Accounting Disclosure and Market Reaction: A Case Study of Tesco PLC

VerifiedAdded on 2023/06/10

|15

|3631

|98

Report

AI Summary

This report examines the market reaction to Tesco PLC's announcement of a new CEO, Dave Lewis, following a period of declining profits. Part 1 discusses how accounting disclosures affect the capital market's perception of the firm, exploring the value-relevance and information content of these disclosures. It analyzes various sources of disclosures and factors influencing market reactions. Part 2 provides evidence of the market's reaction to the CEO appointment announcement by analyzing Tesco's share price and comparing it to the FTSE 100 index in a three-day window around the announcement date. The report uses tabular and graphical representations to illustrate the changes in share price and trading volume, offering insights into investor behavior and market dynamics during this period. Desklib provides a platform for students to access this and similar solved assignments for academic support.

Running head: MARKET BASED ACCOUNTING

Market Based Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Market Based Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MARKET BASED ACCOUNTING

Table of Contents

Part 1:.........................................................................................................................................2

Accounting disclosure effecting the capital market perception of the firm:..............................2

Introduction:...............................................................................................................................2

Market response to Accounting Disclosure:..............................................................................2

The information content of specific accounting data:................................................................4

Conclusion:................................................................................................................................6

Part 2:.........................................................................................................................................7

Market reaction to the announcement of appointment of new CEO:.........................................7

Reasons behind investors reactions:...........................................................................................9

References................................................................................................................................12

Table of Contents

Part 1:.........................................................................................................................................2

Accounting disclosure effecting the capital market perception of the firm:..............................2

Introduction:...............................................................................................................................2

Market response to Accounting Disclosure:..............................................................................2

The information content of specific accounting data:................................................................4

Conclusion:................................................................................................................................6

Part 2:.........................................................................................................................................7

Market reaction to the announcement of appointment of new CEO:.........................................7

Reasons behind investors reactions:...........................................................................................9

References................................................................................................................................12

2MARKET BASED ACCOUNTING

Part 1:

Accounting disclosure effecting the capital market perception of the firm:

Introduction:

Accounting disclosure is related with the revealing the information to the capital

market. Accounting disclosure is not concerned with discovering the information by the firm.

Disclosure assumes that the information is before-hand known to the entity disclosing

information (Miller and Skinner 2015). Accounting disclosure is related to external parties

and the disclosure is regarding the company’s economic transactions and information about

the cash flows which is already held by the firm’s managers.

Given the problems of asymmetry of information, there has been growing number of

calls for firms to improve the accounting disclosure of intellectual capital as it helps in

improving the market understanding of the company’s value creation procedure and

facilitating the more precise firm’s valuation. The relationship amid the accounting

information and the capital markets has long been the matter of extensive study. The purpose

of this study is to examine how the accounting information affects the capital market.

Market response to Accounting Disclosure:

According to Park, Chae and Cho (2017) the relationship among the accounting

information and capital market has engrossed substantial amount of attention to an extent that

is possibly very highly prevalent issues in the work of accounting. The importance in this

matter is genuine, assumed that the normally recognized accounting report are directed at

offering the stakeholders with the appropriate information for making decisions related to

shares. Even though the information of accounting is used in numerous context such as

process of contracting inside the company or amid the firms and its creditors and contractors

Part 1:

Accounting disclosure effecting the capital market perception of the firm:

Introduction:

Accounting disclosure is related with the revealing the information to the capital

market. Accounting disclosure is not concerned with discovering the information by the firm.

Disclosure assumes that the information is before-hand known to the entity disclosing

information (Miller and Skinner 2015). Accounting disclosure is related to external parties

and the disclosure is regarding the company’s economic transactions and information about

the cash flows which is already held by the firm’s managers.

Given the problems of asymmetry of information, there has been growing number of

calls for firms to improve the accounting disclosure of intellectual capital as it helps in

improving the market understanding of the company’s value creation procedure and

facilitating the more precise firm’s valuation. The relationship amid the accounting

information and the capital markets has long been the matter of extensive study. The purpose

of this study is to examine how the accounting information affects the capital market.

Market response to Accounting Disclosure:

According to Park, Chae and Cho (2017) the relationship among the accounting

information and capital market has engrossed substantial amount of attention to an extent that

is possibly very highly prevalent issues in the work of accounting. The importance in this

matter is genuine, assumed that the normally recognized accounting report are directed at

offering the stakeholders with the appropriate information for making decisions related to

shares. Even though the information of accounting is used in numerous context such as

process of contracting inside the company or amid the firms and its creditors and contractors

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MARKET BASED ACCOUNTING

relating to the capital markets, such information are hypothetical to ease the forecast of the

company’s future cash flows. They are also assigned to assist the investors in assessing the

future securities risk and return.

