Financial Analysis of Tesco PLC (2015-2018): BA4008 Coursework

VerifiedAdded on 2022/10/17

|11

|2220

|441

Report

AI Summary

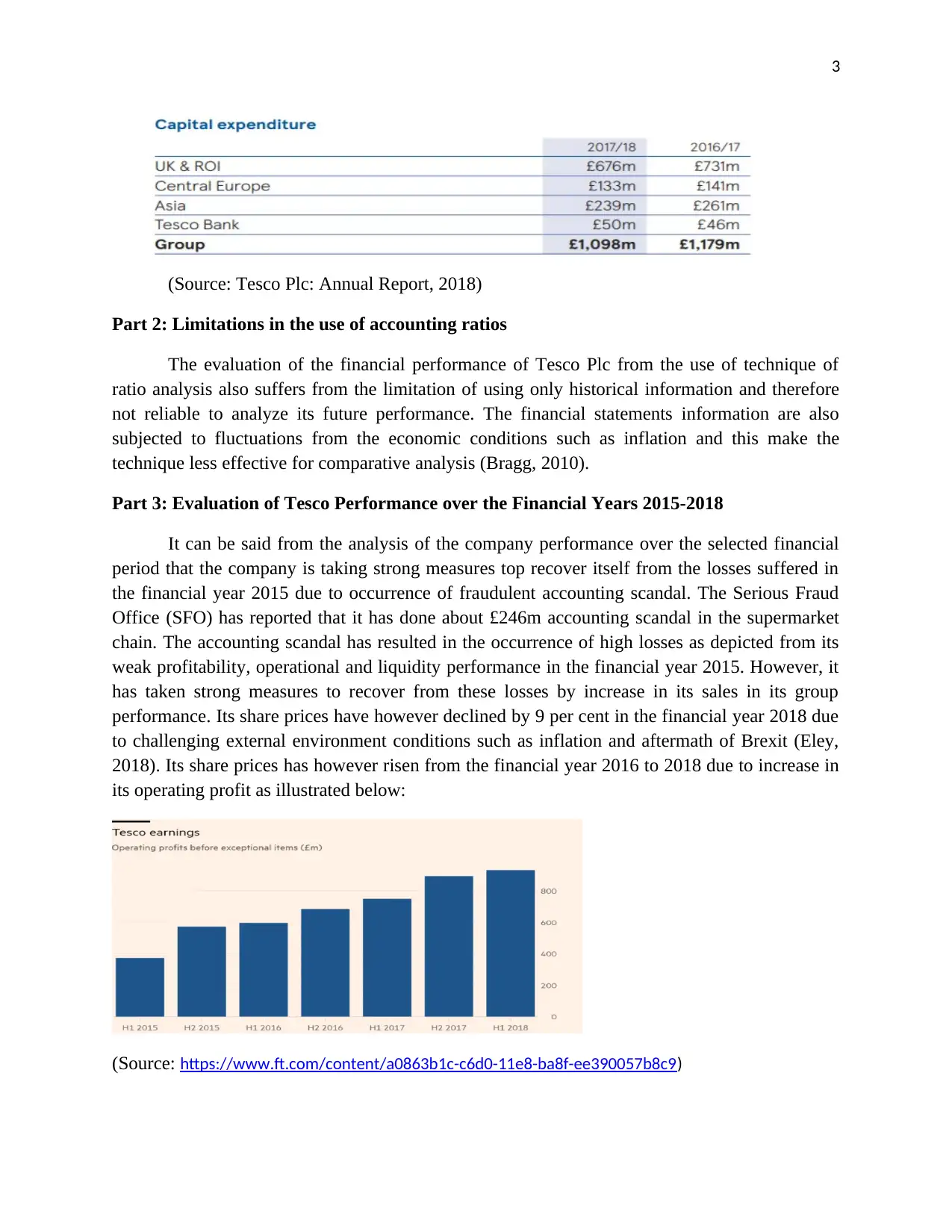

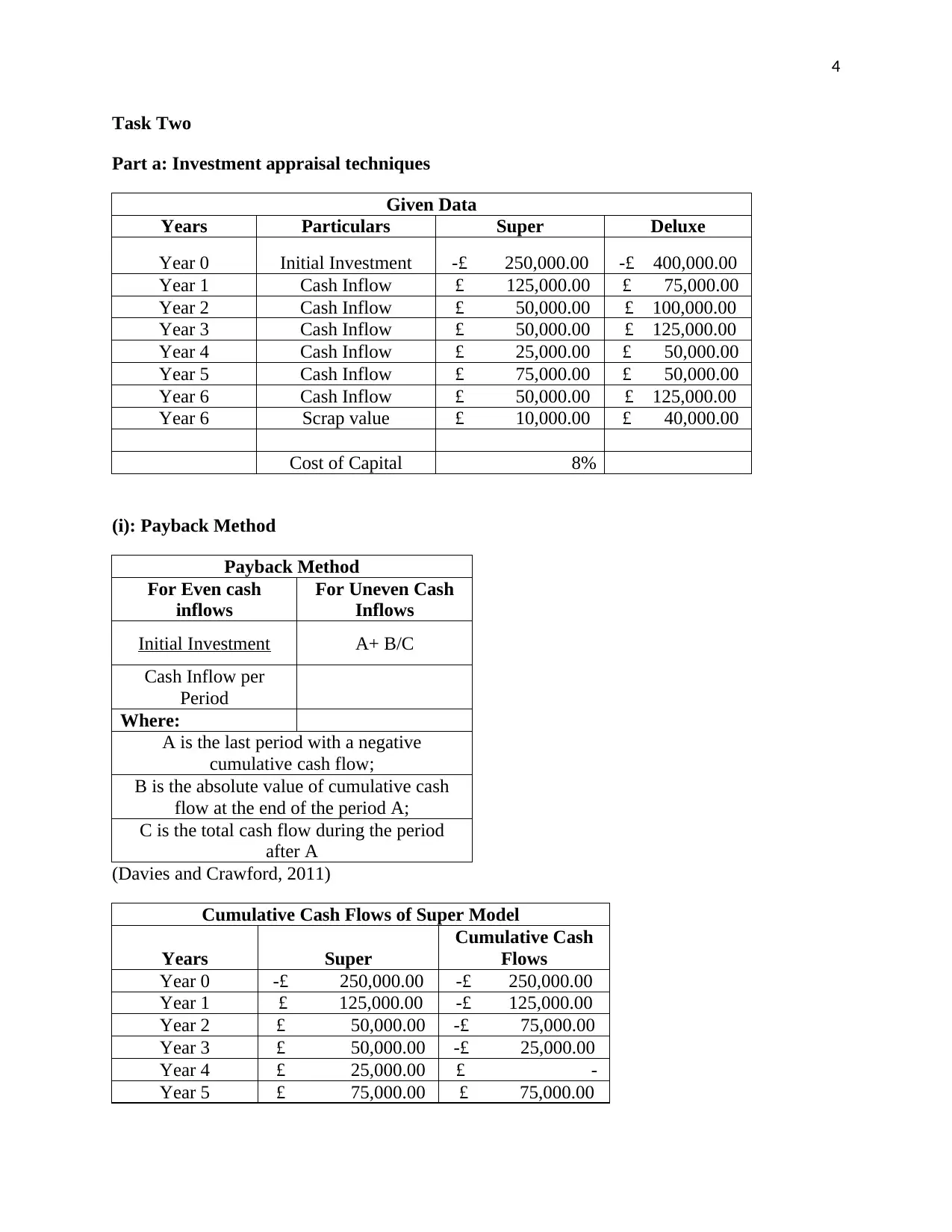

