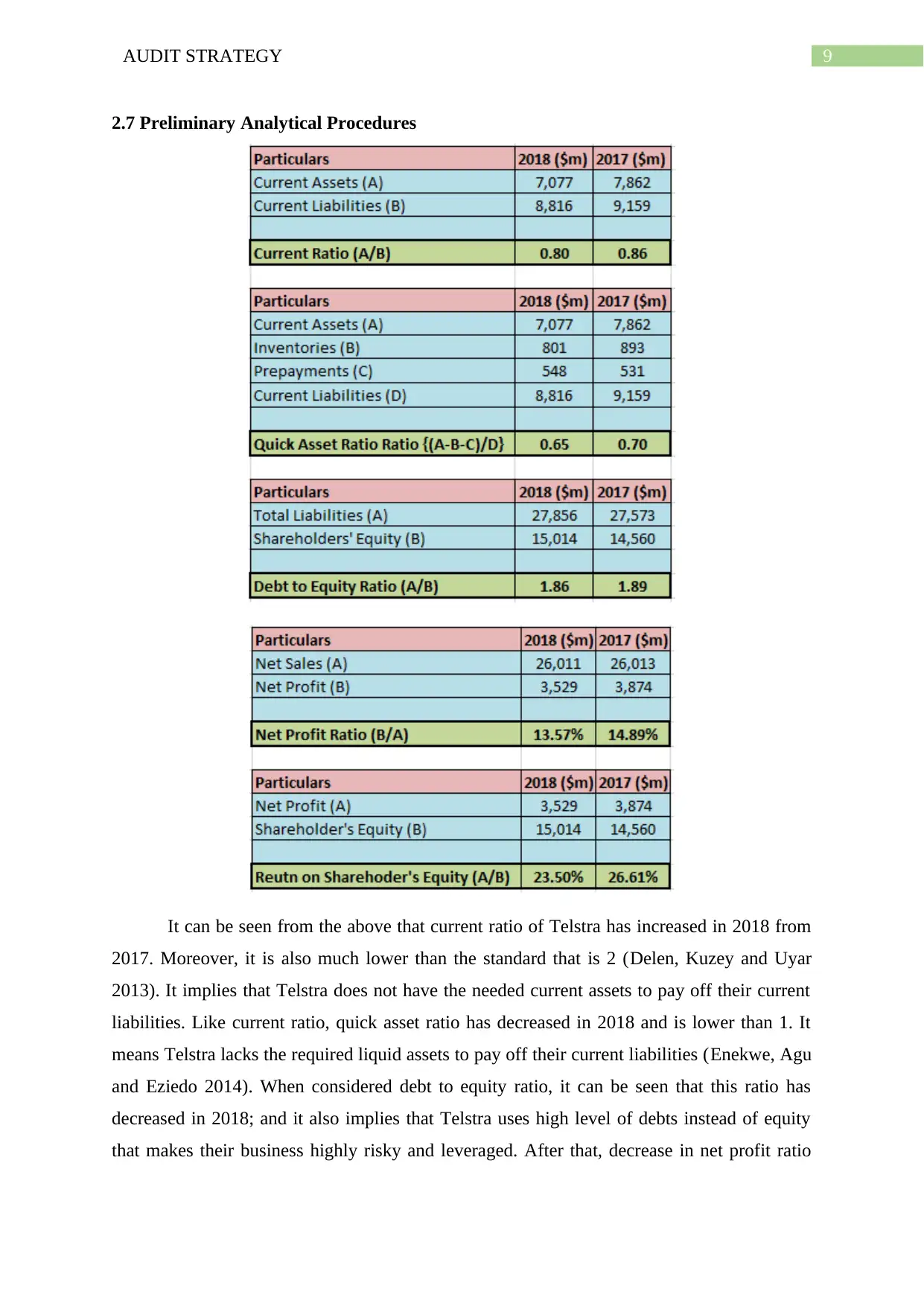

2.7 Preliminary Analytical Procedures

It can be seen from the above that current ratio of Telstra has increased in 2018 from

2017. Moreover, it is also much lower than the standard that is 2 (Delen, Kuzey and Uyar

2013). It implies that Telstra does not have the needed current assets to pay off their current

liabilities. Like current ratio, quick asset ratio has decreased in 2018 and is lower than 1. It

means Telstra lacks the required liquid assets to pay off their current liabilities (Enekwe, Agu

and Eziedo 2014). When considered debt to equity ratio, it can be seen that this ratio has

decreased in 2018; and it also implies that Telstra uses high level of debts instead of equity

that makes their business highly risky and leveraged. After that, decrease in net profit ratio