The main purpose of researching on the capital market is to evaluate whether the

bookkeeping data that is provided is value relevant statistics to the investors and incremental

to all the other source of information that is available in public (Qiu, Shaukat and Tharyan

2016). The information containing the accounting number is concluded from the variations in

the level or otherwise the inconsistency of the stock prices and inferred from the variations in

the level or in the inconsistency of the stock values and from the alterations in the shares that

is traded over the period of short time in which the data is released in public. If the capital

market is efficient, share prices should reflect the complete and newly released information

(Li 2015). As a result, variation in the share prices or alterations in the security traded is

anticipated during the publication phase given that the released numbers deliver new info to

the participants in the market regarding the sum or improbability of projected future cash

flows. The informative content of earning is concluded from the abnormal mean returns or

from the variations in the size of trading over the short period of announcing data.

Since the sum of incomes is futile, such amount should be contrasted with the market

anticipations regarding the incomes. Under the hypothesis information-subject, positive

unanticipated earnings may on average result in positive irregular returns and negative

unanticipated incomes with positive unanticipated earnings (Harrison and Smith 2015). It

also reveals statistically negative for firms that have unanticipated earnings.

As the accounting figures are reported by firms all through the year Christensen, Hail

and Leuz (2016) proposed to conduct an examination of the incremental data content of

bookkeeping proceedings for better understanding of how the shareholders route the

relating to the capital markets, such information are hypothetical to ease the forecast of the

company’s future cash flows. They are also assigned to assist the investors in assessing the

future securities risk and return.

The main purpose of researching on the capital market is to evaluate whether the

bookkeeping data that is provided is value relevant statistics to the investors and incremental

to all the other source of information that is available in public (Qiu, Shaukat and Tharyan

2016). The information containing the accounting number is concluded from the variations in

the level or otherwise the inconsistency of the stock prices and inferred from the variations in

the level or in the inconsistency of the stock values and from the alterations in the shares that

is traded over the period of short time in which the data is released in public. If the capital

market is efficient, share prices should reflect the complete and newly released information

(Li 2015). As a result, variation in the share prices or alterations in the security traded is

anticipated during the publication phase given that the released numbers deliver new info to

the participants in the market regarding the sum or improbability of projected future cash

flows. The informative content of earning is concluded from the abnormal mean returns or

from the variations in the size of trading over the short period of announcing data.

Since the sum of incomes is futile, such amount should be contrasted with the market

anticipations regarding the incomes. Under the hypothesis information-subject, positive

unanticipated earnings may on average result in positive irregular returns and negative

unanticipated incomes with positive unanticipated earnings (Harrison and Smith 2015). It

also reveals statistically negative for firms that have unanticipated earnings.

As the accounting figures are reported by firms all through the year Christensen, Hail

and Leuz (2016) proposed to conduct an examination of the incremental data content of

bookkeeping proceedings for better understanding of how the shareholders route the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MARKET BASED ACCOUNTING

accounting information. Study conducted on 120 randomly chosen UK companies shows that

both the introductory and provisional announcement have the highest number of information

content. The accounting disclosure of firms unveils noteworthy content of information. In

contrast to this, the price effect of the annual general meetings appears to the insignificant.

The correlation tests reveal that abnormal returns related with the introductory earnings

pronouncement were related positively to the abnormal return both at the provisional

disclosure and firms annual accounting disclosure dates. This provides a suggestion that firms

which unveil higher preliminary informative announcement also tends to possess highly

informative accounting reports and interim accounting disclosure.

The information content of specific accounting data:

According to the investigation conducted by Macve (2015) info content of present

cost information disclosed by numerous businesses listed on the London Stock Exchange

shows that such information has small but real effect on the stock returns. As the market

reaction to the accounting disclosure varies among the firms, several studies have assessed

the possibilities of determinants of such differences. Results of the studies shows that

volatility in returns or the abnormal mean return is positively associated with the size of

unanticipated yearly or interim earnings.

