International Finance: Tesco Company Financial Analysis Report

VerifiedAdded on 2020/01/21

|10

|3272

|292

Report

AI Summary

This report provides a comprehensive financial analysis of Tesco, a leading global company. It begins with an introduction to international finance and its relevance to business valuation. The report then delves into ratio analysis, including gross profit ratio, net profit ratio, current ratio, quick ratio, debt-equity ratio, return on equity, and price-earnings ratio, providing a detailed assessment of Tesco's financial health. Furthermore, the report explores three valuation methods: net asset basis, price-earnings ratio, and dividend valuation, comparing their advantages, disadvantages, and results. It also examines the risk factors faced by Tesco and the impact of market situations on the choice of valuation methods. Finally, the report offers a recommendation regarding acquisition based on the financial analysis, followed by a conclusion and references.

INTERNATIONAL FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Ratio analysis...............................................................................................................................3

TASK 2............................................................................................................................................6

(a) Advantages and disadvantages of three valuation methods...................................................6

(b) Valuation of shares.................................................................................................................7

© Reasons due to which valuation methods generate different results.......................................7

(d) Risk faced by the FTSE 100 Company Tesco in its business................................................8

(e) Impact of situation on the choice of valuation method in this case.......................................8

TASK 3............................................................................................................................................8

(a) Recommendation in relation to acquisition............................................................................8

CONCLUSION................................................................................................................................9

REFERNECES..............................................................................................................................10

Table 1Ratio analysis of the Tesco..................................................................................................3

Table 2 Shares valuation for Tesco.................................................................................................7

Table 3 Valuation on the basis of Price earnings ratio....................................................................7

Table 4 Valuation on the basis of dividend growth model..............................................................7

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Ratio analysis...............................................................................................................................3

TASK 2............................................................................................................................................6

(a) Advantages and disadvantages of three valuation methods...................................................6

(b) Valuation of shares.................................................................................................................7

© Reasons due to which valuation methods generate different results.......................................7

(d) Risk faced by the FTSE 100 Company Tesco in its business................................................8

(e) Impact of situation on the choice of valuation method in this case.......................................8

TASK 3............................................................................................................................................8

(a) Recommendation in relation to acquisition............................................................................8

CONCLUSION................................................................................................................................9

REFERNECES..............................................................................................................................10

Table 1Ratio analysis of the Tesco..................................................................................................3

Table 2 Shares valuation for Tesco.................................................................................................7

Table 3 Valuation on the basis of Price earnings ratio....................................................................7

Table 4 Valuation on the basis of dividend growth model..............................................................7