2.7 Preliminary Analytical Procedures

It can be seen from the above that current ratio of Telstra has increased in 2018 from

2017. Moreover, it is also much lower than the standard that is 2 (Delen, Kuzey and Uyar

2013). It implies that Telstra does not have the needed current assets to pay off their current

liabilities. Like current ratio, quick asset ratio has decreased in 2018 and is lower than 1. It

means Telstra lacks the required liquid assets to pay off their current liabilities (Enekwe, Agu

and Eziedo 2014). When considered debt to equity ratio, it can be seen that this ratio has

decreased in 2018; and it also implies that Telstra uses high level of debts instead of equity

that makes their business highly risky and leveraged. After that, decrease in net profit ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT STRATEGY

can be seen in 2018 due to the decrease in net profit and sales. In addition, 2018 witnessed

decrease in return on shareholders’ equity (Waworuntu, Wantah and Rusmanto 2014).

It can be seen that all these ratios of Telstra are showing decreasing financial

performance of the company in 2018. Since these ratios are not in accordance with the

expectation of the auditors, the auditors will be needed to put significant audit attention to

these aspects as there could be the presence of material misstatements in the financial

statements of Telstra. At the same time, the auditors will be needed to compare the outcome

of these ratios with average ratios in the industries listed in ASX and internal data of previous

year, budget and segment data. Hence, these will increase the future audit work (Newton

2013).

As per the outcome of the ratio analysis, Telstra has a weak liquidity position that

shown the inability of the company to pay off their current liabilities. In addition, there is

decrease in profitability and return on shareholder’s equity (Provasi and Riva 2015). In

addition, the business of Telstra is highly risky as well as highly leveraged in the presence of

huge amount of debts. All these negative aspects raise the question about the ability of Telstra

to continue as going concern. Thus, there are certain major doubts about the going concern

status of Telstra (Shvyreva and Kruglyak 2016).

2.8 Measurement and Review of Financial Performance

According to the 2018 Annual Report of Telstra, the company has employed certain

mechanism to measure the performance of their directors with the aim to provide them with

the correct amount of remuneration (telstra.com.au 2019). The directors of Telstra are

provided with Fixed Remuneration and Executive Variable Remuneration Plan (EVP). Fixed

remuneration is paid in cash as basic salary plus superannuation; and EVP is provided with

both cash and equity. The performance is measured based on financial aspect, customer

aspect and individual aspect. The weightage is 10% of total income, 20% of EBITDA, 20%

of FCF, 20% of Episode NPS, 20% of Strategic NPS and 10% of Individual Performance

(telstra.com.au 2019). As per the financial performance of Telstra, total income has increased

in 2018 from 2017 and the same aspect can be seen in case of EBITDA. However, decrease

in net profit can be seen in 2018 from 2017. Share price decreased in 2018 from 2017; and

the company paid less amount of dividend per share in 2018 due to the decrease in net profit.

In addition, it can be seen that Telstra maintain a gearing ratio of 50 to 70% for the non-

current borrowings (telstra.com.au 2019).

can be seen in 2018 due to the decrease in net profit and sales. In addition, 2018 witnessed

decrease in return on shareholders’ equity (Waworuntu, Wantah and Rusmanto 2014).

It can be seen that all these ratios of Telstra are showing decreasing financial

performance of the company in 2018. Since these ratios are not in accordance with the

expectation of the auditors, the auditors will be needed to put significant audit attention to

these aspects as there could be the presence of material misstatements in the financial

statements of Telstra. At the same time, the auditors will be needed to compare the outcome

of these ratios with average ratios in the industries listed in ASX and internal data of previous

year, budget and segment data. Hence, these will increase the future audit work (Newton

2013).

As per the outcome of the ratio analysis, Telstra has a weak liquidity position that

shown the inability of the company to pay off their current liabilities. In addition, there is

decrease in profitability and return on shareholder’s equity (Provasi and Riva 2015). In

addition, the business of Telstra is highly risky as well as highly leveraged in the presence of

huge amount of debts. All these negative aspects raise the question about the ability of Telstra

to continue as going concern. Thus, there are certain major doubts about the going concern

status of Telstra (Shvyreva and Kruglyak 2016).

