Australian Accounting and Finance: Telstra and Woolworths Report

VerifiedAdded on 2022/11/02

|15

|3257

|234

Report

AI Summary

This report provides a comprehensive analysis of accounting and finance practices in Australia, focusing on two major companies: Telstra Group and Woolworths Group. The introduction offers background information on both companies, detailing their business operations, market position, and financial performance. Task 1 presents a comparative analysis of the equity and liabilities of both companies over three years (2017-2019), highlighting key trends in share capital, reserves, retained earnings, and non-controlling interests for equity, and borrowings, payables, employee benefits, and provisions for liabilities. The analysis includes detailed financial data, identifying significant changes and patterns in each company's financial structure. Task 2 explores the concept of reporting entities under Australian Securities Law, differentiating between general-purpose financial reports (GPFR) and special-purpose financial reports, and discussing the implications for various stakeholders. It also explains the criteria for classifying proprietary companies as small or large, based on the Corporations Act 2001, and the associated reporting requirements and thresholds. The report concludes by summarizing the key findings regarding the sources of funds for both Telstra and Woolworths, emphasizing the importance of long-term debt and share issuance in their financial strategies.

ACCOUNTING AND FINANCE IN

AUSTRALIA

AUSTRALIA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.....................................................................................................................................2

TASK 1:...................................................................................................................................................3

TASK 2:...................................................................................................................................................9

CONCLUSION.......................................................................................................................................12

BIBLIOGRAPHY.....................................................................................................................................13

INTRODUCTION.....................................................................................................................................2

TASK 1:...................................................................................................................................................3

TASK 2:...................................................................................................................................................9

CONCLUSION.......................................................................................................................................12

BIBLIOGRAPHY.....................................................................................................................................13

INTRODUCTION

The two companies chosen are Woolsworth Group and Telstra Group for the purpose of

analysis. Telstra group of companies, popularly known as the TCL (Telstar Corporation

Limited) is an Australian based organization engaged in telecommunication business. The

organisation is witnessed to build such telecommunication networks including mobile

services along with Internet access, television services and similar other products and

services. This is a public listed company traded on both the Australian stock exchange and

the New Zealand stock exchange (Bailey, et al., 2017). Founded 44 years ago, it has its

headquarters in Melbourne named as the Telstra corporate Centre. It serves the country and is

estimated to generate an operating revenue of Australian dollars 6 billion. It has a user

employee base of 32,000 working in the entity including its 150 subsidiaries. It is popularly

known as the country‘s largest mobile service providers. It is also known to hold and

maintain more than 50% of the Australia’s total public phones. This company was the 1st to

launch the digital mobile network in the country. It has also witnessed to provide mobile

telephonic services as the first organisation in Australia. (Anon., 2019)

Woolworths Supermarkets, on the other hand, is a grocery chain store in Australia. It’s

conglomeration along with Coles covers about 4/5 of the total Australian market. This is a

company working as a subsidiary in the retail industry with its headquarters situated in New

South Wales, Australia. Generating an operating revenue of about AUD 56.73 -13824, it

seems to employ a large base of 115,000 management personnel. It is known to sell groceries

including fruit, frozen foods, vegetables, other packaged foods, etc. Recently it has also

witnessed in distributing magazines, beauty related items, Baby supplies, and stationery

related items (Wild, et al., 2015). It is known to own more than 950 stores across the country

apart from working online as well. The organisation said about benchmark last year in 2018

The two companies chosen are Woolsworth Group and Telstra Group for the purpose of

analysis. Telstra group of companies, popularly known as the TCL (Telstar Corporation

Limited) is an Australian based organization engaged in telecommunication business. The

organisation is witnessed to build such telecommunication networks including mobile

services along with Internet access, television services and similar other products and

services. This is a public listed company traded on both the Australian stock exchange and

the New Zealand stock exchange (Bailey, et al., 2017). Founded 44 years ago, it has its

headquarters in Melbourne named as the Telstra corporate Centre. It serves the country and is

estimated to generate an operating revenue of Australian dollars 6 billion. It has a user

employee base of 32,000 working in the entity including its 150 subsidiaries. It is popularly

known as the country‘s largest mobile service providers. It is also known to hold and

maintain more than 50% of the Australia’s total public phones. This company was the 1st to

launch the digital mobile network in the country. It has also witnessed to provide mobile

telephonic services as the first organisation in Australia. (Anon., 2019)

Woolworths Supermarkets, on the other hand, is a grocery chain store in Australia. It’s

conglomeration along with Coles covers about 4/5 of the total Australian market. This is a

company working as a subsidiary in the retail industry with its headquarters situated in New

South Wales, Australia. Generating an operating revenue of about AUD 56.73 -13824, it

seems to employ a large base of 115,000 management personnel. It is known to sell groceries

including fruit, frozen foods, vegetables, other packaged foods, etc. Recently it has also

witnessed in distributing magazines, beauty related items, Baby supplies, and stationery

related items (Wild, et al., 2015). It is known to own more than 950 stores across the country

apart from working online as well. The organisation said about benchmark last year in 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

