Telstra Corporation Ltd: A Detailed Analysis of Financial Statements

VerifiedAdded on 2023/06/11

|16

|3219

|143

Report

AI Summary

This report provides a detailed analysis of Telstra Corporation Ltd's financial performance, focusing on cash flow statements, other comprehensive income, and corporate income tax accounting. The cash flow analysis categorizes activities into operating, investing, and financing, highlighting trends and significant changes over three years. The report also examines items included in other comprehensive income and their impact on financial reporting. Furthermore, it delves into Telstra's corporate income tax obligations, deferred tax assets and liabilities, and the relationship between accounting income and tax expense. The analysis provides insights into Telstra's financial strategies and performance based on its financial statements.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Cash flow statement:........................................................................................................................2

Requirement (i):...........................................................................................................................2

Requirement (ii):..........................................................................................................................6

Other comprehensive income statement:.........................................................................................8

Requirement (iii):.........................................................................................................................8

Requirement (iv):.........................................................................................................................8

Requirement (v):..........................................................................................................................8

Accounting for corporate income tax:.............................................................................................9

Requirement (vi):.........................................................................................................................9

Requirement (vii):........................................................................................................................9

Requirement (viii):.......................................................................................................................9

Requirement (ix):.........................................................................................................................9

Requirement (x):........................................................................................................................10

Requirement (xi):.......................................................................................................................11

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................2

Cash flow statement:........................................................................................................................2

Requirement (i):...........................................................................................................................2

Requirement (ii):..........................................................................................................................6

Other comprehensive income statement:.........................................................................................8

Requirement (iii):.........................................................................................................................8

Requirement (iv):.........................................................................................................................8

Requirement (v):..........................................................................................................................8

Accounting for corporate income tax:.............................................................................................9

Requirement (vi):.........................................................................................................................9

Requirement (vii):........................................................................................................................9

Requirement (viii):.......................................................................................................................9

Requirement (ix):.........................................................................................................................9

Requirement (x):........................................................................................................................10

Requirement (xi):.......................................................................................................................11

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

2CORPORATE ACCOUNTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Introduction

The report intends to state on the various types of finding based on cash flow assessment

of “Telstra corporations Ltd.” Some of the main assessment of the study has included a

comparative analysis of three important aspects of cash flows specifically stated with operating,

investing and financing events. It is also discussed on the various changes over the past three

years based on the categorisation of information. The second section of the report have shown

the elements from other comprehensive income statement and items which are not reported in the

“profit and loss statement” or “income statement” of the company. The third section of the study

have shown the expense of the formats for latest financial statement and included various other

depictions on corporate income tax including the items which are not reported in the PL

statement or income statement of the company. These interpretations are further followed with

accounting for corporate income tax. This is done based on the depictions of firm’s tax expense

as for the latest financial statement. Additionally, the report has shown that deferred tax assets

and liabilities along with possible reason for recording the same. The last section of the report

has depicted with the firm’s tax expense as per company tax rate times firms accounting income

has been presented

Cash flow statement:

Requirement (i):

The important analysis on cash flow statement for this report has been prepared with

“Telstra Corporation Ltd”, which is one of the leading communications and technology company

in Australia known for “offering full range of communications services and competing in all

Introduction

The report intends to state on the various types of finding based on cash flow assessment

of “Telstra corporations Ltd.” Some of the main assessment of the study has included a

comparative analysis of three important aspects of cash flows specifically stated with operating,

investing and financing events. It is also discussed on the various changes over the past three

years based on the categorisation of information. The second section of the report have shown

the elements from other comprehensive income statement and items which are not reported in the

“profit and loss statement” or “income statement” of the company. The third section of the study

have shown the expense of the formats for latest financial statement and included various other

depictions on corporate income tax including the items which are not reported in the PL

statement or income statement of the company. These interpretations are further followed with

accounting for corporate income tax. This is done based on the depictions of firm’s tax expense

as for the latest financial statement. Additionally, the report has shown that deferred tax assets

and liabilities along with possible reason for recording the same. The last section of the report

has depicted with the firm’s tax expense as per company tax rate times firms accounting income

has been presented

Cash flow statement:

Requirement (i):

The important analysis on cash flow statement for this report has been prepared with

“Telstra Corporation Ltd”, which is one of the leading communications and technology company

in Australia known for “offering full range of communications services and competing in all

