Tesco Plc. Corporate Social Responsibility and Financial Report

VerifiedAdded on 2020/10/05

|16

|4046

|435

Report

AI Summary

This report provides a comprehensive analysis of Tesco Plc., focusing on its stakeholders, environmental and social review, and corporate governance report. It delves into the types of stakeholders, particularly examining the roles of customers, suppliers, and colleagues. The report highlights how Tesco demonstrates its corporate and social responsibilities through initiatives such as the "Every little help makes a big difference" value, health partnerships, food waste reduction programs, and the Community Food Connection program. Furthermore, the report includes an analysis of Benedict Co.'s financial position, evaluating various financial ratios like current ratio, quick ratio, trade receivables, trade payables, and inventory turnover ratio, to assess its liquidity and efficiency over two years. The purpose and relevance of each ratio are explained, along with the results, movements, and performance aspects of Benedict Co. The report also critically evaluates the application of financial ratios for measuring and interpreting an organization's performance.

PREPARE A REPORT FOR YOUR MANAGER

WHICH: 1) USING THE ANNUAL REPORT

OF TESCO AVAILABLE AT THE FOL

WHICH: 1) USING THE ANNUAL REPORT

OF TESCO AVAILABLE AT THE FOL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1: TESCO PLC...........................................................................................................1

a) Explaining term stakeholders with its types in Tesco Plc.......................................................1

b) The way Environmental and Social Review and the Corporate Governance Report help

Tesco to demonstrate its performance in terms of its corporate and social responsibilities to

two of the stakeholders...............................................................................................................2

QUESTION 2: FINANCIAL POSITION OF BENEDICT CO......................................................4

a) Purpose and relevance of chosen ratio....................................................................................4

b) Results and movement of ratio in two years...........................................................................5

c) Performance aspect of Benedict co. which provides cause of concern................................10

d) Critical evaluation of application of financial ratio for measuring and interpreting

organization's performance.......................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

APPENDIX....................................................................................................................................14

INTRODUCTION...........................................................................................................................1

QUESTION 1: TESCO PLC...........................................................................................................1

a) Explaining term stakeholders with its types in Tesco Plc.......................................................1

b) The way Environmental and Social Review and the Corporate Governance Report help

Tesco to demonstrate its performance in terms of its corporate and social responsibilities to

two of the stakeholders...............................................................................................................2

QUESTION 2: FINANCIAL POSITION OF BENEDICT CO......................................................4

a) Purpose and relevance of chosen ratio....................................................................................4

b) Results and movement of ratio in two years...........................................................................5

c) Performance aspect of Benedict co. which provides cause of concern................................10

d) Critical evaluation of application of financial ratio for measuring and interpreting

organization's performance.......................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

APPENDIX....................................................................................................................................14

INTRODUCTION

Financial performance is referred as a subjective measure about application of asset with

reference to organization. The present report has considered two organizations i.e. Tesco Plc. and

Benedict co. for proper understanding of their financial position. In the same series, it has

articulated about stakeholders with its different types related to Tesco Plc. Further, it has

analysed environmental and social review of same. With reference to Benedict co., different

range of financial ratios have been implicated for meeting its requirements of potential

customers, lenders, investors and suppliers. It has also explained about objective and relevance

of various ratios.

QUESTION 1: TESCO PLC

a) Explaining term stakeholders with its types in Tesco Plc.

Stakeholder could be described as a person, organization or group which has direct

concern or interest in a specific business entity. It could affect or get affected through different

objectives, policies and actions. In any corporation, its primary stakeholders are suppliers,

investors, customers and employees. Generally, the stakeholders are classified in two types such

as external or internal. The individuals who are not directly working with organization as they

are indirectly affected by outcome and actions of any organization are known as external

stakeholders. The ones who give interest in a business entity via direct relationship like

investment or ownership and employment are known as internal stakeholders (Souza and et. al.,

2015).

Tesco Plc. has three types of stakeholders such as colleagues, suppliers and customers for

building transparent and more open relationships.

External stakeholders Customers: In the present scenario, business environment has been given with more

emphasis for creating long term relationships with its potential customers. Business

entities are viewed as particular drivers of long term profitability and viability of

business. Tesco Plc. is providing stable, lower and simpler prices for the purpose of

ensuring trust for delivering trip of the best shopping at good price.

Suppliers: The business entity highly relies on its partners for giving the best value in

context of its customers. The retailers have given huge reliance on relationship of

1

Financial performance is referred as a subjective measure about application of asset with

reference to organization. The present report has considered two organizations i.e. Tesco Plc. and

Benedict co. for proper understanding of their financial position. In the same series, it has

articulated about stakeholders with its different types related to Tesco Plc. Further, it has

analysed environmental and social review of same. With reference to Benedict co., different

range of financial ratios have been implicated for meeting its requirements of potential

customers, lenders, investors and suppliers. It has also explained about objective and relevance

of various ratios.

QUESTION 1: TESCO PLC

a) Explaining term stakeholders with its types in Tesco Plc.

Stakeholder could be described as a person, organization or group which has direct

concern or interest in a specific business entity. It could affect or get affected through different

objectives, policies and actions. In any corporation, its primary stakeholders are suppliers,

investors, customers and employees. Generally, the stakeholders are classified in two types such

as external or internal. The individuals who are not directly working with organization as they

are indirectly affected by outcome and actions of any organization are known as external

stakeholders. The ones who give interest in a business entity via direct relationship like

investment or ownership and employment are known as internal stakeholders (Souza and et. al.,

2015).

Tesco Plc. has three types of stakeholders such as colleagues, suppliers and customers for

building transparent and more open relationships.

External stakeholders Customers: In the present scenario, business environment has been given with more

emphasis for creating long term relationships with its potential customers. Business

entities are viewed as particular drivers of long term profitability and viability of

business. Tesco Plc. is providing stable, lower and simpler prices for the purpose of

ensuring trust for delivering trip of the best shopping at good price.

Suppliers: The business entity highly relies on its partners for giving the best value in

context of its customers. The retailers have given huge reliance on relationship of

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

suppliers in strong aspect as it also gives qualitative products to their customers at

optimal price. The partners of supply chain directly collaborates on distribution, logistics

and transportation process as well as environmental preservation. Tesco Plc. has

reorganised its relationship with reference to its suppliers. They have altered the way of

operating and implementing different initiatives for improving work with suppliers and

commercial culture (Kuo and et. al., 2018).