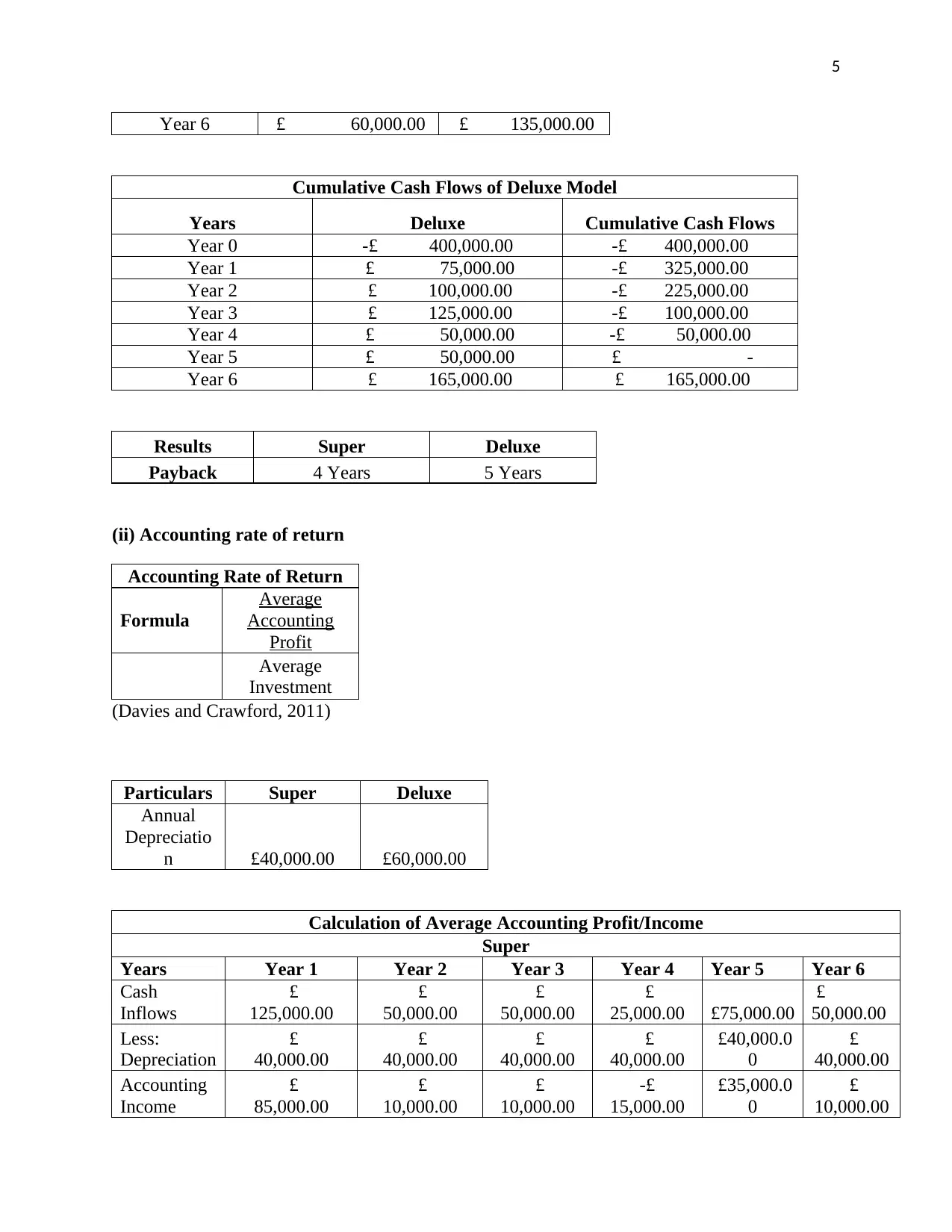

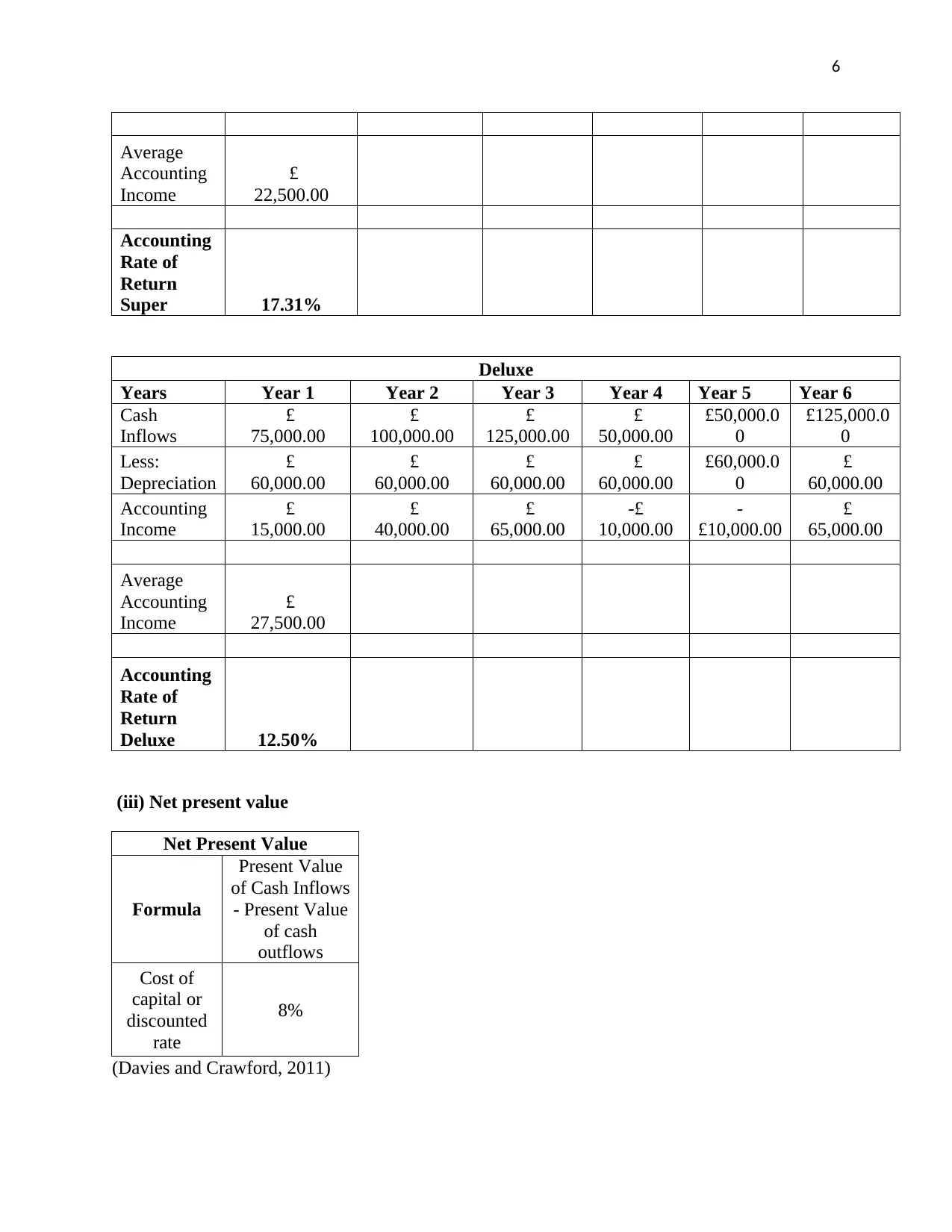

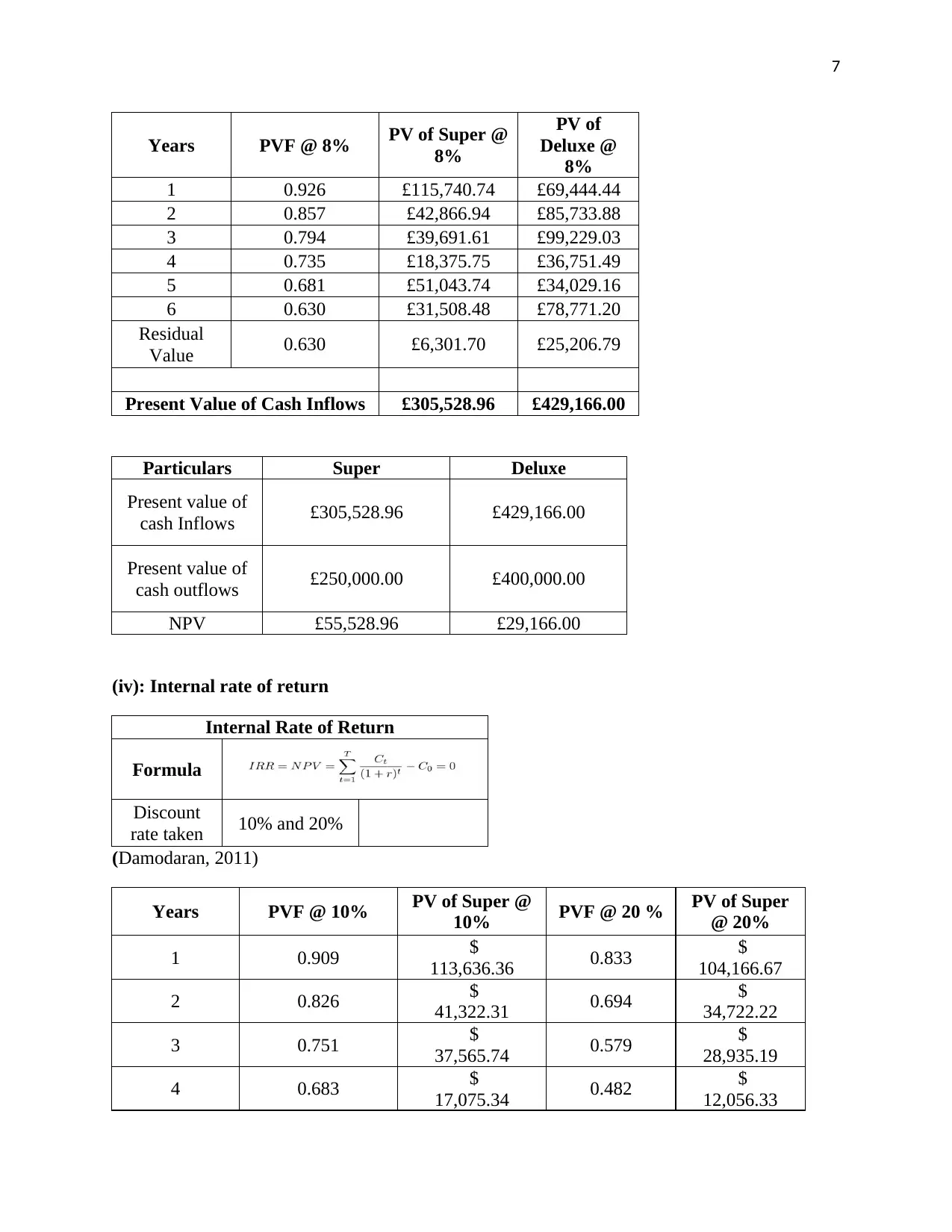

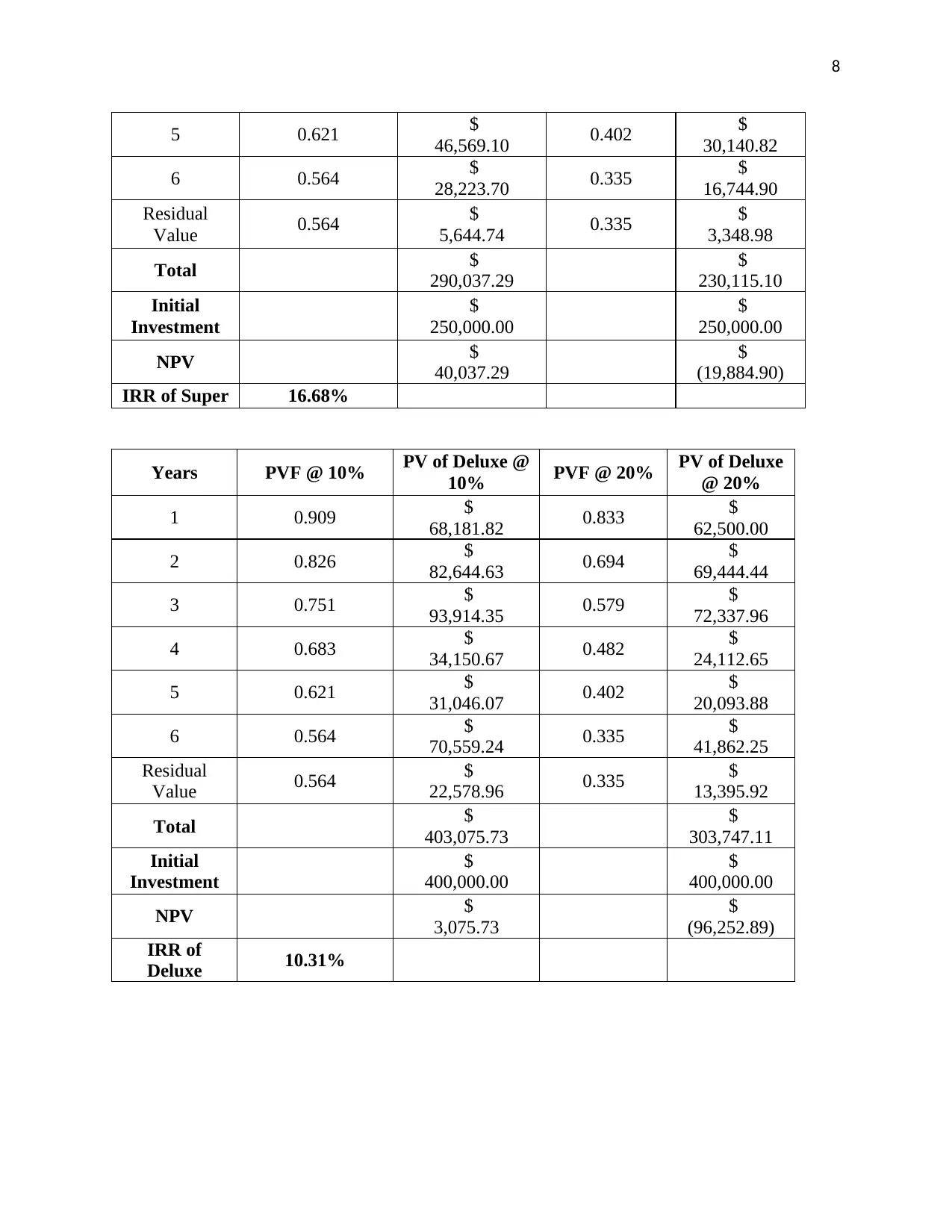

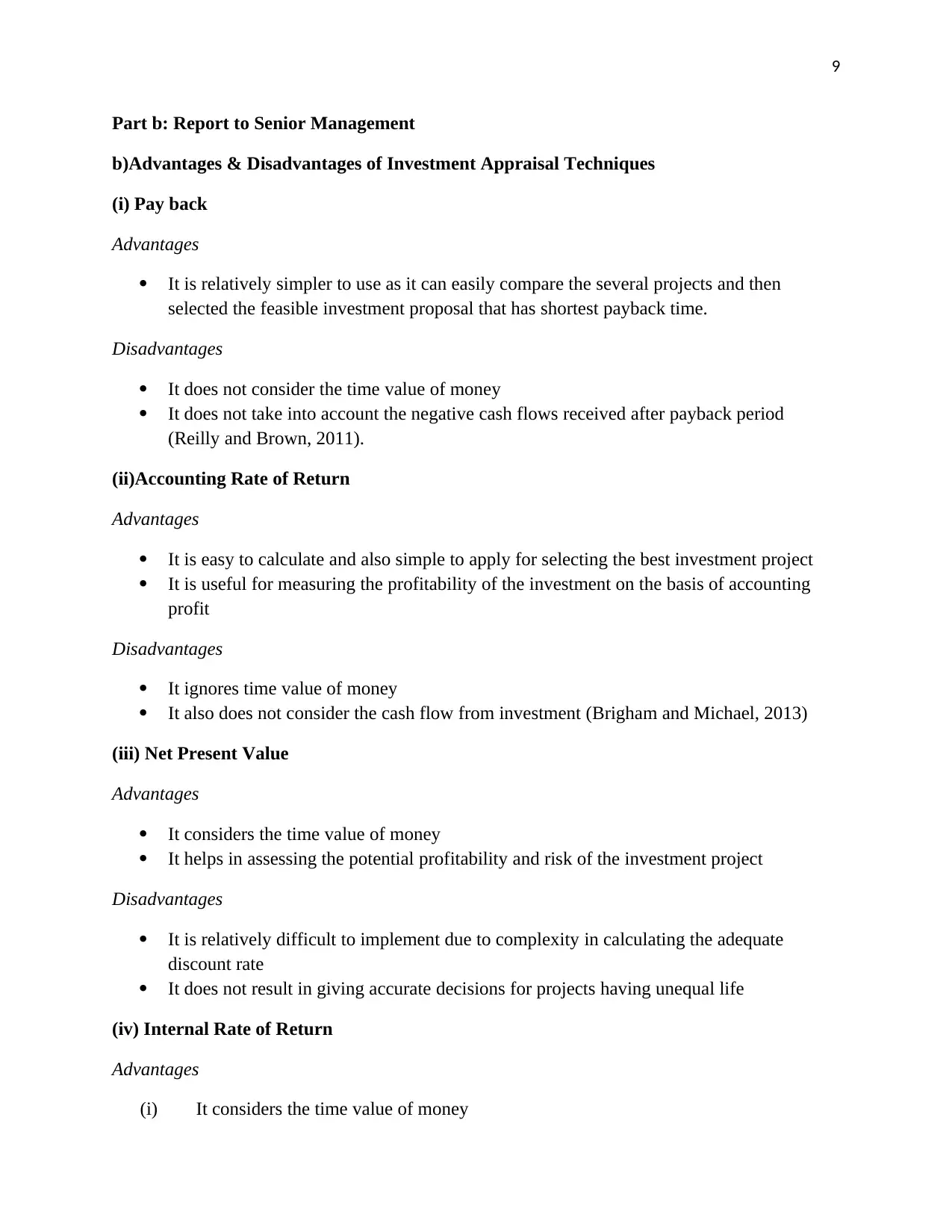