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

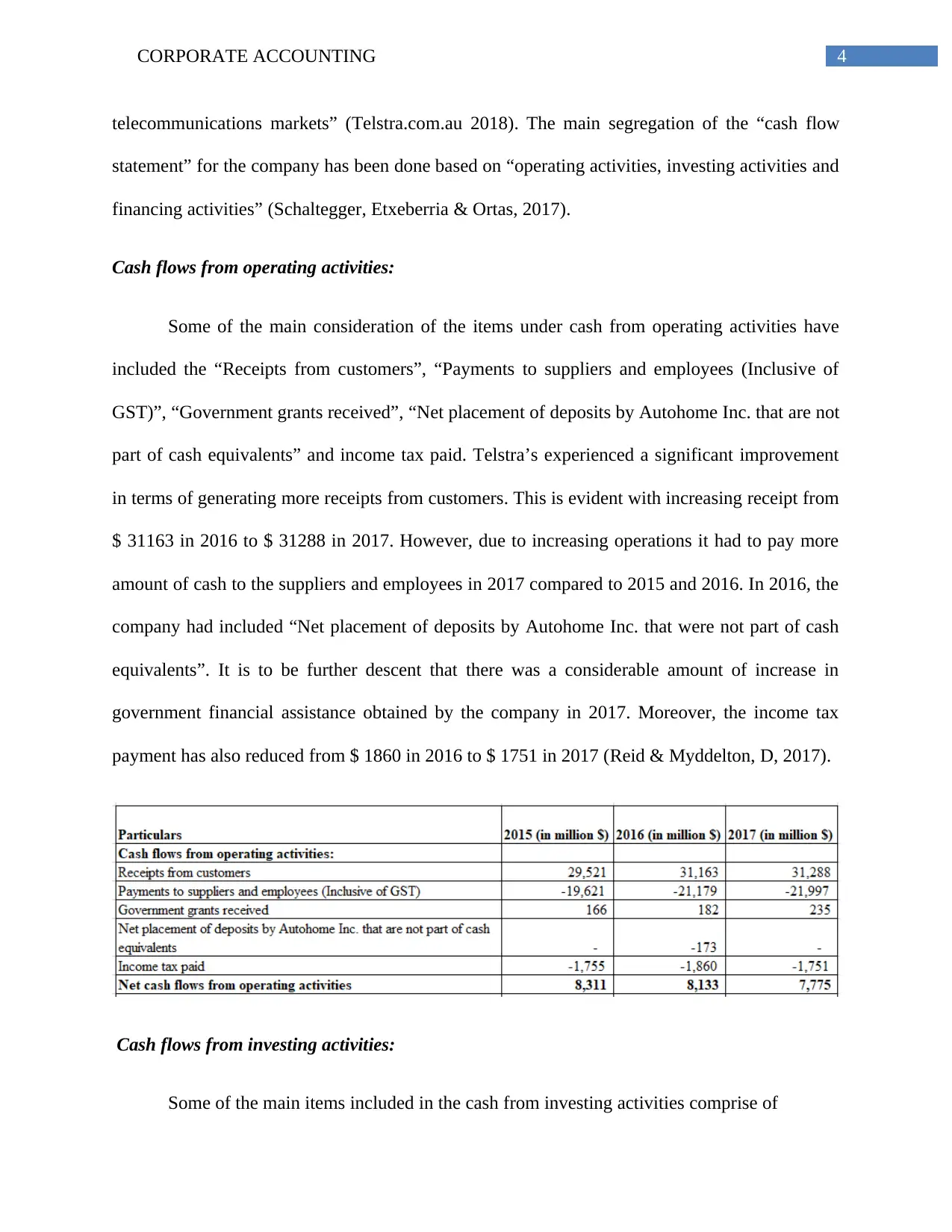

telecommunications markets” (Telstra.com.au 2018). The main segregation of the “cash flow

statement” for the company has been done based on “operating activities, investing activities and

financing activities” (Schaltegger, Etxeberria & Ortas, 2017).

Cash flows from operating activities:

Some of the main consideration of the items under cash from operating activities have

included the “Receipts from customers”, “Payments to suppliers and employees (Inclusive of

GST)”, “Government grants received”, “Net placement of deposits by Autohome Inc. that are not

part of cash equivalents” and income tax paid. Telstra’s experienced a significant improvement

in terms of generating more receipts from customers. This is evident with increasing receipt from

$ 31163 in 2016 to $ 31288 in 2017. However, due to increasing operations it had to pay more

amount of cash to the suppliers and employees in 2017 compared to 2015 and 2016. In 2016, the

company had included “Net placement of deposits by Autohome Inc. that were not part of cash

equivalents”. It is to be further descent that there was a considerable amount of increase in

government financial assistance obtained by the company in 2017. Moreover, the income tax

payment has also reduced from $ 1860 in 2016 to $ 1751 in 2017 (Reid & Myddelton, D, 2017).

Cash flows from investing activities:

Some of the main items included in the cash from investing activities comprise of

telecommunications markets” (Telstra.com.au 2018). The main segregation of the “cash flow

statement” for the company has been done based on “operating activities, investing activities and

financing activities” (Schaltegger, Etxeberria & Ortas, 2017).

Cash flows from operating activities:

Some of the main consideration of the items under cash from operating activities have

included the “Receipts from customers”, “Payments to suppliers and employees (Inclusive of

GST)”, “Government grants received”, “Net placement of deposits by Autohome Inc. that are not

part of cash equivalents” and income tax paid. Telstra’s experienced a significant improvement

in terms of generating more receipts from customers. This is evident with increasing receipt from

$ 31163 in 2016 to $ 31288 in 2017. However, due to increasing operations it had to pay more

amount of cash to the suppliers and employees in 2017 compared to 2015 and 2016. In 2016, the

company had included “Net placement of deposits by Autohome Inc. that were not part of cash

equivalents”. It is to be further descent that there was a considerable amount of increase in

government financial assistance obtained by the company in 2017. Moreover, the income tax

payment has also reduced from $ 1860 in 2016 to $ 1751 in 2017 (Reid & Myddelton, D, 2017).

