EG5115 - Tendering, Estimating & Cost Control: Valuation Report

VerifiedAdded on 2023/04/10

|21

|2980

|226

Report

AI Summary

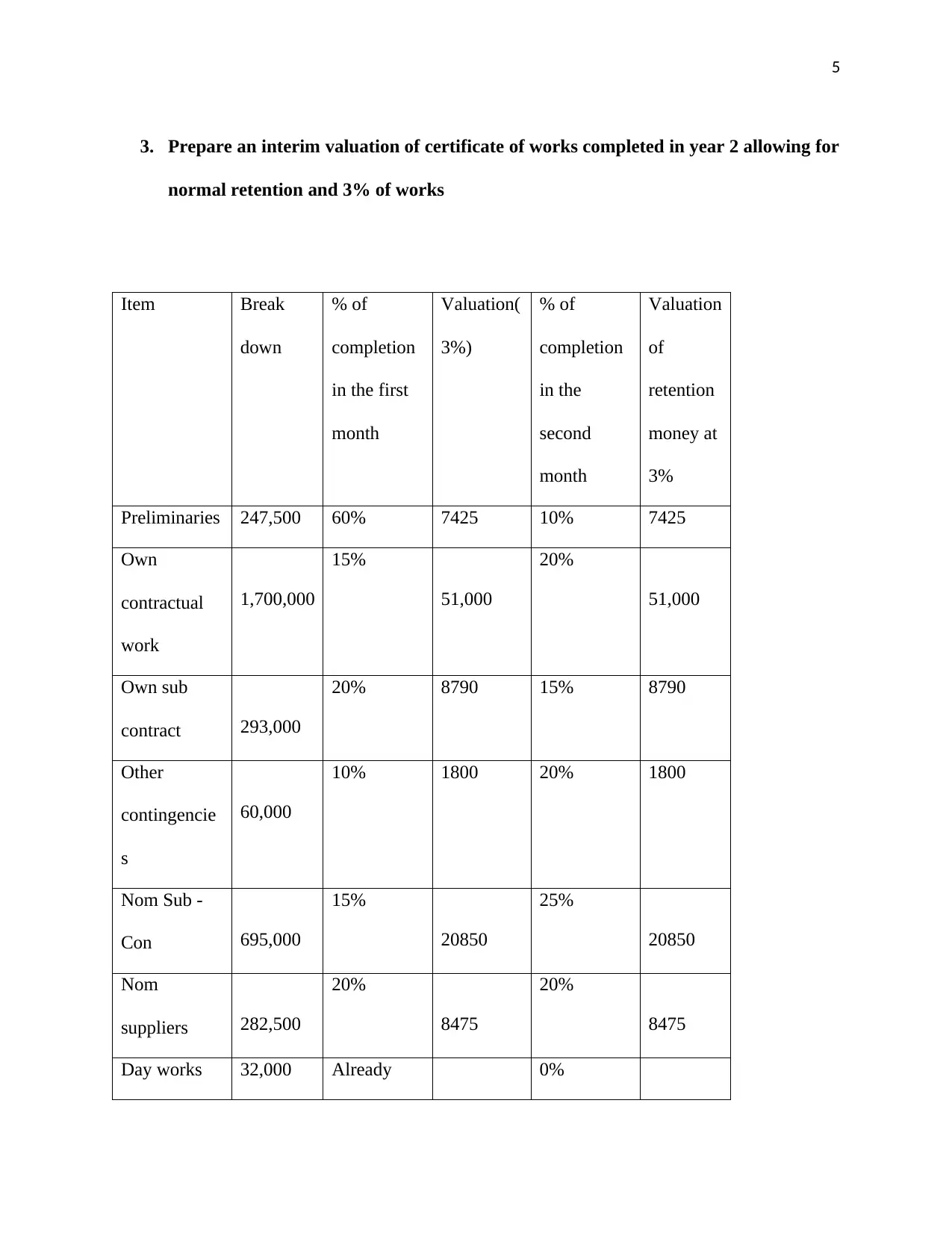

This report provides a comprehensive overview of tendering, estimating, and cost control in contracts. It discusses the benefits of regular payments to contractors, the importance of retention money, and methods for valuing work for payments. An interim valuation certificate is prepared, considering retention and work percentages. The report also outlines the procedure for obtaining a quote, tendering, receiving goods, and making payments. Furthermore, it includes a depreciation analysis of a JCB plant using both the double-declining and straight-line methods. Finally, the report argues the importance of information documented in a Pre-Qualification Questionnaire (PQQ) and its impact on a contractor's chances of securing a tender. Desklib offers a wealth of resources, including similar reports and solved assignments, for students.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.