Engineering Report: Terotechnology, Lifecycle Costing, and Investment

VerifiedAdded on 2022/11/24

|14

|1558

|427

Report

AI Summary

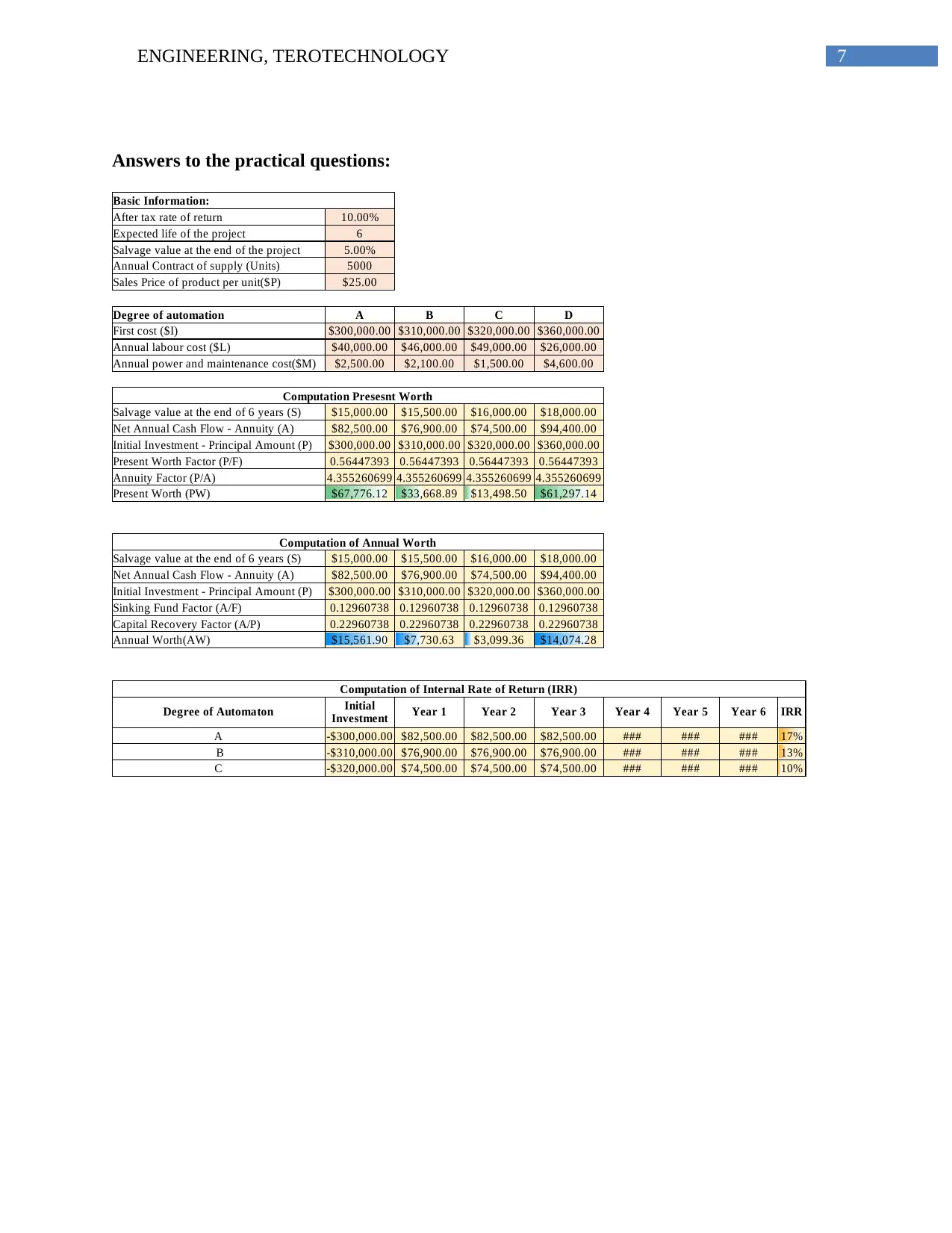

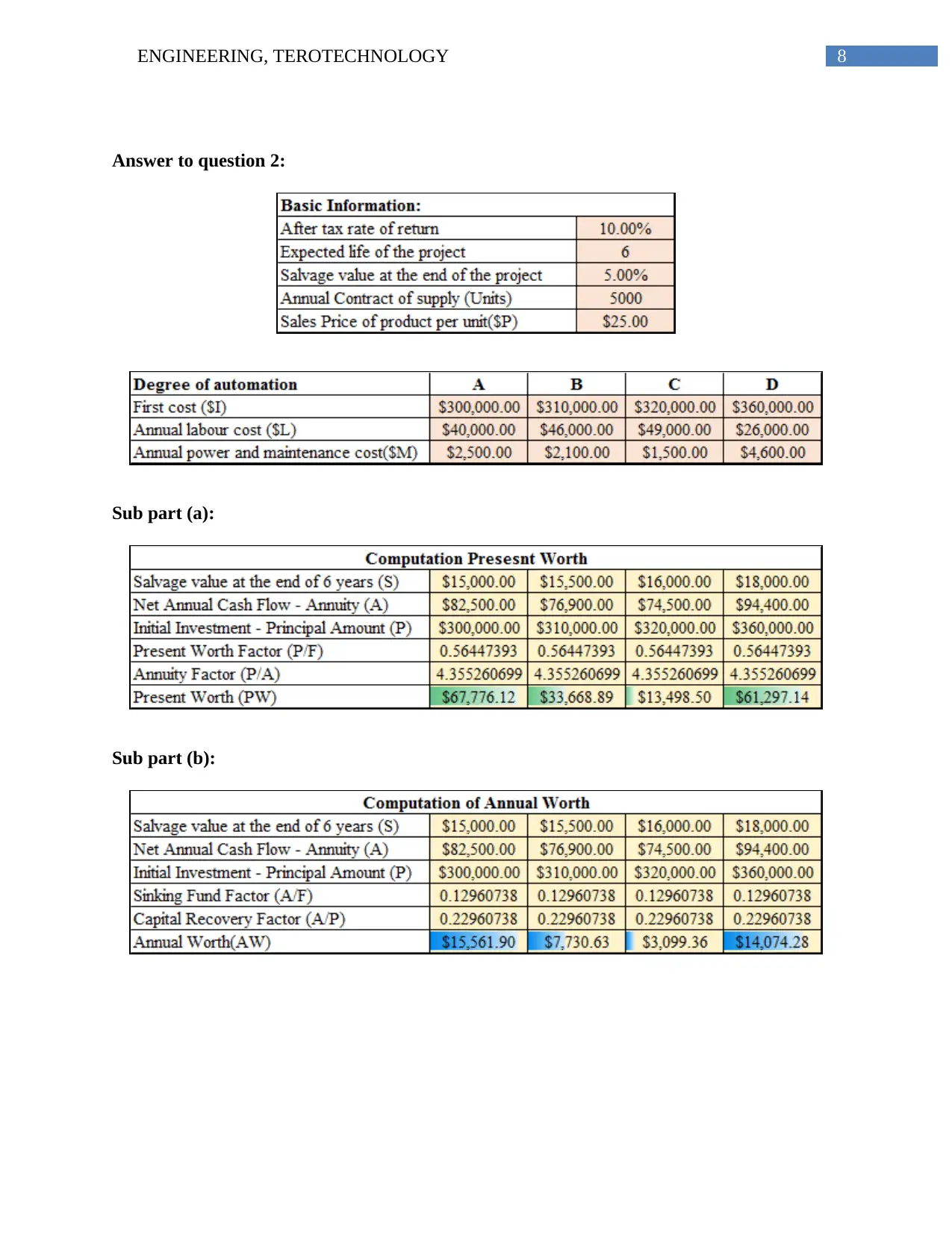

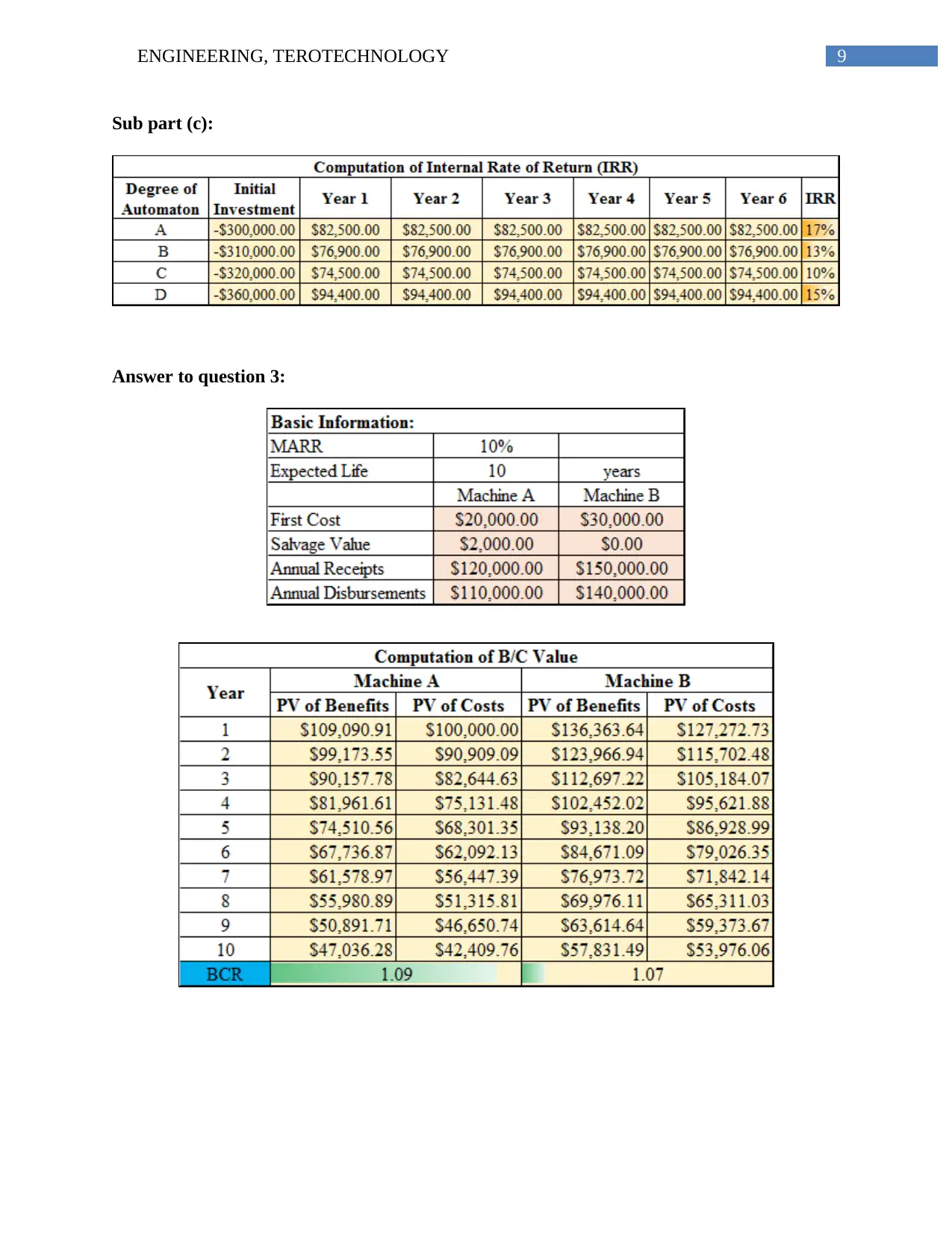

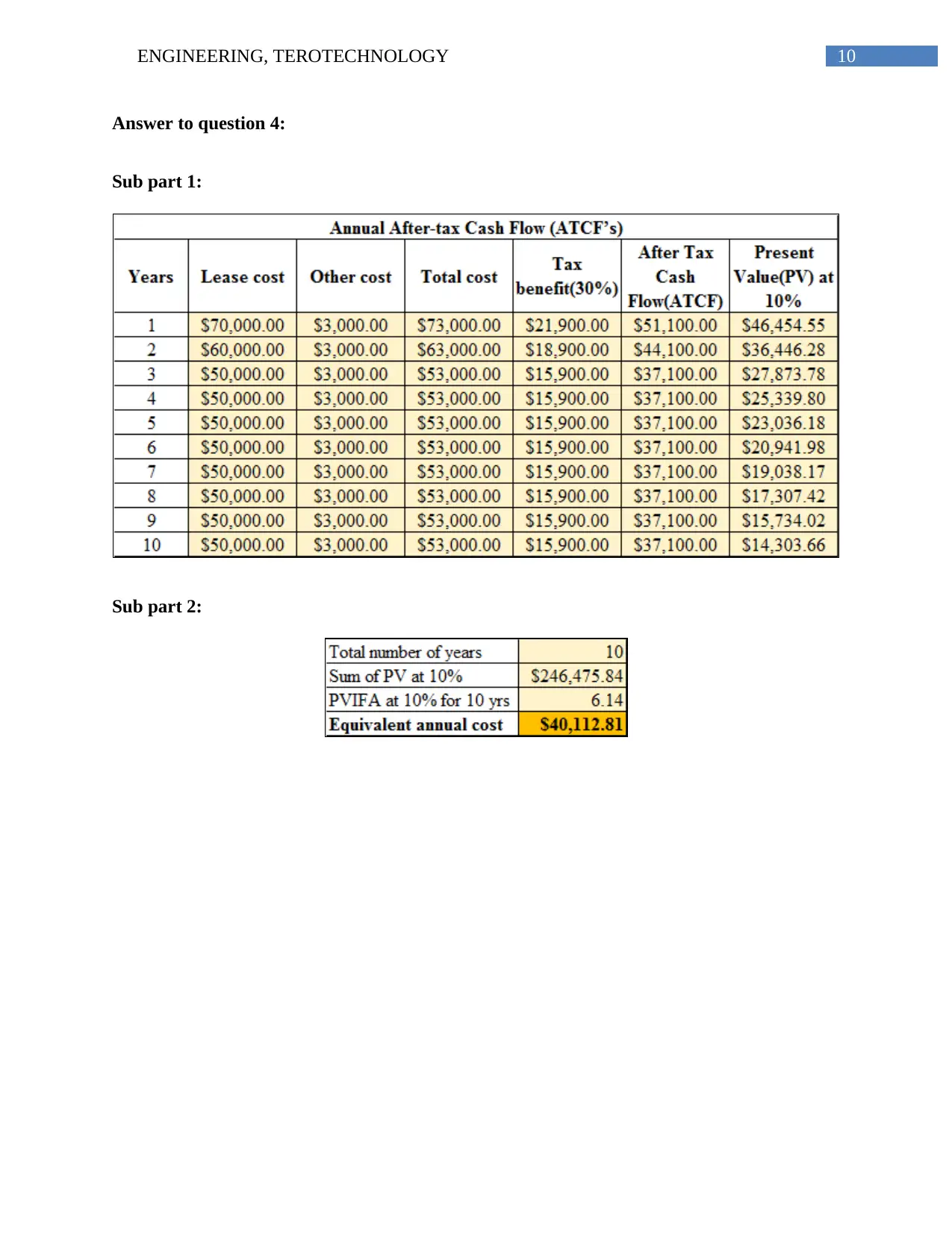