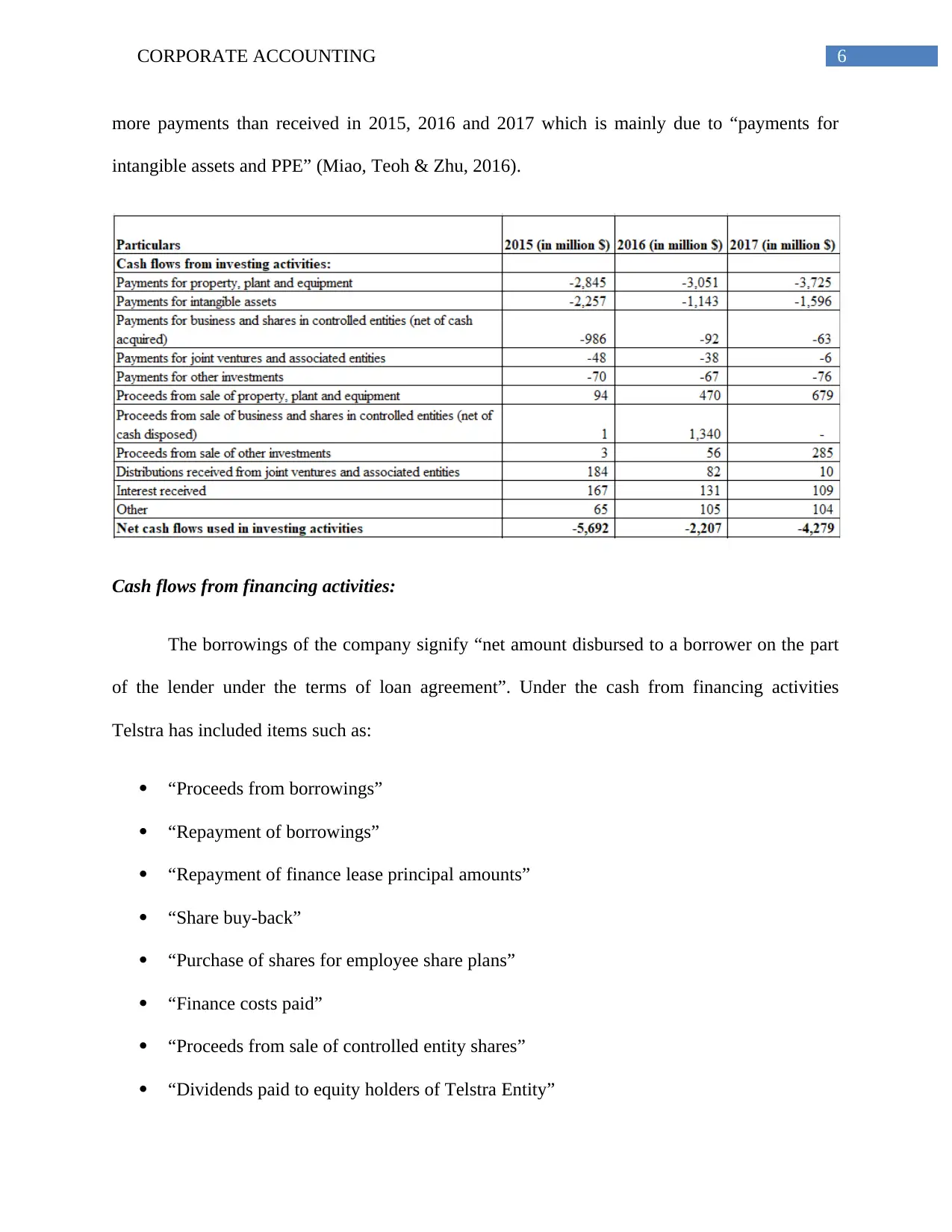

Cash flows from investing activities:

Some of the main items included in the cash from investing activities comprise of

5CORPORATE ACCOUNTING

“Payments for property, plant and equipment”

“Payments for intangible assets”

“Payments for business and shares in controlled entities (net of cash acquired)”

“Payments for joint ventures and associated entities”

“Payments for other investments”

“Proceeds from sale of property, plant and equipment”

“Proceeds from sale of business and shares in controlled entities (net of cash disposed)”

“Proceeds from sale of other investments”

“Distributions received from joint ventures and associated entities”

“Interest received”

“Other investing activities”

The various types of payment associated to “property, plant and equipment” are

considered to be a part of proceeds from the advances and deposits. The different types of

payments associated to “property, plant and equipment” are recognised as the amounts which are

needed to conduct business activity. On the contrary, these assets have been conducive in

providing several types of economic benefits to Telstra Corporations which are included as

proceeds (Ramanna, 2014). It needs to be further discerned that Telstra has experienced a

considerable increase in proceeds from sale of other investments and this clearly shows that the

company has been able to generate adequate cash from items included under fixed assets. These

proceeds are considered as a contract specifying the total tenure of the payment and the amount

which is to be received along with any interest payable. However, based on the depiction of

overall cash used in the investment activities it can be clearly depicted that Telstra has made

“Payments for property, plant and equipment”

“Payments for intangible assets”

“Payments for business and shares in controlled entities (net of cash acquired)”

“Payments for joint ventures and associated entities”

“Payments for other investments”

“Proceeds from sale of property, plant and equipment”

“Proceeds from sale of business and shares in controlled entities (net of cash disposed)”

“Proceeds from sale of other investments”

“Distributions received from joint ventures and associated entities”

“Interest received”

“Other investing activities”

The various types of payment associated to “property, plant and equipment” are

considered to be a part of proceeds from the advances and deposits. The different types of

payments associated to “property, plant and equipment” are recognised as the amounts which are

needed to conduct business activity. On the contrary, these assets have been conducive in

providing several types of economic benefits to Telstra Corporations which are included as

proceeds (Ramanna, 2014). It needs to be further discerned that Telstra has experienced a

considerable increase in proceeds from sale of other investments and this clearly shows that the

company has been able to generate adequate cash from items included under fixed assets. These

proceeds are considered as a contract specifying the total tenure of the payment and the amount

which is to be received along with any interest payable. However, based on the depiction of

overall cash used in the investment activities it can be clearly depicted that Telstra has made

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

more payments than received in 2015, 2016 and 2017 which is mainly due to “payments for

intangible assets and PPE” (Miao, Teoh & Zhu, 2016).