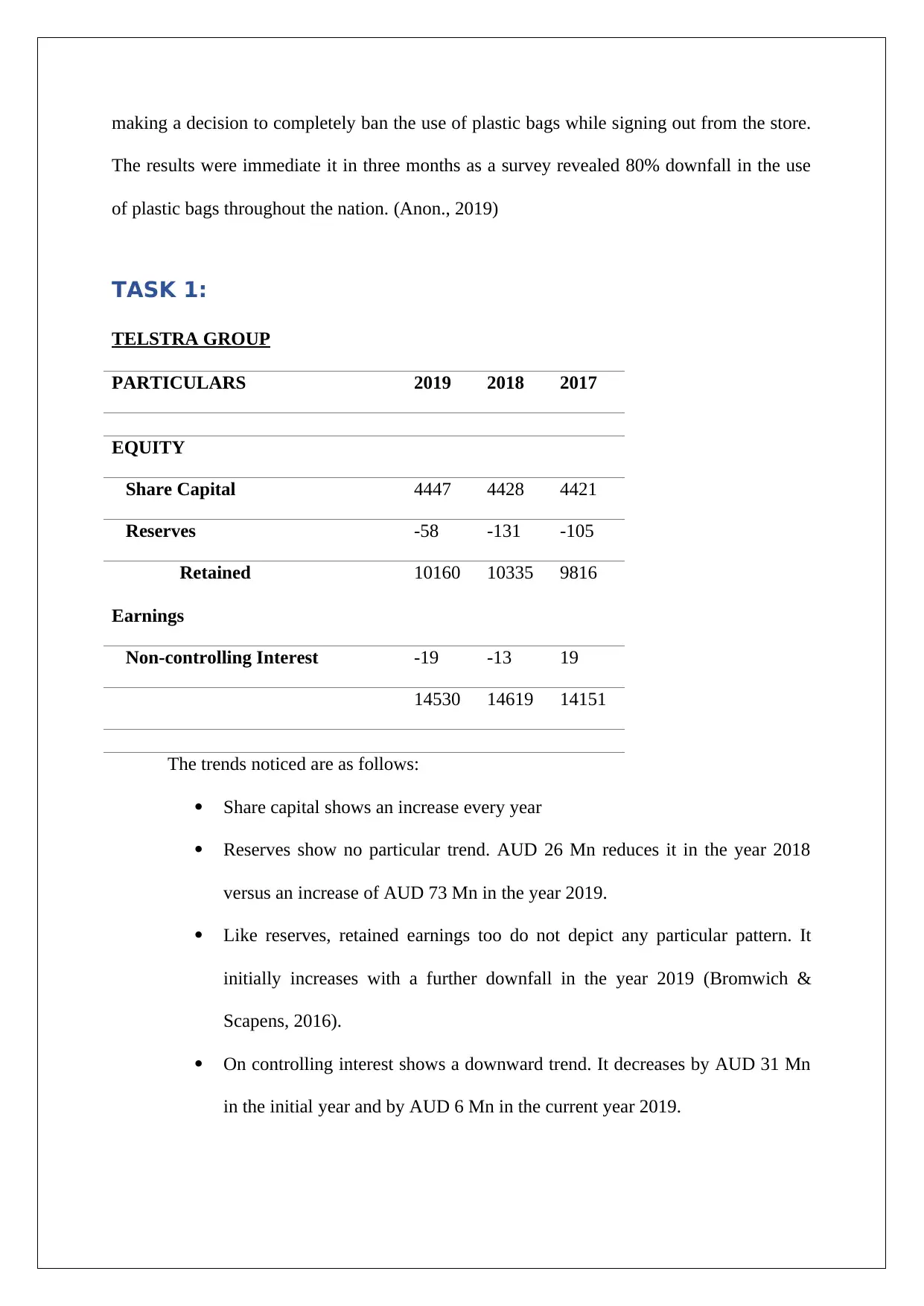

making a decision to completely ban the use of plastic bags while signing out from the store.

The results were immediate it in three months as a survey revealed 80% downfall in the use

of plastic bags throughout the nation. (Anon., 2019)

TASK 1:

TELSTRA GROUP

PARTICULARS 2019 2018 2017

EQUITY

Share Capital 4447 4428 4421

Reserves -58 -131 -105

Retained

Earnings

10160 10335 9816

Non-controlling Interest -19 -13 19

14530 14619 14151

The trends noticed are as follows:

Share capital shows an increase every year

Reserves show no particular trend. AUD 26 Mn reduces it in the year 2018

versus an increase of AUD 73 Mn in the year 2019.

Like reserves, retained earnings too do not depict any particular pattern. It

initially increases with a further downfall in the year 2019 (Bromwich &

Scapens, 2016).

On controlling interest shows a downward trend. It decreases by AUD 31 Mn

in the initial year and by AUD 6 Mn in the current year 2019.

The results were immediate it in three months as a survey revealed 80% downfall in the use

of plastic bags throughout the nation. (Anon., 2019)

TASK 1:

TELSTRA GROUP

PARTICULARS 2019 2018 2017

EQUITY

Share Capital 4447 4428 4421

Reserves -58 -131 -105

Retained

Earnings

10160 10335 9816

Non-controlling Interest -19 -13 19

14530 14619 14151

The trends noticed are as follows:

Share capital shows an increase every year

Reserves show no particular trend. AUD 26 Mn reduces it in the year 2018

versus an increase of AUD 73 Mn in the year 2019.

Like reserves, retained earnings too do not depict any particular pattern. It

initially increases with a further downfall in the year 2019 (Bromwich &

Scapens, 2016).

