AF4S31 Financial Analysis Report: Tesco and Benedict Company

VerifiedAdded on 2022/10/19

|16

|4079

|236

Report

AI Summary

This report presents a comprehensive financial analysis of Tesco and Benedict, examining their financial performance through various lenses. The report begins with an introduction that underscores the significance of financial analysis for organizations and their stakeholders. It then delves into a stakeholder analysis of Tesco, identifying and assessing the interests of directors, suppliers/creditors, and employees. The report continues with a detailed ratio analysis of Benedict Company, evaluating liquidity, profitability, solvency, and efficiency ratios for the years 2000 and 2001. The analysis includes the current ratio, quick ratio, gross profit, return on assets, net profit, return on equity, debt-to-equity ratio, and inventory, creditor, and debtor ratios. The report highlights areas of concern, such as declining ratios, and provides recommendations for improvement. Ultimately, this report offers valuable insights into the financial health and performance of the two companies, providing a basis for informed decision-making by stakeholders.

Running Head: Financial analysis 1

TESCO AND BENEDICT

TESCO AND BENEDICT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial analysis 2

Table of Contents

Introduction......................................................................................................................................3

Stakeholder Analysis of the Tesco Company..................................................................................3

A).................................................................................................................................................3

B)..................................................................................................................................................5

Ratio Analysis..................................................................................................................................6

Liquidity ratios.................................................................................................................................6

Current ratio.................................................................................................................................6

Quick Ratio..................................................................................................................................8

Profitability ratios............................................................................................................................8

Gross Profit..................................................................................................................................9

Return on Assets........................................................................................................................10

Net Profit....................................................................................................................................10

Return on Equity........................................................................................................................10

Solvency Ratios.............................................................................................................................11

Debt to Equity ratio....................................................................................................................11

Debt ot total assets of the company...........................................................................................11

Efficiency Ratios...........................................................................................................................12

Inventory Ratio..........................................................................................................................13

Creditor’s Ratio..........................................................................................................................13

Debtors Ratio.............................................................................................................................13

Cause of Concern...........................................................................................................................14

Recommendations and Conclusions..............................................................................................14

References......................................................................................................................................15

Table of Contents

Introduction......................................................................................................................................3

Stakeholder Analysis of the Tesco Company..................................................................................3

A).................................................................................................................................................3

B)..................................................................................................................................................5

Ratio Analysis..................................................................................................................................6

Liquidity ratios.................................................................................................................................6

Current ratio.................................................................................................................................6

Quick Ratio..................................................................................................................................8

Profitability ratios............................................................................................................................8

Gross Profit..................................................................................................................................9

Return on Assets........................................................................................................................10

Net Profit....................................................................................................................................10

Return on Equity........................................................................................................................10

Solvency Ratios.............................................................................................................................11

Debt to Equity ratio....................................................................................................................11

Debt ot total assets of the company...........................................................................................11

Efficiency Ratios...........................................................................................................................12

Inventory Ratio..........................................................................................................................13

Creditor’s Ratio..........................................................................................................................13

Debtors Ratio.............................................................................................................................13

Cause of Concern...........................................................................................................................14

Recommendations and Conclusions..............................................................................................14

References......................................................................................................................................15

Financial analysis 3

Introduction

Every organization once in a while conducts a financial analysis in order to get aware about

financial position of the company. As per the current requirements the users of the financial

statements has deep interest in the financial performances so that it becomes helpful in making

the strategic business decisions. The statements of the financial nature are the components for

any organization and partners have a profound enthusiasm to break down how well the

organization is working is the real market scenario in terms of the other competitive companies.

The below report examines about the engagement of the stakeholders in order to have an

understanding of the Tesco organization as well how sustainable the organization is. Besides

this, there is one more section of the report that clearly discusses the role of the Benedict

Company, how it has been embraced so as to keep up the potential clients, shareholders,

creditors so as to evaluate whether the decision to make the investment is correct or not

(Martínez‐Ferrero, Garcia‐Sanchez and Cuadrado‐Ballesteros, 2015).

Stakeholder Analysis of the Tesco Company

A)

The term stakeholder in the corporation is one that can be examined as the team without whose

assistance; the firm would cease to exist. The usage of the word stakeholder happens to be in the

year 1963 at Stanford research Institute. At times the stakeholders can also have the 50% interest

in the products or the services which has been provided by the organization. While talking about

the internal stakeholders, the list is made up of the management, employees, administrators,

external stakeholder and the suppliers. In this section a detailed analysis of the Tesco Company

Introduction

Every organization once in a while conducts a financial analysis in order to get aware about

financial position of the company. As per the current requirements the users of the financial

statements has deep interest in the financial performances so that it becomes helpful in making

the strategic business decisions. The statements of the financial nature are the components for

any organization and partners have a profound enthusiasm to break down how well the

organization is working is the real market scenario in terms of the other competitive companies.