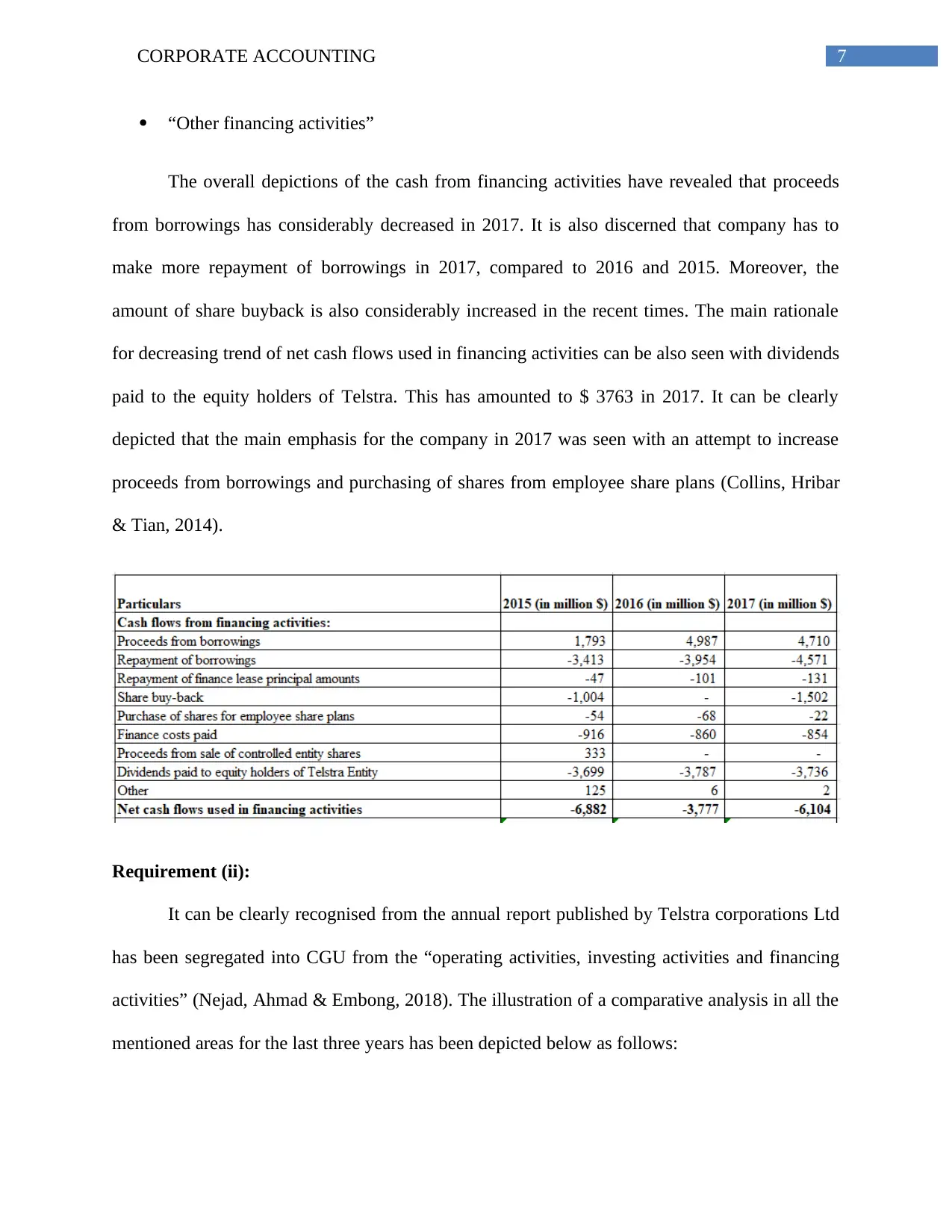

Cash flows from financing activities:

The borrowings of the company signify “net amount disbursed to a borrower on the part

of the lender under the terms of loan agreement”. Under the cash from financing activities

Telstra has included items such as:

“Proceeds from borrowings”

“Repayment of borrowings”

“Repayment of finance lease principal amounts”

“Share buy-back”

“Purchase of shares for employee share plans”

“Finance costs paid”

“Proceeds from sale of controlled entity shares”

“Dividends paid to equity holders of Telstra Entity”

more payments than received in 2015, 2016 and 2017 which is mainly due to “payments for

intangible assets and PPE” (Miao, Teoh & Zhu, 2016).

