Comparative Financial Performance: Telstra vs. Queste Communications

VerifiedAdded on 2020/05/28

|23

|3643

|333

AI Summary

The document provides an extensive analysis comparing the financial performances of Telstra and Queste Communications using a variety of financial ratios. Key aspects such as profitability, efficiency, liquidity, and capital structures are examined. The analyses highlight that despite certain negative cash flows in specific years, Telstra has shown overall better performance compared to Queste. This is evidenced through its superior profit margins, efficient use of assets, effective debt management, and robust liquidity positions. The study underscores Telstra's ability to generate profits more effectively than Queste Communications.

ACCOUNTING AND FINANCE 1

Executive summary

Telstra Corporation Ltd. is a telecommunication company in Australia. This report is all

about the overall financial analysis of the company, comparing with Queste Communications

Ltd, another company in telecom sector which is listed on Australian Securities Exchange

(About Us. 2018). It includes the financial statements and ratio analysis from year 2013 to

2017.

First part of the report deals with the horizontal and vertical analysis of Telstra’s income

statement, balance sheet and cash flow statement. It shows the percentage change of each of

the item mentioned in the statements. Some variations can be seen in the sales and net profit

made by the company. Telstra’s liabilities, assets and equities, all has increased with some

proportion during the period of five years. The analysis of cash flow statement has also

reported negative cash flows over the period.

The second part deals with the ratio analysis of the company which includes calculation of

profitability, efficiency, liquidity and capital structure ratios compared with Queste

communication Ltd. Telstra’s profitability and efficiency is much better than Queste. The

profits of Queste are in negative values whereas Telstra’s profits are positive, though

declining. Looking at the liquidity ratio, it can be said that Queste is much more liquid than

Telstra. Debt to equity ratio indicates that the liabilities of Telstra are comparatively more

than Queste in proportion to its total equities. Equity ratio of Queste is more than Telstra

where as its Debt ratio is lower than it.

The third part has conclusion which includes the overall findings of the analysis done. It

states that although the net profit of the former company is reducing but it is performing

much better than the latter company in terms of profitability and efficiency.

Executive summary

Telstra Corporation Ltd. is a telecommunication company in Australia. This report is all

about the overall financial analysis of the company, comparing with Queste Communications

Ltd, another company in telecom sector which is listed on Australian Securities Exchange

(About Us. 2018). It includes the financial statements and ratio analysis from year 2013 to

2017.

First part of the report deals with the horizontal and vertical analysis of Telstra’s income

statement, balance sheet and cash flow statement. It shows the percentage change of each of

the item mentioned in the statements. Some variations can be seen in the sales and net profit

made by the company. Telstra’s liabilities, assets and equities, all has increased with some

proportion during the period of five years. The analysis of cash flow statement has also

reported negative cash flows over the period.

The second part deals with the ratio analysis of the company which includes calculation of

profitability, efficiency, liquidity and capital structure ratios compared with Queste

communication Ltd. Telstra’s profitability and efficiency is much better than Queste. The

profits of Queste are in negative values whereas Telstra’s profits are positive, though

declining. Looking at the liquidity ratio, it can be said that Queste is much more liquid than

Telstra. Debt to equity ratio indicates that the liabilities of Telstra are comparatively more

than Queste in proportion to its total equities. Equity ratio of Queste is more than Telstra

where as its Debt ratio is lower than it.

The third part has conclusion which includes the overall findings of the analysis done. It

states that although the net profit of the former company is reducing but it is performing

much better than the latter company in terms of profitability and efficiency.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 2

Contents

Introduction...........................................................................................................................................3

Income statement...................................................................................................................................3

Balance sheet.........................................................................................................................................5

Cash Flow Statement.............................................................................................................................7

Financial Ratio Analysis........................................................................................................................8

Profitability ratios..............................................................................................................................8

Efficiency ratios.................................................................................................................................9

Liquidity ratios................................................................................................................................10

Capital structure ratio......................................................................................................................12

Conclusion...........................................................................................................................................12

References...........................................................................................................................................13

Appendix.............................................................................................................................................15

Contents

Introduction...........................................................................................................................................3

Income statement...................................................................................................................................3

Balance sheet.........................................................................................................................................5

Cash Flow Statement.............................................................................................................................7

Financial Ratio Analysis........................................................................................................................8

Profitability ratios..............................................................................................................................8

Efficiency ratios.................................................................................................................................9

Liquidity ratios................................................................................................................................10

Capital structure ratio......................................................................................................................12

Conclusion...........................................................................................................................................12

References...........................................................................................................................................13

Appendix.............................................................................................................................................15

ACCOUNTING AND FINANCE 3

Introduction

Telstra Corporation Limited is a leading telecommunications and technology company

operating in Australia. The company builds telecommunication networks and provide product

and services like mobile, internet access, pay television and many other. It provides 17.4

million mobile services, 6.8 million fixed voice services and 3.5 million retail fixed

broadband services.

The vision and mission of the company is to connect more and more people and to provide

them more opportunities. For this, the company build simple and easy to use technology and

content solutions, making it the largest national mobile network of Australia ("Telstra",

2018).

Telstra was previously originated with the Australia Post as a government department but

now it is fully privatized. The CEO of the company is now focusing to make the company

more consumer focused by undergoing a change program. In August 2011, Telstra announces

to expand its customer services to social media having 24/7 coverage. By the end of

November 2012, the company enjoys the increase in its live chats and the growth rate of this

service has also increased to a great extent ("Telstra", 2018).

As of 2016, the company owns about 360 retail stores and more than 300 stores are equipped

with low energy Bluetooth beacons. After the privatization, the shares of Telstra has risen to

$5 per share in December 2013 to $6 per share in December 2014. The company is listed on

Australian Stock Exchange (ASX) and traded as ASX: TLS. The company is looking forward

to extend its growth in the international markets under the new CEO Andy Penn ("Telstra -

Investors", 2018).

Income statement

The income statement also known as statement of performance, is prepared to measure the

amount of profit created by the company. It also provides users with an idea about the

profitability of a concern (Buckland & Davis, 2016). Profit and loss is basically the difference

between the total income and total expense. If the difference is positive, it is profit and if it is

negative, there is a loss. A financial profit shows an increase in the owner’s equity and a loss

shows a decrease in the same. Income means earning benefits through reduction in liabilities

or inflow of assets (Hussey, 2011).

Introduction

Telstra Corporation Limited is a leading telecommunications and technology company

operating in Australia. The company builds telecommunication networks and provide product

and services like mobile, internet access, pay television and many other. It provides 17.4

million mobile services, 6.8 million fixed voice services and 3.5 million retail fixed

broadband services.