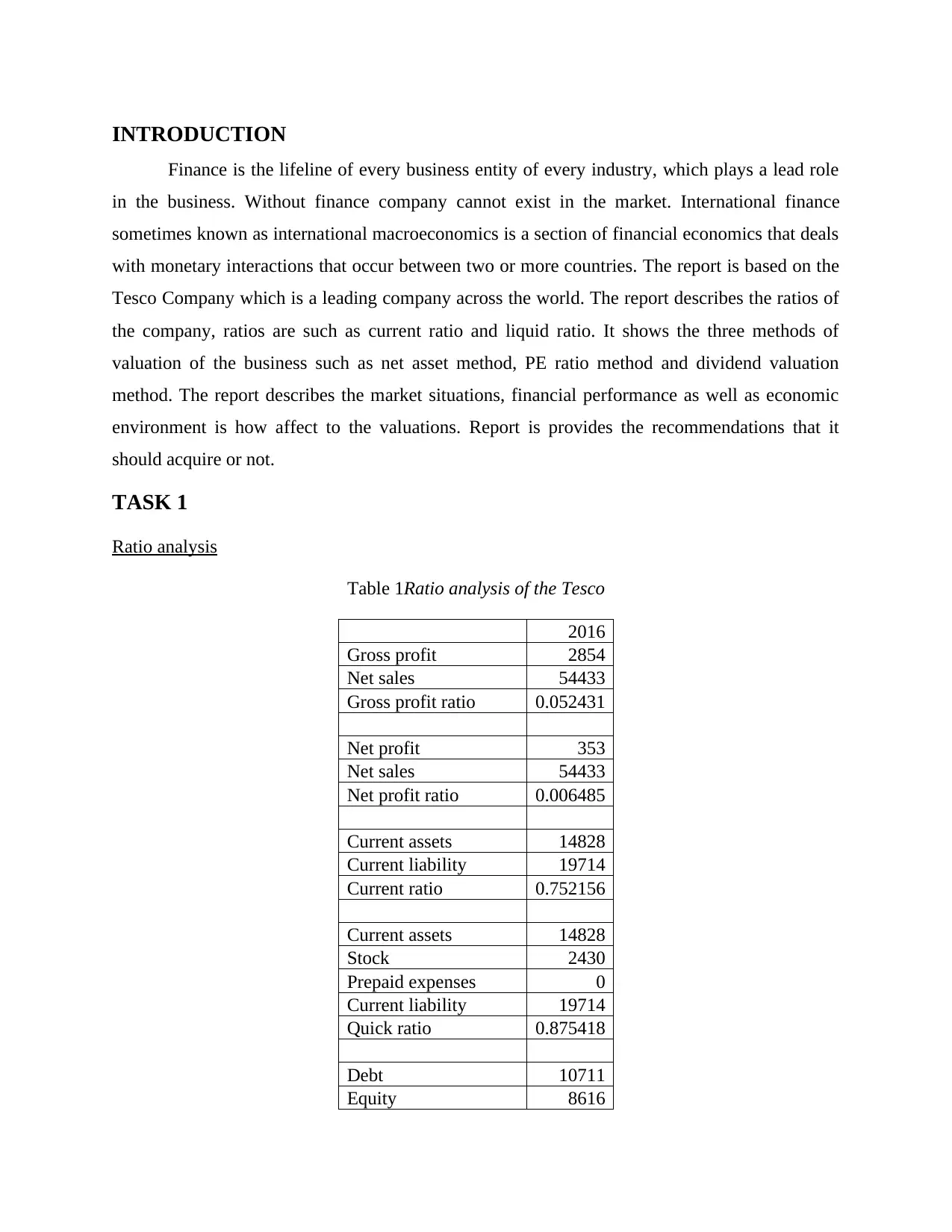

INTRODUCTION

Finance is the lifeline of every business entity of every industry, which plays a lead role

in the business. Without finance company cannot exist in the market. International finance

sometimes known as international macroeconomics is a section of financial economics that deals

with monetary interactions that occur between two or more countries. The report is based on the

Tesco Company which is a leading company across the world. The report describes the ratios of

the company, ratios are such as current ratio and liquid ratio. It shows the three methods of

valuation of the business such as net asset method, PE ratio method and dividend valuation

method. The report describes the market situations, financial performance as well as economic

environment is how affect to the valuations. Report is provides the recommendations that it

should acquire or not.

TASK 1

Ratio analysis

Table 1Ratio analysis of the Tesco

2016

Gross profit 2854

Net sales 54433

Gross profit ratio 0.052431

Net profit 353

Net sales 54433

Net profit ratio 0.006485

Current assets 14828

Current liability 19714

Current ratio 0.752156

Current assets 14828

Stock 2430

Prepaid expenses 0

Current liability 19714

Quick ratio 0.875418

Debt 10711

Equity 8616

Finance is the lifeline of every business entity of every industry, which plays a lead role

in the business. Without finance company cannot exist in the market. International finance

sometimes known as international macroeconomics is a section of financial economics that deals

with monetary interactions that occur between two or more countries. The report is based on the

Tesco Company which is a leading company across the world. The report describes the ratios of

the company, ratios are such as current ratio and liquid ratio. It shows the three methods of

valuation of the business such as net asset method, PE ratio method and dividend valuation

method. The report describes the market situations, financial performance as well as economic

environment is how affect to the valuations. Report is provides the recommendations that it

should acquire or not.