Cash flows from financing activities:

The borrowings of the company signify “net amount disbursed to a borrower on the part

of the lender under the terms of loan agreement”. Under the cash from financing activities

Telstra has included items such as:

“Proceeds from borrowings”

“Repayment of borrowings”

“Repayment of finance lease principal amounts”

“Share buy-back”

“Purchase of shares for employee share plans”

“Finance costs paid”

“Proceeds from sale of controlled entity shares”

“Dividends paid to equity holders of Telstra Entity”

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

“Other financing activities”

The overall depictions of the cash from financing activities have revealed that proceeds

from borrowings has considerably decreased in 2017. It is also discerned that company has to

make more repayment of borrowings in 2017, compared to 2016 and 2015. Moreover, the

amount of share buyback is also considerably increased in the recent times. The main rationale

for decreasing trend of net cash flows used in financing activities can be also seen with dividends

paid to the equity holders of Telstra. This has amounted to $ 3763 in 2017. It can be clearly

depicted that the main emphasis for the company in 2017 was seen with an attempt to increase

proceeds from borrowings and purchasing of shares from employee share plans (Collins, Hribar

& Tian, 2014).

Requirement (ii):

It can be clearly recognised from the annual report published by Telstra corporations Ltd

has been segregated into CGU from the “operating activities, investing activities and financing

activities” (Nejad, Ahmad & Embong, 2018). The illustration of a comparative analysis in all the

mentioned areas for the last three years has been depicted below as follows:

“Other financing activities”

The overall depictions of the cash from financing activities have revealed that proceeds

from borrowings has considerably decreased in 2017. It is also discerned that company has to

make more repayment of borrowings in 2017, compared to 2016 and 2015. Moreover, the

amount of share buyback is also considerably increased in the recent times. The main rationale

for decreasing trend of net cash flows used in financing activities can be also seen with dividends

paid to the equity holders of Telstra. This has amounted to $ 3763 in 2017. It can be clearly

depicted that the main emphasis for the company in 2017 was seen with an attempt to increase

proceeds from borrowings and purchasing of shares from employee share plans (Collins, Hribar

& Tian, 2014).

Requirement (ii):

It can be clearly recognised from the annual report published by Telstra corporations Ltd

has been segregated into CGU from the “operating activities, investing activities and financing

activities” (Nejad, Ahmad & Embong, 2018). The illustration of a comparative analysis in all the

mentioned areas for the last three years has been depicted below as follows:

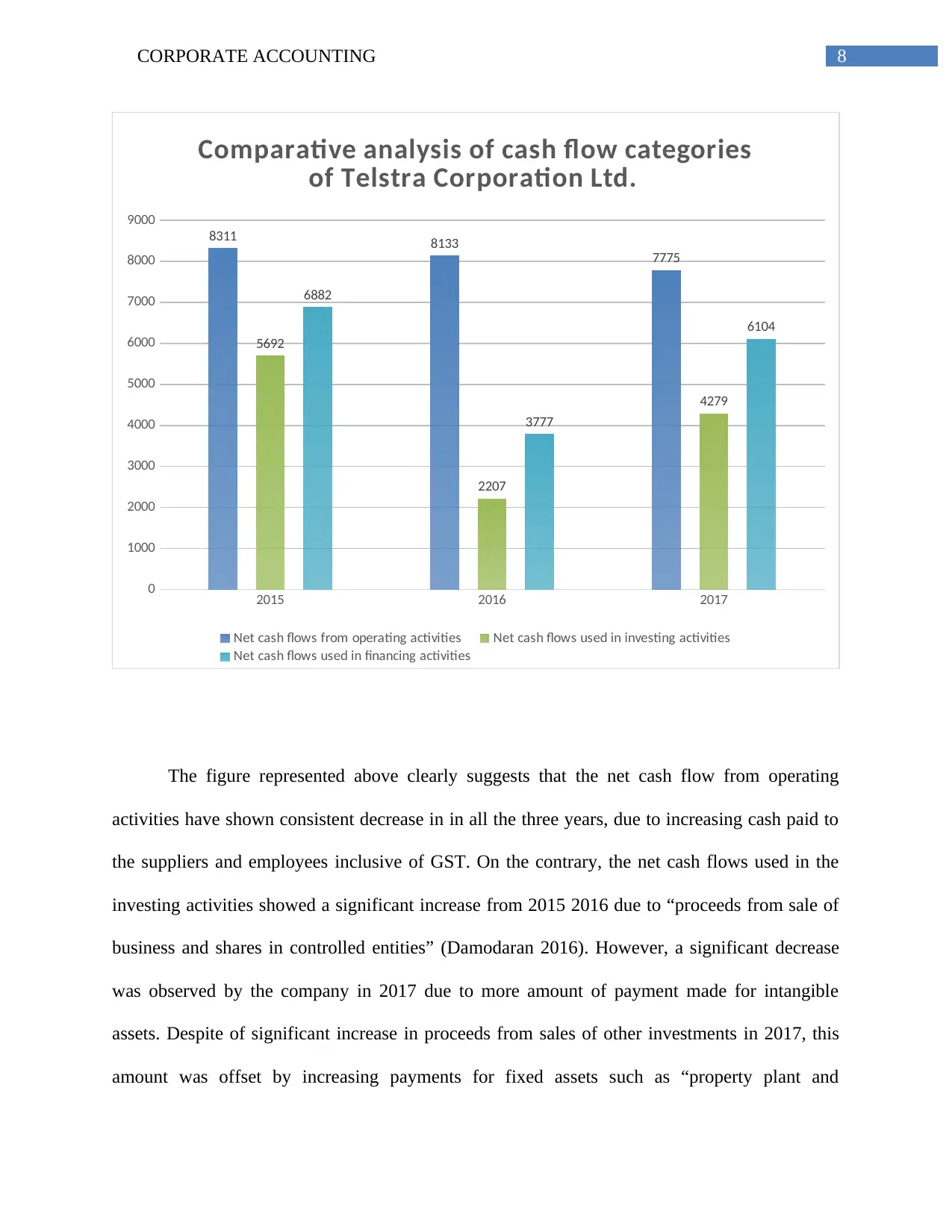

8CORPORATE ACCOUNTING

2015 2016 2017

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

8311 8133

7775

5692

2207

4279

6882

3777

6104

Comparative analysis of cash flow categories

of Telstra Corporation Ltd.

Net cash flows from operating activities Net cash flows used in investing activities

Net cash flows used in financing activities

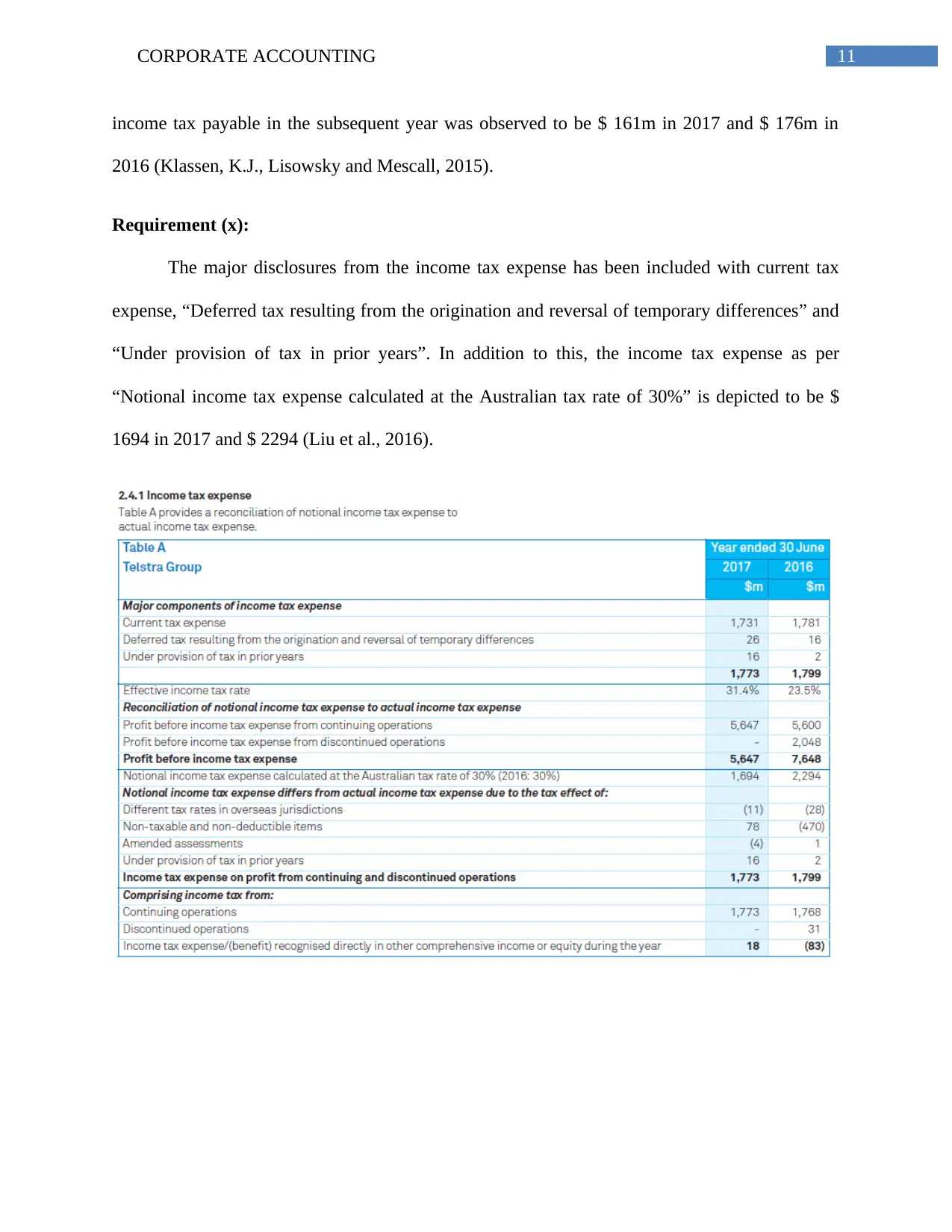

The figure represented above clearly suggests that the net cash flow from operating

activities have shown consistent decrease in in all the three years, due to increasing cash paid to

the suppliers and employees inclusive of GST. On the contrary, the net cash flows used in the

investing activities showed a significant increase from 2015 2016 due to “proceeds from sale of

business and shares in controlled entities” (Damodaran 2016). However, a significant decrease

was observed by the company in 2017 due to more amount of payment made for intangible

assets. Despite of significant increase in proceeds from sales of other investments in 2017, this

amount was offset by increasing payments for fixed assets such as “property plant and

2015 2016 2017

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

8311 8133

7775

5692

2207

4279

6882

3777

6104

Comparative analysis of cash flow categories

of Telstra Corporation Ltd.