On controlling interest shows a downward trend. It decreases by AUD 31 Mn

in the initial year and by AUD 6 Mn in the current year 2019.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

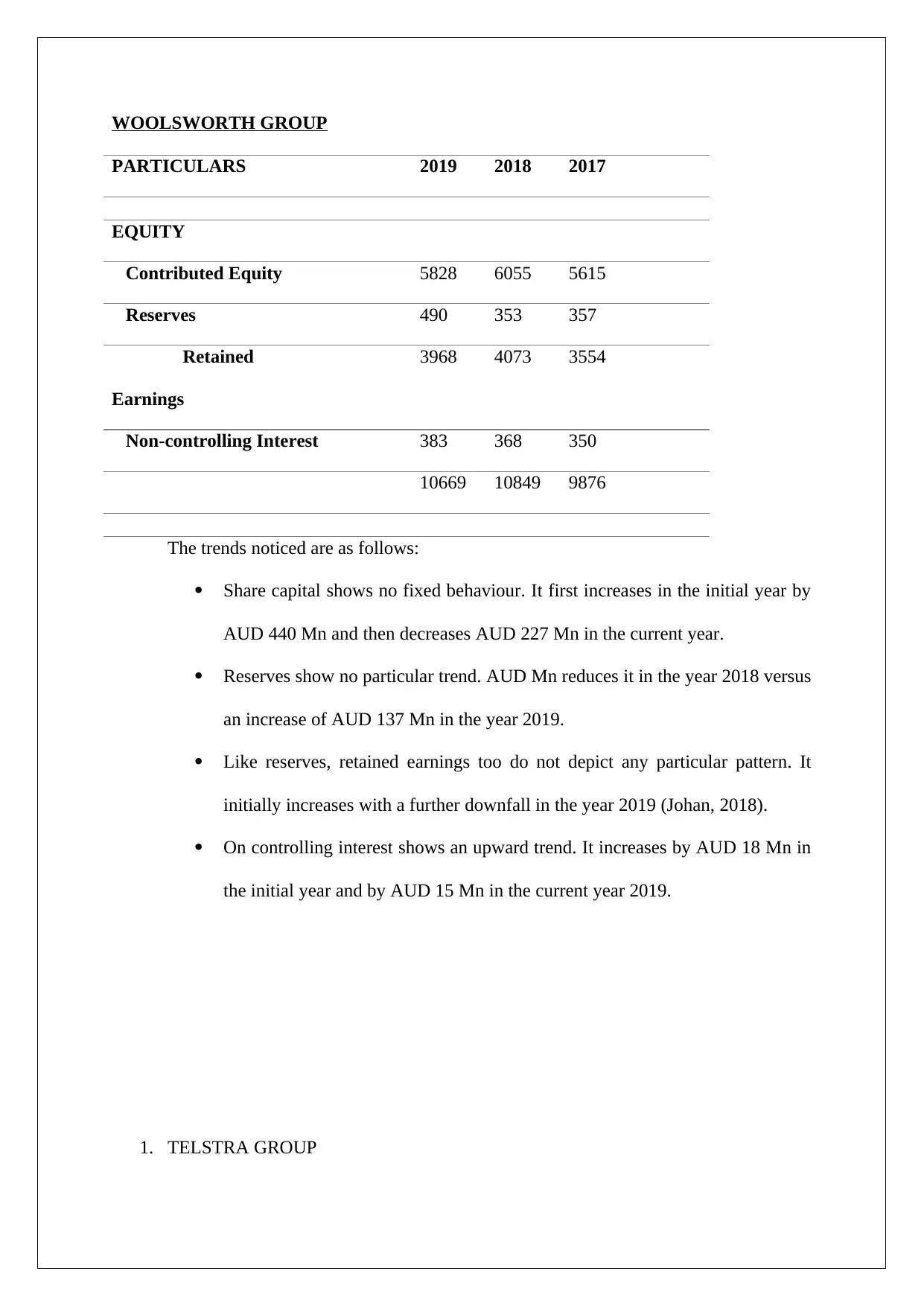

WOOLSWORTH GROUP

PARTICULARS 2019 2018 2017

EQUITY

Contributed Equity 5828 6055 5615

Reserves 490 353 357

Retained

Earnings

3968 4073 3554

Non-controlling Interest 383 368 350

10669 10849 9876

The trends noticed are as follows:

Share capital shows no fixed behaviour. It first increases in the initial year by

AUD 440 Mn and then decreases AUD 227 Mn in the current year.

Reserves show no particular trend. AUD Mn reduces it in the year 2018 versus

an increase of AUD 137 Mn in the year 2019.

Like reserves, retained earnings too do not depict any particular pattern. It

initially increases with a further downfall in the year 2019 (Johan, 2018).

On controlling interest shows an upward trend. It increases by AUD 18 Mn in

the initial year and by AUD 15 Mn in the current year 2019.

1. TELSTRA GROUP

PARTICULARS 2019 2018 2017

EQUITY

Contributed Equity 5828 6055 5615

Reserves 490 353 357

Retained

Earnings

3968 4073 3554

Non-controlling Interest 383 368 350

10669 10849 9876

The trends noticed are as follows:

Share capital shows no fixed behaviour. It first increases in the initial year by

AUD 440 Mn and then decreases AUD 227 Mn in the current year.