The below report examines about the engagement of the stakeholders in order to have an

understanding of the Tesco organization as well how sustainable the organization is. Besides

this, there is one more section of the report that clearly discusses the role of the Benedict

Company, how it has been embraced so as to keep up the potential clients, shareholders,

creditors so as to evaluate whether the decision to make the investment is correct or not

(Martínez‐Ferrero, Garcia‐Sanchez and Cuadrado‐Ballesteros, 2015).

Stakeholder Analysis of the Tesco Company

A)

The term stakeholder in the corporation is one that can be examined as the team without whose

assistance; the firm would cease to exist. The usage of the word stakeholder happens to be in the

year 1963 at Stanford research Institute. At times the stakeholders can also have the 50% interest

in the products or the services which has been provided by the organization. While talking about

the internal stakeholders, the list is made up of the management, employees, administrators,

external stakeholder and the suppliers. In this section a detailed analysis of the Tesco Company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial analysis 4

and its stakeholders has been carried out to understand their needs and the preferences. The three

types of the stakeholders that have been analyzed below are the directors, suppliers, and the

management or say employees of the organization (Asay, Elliott and Rennekamp, 2016).

Directors: As per the stakeholders the directors possess the direct interest in the company and its

affair as they have taken a huge risk by investing in the business. From the analysis it can be

understood that the directors the key people in deciding most of the decisions of Tesco and

hence, their interest becomes imperative automatically. Further the directors also furnish a report

wherein all the necessary and the substantial information is given which ultimately is provided to

the shareholders and hence in this manner the directors become a relevant stakeholder (Tse, et al

2016).

Suppliers/ Creditors: the fundamental strategy of the Tesco is to treat the individuals the

manner in which they need to treat themselves, and it's something they apply solidly to give the

relationship another touch among the suppliers and the creditors of the organization. As per the

annual report it can be observed that the suppliers are considered on the second number while

analyzing the stakeholder theory of Tesco as they are the major element, which Tesco must

satisfy to. Further, the suppliers can take the strategic business decision only they will be fully

aware about the financial health; events and the important decision are taking place in the

business. The suppliers supply the material at the commercial level as well as to different

branches of it (Jenkins and Williamson, 2015).

Employees: Employees are the key members of the organization and it is very important to

understand their needs and preferences. The managers have the core responsibility of creating the

goals, atmosphere of the work among the workers of Tesco. There are different fields which a

and its stakeholders has been carried out to understand their needs and the preferences. The three

types of the stakeholders that have been analyzed below are the directors, suppliers, and the

management or say employees of the organization (Asay, Elliott and Rennekamp, 2016).

Directors: As per the stakeholders the directors possess the direct interest in the company and its

affair as they have taken a huge risk by investing in the business. From the analysis it can be

understood that the directors the key people in deciding most of the decisions of Tesco and

hence, their interest becomes imperative automatically. Further the directors also furnish a report

wherein all the necessary and the substantial information is given which ultimately is provided to

the shareholders and hence in this manner the directors become a relevant stakeholder (Tse, et al

2016).

Suppliers/ Creditors: the fundamental strategy of the Tesco is to treat the individuals the

manner in which they need to treat themselves, and it's something they apply solidly to give the

relationship another touch among the suppliers and the creditors of the organization. As per the

annual report it can be observed that the suppliers are considered on the second number while

analyzing the stakeholder theory of Tesco as they are the major element, which Tesco must

satisfy to. Further, the suppliers can take the strategic business decision only they will be fully

aware about the financial health; events and the important decision are taking place in the

business. The suppliers supply the material at the commercial level as well as to different

branches of it (Jenkins and Williamson, 2015).

Employees: Employees are the key members of the organization and it is very important to

understand their needs and preferences. The managers have the core responsibility of creating the

goals, atmosphere of the work among the workers of Tesco. There are different fields which a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial analysis 5

manger has to handle such as law, finance, marketing, sales and production and without them it

becomes impossible for the company to grow and sustain. Hence under the concept of the

stakeholders the next best stakeholder is employee (Sadler and Evans, 2016).

B)

Corporate Social Responsibility' is viewed as the future of all associations explicitly as well as

implicitly. Furthermore, the organizations must be increasingly dynamic on the classification of

'CSR' exercises and on how the steady usage in the retail association and in their dispersion

channels could be availed (Tesco, 2016). As per the Tesco's Environmental and Social Review

and the Corporate Governance Report, it is evident with regards to contribution being made and

it also defines the performance of the stakeholders on the grounds of responsibility. The two

stakeholders that have been analyzed in the detailed manner are the suppliers and the employees.

With the creditors and suppliers the general methodology of the organization is, it has

consistently been encouraging to utilize the dibble crop which is comprehensive of various

frames and figures. Besides this year the new yields have been presented and the new facility to

grow the crops is also available. This also helped in easing down the business to an extremely

high level by allowing the opportunity or say flexibility to order online (Karim, Suh, Carter and

Zhang, 2015).

Ratio Analysis

The ratios are the key determinants and they acts as a driver or a tool that can be used to analyze

the health of the companies in terms of the competitor or even against the industry benchmark.

