Accounting and Finance: MMBB08 Tesco PLC Financial Analysis Report

VerifiedAdded on 2022/08/24

|11

|2034

|19

Report

AI Summary

This report presents a comprehensive financial analysis of Tesco PLC, a major UK-based company. It delves into the company's financial position and performance over two years (2018 and 2019), employing ratio analysis to evaluate profitability, solvency, liquidity, and efficiency. The analysis includes calculations of net profit ratio, return on equity, debt-to-equity ratio, times interest coverage ratio, current ratio, quick ratio, total asset turnover, and days receivable outstanding. The report compares Tesco's performance to industry standards and assesses its potential as a good investment, considering both strengths and weaknesses. It also acknowledges the limitations of the analysis, such as reliance on past data and potential accounting policy changes. The report concludes with a summary of findings and investment recommendations.

Running Head: TESCO PLC ANALYSIS 1

TESCO PLC ANALYSIS

TESCO PLC ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: TESCO PLC ANALYSIS

Table of Contents

Tesco Introduction...........................................................................................................................3

Financial position and Analysis.......................................................................................................3

Good investment or not...................................................................................................................3

Limitations of Analysis....................................................................................................................3

References........................................................................................................................................4

Table of Contents

Tesco Introduction...........................................................................................................................3

Financial position and Analysis.......................................................................................................3

Good investment or not...................................................................................................................3

Limitations of Analysis....................................................................................................................3

References........................................................................................................................................4

Running Head: TESCO PLC ANALYSIS

Tesco Introduction

The most renowned company situated in Welwyn Garden City, Hertfordshire and belongs to

British arena; Tesco Plc has been discussed in this report. Founded in the year 1919, 100 years

ago, the company is engaged in the business of groceries and general merchandise. The current

operations of the company are in United Kingdom, Ireland, India, Malaysia, Thailand, Czech

Republic and Hungary. The company has almost 6800 shops operating having a current revenue

of £63911 million. The net profit being 1320 million for the financial year 2019 and this has

been achieved only with the help of 450000 employees. There are so many subsidiaries of the

company such as Tesco Ireland, Tesco Mobile, Dunnhumby. The key people associated with this

company are John Allan who is Chairperson and Dave Lewis who is CEO of the company.

Under this report a detailed financial analysis has been undertaken via implementing the ratio

analysis technique and at the same time to figure out whether it shall be a good investment or

not. Further, the limitations have also been listed in the report which have been found out and

stated.

Financial position and Analysis

The financial performance and valuation report on Telco Plc will cover the last two financial

years that is 2018 and 2019. In order to analyze the financial statements the company has chosen

the ratio analysis technique which will evaluate the company from all the aspects. These ratios

have been calculated and analyzed below in detail (Goldmann, 2017). The organization's

exhibition will likewise be contrasted with different firms inside the retail and discount industry

particularly contenders. Financial investigation figuring will be remembered for the reference

Tesco Introduction

The most renowned company situated in Welwyn Garden City, Hertfordshire and belongs to

British arena; Tesco Plc has been discussed in this report. Founded in the year 1919, 100 years

ago, the company is engaged in the business of groceries and general merchandise. The current

operations of the company are in United Kingdom, Ireland, India, Malaysia, Thailand, Czech

Republic and Hungary. The company has almost 6800 shops operating having a current revenue

of £63911 million. The net profit being 1320 million for the financial year 2019 and this has

been achieved only with the help of 450000 employees. There are so many subsidiaries of the

company such as Tesco Ireland, Tesco Mobile, Dunnhumby. The key people associated with this

company are John Allan who is Chairperson and Dave Lewis who is CEO of the company.

Under this report a detailed financial analysis has been undertaken via implementing the ratio

analysis technique and at the same time to figure out whether it shall be a good investment or

not. Further, the limitations have also been listed in the report which have been found out and

stated.

Financial position and Analysis

The financial performance and valuation report on Telco Plc will cover the last two financial

years that is 2018 and 2019. In order to analyze the financial statements the company has chosen

the ratio analysis technique which will evaluate the company from all the aspects. These ratios

have been calculated and analyzed below in detail (Goldmann, 2017). The organization's

exhibition will likewise be contrasted with different firms inside the retail and discount industry

particularly contenders. Financial investigation figuring will be remembered for the reference

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: TESCO PLC ANALYSIS

sections and some other data portrayal as diagrams. Estimations were finished utilizing

Microsoft Excel

Financial ratio Formula

Net profit (profit after tax / Net sales) * 100

Return on equity (profit after tax / equity) * 100

Current ratio current assets / current liabilities

Quick ratio (current assets – inventory) / current liabilities

Times interest coverage ratio (EBIT/ interest expense)

