Corporate Accounting: Comparative Financial Analysis of Telstra & TPG

VerifiedAdded on 2023/06/07

|19

|4925

|99

Report

AI Summary

This report provides a comparative financial analysis of Telstra Corporation Limited and TPG Telecom Limited, two companies operating in the telecommunications industry. The analysis covers a three-year period, focusing on key components of their financial statements, including owner's equity, capital structure, and cash flow statements. It examines trends in retained earnings, debt levels, and the use of equity versus debt financing. The report also delves into the companies' income tax accounting practices, calculating effective tax rates and distinguishing between cash and book tax rates. The analysis provides insights into the financial strategies and performance of both Telstra and TPG.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

University Name

Student Name

Authors’ Note

Corporate Accounting

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Executive Summary

The primary intention of the study is to evaluate financial assertions of two firms for three

years. The current report presents the companies that are chosen for this assessment are

Telstra Corporation Limited and TPG Telecom Limited. The report evaluates diverse

components that are revealed in the yearly account for instance Income tax expenditures. The

current report evaluates flow of cash statement thoroughly for both the firms in a bid to

analyse streams of cash of the corporation during the period. The analysis undertakes a

relative analysis of statement of stream of cash between Telstra Corporation Limited and

TPG Telecom Limited. The evaluation also entails computation of effective rate of tax and

tax rates (Cash as well as Book) and presents an elucidation of tax expends and tax

framework of both the firms.

CORPORATE ACCOUNTING

Executive Summary

The primary intention of the study is to evaluate financial assertions of two firms for three

years. The current report presents the companies that are chosen for this assessment are

Telstra Corporation Limited and TPG Telecom Limited. The report evaluates diverse

components that are revealed in the yearly account for instance Income tax expenditures. The

current report evaluates flow of cash statement thoroughly for both the firms in a bid to

analyse streams of cash of the corporation during the period. The analysis undertakes a

relative analysis of statement of stream of cash between Telstra Corporation Limited and

TPG Telecom Limited. The evaluation also entails computation of effective rate of tax and

tax rates (Cash as well as Book) and presents an elucidation of tax expends and tax

framework of both the firms.

2

CORPORATE ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

Owner’s Equity..........................................................................................................................4

Capital Structure Position of Both the Companies....................................................................6

Comparative Evaluation of Three different Components of Statement of Cash Flow........10

Insight of Cash flow Statement............................................................................................11

Analysis of Other Comprehensive Income Statement.............................................................11

Reporting of Comprehensive Items.....................................................................................12

Comparative Analysis of Comprehensive Items..................................................................12

Accounting for the purpose of Income Tax.........................................................................13

Effective Rate of Tax...........................................................................................................13

Deferred Tax Assets and Liabilities.....................................................................................14

Cash Tax Amount and Rate of Both Company....................................................................15

Distinction Between Cash Tax Rate and Book Tax Rate....................................................16

References................................................................................................................................17

CORPORATE ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

Owner’s Equity..........................................................................................................................4

Capital Structure Position of Both the Companies....................................................................6

Comparative Evaluation of Three different Components of Statement of Cash Flow........10

Insight of Cash flow Statement............................................................................................11

Analysis of Other Comprehensive Income Statement.............................................................11

Reporting of Comprehensive Items.....................................................................................12

Comparative Analysis of Comprehensive Items..................................................................12

Accounting for the purpose of Income Tax.........................................................................13

Effective Rate of Tax...........................................................................................................13

Deferred Tax Assets and Liabilities.....................................................................................14

Cash Tax Amount and Rate of Both Company....................................................................15

Distinction Between Cash Tax Rate and Book Tax Rate....................................................16

References................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

Introduction

The primary aim of this report is to analyze financial assertions of two different firms that

operate in the same industry and has related operations levels. In essence, the two different

firms that are chosen for this report are Telstra Corporation Limited and TPG Telecom

Limited that are both engaged in telecommunication business. Essentially, the analysis takes

into account yearly reports of both the firm for the purpose of assessing different components

of financial assertions and also presents a comparative evaluation between the two firms and

this has a superior reporting of these components of annual reports.

Telstra is a leading telecommunications as well as technology company in the nation

Australia, providing a wide range of communications services and competing in different

markets of telecommunications. In the nation Australia, it is important to offer 17.7 million

mobile services in the retail market, 4.9 million fixed voice services in the retail segment and

3.6 million fixed broadband services in the retail section.

TPG Telecom Limited refers to an Australian telecommunications as well as IT firm that

concentrates in consumer as well as business internet services with mobile telephone

services. During the period August of the year 2015, TPG Telecom Limited is the second

internet service provider in the nation Australia and functions as the prime operator of mobile

virtual network. The company TPG delivers five different ranges of products as well as

services counting mobile phone service, internet accessibility, software in accounting,

networking as well as OEM services.