Researchers such as Maynard (2017) theorize that companies select the accounting

programs or take into the consideration the flexible accruals in accounting to reveal the

secluded information of the management regarding the forthcoming prospects. If it is found

that the discretionary accruals are actually informative then the irregular stocks return around

the financial statements release must be associated to the sign and amount of earnings that

originates through manipulations.

accounting information. Study conducted on 120 randomly chosen UK companies shows that

both the introductory and provisional announcement have the highest number of information

content. The accounting disclosure of firms unveils noteworthy content of information. In

contrast to this, the price effect of the annual general meetings appears to the insignificant.

The correlation tests reveal that abnormal returns related with the introductory earnings

pronouncement were related positively to the abnormal return both at the provisional

disclosure and firms annual accounting disclosure dates. This provides a suggestion that firms

which unveil higher preliminary informative announcement also tends to possess highly

informative accounting reports and interim accounting disclosure.

The information content of specific accounting data:

According to the investigation conducted by Macve (2015) info content of present

cost information disclosed by numerous businesses listed on the London Stock Exchange

shows that such information has small but real effect on the stock returns. As the market

reaction to the accounting disclosure varies among the firms, several studies have assessed

the possibilities of determinants of such differences. Results of the studies shows that

volatility in returns or the abnormal mean return is positively associated with the size of

unanticipated yearly or interim earnings.

Researchers such as Maynard (2017) theorize that companies select the accounting

programs or take into the consideration the flexible accruals in accounting to reveal the

secluded information of the management regarding the forthcoming prospects. If it is found

that the discretionary accruals are actually informative then the irregular stocks return around

the financial statements release must be associated to the sign and amount of earnings that

originates through manipulations.

5MARKET BASED ACCOUNTING

The efficient market hypothesis explains that the share prices must react promptly and

totally to any form of value-relevant information and the subsequent changes in price must

not be associated to such reactions (Martin and Roychowdhury 2015). In contrary to such

hypothesis, numerous empirical studies have represented that stock price reactions on the

incomes publication date is unfinished, this is because prices adjust progressively to the new

info. As the abnormal returns have the identical sign as the unanticipated earnings, investors

appear to underact to the information that is contained in the earnings.

The different event studies have concentrated on the reaction of market to the

accounting disclosure in short time period, the associated studies assess the connection amid

the stock returns and bookkeeping disclosure over the long period (Hoitash, Hoitash and

Yezegel 2017). While the previous studies have examined accounting data role in offering

incremental info which may create an impact on the perception of investors over the

forthcoming prospects of the firm, the latter offer the evidence regarding the part of these

information in the form of summary of the events that have impacted firms throughout the

reporting period.

In opposed to the studies related to market reaction, related studies do not provide any

casual association among the secretarial facts and stock values. They hardly assume that the

participants in the market make the use of accounting information in their course of valuation

(Macve 2015). They only theorize that if the accounting information provides the measures of

worthy summary of occasions combined in the price of shares, they are value relevant since

their usage might provide the firm with value which is near the market value.

According to Maynard (2017) differences in conservative earnings amid the two

groups is largely associated to the circumstance that managers that are more risk opposed,

expect the recognition of bad news while the co-efficient of good news are significant for the

The efficient market hypothesis explains that the share prices must react promptly and

totally to any form of value-relevant information and the subsequent changes in price must

not be associated to such reactions (Martin and Roychowdhury 2015). In contrary to such

hypothesis, numerous empirical studies have represented that stock price reactions on the

incomes publication date is unfinished, this is because prices adjust progressively to the new

info. As the abnormal returns have the identical sign as the unanticipated earnings, investors

appear to underact to the information that is contained in the earnings.

The different event studies have concentrated on the reaction of market to the

accounting disclosure in short time period, the associated studies assess the connection amid

the stock returns and bookkeeping disclosure over the long period (Hoitash, Hoitash and

Yezegel 2017). While the previous studies have examined accounting data role in offering

incremental info which may create an impact on the perception of investors over the

forthcoming prospects of the firm, the latter offer the evidence regarding the part of these

information in the form of summary of the events that have impacted firms throughout the

reporting period.

In opposed to the studies related to market reaction, related studies do not provide any

casual association among the secretarial facts and stock values. They hardly assume that the

participants in the market make the use of accounting information in their course of valuation

(Macve 2015). They only theorize that if the accounting information provides the measures of

worthy summary of occasions combined in the price of shares, they are value relevant since

their usage might provide the firm with value which is near the market value.

According to Maynard (2017) differences in conservative earnings amid the two

groups is largely associated to the circumstance that managers that are more risk opposed,

expect the recognition of bad news while the co-efficient of good news are significant for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MARKET BASED ACCOUNTING

risk averse managers. Whereas the bad news is more significant for the risk opposed group

only. The lower association among the earnings and the returns which is undesirable earnings

are not considered as value relevant as losses are anticipated to preserve indefinitely.