The ratio investigation helps in making mindful decisions about the changes observed in the

organization. It basically satisfies the request of the users of the financial statements as they are

manger has to handle such as law, finance, marketing, sales and production and without them it

becomes impossible for the company to grow and sustain. Hence under the concept of the

stakeholders the next best stakeholder is employee (Sadler and Evans, 2016).

B)

Corporate Social Responsibility' is viewed as the future of all associations explicitly as well as

implicitly. Furthermore, the organizations must be increasingly dynamic on the classification of

'CSR' exercises and on how the steady usage in the retail association and in their dispersion

channels could be availed (Tesco, 2016). As per the Tesco's Environmental and Social Review

and the Corporate Governance Report, it is evident with regards to contribution being made and

it also defines the performance of the stakeholders on the grounds of responsibility. The two

stakeholders that have been analyzed in the detailed manner are the suppliers and the employees.

With the creditors and suppliers the general methodology of the organization is, it has

consistently been encouraging to utilize the dibble crop which is comprehensive of various

frames and figures. Besides this year the new yields have been presented and the new facility to

grow the crops is also available. This also helped in easing down the business to an extremely

high level by allowing the opportunity or say flexibility to order online (Karim, Suh, Carter and

Zhang, 2015).

Ratio Analysis

The ratios are the key determinants and they acts as a driver or a tool that can be used to analyze

the health of the companies in terms of the competitor or even against the industry benchmark.

The ratio investigation helps in making mindful decisions about the changes observed in the

organization. It basically satisfies the request of the users of the financial statements as they are

Financial analysis 6

keen to know the happenings of the company and moreover they are also helpful in deciding

whether to carry on the business terms with the organization or not. In this section the ratios of

the Benedict Company has been evaluated for the year 2000 and the year 2001. This will give an

insight to the changes that have taken place over the period of the last two years and the

necessary adjustments as well as strategies are also discussed to improve the position. The ratios

are generally assessed on the basis of the profitability, liquidity, efficiency, and solvency

(Williams and Dobelman, 2017).

Liquidity ratios

The primary proportion that will be chosen by the organization is in terms of the liquidity, which

is utilized to gauge the financial situation of the business as far as how fluid the organization can

move in order to meet its present commitments and the liabilities of the current nature. This is

also to check whether the organization will have adequate amount to compensation back the

present liabilities proficiently and viably. The liquidity proportions are additionally distributed

into the current ratio and the quick ratios (Robinson, et al 2015).