Internal stakeholders

Colleagues: The relationship with colleagues is very important as they help in developing

confidence and skills for managing operations. They would also identify stakeholder’s

value for understanding of influences, aims, roles and interest.

b) The way Environmental and Social Review and the Corporate Governance Report help Tesco

to demonstrate its performance in terms of its corporate and social responsibilities to two

of the stakeholders

Environmental and social review:

“Every little help makes a big difference”. It is a value on which Tesco ensures to serve

its customers, colleagues and their communities better day by day. The important part of this

purpose is to ensure social and environmental challenges affecting communities in which it

operates. The colleagues rely on this value that plays a role in making it easier for both

customers and colleagues to make healthier choices like reducing food waste and tackle food

poverty with developing sustainable supply chain.

The CSR report gives reviews about all the functions with set up of all corporate

responsibilities. Tesco have a clear and robust governance framework for responsibilities. Tesco

works on both challenges of health and food waste. The management wants to make it easier for

customer and colleagues and the community to be healthier (An update on our Corporate

Responsibility commitments ,2018). Tesco made partnership with health experts like Diabetes

UK and the British Heart Foundation so that it can support prevention and cure for the biggest

health challenges which company is facing. With the partnership, company is expertise in health

and health and enhancing its ability so that it can reach to every locality in UK. The company has

launched The Tesco Eat Happy Project, which has reached to over 1.3 million children as a part

of this program. It is helping children to learn more about their food and to involve more in

cooking at home.

2

optimal price. The partners of supply chain directly collaborates on distribution, logistics

and transportation process as well as environmental preservation. Tesco Plc. has

reorganised its relationship with reference to its suppliers. They have altered the way of

operating and implementing different initiatives for improving work with suppliers and

commercial culture (Kuo and et. al., 2018).

Internal stakeholders

Colleagues: The relationship with colleagues is very important as they help in developing

confidence and skills for managing operations. They would also identify stakeholder’s

value for understanding of influences, aims, roles and interest.

b) The way Environmental and Social Review and the Corporate Governance Report help Tesco

to demonstrate its performance in terms of its corporate and social responsibilities to two

of the stakeholders

Environmental and social review:

“Every little help makes a big difference”. It is a value on which Tesco ensures to serve

its customers, colleagues and their communities better day by day. The important part of this

purpose is to ensure social and environmental challenges affecting communities in which it

operates. The colleagues rely on this value that plays a role in making it easier for both

customers and colleagues to make healthier choices like reducing food waste and tackle food

poverty with developing sustainable supply chain.

The CSR report gives reviews about all the functions with set up of all corporate

responsibilities. Tesco have a clear and robust governance framework for responsibilities. Tesco

works on both challenges of health and food waste. The management wants to make it easier for

customer and colleagues and the community to be healthier (An update on our Corporate

Responsibility commitments ,2018). Tesco made partnership with health experts like Diabetes

UK and the British Heart Foundation so that it can support prevention and cure for the biggest

health challenges which company is facing. With the partnership, company is expertise in health

and health and enhancing its ability so that it can reach to every locality in UK. The company has

launched The Tesco Eat Happy Project, which has reached to over 1.3 million children as a part

of this program. It is helping children to learn more about their food and to involve more in

cooking at home.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Food waste is an area where Tesco is trying to make progress to prevent food from

wasting from farm to folk. With suppliers the overall approach of company has always been

assure to make as much use of edible crop as possible. In some cases, the company works on the

specification for broadened to accommodate more crops. In addition to this the company has

developed a range of new ways to change the forecast and order to help supplier reduce waste.

Tesco was the first UK retailer to measure and publish assured food waste data for UK

operations. Tesco has set a target for 2017 that no food that is safe for consumption will go to

waste from UK stores. To make it easier for the customer in UK, Tesco removed display unit

dates and moved to single date code of either best before or used by across the fresh products

like meat and dairy categories (Rahman, 2016).

Tesco is working on another area of tackling food waste within the organization's own

operations. Tesco initiated to deliver a goal that never to waste food that could be eaten, to meet

this goal The Community Food Connection program has been started. The CFS programme

allows stores to alert local charity and communities about the surplus food available at the end of

each day.

Tesco has started “Eat Fresh” campaign both in its stores and on social media. Tesco

started organizing free aerobics session for anyone in community in front of over 60 stores in

Thailand. It is complemented by Eat Fresh campaign to raise awareness of eating healthy. In UK

Tesco had partnership of over 15 years with Race for Life also funding for cancer Research UK

and encouraging colleagues and customers to take part.

Corporate Governance Report

Tesco's Boards and Executive Committee operates all its processes within a framework of

wider corporate governance. It ensures that all the decisions taken should be taken while

considering the right level of business. Tesco is creating a truly comprising such environment

where everyone is welcome there no biased on the basis of race, religion, national origin, colour,

nationality etc. Tesco values the diversity and skills and experiences that over 440000 colleagues

across the world bring to our business to help the customer more efficiently. Tesco experienced a

culture where all their colleagues are growing and developing their career at Tesco. Whistle-

blowing policy in Tesco is introduced to protect the colleagues, customers and business (Whistle-

blowing policy ,2018). The code of conduct in business makes it clear in company that wherever

it operates, the colleagues will be abide by law. To ensure about any wrongdoing Tesco provides

3

wasting from farm to folk. With suppliers the overall approach of company has always been

assure to make as much use of edible crop as possible. In some cases, the company works on the

specification for broadened to accommodate more crops. In addition to this the company has

developed a range of new ways to change the forecast and order to help supplier reduce waste.

Tesco was the first UK retailer to measure and publish assured food waste data for UK

operations. Tesco has set a target for 2017 that no food that is safe for consumption will go to

waste from UK stores. To make it easier for the customer in UK, Tesco removed display unit

dates and moved to single date code of either best before or used by across the fresh products

like meat and dairy categories (Rahman, 2016).

Tesco is working on another area of tackling food waste within the organization's own

operations. Tesco initiated to deliver a goal that never to waste food that could be eaten, to meet

this goal The Community Food Connection program has been started. The CFS programme

allows stores to alert local charity and communities about the surplus food available at the end of

each day.

Tesco has started “Eat Fresh” campaign both in its stores and on social media. Tesco

started organizing free aerobics session for anyone in community in front of over 60 stores in

Thailand. It is complemented by Eat Fresh campaign to raise awareness of eating healthy. In UK

Tesco had partnership of over 15 years with Race for Life also funding for cancer Research UK

and encouraging colleagues and customers to take part.