TASK 1

Ratio analysis

Table 1Ratio analysis of the Tesco

2016

Gross profit 2854

Net sales 54433

Gross profit ratio 0.052431

Net profit 353

Net sales 54433

Net profit ratio 0.006485

Current assets 14828

Current liability 19714

Current ratio 0.752156

Current assets 14828

Stock 2430

Prepaid expenses 0

Current liability 19714

Quick ratio 0.875418

Debt 10711

Equity 8616

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Debt equity ratio 1.243152

Net profit 353

Equity 8616

ROE 0.04097

Price 214

EPS 0.05

Price earnings ratio 4280

Gross profit ratio: It is the ratio which is used by the business firms to measure the firm

business performance. Cost is the one of the most important factor that greatly influence the

profitability and growth of the business firms. Gross profit ratio help business firms in

computing the portion of sales that is encompassed by the gross profit. Higher is the gross

profit ratio of the firm more company is better condition (Garcia and Tsafack, 2011). This is

because such kind of performance on the ratio indicate that firm have a stiff control on its

direct expenses. It can be seen from the table that gross profit ratio of Tesco is 0.05 which is

5% and is very low in the business. On this basis it can be said that firm performance is very

poor and it have very loose control on its direct expenses.

Net profit ratio: Net profit ratio is the one of the most important ratio which is used by the

managers to measure firm’s business performance. Performance on the ratio reflect the firm

capacity to control indirect expenses in the business. Business firms must try to ensure that

there net profit ratio is increasing consistently. It can be observed from the table given above

that net profit ratio of Tesco is 0.06 which is 6%. It is clear that firm is earning very low

profit margin in its business. This reflects that firm have less control on its indirect expenses.

On analysis of gross and net profit ratio of the firm it can be said that company expenses

control policy is very weak and this is the area in which it needs to work in order to improve

its performance.

Current ratio: This is the ratio which help managers in ascertaining and evaluating the

liquidity position of the firm (Houston, Lin and Ma, 2012). It is very important to ensure that

there is high liquidity in the business. This is because high liquidity reflects that there is

greater amount of money in the firm business. It can be observed from the table that current

ratio of Tesco is 0.77 which is below standard value of the ratio 2. It can be said that for

every one GBP of current liability firm must have two GBP in its business. In case of Tesco

Net profit 353

Equity 8616

ROE 0.04097

Price 214

EPS 0.05

Price earnings ratio 4280

Gross profit ratio: It is the ratio which is used by the business firms to measure the firm

business performance. Cost is the one of the most important factor that greatly influence the

profitability and growth of the business firms. Gross profit ratio help business firms in

computing the portion of sales that is encompassed by the gross profit. Higher is the gross

profit ratio of the firm more company is better condition (Garcia and Tsafack, 2011). This is

because such kind of performance on the ratio indicate that firm have a stiff control on its

direct expenses. It can be seen from the table that gross profit ratio of Tesco is 0.05 which is

5% and is very low in the business. On this basis it can be said that firm performance is very

poor and it have very loose control on its direct expenses.

Net profit ratio: Net profit ratio is the one of the most important ratio which is used by the

managers to measure firm’s business performance. Performance on the ratio reflect the firm

capacity to control indirect expenses in the business. Business firms must try to ensure that

there net profit ratio is increasing consistently. It can be observed from the table given above

that net profit ratio of Tesco is 0.06 which is 6%. It is clear that firm is earning very low

profit margin in its business. This reflects that firm have less control on its indirect expenses.

On analysis of gross and net profit ratio of the firm it can be said that company expenses

control policy is very weak and this is the area in which it needs to work in order to improve

its performance.

Current ratio: This is the ratio which help managers in ascertaining and evaluating the

liquidity position of the firm (Houston, Lin and Ma, 2012). It is very important to ensure that

there is high liquidity in the business. This is because high liquidity reflects that there is

greater amount of money in the firm business. It can be observed from the table that current

ratio of Tesco is 0.77 which is below standard value of the ratio 2. It can be said that for

every one GBP of current liability firm must have two GBP in its business. In case of Tesco

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

current ratio is 0.77 which is below standard value 2. Even value of ratio is less than 1 and it

reflects that firm is not capable to pay its current liability on time by using current assets.