Preceding from the above explanation the strength of relationship amid the earnings

and returns can be regarded as the measure of the value-relevant of accounting information or

disclosure. Hypothesizing, that greater is the value relevance the better are accounting

figures.

Conclusion:

The empirical evidences are associated largely with the informational perspective of

accounting figures which states that the accounting disclosure by firms are relevant for the

purpose of valuation given the information reflects the influence on the stock prices of offer

the incremental information that impact the perceptions of investors on firms. Overall, the

study intended to explain how the accounting numbers and stocks returns are related to each

other.

risk averse managers. Whereas the bad news is more significant for the risk opposed group

only. The lower association among the earnings and the returns which is undesirable earnings

are not considered as value relevant as losses are anticipated to preserve indefinitely.

Preceding from the above explanation the strength of relationship amid the earnings

and returns can be regarded as the measure of the value-relevant of accounting information or

disclosure. Hypothesizing, that greater is the value relevance the better are accounting

figures.

Conclusion:

The empirical evidences are associated largely with the informational perspective of

accounting figures which states that the accounting disclosure by firms are relevant for the

purpose of valuation given the information reflects the influence on the stock prices of offer

the incremental information that impact the perceptions of investors on firms. Overall, the

study intended to explain how the accounting numbers and stocks returns are related to each

other.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MARKET BASED ACCOUNTING

Part 2:

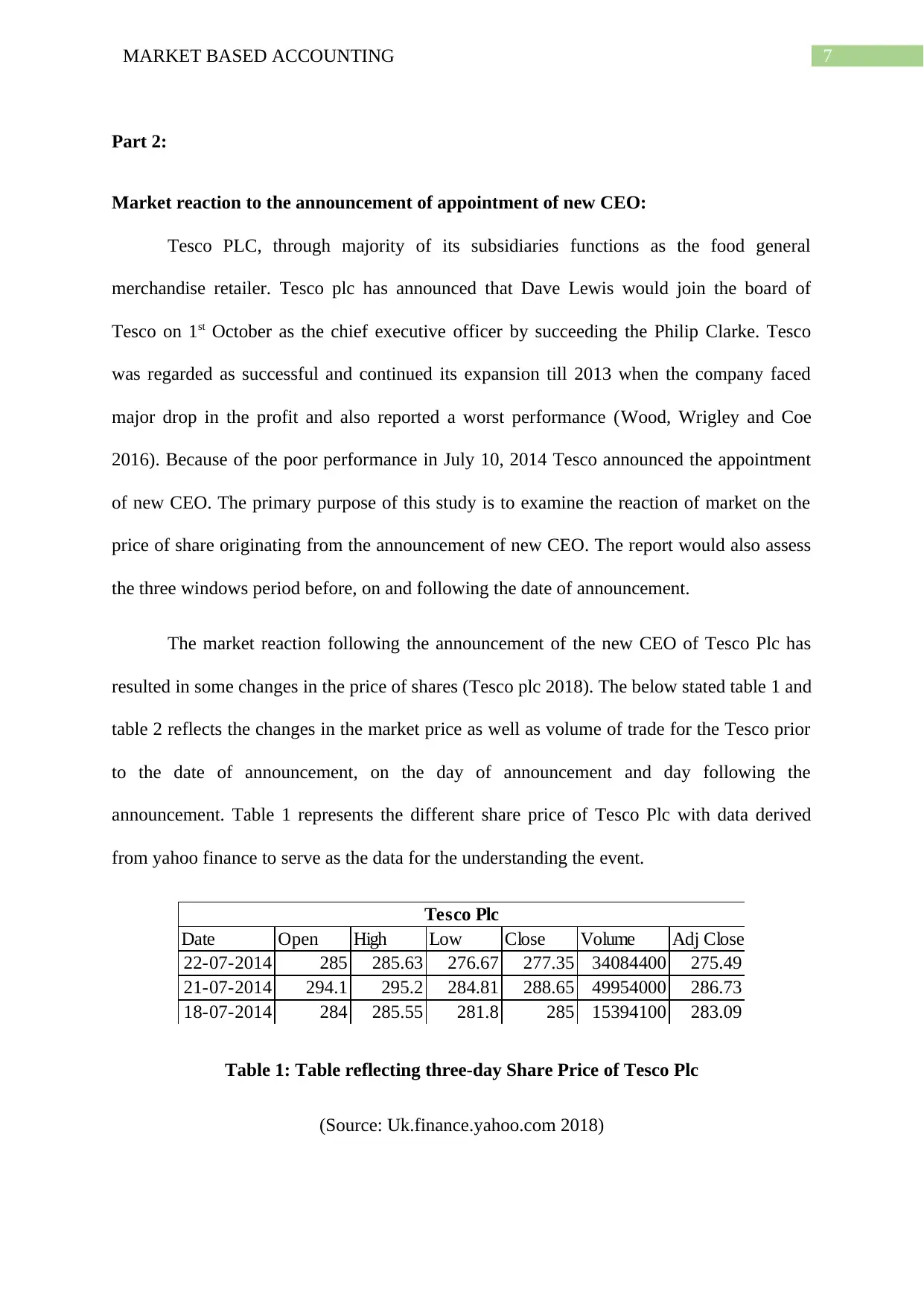

Market reaction to the announcement of appointment of new CEO:

Tesco PLC, through majority of its subsidiaries functions as the food general

merchandise retailer. Tesco plc has announced that Dave Lewis would join the board of

Tesco on 1st October as the chief executive officer by succeeding the Philip Clarke. Tesco

was regarded as successful and continued its expansion till 2013 when the company faced

major drop in the profit and also reported a worst performance (Wood, Wrigley and Coe

2016). Because of the poor performance in July 10, 2014 Tesco announced the appointment

of new CEO. The primary purpose of this study is to examine the reaction of market on the

price of share originating from the announcement of new CEO. The report would also assess

the three windows period before, on and following the date of announcement.

The market reaction following the announcement of the new CEO of Tesco Plc has

resulted in some changes in the price of shares (Tesco plc 2018). The below stated table 1 and

table 2 reflects the changes in the market price as well as volume of trade for the Tesco prior

to the date of announcement, on the day of announcement and day following the

announcement. Table 1 represents the different share price of Tesco Plc with data derived

from yahoo finance to serve as the data for the understanding the event.

Date Open High Low Close Volume Adj Close

22-07-2014 285 285.63 276.67 277.35 34084400 275.49

21-07-2014 294.1 295.2 284.81 288.65 49954000 286.73

18-07-2014 284 285.55 281.8 285 15394100 283.09

Tesco Plc

Table 1: Table reflecting three-day Share Price of Tesco Plc

(Source: Uk.finance.yahoo.com 2018)

Part 2:

Market reaction to the announcement of appointment of new CEO:

Tesco PLC, through majority of its subsidiaries functions as the food general

merchandise retailer. Tesco plc has announced that Dave Lewis would join the board of

Tesco on 1st October as the chief executive officer by succeeding the Philip Clarke. Tesco

was regarded as successful and continued its expansion till 2013 when the company faced

major drop in the profit and also reported a worst performance (Wood, Wrigley and Coe

2016). Because of the poor performance in July 10, 2014 Tesco announced the appointment

of new CEO. The primary purpose of this study is to examine the reaction of market on the

price of share originating from the announcement of new CEO. The report would also assess

the three windows period before, on and following the date of announcement.

The market reaction following the announcement of the new CEO of Tesco Plc has

resulted in some changes in the price of shares (Tesco plc 2018). The below stated table 1 and

table 2 reflects the changes in the market price as well as volume of trade for the Tesco prior

to the date of announcement, on the day of announcement and day following the

announcement. Table 1 represents the different share price of Tesco Plc with data derived

from yahoo finance to serve as the data for the understanding the event.

Date Open High Low Close Volume Adj Close

22-07-2014 285 285.63 276.67 277.35 34084400 275.49

21-07-2014 294.1 295.2 284.81 288.65 49954000 286.73

18-07-2014 284 285.55 281.8 285 15394100 283.09

Tesco Plc

Table 1: Table reflecting three-day Share Price of Tesco Plc

(Source: Uk.finance.yahoo.com 2018)