Corporate Governance Report

Tesco's Boards and Executive Committee operates all its processes within a framework of

wider corporate governance. It ensures that all the decisions taken should be taken while

considering the right level of business. Tesco is creating a truly comprising such environment

where everyone is welcome there no biased on the basis of race, religion, national origin, colour,

nationality etc. Tesco values the diversity and skills and experiences that over 440000 colleagues

across the world bring to our business to help the customer more efficiently. Tesco experienced a

culture where all their colleagues are growing and developing their career at Tesco. Whistle-

blowing policy in Tesco is introduced to protect the colleagues, customers and business (Whistle-

blowing policy ,2018). The code of conduct in business makes it clear in company that wherever

it operates, the colleagues will be abide by law. To ensure about any wrongdoing Tesco provides

3

free professional, confidential and secure service that enables colleagues, suppliers and the staffs

to raise concern.

Over the last few years, Tesco's business has gone through a significant restructuring and

committed to be open and transparent with colleagues is very important. One of the significant

change company made is the pay of colleagues working in stores across the UK. Tesco has made

an important investment in central Europe to offer store colleagues an average an average pay

increase of 5%, focusing on lower paid colleagues to increase their base salaries.

Tesco's corporate responsibility is provided in two ways: internally, through boards

committee and through advice and critical feedback externally. The central pillar of governance

framework is our Schedule of Group Delegated Authorities. Tesco have also taken additional

action to promote a positive culture and to tackle the unfavourable practices. For this, a new

Code of Conduct was launched in March 2015 to promote ethical practices at all level of our

business. Tesco has also changed the code of business with suppliers in order to build healthy

relationship with key stakeholders (Ismail, 2017).

The latest Supplier Viewpoint measure of how suppliers view their relation with

company that recognises the positive impact of the changes. Tesco is initiated towards aim to

gain the trust and improve transparency by ensuring that all colleagues understand their role and

responsibilities by creating an environment of workplace where everyone can feel empowered to

give their reviews and opinions. In addition to this, Tesco continues to improve opportunities for

women in company to progress throughout and particularly to the rank in senior and executive

management. By providing opportunities to all the colleagues, company aims in developed

broader talent pool that will support in regaining strategic competitiveness. This provides the

governance processes at Tesco and explained all the changes that has made.

QUESTION 2: FINANCIAL POSITION OF BENEDICT CO.

a) Purpose and relevance of chosen ratio

Current ratio: This ratio is referred as an important measure for liquidity aspect as

liabilities of short term are due in next year. Generally, it provides ability of organization

for repaying its liabilities such as debt and account payable along with its assets which

are accounts receivable, cash, marketable securities and inventory. In simple words, it

provides small view of financial health of organization (Almamy, Aston and Ngwa,

2016).

4

to raise concern.

Over the last few years, Tesco's business has gone through a significant restructuring and

committed to be open and transparent with colleagues is very important. One of the significant

change company made is the pay of colleagues working in stores across the UK. Tesco has made

an important investment in central Europe to offer store colleagues an average an average pay

increase of 5%, focusing on lower paid colleagues to increase their base salaries.

Tesco's corporate responsibility is provided in two ways: internally, through boards

committee and through advice and critical feedback externally. The central pillar of governance

framework is our Schedule of Group Delegated Authorities. Tesco have also taken additional

action to promote a positive culture and to tackle the unfavourable practices. For this, a new

Code of Conduct was launched in March 2015 to promote ethical practices at all level of our

business. Tesco has also changed the code of business with suppliers in order to build healthy

relationship with key stakeholders (Ismail, 2017).

The latest Supplier Viewpoint measure of how suppliers view their relation with

company that recognises the positive impact of the changes. Tesco is initiated towards aim to

gain the trust and improve transparency by ensuring that all colleagues understand their role and

responsibilities by creating an environment of workplace where everyone can feel empowered to

give their reviews and opinions. In addition to this, Tesco continues to improve opportunities for

women in company to progress throughout and particularly to the rank in senior and executive

management. By providing opportunities to all the colleagues, company aims in developed

broader talent pool that will support in regaining strategic competitiveness. This provides the

governance processes at Tesco and explained all the changes that has made.

QUESTION 2: FINANCIAL POSITION OF BENEDICT CO.

a) Purpose and relevance of chosen ratio

Current ratio: This ratio is referred as an important measure for liquidity aspect as

liabilities of short term are due in next year. Generally, it provides ability of organization

for repaying its liabilities such as debt and account payable along with its assets which

are accounts receivable, cash, marketable securities and inventory. In simple words, it

provides small view of financial health of organization (Almamy, Aston and Ngwa,

2016).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Quick ratio: It measures the capability or organization to meet its obligations of short

term with its liquid assets. Usually, the lenders prefer this ratio due to more liquidity

which signifies better aspect for adapting its changing conditions. It excludes inventory

from current ratio as it provides comparison from current assets to debts.

Trade receivable (in days): This ratio represents about its liquidity. It gives special

emphasis on time taken in context to its trade debtors for settling its bills or invoices.

Generally, it indicates that whether debtors are allowed for excessive credit or not.

Trade payable (in days): It gives similar aspect from trade receivables days. It provides

deep insight about business that whether it considers full benefit with reference to

availability of trade credit or not. It helps in estimating average time taken for settling its

debt along with its trade suppliers. It assesses liquidity position of businesses (Setiawan

and Amboningtyas, 2018).

Inventory turnover ratio (in days): It represents efficiency of organization in context of

inventory. It helps in measuring average number of days on which organization holds its

inventory before activities of selling. In the same series, it measures sales potential or a

number which is more than norms of industry which indicate issues related to sales

forecast. If situation is vice versa then organization has inability to fulfil its specific

demand.

