Management Accounting Report: Tesco's Systems and Strategies Analysis

VerifiedAdded on 2020/12/18

|16

|5069

|95

Report

AI Summary

This report provides a detailed analysis of management accounting practices within Tesco, a leading retail company. It explores various aspects of management accounting, including cost accounting systems, price optimization, job costing, and inventory management. The report examines different types of management accounting systems used by Tesco, such as cost accounting, price optimization, job costing, and inventory management systems, highlighting their benefits and applications. Furthermore, it delves into the generation and significance of management accounting reports, including performance reports, inventory management reports, account receivable reports, budget reports, and job cost reports. The report also discusses the integration of management accounting systems and reports with organizational processes, emphasizing their role in evaluating business performance and informing strategic decision-making. Additionally, the report touches on the importance of appropriate costing techniques and the advantages and disadvantages of planning tools used in budgetary control, concluding with an overview of how management accounting systems can be adopted to address financial challenges and contribute to sustainable success within the organization. The report is concluded with references.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and requirement of its systems......................................................1

P2 Management accounting reporting........................................................................................3

M1 Benefits of management accounting system........................................................................4

D1 Management accounting system and its reports are integrated with organisational process 5

TASK 2............................................................................................................................................5

P3 Appropriate costing technique...............................................................................................5

M2 various costing techniques....................................................................................................7

D2 Data interpretation................................................................................................................7

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of planning tools used in budgetary control.........................8

M3 Use and application of planning tools is preparing and forecasting budgets.......................9

TASK 4..........................................................................................................................................10

P5 Adoption of management accounting system to respond financial problems.....................10

M4 Management accounting can lead sustainable success.......................................................12

D3 Planning tools can lead organisation toward success..........................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and requirement of its systems......................................................1

P2 Management accounting reporting........................................................................................3

M1 Benefits of management accounting system........................................................................4

D1 Management accounting system and its reports are integrated with organisational process 5

TASK 2............................................................................................................................................5

P3 Appropriate costing technique...............................................................................................5

M2 various costing techniques....................................................................................................7

D2 Data interpretation................................................................................................................7

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of planning tools used in budgetary control.........................8

M3 Use and application of planning tools is preparing and forecasting budgets.......................9

TASK 4..........................................................................................................................................10

P5 Adoption of management accounting system to respond financial problems.....................10

M4 Management accounting can lead sustainable success.......................................................12

D3 Planning tools can lead organisation toward success..........................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is used to analyse the ways in which company is performing its

operational activities and effective execution of business by manager. It is a process of

generating various business reports that provide business information to internal stakeholders.

Managers analyse such information and than make strategic decision in order to enhance

performance of their company (Management accounting. 2018). It directs managers to analyse

cost which is involved in different activities of an organisation so to increase profitability.

Company chosen for this project report is Tesco, it is a leading retailer in its industry and its

headquarter is in Welwyn Garden City, Hertfordshire, England, UK. Main objective of this

reports is to figure out that the way in which various reports and systems of management

accounting helps internal stakeholder to make strategies to increase productivity.

This project report covers various topics such as management accounting systems and its

reports with benefits, various costing techniques to calculate operating profits, advantages and

disadvantages of planning tools used in budgetary control and use of management accounting

systems to deal financial problems.

TASK 1

P1 Management accounting and requirement of its systems

Management accounting: It refers to the process of controlling, managing, recording

and measuring accounting information which is presented to internal stakeholders to examine

performance of a company (Wickramasinghe and Alawattage, 2012). In Tesco managers use it to

formulate different policies that are going to be implemented within the organisation. It assist

managers to keep information of day-to-day activities of business.

Management accounting system: It guides managers and owners to get information of

various activities that are executed by their organisation. It provides data of costs, inventory,

customer's needs, appropriate pricing for product and different jobs that are performed according

to specification of clients. Management of Tesco use this system to keep a track record of each

action which is taken by organisation's staff and other members. Various types of management

accounting systems are used by managers of the company. These systems are as follows:

Cost accounting system: It is used by different kind of firms such as manufacturing,

retailing, distributing etc. to estimate actual costs that are involved in their production, supply

1

Management accounting is used to analyse the ways in which company is performing its

operational activities and effective execution of business by manager. It is a process of

generating various business reports that provide business information to internal stakeholders.

Managers analyse such information and than make strategic decision in order to enhance

performance of their company (Management accounting. 2018). It directs managers to analyse

cost which is involved in different activities of an organisation so to increase profitability.

Company chosen for this project report is Tesco, it is a leading retailer in its industry and its

headquarter is in Welwyn Garden City, Hertfordshire, England, UK. Main objective of this

reports is to figure out that the way in which various reports and systems of management

accounting helps internal stakeholder to make strategies to increase productivity.

This project report covers various topics such as management accounting systems and its

reports with benefits, various costing techniques to calculate operating profits, advantages and

disadvantages of planning tools used in budgetary control and use of management accounting

systems to deal financial problems.

TASK 1

P1 Management accounting and requirement of its systems

Management accounting: It refers to the process of controlling, managing, recording

and measuring accounting information which is presented to internal stakeholders to examine

performance of a company (Wickramasinghe and Alawattage, 2012). In Tesco managers use it to

formulate different policies that are going to be implemented within the organisation. It assist

managers to keep information of day-to-day activities of business.