Quick ratio: Quick ratio is also one of the most important ratio that help firm in measuring

liquidity in the business. This ratio give clearer picture of the firm liquidity then current ratio.

This is because it is the ratio which is interpreted above stock and prepaid expenses are

included. Stock is the one of the most important asset of the business firm. The main feature

of this asset is that it takes time to get converted in to cash in the business (Kresta and Tichy,

2012). Hence, it can be said that quick ratio does not give better overview of the liquidity to

the business firm. It can be observed from the table that quick ratio of the firm is 0.87 which

is nearby to 1. On this basis it can be said that firm liquidity position is good and to great

extent but not completely it can pay current liability by using current assets in the business.

Hence, on this ratio Tesco give good performance.

Debt equity ratio: It is one of the most important ratio because it reflect the capital structure

of the firm. It is the capital structure which determine the business cost of capital. Firms must

ensure that capital structure of the business is balanced. Capital structure in the business must

not be covered mostly by debt or equity (Eichengreen and Flandreau, 2012). Capital structure

must be balanced because by doing so cost of capital can be minimized in the business. It can

be observed that debt equity ratio of the Tesco is 1.24. This means that for everyone unit of

the GBP of equity there is 1.24 unit of debt. It is clear that capital structure of the firm is

mainly covered by the debt. However, this coverage is not so high. On this basis it can be

said that there is high debt in the firm business and it needs to control same.

Return on equity: Return on equity is the one of the main ratio that is used to measure the

firm business performance in terms of return it give to its shareholders. It can be observed

from the return on equity ratio that return on equity is 0.04 or 4% which is very low. On this

basis it can be said that firm is giving less return to its shareholders which is not good in the

business.

Price earnings ratio: Price earnings ratio help firm in doing valuation of the shares. By using

this ratio it can be identified that firm shares are undervalued or overvalued (Frankel and

Poonawala, 2010). In order to do valuation of the firm share industry PE ratio is required. By

comparison company and industry PE ratio it is identified whether shares are undervalued or

overvalued. On analysis of firm PE ratio it can be said that its shares are overvalued. This is

reflects that firm is not capable to pay its current liability on time by using current assets.

Quick ratio: Quick ratio is also one of the most important ratio that help firm in measuring

liquidity in the business. This ratio give clearer picture of the firm liquidity then current ratio.

This is because it is the ratio which is interpreted above stock and prepaid expenses are

included. Stock is the one of the most important asset of the business firm. The main feature

of this asset is that it takes time to get converted in to cash in the business (Kresta and Tichy,

2012). Hence, it can be said that quick ratio does not give better overview of the liquidity to

the business firm. It can be observed from the table that quick ratio of the firm is 0.87 which

is nearby to 1. On this basis it can be said that firm liquidity position is good and to great

extent but not completely it can pay current liability by using current assets in the business.

Hence, on this ratio Tesco give good performance.

Debt equity ratio: It is one of the most important ratio because it reflect the capital structure

of the firm. It is the capital structure which determine the business cost of capital. Firms must

ensure that capital structure of the business is balanced. Capital structure in the business must

not be covered mostly by debt or equity (Eichengreen and Flandreau, 2012). Capital structure

must be balanced because by doing so cost of capital can be minimized in the business. It can

be observed that debt equity ratio of the Tesco is 1.24. This means that for everyone unit of

the GBP of equity there is 1.24 unit of debt. It is clear that capital structure of the firm is

mainly covered by the debt. However, this coverage is not so high. On this basis it can be

said that there is high debt in the firm business and it needs to control same.

Return on equity: Return on equity is the one of the main ratio that is used to measure the

firm business performance in terms of return it give to its shareholders. It can be observed

from the return on equity ratio that return on equity is 0.04 or 4% which is very low. On this

basis it can be said that firm is giving less return to its shareholders which is not good in the

business.