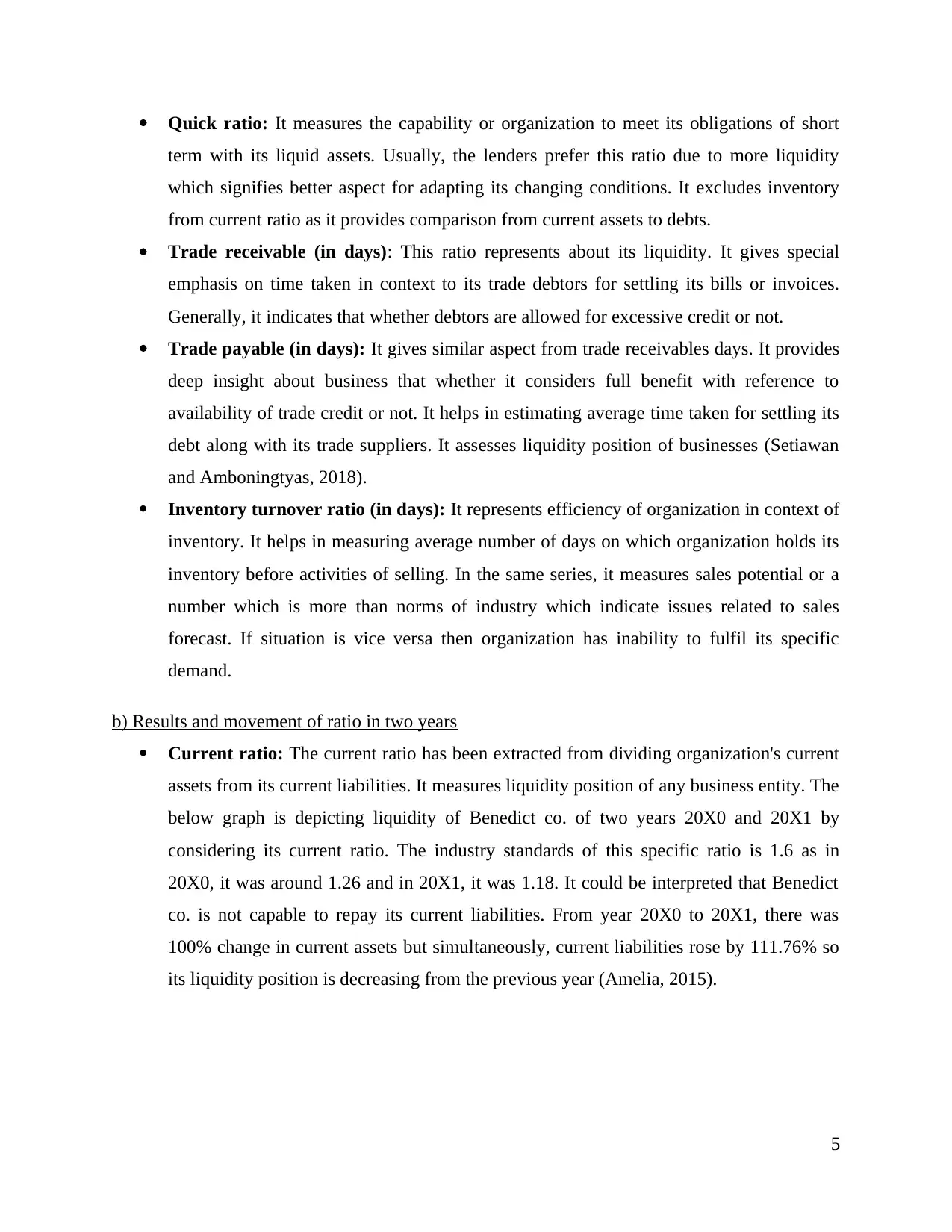

b) Results and movement of ratio in two years

Current ratio: The current ratio has been extracted from dividing organization's current

assets from its current liabilities. It measures liquidity position of any business entity. The

below graph is depicting liquidity of Benedict co. of two years 20X0 and 20X1 by

considering its current ratio. The industry standards of this specific ratio is 1.6 as in

20X0, it was around 1.26 and in 20X1, it was 1.18. It could be interpreted that Benedict

co. is not capable to repay its current liabilities. From year 20X0 to 20X1, there was

100% change in current assets but simultaneously, current liabilities rose by 111.76% so

its liquidity position is decreasing from the previous year (Amelia, 2015).

5

term with its liquid assets. Usually, the lenders prefer this ratio due to more liquidity

which signifies better aspect for adapting its changing conditions. It excludes inventory

from current ratio as it provides comparison from current assets to debts.

Trade receivable (in days): This ratio represents about its liquidity. It gives special

emphasis on time taken in context to its trade debtors for settling its bills or invoices.

Generally, it indicates that whether debtors are allowed for excessive credit or not.

Trade payable (in days): It gives similar aspect from trade receivables days. It provides

deep insight about business that whether it considers full benefit with reference to

availability of trade credit or not. It helps in estimating average time taken for settling its

debt along with its trade suppliers. It assesses liquidity position of businesses (Setiawan

and Amboningtyas, 2018).

Inventory turnover ratio (in days): It represents efficiency of organization in context of

inventory. It helps in measuring average number of days on which organization holds its

inventory before activities of selling. In the same series, it measures sales potential or a

number which is more than norms of industry which indicate issues related to sales

forecast. If situation is vice versa then organization has inability to fulfil its specific

demand.

b) Results and movement of ratio in two years

Current ratio: The current ratio has been extracted from dividing organization's current

assets from its current liabilities. It measures liquidity position of any business entity. The

below graph is depicting liquidity of Benedict co. of two years 20X0 and 20X1 by

considering its current ratio. The industry standards of this specific ratio is 1.6 as in

20X0, it was around 1.26 and in 20X1, it was 1.18. It could be interpreted that Benedict

co. is not capable to repay its current liabilities. From year 20X0 to 20X1, there was

100% change in current assets but simultaneously, current liabilities rose by 111.76% so

its liquidity position is decreasing from the previous year (Amelia, 2015).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