The primary emphasis of the report can help in analysis of yearly reports of both the firms for

a period of past three successive years beginning from the period 2017. The appraisal also

reflects examination and relative study of the components that are reflected in the yearly

reports of the company. There are certain important areas that are regarded in the yearly

CORPORATE ACCOUNTING

Introduction

The primary aim of this report is to analyze financial assertions of two different firms that

operate in the same industry and has related operations levels. In essence, the two different

firms that are chosen for this report are Telstra Corporation Limited and TPG Telecom

Limited that are both engaged in telecommunication business. Essentially, the analysis takes

into account yearly reports of both the firm for the purpose of assessing different components

of financial assertions and also presents a comparative evaluation between the two firms and

this has a superior reporting of these components of annual reports.

Telstra is a leading telecommunications as well as technology company in the nation

Australia, providing a wide range of communications services and competing in different

markets of telecommunications. In the nation Australia, it is important to offer 17.7 million

mobile services in the retail market, 4.9 million fixed voice services in the retail segment and

3.6 million fixed broadband services in the retail section.

TPG Telecom Limited refers to an Australian telecommunications as well as IT firm that

concentrates in consumer as well as business internet services with mobile telephone

services. During the period August of the year 2015, TPG Telecom Limited is the second

internet service provider in the nation Australia and functions as the prime operator of mobile

virtual network. The company TPG delivers five different ranges of products as well as

services counting mobile phone service, internet accessibility, software in accounting,

networking as well as OEM services.

The primary emphasis of the report can help in analysis of yearly reports of both the firms for

a period of past three successive years beginning from the period 2017. The appraisal also

reflects examination and relative study of the components that are reflected in the yearly

reports of the company. There are certain important areas that are regarded in the yearly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

statements of both the firms are cash flow declarations, equity capital utilized, treatments and

revelations of tax. Furthermore, the appraisal shall contain enumerations concerning effectual

rate of tax as well as other tax enumerations.

Discussion

Owner’s Equity

The equity of the firm reflects equity capital and retained earnings of the firm that is utilized

for funding the actions of the firm (Wahlen et al. 2014). The yearly account of the period

2017 is regarded for both the firms for evaluating equity of owner of the particular business.

According to the yearly statement of the period 2017 for Telstra Corporation Limited, the

equity of the owner is reflected in the balance sheet statement. The equity of the owner of

Telstra Corporation Limited comprises of equity, firm’s retained earnings as well as other

reserves. The equity of the firm indicates towards the share capital that the firm has acquired

by means of public issuance of shares. The figure for equity of the firm for the year 2017 is

observed to be $ 14560 million that has decreased from $15907 million recorded during the

year 2016 (DeFusco et al. 2015). In essence, retained earnings registered for the firm

represent particular a division of profits that are kept to one side either for the purpose of

reinvestment of the same in the operations of the corporation or for the purpose of satisfying

specific obligations of the enterprise. Particularly, the retained earnings of the enterprise

during the financial year 2017 have considerably decreased in comparison to previous year

analysis and the same is observed to be $ 10225 million in 2017 as compared to the year ago

figure of $10642 million in 2016. As a result, it can be hereby mentioned that there is a

general downward moving trajectory for the retained earnings of the firm that reflects

decrease in overall retained earnings of the enterprise. Basically, this might be owing to the

decrease in profitability of the firm from continuing as well as discontinuing operations.

CORPORATE ACCOUNTING

statements of both the firms are cash flow declarations, equity capital utilized, treatments and

revelations of tax. Furthermore, the appraisal shall contain enumerations concerning effectual

rate of tax as well as other tax enumerations.

Discussion

Owner’s Equity

The equity of the firm reflects equity capital and retained earnings of the firm that is utilized

for funding the actions of the firm (Wahlen et al. 2014). The yearly account of the period

2017 is regarded for both the firms for evaluating equity of owner of the particular business.

According to the yearly statement of the period 2017 for Telstra Corporation Limited, the

equity of the owner is reflected in the balance sheet statement. The equity of the owner of

Telstra Corporation Limited comprises of equity, firm’s retained earnings as well as other

reserves. The equity of the firm indicates towards the share capital that the firm has acquired

by means of public issuance of shares. The figure for equity of the firm for the year 2017 is

observed to be $ 14560 million that has decreased from $15907 million recorded during the

year 2016 (DeFusco et al. 2015). In essence, retained earnings registered for the firm

represent particular a division of profits that are kept to one side either for the purpose of

reinvestment of the same in the operations of the corporation or for the purpose of satisfying

specific obligations of the enterprise. Particularly, the retained earnings of the enterprise

during the financial year 2017 have considerably decreased in comparison to previous year

analysis and the same is observed to be $ 10225 million in 2017 as compared to the year ago

figure of $10642 million in 2016. As a result, it can be hereby mentioned that there is a

general downward moving trajectory for the retained earnings of the firm that reflects

decrease in overall retained earnings of the enterprise. Basically, this might be owing to the

decrease in profitability of the firm from continuing as well as discontinuing operations.