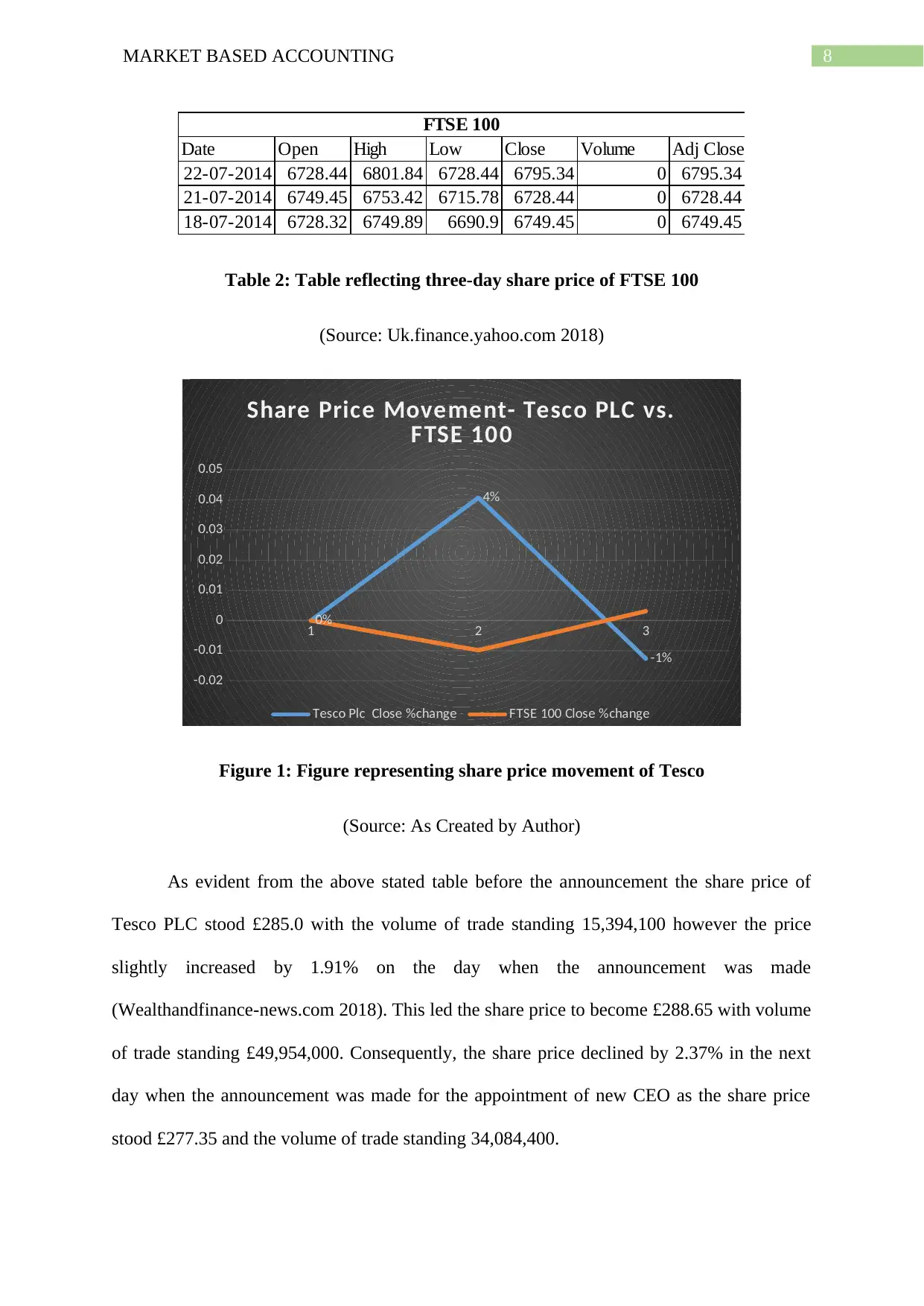

8MARKET BASED ACCOUNTING

Date Open High Low Close Volume Adj Close

22-07-2014 6728.44 6801.84 6728.44 6795.34 0 6795.34

21-07-2014 6749.45 6753.42 6715.78 6728.44 0 6728.44

18-07-2014 6728.32 6749.89 6690.9 6749.45 0 6749.45

FTSE 100

Table 2: Table reflecting three-day share price of FTSE 100

(Source: Uk.finance.yahoo.com 2018)

1 2 3

-0.02

-0.01

0

0.01

0.02

0.03

0.04

0.05

0%

4%

-1%

Share Price Movement- Tesco PLC vs.

FTSE 100

Tesco Plc Close %change FTSE 100 Close %change

Figure 1: Figure representing share price movement of Tesco

(Source: As Created by Author)

As evident from the above stated table before the announcement the share price of

Tesco PLC stood £285.0 with the volume of trade standing 15,394,100 however the price

slightly increased by 1.91% on the day when the announcement was made

(Wealthandfinance-news.com 2018). This led the share price to become £288.65 with volume

of trade standing £49,954,000. Consequently, the share price declined by 2.37% in the next

day when the announcement was made for the appointment of new CEO as the share price

stood £277.35 and the volume of trade standing 34,084,400.