20X0 20X1

1.14

1.16

1.18

1.2

1.22

1.24

1.26

1.28

Current ratio

Year

Ratio

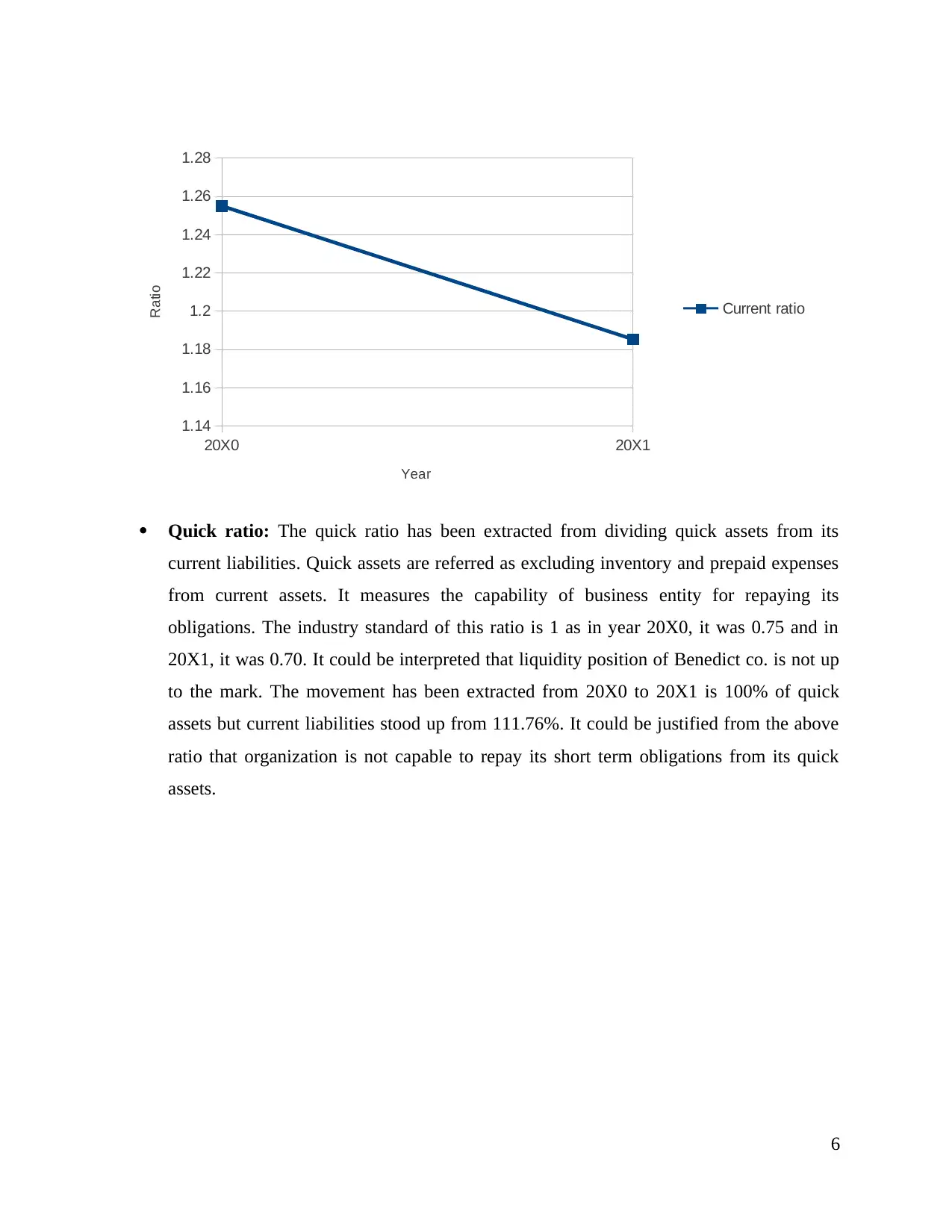

Quick ratio: The quick ratio has been extracted from dividing quick assets from its

current liabilities. Quick assets are referred as excluding inventory and prepaid expenses

from current assets. It measures the capability of business entity for repaying its

obligations. The industry standard of this ratio is 1 as in year 20X0, it was 0.75 and in

20X1, it was 0.70. It could be interpreted that liquidity position of Benedict co. is not up

to the mark. The movement has been extracted from 20X0 to 20X1 is 100% of quick

assets but current liabilities stood up from 111.76%. It could be justified from the above

ratio that organization is not capable to repay its short term obligations from its quick

assets.

6

1.14

1.16

1.18

1.2

1.22

1.24

1.26

1.28

Current ratio

Year

Ratio

Quick ratio: The quick ratio has been extracted from dividing quick assets from its

current liabilities. Quick assets are referred as excluding inventory and prepaid expenses

from current assets. It measures the capability of business entity for repaying its

obligations. The industry standard of this ratio is 1 as in year 20X0, it was 0.75 and in

20X1, it was 0.70. It could be interpreted that liquidity position of Benedict co. is not up

to the mark. The movement has been extracted from 20X0 to 20X1 is 100% of quick

assets but current liabilities stood up from 111.76%. It could be justified from the above

ratio that organization is not capable to repay its short term obligations from its quick

assets.