The vision and mission of the company is to connect more and more people and to provide

them more opportunities. For this, the company build simple and easy to use technology and

content solutions, making it the largest national mobile network of Australia ("Telstra",

2018).

Telstra was previously originated with the Australia Post as a government department but

now it is fully privatized. The CEO of the company is now focusing to make the company

more consumer focused by undergoing a change program. In August 2011, Telstra announces

to expand its customer services to social media having 24/7 coverage. By the end of

November 2012, the company enjoys the increase in its live chats and the growth rate of this

service has also increased to a great extent ("Telstra", 2018).

As of 2016, the company owns about 360 retail stores and more than 300 stores are equipped

with low energy Bluetooth beacons. After the privatization, the shares of Telstra has risen to

$5 per share in December 2013 to $6 per share in December 2014. The company is listed on

Australian Stock Exchange (ASX) and traded as ASX: TLS. The company is looking forward

to extend its growth in the international markets under the new CEO Andy Penn ("Telstra -

Investors", 2018).

Income statement

The income statement also known as statement of performance, is prepared to measure the

amount of profit created by the company. It also provides users with an idea about the

profitability of a concern (Buckland & Davis, 2016). Profit and loss is basically the difference

between the total income and total expense. If the difference is positive, it is profit and if it is

negative, there is a loss. A financial profit shows an increase in the owner’s equity and a loss

shows a decrease in the same. Income means earning benefits through reduction in liabilities

or inflow of assets (Hussey, 2011).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE 4

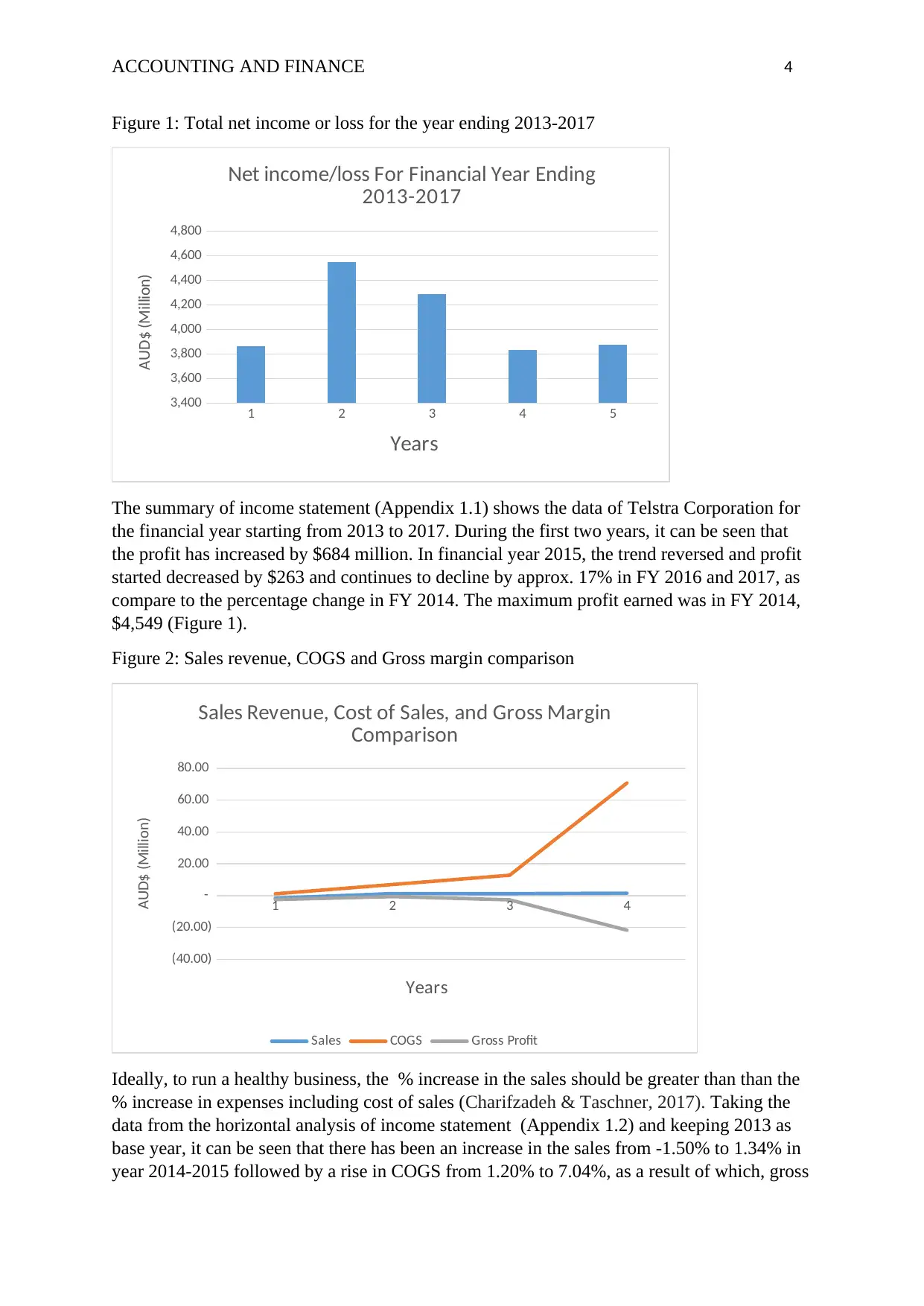

Figure 1: Total net income or loss for the year ending 2013-2017

1 2 3 4 5

3,400

3,600

3,800

4,000

4,200

4,400

4,600

4,800

Net income/loss For Financial Year Ending

2013-2017

Years

AUD$ (Million)

The summary of income statement (Appendix 1.1) shows the data of Telstra Corporation for

the financial year starting from 2013 to 2017. During the first two years, it can be seen that

the profit has increased by $684 million. In financial year 2015, the trend reversed and profit

started decreased by $263 and continues to decline by approx. 17% in FY 2016 and 2017, as

compare to the percentage change in FY 2014. The maximum profit earned was in FY 2014,

$4,549 (Figure 1).

Figure 2: Sales revenue, COGS and Gross margin comparison

1 2 3 4

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

Sales Revenue, Cost of Sales, and Gross Margin

Comparison

Sales COGS Gross Profit

Years

AUD$ (Million)

Ideally, to run a healthy business, the % increase in the sales should be greater than than the

% increase in expenses including cost of sales (Charifzadeh & Taschner, 2017). Taking the

data from the horizontal analysis of income statement (Appendix 1.2) and keeping 2013 as

base year, it can be seen that there has been an increase in the sales from -1.50% to 1.34% in

year 2014-2015 followed by a rise in COGS from 1.20% to 7.04%, as a result of which, gross

Figure 1: Total net income or loss for the year ending 2013-2017

1 2 3 4 5

3,400

3,600

3,800

4,000

4,200

4,400

4,600

4,800

Net income/loss For Financial Year Ending

2013-2017

Years

AUD$ (Million)

The summary of income statement (Appendix 1.1) shows the data of Telstra Corporation for

the financial year starting from 2013 to 2017. During the first two years, it can be seen that

the profit has increased by $684 million. In financial year 2015, the trend reversed and profit

started decreased by $263 and continues to decline by approx. 17% in FY 2016 and 2017, as

compare to the percentage change in FY 2014. The maximum profit earned was in FY 2014,

$4,549 (Figure 1).