5

CORPORATE ACCOUNTING

Also, the reserves of the firm are registered to be negative which reflects accumulated losses

of the firm as compared to the figure registered during the previous year.

. The equity share capital of the firm has also decreased to the level of $ 4421 million

recorded in financial year 2017 from $5167 million registered during financial year 2016. As

suggested by Weygandt et al. (2015), the equity capital reflects the funds that are essentially

utilized by the enterprise for the purpose of satisfying various obligations. The figure on

reserves mentioned in the section of equity in the balance sheet statement of the firm is

observed to be negative that implies that the enterprise has accumulated losses (Nobes 2014).

The share capital indicated in the balance sheet statement of Telstra has significantly declined

as compared to the year ago period. In essence, this might be owing to the fact that enterprise

has a reduction in capital and the total number of shares in the enterprise has decreased by the

amount of reduction (Bekaert and Hodrick 2017). The retained earnings of the enterprise are

observed to be $ 10225 million. Based on the registered figures on retained earnings of the

enterprise that has decreased during FY 2017 it can be said that retained earnings of the

enterprise is affected by the decrease in net earnings as well as payment of dividends to the

company’s shareholders. Consequently, the items that exert impact on net earnings and push

it at higher or else lower level shall necessarily influence the retained earnings of the

corporation.

Again, various elements of equity of the owner of the firm TPG that is shown in the yearly

declaration of the enterprise for the financial year 2017 include equity share capital of the

enterprise, retained earnings and reserves. The equity share capital of TPG has considerably

improved to $1449.4 million in the financial year 2017 as compared to the year ago figure of

1051.8 million registered in financial year 2016. This may perhaps because of increase in

overall issuance of shares and improvement in overall operational framework of the firm.

However, the reserves of the company TPG is registered to be negative and that stands at

CORPORATE ACCOUNTING

Also, the reserves of the firm are registered to be negative which reflects accumulated losses

of the firm as compared to the figure registered during the previous year.

. The equity share capital of the firm has also decreased to the level of $ 4421 million

recorded in financial year 2017 from $5167 million registered during financial year 2016. As

suggested by Weygandt et al. (2015), the equity capital reflects the funds that are essentially

utilized by the enterprise for the purpose of satisfying various obligations. The figure on

reserves mentioned in the section of equity in the balance sheet statement of the firm is

observed to be negative that implies that the enterprise has accumulated losses (Nobes 2014).

The share capital indicated in the balance sheet statement of Telstra has significantly declined

as compared to the year ago period. In essence, this might be owing to the fact that enterprise

has a reduction in capital and the total number of shares in the enterprise has decreased by the

amount of reduction (Bekaert and Hodrick 2017). The retained earnings of the enterprise are

observed to be $ 10225 million. Based on the registered figures on retained earnings of the

enterprise that has decreased during FY 2017 it can be said that retained earnings of the

enterprise is affected by the decrease in net earnings as well as payment of dividends to the

company’s shareholders. Consequently, the items that exert impact on net earnings and push

it at higher or else lower level shall necessarily influence the retained earnings of the

corporation.

Again, various elements of equity of the owner of the firm TPG that is shown in the yearly

declaration of the enterprise for the financial year 2017 include equity share capital of the

enterprise, retained earnings and reserves. The equity share capital of TPG has considerably

improved to $1449.4 million in the financial year 2017 as compared to the year ago figure of

1051.8 million registered in financial year 2016. This may perhaps because of increase in

overall issuance of shares and improvement in overall operational framework of the firm.

However, the reserves of the company TPG is registered to be negative and that stands at

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

$(18.1) million in 2017 in comparison to previous period’s figure of $41.2 million in 2016,

reflecting accumulates loss of the firm. However, the retained earnings of the firm has

enhanced considerably from $681 million in 2016 to around $963.3 million. This is said to be

influenced by the net income registered during the period and payments for dividends of the

enterprise.

Capital Structure Position of Both the Companies

The gross position of debt of the firm Telstra Corporation Limited during the financial year

2017 was registered to be $16,218 million (Telstra.com.au 2018). The debt position

comprises of the borrowings of the firm recorded to be $17,284 million along with net

derivative assets of the firm that stands at $1,066 million. In the regard, it can be said that

Gross debt of the enterprise is somewhat alike to that of the period 2016 ($16,009 million).

This occurs as a consequence of enhancement in debt by $2,215 million during the period

that was being chiefly offset by debt maturities worth $ 2,207 million. Thus, it can be said

that net debt of the firm Telstra has increased by approximately $2821 million compared to

the prior year. In essence, this specific movement is primarily due enhancement in gross debt

of around $209 million and a decline in overall cash as well as cash equivalents of

approximately $2612 million (Telstra.com.au 2018). The gearing ratio of the firm is reported

to be 51.2% and is observed to have increased from 49.3% recorded during the financial year

2016. This reflects greater use of debt in place of equity for financing operations of the

enterprise. Nevertheless, the company is within the comfort zone of the credit metrics.