Reserves show no particular trend. AUD Mn reduces it in the year 2018 versus

an increase of AUD 137 Mn in the year 2019.

Like reserves, retained earnings too do not depict any particular pattern. It

initially increases with a further downfall in the year 2019 (Johan, 2018).

On controlling interest shows an upward trend. It increases by AUD 18 Mn in

the initial year and by AUD 15 Mn in the current year 2019.

1. TELSTRA GROUP

PARTICULARS 2019 2018 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

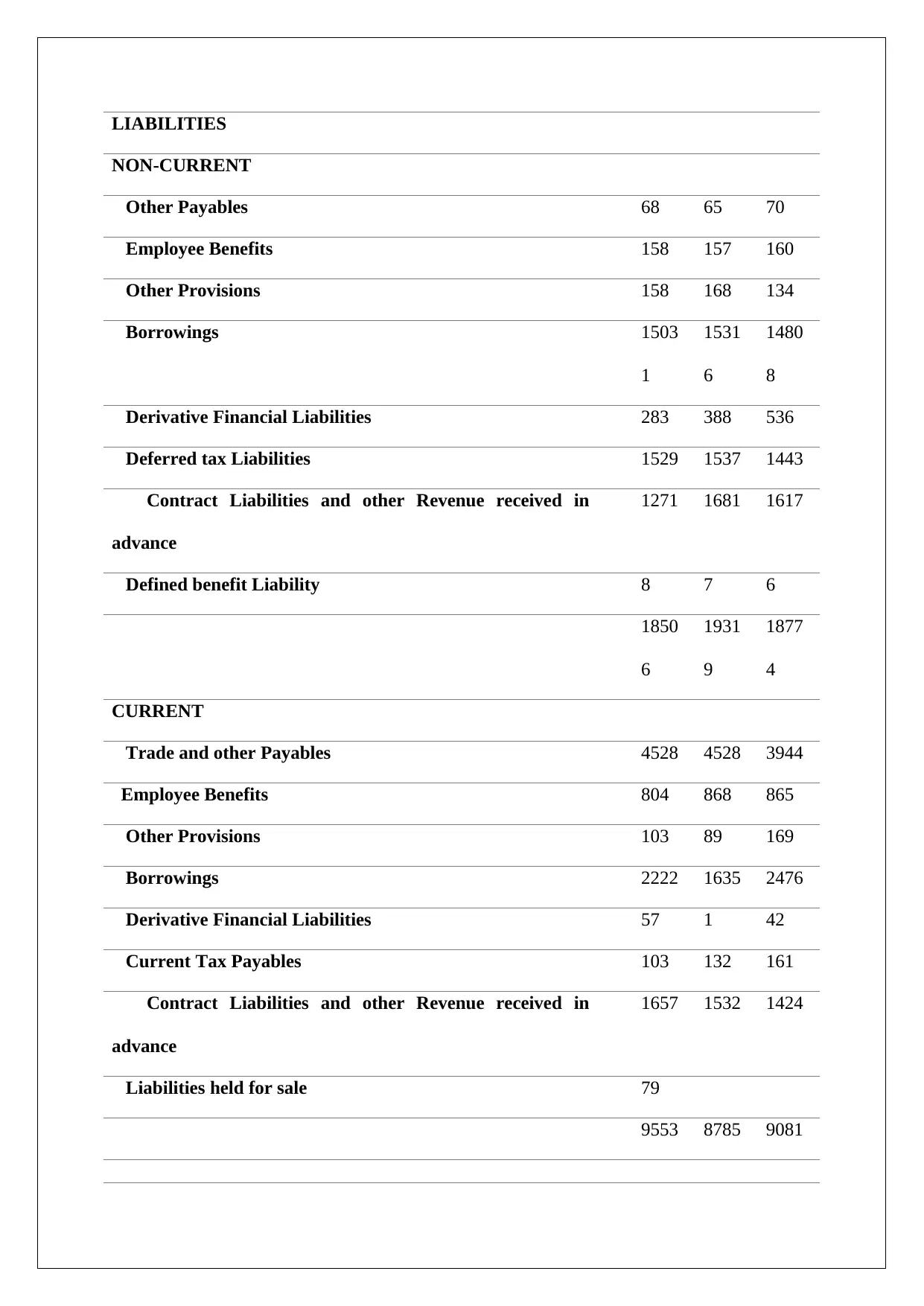

LIABILITIES

NON-CURRENT

Other Payables 68 65 70

Employee Benefits 158 157 160

Other Provisions 158 168 134

Borrowings 1503

1

1531

6

1480

8

Derivative Financial Liabilities 283 388 536

Deferred tax Liabilities 1529 1537 1443

Contract Liabilities and other Revenue received in

advance

1271 1681 1617

Defined benefit Liability 8 7 6

1850

6

1931

9

1877

4

CURRENT

Trade and other Payables 4528 4528 3944

Employee Benefits 804 868 865

Other Provisions 103 89 169

Borrowings 2222 1635 2476

Derivative Financial Liabilities 57 1 42

Current Tax Payables 103 132 161

Contract Liabilities and other Revenue received in

advance

1657 1532 1424

Liabilities held for sale 79

9553 8785 9081

NON-CURRENT

Other Payables 68 65 70

Employee Benefits 158 157 160

Other Provisions 158 168 134

Borrowings 1503

1

1531

6

1480

8

Derivative Financial Liabilities 283 388 536

Deferred tax Liabilities 1529 1537 1443

Contract Liabilities and other Revenue received in

advance