Figure 2: Sales revenue, COGS and Gross margin comparison

1 2 3 4

(40.00)

(20.00)

-

20.00

40.00

60.00

80.00

Sales Revenue, Cost of Sales, and Gross Margin

Comparison

Sales COGS Gross Profit

Years

AUD$ (Million)

Ideally, to run a healthy business, the % increase in the sales should be greater than than the

% increase in expenses including cost of sales (Charifzadeh & Taschner, 2017). Taking the

data from the horizontal analysis of income statement (Appendix 1.2) and keeping 2013 as

base year, it can be seen that there has been an increase in the sales from -1.50% to 1.34% in

year 2014-2015 followed by a rise in COGS from 1.20% to 7.04%, as a result of which, gross

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 5

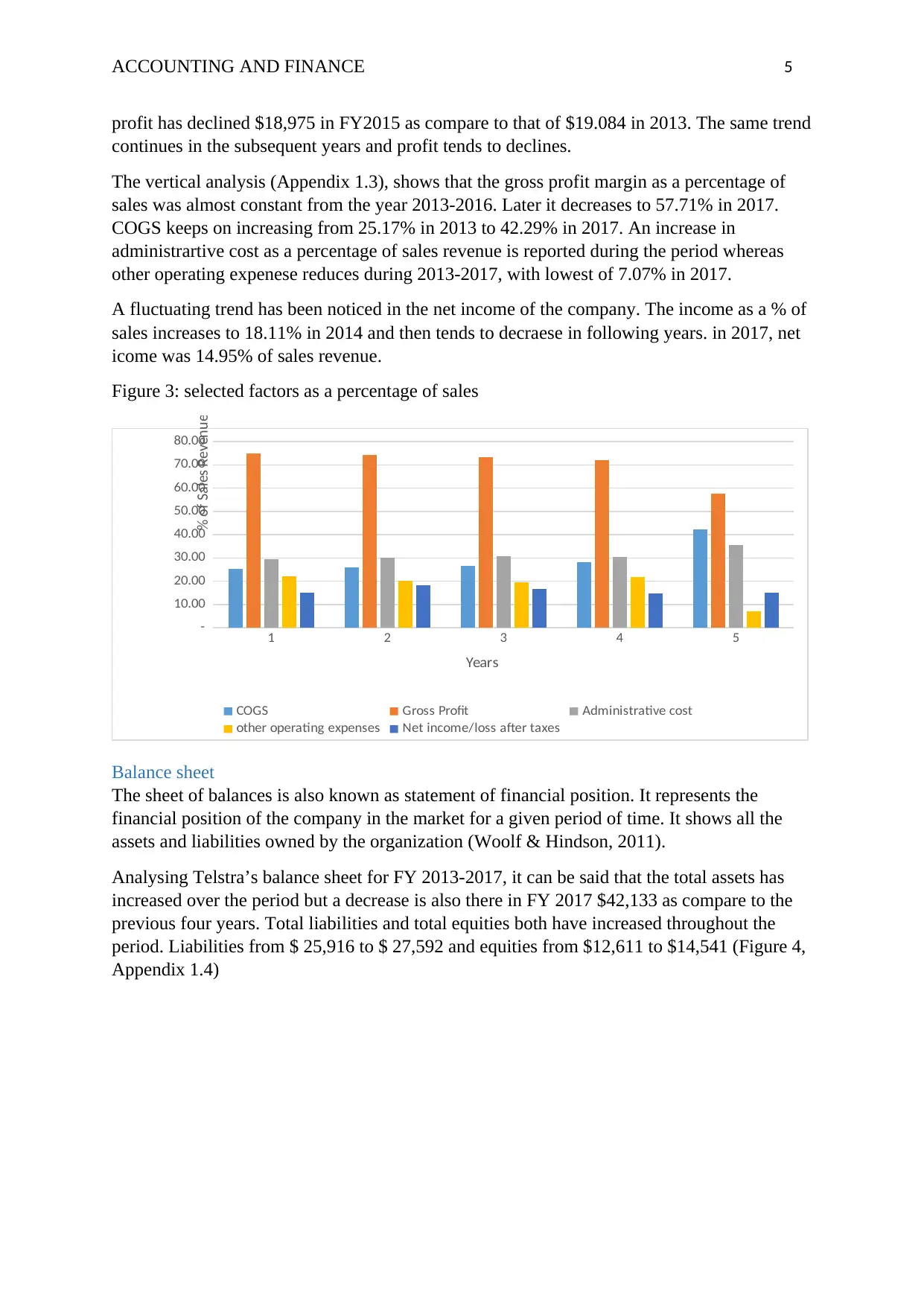

profit has declined $18,975 in FY2015 as compare to that of $19.084 in 2013. The same trend

continues in the subsequent years and profit tends to declines.

The vertical analysis (Appendix 1.3), shows that the gross profit margin as a percentage of

sales was almost constant from the year 2013-2016. Later it decreases to 57.71% in 2017.

COGS keeps on increasing from 25.17% in 2013 to 42.29% in 2017. An increase in

administrartive cost as a percentage of sales revenue is reported during the period whereas

other operating expenese reduces during 2013-2017, with lowest of 7.07% in 2017.

A fluctuating trend has been noticed in the net income of the company. The income as a % of

sales increases to 18.11% in 2014 and then tends to decraese in following years. in 2017, net

icome was 14.95% of sales revenue.

Figure 3: selected factors as a percentage of sales

1 2 3 4 5

-

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

COGS Gross Profit Administrative cost

other operating expenses Net income/loss after taxes

Years

% of Sales Revenue

Balance sheet

The sheet of balances is also known as statement of financial position. It represents the

financial position of the company in the market for a given period of time. It shows all the

assets and liabilities owned by the organization (Woolf & Hindson, 2011).