6

20X0 20X1

0.68

0.69

0.7

0.71

0.72

0.73

0.74

0.75

Quick ratio

Year

Ratio

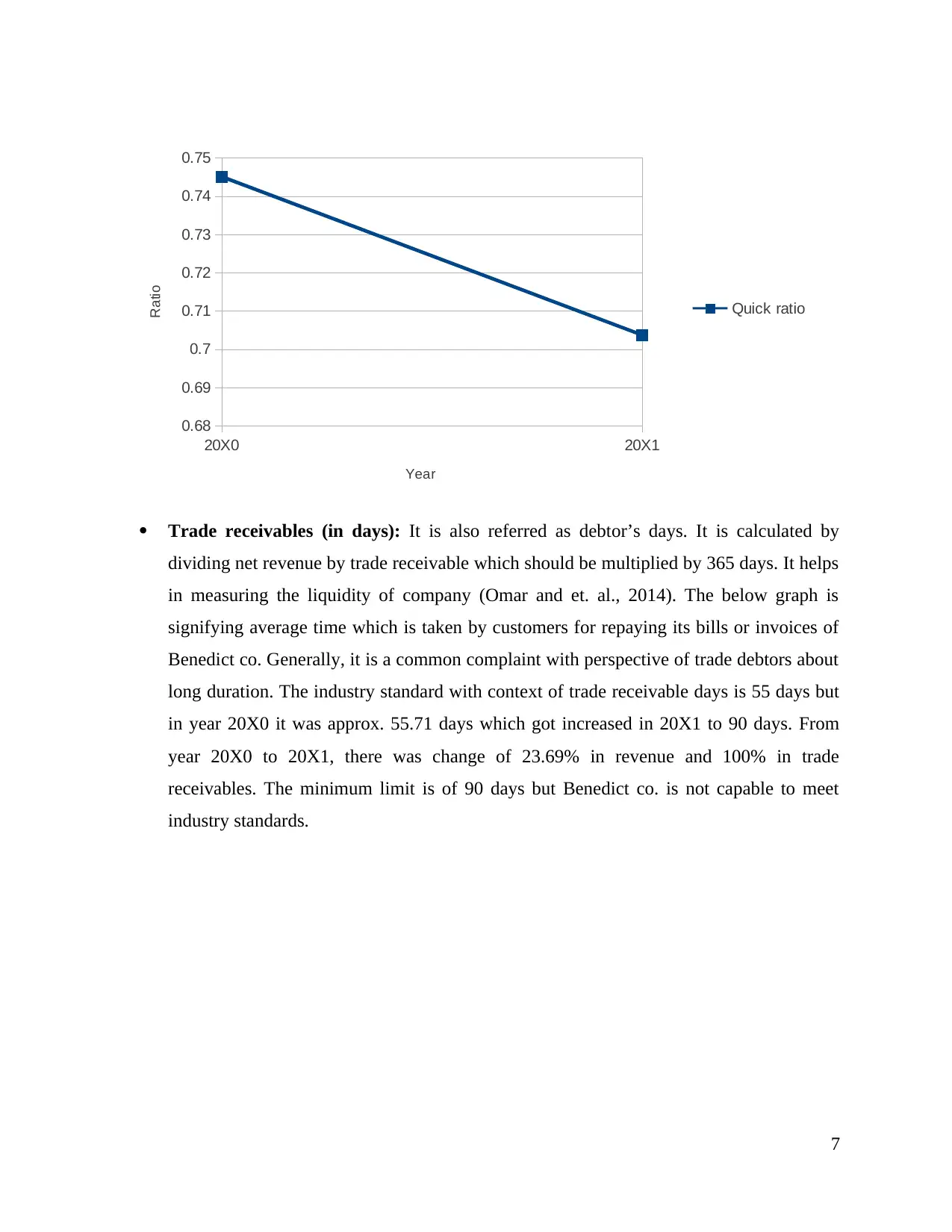

Trade receivables (in days): It is also referred as debtor’s days. It is calculated by

dividing net revenue by trade receivable which should be multiplied by 365 days. It helps

in measuring the liquidity of company (Omar and et. al., 2014). The below graph is

signifying average time which is taken by customers for repaying its bills or invoices of

Benedict co. Generally, it is a common complaint with perspective of trade debtors about

long duration. The industry standard with context of trade receivable days is 55 days but

in year 20X0 it was approx. 55.71 days which got increased in 20X1 to 90 days. From

year 20X0 to 20X1, there was change of 23.69% in revenue and 100% in trade

receivables. The minimum limit is of 90 days but Benedict co. is not capable to meet

industry standards.

7

0.68

0.69

0.7

0.71

0.72

0.73

0.74

0.75

Quick ratio

Year

Ratio

Trade receivables (in days): It is also referred as debtor’s days. It is calculated by

dividing net revenue by trade receivable which should be multiplied by 365 days. It helps

in measuring the liquidity of company (Omar and et. al., 2014). The below graph is

signifying average time which is taken by customers for repaying its bills or invoices of

Benedict co. Generally, it is a common complaint with perspective of trade debtors about

long duration. The industry standard with context of trade receivable days is 55 days but

in year 20X0 it was approx. 55.71 days which got increased in 20X1 to 90 days. From

year 20X0 to 20X1, there was change of 23.69% in revenue and 100% in trade

receivables. The minimum limit is of 90 days but Benedict co. is not capable to meet

industry standards.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

20X0 20X1

0

10

20

30

40

50

60

70

80

90

100

Trade receivables days

Year

Days

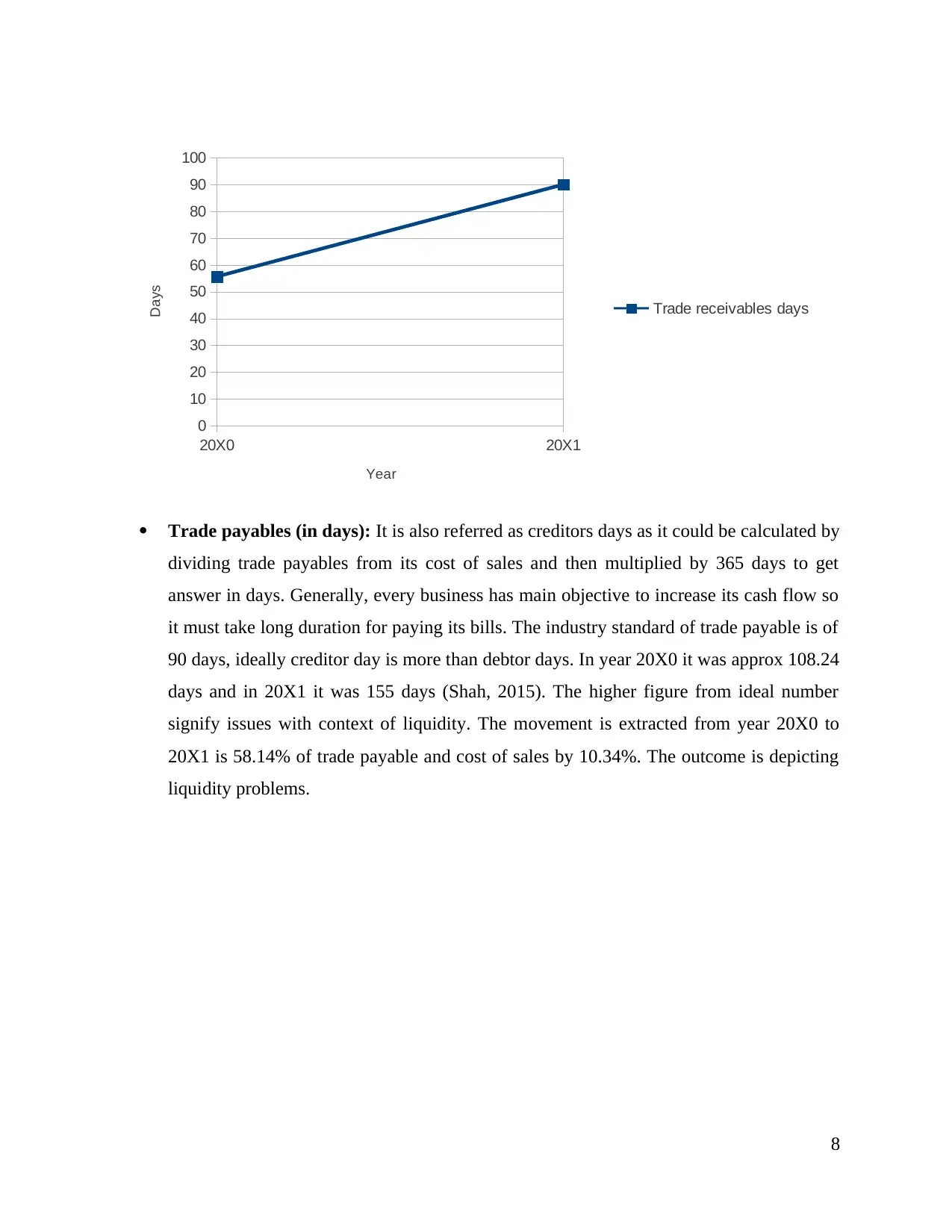

Trade payables (in days): It is also referred as creditors days as it could be calculated by

dividing trade payables from its cost of sales and then multiplied by 365 days to get

answer in days. Generally, every business has main objective to increase its cash flow so

it must take long duration for paying its bills. The industry standard of trade payable is of

90 days, ideally creditor day is more than debtor days. In year 20X0 it was approx 108.24

days and in 20X1 it was 155 days (Shah, 2015). The higher figure from ideal number

signify issues with context of liquidity. The movement is extracted from year 20X0 to

20X1 is 58.14% of trade payable and cost of sales by 10.34%. The outcome is depicting

liquidity problems.