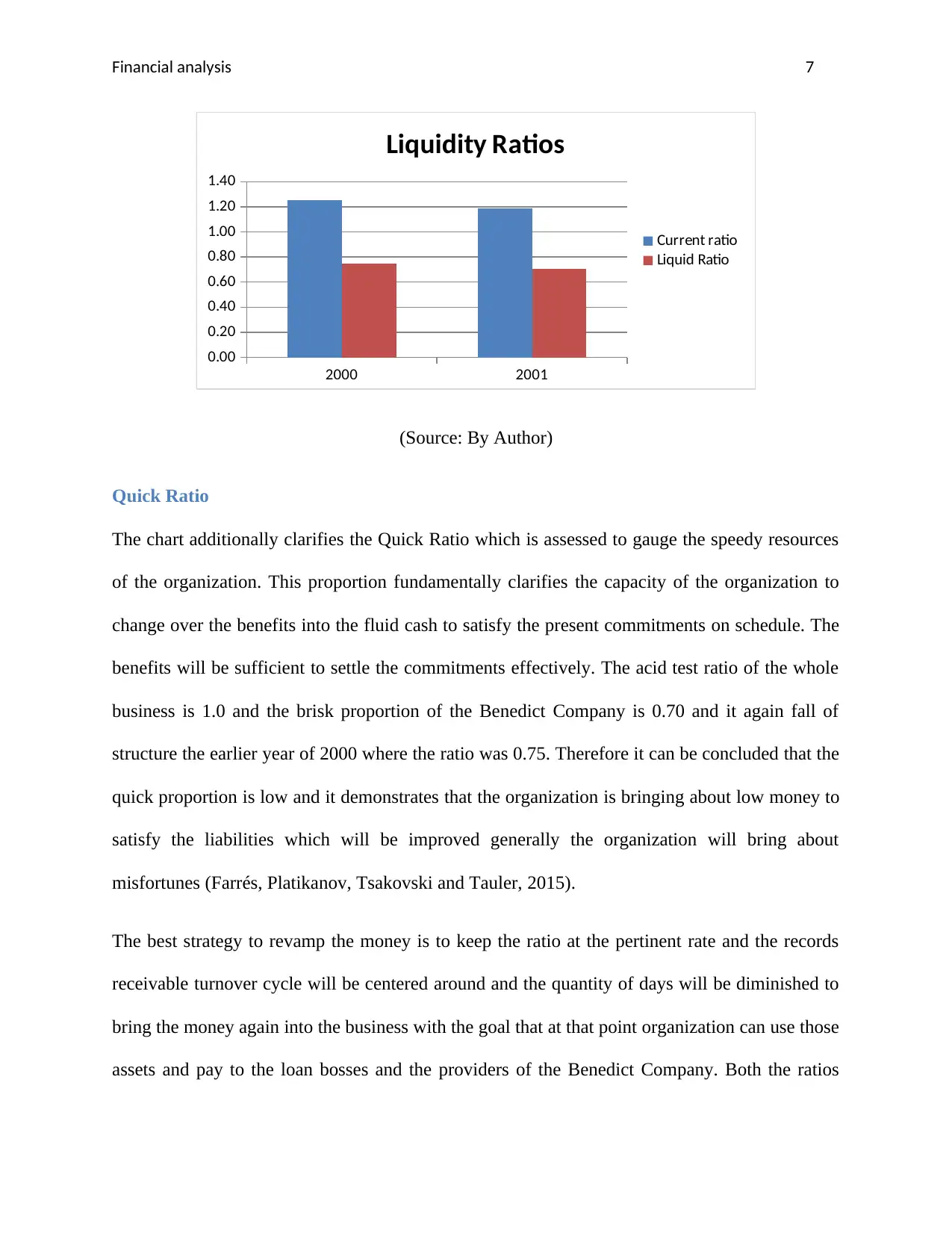

Current ratio

Current Ratio is the proportion which is determined to discover the capacity of the organization

to compensation its present liabilities on the basis of the existing resources. The present current

ratio of the company is 1.19 and it decreased in comparison to the previous year of 2000. When

the position is realized in terms of the industry benchmark it can be seen that the ratio is 1.60.

The company is nowhere close to this ratio whereas it declined in terms of the previous year.

This indicates that the company needs to buck up to settle the liabilities as soon as possible by

making use of the assets in the most judicious manner (Wen and Zhu, 2019).

keen to know the happenings of the company and moreover they are also helpful in deciding

whether to carry on the business terms with the organization or not. In this section the ratios of

the Benedict Company has been evaluated for the year 2000 and the year 2001. This will give an

insight to the changes that have taken place over the period of the last two years and the

necessary adjustments as well as strategies are also discussed to improve the position. The ratios

are generally assessed on the basis of the profitability, liquidity, efficiency, and solvency

(Williams and Dobelman, 2017).

Liquidity ratios

The primary proportion that will be chosen by the organization is in terms of the liquidity, which

is utilized to gauge the financial situation of the business as far as how fluid the organization can

move in order to meet its present commitments and the liabilities of the current nature. This is

also to check whether the organization will have adequate amount to compensation back the

present liabilities proficiently and viably. The liquidity proportions are additionally distributed

into the current ratio and the quick ratios (Robinson, et al 2015).

Current ratio

Current Ratio is the proportion which is determined to discover the capacity of the organization

to compensation its present liabilities on the basis of the existing resources. The present current

ratio of the company is 1.19 and it decreased in comparison to the previous year of 2000. When

the position is realized in terms of the industry benchmark it can be seen that the ratio is 1.60.

The company is nowhere close to this ratio whereas it declined in terms of the previous year.

This indicates that the company needs to buck up to settle the liabilities as soon as possible by

making use of the assets in the most judicious manner (Wen and Zhu, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial analysis 7

2000 2001

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Liquidity Ratios

Current ratio

Liquid Ratio

(Source: By Author)

Quick Ratio

The chart additionally clarifies the Quick Ratio which is assessed to gauge the speedy resources

of the organization. This proportion fundamentally clarifies the capacity of the organization to

change over the benefits into the fluid cash to satisfy the present commitments on schedule. The

benefits will be sufficient to settle the commitments effectively. The acid test ratio of the whole

business is 1.0 and the brisk proportion of the Benedict Company is 0.70 and it again fall of

structure the earlier year of 2000 where the ratio was 0.75. Therefore it can be concluded that the

quick proportion is low and it demonstrates that the organization is bringing about low money to

satisfy the liabilities which will be improved generally the organization will bring about

misfortunes (Farrés, Platikanov, Tsakovski and Tauler, 2015).

The best strategy to revamp the money is to keep the ratio at the pertinent rate and the records

receivable turnover cycle will be centered around and the quantity of days will be diminished to

bring the money again into the business with the goal that at that point organization can use those

assets and pay to the loan bosses and the providers of the Benedict Company. Both the ratios

2000 2001

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Liquidity Ratios

Current ratio

Liquid Ratio

(Source: By Author)

Quick Ratio

The chart additionally clarifies the Quick Ratio which is assessed to gauge the speedy resources

of the organization. This proportion fundamentally clarifies the capacity of the organization to

change over the benefits into the fluid cash to satisfy the present commitments on schedule. The

benefits will be sufficient to settle the commitments effectively. The acid test ratio of the whole

business is 1.0 and the brisk proportion of the Benedict Company is 0.70 and it again fall of

structure the earlier year of 2000 where the ratio was 0.75. Therefore it can be concluded that the

quick proportion is low and it demonstrates that the organization is bringing about low money to

satisfy the liabilities which will be improved generally the organization will bring about

misfortunes (Farrés, Platikanov, Tsakovski and Tauler, 2015).