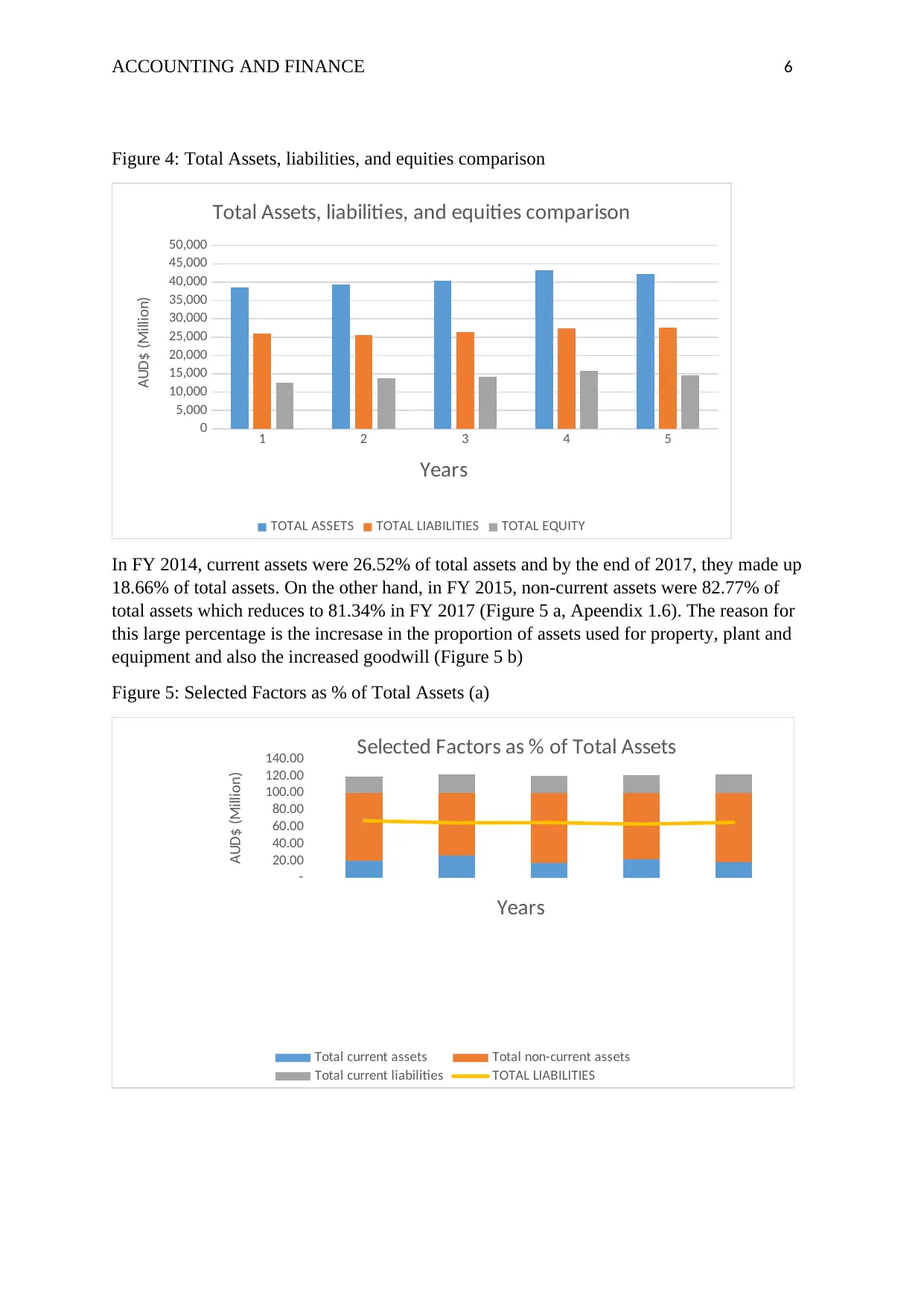

Analysing Telstra’s balance sheet for FY 2013-2017, it can be said that the total assets has

increased over the period but a decrease is also there in FY 2017 $42,133 as compare to the

previous four years. Total liabilities and total equities both have increased throughout the

period. Liabilities from $ 25,916 to $ 27,592 and equities from $12,611 to $14,541 (Figure 4,

Appendix 1.4)

profit has declined $18,975 in FY2015 as compare to that of $19.084 in 2013. The same trend

continues in the subsequent years and profit tends to declines.

The vertical analysis (Appendix 1.3), shows that the gross profit margin as a percentage of

sales was almost constant from the year 2013-2016. Later it decreases to 57.71% in 2017.

COGS keeps on increasing from 25.17% in 2013 to 42.29% in 2017. An increase in

administrartive cost as a percentage of sales revenue is reported during the period whereas

other operating expenese reduces during 2013-2017, with lowest of 7.07% in 2017.

A fluctuating trend has been noticed in the net income of the company. The income as a % of

sales increases to 18.11% in 2014 and then tends to decraese in following years. in 2017, net

icome was 14.95% of sales revenue.

Figure 3: selected factors as a percentage of sales

1 2 3 4 5

-

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

COGS Gross Profit Administrative cost

other operating expenses Net income/loss after taxes

Years

% of Sales Revenue

Balance sheet

The sheet of balances is also known as statement of financial position. It represents the

financial position of the company in the market for a given period of time. It shows all the

assets and liabilities owned by the organization (Woolf & Hindson, 2011).

Analysing Telstra’s balance sheet for FY 2013-2017, it can be said that the total assets has

increased over the period but a decrease is also there in FY 2017 $42,133 as compare to the

previous four years. Total liabilities and total equities both have increased throughout the

period. Liabilities from $ 25,916 to $ 27,592 and equities from $12,611 to $14,541 (Figure 4,

Appendix 1.4)

ACCOUNTING AND FINANCE 6

Figure 4: Total Assets, liabilities, and equities comparison

1 2 3 4 5

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Total Assets, liabilities, and equities comparison

TOTAL ASSETS TOTAL LIABILITIES TOTAL EQUITY

Years

AUD$ (Million)

In FY 2014, current assets were 26.52% of total assets and by the end of 2017, they made up

18.66% of total assets. On the other hand, in FY 2015, non-current assets were 82.77% of

total assets which reduces to 81.34% in FY 2017 (Figure 5 a, Apeendix 1.6). The reason for

this large percentage is the incresase in the proportion of assets used for property, plant and

equipment and also the increased goodwill (Figure 5 b)

Figure 5: Selected Factors as % of Total Assets (a)

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00 Selected Factors as % of Total Assets

Total current assets Total non-current assets

Total current liabilities TOTAL LIABILITIES

Years

AUD$ (Million)

Figure 4: Total Assets, liabilities, and equities comparison

1 2 3 4 5

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Total Assets, liabilities, and equities comparison

TOTAL ASSETS TOTAL LIABILITIES TOTAL EQUITY

Years

AUD$ (Million)

In FY 2014, current assets were 26.52% of total assets and by the end of 2017, they made up