1271 1681 1617

Defined benefit Liability 8 7 6

1850

6

1931

9

1877

4

CURRENT

Trade and other Payables 4528 4528 3944

Employee Benefits 804 868 865

Other Provisions 103 89 169

Borrowings 2222 1635 2476

Derivative Financial Liabilities 57 1 42

Current Tax Payables 103 132 161

Contract Liabilities and other Revenue received in

advance

1657 1532 1424

Liabilities held for sale 79

9553 8785 9081

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

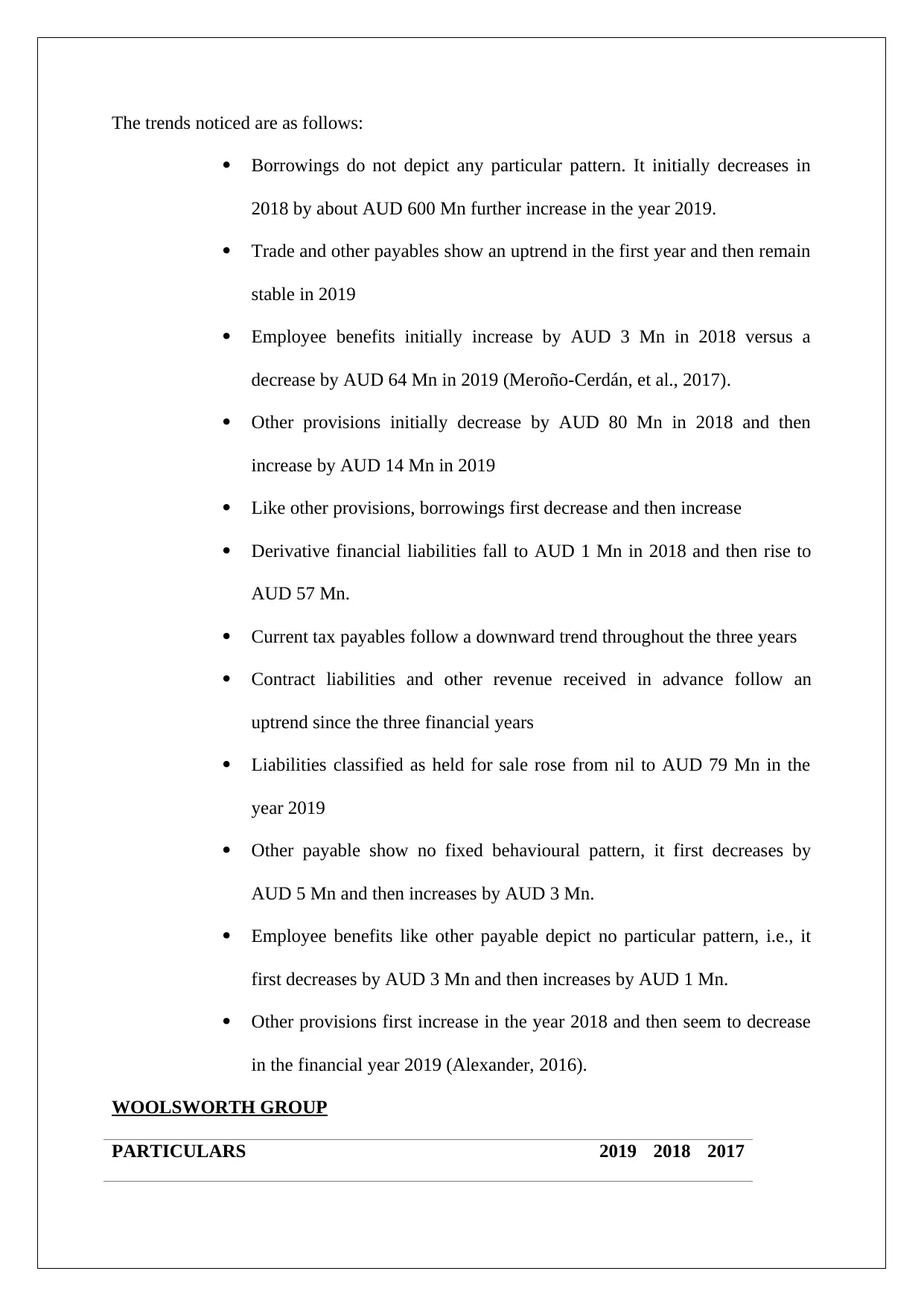

The trends noticed are as follows:

Borrowings do not depict any particular pattern. It initially decreases in

2018 by about AUD 600 Mn further increase in the year 2019.

Trade and other payables show an uptrend in the first year and then remain

stable in 2019

Employee benefits initially increase by AUD 3 Mn in 2018 versus a

decrease by AUD 64 Mn in 2019 (Meroño-Cerdán, et al., 2017).

Other provisions initially decrease by AUD 80 Mn in 2018 and then

increase by AUD 14 Mn in 2019

Like other provisions, borrowings first decrease and then increase

Derivative financial liabilities fall to AUD 1 Mn in 2018 and then rise to

AUD 57 Mn.

Current tax payables follow a downward trend throughout the three years

Contract liabilities and other revenue received in advance follow an

uptrend since the three financial years

Liabilities classified as held for sale rose from nil to AUD 79 Mn in the

year 2019

Other payable show no fixed behavioural pattern, it first decreases by

AUD 5 Mn and then increases by AUD 3 Mn.