The best strategy to revamp the money is to keep the ratio at the pertinent rate and the records

receivable turnover cycle will be centered around and the quantity of days will be diminished to

bring the money again into the business with the goal that at that point organization can use those

assets and pay to the loan bosses and the providers of the Benedict Company. Both the ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial analysis 8

hold equal importance and are required to be attended on the emergency basis to save the future

performance of the business (Kajananthan and Velnampy, 2018).

Profitability ratios

The ratios of the profitability of the organization are the ones that are determined to decide if the

organization is working productively or not. The profits are additionally significant structure the

perspective of the speculators and the investors as the greater part of the income are the key

drivers for the investors. The productivity is the most significant factor regarding the entomb

also intra organization examination with the goal that it gives the plan to the administration about

whether the organization will improve the presentation of the organization, or whether it is

working great or not or experiencing misfortunes that should be recouped. There are four

parameters on the basis of which the profitability is measured such as gross profit, net profit,

return on equity and the return on assets .

Gross Profit

Profitability ratios 2000 2001

Gross Profit Gross profit 42% 48%

Sales

Net Profit Net Proift 28% 21%

Sales

Return on Assets Net Profit 17.95% 12.99%

Total Assets

Return on Equity Net Profit 27.03% 23.57%

Total Equity

hold equal importance and are required to be attended on the emergency basis to save the future

performance of the business (Kajananthan and Velnampy, 2018).

Profitability ratios

The ratios of the profitability of the organization are the ones that are determined to decide if the

organization is working productively or not. The profits are additionally significant structure the

perspective of the speculators and the investors as the greater part of the income are the key

drivers for the investors. The productivity is the most significant factor regarding the entomb

also intra organization examination with the goal that it gives the plan to the administration about

whether the organization will improve the presentation of the organization, or whether it is

working great or not or experiencing misfortunes that should be recouped. There are four

parameters on the basis of which the profitability is measured such as gross profit, net profit,

return on equity and the return on assets .

Gross Profit

Profitability ratios 2000 2001

Gross Profit Gross profit 42% 48%

Sales

Net Profit Net Proift 28% 21%

Sales

Return on Assets Net Profit 17.95% 12.99%

Total Assets

Return on Equity Net Profit 27.03% 23.57%

Total Equity

Financial analysis 9

From the above table it very well may be seen that the gross benefit of the organization is 48% in

the year 2001 and same has been expanded from the earlier year where the gross net revenue was

at 42%. The proportion has been expanded which in this way mirrors the way that organization is

diminishing the expense of products sold and the other working direct expenses to make a large

portion of the income.

As far as the business ratio the productivity proportion of the Benedict Company is better. The

general business is working at 43% and the organization is working at 48%. In spite of the fact

that there is certainly not a noteworthy distinction yet the organization can improve the

presentation by assembling the items itself and reducing the cost of goods to an acceptably low

level.

Return on Assets

The return on assets can be assessed by the table above which demonstrates that there is a great

fall from 17.95% to 12.99%. This shows the organization isn't using its assets well and this is a

reason for concern which should be viewed by the administration of the benedict organization.

As far as the business the proportion is 14.26%, covering generally organizations, the

circumstance mirrors different organizations have shown an increase in their performance and

the way and it's a risk to the Benedict Company (Wolski and Bolek, 2016).

Net Profit

The net benefit proportion is the proportion determined in the wake of deducting the enthusiasm

just as the duty cost to get the general circumstance of the organization. The net benefit

proportion of the benedict organization is 21% in the present year in contrast with the earlier year

which was 28%. The business is additionally working at 25%, in this manner the organization

From the above table it very well may be seen that the gross benefit of the organization is 48% in

the year 2001 and same has been expanded from the earlier year where the gross net revenue was

at 42%. The proportion has been expanded which in this way mirrors the way that organization is

diminishing the expense of products sold and the other working direct expenses to make a large

portion of the income.

As far as the business ratio the productivity proportion of the Benedict Company is better. The

general business is working at 43% and the organization is working at 48%. In spite of the fact

that there is certainly not a noteworthy distinction yet the organization can improve the

presentation by assembling the items itself and reducing the cost of goods to an acceptably low

level.

Return on Assets

The return on assets can be assessed by the table above which demonstrates that there is a great

fall from 17.95% to 12.99%. This shows the organization isn't using its assets well and this is a

reason for concern which should be viewed by the administration of the benedict organization.

As far as the business the proportion is 14.26%, covering generally organizations, the

circumstance mirrors different organizations have shown an increase in their performance and

the way and it's a risk to the Benedict Company (Wolski and Bolek, 2016).