Management accounting system: It guides managers and owners to get information of

various activities that are executed by their organisation. It provides data of costs, inventory,

customer's needs, appropriate pricing for product and different jobs that are performed according

to specification of clients. Management of Tesco use this system to keep a track record of each

action which is taken by organisation's staff and other members. Various types of management

accounting systems are used by managers of the company. These systems are as follows:

Cost accounting system: It is used by different kind of firms such as manufacturing,

retailing, distributing etc. to estimate actual costs that are involved in their production, supply

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

chain and distribution activities. In Tesco this system is used by managers to determine all the

costs that are related to their products. Estimating accurate costs can lead an organisation toward

success and helps to increase profitability by deciding accurate prices for products (Suomala,

Lyly-Yrjänäinen and Lukka, 2014). There are three different costing systems that are used by

organisations. Standard costing, which is used to determine difference between budgeted and

actual cost of products. Actual costing, is utilised to record actual costs of labour, material and

overheads that are incurred at the time of manufacturing. Normal costing, is used to allot costs

to products and it is based on actual data. In Tesco standard costing method is adopted by

managers to analyse variation in standard and real cost. It is very important for the organisation

because it helps to determine exact costs of products.

Price optimization system: When a company is using price optimisation strategies this

system can help to analyse customer's reaction toward the same. Managers of Tesco use price

optimisation system to set best price for their products which can help to achieve organisational

goals such as customer satisfaction and profit maximisation. It facilitates managers or marketers

of Tesco to determine customer's willingness to pay for products and decide prices accordingly

which can help to attract maximum customers. It is beneficial for the organisation as it guides to

set that price for products which can create urge in customers to buy products.

Job costing system: It is a system which is used to analyse costs of different jobs or

activities that are executed in bulk or according to customer's specification (Soin and Collier,

2013). Managers of Tesco use this system to determine cost of labour and overheads which is

involved in their products. It also assists to ascertain cost of distribution and supply chain, which

is used to set appropriate prices for products of Tesco. Job costing system is advantageous for the

organisation as it can help to get idea of accurate costs that are involved in different jobs.

Inventory management system: In large organisations this system is used to keep a

track record of different inventories. It help managers to track inventory of a company when it

goes out or taken in. It include ordering, storing and using inventory which is going to be used

for different business activities such as distribution and others. In Tesco inventory management

system is used to keep detailed information of stock whether it is in warehouses or any other

places. There are three different types of this system that are LIFO, in which recently received

inventory is used for sale first. FIFO, in which earlier received goods are used by companies to

sale first. AVCO, in this system stock is used on average basis for sale. In Tesco FIFO system is

2

costs that are related to their products. Estimating accurate costs can lead an organisation toward

success and helps to increase profitability by deciding accurate prices for products (Suomala,

Lyly-Yrjänäinen and Lukka, 2014). There are three different costing systems that are used by

organisations. Standard costing, which is used to determine difference between budgeted and

actual cost of products. Actual costing, is utilised to record actual costs of labour, material and

overheads that are incurred at the time of manufacturing. Normal costing, is used to allot costs

to products and it is based on actual data. In Tesco standard costing method is adopted by

managers to analyse variation in standard and real cost. It is very important for the organisation

because it helps to determine exact costs of products.

Price optimization system: When a company is using price optimisation strategies this

system can help to analyse customer's reaction toward the same. Managers of Tesco use price

optimisation system to set best price for their products which can help to achieve organisational

goals such as customer satisfaction and profit maximisation. It facilitates managers or marketers

of Tesco to determine customer's willingness to pay for products and decide prices accordingly

which can help to attract maximum customers. It is beneficial for the organisation as it guides to

set that price for products which can create urge in customers to buy products.

Job costing system: It is a system which is used to analyse costs of different jobs or

activities that are executed in bulk or according to customer's specification (Soin and Collier,

2013). Managers of Tesco use this system to determine cost of labour and overheads which is

involved in their products. It also assists to ascertain cost of distribution and supply chain, which

is used to set appropriate prices for products of Tesco. Job costing system is advantageous for the

organisation as it can help to get idea of accurate costs that are involved in different jobs.

Inventory management system: In large organisations this system is used to keep a

track record of different inventories. It help managers to track inventory of a company when it

goes out or taken in. It include ordering, storing and using inventory which is going to be used

for different business activities such as distribution and others. In Tesco inventory management

system is used to keep detailed information of stock whether it is in warehouses or any other

places. There are three different types of this system that are LIFO, in which recently received

inventory is used for sale first. FIFO, in which earlier received goods are used by companies to

sale first. AVCO, in this system stock is used on average basis for sale. In Tesco FIFO system is

2

followed by managers as it is very important for the company because it helps to maintain all the

information of goods.

