Telstra Corporation: A Strategic Analysis of Capital Restructuring

VerifiedAdded on 2023/04/21

|24

|1735

|422

Presentation

AI Summary

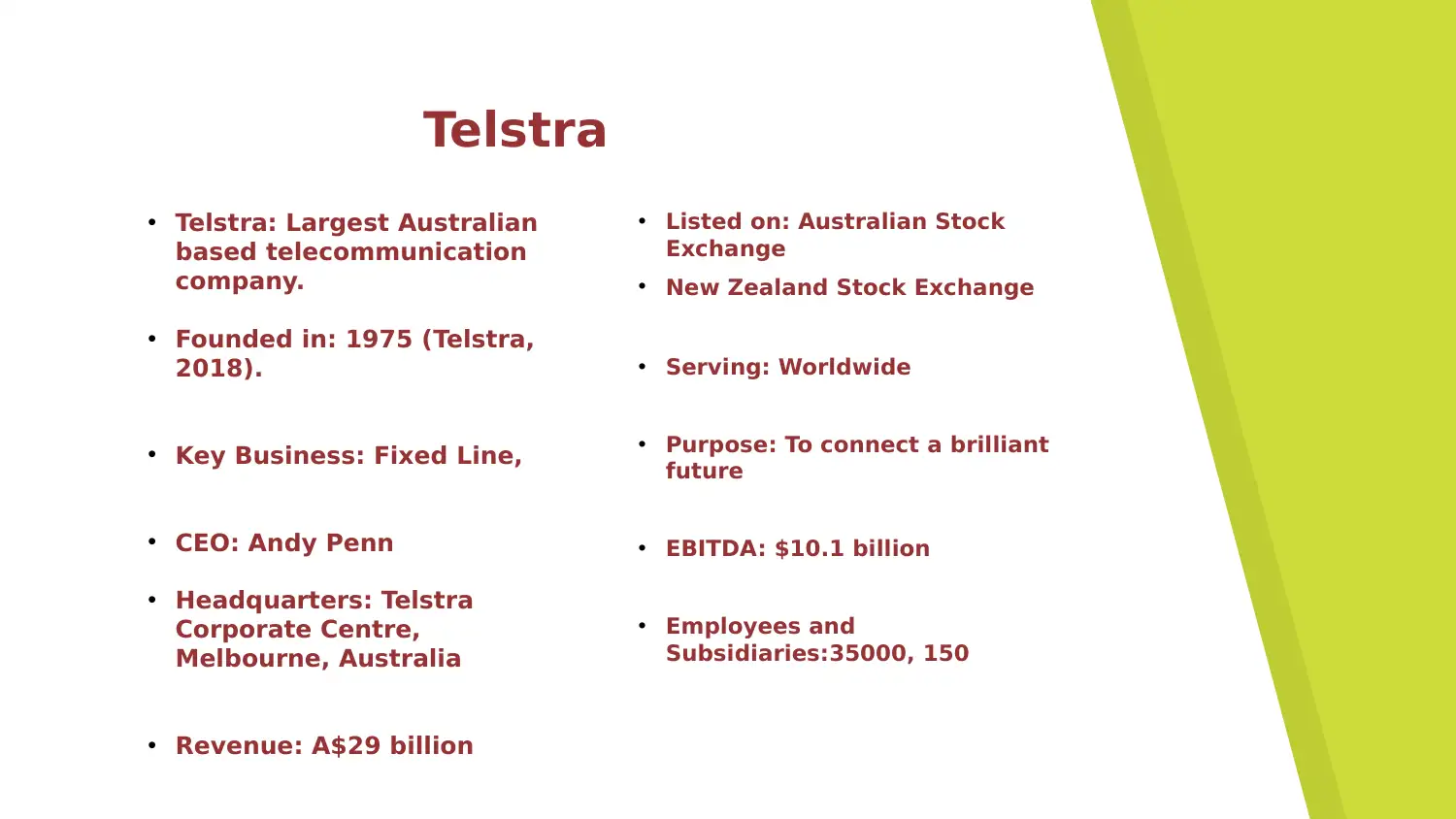

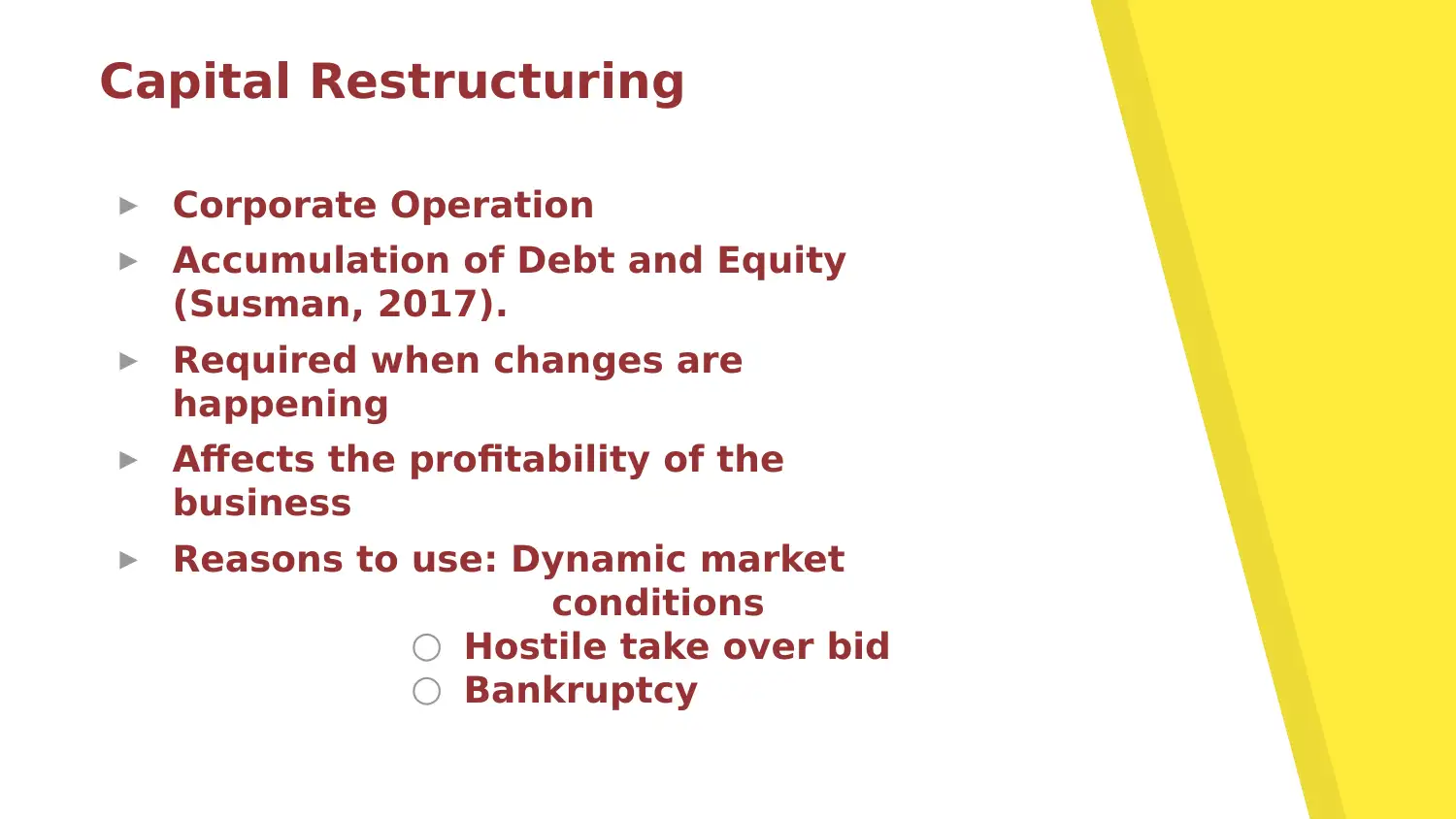

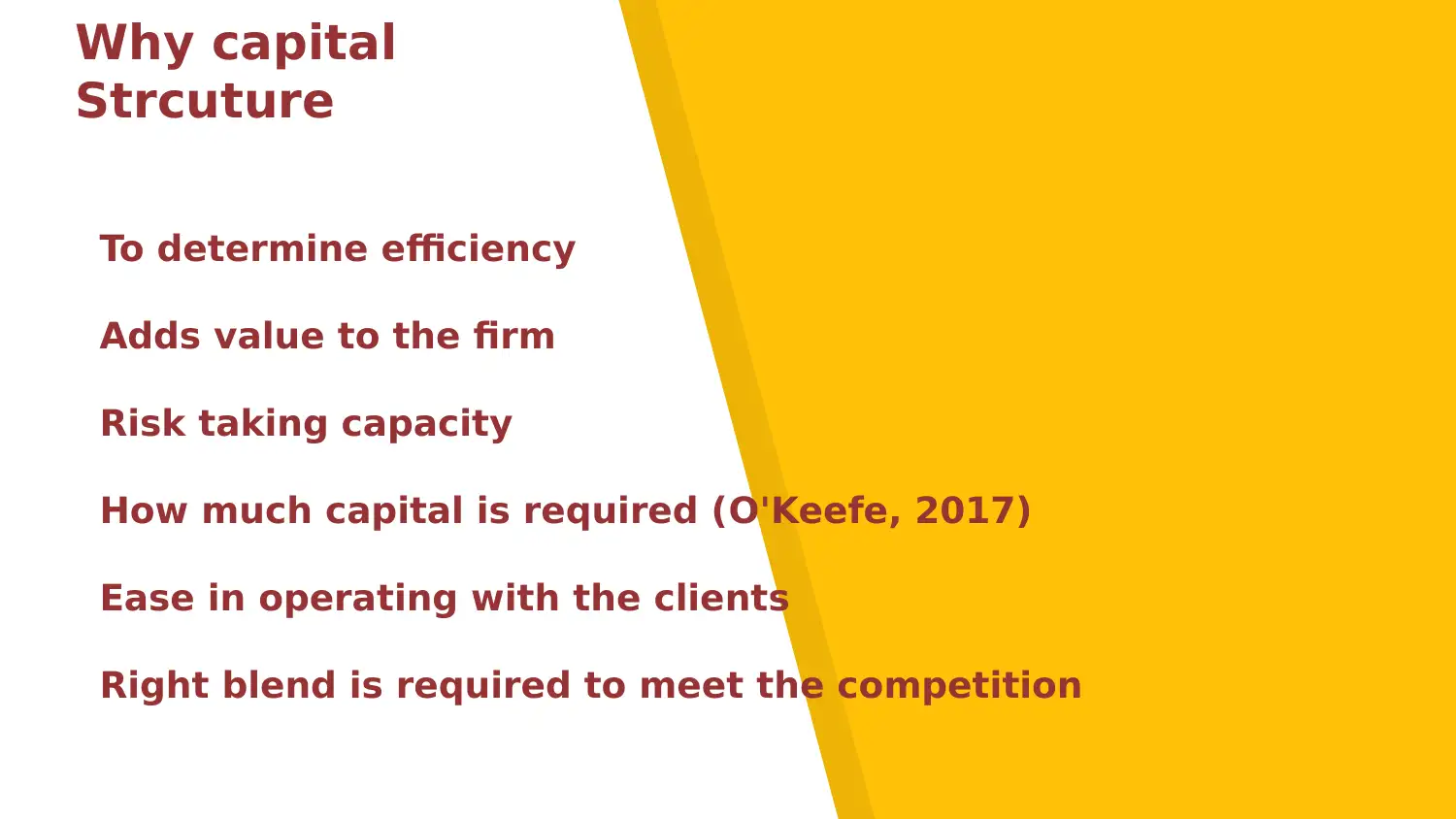