2.8 Measurement and Review of Financial Performance

According to the 2018 Annual Report of Telstra, the company has employed certain

mechanism to measure the performance of their directors with the aim to provide them with

the correct amount of remuneration (telstra.com.au 2019). The directors of Telstra are

provided with Fixed Remuneration and Executive Variable Remuneration Plan (EVP). Fixed

remuneration is paid in cash as basic salary plus superannuation; and EVP is provided with

both cash and equity. The performance is measured based on financial aspect, customer

aspect and individual aspect. The weightage is 10% of total income, 20% of EBITDA, 20%

of FCF, 20% of Episode NPS, 20% of Strategic NPS and 10% of Individual Performance

(telstra.com.au 2019). As per the financial performance of Telstra, total income has increased

in 2018 from 2017 and the same aspect can be seen in case of EBITDA. However, decrease

in net profit can be seen in 2018 from 2017. Share price decreased in 2018 from 2017; and

the company paid less amount of dividend per share in 2018 due to the decrease in net profit.

In addition, it can be seen that Telstra maintain a gearing ratio of 50 to 70% for the non-

current borrowings (telstra.com.au 2019).

11AUDIT STRATEGY

Hence, the auditor of Telstra is needed to consider all these above aspects in their

auditing works. For example, the auditor needs to ascertain the fact that whether the

remuneration is paid to the directors as per the remuneration structure while considering the

achievements and non-achievement of financial goals. After that, the auditor is also needed to

ensure that whether Telstra has maintained a gearing ratio of 50% to 70% for raising capital

through non-current borrowings. In case the auditor is not satisfied with the outcomes, they

need to put special audit consideration to these aspects (Bing et al. 2014).

2.9 Objectives, Strategies and Related Business Risks

The main strategy of Telstra is to expand their business in Australia and

internationally. The company is considering implementation of program for efficiently use

assets, to improve distribution capabilities and improve productivity in delivering the

products and services. For this, the focus of Telstra is on the sales and marketing activities so

that costs can be controlled and services to the customers can be improved (telstra.com.au

2019).

As per the 2018 Annual Report, the business activities of Telstra are exposed to

certain risks; they are interest rate risk, foreign currency risk, credit risk and liquidity risk. It

needs to be mentioned that these risks include both internal as well as external forces creating

difficulties for the company to attain the strategic objectives and business goals (Belás et al.

2014).

It is the responsibility of the auditor of Telstra to take into consideration these

business risks for ascertaining whether these risks can create material misstatements in the

financial statements of Telstra or not. For this reason, the audit works will include the

analysis and examination of the relevant financial statements and figures related to these risks

with the aim to measure their impact on the financial statements and financial outcomes of

Telstra (Kilgore, Harrison and Radich 2014).

3. Conclusion

It can be seen from the above discussion that the auditors are needed to take into

account many aspects at the time of the development of audit strategies. In case of Telstra,

the auditor of the company must acquire understanding about various aspects of the client’s

business such as nature of the industry, accounting policies and others; and this acquired

understanding provides the auditor with the directors in developing the audit strategy. In this

process, the auditor is needed to examine employed accounting policies by Telstra for the

Hence, the auditor of Telstra is needed to consider all these above aspects in their

auditing works. For example, the auditor needs to ascertain the fact that whether the

remuneration is paid to the directors as per the remuneration structure while considering the

achievements and non-achievement of financial goals. After that, the auditor is also needed to

ensure that whether Telstra has maintained a gearing ratio of 50% to 70% for raising capital

through non-current borrowings. In case the auditor is not satisfied with the outcomes, they

need to put special audit consideration to these aspects (Bing et al. 2014).

2.9 Objectives, Strategies and Related Business Risks

The main strategy of Telstra is to expand their business in Australia and

internationally. The company is considering implementation of program for efficiently use

assets, to improve distribution capabilities and improve productivity in delivering the

products and services. For this, the focus of Telstra is on the sales and marketing activities so

that costs can be controlled and services to the customers can be improved (telstra.com.au

2019).

As per the 2018 Annual Report, the business activities of Telstra are exposed to

certain risks; they are interest rate risk, foreign currency risk, credit risk and liquidity risk. It

needs to be mentioned that these risks include both internal as well as external forces creating

difficulties for the company to attain the strategic objectives and business goals (Belás et al.

2014).

It is the responsibility of the auditor of Telstra to take into consideration these

business risks for ascertaining whether these risks can create material misstatements in the

financial statements of Telstra or not. For this reason, the audit works will include the

analysis and examination of the relevant financial statements and figures related to these risks

with the aim to measure their impact on the financial statements and financial outcomes of

Telstra (Kilgore, Harrison and Radich 2014).

3. Conclusion

It can be seen from the above discussion that the auditors are needed to take into

account many aspects at the time of the development of audit strategies. In case of Telstra,

the auditor of the company must acquire understanding about various aspects of the client’s

business such as nature of the industry, accounting policies and others; and this acquired

understanding provides the auditor with the directors in developing the audit strategy. In this

process, the auditor is needed to examine employed accounting policies by Telstra for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.