Net Profit

The net benefit proportion is the proportion determined in the wake of deducting the enthusiasm

just as the duty cost to get the general circumstance of the organization. The net benefit

proportion of the benedict organization is 21% in the present year in contrast with the earlier year

which was 28%. The business is additionally working at 25%, in this manner the organization

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial analysis 10

can build the net benefit proportion as there isn't much hole between the earlier year execution

and the business hole.

Return on Equity

Profit for Equity is an extent which is resolved to check the budgetary execution of the business

and the firms in general. Such proportion is determined with a desire to measure the limit of the

business to make profits by the endeavors made by the budgetary specialists of the association

(Wolski and Bolek, 2016).

The return on Equity anyway tumbled down from 27.03 to 23.57% structure the year 2000 to

year 2001. A rising ROE proposes that the organization is expanding the capacity to create the

benefit despite having the requirement of the capital assets through and the diminishing value is

the other way around case. Regarding the business the arrival on value is 38.58% and the

organization is 11% behind this proportion. This recommends the circumstance can in any case

be improved and has not come to the dreadful situation yet (Kumar and Bakshi, 2018).

Solvency Ratios

Solvency ratio is one of the parameter that is used by the company in order to gain knowledge an

understanding of how the company is operating at the solvency foot front. The solvency term is

crucial from the point of view of the business as it indicates the amount that has been financed in

the different forms such as debt and equity. The debt to Equity ratio, the debt to total assets is

the major ratios that have been analyzed below.

Debt to Equity ratio

The real reason for this proportion is to compute the money related influence of the organization.

In the event that the measure of obligation utilized by the organization is more to fund the

can build the net benefit proportion as there isn't much hole between the earlier year execution

and the business hole.

Return on Equity

Profit for Equity is an extent which is resolved to check the budgetary execution of the business

and the firms in general. Such proportion is determined with a desire to measure the limit of the

business to make profits by the endeavors made by the budgetary specialists of the association

(Wolski and Bolek, 2016).

The return on Equity anyway tumbled down from 27.03 to 23.57% structure the year 2000 to

year 2001. A rising ROE proposes that the organization is expanding the capacity to create the

benefit despite having the requirement of the capital assets through and the diminishing value is

the other way around case. Regarding the business the arrival on value is 38.58% and the

organization is 11% behind this proportion. This recommends the circumstance can in any case

be improved and has not come to the dreadful situation yet (Kumar and Bakshi, 2018).

Solvency Ratios

Solvency ratio is one of the parameter that is used by the company in order to gain knowledge an

understanding of how the company is operating at the solvency foot front. The solvency term is

crucial from the point of view of the business as it indicates the amount that has been financed in

the different forms such as debt and equity. The debt to Equity ratio, the debt to total assets is

the major ratios that have been analyzed below.

Debt to Equity ratio

The real reason for this proportion is to compute the money related influence of the organization.

In the event that the measure of obligation utilized by the organization is more to fund the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial analysis 11