P2 Management accounting reporting

Management accounting reporting: In every organisation some reports are generated to

record information of various business activities to analyse business performance and its ability

to maximize profits in coming years. It helps internal stakeholders to determine position of

company in market (Richardson, 2012). Tesco is a retail company, which is a large organisation

hence, it is very important for managers to create management accounting reports which can

assist owners and managers while formulating strategies to attain organisational goals. Process of

recording information is called reporting. Such reports also help to make decision to increase

profitability and enhance productivity by gathering information of different departments of the

company. Following reports are generated by managers of Tesco:

Performance report: In an organisation performance evaluation is very important

whether it is for individuals, whole organisation or activities and such reports helps to evaluate

performance of all of them. These reports help managers to evaluate presentation of employees

and than provide them rewards to motivate them to perform their duties more effectively. In

Tesco it is created to evaluate performance of whole organisation to make strategic decision that

can helps to enhance the quality of executional activities. It is very important as it can provide

deep insight into working activities of an organisation.

Inventory management report: The companies who are maintaining inventories on

regular basis, such reports are generated there to record each activity. Managers of an

organisation try to make higher profits by supplying goods on time to clients but it is not easy

because managing inventory accurately is a complex task. Such reports facilitate s the work of

managers by providing them transparent information of stocks. In Tesco this report is created to

reduce faults in distribution chain by keeping detailed data of goods that are supplied to different

clients. Inventory management reports are very important to generate because it helps to compare

different supply chains of the organisation.

Account receivable report: A company who is providing goods to its clients on credit

should create this report because it provides information of exact outstanding amount of different

clients. It is tool which is used to manage cash flow of an organisation. As Tesco is a large

company hence it is essential for managers to generate account receivables reports, in which

3

information of goods.

P2 Management accounting reporting

Management accounting reporting: In every organisation some reports are generated to

record information of various business activities to analyse business performance and its ability

to maximize profits in coming years. It helps internal stakeholders to determine position of

company in market (Richardson, 2012). Tesco is a retail company, which is a large organisation

hence, it is very important for managers to create management accounting reports which can

assist owners and managers while formulating strategies to attain organisational goals. Process of

recording information is called reporting. Such reports also help to make decision to increase

profitability and enhance productivity by gathering information of different departments of the

company. Following reports are generated by managers of Tesco:

Performance report: In an organisation performance evaluation is very important

whether it is for individuals, whole organisation or activities and such reports helps to evaluate

performance of all of them. These reports help managers to evaluate presentation of employees

and than provide them rewards to motivate them to perform their duties more effectively. In

Tesco it is created to evaluate performance of whole organisation to make strategic decision that

can helps to enhance the quality of executional activities. It is very important as it can provide

deep insight into working activities of an organisation.

Inventory management report: The companies who are maintaining inventories on

regular basis, such reports are generated there to record each activity. Managers of an

organisation try to make higher profits by supplying goods on time to clients but it is not easy

because managing inventory accurately is a complex task. Such reports facilitate s the work of

managers by providing them transparent information of stocks. In Tesco this report is created to

reduce faults in distribution chain by keeping detailed data of goods that are supplied to different

clients. Inventory management reports are very important to generate because it helps to compare

different supply chains of the organisation.

Account receivable report: A company who is providing goods to its clients on credit

should create this report because it provides information of exact outstanding amount of different

clients. It is tool which is used to manage cash flow of an organisation. As Tesco is a large

company hence it is essential for managers to generate account receivables reports, in which