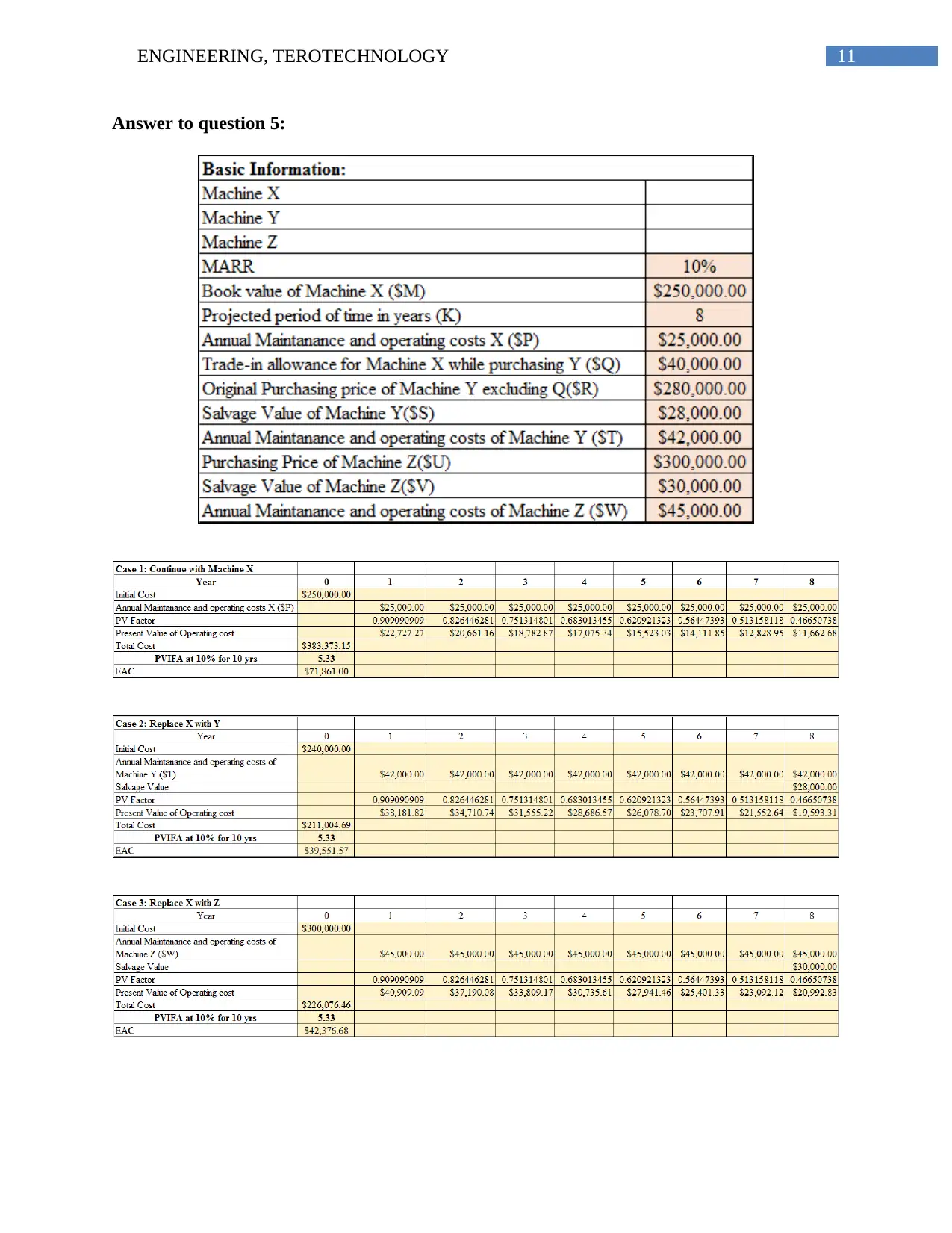

This report explores Terotechnology and asset lifecycle costing within the context of capital investment analysis, focusing on the application of these concepts to evaluate long-term investments in capital assets. The report begins with an introduction to Terotechnology, which involves balancing the costs and benefits associated with capital investments throughout their lifecycle, and asset lifecycle costing, which involves analyzing all costs associated with an asset from its acquisition to its disposal. The report uses the example of Santa FE Minerals Limited to illustrate the practical application of these concepts, analyzing the company's investment in capital assets and identifying gaps in its lifecycle costing approach. The report then presents recommendations for improving the company's investment evaluation and appraisal process, emphasizing the importance of considering all costs and benefits associated with capital assets throughout their lifecycle to make informed investment decisions. The report also includes answers to practical questions related to the assignment brief, and concludes with a list of references and bibliography.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.