MREGC5001: Terotechnology Report on Capital Investment Analysis

VerifiedAdded on 2023/01/12

|14

|1918

|25

Report

AI Summary

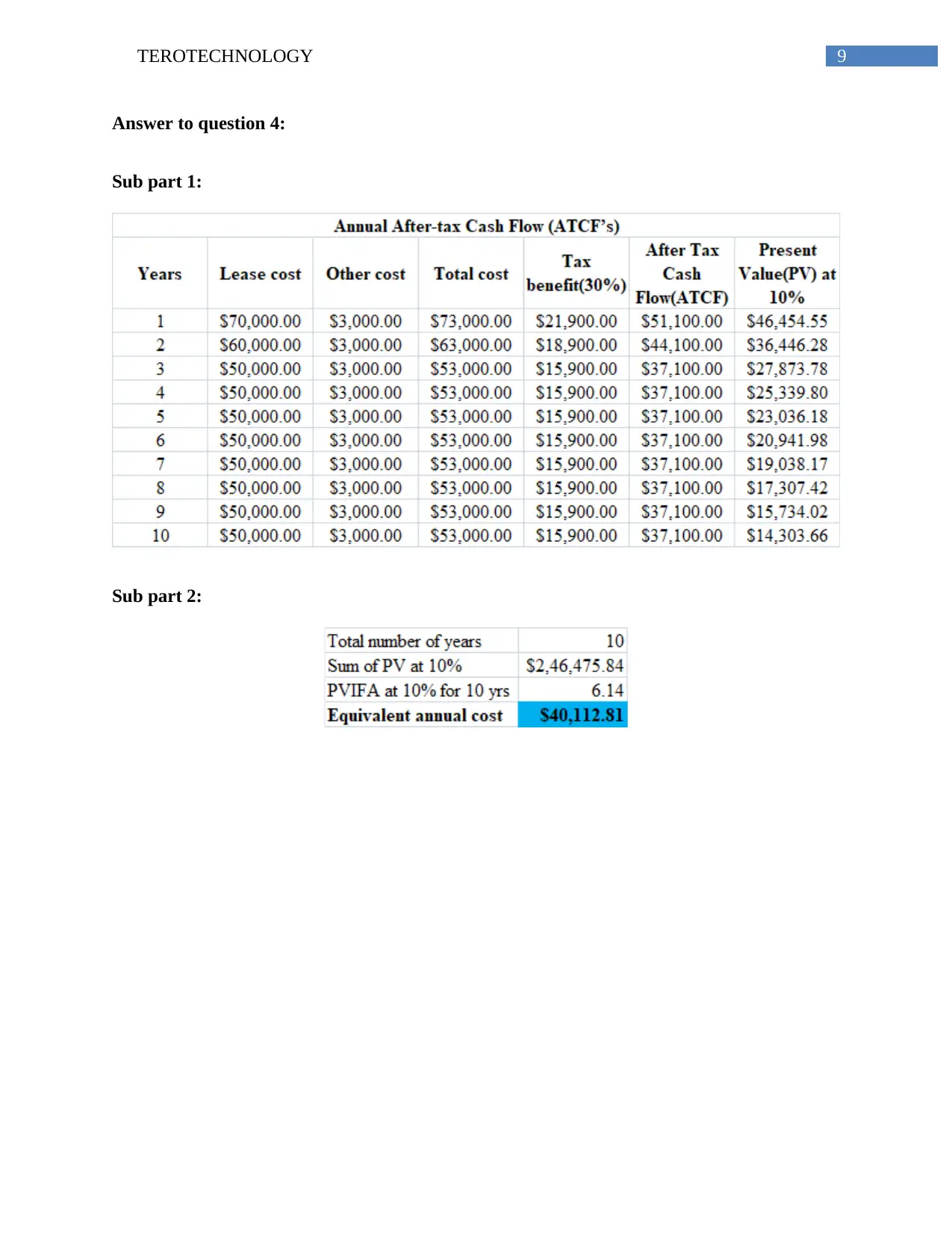

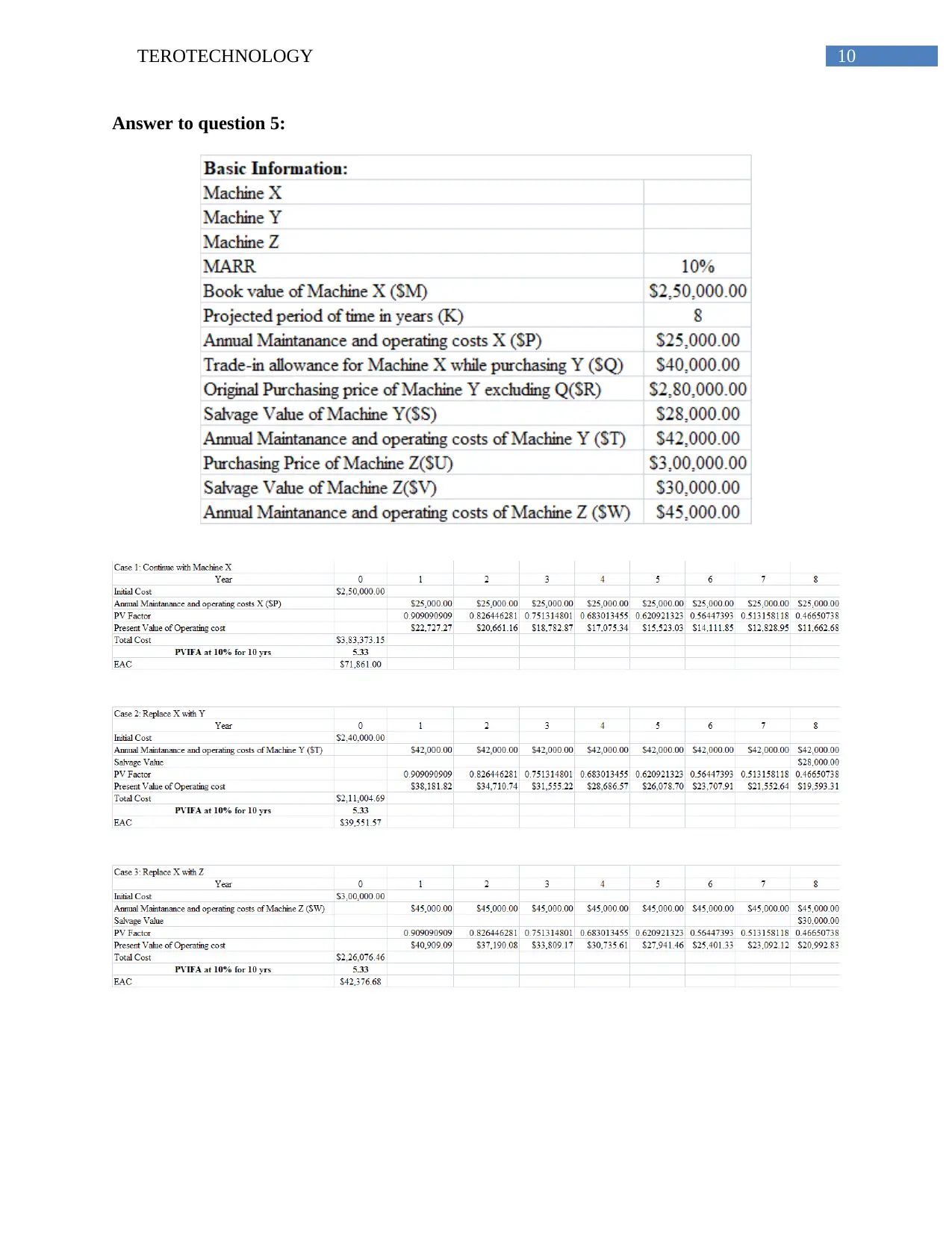

This report delves into the concept of Terotechnology, focusing on capital investment, asset lifecycle costing, and investment appraisal techniques. It begins with an introduction to capital investment and its evaluation, followed by a detailed explanation of Terotechnology as a method for assessing the profitability and economic benefits of assets throughout their lifecycle, considering associated costs like maintenance and repairs. The report uses Soon Mining Limited as a case study, analyzing its capital assets and highlighting gaps in lifecycle costing practices. It includes practical examples and calculations related to investment valuation, such as present worth, annual worth, and internal rate of return (IRR) for different automation degrees. The report concludes with recommendations for improving capital investment strategies, emphasizing the importance of cost-benefit analysis and efficient asset management. References and an appendix with additional financial data are also included.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.