Employee benefits like other payable depict no particular pattern, i.e., it

first decreases by AUD 3 Mn and then increases by AUD 1 Mn.

Other provisions first increase in the year 2018 and then seem to decrease

in the financial year 2019 (Alexander, 2016).

WOOLSWORTH GROUP

PARTICULARS 2019 2018 2017

Borrowings do not depict any particular pattern. It initially decreases in

2018 by about AUD 600 Mn further increase in the year 2019.

Trade and other payables show an uptrend in the first year and then remain

stable in 2019

Employee benefits initially increase by AUD 3 Mn in 2018 versus a

decrease by AUD 64 Mn in 2019 (Meroño-Cerdán, et al., 2017).

Other provisions initially decrease by AUD 80 Mn in 2018 and then

increase by AUD 14 Mn in 2019

Like other provisions, borrowings first decrease and then increase

Derivative financial liabilities fall to AUD 1 Mn in 2018 and then rise to

AUD 57 Mn.

Current tax payables follow a downward trend throughout the three years

Contract liabilities and other revenue received in advance follow an

uptrend since the three financial years

Liabilities classified as held for sale rose from nil to AUD 79 Mn in the

year 2019

Other payable show no fixed behavioural pattern, it first decreases by

AUD 5 Mn and then increases by AUD 3 Mn.

Employee benefits like other payable depict no particular pattern, i.e., it

first decreases by AUD 3 Mn and then increases by AUD 1 Mn.

Other provisions first increase in the year 2018 and then seem to decrease

in the financial year 2019 (Alexander, 2016).