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

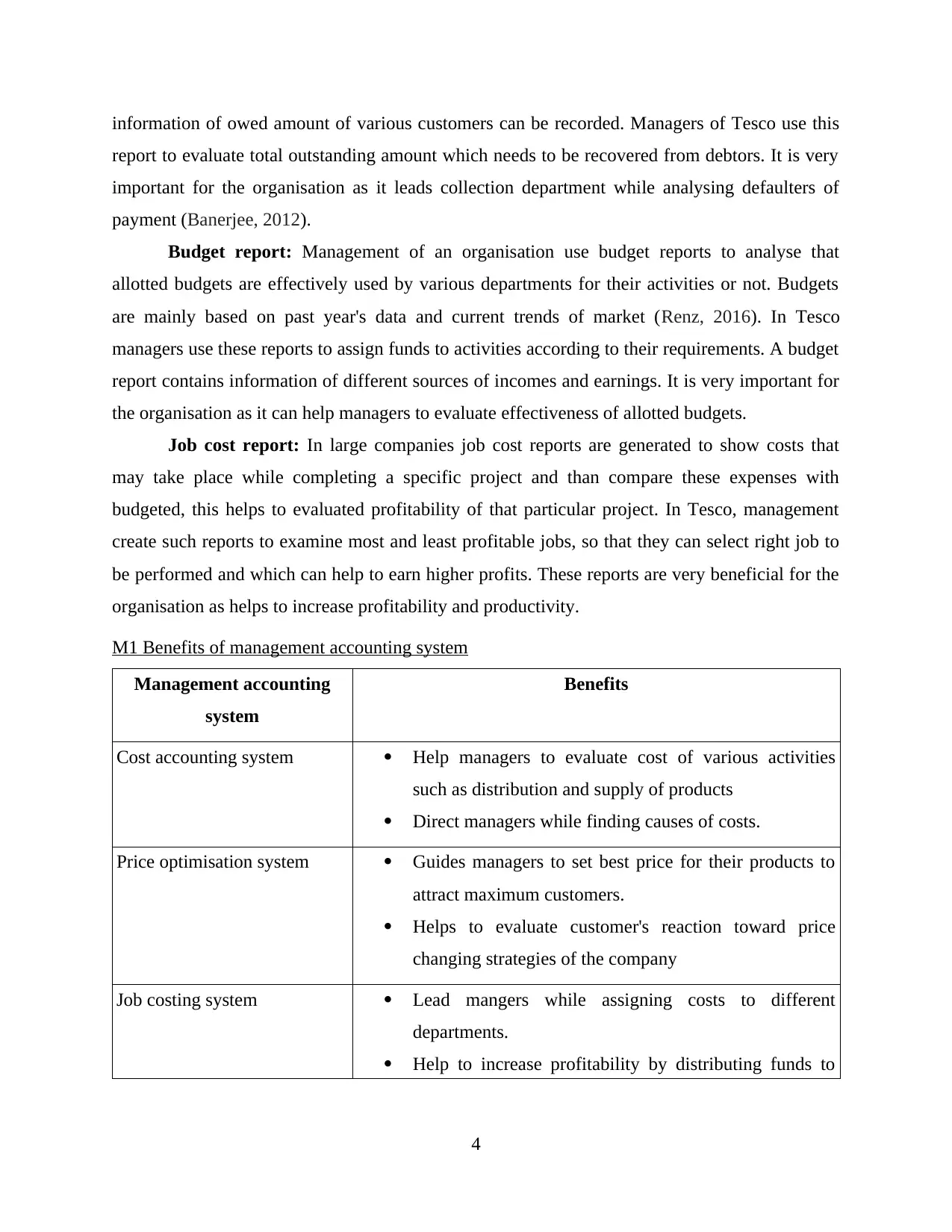

information of owed amount of various customers can be recorded. Managers of Tesco use this

report to evaluate total outstanding amount which needs to be recovered from debtors. It is very

important for the organisation as it leads collection department while analysing defaulters of

payment (Banerjee, 2012).

Budget report: Management of an organisation use budget reports to analyse that

allotted budgets are effectively used by various departments for their activities or not. Budgets

are mainly based on past year's data and current trends of market (Renz, 2016). In Tesco

managers use these reports to assign funds to activities according to their requirements. A budget

report contains information of different sources of incomes and earnings. It is very important for

the organisation as it can help managers to evaluate effectiveness of allotted budgets.

Job cost report: In large companies job cost reports are generated to show costs that

may take place while completing a specific project and than compare these expenses with

budgeted, this helps to evaluated profitability of that particular project. In Tesco, management

create such reports to examine most and least profitable jobs, so that they can select right job to

be performed and which can help to earn higher profits. These reports are very beneficial for the

organisation as helps to increase profitability and productivity.

M1 Benefits of management accounting system

Management accounting

system

Benefits

Cost accounting system Help managers to evaluate cost of various activities

such as distribution and supply of products

Direct managers while finding causes of costs.

Price optimisation system Guides managers to set best price for their products to

attract maximum customers.

Helps to evaluate customer's reaction toward price

changing strategies of the company

Job costing system Lead mangers while assigning costs to different

departments.

Help to increase profitability by distributing funds to

4

report to evaluate total outstanding amount which needs to be recovered from debtors. It is very

important for the organisation as it leads collection department while analysing defaulters of

payment (Banerjee, 2012).

Budget report: Management of an organisation use budget reports to analyse that

allotted budgets are effectively used by various departments for their activities or not. Budgets

are mainly based on past year's data and current trends of market (Renz, 2016). In Tesco

managers use these reports to assign funds to activities according to their requirements. A budget

report contains information of different sources of incomes and earnings. It is very important for

the organisation as it can help managers to evaluate effectiveness of allotted budgets.

Job cost report: In large companies job cost reports are generated to show costs that

may take place while completing a specific project and than compare these expenses with

budgeted, this helps to evaluated profitability of that particular project. In Tesco, management

create such reports to examine most and least profitable jobs, so that they can select right job to

be performed and which can help to earn higher profits. These reports are very beneficial for the

organisation as helps to increase profitability and productivity.

M1 Benefits of management accounting system

Management accounting

system

Benefits

Cost accounting system Help managers to evaluate cost of various activities

such as distribution and supply of products

Direct managers while finding causes of costs.

Price optimisation system Guides managers to set best price for their products to

attract maximum customers.

Helps to evaluate customer's reaction toward price

changing strategies of the company

Job costing system Lead mangers while assigning costs to different

departments.

Help to increase profitability by distributing funds to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

activities according to their requirement.

Inventory management system Help to improve accuracy on different inventory orders.

Increase the level of transparent information by keeping

record of every activity.

D1 Management accounting system and its reports are integrated with organisational process

Management accounting system and its reports help internal stakeholder to evaluate

performance of business of Tesco. Managers take decisions to attain organisational goals by

analysing information which is recorded in different reports. Accounts receivable reports provide

information of actual owed amount by various clients and direct managers to tighten credit

policies so that it will reduce outstanding amount. Inventory management reports guides

managers to maintain supply chain effectively and identify areas where modifications is required

to improve profitability of organisation. Performance report are generated by management to

evaluate effectiveness of performing different activities. Cost accounting system can help

managers to determine actual costs of their products and job costing system helps to assign costs

to different activities according to their requirements.