In the case of the firm TPG, the balance sheet of the firm for the year 2017 reflects that the

net borrowings as well as loans of the firm is registered to be $872.4 million and this figure is

net of costs of borrowing (prepaid). Analysis of the balance sheet statement of the firm

reveals that the gross borrowings of the firm recorded to be $932.5 million comprises of bank

CORPORATE ACCOUNTING

$(18.1) million in 2017 in comparison to previous period’s figure of $41.2 million in 2016,

reflecting accumulates loss of the firm. However, the retained earnings of the firm has

enhanced considerably from $681 million in 2016 to around $963.3 million. This is said to be

influenced by the net income registered during the period and payments for dividends of the

enterprise.

Capital Structure Position of Both the Companies

The gross position of debt of the firm Telstra Corporation Limited during the financial year

2017 was registered to be $16,218 million (Telstra.com.au 2018). The debt position

comprises of the borrowings of the firm recorded to be $17,284 million along with net

derivative assets of the firm that stands at $1,066 million. In the regard, it can be said that

Gross debt of the enterprise is somewhat alike to that of the period 2016 ($16,009 million).

This occurs as a consequence of enhancement in debt by $2,215 million during the period

that was being chiefly offset by debt maturities worth $ 2,207 million. Thus, it can be said

that net debt of the firm Telstra has increased by approximately $2821 million compared to

the prior year. In essence, this specific movement is primarily due enhancement in gross debt

of around $209 million and a decline in overall cash as well as cash equivalents of

approximately $2612 million (Telstra.com.au 2018). The gearing ratio of the firm is reported

to be 51.2% and is observed to have increased from 49.3% recorded during the financial year

2016. This reflects greater use of debt in place of equity for financing operations of the

enterprise. Nevertheless, the company is within the comfort zone of the credit metrics.

In the case of the firm TPG, the balance sheet of the firm for the year 2017 reflects that the

net borrowings as well as loans of the firm is registered to be $872.4 million and this figure is

net of costs of borrowing (prepaid). Analysis of the balance sheet statement of the firm

reveals that the gross borrowings of the firm recorded to be $932.5 million comprises of bank

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

debt worth $900 million as well as liabilities of lease worth $32.5 million. Considering bank

debt and balance of cash, the net debt of the firm stands at $853.7 million in the financial year

2017. However, the equity of the firm is recorded to be 2399.3 in 2017 and is said to have

enhanced in the period 2017 as compared to the year ago period of 2016. Thus, this firm TPG

is said to have a low gearing ratio reflecting proportionately less debt financing as compared

to debt financing.

Thus, the examination of the debt as well as equity capital that is utilised by both the firm

reveals the fact that Telstra is more dependent on debt financing whereas the management of

TPG is more dependent on equity capital in contrast since the enterprise is striving to

decrease the level of debt capital that is utilized by the enterprise.

Analysis of the statement of Cash Flow

The cash flow announcement reflects overall position of cash of the business

enterprise elucidates comprehensively both inflow as well as outflow of cash for the business.