WOOLSWORTH GROUP

PARTICULARS 2019 2018 2017

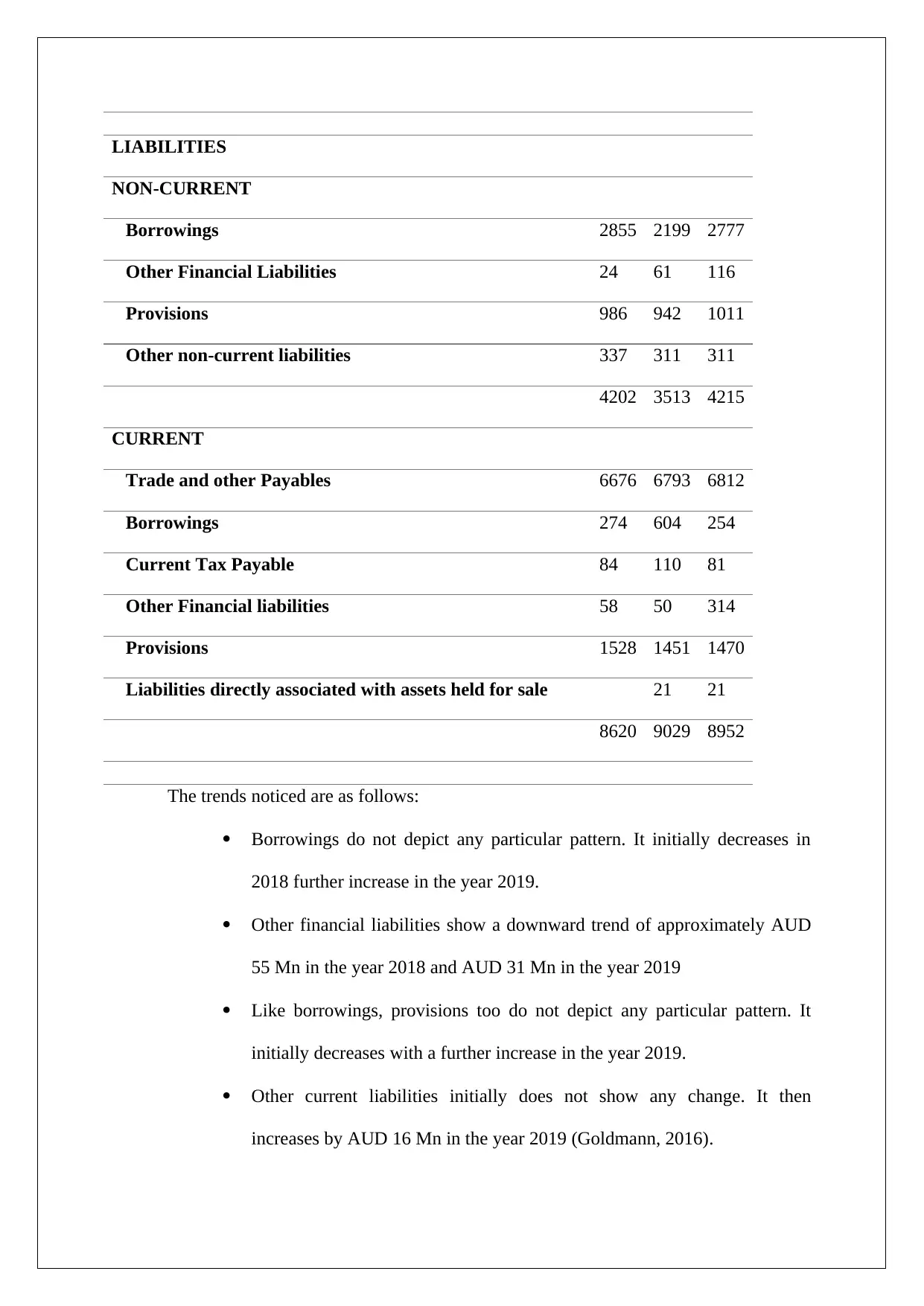

LIABILITIES

NON-CURRENT

Borrowings 2855 2199 2777

Other Financial Liabilities 24 61 116

Provisions 986 942 1011

Other non-current liabilities 337 311 311

4202 3513 4215

CURRENT

Trade and other Payables 6676 6793 6812

Borrowings 274 604 254

Current Tax Payable 84 110 81

Other Financial liabilities 58 50 314

Provisions 1528 1451 1470

Liabilities directly associated with assets held for sale 21 21

8620 9029 8952

The trends noticed are as follows:

Borrowings do not depict any particular pattern. It initially decreases in

2018 further increase in the year 2019.

Other financial liabilities show a downward trend of approximately AUD

55 Mn in the year 2018 and AUD 31 Mn in the year 2019

Like borrowings, provisions too do not depict any particular pattern. It

initially decreases with a further increase in the year 2019.

Other current liabilities initially does not show any change. It then

increases by AUD 16 Mn in the year 2019 (Goldmann, 2016).

NON-CURRENT

Borrowings 2855 2199 2777

Other Financial Liabilities 24 61 116

Provisions 986 942 1011

Other non-current liabilities 337 311 311

4202 3513 4215

CURRENT

Trade and other Payables 6676 6793 6812

Borrowings 274 604 254

Current Tax Payable 84 110 81

Other Financial liabilities 58 50 314

Provisions 1528 1451 1470

Liabilities directly associated with assets held for sale 21 21

8620 9029 8952

The trends noticed are as follows:

Borrowings do not depict any particular pattern. It initially decreases in

2018 further increase in the year 2019.

Other financial liabilities show a downward trend of approximately AUD

55 Mn in the year 2018 and AUD 31 Mn in the year 2019

Like borrowings, provisions too do not depict any particular pattern. It

initially decreases with a further increase in the year 2019.

Other current liabilities initially does not show any change. It then

increases by AUD 16 Mn in the year 2019 (Goldmann, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The company has been witnessing to clear off its creditors with every year.

Hence, they show a downward trend in the figure.

Current term borrowings have initially increased by approximately AUD

350 Mn and then decreased by the same amount in the year 2019

Taxes payables show the same trend as current term borrowings. The

liability is first increased by AUD 26 Mn and then decreased by the same

amount.

Other financial liabilities has drastically reduced in the year 2018 by

approx. AUD 250 Mn and then increased by AUD 8 Mn.

Liabilities associated with assets directly held for sale remained constant in

the next year but fall down to zero in the FY 2019.

Current term provisions have decreased significantly in the FY 2018.

Studying the annual reports of the two selected companies mentioned as above, critical

findings that are revealed about their sources of funds are as follows:

The Telstra group has its sources of finance from long term debt and by issue of

shares to the public at large

The Woolworth group also draws its required funds from long-term debt in the

current financial year 2019 (Farmer, 2018).

TASK 2:

A reporting entity, as expressed by the provisions of the Australian Securities Law, is an

organisation or a financial entity that have users significantly dependant on its financial

reports. Hence, the performance of the financial entity is likely to affect its user’s investment

decisions extensively. (Stuchbery, 2017) This seems to arise a reasonable expectation on the

entity to prepare a GPFR, that is, general-purpose financial reports. These reports are true

Hence, they show a downward trend in the figure.

Current term borrowings have initially increased by approximately AUD

350 Mn and then decreased by the same amount in the year 2019

Taxes payables show the same trend as current term borrowings. The

liability is first increased by AUD 26 Mn and then decreased by the same

amount.

Other financial liabilities has drastically reduced in the year 2018 by

approx. AUD 250 Mn and then increased by AUD 8 Mn.

Liabilities associated with assets directly held for sale remained constant in

the next year but fall down to zero in the FY 2019.

Current term provisions have decreased significantly in the FY 2018.

Studying the annual reports of the two selected companies mentioned as above, critical

findings that are revealed about their sources of funds are as follows:

The Telstra group has its sources of finance from long term debt and by issue of

shares to the public at large

The Woolworth group also draws its required funds from long-term debt in the

current financial year 2019 (Farmer, 2018).

TASK 2:

A reporting entity, as expressed by the provisions of the Australian Securities Law, is an

organisation or a financial entity that have users significantly dependant on its financial

reports. Hence, the performance of the financial entity is likely to affect its user’s investment

decisions extensively. (Stuchbery, 2017) This seems to arise a reasonable expectation on the

entity to prepare a GPFR, that is, general-purpose financial reports. These reports are true

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reflection of the entity’s financial position by disclosing material facts and figures for its

users. These users comprise of the managers, the government both at the Centre and the state,

shareholders both potential and existing, employees, lenders, creditors, etc. On the contrary, a

non-reporting entity is an entity where users are recognised to be not dependent on the GPFR.

