Qualitative Characteristics of Financial Reporting: Telstra Case Study

VerifiedAdded on 2020/03/23

|9

|2050

|41

Report

AI Summary

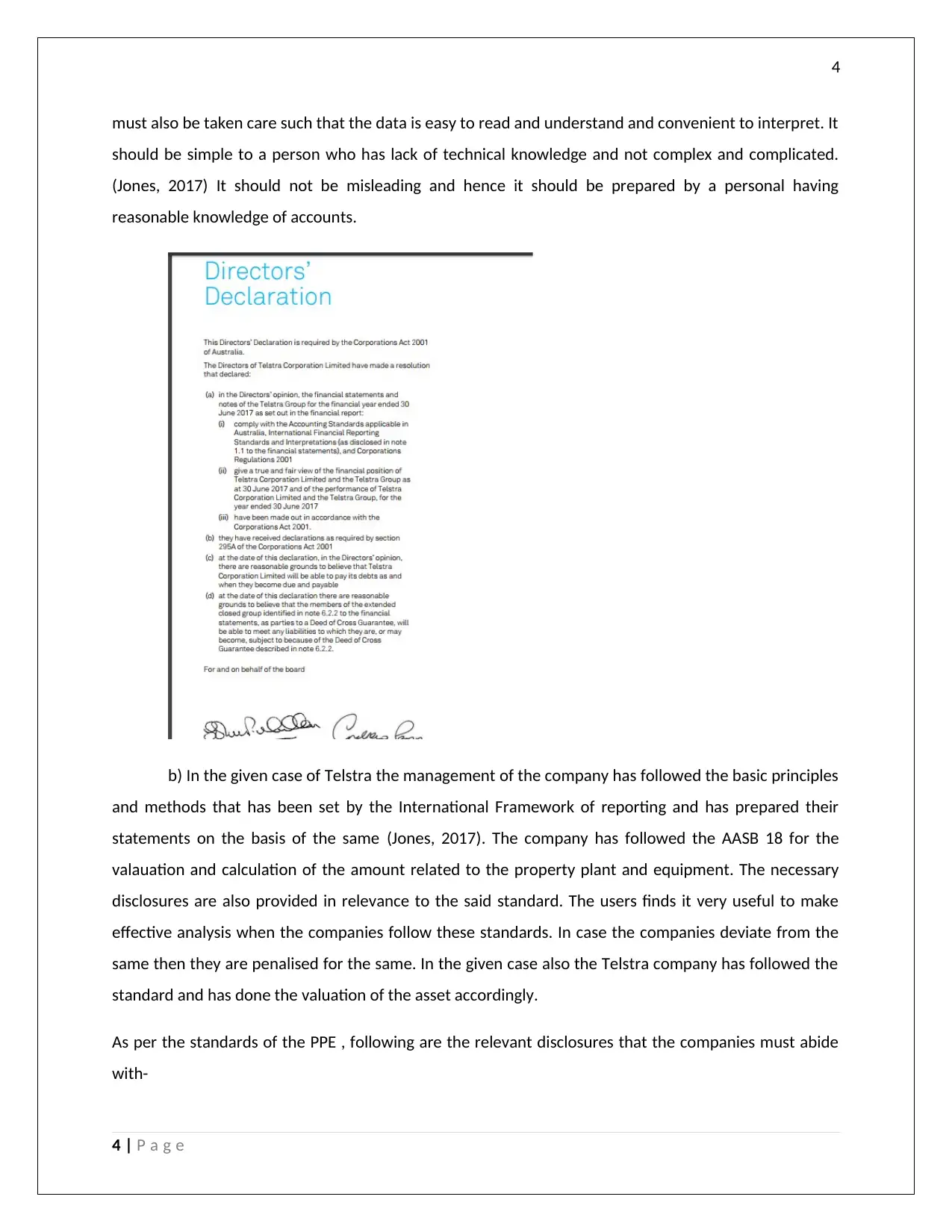

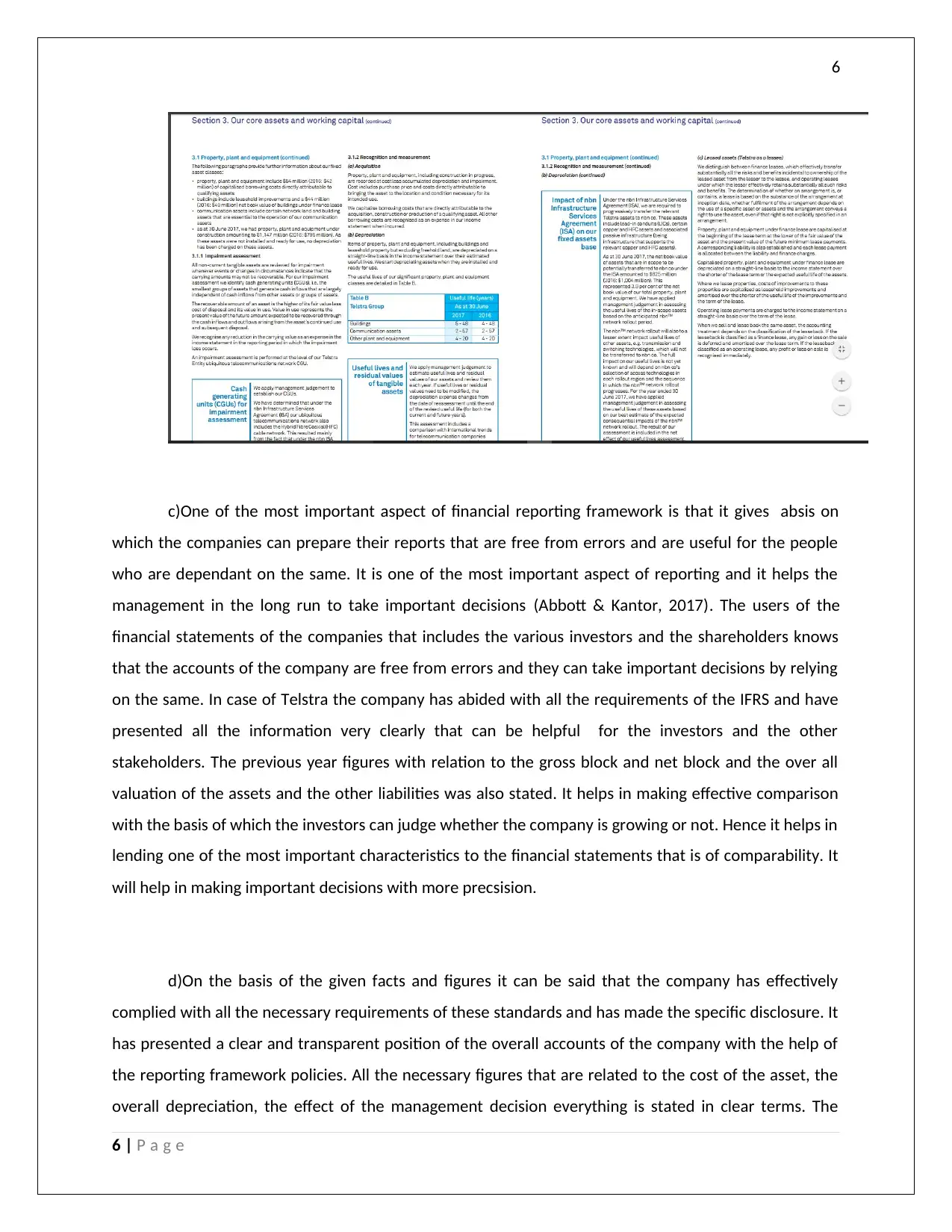

This report provides an analysis of the qualitative characteristics of financial reporting, with a focus on the application of AASB 18, related to the valuation of property, plant, and equipment. The report uses Telstra Corporation as a case study to illustrate the practical application of these principles. It discusses the conceptual framework of financial reporting, emphasizing the importance of relevant and reliable information for both internal and external users. The report examines the disclosures made by Telstra Corporation in accordance with AASB 18, including asset classifications, depreciation methods, impairment losses, and the impact of exchange rate fluctuations. The analysis highlights how Telstra has complied with IFRS and provides insights into how financial statements are prepared to ensure they are free from errors and useful for decision-making. The report also discusses the importance of comparability in financial statements and how effective reporting helps stakeholders make informed decisions. Finally, the report suggests potential improvements for the application of standards and the quality of financial reporting.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.