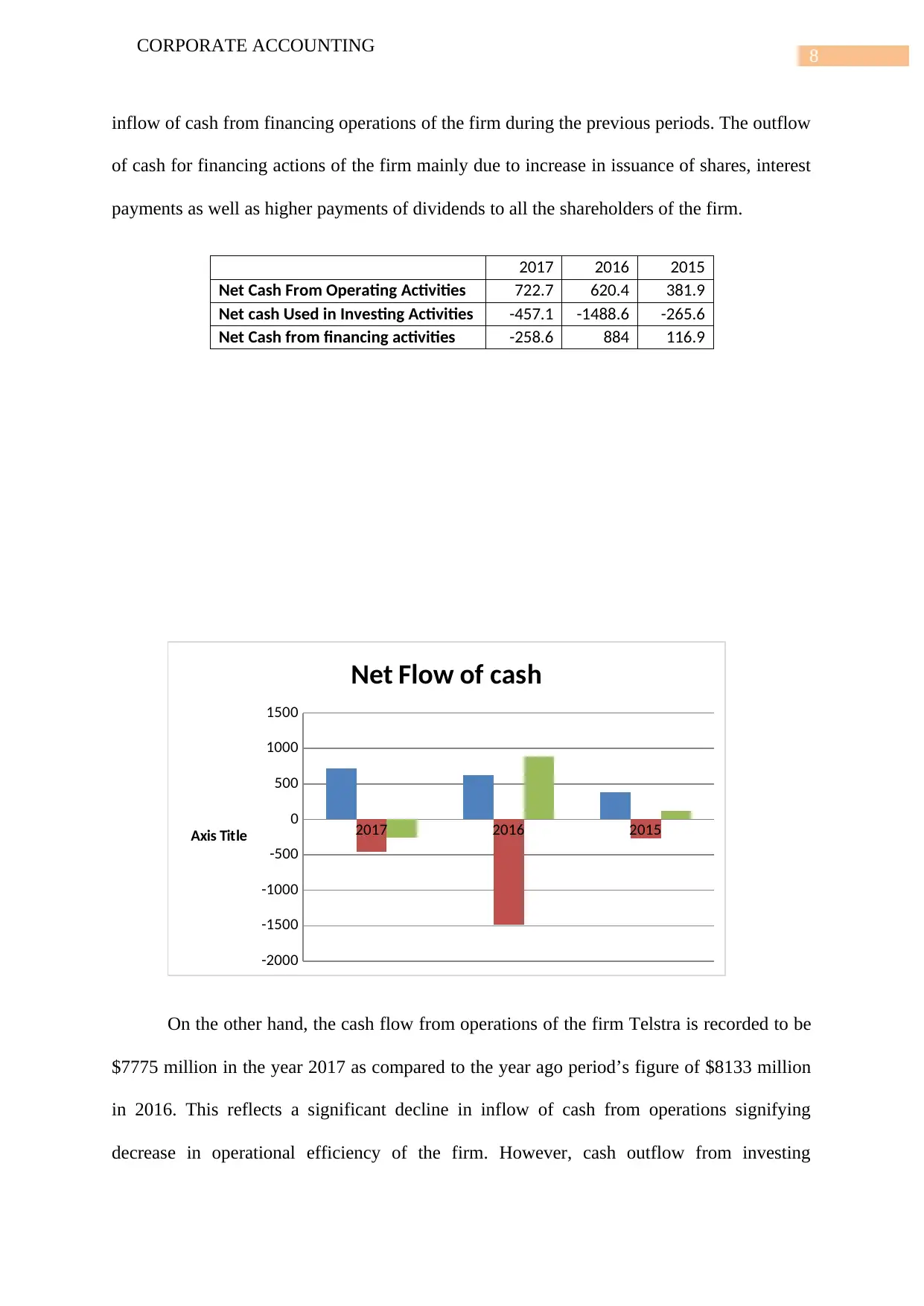

The cash flow from operating activities of the firm TPG is said to have enhanced to $722.7

million in 2017 as compared to recorded figures of the previous period that stands at $620.4

million in 2016 and roughly $381 million in 2015. The increase in cash inflow from operating

actions is mainly due to increase in generations of cash from diverse operations of the firm

and enhancement in receipts of the firm. Again, there is a net outflow of cash for investing

actions of the firm. However, outflow of cash for different investing actions of the firm is

said to have decreased to the level of (457.1) million during the period 2017 as compared to

the previous period’s figure of (1488.6) million in 2016 and approximately $(265) million in

the year 2015. The decrease in outflows mainly owes to increase in disposal of investments of

the firm TPG. Again, analysis of statement of cash flow shows that there is a net outflow of

cash for financing actions of the firm TPG during the period 2017. However, there has been

CORPORATE ACCOUNTING

debt worth $900 million as well as liabilities of lease worth $32.5 million. Considering bank

debt and balance of cash, the net debt of the firm stands at $853.7 million in the financial year

2017. However, the equity of the firm is recorded to be 2399.3 in 2017 and is said to have

enhanced in the period 2017 as compared to the year ago period of 2016. Thus, this firm TPG

is said to have a low gearing ratio reflecting proportionately less debt financing as compared

to debt financing.

Thus, the examination of the debt as well as equity capital that is utilised by both the firm

reveals the fact that Telstra is more dependent on debt financing whereas the management of

TPG is more dependent on equity capital in contrast since the enterprise is striving to

decrease the level of debt capital that is utilized by the enterprise.

Analysis of the statement of Cash Flow

The cash flow announcement reflects overall position of cash of the business

enterprise elucidates comprehensively both inflow as well as outflow of cash for the business.

The cash flow from operating activities of the firm TPG is said to have enhanced to $722.7

million in 2017 as compared to recorded figures of the previous period that stands at $620.4

million in 2016 and roughly $381 million in 2015. The increase in cash inflow from operating

actions is mainly due to increase in generations of cash from diverse operations of the firm

and enhancement in receipts of the firm. Again, there is a net outflow of cash for investing

actions of the firm. However, outflow of cash for different investing actions of the firm is

said to have decreased to the level of (457.1) million during the period 2017 as compared to

the previous period’s figure of (1488.6) million in 2016 and approximately $(265) million in

the year 2015. The decrease in outflows mainly owes to increase in disposal of investments of

the firm TPG. Again, analysis of statement of cash flow shows that there is a net outflow of

cash for financing actions of the firm TPG during the period 2017. However, there has been

8

CORPORATE ACCOUNTING

inflow of cash from financing operations of the firm during the previous periods. The outflow

of cash for financing actions of the firm mainly due to increase in issuance of shares, interest

payments as well as higher payments of dividends to all the shareholders of the firm.