Price earnings ratio: Price earnings ratio help firm in doing valuation of the shares. By using

this ratio it can be identified that firm shares are undervalued or overvalued (Frankel and

Poonawala, 2010). In order to do valuation of the firm share industry PE ratio is required. By

comparison company and industry PE ratio it is identified whether shares are undervalued or

overvalued. On analysis of firm PE ratio it can be said that its shares are overvalued. This is

because PE ratio value is very high. It can be said that investors are paying more amount then

required to purchase shares of the Tesco.

On analysis of figures it can be said that Tesco must nor acquire other FTSE 100

company. This is because its condition is not good. There is very low profit in the business.

Liquidity position is very poor in the business. Moreover, firm is not able to give good return to

its investors. If firm failed to earn profit in the newly acquired company then it will face huge

loss in its business. Thus, it is assumed that Tesco must not try to acquire small FTSE 100

Company.

TASK 2

(a) Advantages and disadvantages of three valuation methods

There are various types of method that can be used to do valuation of the shares. Some

specific methods that are used to do valuation of shares are given below. Net assets basis: It is the method under which liabilities are deducted from the assets and

output value is divided by the number of shares that are issued by the firm in the market.

There are number of advantages and disadvantages of this method (Gilpin, 2011). The main

merit of this method is that data that is required for valuation can be easily obtained by the

business firm or equity research analysts. Moreover, it does not consider market data to do

valuation of shares. The main demerit of this method is that intangible assets like goodwill

are not used in doing valuation of shares of the firm. Hence, it can be said that this method

have both merits and demerits. Price earnings ratio: This is the method of valuation that is used by all sort of investors and

research analysts. The main merit of this approach is that in this shares are overvalued or

undervalued is determined by comparing PE ratio with standards. The main demerit of this

method is that in this approach share price is taken in to account which keeps on changing

consistently (Hunter, Kaufman and Krueger, 2012). Hence, everyday PE ratio keeps on

changing consistently. It is very difficult to take investment decisions solely on the basis of

PE ratio. Dividend valuation basis: This is the method in which prediction is made about the dividend

and its present value is computed by using discount factor. Gordon growth dividend model is

used in the present report to do valuation of shares. The main advantage of this method is that

required to purchase shares of the Tesco.

On analysis of figures it can be said that Tesco must nor acquire other FTSE 100

company. This is because its condition is not good. There is very low profit in the business.

Liquidity position is very poor in the business. Moreover, firm is not able to give good return to

its investors. If firm failed to earn profit in the newly acquired company then it will face huge

loss in its business. Thus, it is assumed that Tesco must not try to acquire small FTSE 100

Company.

TASK 2

(a) Advantages and disadvantages of three valuation methods

There are various types of method that can be used to do valuation of the shares. Some

specific methods that are used to do valuation of shares are given below. Net assets basis: It is the method under which liabilities are deducted from the assets and

output value is divided by the number of shares that are issued by the firm in the market.

There are number of advantages and disadvantages of this method (Gilpin, 2011). The main

merit of this method is that data that is required for valuation can be easily obtained by the

business firm or equity research analysts. Moreover, it does not consider market data to do

valuation of shares. The main demerit of this method is that intangible assets like goodwill

are not used in doing valuation of shares of the firm. Hence, it can be said that this method

have both merits and demerits. Price earnings ratio: This is the method of valuation that is used by all sort of investors and

research analysts. The main merit of this approach is that in this shares are overvalued or

undervalued is determined by comparing PE ratio with standards. The main demerit of this

method is that in this approach share price is taken in to account which keeps on changing

consistently (Hunter, Kaufman and Krueger, 2012). Hence, everyday PE ratio keeps on

changing consistently. It is very difficult to take investment decisions solely on the basis of

PE ratio. Dividend valuation basis: This is the method in which prediction is made about the dividend

and its present value is computed by using discount factor. Gordon growth dividend model is

used in the present report to do valuation of shares. The main advantage of this method is that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

it is easy to apply this approach for doing valuation of shares. The demerit of this method is

that apart from dividend it does not taken in to account any factor to do valuation of shares.