TASK 2

P3 Appropriate costing technique

Cost: It is a monetary value of different expenses that are involved in the manufacturing

of a products. It includes direct labour, material and overheads. It is an amount which has to be

paid by the buyer to the seller of product (Parker, 2012). There are three different types of costs

fixed, variable and semi variable. Fixed costs are the costs that does not change with the

production, variable costs change with the production if units produced increases than variable

cost will also increase, semi variable costs are those costs that are partially fixed and partially

variable.

As Tesco is a retail company, so there manufacturing costs are not applicable here but

distribution costs are considered for the company. It is suggested to the mangers to set

appropriate cost for their products because before buying product customer will always try to

figure out actual cost of that particular product.

(a) Calculation of the average production costs and marginal cost per unit is,

Average production cost per unit = total cost of production/total actual production units

5

Inventory management system Help to improve accuracy on different inventory orders.

Increase the level of transparent information by keeping

record of every activity.

D1 Management accounting system and its reports are integrated with organisational process

Management accounting system and its reports help internal stakeholder to evaluate

performance of business of Tesco. Managers take decisions to attain organisational goals by

analysing information which is recorded in different reports. Accounts receivable reports provide

information of actual owed amount by various clients and direct managers to tighten credit

policies so that it will reduce outstanding amount. Inventory management reports guides

managers to maintain supply chain effectively and identify areas where modifications is required

to improve profitability of organisation. Performance report are generated by management to

evaluate effectiveness of performing different activities. Cost accounting system can help

managers to determine actual costs of their products and job costing system helps to assign costs

to different activities according to their requirements.

TASK 2

P3 Appropriate costing technique

Cost: It is a monetary value of different expenses that are involved in the manufacturing

of a products. It includes direct labour, material and overheads. It is an amount which has to be

paid by the buyer to the seller of product (Parker, 2012). There are three different types of costs

fixed, variable and semi variable. Fixed costs are the costs that does not change with the

production, variable costs change with the production if units produced increases than variable

cost will also increase, semi variable costs are those costs that are partially fixed and partially

variable.

As Tesco is a retail company, so there manufacturing costs are not applicable here but

distribution costs are considered for the company. It is suggested to the mangers to set

appropriate cost for their products because before buying product customer will always try to

figure out actual cost of that particular product.

(a) Calculation of the average production costs and marginal cost per unit is,

Average production cost per unit = total cost of production/total actual production units