Net cash flows from operating activities Net cash flows used in investing activities

Net cash flows used in financing activities

The figure represented above clearly suggests that the net cash flow from operating

activities have shown consistent decrease in in all the three years, due to increasing cash paid to

the suppliers and employees inclusive of GST. On the contrary, the net cash flows used in the

investing activities showed a significant increase from 2015 2016 due to “proceeds from sale of

business and shares in controlled entities” (Damodaran 2016). However, a significant decrease

was observed by the company in 2017 due to more amount of payment made for intangible

assets. Despite of significant increase in proceeds from sales of other investments in 2017, this

amount was offset by increasing payments for fixed assets such as “property plant and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

equipment” and “payment for intangible assets”. Therefore, due to the factors such as more

payments for fixed assets and intangibles and less amount of distributions received from joint

ventures, the company has experienced a cash crunch towards investing activities in 2017

(Christensen et al. 2015).

Other comprehensive income statement:

Requirement (iii):

The annual report of Telstra corporations Ltd has been used to list down the items under

the other comprehensive income statement with “Foreign currency translation reserve, Cash flow

hedging reserve and Foreign currency basis spread reserve”.

Requirement (iv):

It has been depicted that the company has used the reserve for foreign Currency

translation for the conversion of outcomes associated to foreign subsidiaries of “parent firm to

the reporting currency”. The application of cash flow hedging reserve has been conducive in

depicting the firm’s intention to minimise the overall exposure of variations in cash flow of an

asset or liability due to the changes in risk areas such as rate of interest on debt instrument

associated to floating rate. It is also discerned that the income tax expense has been incurred on

the PBT of Telstra (Goh et al. 2016).

Requirement (v):

A more elaborated explanation of net income has been depicted with other

comprehensive income. Telstra corporations have incorporated this statement for assimilating the

important details based on the value of aforementioned items. The main rationale for including

these items are being mentioned in terms of “other comprehensive income statement” as these

equipment” and “payment for intangible assets”. Therefore, due to the factors such as more

payments for fixed assets and intangibles and less amount of distributions received from joint

ventures, the company has experienced a cash crunch towards investing activities in 2017

(Christensen et al. 2015).

Other comprehensive income statement:

Requirement (iii):

The annual report of Telstra corporations Ltd has been used to list down the items under

the other comprehensive income statement with “Foreign currency translation reserve, Cash flow

hedging reserve and Foreign currency basis spread reserve”.

Requirement (iv):

It has been depicted that the company has used the reserve for foreign Currency

translation for the conversion of outcomes associated to foreign subsidiaries of “parent firm to

the reporting currency”. The application of cash flow hedging reserve has been conducive in

depicting the firm’s intention to minimise the overall exposure of variations in cash flow of an

asset or liability due to the changes in risk areas such as rate of interest on debt instrument

associated to floating rate. It is also discerned that the income tax expense has been incurred on

the PBT of Telstra (Goh et al. 2016).

Requirement (v):

A more elaborated explanation of net income has been depicted with other

comprehensive income. Telstra corporations have incorporated this statement for assimilating the

important details based on the value of aforementioned items. The main rationale for including

these items are being mentioned in terms of “other comprehensive income statement” as these

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

are seen to be providing a more comprehensive and complete overview for the factors associated

to operations of the business which we are not disclosed in the income statement of the company

(Grubert and Altshuler 2016).

Accounting for corporate income tax:

Requirement (vi):

The obligation for tax expense is mainly due to the factors associated to state government

proceedings, federal and municipal activities. In case of Telstra, the total income tax expense has

amounted to $ 1773 in 2017 in contrast to $ 1768 in 2016 (Graham et al., 2017).

Requirement (vii):

It is clearly depicted that Telstra corporations earned profit before income tax expense

amounting to $ 5600 in 2016 and $ 5647 in 2017. This amount has been clearly inherent from the

tax rate of 30% on PBIT.

Requirement (viii):

The review of the deferred tax assets is done by the company at the end of each reporting

period. The carrying amount is seen to be recognised to only that extent it is seen to be probable

as for the sufficient taxable profit which shall be utilised with the benefits of the company. In

addition to this, the company offsets the DTL and DTA in the financial statement which are

related to income taxes levied by the taxation authority (Khan, M., Srinivasan, S. and Tan, 2016).

Requirement (ix):

The different types of disclosures about franking credits as a result of income tax payable

was discerned to be $ 146m in 2017 and $ 158m in 2016. In addition to this, the total amount of

are seen to be providing a more comprehensive and complete overview for the factors associated

to operations of the business which we are not disclosed in the income statement of the company

(Grubert and Altshuler 2016).

Accounting for corporate income tax:

Requirement (vi):

The obligation for tax expense is mainly due to the factors associated to state government

proceedings, federal and municipal activities. In case of Telstra, the total income tax expense has

amounted to $ 1773 in 2017 in contrast to $ 1768 in 2016 (Graham et al., 2017).

Requirement (vii):

It is clearly depicted that Telstra corporations earned profit before income tax expense

amounting to $ 5600 in 2016 and $ 5647 in 2017. This amount has been clearly inherent from the

tax rate of 30% on PBIT.