18.66% of total assets. On the other hand, in FY 2015, non-current assets were 82.77% of

total assets which reduces to 81.34% in FY 2017 (Figure 5 a, Apeendix 1.6). The reason for

this large percentage is the incresase in the proportion of assets used for property, plant and

equipment and also the increased goodwill (Figure 5 b)

Figure 5: Selected Factors as % of Total Assets (a)

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00 Selected Factors as % of Total Assets

Total current assets Total non-current assets

Total current liabilities TOTAL LIABILITIES

Years

AUD$ (Million)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE 7

Figure 5: Selected Factors as % of Total Assets (b)

1 2 3 4 5

-

10.00

20.00

30.00

40.00

50.00

60.00

Selected Factors as % of Total Assets

Inventories Prepaid expenses

Property, Plant and equipment goodwill

Years

% of Total Assets

The reason for the increase in total liabilities over the period is the rise in current liabilities

including deferred revenues, short trem borrowings and other current liabilities. Total equities

has also increased in proportion to total assets. In FY 2013, equities were $12,611 (32.73%),

which gradually increased to $14,541 (34.51%) in FY 2017. Constant increase in retained

earnings and less fluctuation in value of common stock is the reason for increased equities

(Figure 6).

Figure 6: Change in Total Liabilities and Equities (%)

1 2 3 4 5

-

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

Change in total liabilities and equities (%)

TOTAL LIABILITIES TOTAL EQUITY

Years

% chnage

Cash Flow Statement

It is the statement which shows total cash inflows and total cash outflows of the company. It

gives an idea about the company’s cash movements for a particular time period (Vogel,

2014). Apart from examining the profit and loss statement and balance sheet of Talestra Ltd.,

Figure 5: Selected Factors as % of Total Assets (b)

1 2 3 4 5

-

10.00

20.00

30.00

40.00

50.00

60.00

Selected Factors as % of Total Assets

Inventories Prepaid expenses

Property, Plant and equipment goodwill

Years

% of Total Assets

The reason for the increase in total liabilities over the period is the rise in current liabilities

including deferred revenues, short trem borrowings and other current liabilities. Total equities

has also increased in proportion to total assets. In FY 2013, equities were $12,611 (32.73%),

which gradually increased to $14,541 (34.51%) in FY 2017. Constant increase in retained

earnings and less fluctuation in value of common stock is the reason for increased equities

(Figure 6).

Figure 6: Change in Total Liabilities and Equities (%)

1 2 3 4 5

-

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

Change in total liabilities and equities (%)

TOTAL LIABILITIES TOTAL EQUITY

Years

% chnage

Cash Flow Statement

It is the statement which shows total cash inflows and total cash outflows of the company. It

gives an idea about the company’s cash movements for a particular time period (Vogel,

2014). Apart from examining the profit and loss statement and balance sheet of Talestra Ltd.,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 8

it is also necessary to examine and evaluate its cash flow satement, just to know about the

cash position of the company and the problems related to it, if any.

Cash Flow from Operating Activities

It is the net flow of cash from company’s operations. Telstra’s operating cash flow had

fluctuated to great extent. In FY 2014, it was $8,613 which was more than $8,359 of 2013.

After that it continues to fall in subsequent years and reported at $7,775 in FY 2017.

Cash Flow from Investing Activities

Investing activities shows negative cash flow over the period of five years. Large variations

can be seen as in 2014, net cash used was $1,130 and it boost up to $5,692 in FY 2015. Then,

again it reduces in 2016 and increases in 2017 at $4,279. The reasons for these variations are

increase in the investments in plant and property and purchase of intangibles throughout the

year. The sale proceeds of intangibles and investment are compartive less.

Net cash inflow/outflow

The result of company’s cashflow activities comprises the net cash inflow and outflow. In FY

2014, it has increased from negative -$1,466 to positive $3,048. However, the trend changes

in 2015 and net cash become negative -$4,131. It again became positive in 2016 and then in

2017, it became negative -$2,614. The fluctuations in the cashflow activities are the result for

these variations.

Financial Ratio Analysis

Profitability ratios

Return on assets (ROA)

It is a ratio which gives an idea about how efficiently, a company is using its assets to make

revenue. It is calculated by dividing net income with company’s total assets (Barman &

Sengupta, 2017). Referring to (Appendix 1.9, Figure 7), it can be seen that ROA of Telstra

has been compared to ROA of Queste communications Ltd. Telstra’s ROA has dropped from

10.98% to 10.60% during FY 2014-2015. It again increases to 13.81% in year 2016 and then

reduces to 9.11% in year 2017. This fluctuation and reduction in FY 2017, shows that the

company is not able to produce more revenue from its assets as it is less efficient in managing

them. On the other hand, ROA of Queste remain negative throughout the period. In FY 2014,

it was -7.27% and in 2017 is was -20.67%.

it is also necessary to examine and evaluate its cash flow satement, just to know about the

cash position of the company and the problems related to it, if any.

Cash Flow from Operating Activities

It is the net flow of cash from company’s operations. Telstra’s operating cash flow had

fluctuated to great extent. In FY 2014, it was $8,613 which was more than $8,359 of 2013.

After that it continues to fall in subsequent years and reported at $7,775 in FY 2017.

Cash Flow from Investing Activities

Investing activities shows negative cash flow over the period of five years. Large variations

can be seen as in 2014, net cash used was $1,130 and it boost up to $5,692 in FY 2015. Then,

again it reduces in 2016 and increases in 2017 at $4,279. The reasons for these variations are

increase in the investments in plant and property and purchase of intangibles throughout the

year. The sale proceeds of intangibles and investment are compartive less.

Net cash inflow/outflow

The result of company’s cashflow activities comprises the net cash inflow and outflow. In FY

2014, it has increased from negative -$1,466 to positive $3,048. However, the trend changes

in 2015 and net cash become negative -$4,131. It again became positive in 2016 and then in

2017, it became negative -$2,614. The fluctuations in the cashflow activities are the result for

these variations.

Financial Ratio Analysis

Profitability ratios

Return on assets (ROA)

It is a ratio which gives an idea about how efficiently, a company is using its assets to make

revenue. It is calculated by dividing net income with company’s total assets (Barman &

Sengupta, 2017). Referring to (Appendix 1.9, Figure 7), it can be seen that ROA of Telstra

has been compared to ROA of Queste communications Ltd. Telstra’s ROA has dropped from

10.98% to 10.60% during FY 2014-2015. It again increases to 13.81% in year 2016 and then

reduces to 9.11% in year 2017. This fluctuation and reduction in FY 2017, shows that the

company is not able to produce more revenue from its assets as it is less efficient in managing

them. On the other hand, ROA of Queste remain negative throughout the period. In FY 2014,

it was -7.27% and in 2017 is was -20.67%.