8

0

10

20

30

40

50

60

70

80

90

100

Trade receivables days

Year

Days

Trade payables (in days): It is also referred as creditors days as it could be calculated by

dividing trade payables from its cost of sales and then multiplied by 365 days to get

answer in days. Generally, every business has main objective to increase its cash flow so

it must take long duration for paying its bills. The industry standard of trade payable is of

90 days, ideally creditor day is more than debtor days. In year 20X0 it was approx 108.24

days and in 20X1 it was 155 days (Shah, 2015). The higher figure from ideal number

signify issues with context of liquidity. The movement is extracted from year 20X0 to

20X1 is 58.14% of trade payable and cost of sales by 10.34%. The outcome is depicting

liquidity problems.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

20X0 20X1

0

20

40

60

80

100

120

140

160

180

Trade payables days

Year

Days

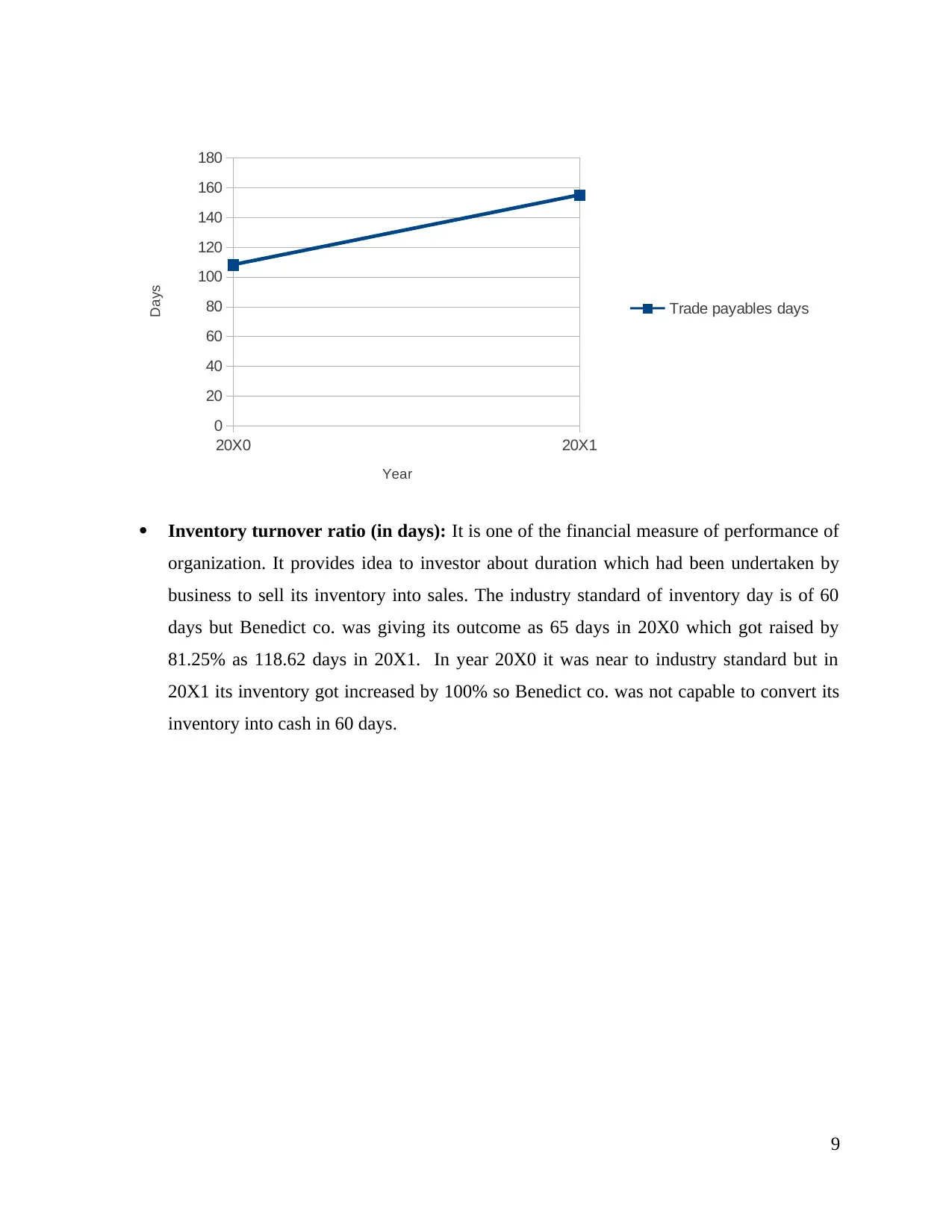

Inventory turnover ratio (in days): It is one of the financial measure of performance of

organization. It provides idea to investor about duration which had been undertaken by

business to sell its inventory into sales. The industry standard of inventory day is of 60

days but Benedict co. was giving its outcome as 65 days in 20X0 which got raised by

81.25% as 118.62 days in 20X1. In year 20X0 it was near to industry standard but in

20X1 its inventory got increased by 100% so Benedict co. was not capable to convert its

inventory into cash in 60 days.

9

0

20

40

60

80

100

120

140

160

180

Trade payables days

Year

Days

Inventory turnover ratio (in days): It is one of the financial measure of performance of

organization. It provides idea to investor about duration which had been undertaken by

business to sell its inventory into sales. The industry standard of inventory day is of 60

days but Benedict co. was giving its outcome as 65 days in 20X0 which got raised by

81.25% as 118.62 days in 20X1. In year 20X0 it was near to industry standard but in

20X1 its inventory got increased by 100% so Benedict co. was not capable to convert its

inventory into cash in 60 days.

