Financial Accounting Analysis of Telstra Group - ACC 201 Report

VerifiedAdded on 2024/06/03

|16

|2501

|273

Report

AI Summary

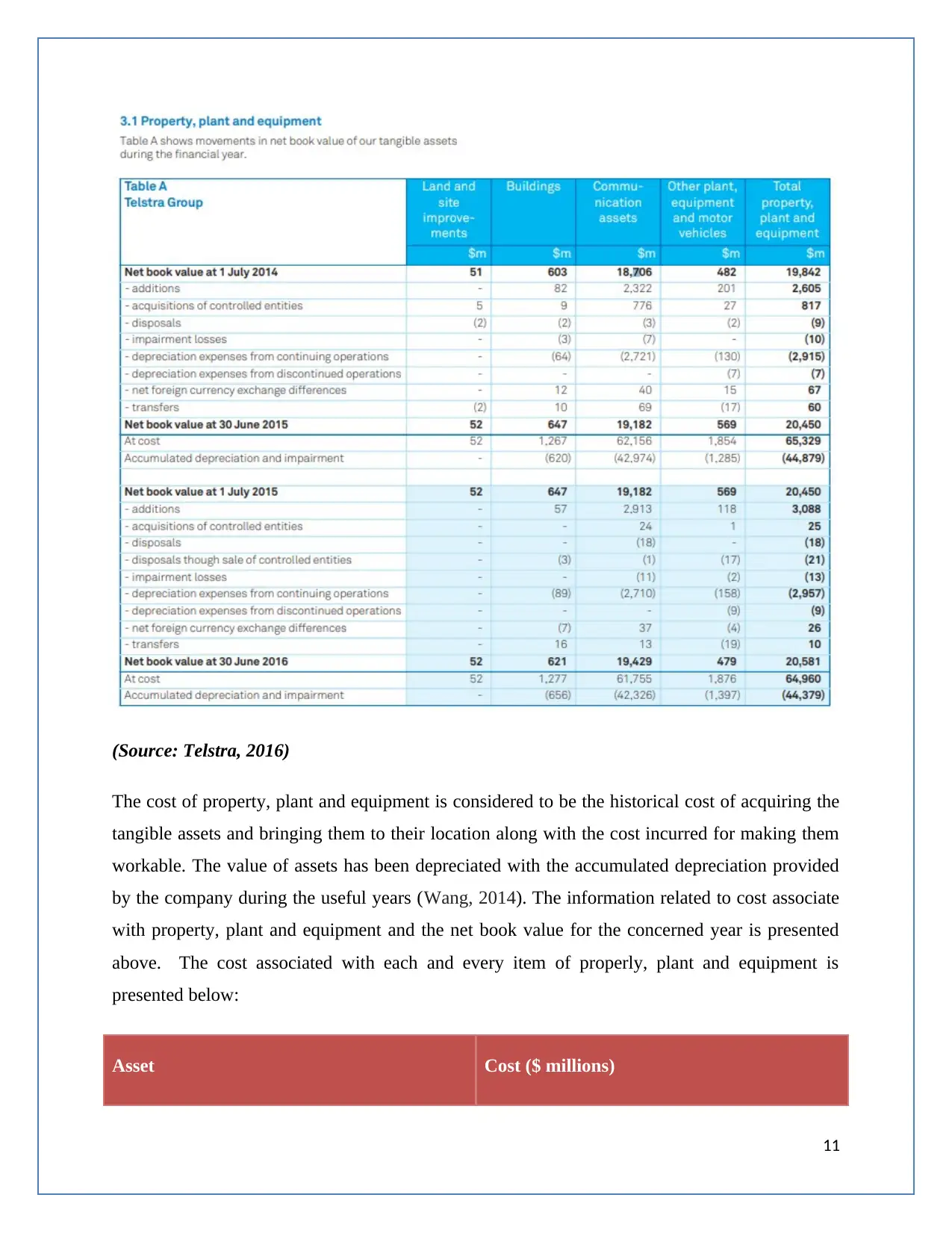

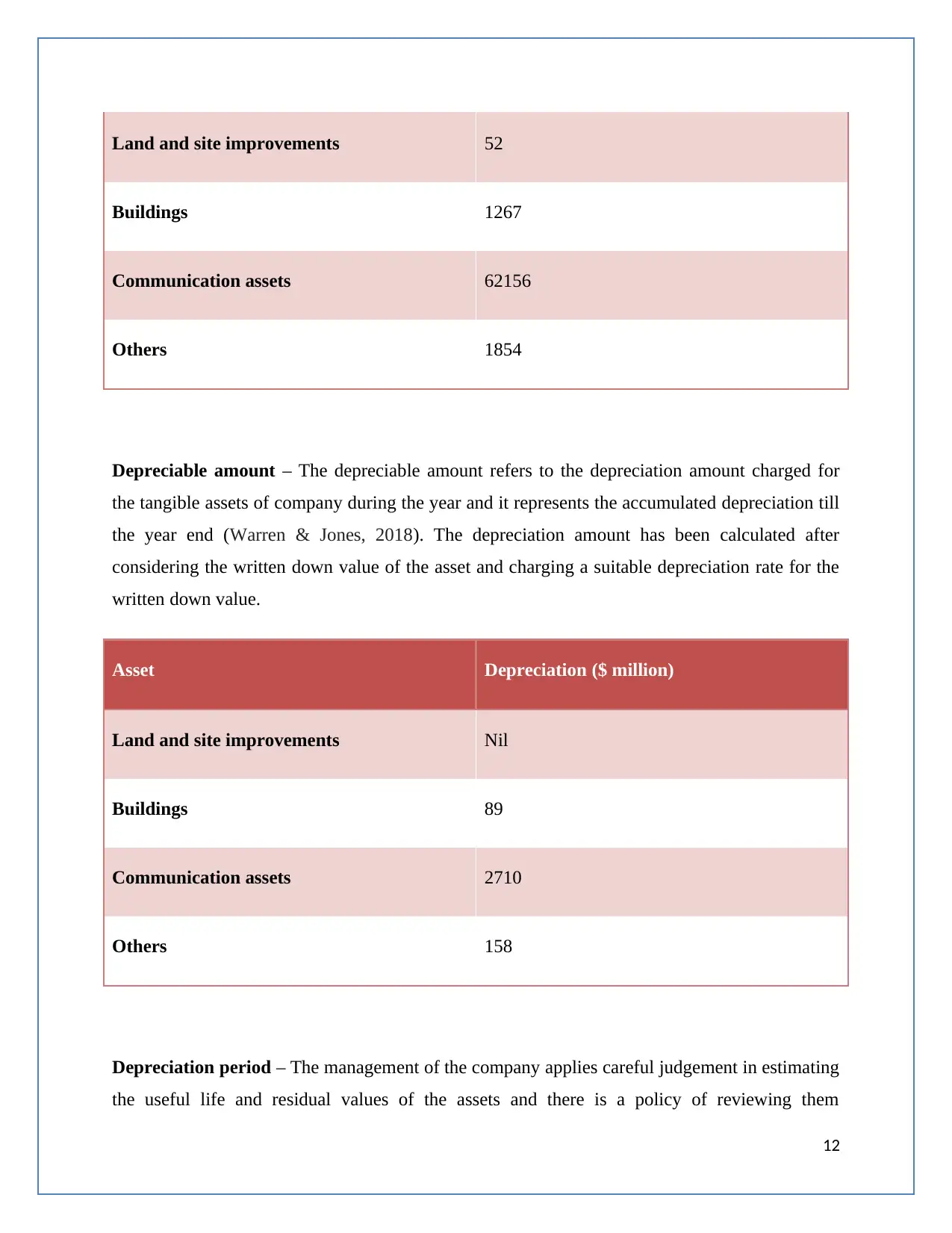

This financial accounting report provides an analysis of Telstra Group, focusing on key aspects of their financial statements. It begins with an examination of expense classification, determining whether expenses are classified by nature or function and providing reasons for the chosen methods. The report then delves into the company's accounting policies, including key estimates, judgements, and any changes in policies, particularly concerning AASB standards. Finally, it analyzes the notes to the 2016 financial statements, with a focus on depreciation methods, the cost of plant, property, and equipment, depreciable amounts, depreciation periods, and the approach to asset revaluation and impairment. The report concludes that Telstra Group applies concurrent and adequate accounting policies, resulting in a true and fair view of the company's financial position and performance.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.