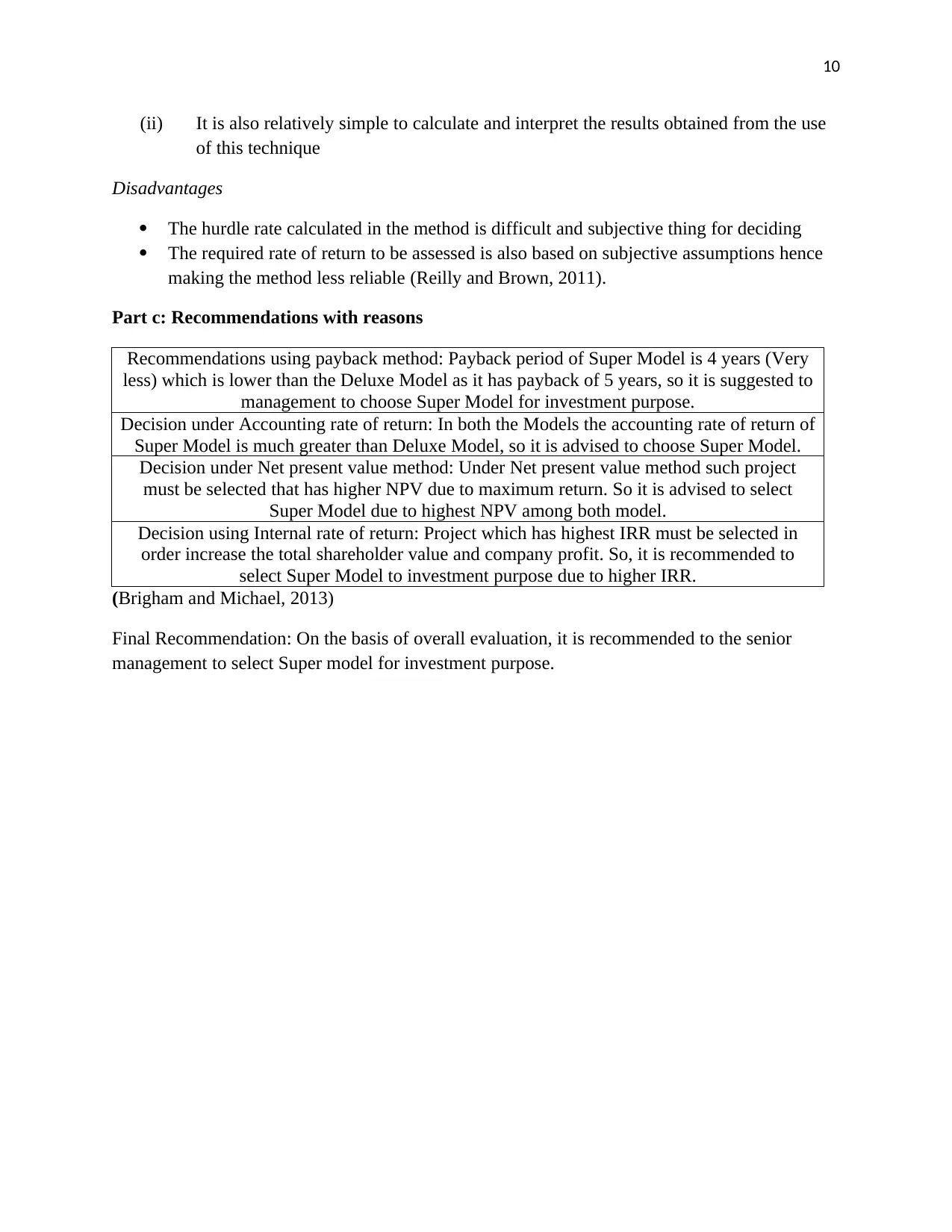

This report presents a comprehensive financial analysis of Tesco PLC over the period from 2015 to 2018, fulfilling the requirements of a BA4008 coursework assignment. The analysis begins with an evaluation of Tesco's performance, liquidity, and financial structure, utilizing key accounting ratios such as return on shareholders' funds, return on capital employed, and profit margins. The report examines the trends in these ratios, highlighting improvements in profitability and operational efficiency, while also acknowledging the impact of past accounting scandals and external economic factors. Furthermore, the report delves into investment appraisal techniques, including the payback method, accounting rate of return, net present value (NPV), and internal rate of return (IRR), to evaluate two investment models ('Super' and 'Deluxe'). The analysis calculates and compares the results of each method, providing recommendations to senior management regarding the selection of the most viable investment option. The report concludes with a summary of the advantages and disadvantages of each investment appraisal technique, justifying the final recommendation based on the overall evaluation and the specific context of Tesco's financial performance.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.