2017 2016 2015

Net Cash From Operating Activities 722.7 620.4 381.9

Net cash Used in Investing Activities -457.1 -1488.6 -265.6

Net Cash from financing activities -258.6 884 116.9

2017 2016 2015

-2000

-1500

-1000

-500

0

500

1000

1500

Net Flow of cash

Axis Title

On the other hand, the cash flow from operations of the firm Telstra is recorded to be

$7775 million in the year 2017 as compared to the year ago period’s figure of $8133 million

in 2016. This reflects a significant decline in inflow of cash from operations signifying

decrease in operational efficiency of the firm. However, cash outflow from investing

CORPORATE ACCOUNTING

inflow of cash from financing operations of the firm during the previous periods. The outflow

of cash for financing actions of the firm mainly due to increase in issuance of shares, interest

payments as well as higher payments of dividends to all the shareholders of the firm.

2017 2016 2015

Net Cash From Operating Activities 722.7 620.4 381.9

Net cash Used in Investing Activities -457.1 -1488.6 -265.6

Net Cash from financing activities -258.6 884 116.9

2017 2016 2015

-2000

-1500

-1000

-500

0

500

1000

1500

Net Flow of cash

Axis Title

On the other hand, the cash flow from operations of the firm Telstra is recorded to be

$7775 million in the year 2017 as compared to the year ago period’s figure of $8133 million

in 2016. This reflects a significant decline in inflow of cash from operations signifying

decrease in operational efficiency of the firm. However, cash outflow from investing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