5

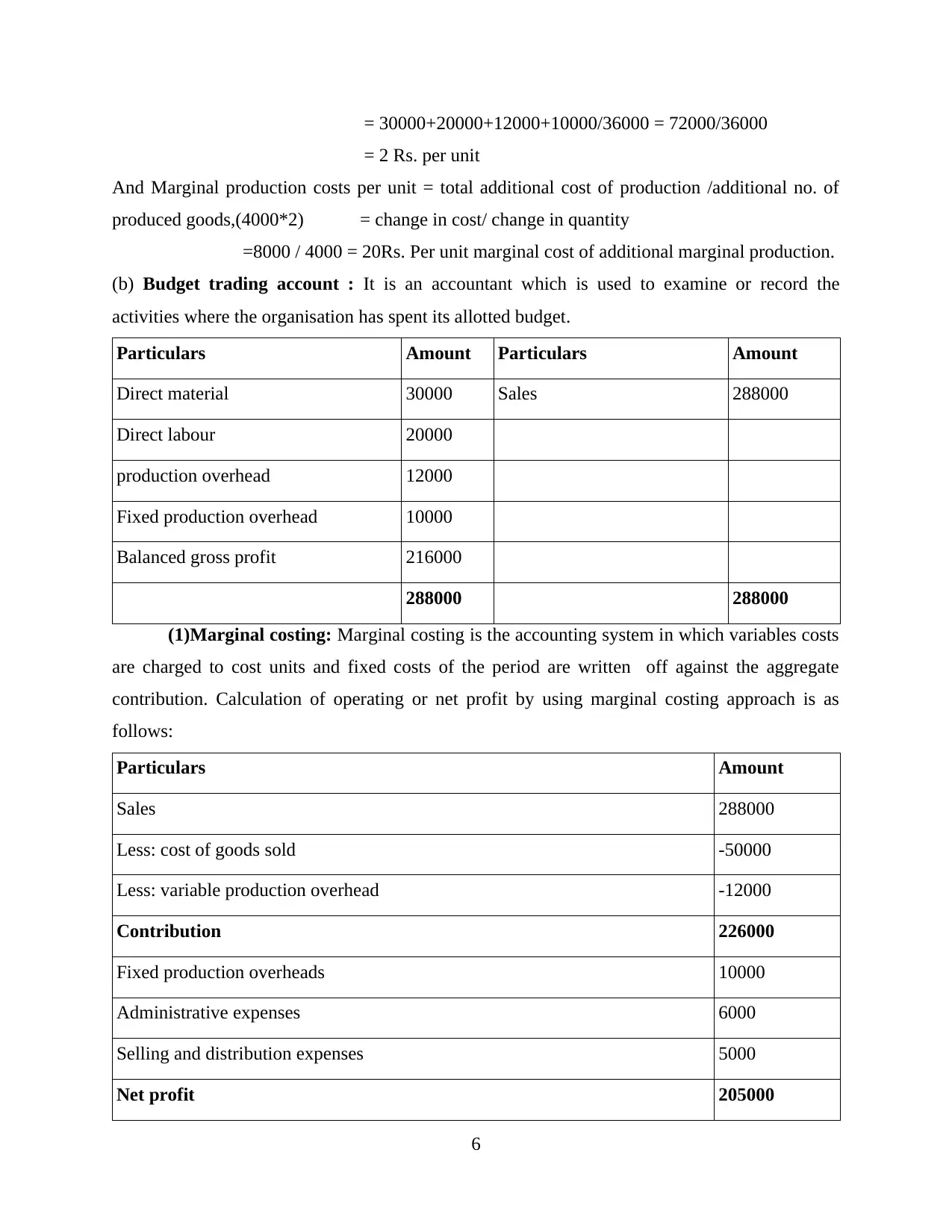

= 30000+20000+12000+10000/36000 = 72000/36000

= 2 Rs. per unit

And Marginal production costs per unit = total additional cost of production /additional no. of

produced goods,(4000*2) = change in cost/ change in quantity

=8000 / 4000 = 20Rs. Per unit marginal cost of additional marginal production.

(b) Budget trading account : It is an accountant which is used to examine or record the

activities where the organisation has spent its allotted budget.

Particulars Amount Particulars Amount

Direct material 30000 Sales 288000

Direct labour 20000

production overhead 12000

Fixed production overhead 10000

Balanced gross profit 216000

288000 288000

(1)Marginal costing: Marginal costing is the accounting system in which variables costs

are charged to cost units and fixed costs of the period are written off against the aggregate

contribution. Calculation of operating or net profit by using marginal costing approach is as

follows:

Particulars Amount

Sales 288000

Less: cost of goods sold -50000

Less: variable production overhead -12000

Contribution 226000

Fixed production overheads 10000

Administrative expenses 6000

Selling and distribution expenses 5000

Net profit 205000

6

= 2 Rs. per unit

And Marginal production costs per unit = total additional cost of production /additional no. of

produced goods,(4000*2) = change in cost/ change in quantity

=8000 / 4000 = 20Rs. Per unit marginal cost of additional marginal production.

(b) Budget trading account : It is an accountant which is used to examine or record the

activities where the organisation has spent its allotted budget.

Particulars Amount Particulars Amount

Direct material 30000 Sales 288000

Direct labour 20000

production overhead 12000

Fixed production overhead 10000

Balanced gross profit 216000

288000 288000

(1)Marginal costing: Marginal costing is the accounting system in which variables costs

are charged to cost units and fixed costs of the period are written off against the aggregate

contribution. Calculation of operating or net profit by using marginal costing approach is as

follows:

Particulars Amount

Sales 288000

Less: cost of goods sold -50000

Less: variable production overhead -12000

Contribution 226000

Fixed production overheads 10000

Administrative expenses 6000

Selling and distribution expenses 5000

Net profit 205000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

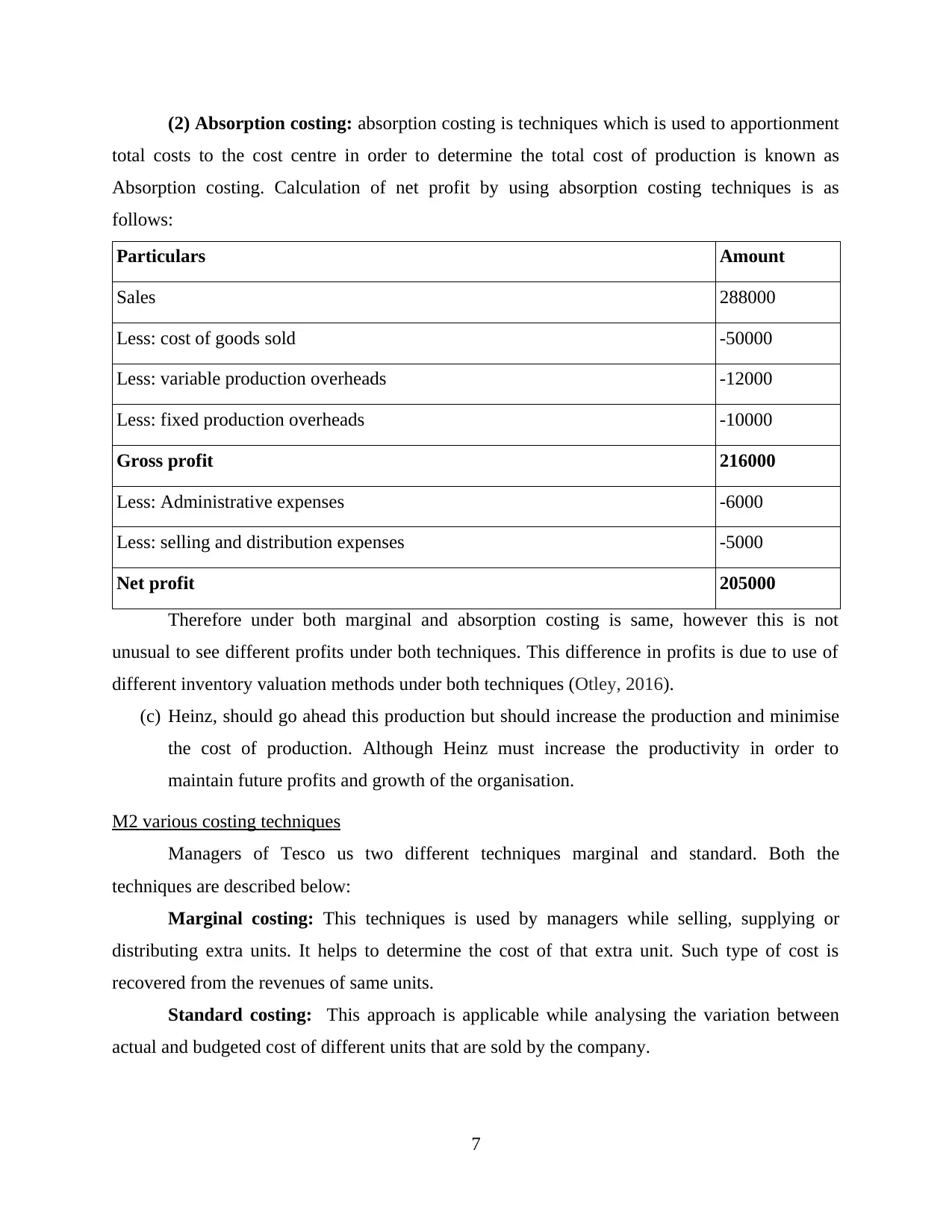

(2) Absorption costing: absorption costing is techniques which is used to apportionment

total costs to the cost centre in order to determine the total cost of production is known as

Absorption costing. Calculation of net profit by using absorption costing techniques is as

follows:

Particulars Amount

Sales 288000

Less: cost of goods sold -50000

Less: variable production overheads -12000

Less: fixed production overheads -10000

Gross profit 216000

Less: Administrative expenses -6000

Less: selling and distribution expenses -5000

Net profit 205000

Therefore under both marginal and absorption costing is same, however this is not

unusual to see different profits under both techniques. This difference in profits is due to use of

different inventory valuation methods under both techniques (Otley, 2016).

(c) Heinz, should go ahead this production but should increase the production and minimise

the cost of production. Although Heinz must increase the productivity in order to

maintain future profits and growth of the organisation.

M2 various costing techniques

Managers of Tesco us two different techniques marginal and standard. Both the

techniques are described below:

Marginal costing: This techniques is used by managers while selling, supplying or

distributing extra units. It helps to determine the cost of that extra unit. Such type of cost is

recovered from the revenues of same units.

Standard costing: This approach is applicable while analysing the variation between

actual and budgeted cost of different units that are sold by the company.

7

total costs to the cost centre in order to determine the total cost of production is known as

Absorption costing. Calculation of net profit by using absorption costing techniques is as

follows:

Particulars Amount

Sales 288000

Less: cost of goods sold -50000

Less: variable production overheads -12000

Less: fixed production overheads -10000

Gross profit 216000

Less: Administrative expenses -6000

Less: selling and distribution expenses -5000

Net profit 205000

Therefore under both marginal and absorption costing is same, however this is not

unusual to see different profits under both techniques. This difference in profits is due to use of

different inventory valuation methods under both techniques (Otley, 2016).

(c) Heinz, should go ahead this production but should increase the production and minimise

the cost of production. Although Heinz must increase the productivity in order to

maintain future profits and growth of the organisation.

M2 various costing techniques

Managers of Tesco us two different techniques marginal and standard. Both the

techniques are described below:

Marginal costing: This techniques is used by managers while selling, supplying or

distributing extra units. It helps to determine the cost of that extra unit. Such type of cost is

recovered from the revenues of same units.

Standard costing: This approach is applicable while analysing the variation between

actual and budgeted cost of different units that are sold by the company.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D2 Data interpretation

From the above calculation it has been analysed that total gross profit of budget trading

account is 216000. The mangers of Tesco has used two different techniques to calculate net

profits that are marginal and absorption costing. While using marginal costing it has resulted

205000 as net profits. While using absorption costing it has resulted 205000 as net profits. The

company can choose any of these techniques as both have resulted the same.

TASK 3

P4 Advantages and disadvantages of planning tools used in budgetary control

Budget and budgetary control: Budget is the estimation of revenues and expenses over

a specified period of time. Moreover it is a financial plan for a specified period usually a year. It

is sum of money allocated for a particular purpose and the summary of intended expenditures

along with proposals for how to accomplish them. Budgetary control is the process of controlling

and managing budgets in an effective way. It helps managers to allot budgets to different

activities according to their requirements (Lavia López and Hiebl, 2014). In Tesco it is

implemented to plan and forecast budgets. Planning tool are used in budgetary control to help the

management in its attempts to cope with the uncertainty of the future, relying mainly on data

from the past and present and analysis of trends. There are three planning tools that are used by

the managers of company:

Forecasting tools: it means a predictions about the future. Moreover it is a systematic

analysis to make predictions about what will happen in future. There are two types of forecasting

techniques long term forecasting and short term forecasting (Chenhall and Moers, 2015). Tesco

use short term forecasting while creating budgets and estimating expenses. Long term

forecasting pertains both quantitative and qualitative data and based on experts advice and

opinions and insights. Following are the advantages and disadvantages of forecasting tools.