9

20X0 20X1

0

20

40

60

80

100

120

140

Inventory days

Year

Days

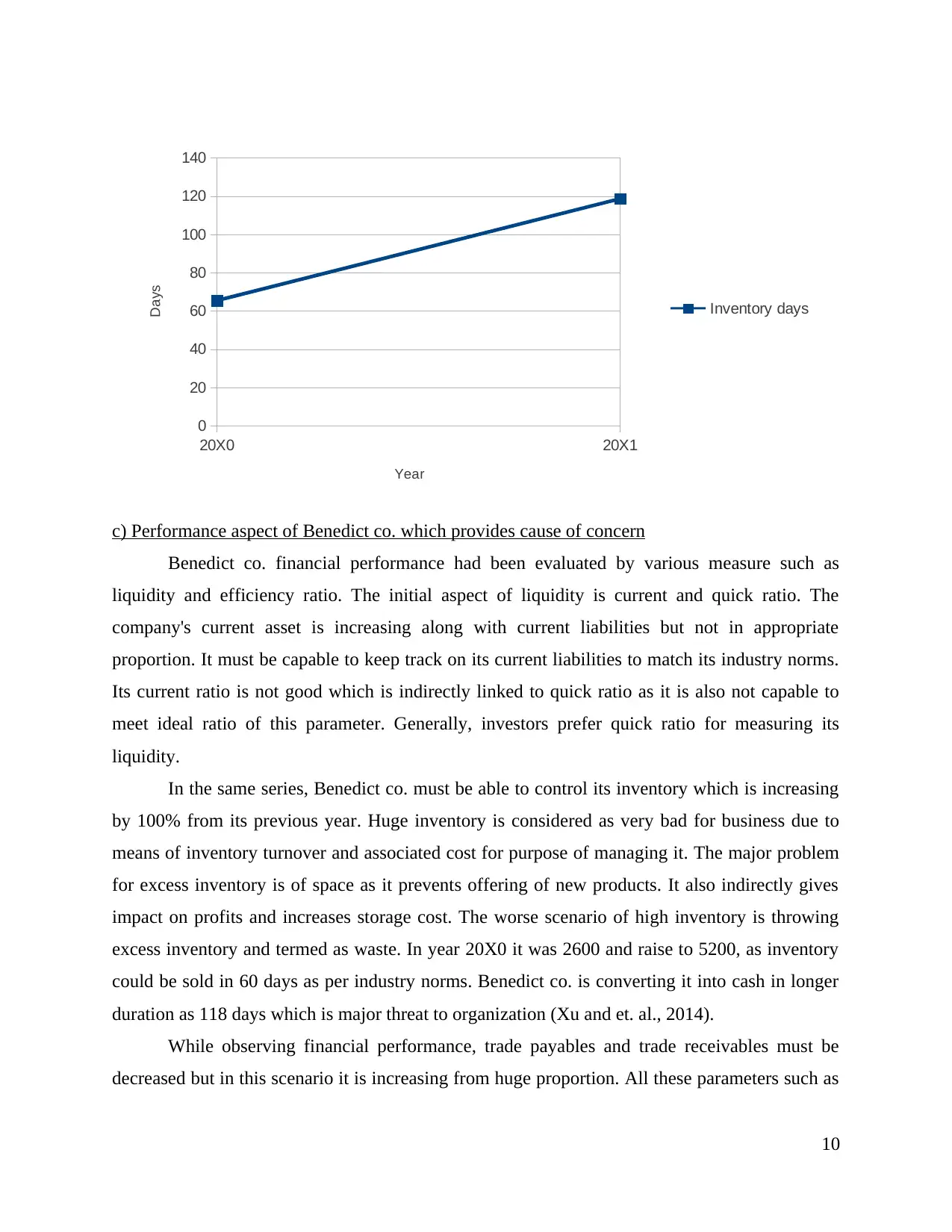

c) Performance aspect of Benedict co. which provides cause of concern

Benedict co. financial performance had been evaluated by various measure such as

liquidity and efficiency ratio. The initial aspect of liquidity is current and quick ratio. The

company's current asset is increasing along with current liabilities but not in appropriate

proportion. It must be capable to keep track on its current liabilities to match its industry norms.

Its current ratio is not good which is indirectly linked to quick ratio as it is also not capable to

meet ideal ratio of this parameter. Generally, investors prefer quick ratio for measuring its

liquidity.

In the same series, Benedict co. must be able to control its inventory which is increasing

by 100% from its previous year. Huge inventory is considered as very bad for business due to

means of inventory turnover and associated cost for purpose of managing it. The major problem

for excess inventory is of space as it prevents offering of new products. It also indirectly gives

impact on profits and increases storage cost. The worse scenario of high inventory is throwing

excess inventory and termed as waste. In year 20X0 it was 2600 and raise to 5200, as inventory

could be sold in 60 days as per industry norms. Benedict co. is converting it into cash in longer

duration as 118 days which is major threat to organization (Xu and et. al., 2014).

While observing financial performance, trade payables and trade receivables must be

decreased but in this scenario it is increasing from huge proportion. All these parameters such as

10

0

20

40

60

80

100

120

140

Inventory days

Year

Days

c) Performance aspect of Benedict co. which provides cause of concern

Benedict co. financial performance had been evaluated by various measure such as

liquidity and efficiency ratio. The initial aspect of liquidity is current and quick ratio. The

company's current asset is increasing along with current liabilities but not in appropriate

proportion. It must be capable to keep track on its current liabilities to match its industry norms.

Its current ratio is not good which is indirectly linked to quick ratio as it is also not capable to

meet ideal ratio of this parameter. Generally, investors prefer quick ratio for measuring its

liquidity.

In the same series, Benedict co. must be able to control its inventory which is increasing

by 100% from its previous year. Huge inventory is considered as very bad for business due to

means of inventory turnover and associated cost for purpose of managing it. The major problem

for excess inventory is of space as it prevents offering of new products. It also indirectly gives

impact on profits and increases storage cost. The worse scenario of high inventory is throwing

excess inventory and termed as waste. In year 20X0 it was 2600 and raise to 5200, as inventory

could be sold in 60 days as per industry norms. Benedict co. is converting it into cash in longer

duration as 118 days which is major threat to organization (Xu and et. al., 2014).

While observing financial performance, trade payables and trade receivables must be

decreased but in this scenario it is increasing from huge proportion. All these parameters such as

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.