Date Open High Low Close Volume Adj Close

22-07-2014 6728.44 6801.84 6728.44 6795.34 0 6795.34

21-07-2014 6749.45 6753.42 6715.78 6728.44 0 6728.44

18-07-2014 6728.32 6749.89 6690.9 6749.45 0 6749.45

FTSE 100

Table 2: Table reflecting three-day share price of FTSE 100

(Source: Uk.finance.yahoo.com 2018)

1 2 3

-0.02

-0.01

0

0.01

0.02

0.03

0.04

0.05

0%

4%

-1%

Share Price Movement- Tesco PLC vs.

FTSE 100

Tesco Plc Close %change FTSE 100 Close %change

Figure 1: Figure representing share price movement of Tesco

(Source: As Created by Author)

As evident from the above stated table before the announcement the share price of

Tesco PLC stood £285.0 with the volume of trade standing 15,394,100 however the price

slightly increased by 1.91% on the day when the announcement was made

(Wealthandfinance-news.com 2018). This led the share price to become £288.65 with volume

of trade standing £49,954,000. Consequently, the share price declined by 2.37% in the next

day when the announcement was made for the appointment of new CEO as the share price

stood £277.35 and the volume of trade standing 34,084,400.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MARKET BASED ACCOUNTING

In comparison to the Tesco overall changes in the market price of FTSE 100 the study

provides that there was the slight difference. This is because the FTSE 100 market price prior

to the day of announcement stood £6,749.45 then it slightly fell to 0.31% (Turker 2018).

Unlike the share price of Tesco that went up on that particular day, making the FTSE price to

fall by £6,728.44 on the date of announcement. However, the price increased to £6,795.34

representing a rise of 0.99% rise in the market price while the share price of Tesco fell by

2.37% on the same day.

The appointment of new investors may enable the investors to think that the company

is having the problem in future and they may react in both positive or negative way. The

market reactions have significant effect on the outcome of the announcement of new CEO for

Tesco Plc (Haddock-Millar and Rigby 2015). The announcement relating to the appointment

of new CEO was embraced by the investors in a positive manner. The investors assumed that

it would reflect an anticipation in their future cash flow and there was positive response in the

share price on the day of announcement which was oboe the share price prior to the

announcement day. The market reactions also included that the new leadership would help in

stabilizing the organizations poor corporate governance in future and would bring a better

name to the company which may interest additional investors.

Reasons behind investors reactions:

The market price of the company refers to the economic price where goods and

services is provided in the market place. The market price and the market value remains equal

under the conditions of market efficiency and rational expectations. However, Mason and

Evans (2015) pointed out that determination of market price comprises of market mix

strategy and decisions related to demand. It also includes the costs and other environmental

factors namely the economy, considerations resellers and the government. Ismail, (2017)

additionally added certain internal factors that creates the market price of Tesco.

In comparison to the Tesco overall changes in the market price of FTSE 100 the study

provides that there was the slight difference. This is because the FTSE 100 market price prior

to the day of announcement stood £6,749.45 then it slightly fell to 0.31% (Turker 2018).

Unlike the share price of Tesco that went up on that particular day, making the FTSE price to

fall by £6,728.44 on the date of announcement. However, the price increased to £6,795.34

representing a rise of 0.99% rise in the market price while the share price of Tesco fell by

2.37% on the same day.

The appointment of new investors may enable the investors to think that the company

is having the problem in future and they may react in both positive or negative way. The

market reactions have significant effect on the outcome of the announcement of new CEO for

Tesco Plc (Haddock-Millar and Rigby 2015). The announcement relating to the appointment

of new CEO was embraced by the investors in a positive manner. The investors assumed that

it would reflect an anticipation in their future cash flow and there was positive response in the

share price on the day of announcement which was oboe the share price prior to the

announcement day. The market reactions also included that the new leadership would help in

stabilizing the organizations poor corporate governance in future and would bring a better

name to the company which may interest additional investors.

Reasons behind investors reactions:

The market price of the company refers to the economic price where goods and

services is provided in the market place. The market price and the market value remains equal

under the conditions of market efficiency and rational expectations. However, Mason and

Evans (2015) pointed out that determination of market price comprises of market mix

strategy and decisions related to demand. It also includes the costs and other environmental

factors namely the economy, considerations resellers and the government. Ismail, (2017)

additionally added certain internal factors that creates the market price of Tesco.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MARKET BASED ACCOUNTING

There are internal factors that create an effect on the market price of the company and

these includes the quality of the product, leadership, quality of performance and research and

development. There are some of the important economic or regulatory factors that resulted in

possible reaction to the market which included inflation, demand and cost price (Tesco 2014).