(b) Valuation of shares

Table 2 Shares valuation for Tesco

Assets 43904

Liability 35288

Net assets 8616

Outstanding shares 2714

NAV 3.17465

Interpretation

It is clear from the table that on the basis of net asset value method real price of the Tesco

share is 3.17GBP. Hence, it can be said that Tesco shares are not fairly valued in the market.

Table 3 Valuation on the basis of Price earnings ratio

Price 214

EPS 0.05

Price earnings ratio 4280

Interpretation

Price earnings ratio of Tesco is higher than same of the industry. On this basis it can be

said that firm shares are overvalued.

Table 4 Valuation on the basis of dividend growth model

Next year dividend 0.35

MPS 214

G 2.00%

Dividend Value D1/P0+G 0.02163551

Interpretation

On the basis of dividend growth model it can be said that actual value of the firm shares

is 0.021 GBP. Hence, it can be said that on the basis of these valuation methods Tesco shares are

valued in proper way.

© Reasons due to which valuation methods generate different results

Each valuation method give different value of the shares. This is because in all valuation

methods different items are taken in to consideration (Devereux and Yetman, 2010). Hence, it is

not possible to obtain similar results from all valuation methods. In PE ratio market data is taken

that apart from dividend it does not taken in to account any factor to do valuation of shares.

(b) Valuation of shares

Table 2 Shares valuation for Tesco

Assets 43904

Liability 35288

Net assets 8616

Outstanding shares 2714

NAV 3.17465

Interpretation

It is clear from the table that on the basis of net asset value method real price of the Tesco

share is 3.17GBP. Hence, it can be said that Tesco shares are not fairly valued in the market.

Table 3 Valuation on the basis of Price earnings ratio

Price 214

EPS 0.05

Price earnings ratio 4280

Interpretation

Price earnings ratio of Tesco is higher than same of the industry. On this basis it can be

said that firm shares are overvalued.

Table 4 Valuation on the basis of dividend growth model

Next year dividend 0.35

MPS 214

G 2.00%

Dividend Value D1/P0+G 0.02163551

Interpretation

On the basis of dividend growth model it can be said that actual value of the firm shares

is 0.021 GBP. Hence, it can be said that on the basis of these valuation methods Tesco shares are

valued in proper way.

© Reasons due to which valuation methods generate different results

Each valuation method give different value of the shares. This is because in all valuation

methods different items are taken in to consideration (Devereux and Yetman, 2010). Hence, it is

not possible to obtain similar results from all valuation methods. In PE ratio market data is taken

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in to account. On other hand, in case of dividend growth model internal data related to firm

performance is considered. Hence, it can be said that all methods of valuation calculate price of

the shares in the different manner. Due to this reason it is very hard to obtain similar results from

the all valuation models.

(d) Risk faced by the FTSE 100 Company Tesco in its business

There are many sort of risks that faced by the FTSE 100 company in its business. Currently,

Tesco revenue and profit is declining consistently and it is the big problem that firm currently is

facing in its business. Firm needs to solve this problem and in this regard it needs to formulate

sound business strategy (Lall, 2012). It can generate economies of scale in its business which

will reduce cost and will elevate its profitability. This will lead to development of investors’

confidence on the business firm. The rate of sale of shares in the secondary market will decline

to some extent. On other hand, with increase in the firm profit its image will get improved

among the investors which lead to elevation in purchase of the firm shares. In this way risk faced

by the firm can be managed.

(e) Impact of situation on the choice of valuation method in this case

Disposable of the asset to some extent affects the choice of the specific valuation method.

This is because assets are the important part of the business and is used to measure the firm

financial position (Obstfeld, Shambaugh and Taylor, 2010). In case of acquisition if one firm is

acquiring other one then in that situation it is better to use discounted cash flow model for

valuation of shares. This is because in this model projections are made about the cash inflow and

outflow. Cash inflow to some extent is determined by the investment that firm currently made in

the business. Hence, it is very important for the business firms to make use of appropriate

valuation method. The way in which firm is going to acquire other one help one in determining

the valuation method that must be used in the business for computing value of shares.