ACCOUNTING AND FINANCE 9

Figure 7: ROA

1 2 3 4

0.0

5000.0

10000.0

15000.0

20000.0

25000.0

30000.0

35000.0

40000.0

45000.0

50000.0

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Return on Assets (Telstra Corporation Ltd.)

Net income Total assets

Average total assets ROA

Years

AUD$ (Million)

Return on Equity

The ROE of Telstra was almost same fo year 2014 and 2016, whereas it was highest in 2017

at 25.72% (figure 8). In comparision to this, Queste’s ROE was negative in all the years. in

FY 2014 and 2016, it was almost same and in 2017 it was -21.97%, highest among all

(Appendix 1.9).

Figure8: ROE

1 2 3 4

0.0

5000.0

10000.0

15000.0

20000.0

25000.0

-

5.00

10.00

15.00

20.00

25.00

30.00

Return on Equity (Telstra Corporation Ltd.)

Net income available for equity shareholders

Total Equity

Average Equity

ROE

Years

AUD$ (Million)

%

Efficiency ratios

These ratios indicate how effectively and efficiently company manages its assets and

liabilities. They are used to measure company’s short term performance (Jordan, 2014). A

comparison of all the efficiency ratios between Telstra and Queste is done in Appendix 1.10.

Figure 7: ROA

1 2 3 4

0.0

5000.0

10000.0

15000.0

20000.0

25000.0

30000.0

35000.0

40000.0

45000.0

50000.0

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Return on Assets (Telstra Corporation Ltd.)

Net income Total assets

Average total assets ROA

Years

AUD$ (Million)

Return on Equity

The ROE of Telstra was almost same fo year 2014 and 2016, whereas it was highest in 2017

at 25.72% (figure 8). In comparision to this, Queste’s ROE was negative in all the years. in

FY 2014 and 2016, it was almost same and in 2017 it was -21.97%, highest among all

(Appendix 1.9).

Figure8: ROE

1 2 3 4

0.0

5000.0

10000.0

15000.0

20000.0

25000.0

-

5.00

10.00

15.00

20.00

25.00

30.00

Return on Equity (Telstra Corporation Ltd.)

Net income available for equity shareholders

Total Equity

Average Equity

ROE

Years

AUD$ (Million)

%

Efficiency ratios

These ratios indicate how effectively and efficiently company manages its assets and

liabilities. They are used to measure company’s short term performance (Jordan, 2014). A

comparison of all the efficiency ratios between Telstra and Queste is done in Appendix 1.10.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE 10

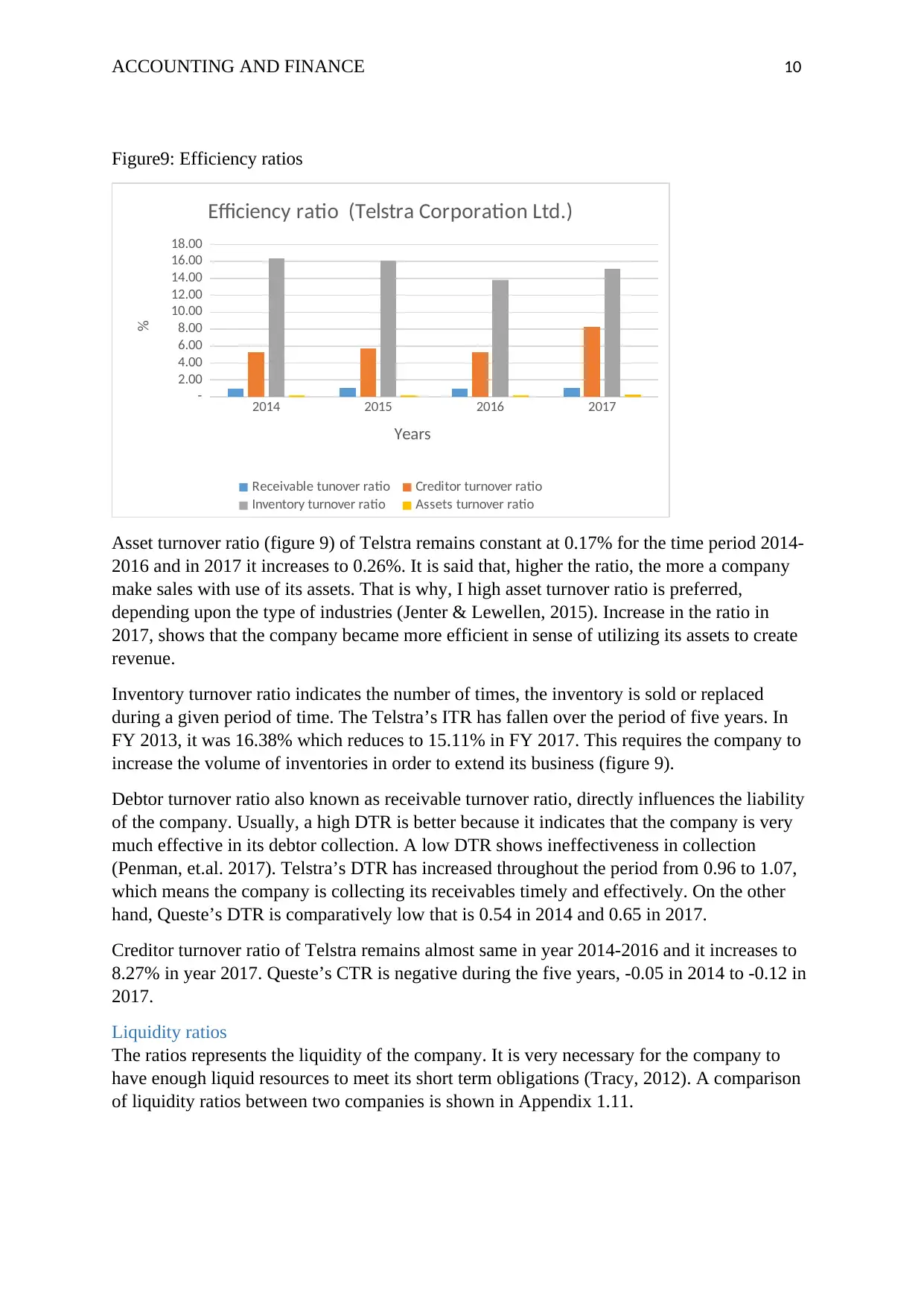

Figure9: Efficiency ratios

2014 2015 2016 2017

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Efficiency ratio (Telstra Corporation Ltd.)