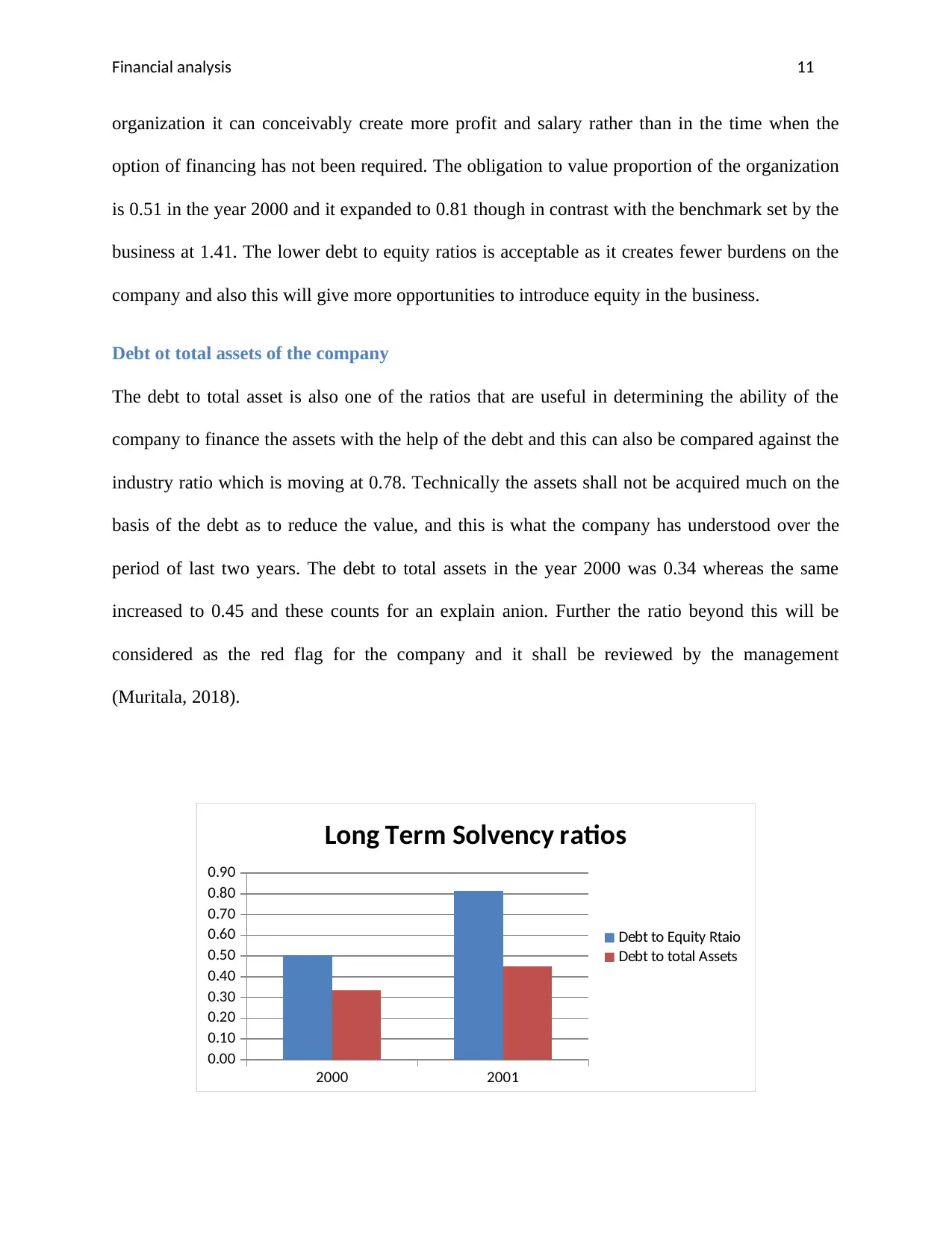

organization it can conceivably create more profit and salary rather than in the time when the

option of financing has not been required. The obligation to value proportion of the organization

is 0.51 in the year 2000 and it expanded to 0.81 though in contrast with the benchmark set by the

business at 1.41. The lower debt to equity ratios is acceptable as it creates fewer burdens on the

company and also this will give more opportunities to introduce equity in the business.

Debt ot total assets of the company

The debt to total asset is also one of the ratios that are useful in determining the ability of the

company to finance the assets with the help of the debt and this can also be compared against the

industry ratio which is moving at 0.78. Technically the assets shall not be acquired much on the

basis of the debt as to reduce the value, and this is what the company has understood over the

period of last two years. The debt to total assets in the year 2000 was 0.34 whereas the same

increased to 0.45 and these counts for an explain anion. Further the ratio beyond this will be

considered as the red flag for the company and it shall be reviewed by the management

(Muritala, 2018).

2000 2001

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Long Term Solvency ratios

Debt to Equity Rtaio

Debt to total Assets

organization it can conceivably create more profit and salary rather than in the time when the

option of financing has not been required. The obligation to value proportion of the organization

is 0.51 in the year 2000 and it expanded to 0.81 though in contrast with the benchmark set by the

business at 1.41. The lower debt to equity ratios is acceptable as it creates fewer burdens on the

company and also this will give more opportunities to introduce equity in the business.

Debt ot total assets of the company

The debt to total asset is also one of the ratios that are useful in determining the ability of the

company to finance the assets with the help of the debt and this can also be compared against the

industry ratio which is moving at 0.78. Technically the assets shall not be acquired much on the

basis of the debt as to reduce the value, and this is what the company has understood over the

period of last two years. The debt to total assets in the year 2000 was 0.34 whereas the same

increased to 0.45 and these counts for an explain anion. Further the ratio beyond this will be

considered as the red flag for the company and it shall be reviewed by the management

(Muritala, 2018).

2000 2001

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Long Term Solvency ratios

Debt to Equity Rtaio

Debt to total Assets

Financial analysis 12

(Source: By Author)