TASK 3

(a) Recommendation in relation to acquisition

On the basis of ratio analysis it is recommended that Tesco must not acquire any FTSE 100

company. This is because firm is earning very low amount of profit. Its gross and net profit ratio

is very low. Hence, company is earning less amount of retained earnings in its business. It is not

possible for the company to acquire other one by using internal sources of finance. In order to

performance is considered. Hence, it can be said that all methods of valuation calculate price of

the shares in the different manner. Due to this reason it is very hard to obtain similar results from

the all valuation models.

(d) Risk faced by the FTSE 100 Company Tesco in its business

There are many sort of risks that faced by the FTSE 100 company in its business. Currently,

Tesco revenue and profit is declining consistently and it is the big problem that firm currently is

facing in its business. Firm needs to solve this problem and in this regard it needs to formulate

sound business strategy (Lall, 2012). It can generate economies of scale in its business which

will reduce cost and will elevate its profitability. This will lead to development of investors’

confidence on the business firm. The rate of sale of shares in the secondary market will decline

to some extent. On other hand, with increase in the firm profit its image will get improved

among the investors which lead to elevation in purchase of the firm shares. In this way risk faced

by the firm can be managed.

(e) Impact of situation on the choice of valuation method in this case

Disposable of the asset to some extent affects the choice of the specific valuation method.

This is because assets are the important part of the business and is used to measure the firm

financial position (Obstfeld, Shambaugh and Taylor, 2010). In case of acquisition if one firm is

acquiring other one then in that situation it is better to use discounted cash flow model for

valuation of shares. This is because in this model projections are made about the cash inflow and

outflow. Cash inflow to some extent is determined by the investment that firm currently made in

the business. Hence, it is very important for the business firms to make use of appropriate

valuation method. The way in which firm is going to acquire other one help one in determining

the valuation method that must be used in the business for computing value of shares.

TASK 3

(a) Recommendation in relation to acquisition

On the basis of ratio analysis it is recommended that Tesco must not acquire any FTSE 100

company. This is because firm is earning very low amount of profit. Its gross and net profit ratio

is very low. Hence, company is earning less amount of retained earnings in its business. It is not

possible for the company to acquire other one by using internal sources of finance. In order to

acquire other company firm will need to take heavy amount of debt from the market. Interest rate

will be moderate or high. Hence, after acquisition finance burden will increase on the business

firm. On other hand, if acquired firm failed to perform better then Tesco will face heavy loss in

its business which will not be good for the firm (International finance, 2016). Thus, on this basis

it is recommended that is will not be beneficial for Tesco to acquire other company. Value of the

firm shares is very low. It can be seen that value of shares is different in varied valuation models.

Share price is very low in case of all valuation models. There is very little fair value of the firm

shares. It can be said that Tesco is not in better condition and due to this reason it can take

decision to acquire other company.

CONCLUSION

On the basis of above report it can be articulated that the company Tesco is not

performing well in the market. All the financial ratios of the company is continuously

decreasing, which shows that company is in bad condition and performing badly. The suggestion

is that it should not acquire the business. According to the three valuations also the company not

performing well. So, the company is not good for the investment as well. It can be suggested that

should not choose the company to make investment and acquire.

will be moderate or high. Hence, after acquisition finance burden will increase on the business

firm. On other hand, if acquired firm failed to perform better then Tesco will face heavy loss in

its business which will not be good for the firm (International finance, 2016). Thus, on this basis

it is recommended that is will not be beneficial for Tesco to acquire other company. Value of the

firm shares is very low. It can be seen that value of shares is different in varied valuation models.

Share price is very low in case of all valuation models. There is very little fair value of the firm

shares. It can be said that Tesco is not in better condition and due to this reason it can take

decision to acquire other company.