Receivable tunover ratio Creditor turnover ratio

Inventory turnover ratio Assets turnover ratio

Years

%

Asset turnover ratio (figure 9) of Telstra remains constant at 0.17% for the time period 2014-

2016 and in 2017 it increases to 0.26%. It is said that, higher the ratio, the more a company

make sales with use of its assets. That is why, I high asset turnover ratio is preferred,

depending upon the type of industries (Jenter & Lewellen, 2015). Increase in the ratio in

2017, shows that the company became more efficient in sense of utilizing its assets to create

revenue.

Inventory turnover ratio indicates the number of times, the inventory is sold or replaced

during a given period of time. The Telstra’s ITR has fallen over the period of five years. In

FY 2013, it was 16.38% which reduces to 15.11% in FY 2017. This requires the company to

increase the volume of inventories in order to extend its business (figure 9).

Debtor turnover ratio also known as receivable turnover ratio, directly influences the liability

of the company. Usually, a high DTR is better because it indicates that the company is very

much effective in its debtor collection. A low DTR shows ineffectiveness in collection

(Penman, et.al. 2017). Telstra’s DTR has increased throughout the period from 0.96 to 1.07,

which means the company is collecting its receivables timely and effectively. On the other

hand, Queste’s DTR is comparatively low that is 0.54 in 2014 and 0.65 in 2017.

Creditor turnover ratio of Telstra remains almost same in year 2014-2016 and it increases to

8.27% in year 2017. Queste’s CTR is negative during the five years, -0.05 in 2014 to -0.12 in

2017.

Liquidity ratios

The ratios represents the liquidity of the company. It is very necessary for the company to

have enough liquid resources to meet its short term obligations (Tracy, 2012). A comparison

of liquidity ratios between two companies is shown in Appendix 1.11.

Figure9: Efficiency ratios

2014 2015 2016 2017

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Efficiency ratio (Telstra Corporation Ltd.)

Receivable tunover ratio Creditor turnover ratio

Inventory turnover ratio Assets turnover ratio

Years

%

Asset turnover ratio (figure 9) of Telstra remains constant at 0.17% for the time period 2014-

2016 and in 2017 it increases to 0.26%. It is said that, higher the ratio, the more a company

make sales with use of its assets. That is why, I high asset turnover ratio is preferred,

depending upon the type of industries (Jenter & Lewellen, 2015). Increase in the ratio in

2017, shows that the company became more efficient in sense of utilizing its assets to create

revenue.

Inventory turnover ratio indicates the number of times, the inventory is sold or replaced

during a given period of time. The Telstra’s ITR has fallen over the period of five years. In

FY 2013, it was 16.38% which reduces to 15.11% in FY 2017. This requires the company to

increase the volume of inventories in order to extend its business (figure 9).

Debtor turnover ratio also known as receivable turnover ratio, directly influences the liability

of the company. Usually, a high DTR is better because it indicates that the company is very

much effective in its debtor collection. A low DTR shows ineffectiveness in collection

(Penman, et.al. 2017). Telstra’s DTR has increased throughout the period from 0.96 to 1.07,

which means the company is collecting its receivables timely and effectively. On the other

hand, Queste’s DTR is comparatively low that is 0.54 in 2014 and 0.65 in 2017.

Creditor turnover ratio of Telstra remains almost same in year 2014-2016 and it increases to

8.27% in year 2017. Queste’s CTR is negative during the five years, -0.05 in 2014 to -0.12 in

2017.

Liquidity ratios

The ratios represents the liquidity of the company. It is very necessary for the company to

have enough liquid resources to meet its short term obligations (Tracy, 2012). A comparison

of liquidity ratios between two companies is shown in Appendix 1.11.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 11

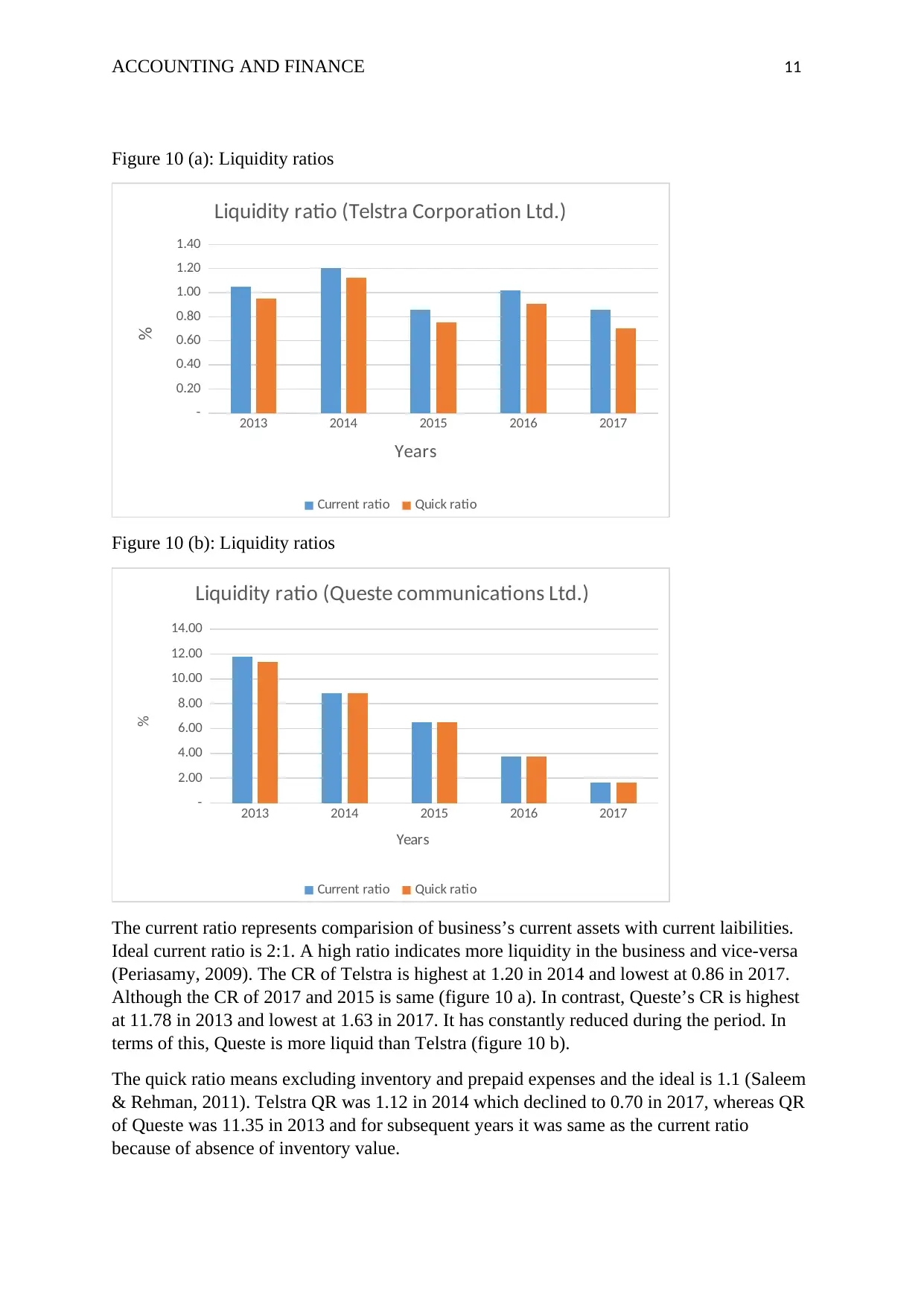

Figure 10 (a): Liquidity ratios

2013 2014 2015 2016 2017

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Liquidity ratio (Telstra Corporation Ltd.)