Advantages Disadvantages

It provides the business with valuable

information that it provides the business with

valuable information that the business can use

to make decisions about future.

It is based on future predictions, as no one can

absolutely predict the exactly.

It helps in saving the staffing costs and Any unforeseen factors can render a forecast

8

From the above calculation it has been analysed that total gross profit of budget trading

account is 216000. The mangers of Tesco has used two different techniques to calculate net

profits that are marginal and absorption costing. While using marginal costing it has resulted

205000 as net profits. While using absorption costing it has resulted 205000 as net profits. The

company can choose any of these techniques as both have resulted the same.

TASK 3

P4 Advantages and disadvantages of planning tools used in budgetary control

Budget and budgetary control: Budget is the estimation of revenues and expenses over

a specified period of time. Moreover it is a financial plan for a specified period usually a year. It

is sum of money allocated for a particular purpose and the summary of intended expenditures

along with proposals for how to accomplish them. Budgetary control is the process of controlling

and managing budgets in an effective way. It helps managers to allot budgets to different

activities according to their requirements (Lavia López and Hiebl, 2014). In Tesco it is

implemented to plan and forecast budgets. Planning tool are used in budgetary control to help the

management in its attempts to cope with the uncertainty of the future, relying mainly on data

from the past and present and analysis of trends. There are three planning tools that are used by

the managers of company:

Forecasting tools: it means a predictions about the future. Moreover it is a systematic

analysis to make predictions about what will happen in future. There are two types of forecasting

techniques long term forecasting and short term forecasting (Chenhall and Moers, 2015). Tesco

use short term forecasting while creating budgets and estimating expenses. Long term

forecasting pertains both quantitative and qualitative data and based on experts advice and

opinions and insights. Following are the advantages and disadvantages of forecasting tools.

Advantages Disadvantages

It provides the business with valuable

information that it provides the business with

valuable information that the business can use

to make decisions about future.

It is based on future predictions, as no one can

absolutely predict the exactly.

It helps in saving the staffing costs and Any unforeseen factors can render a forecast

8

reducing inventory costs. useless, regardless of the quality of data.

It helps the company in focusing about the

future predictions continuously.

Forecasting methods may use same data but

deliver different forecasts.

Contingency tools: These tools are mainly concerned with the estimation of

unfavourable or negative events that may take place. It also guides managers to make plan to

deal with such type of events. In Tesco such tools are used by managers to identify possible

future consequences and make strategies to resolve them. Following are the advantages and

disadvantages of contingency tools:

Advantages Disadvantages

Help managers to get an idea of possible

negative or unfavourable events.

Cost and time involved in the implementation

process of such tools is very high.

Guides companies to be prepare to deal with

various consequences that can occur.

These tools are very complex to understand so

the company has to train employees before

executing tools.

It also help managers to identify errors in

distribution system to increase effectiveness.

The nature of this tool is reactive not proactive

which means it can only guide at the time of

risk or uncertainty.

Scenario tools: It is making assumptions on what the future will be and how the business

environment will change. Moreover, it is identifying a specific set of uncertainties, different what

might happen in future of business (Otley and Emmanuel, 2013). Some of advantages and

disadvantages of scenario planning are as follows:

Advantages Disadvantages

It may allow real insights and unlock

creativity.

It requires continuous and effective supervision

of managers which is not possible in some of

the organisations.

It allows for bushiness to think outside the box

or explore.

It can be used in long term planning it is not

suitable in short term planning.

It is an emerging method designed to energise Budget for implementing this tool is very high

9

It helps the company in focusing about the

future predictions continuously.

Forecasting methods may use same data but

deliver different forecasts.

Contingency tools: These tools are mainly concerned with the estimation of

unfavourable or negative events that may take place. It also guides managers to make plan to

deal with such type of events. In Tesco such tools are used by managers to identify possible

future consequences and make strategies to resolve them. Following are the advantages and

disadvantages of contingency tools:

Advantages Disadvantages

Help managers to get an idea of possible

negative or unfavourable events.

Cost and time involved in the implementation

process of such tools is very high.

Guides companies to be prepare to deal with

various consequences that can occur.

These tools are very complex to understand so

the company has to train employees before

executing tools.

It also help managers to identify errors in

distribution system to increase effectiveness.

The nature of this tool is reactive not proactive

which means it can only guide at the time of

risk or uncertainty.

Scenario tools: It is making assumptions on what the future will be and how the business

environment will change. Moreover, it is identifying a specific set of uncertainties, different what

might happen in future of business (Otley and Emmanuel, 2013). Some of advantages and

disadvantages of scenario planning are as follows:

Advantages Disadvantages

It may allow real insights and unlock

creativity.

It requires continuous and effective supervision

of managers which is not possible in some of

the organisations.

It allows for bushiness to think outside the box

or explore.

It can be used in long term planning it is not

suitable in short term planning.

It is an emerging method designed to energise Budget for implementing this tool is very high

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.