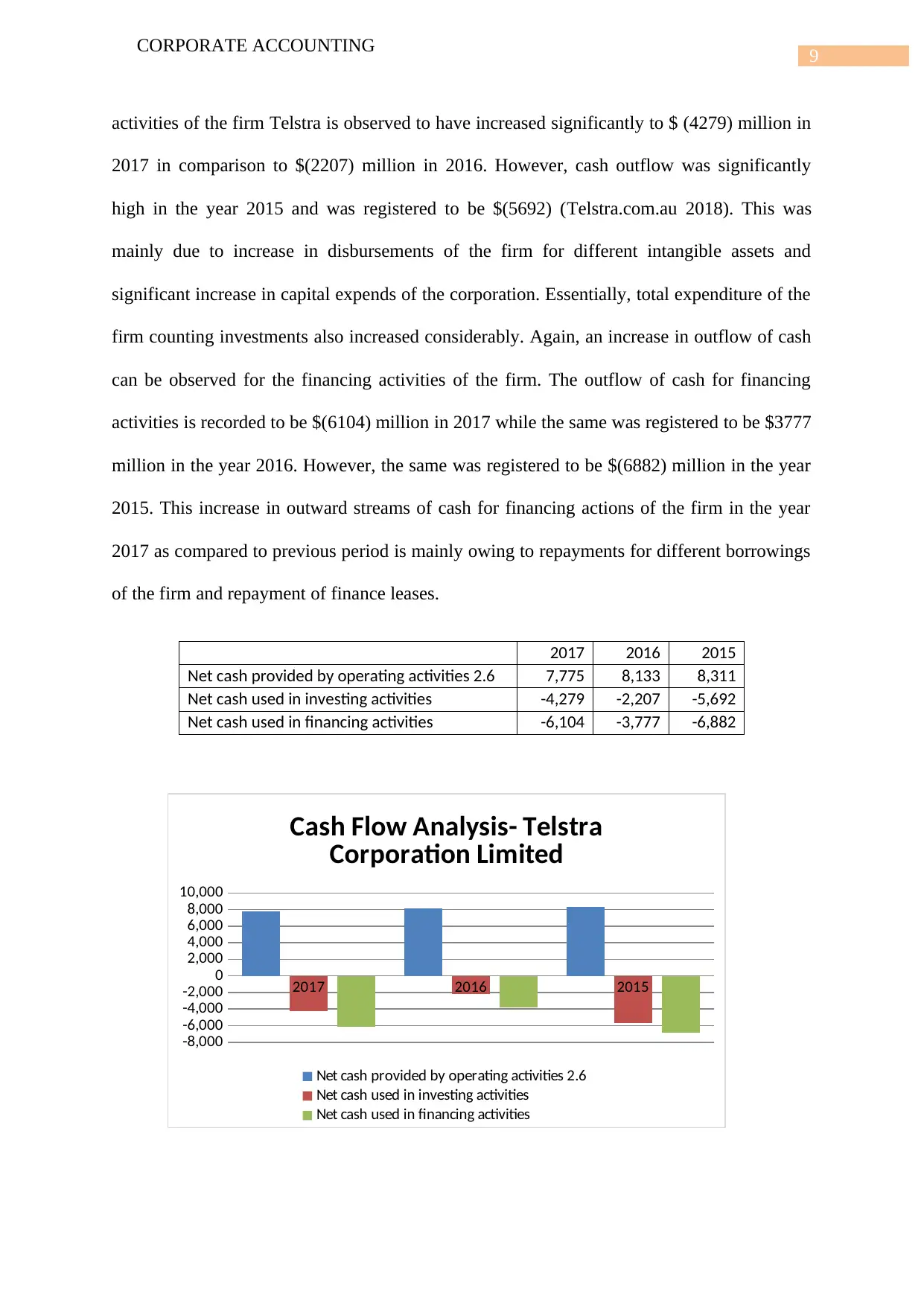

CORPORATE ACCOUNTING

activities of the firm Telstra is observed to have increased significantly to $ (4279) million in

2017 in comparison to $(2207) million in 2016. However, cash outflow was significantly

high in the year 2015 and was registered to be $(5692) (Telstra.com.au 2018). This was

mainly due to increase in disbursements of the firm for different intangible assets and

significant increase in capital expends of the corporation. Essentially, total expenditure of the

firm counting investments also increased considerably. Again, an increase in outflow of cash

can be observed for the financing activities of the firm. The outflow of cash for financing

activities is recorded to be $(6104) million in 2017 while the same was registered to be $3777

million in the year 2016. However, the same was registered to be $(6882) million in the year

2015. This increase in outward streams of cash for financing actions of the firm in the year

2017 as compared to previous period is mainly owing to repayments for different borrowings

of the firm and repayment of finance leases.

2017 2016 2015

Net cash provided by operating activities 2.6 7,775 8,133 8,311

Net cash used in investing activities -4,279 -2,207 -5,692

Net cash used in financing activities -6,104 -3,777 -6,882

2017 2016 2015

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

Cash Flow Analysis- Telstra

Corporation Limited

Net cash provided by operating activities 2.6

Net cash used in investing activities

Net cash used in financing activities

CORPORATE ACCOUNTING

activities of the firm Telstra is observed to have increased significantly to $ (4279) million in

2017 in comparison to $(2207) million in 2016. However, cash outflow was significantly

high in the year 2015 and was registered to be $(5692) (Telstra.com.au 2018). This was

mainly due to increase in disbursements of the firm for different intangible assets and

significant increase in capital expends of the corporation. Essentially, total expenditure of the

firm counting investments also increased considerably. Again, an increase in outflow of cash

can be observed for the financing activities of the firm. The outflow of cash for financing

activities is recorded to be $(6104) million in 2017 while the same was registered to be $3777

million in the year 2016. However, the same was registered to be $(6882) million in the year

2015. This increase in outward streams of cash for financing actions of the firm in the year

2017 as compared to previous period is mainly owing to repayments for different borrowings

of the firm and repayment of finance leases.

2017 2016 2015

Net cash provided by operating activities 2.6 7,775 8,133 8,311

Net cash used in investing activities -4,279 -2,207 -5,692

Net cash used in financing activities -6,104 -3,777 -6,882

2017 2016 2015

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

Cash Flow Analysis- Telstra

Corporation Limited

Net cash provided by operating activities 2.6

Net cash used in investing activities

Net cash used in financing activities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

Comparative Evaluation of Three different Components of Statement of

Cash Flow

The cash flow statement of both the companies which are shown in annual reports of

the business are effectively prepared considering the format showing cash from operating

activities, cash from investing activities and cash from financing activities. The cash from

operating activities of the business is shown to be $ 722.7 million in the financial year 2017

whereas the same was recorded to be $620.4 million in the financial year 2016. This

replicates the fact that flow of cash from diverse operations of the enterprise has enhanced

appreciably. The stream of cash from various operational activities of the firm during the year

2015 is observed to be $ 381 million approximately (Telstra.com.au 2018). Based on the

registered data it can be said that the corporation’s operational efficiency has enhanced

immensely and that can be considered to be favourable financial condition of the firm. On the

other hand, the cash flow from operating activities of the firm Telstra is said to have declined

in comparison to the previous period that is 2016.

Again, outflow of cash for different investing actions of the TPG is said to have

decreased to the level of $(457.1) million during the period 2017 as compared to the previous

period’s figure of $(1488.6) million in 2016. This is mainly due to drop in outflows mainly

due to enhancement in disposal of investments of the corporation TPG. Conversely, On the

other hand, for the business concern Telstra, cash outflow from investing activities of the firm

Telstra is observed to have augmented appreciably. It is primarily because of enhancement in

disbursement of the corporation for intangible assets and considerable enhancement in capital

expenditure of the firm.