Current ratio Quick ratio

Years

%

Figure 10 (b): Liquidity ratios

2013 2014 2015 2016 2017

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Liquidity ratio (Queste communications Ltd.)

Current ratio Quick ratio

Years

%

The current ratio represents comparision of business’s current assets with current laibilities.

Ideal current ratio is 2:1. A high ratio indicates more liquidity in the business and vice-versa

(Periasamy, 2009). The CR of Telstra is highest at 1.20 in 2014 and lowest at 0.86 in 2017.

Although the CR of 2017 and 2015 is same (figure 10 a). In contrast, Queste’s CR is highest

at 11.78 in 2013 and lowest at 1.63 in 2017. It has constantly reduced during the period. In

terms of this, Queste is more liquid than Telstra (figure 10 b).

The quick ratio means excluding inventory and prepaid expenses and the ideal is 1.1 (Saleem

& Rehman, 2011). Telstra QR was 1.12 in 2014 which declined to 0.70 in 2017, whereas QR

of Queste was 11.35 in 2013 and for subsequent years it was same as the current ratio

because of absence of inventory value.

Figure 10 (a): Liquidity ratios

2013 2014 2015 2016 2017

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Liquidity ratio (Telstra Corporation Ltd.)

Current ratio Quick ratio

Years

%

Figure 10 (b): Liquidity ratios

2013 2014 2015 2016 2017

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Liquidity ratio (Queste communications Ltd.)

Current ratio Quick ratio

Years

%

The current ratio represents comparision of business’s current assets with current laibilities.

Ideal current ratio is 2:1. A high ratio indicates more liquidity in the business and vice-versa

(Periasamy, 2009). The CR of Telstra is highest at 1.20 in 2014 and lowest at 0.86 in 2017.

Although the CR of 2017 and 2015 is same (figure 10 a). In contrast, Queste’s CR is highest

at 11.78 in 2013 and lowest at 1.63 in 2017. It has constantly reduced during the period. In

terms of this, Queste is more liquid than Telstra (figure 10 b).

The quick ratio means excluding inventory and prepaid expenses and the ideal is 1.1 (Saleem

& Rehman, 2011). Telstra QR was 1.12 in 2014 which declined to 0.70 in 2017, whereas QR

of Queste was 11.35 in 2013 and for subsequent years it was same as the current ratio

because of absence of inventory value.

ACCOUNTING AND FINANCE 12

Capital structure ratio

Capital structure or gearing ratio (Appendix 1.12) helps the company in determining the level

of risk and long term solvency. If the portion of debt is too high then there will be a risk for

business, to become insolvent (Levi & Segal, 2015). The summary of capital structure ratios

is given in Appendix 1.12.

Debt to equity ratio, Debt ratio and Equity ratios shows the extent to which company has

raised funds through outsiders. It is an important factor to be considered while assessing the

risk. Analysis shows that D/E ratio of Telstra has reduced from 2.06% to 1.90% over the

period. The debt ratio stands at 0.67% in 2013 to 0.65% in 2017. Equity ratio has also

increased from 0.33% to 0.35%

D/E ratio of Queste has almost remain same during the years except in 2017, where it was

0.10%. Debt ratio has risen from 0.4% to 0.9% and equity ratio has decreased during the

period from 0.96% to 0.91%. The portion of debt is more in Queste as compare to Telstra.

Conclusion

The report concludes that the financial analysis of Telstra Corporation Ltd. for years 2013-

2017, represents significant changes in the performance and position of the company. Sales

has grown over the period as it was highest $25,912 in 2017 with the increased COGS of

$10,958 in same year, resulting in decreasing gross profit margin. Total assets and liabilities

both have increased during this period which results in declining net profit. The company’s

cash flow statement has also shown negative cash flows in year 2013, 2015 and 2017,

indicating the state of company’s liquidity and solvency.

Ratio analysis is been used to measure the overall performance of Telstra comparing to

Queste Communications Ltd. Profitability, efficiency, liquidity and capital structure ratios are

used to investigate about the company’s financial performance. Overall it is concluded that,

Telstra is performing pretty well as compare to Queste and is more efficient and effective in

terms of earning profits.

Capital structure ratio

Capital structure or gearing ratio (Appendix 1.12) helps the company in determining the level

of risk and long term solvency. If the portion of debt is too high then there will be a risk for

business, to become insolvent (Levi & Segal, 2015). The summary of capital structure ratios

is given in Appendix 1.12.

Debt to equity ratio, Debt ratio and Equity ratios shows the extent to which company has

raised funds through outsiders. It is an important factor to be considered while assessing the

risk. Analysis shows that D/E ratio of Telstra has reduced from 2.06% to 1.90% over the

period. The debt ratio stands at 0.67% in 2013 to 0.65% in 2017. Equity ratio has also

increased from 0.33% to 0.35%

D/E ratio of Queste has almost remain same during the years except in 2017, where it was

0.10%. Debt ratio has risen from 0.4% to 0.9% and equity ratio has decreased during the

period from 0.96% to 0.91%. The portion of debt is more in Queste as compare to Telstra.

Conclusion

The report concludes that the financial analysis of Telstra Corporation Ltd. for years 2013-

2017, represents significant changes in the performance and position of the company. Sales

has grown over the period as it was highest $25,912 in 2017 with the increased COGS of

$10,958 in same year, resulting in decreasing gross profit margin. Total assets and liabilities

both have increased during this period which results in declining net profit. The company’s

cash flow statement has also shown negative cash flows in year 2013, 2015 and 2017,

indicating the state of company’s liquidity and solvency.

Ratio analysis is been used to measure the overall performance of Telstra comparing to

Queste Communications Ltd. Profitability, efficiency, liquidity and capital structure ratios are

used to investigate about the company’s financial performance. Overall it is concluded that,

Telstra is performing pretty well as compare to Queste and is more efficient and effective in

terms of earning profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.