CONCLUSION

On the basis of above report it can be articulated that the company Tesco is not

performing well in the market. All the financial ratios of the company is continuously

decreasing, which shows that company is in bad condition and performing badly. The suggestion

is that it should not acquire the business. According to the three valuations also the company not

performing well. So, the company is not good for the investment as well. It can be suggested that

should not choose the company to make investment and acquire.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERNECES

Books & journals

Devereux, M.B. and Yetman, J., 2010. Leverage constraints and the international transmission of

shocks. Journal of Money, Credit and Banking. 42(1). pp.71-105.

Eichengreen, B. and Flandreau, M., 2012. The Federal Reserve, the Bank of England, and the

rise of the dollar as an international currency, 1914–1939. Open Economies Review. 23(1).

pp.57-87.

Frankel, J. and Poonawala, J., 2010. The forward market in emerging currencies: Less biased

than in major currencies. Journal of International Money and Finance. 29(3). pp.585-598.

Garcia, R. and Tsafack, G., 2011. Dependence structure and extreme comovements in

international equity and bond markets. Journal of Banking & Finance. 35(8). pp.1954-1970.

Gilpin, R., 2011. Global political economy: Understanding the international economic order.

Princeton University Press.

Houston, J.F., Lin, C. and Ma, Y., 2012. Regulatory arbitrage and international bank flows. The

Journal of Finance. 67(5). pp.1845-1895.

Hunter, W.C., Kaufman, G.G. and Krueger, T.H. eds., 2012. The Asian financial crisis: origins,

implications, and solutions. Springer Science & Business Media.

Kresta, A. and Tichy, T., 2012. International Equity Portfolio Risk Modeling: The Case of the

NIG Model and Ordinary Copula Functions. Finance a Uver. 62(2). p.141.

Lall, R., 2012. From failure to failure: The politics of international banking regulation. Review of

International Political Economy. 19(4). pp.609-638.

Obstfeld, M., Shambaugh, J.C. and Taylor, A.M., 2010. Financial stability, the trilemma, and

international reserves. American Economic Journal: Macroeconomics. 2(2). pp.57-94.

Online

International finance, 2016. [Online]. Available through:<

https://www.tutorialspoint.com/international_finance/international_finance_introduction.ht

m>. [Accessed on 22nd November 2016].

Books & journals

Devereux, M.B. and Yetman, J., 2010. Leverage constraints and the international transmission of

shocks. Journal of Money, Credit and Banking. 42(1). pp.71-105.

Eichengreen, B. and Flandreau, M., 2012. The Federal Reserve, the Bank of England, and the

rise of the dollar as an international currency, 1914–1939. Open Economies Review. 23(1).

pp.57-87.

Frankel, J. and Poonawala, J., 2010. The forward market in emerging currencies: Less biased

than in major currencies. Journal of International Money and Finance. 29(3). pp.585-598.

Garcia, R. and Tsafack, G., 2011. Dependence structure and extreme comovements in

international equity and bond markets. Journal of Banking & Finance. 35(8). pp.1954-1970.

Gilpin, R., 2011. Global political economy: Understanding the international economic order.

Princeton University Press.

Houston, J.F., Lin, C. and Ma, Y., 2012. Regulatory arbitrage and international bank flows. The

Journal of Finance. 67(5). pp.1845-1895.

Hunter, W.C., Kaufman, G.G. and Krueger, T.H. eds., 2012. The Asian financial crisis: origins,

implications, and solutions. Springer Science & Business Media.

Kresta, A. and Tichy, T., 2012. International Equity Portfolio Risk Modeling: The Case of the

NIG Model and Ordinary Copula Functions. Finance a Uver. 62(2). p.141.

Lall, R., 2012. From failure to failure: The politics of international banking regulation. Review of

International Political Economy. 19(4). pp.609-638.

Obstfeld, M., Shambaugh, J.C. and Taylor, A.M., 2010. Financial stability, the trilemma, and

international reserves. American Economic Journal: Macroeconomics. 2(2). pp.57-94.

Online

International finance, 2016. [Online]. Available through:<

https://www.tutorialspoint.com/international_finance/international_finance_introduction.ht

m>. [Accessed on 22nd November 2016].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.