Tesco being the grocery company faced numerous challenges that provided the rival with the

opportunity to take majority of the Tesco’s investors in the year 2014. Gauging into the

annual report of Tesco 2014 there were numerous corporate governance changes that ranged

from non-payment of the due amount of executive remuneration to failure in the board in

meeting target. Hence, this resulted the investors to react negatively towards the market price

of Tesco.

Turker (2018) explained the factors that was related to the disclosure of information

by the analyst in two ways namely positive correlation and negative correlation. Positive

correlation included those factors that caused market reactions due to higher volatile returns

and uncertain cash flow security. Negative correlation included a possible failure of the

company.

The stakeholders and the investors may possibly consider the appointment of CEO as

capable of producing future success. According to Mason and Evans (2015) findings it is

noticed that the press release played the vital role for the stock market since the investors

reacted positively to the media information. The disclosure of media enables the investors to

react upon the market conditions whether there is a good or bad news. According to findings

of Kukreja and Gupta (2016) it is found that investors react to the non-routine turnovers upon

the appointment of the successors from outside the firm as the new CEO of the company.

The CEO is the person that holds the vital position in the company. The CEO designs

the strategy of the company to compete with the other competing firms in the financial

There are internal factors that create an effect on the market price of the company and

these includes the quality of the product, leadership, quality of performance and research and

development. There are some of the important economic or regulatory factors that resulted in

possible reaction to the market which included inflation, demand and cost price (Tesco 2014).

Tesco being the grocery company faced numerous challenges that provided the rival with the

opportunity to take majority of the Tesco’s investors in the year 2014. Gauging into the

annual report of Tesco 2014 there were numerous corporate governance changes that ranged

from non-payment of the due amount of executive remuneration to failure in the board in

meeting target. Hence, this resulted the investors to react negatively towards the market price

of Tesco.

Turker (2018) explained the factors that was related to the disclosure of information

by the analyst in two ways namely positive correlation and negative correlation. Positive

correlation included those factors that caused market reactions due to higher volatile returns

and uncertain cash flow security. Negative correlation included a possible failure of the

company.

The stakeholders and the investors may possibly consider the appointment of CEO as

capable of producing future success. According to Mason and Evans (2015) findings it is

noticed that the press release played the vital role for the stock market since the investors

reacted positively to the media information. The disclosure of media enables the investors to

react upon the market conditions whether there is a good or bad news. According to findings

of Kukreja and Gupta (2016) it is found that investors react to the non-routine turnovers upon

the appointment of the successors from outside the firm as the new CEO of the company.

The CEO is the person that holds the vital position in the company. The CEO designs

the strategy of the company to compete with the other competing firms in the financial

11MARKET BASED ACCOUNTING

market. The poor performance of the CEO is directly related to the share price of the

company and reaction of the investors also create an impact on the company. Similarly,

gauging into the financial report of Tesco it is found that no remuneration has been provided

to the directors since the company has failed to meet the target and there were several

changes in the corporate governance and performance of the company (Turker 2018). This

included the resignation of some of the key officer signalling the problem in the company

which may cause market reaction. The market reaction originating from the announcement of

the Tesco’s new CEO has introduced some changes in the share price.

The appointment of the new CEO would bring Tesco with new international

consumer experience and knowledge in change management, brand administration, business

administration and strategy. The appointment of the new CEO would bring in fresh

perspective to the company as well as new profile. The leadership of new CEO would help

the company in sustaining and improving the company’s top most spot in the retail market.

market. The poor performance of the CEO is directly related to the share price of the

company and reaction of the investors also create an impact on the company. Similarly,

gauging into the financial report of Tesco it is found that no remuneration has been provided

to the directors since the company has failed to meet the target and there were several

changes in the corporate governance and performance of the company (Turker 2018). This

included the resignation of some of the key officer signalling the problem in the company

which may cause market reaction. The market reaction originating from the announcement of

the Tesco’s new CEO has introduced some changes in the share price.

The appointment of the new CEO would bring Tesco with new international

consumer experience and knowledge in change management, brand administration, business

administration and strategy. The appointment of the new CEO would bring in fresh

perspective to the company as well as new profile. The leadership of new CEO would help

the company in sustaining and improving the company’s top most spot in the retail market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.