Efficiency Ratios

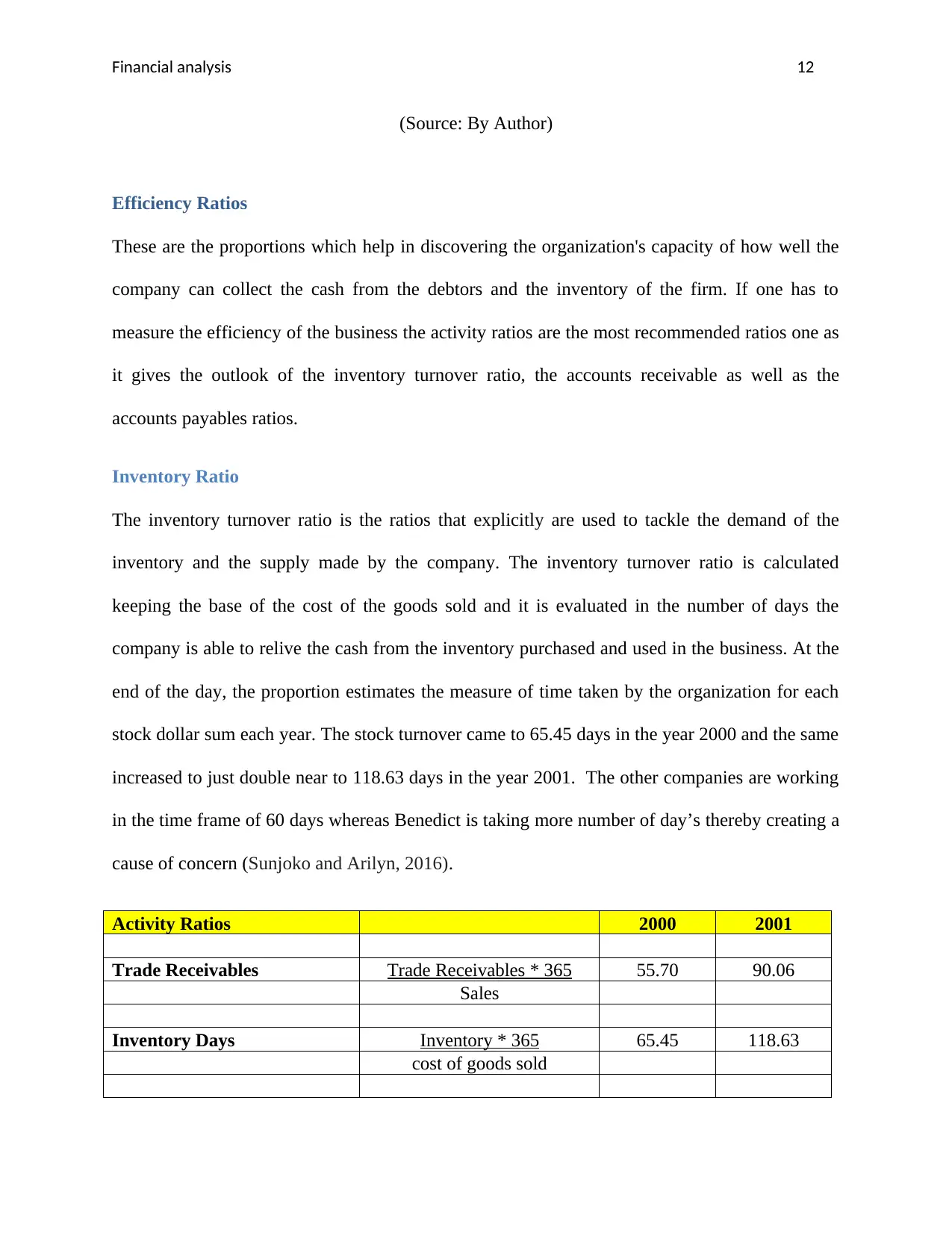

These are the proportions which help in discovering the organization's capacity of how well the

company can collect the cash from the debtors and the inventory of the firm. If one has to

measure the efficiency of the business the activity ratios are the most recommended ratios one as

it gives the outlook of the inventory turnover ratio, the accounts receivable as well as the

accounts payables ratios.

Inventory Ratio

The inventory turnover ratio is the ratios that explicitly are used to tackle the demand of the

inventory and the supply made by the company. The inventory turnover ratio is calculated

keeping the base of the cost of the goods sold and it is evaluated in the number of days the

company is able to relive the cash from the inventory purchased and used in the business. At the

end of the day, the proportion estimates the measure of time taken by the organization for each

stock dollar sum each year. The stock turnover came to 65.45 days in the year 2000 and the same

increased to just double near to 118.63 days in the year 2001. The other companies are working

in the time frame of 60 days whereas Benedict is taking more number of day’s thereby creating a

cause of concern (Sunjoko and Arilyn, 2016).

Activity Ratios 2000 2001

Trade Receivables Trade Receivables * 365 55.70 90.06

Sales

Inventory Days Inventory * 365 65.45 118.63

cost of goods sold

(Source: By Author)

Efficiency Ratios

These are the proportions which help in discovering the organization's capacity of how well the

company can collect the cash from the debtors and the inventory of the firm. If one has to

measure the efficiency of the business the activity ratios are the most recommended ratios one as

it gives the outlook of the inventory turnover ratio, the accounts receivable as well as the

accounts payables ratios.

Inventory Ratio

The inventory turnover ratio is the ratios that explicitly are used to tackle the demand of the

inventory and the supply made by the company. The inventory turnover ratio is calculated

keeping the base of the cost of the goods sold and it is evaluated in the number of days the

company is able to relive the cash from the inventory purchased and used in the business. At the

end of the day, the proportion estimates the measure of time taken by the organization for each

stock dollar sum each year. The stock turnover came to 65.45 days in the year 2000 and the same

increased to just double near to 118.63 days in the year 2001. The other companies are working

in the time frame of 60 days whereas Benedict is taking more number of day’s thereby creating a

cause of concern (Sunjoko and Arilyn, 2016).

Activity Ratios 2000 2001

Trade Receivables Trade Receivables * 365 55.70 90.06

Sales

Inventory Days Inventory * 365 65.45 118.63

cost of goods sold

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.