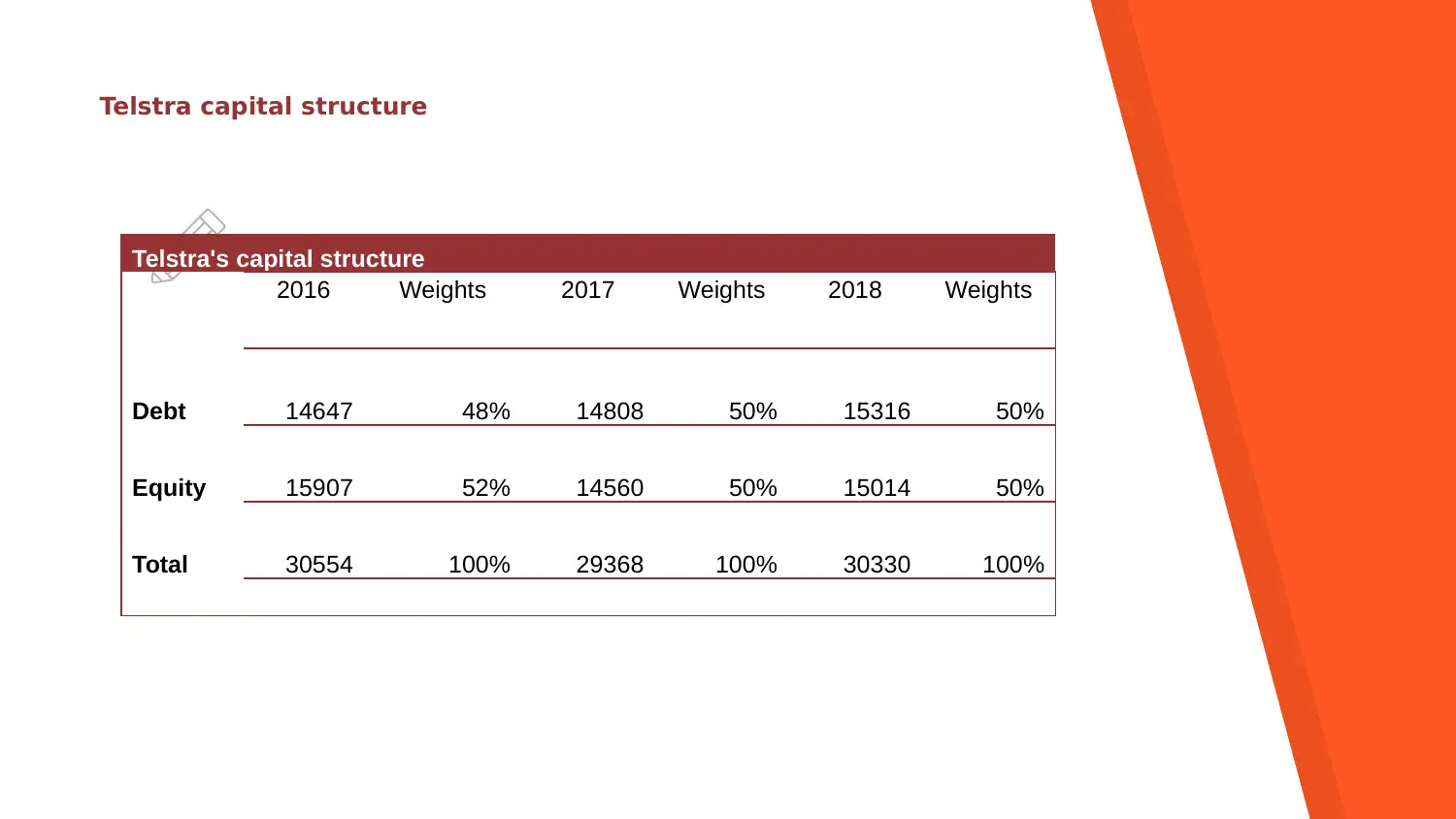

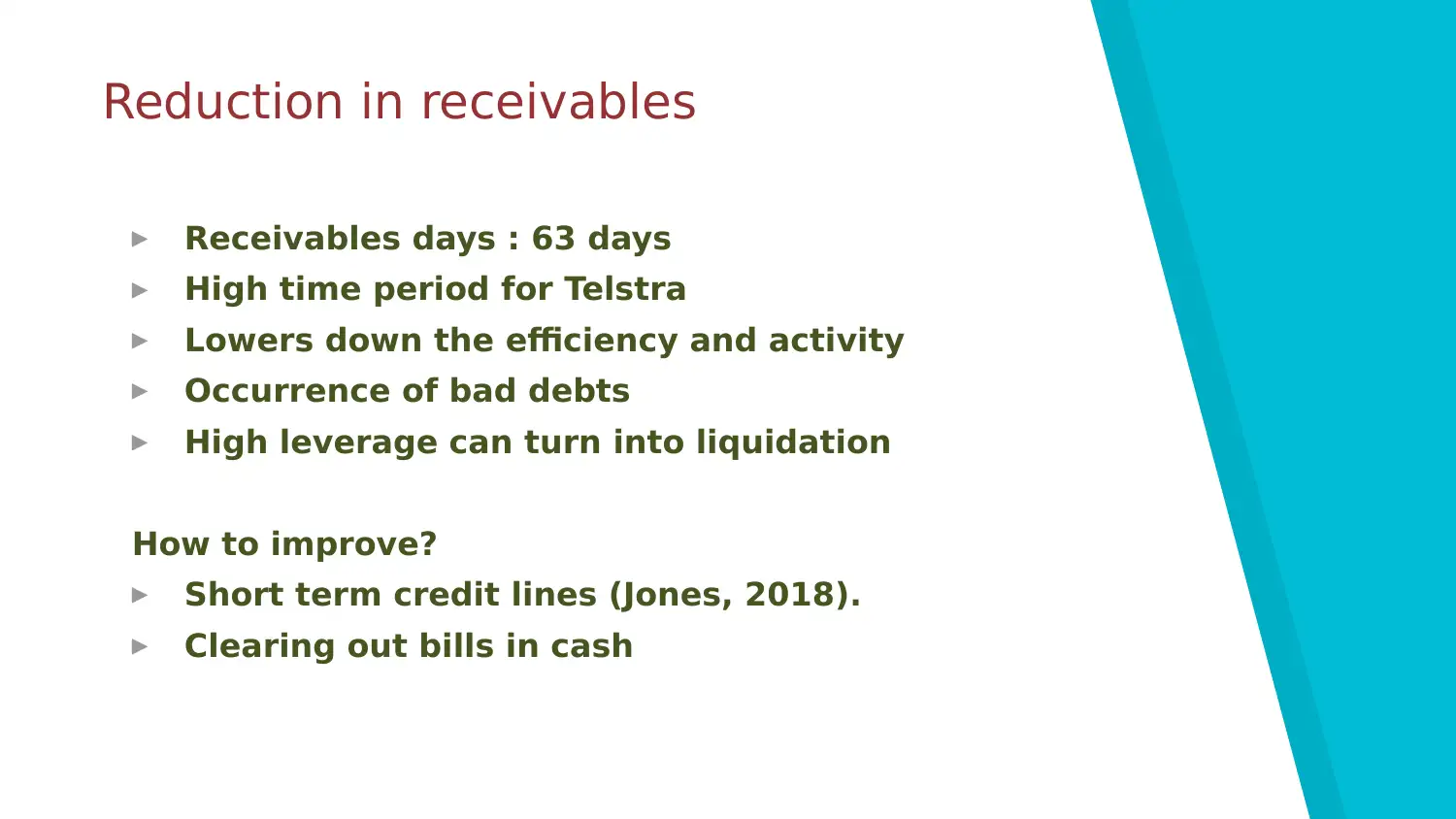

This presentation provides an analysis of Telstra Corporation's capital restructuring, examining aspects such as the debt-to-equity ratio, weighted average cost of capital (WACC), cash conversion cycle, and potential strategies for enhancing the company's value. It assesses Telstra's current capital structure, highlighting areas for improvement, including reducing debt components, optimizing asset utilization, and improving working capital management. The presentation also explores options such as mergers, acquisitions, and dividend policies to determine the best course of action for Telstra to achieve optimal financial performance and shareholder value. The analysis incorporates relevant financial data and industry benchmarks to provide a comprehensive evaluation of Telstra's capital restructuring needs and opportunities.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.