Requirement (viii):

The review of the deferred tax assets is done by the company at the end of each reporting

period. The carrying amount is seen to be recognised to only that extent it is seen to be probable

as for the sufficient taxable profit which shall be utilised with the benefits of the company. In

addition to this, the company offsets the DTL and DTA in the financial statement which are

related to income taxes levied by the taxation authority (Khan, M., Srinivasan, S. and Tan, 2016).

Requirement (ix):

The different types of disclosures about franking credits as a result of income tax payable

was discerned to be $ 146m in 2017 and $ 158m in 2016. In addition to this, the total amount of

11CORPORATE ACCOUNTING

income tax payable in the subsequent year was observed to be $ 161m in 2017 and $ 176m in

2016 (Klassen, K.J., Lisowsky and Mescall, 2015).

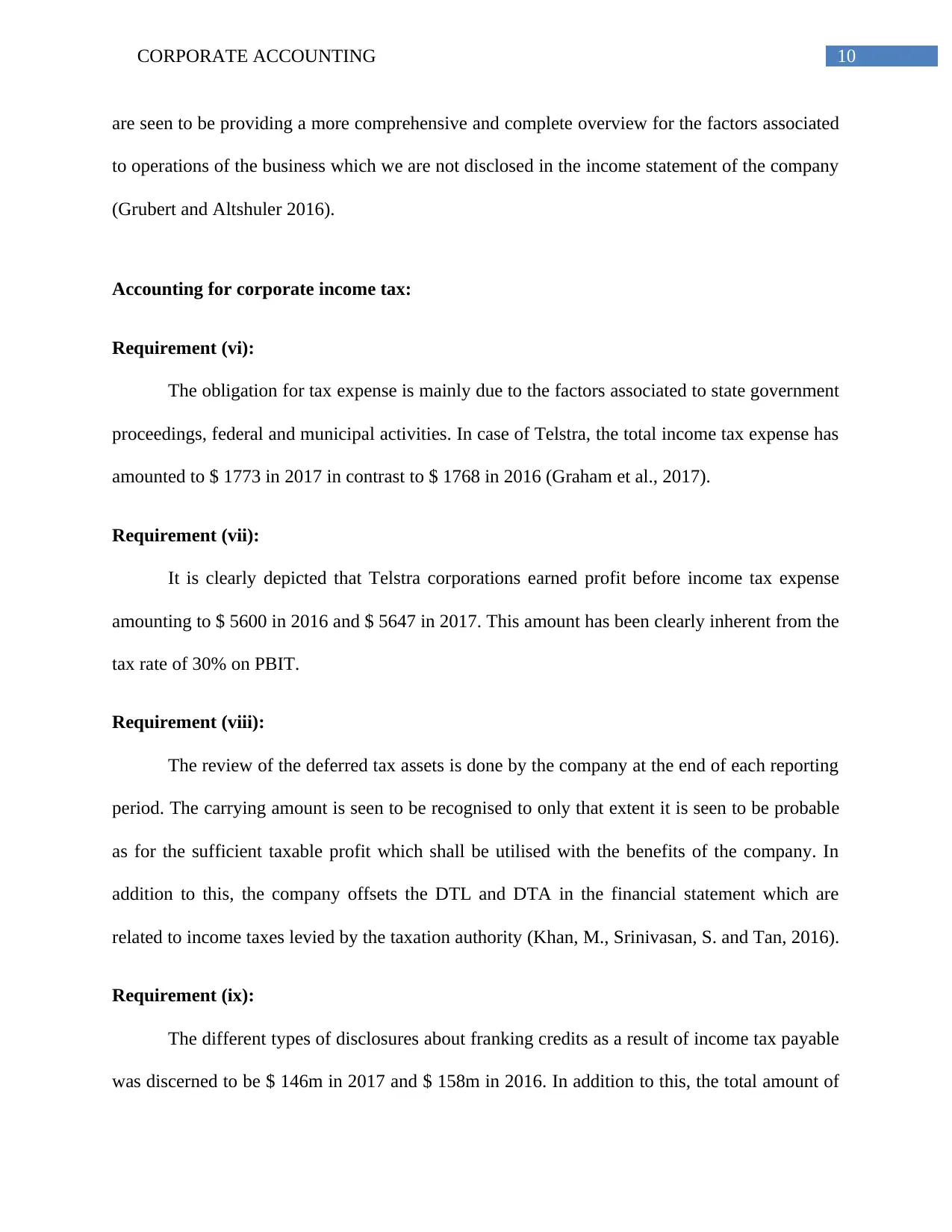

Requirement (x):

The major disclosures from the income tax expense has been included with current tax

expense, “Deferred tax resulting from the origination and reversal of temporary differences” and

“Under provision of tax in prior years”. In addition to this, the income tax expense as per

“Notional income tax expense calculated at the Australian tax rate of 30%” is depicted to be $

1694 in 2017 and $ 2294 (Liu et al., 2016).

income tax payable in the subsequent year was observed to be $ 161m in 2017 and $ 176m in

2016 (Klassen, K.J., Lisowsky and Mescall, 2015).

Requirement (x):

The major disclosures from the income tax expense has been included with current tax

expense, “Deferred tax resulting from the origination and reversal of temporary differences” and

“Under provision of tax in prior years”. In addition to this, the income tax expense as per

“Notional income tax expense calculated at the Australian tax rate of 30%” is depicted to be $

1694 in 2017 and $ 2294 (Liu et al., 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.