Hence, those charged with management and governance is required to prepare a special

purpose financial report instead. These are different from the general purpose financial

reports and hence, have less restrictive implications and impositions than them. Based on the

entity being a reporting one or not, the management then decides the framework of financial

reporting to be used, typically known as the FRF (Dichev, 2017). Public listed companies,

public interest oriented companies like educational institutions, hospitals, etc., large private

companies having external shareholders with no access to other financial data except annual

reports are few examples of reporting entities. The relevant accounting standards applicable

in Australia are applied while preparing the GPFR. This document opens new doors for the

potential investors by attracting them through the financial position of the entity. This

document is significant enough to augment the goodwill of the financial organization and

shape its future. It is highly valuable for exploring new opportunities that come its way. Such

document also assists many listed companies as a marketing tool for promotion of their

managerial activities and demonstrating their efforts of social responsibility. The downside

only being the costs associated with it. (Carey, 2014)

As defined under the provisions of section 45A (1) Relevant to the corporations act 2001, a

proprietary company is a form of a privately constituted company. This can be of two types-

either small or large, limited or unlimited.Since 1 July 2019 and thereafter, proprietary

company satisfying any of the two listed below criteria shall be considered as a large

proprietary company: (Reilly, 2015)

users. These users comprise of the managers, the government both at the Centre and the state,

shareholders both potential and existing, employees, lenders, creditors, etc. On the contrary, a

non-reporting entity is an entity where users are recognised to be not dependent on the GPFR.

Hence, those charged with management and governance is required to prepare a special

purpose financial report instead. These are different from the general purpose financial

reports and hence, have less restrictive implications and impositions than them. Based on the

entity being a reporting one or not, the management then decides the framework of financial

reporting to be used, typically known as the FRF (Dichev, 2017). Public listed companies,

public interest oriented companies like educational institutions, hospitals, etc., large private

companies having external shareholders with no access to other financial data except annual

reports are few examples of reporting entities. The relevant accounting standards applicable

in Australia are applied while preparing the GPFR. This document opens new doors for the

potential investors by attracting them through the financial position of the entity. This

document is significant enough to augment the goodwill of the financial organization and

shape its future. It is highly valuable for exploring new opportunities that come its way. Such

document also assists many listed companies as a marketing tool for promotion of their

managerial activities and demonstrating their efforts of social responsibility. The downside

only being the costs associated with it. (Carey, 2014)

As defined under the provisions of section 45A (1) Relevant to the corporations act 2001, a

proprietary company is a form of a privately constituted company. This can be of two types-

either small or large, limited or unlimited.Since 1 July 2019 and thereafter, proprietary

company satisfying any of the two listed below criteria shall be considered as a large

proprietary company: (Reilly, 2015)

A total number of hundred or exceeding hundred employs been working in the

financial year for the company along with several entities,

The consolidated revenue of the entity along with it several other undertakings to

exceed $50 million or more in any financial year, and

The consolidated asset value for the company along with several undertakings to

exceed $25 million or more in any financial year (ICAEW, 2011).

If the company fulfils any of the above mentioned to criteria, it shall be considered as a large

propriety entity.There are also required to prepare and file a director report as well as its

financial report for every financial year accompanied with yearly auditing conducted for its

books of accounts, unless any relief is granted by ASIC. This threshold requirement has been

increased and hence, it has allowed relaxation to approximately 2200 proprietary entities

from the stringent reporting compliances that earlier attracted to. Reports reveal savings in

regulatory costs of about $81.3 million annually. The new threshold has been imposed ensure

changes in the economy since 2007 with respect to both inflation as well as economic growth.

These changes are significantly deployed to ensure proper assurance to financial obligations.

The effective date of this new threshold has doubled the limits as compared to the one before.

Amendments occur to adjust or take into account the various macroeconomic factors that

change with respect to time. (Kitson, 2019)

On the contrary section 45A (2) of the Corporations Act 2001, states that a small proprietary

entity is the one that may satisfy at least two of the below mentioned criterions:

The consolidated value of assets of the entity along with it several other undertakings

should not exceed $25 million in any financial year.

Consolidated revenue of the entity along with it several other than getting things

should not exceed $50 million in any financial year, and

financial year for the company along with several entities,

The consolidated revenue of the entity along with it several other undertakings to

exceed $50 million or more in any financial year, and

The consolidated asset value for the company along with several undertakings to

exceed $25 million or more in any financial year (ICAEW, 2011).

If the company fulfils any of the above mentioned to criteria, it shall be considered as a large

propriety entity.There are also required to prepare and file a director report as well as its

financial report for every financial year accompanied with yearly auditing conducted for its

books of accounts, unless any relief is granted by ASIC. This threshold requirement has been

increased and hence, it has allowed relaxation to approximately 2200 proprietary entities

from the stringent reporting compliances that earlier attracted to. Reports reveal savings in

regulatory costs of about $81.3 million annually. The new threshold has been imposed ensure

changes in the economy since 2007 with respect to both inflation as well as economic growth.

These changes are significantly deployed to ensure proper assurance to financial obligations.

The effective date of this new threshold has doubled the limits as compared to the one before.

Amendments occur to adjust or take into account the various macroeconomic factors that

change with respect to time. (Kitson, 2019)

On the contrary section 45A (2) of the Corporations Act 2001, states that a small proprietary

entity is the one that may satisfy at least two of the below mentioned criterions:

The consolidated value of assets of the entity along with it several other undertakings

should not exceed $25 million in any financial year.

Consolidated revenue of the entity along with it several other than getting things

should not exceed $50 million in any financial year, and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.