In case of financing activities, TPG is said to have registered an outflow of cash in the

year 2017 as compared to the previous periods when there were inward stream of cash from

CORPORATE ACCOUNTING

Comparative Evaluation of Three different Components of Statement of

Cash Flow

The cash flow statement of both the companies which are shown in annual reports of

the business are effectively prepared considering the format showing cash from operating

activities, cash from investing activities and cash from financing activities. The cash from

operating activities of the business is shown to be $ 722.7 million in the financial year 2017

whereas the same was recorded to be $620.4 million in the financial year 2016. This

replicates the fact that flow of cash from diverse operations of the enterprise has enhanced

appreciably. The stream of cash from various operational activities of the firm during the year

2015 is observed to be $ 381 million approximately (Telstra.com.au 2018). Based on the

registered data it can be said that the corporation’s operational efficiency has enhanced

immensely and that can be considered to be favourable financial condition of the firm. On the

other hand, the cash flow from operating activities of the firm Telstra is said to have declined

in comparison to the previous period that is 2016.

Again, outflow of cash for different investing actions of the TPG is said to have

decreased to the level of $(457.1) million during the period 2017 as compared to the previous

period’s figure of $(1488.6) million in 2016. This is mainly due to drop in outflows mainly

due to enhancement in disposal of investments of the corporation TPG. Conversely, On the

other hand, for the business concern Telstra, cash outflow from investing activities of the firm

Telstra is observed to have augmented appreciably. It is primarily because of enhancement in

disbursement of the corporation for intangible assets and considerable enhancement in capital

expenditure of the firm.

In case of financing activities, TPG is said to have registered an outflow of cash in the

year 2017 as compared to the previous periods when there were inward stream of cash from

11

CORPORATE ACCOUNTING

financing operations in place of outflows. However, in case of Telstra as well, there was an

increase in outward flow of cash for various financing actions of the enterprise for the period

2017.

Insight of Cash flow Statement

The flow of cash from operational functions of the both the firms are observed to be

more for the firm Telstra than TPG. However, the same was recorded to have increased in

comparison to year ago figure for TPG whereas the same declined for Telstra over the time

horizon. Analysis of streams of cash for both the firms reveals that both the enterprises have

considered considerable cash movements associated to purchases of particularly property,

plant as well as equipment along with repayment of diverse loans of the enterprise (Lin et al.

2015). Also, net cash from different investing actions that is created by both the firms is

registered to be negative reflecting (Mohanram et al. 2018). Again, cash generated from

financing actions of the firms entails repayments of loans as well as dividends that are

primarily disbursed by the firm. The net cash generated by the firm TPG is observed to be

greater than the firm Telstra Corporation Limited. TPG has registered a positive inflow of net

cash while the same the same is said to be negative for the firm Telstra during the financial

year 2017.

Analysis of Other Comprehensive Income Statement

As suggested by DeFusco et al. (2015), the statement of comprehensive income

indicates the one that is not reflected in firm’s profit/loss statement. There are different items

that are included and classified to profit/loss necessarily net of tax. This includes variations

in foreign exchange translations, overall loss on particularly hedges of flow of cash, net

alteration in fair value as well as financial assets that are in essence available for sale. For the

company TPG, the overall comprehensive income is registered to be $355.9 million in 2017

CORPORATE ACCOUNTING

financing operations in place of outflows. However, in case of Telstra as well, there was an

increase in outward flow of cash for various financing actions of the enterprise for the period

2017.

Insight of Cash flow Statement

The flow of cash from operational functions of the both the firms are observed to be

more for the firm Telstra than TPG. However, the same was recorded to have increased in

comparison to year ago figure for TPG whereas the same declined for Telstra over the time

horizon. Analysis of streams of cash for both the firms reveals that both the enterprises have

considered considerable cash movements associated to purchases of particularly property,

plant as well as equipment along with repayment of diverse loans of the enterprise (Lin et al.

2015). Also, net cash from different investing actions that is created by both the firms is

registered to be negative reflecting (Mohanram et al. 2018). Again, cash generated from

financing actions of the firms entails repayments of loans as well as dividends that are

primarily disbursed by the firm. The net cash generated by the firm TPG is observed to be

greater than the firm Telstra Corporation Limited. TPG has registered a positive inflow of net

cash while the same the same is said to be negative for the firm Telstra during the financial

year 2017.

Analysis of Other Comprehensive Income Statement

As suggested by DeFusco et al. (2015), the statement of comprehensive income

indicates the one that is not reflected in firm’s profit/loss statement. There are different items

that are included and classified to profit/loss necessarily net of tax. This includes variations

in foreign exchange translations, overall loss on particularly hedges of flow of cash, net

alteration in fair value as well as financial assets that are in essence available for sale. For the

company TPG, the overall comprehensive income is registered to be $355.9 million in 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.