Financial Reporting Analysis: Tesco Plc and IFRS Framework

VerifiedAdded on 2020/09/17

|13

|2290

|38

Report

AI Summary

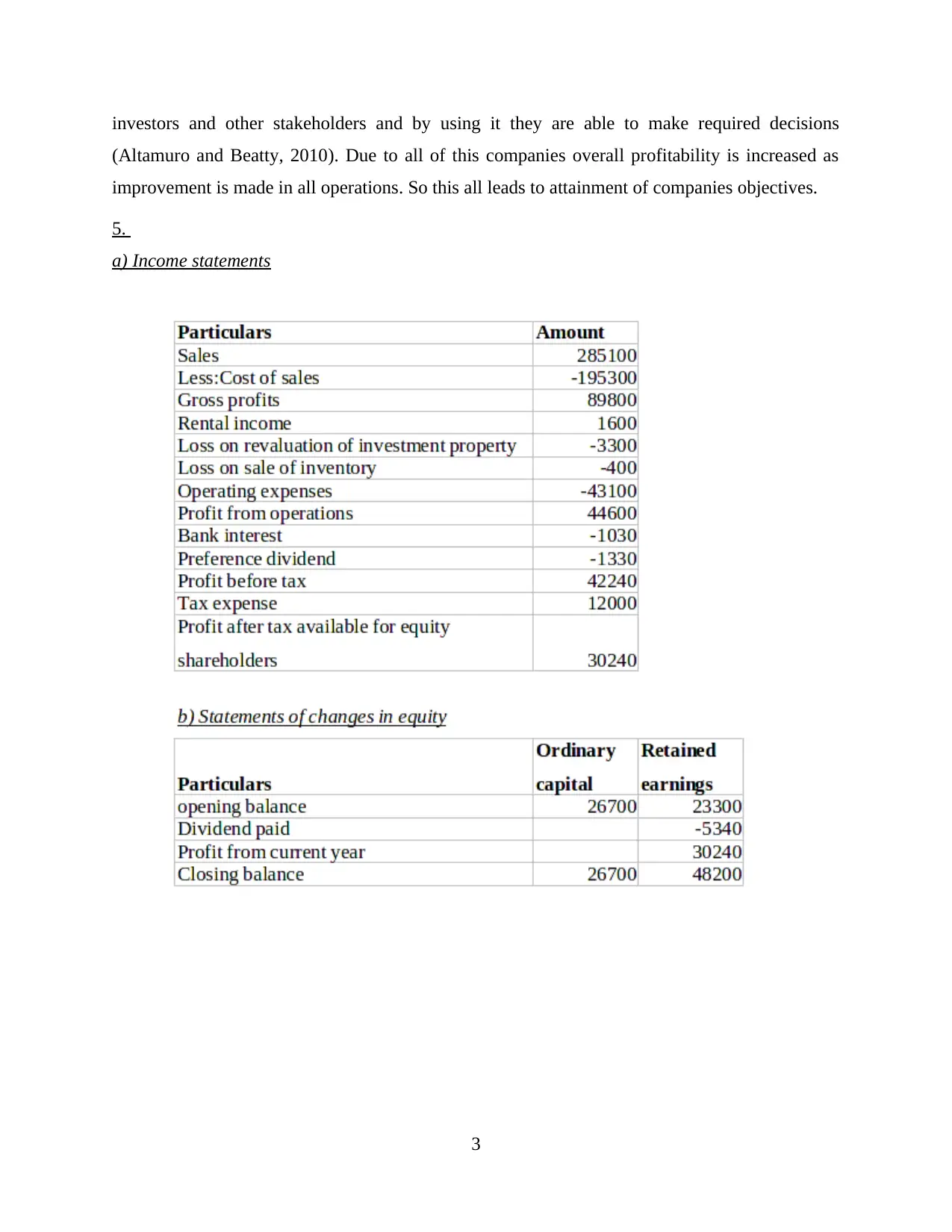

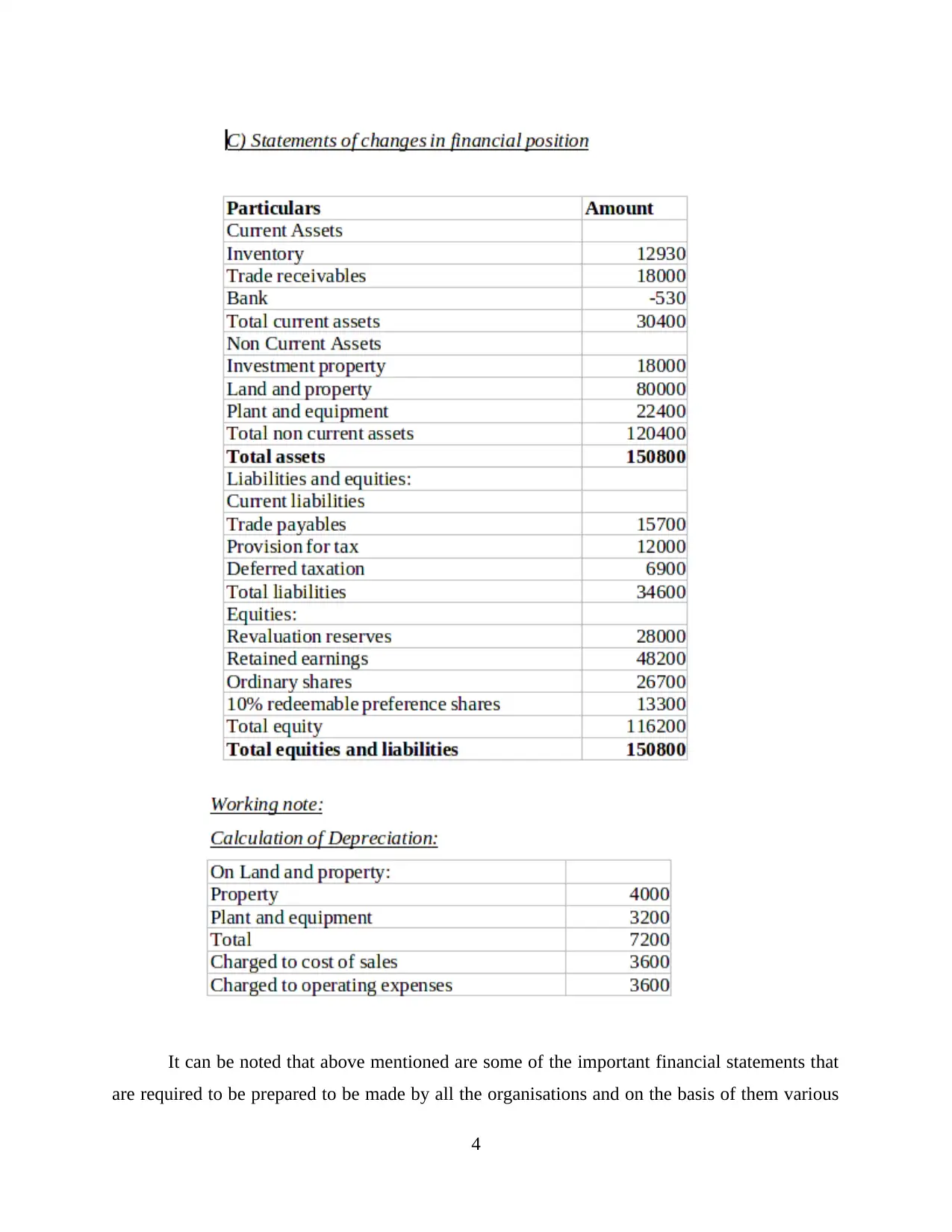

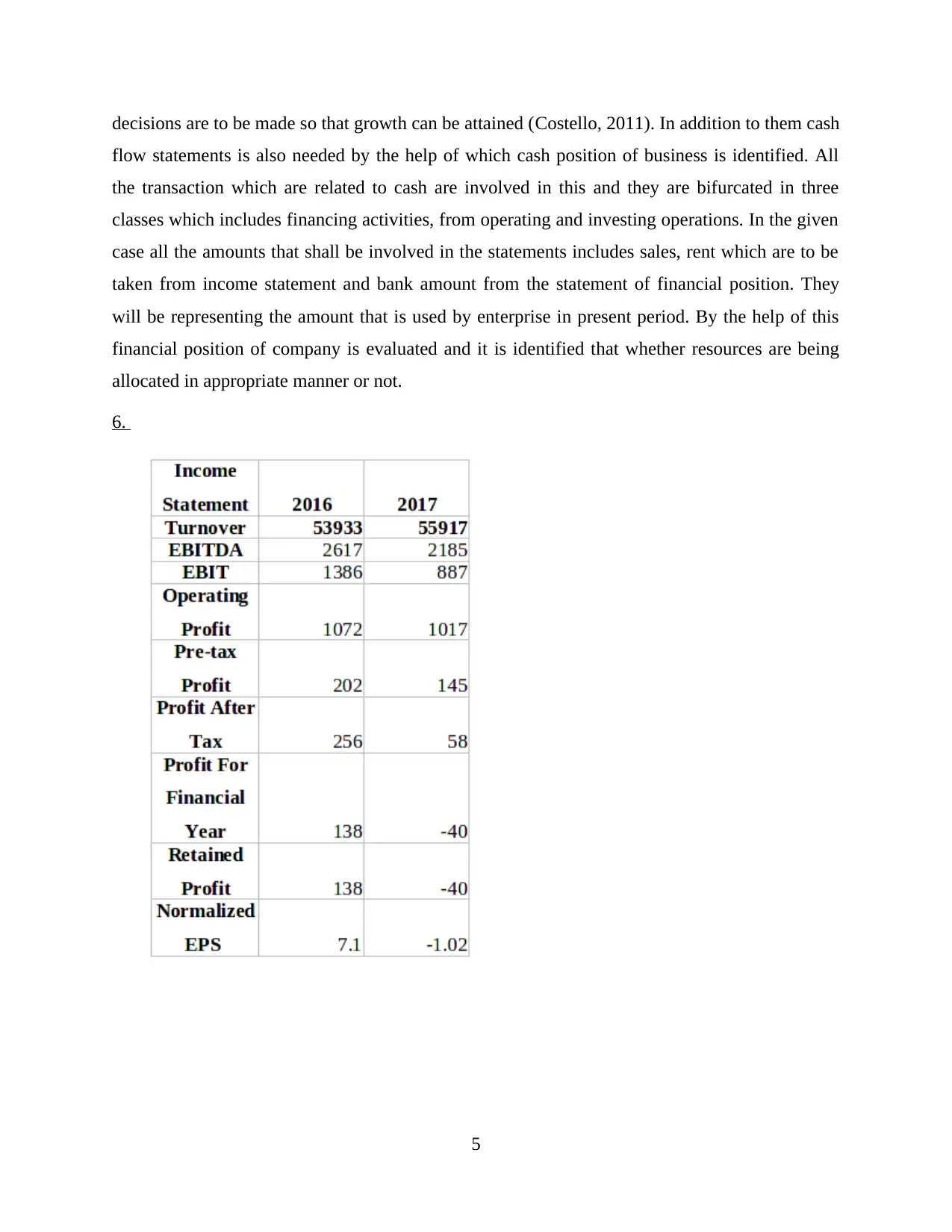

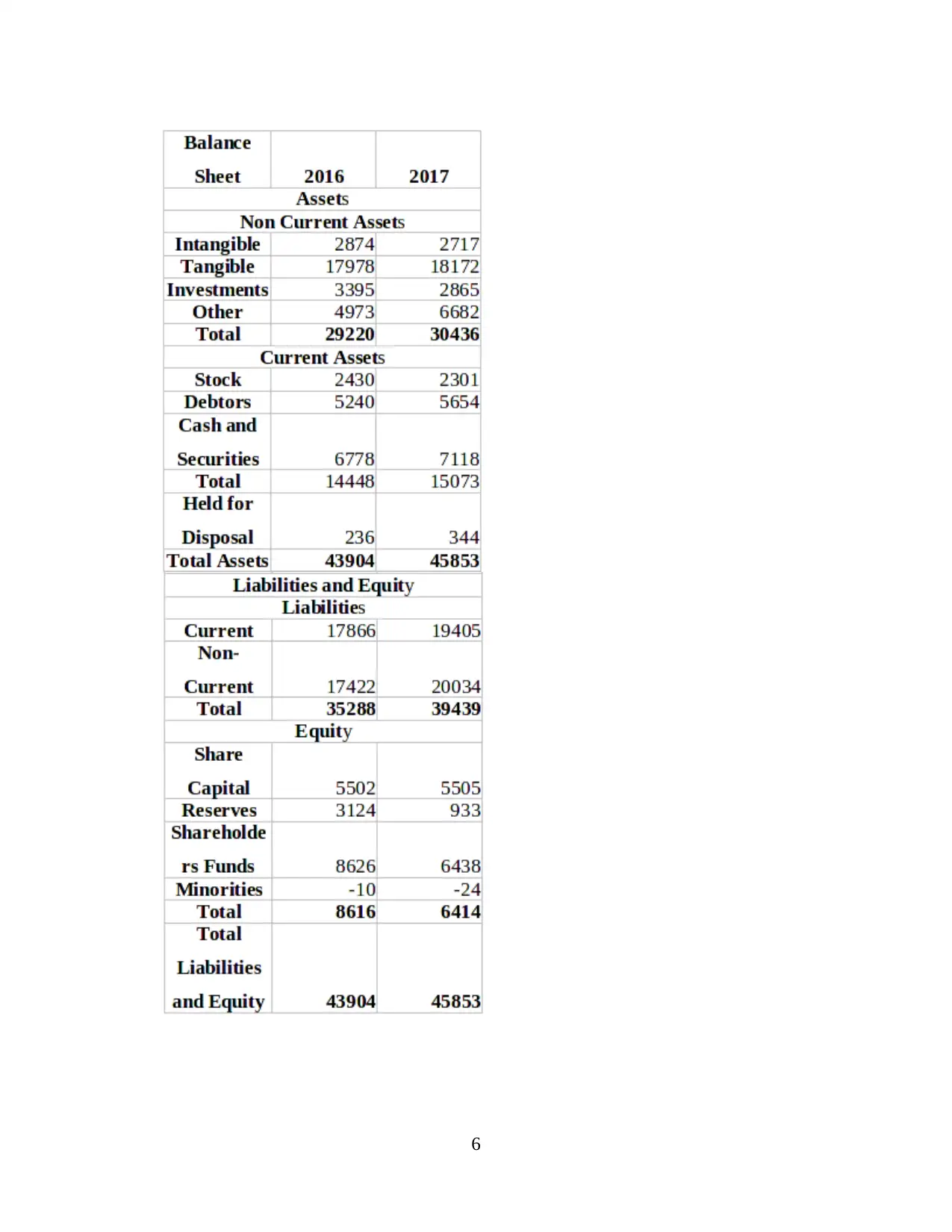

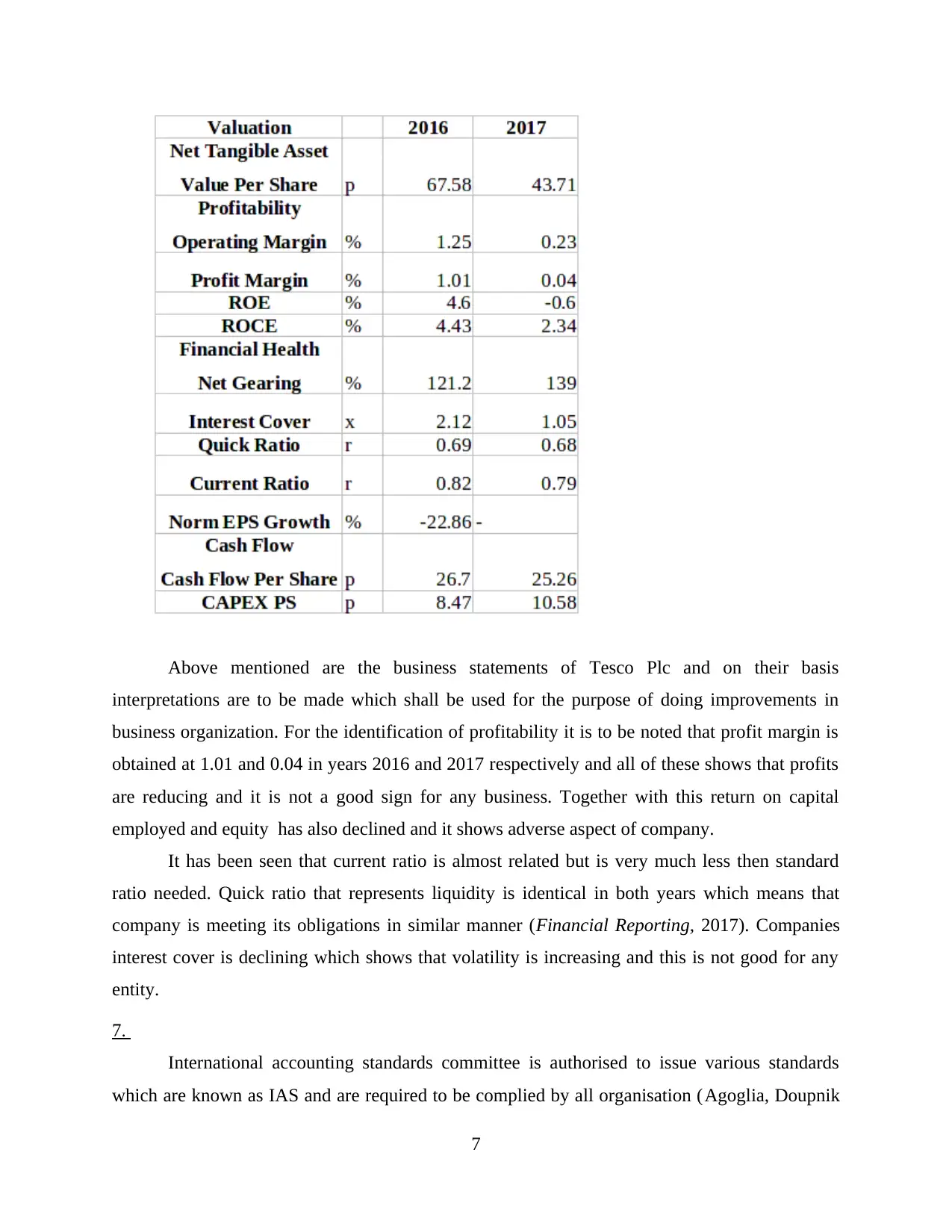

This report offers a detailed financial reporting analysis of Tesco Plc, focusing on the application of the IFRS framework. It begins with an introduction to the global financial landscape and the importance of financial statements in decision-making for investors and management. The report then delves into Task 1, exploring the IFRS framework, its concepts, and its role in providing guidelines for financial reporting. It examines practical issues, the conceptual framework, and the stakeholders involved in financial reporting, including employees, suppliers, and investors. The report further analyzes the importance of financial reporting for performance evaluation, transparency, and achieving company objectives. It also discusses key financial statements like income statements, balance sheets, and cash flow statements and provides an interpretation of Tesco Plc's financial performance, including profitability, liquidity, and solvency ratios. The report highlights the role of the International Accounting Standards Committee and the International Financial Reporting Standards (IFRS), discussing the differences between IAS and IFRS and their impact on financial reporting. Finally, it outlines the benefits of IFRS for investors, including increased accuracy, comparability, and timely loss recognition. The report emphasizes the relevance of IFRS in presenting company transactions fairly and improving clarity in financial reporting, making it easier to access foreign capital markets and compare data with global competitors.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.