Debt ratio totals liabilities / total assets

Debt to equity ratio total liabilities / total equity

Total Asset turnover ratio Net sales/ Average total assets

Days receivable outstanding Accounts receivables *365 / Credit sales

Profitability

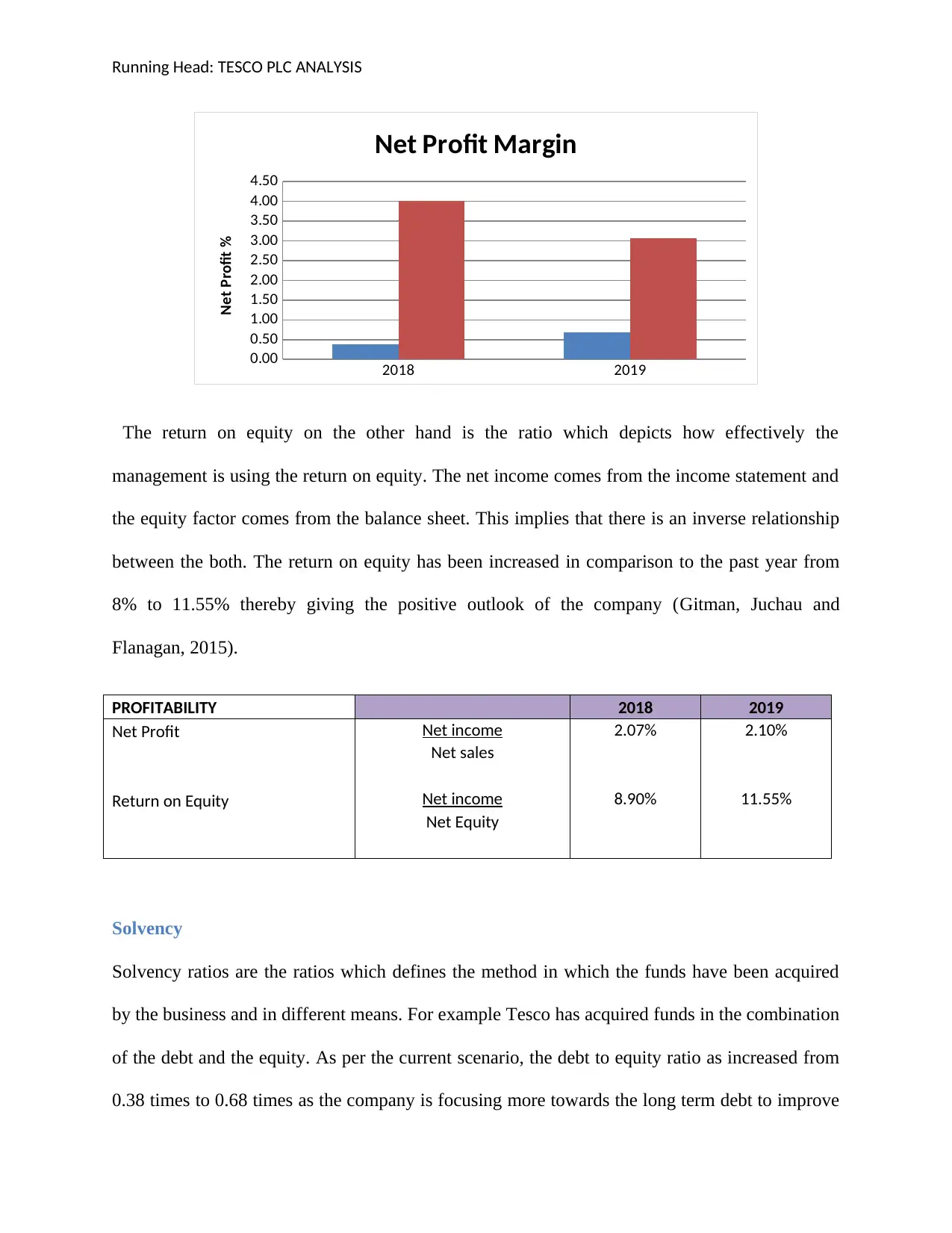

The profitability of any company can be analyzed with the help of calculating ratios such as net

profit ratio and return on equity ratios. The net profit is an important financial metric that is used

to analyze how profitable the business is and how much share will be available to the

shareholders as well as investors. The net profit ratio of Tesco PLC, is too low as it is 2.07% in

the year 2018 and the same was 2.10%. This indicates not much profit has been kept to distribute

to the shareholders.

sections and some other data portrayal as diagrams. Estimations were finished utilizing

Microsoft Excel

Financial ratio Formula

Net profit (profit after tax / Net sales) * 100

Return on equity (profit after tax / equity) * 100

Current ratio current assets / current liabilities

Quick ratio (current assets – inventory) / current liabilities

Times interest coverage ratio (EBIT/ interest expense)

Debt ratio totals liabilities / total assets

Debt to equity ratio total liabilities / total equity

Total Asset turnover ratio Net sales/ Average total assets

Days receivable outstanding Accounts receivables *365 / Credit sales

Profitability

The profitability of any company can be analyzed with the help of calculating ratios such as net

profit ratio and return on equity ratios. The net profit is an important financial metric that is used

to analyze how profitable the business is and how much share will be available to the

shareholders as well as investors. The net profit ratio of Tesco PLC, is too low as it is 2.07% in

the year 2018 and the same was 2.10%. This indicates not much profit has been kept to distribute

to the shareholders.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: TESCO PLC ANALYSIS

2018 2019

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Net Profit Margin

Net Profit %

The return on equity on the other hand is the ratio which depicts how effectively the

management is using the return on equity. The net income comes from the income statement and

the equity factor comes from the balance sheet. This implies that there is an inverse relationship

between the both. The return on equity has been increased in comparison to the past year from

8% to 11.55% thereby giving the positive outlook of the company (Gitman, Juchau and

Flanagan, 2015).

PROFITABILITY 2018 2019

Net Profit Net income 2.07% 2.10%

Net sales

Return on Equity Net income 8.90% 11.55%

Net Equity

Solvency

Solvency ratios are the ratios which defines the method in which the funds have been acquired

by the business and in different means. For example Tesco has acquired funds in the combination

of the debt and the equity. As per the current scenario, the debt to equity ratio as increased from

0.38 times to 0.68 times as the company is focusing more towards the long term debt to improve

2018 2019

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Net Profit Margin

Net Profit %

The return on equity on the other hand is the ratio which depicts how effectively the

management is using the return on equity. The net income comes from the income statement and

the equity factor comes from the balance sheet. This implies that there is an inverse relationship

between the both. The return on equity has been increased in comparison to the past year from

8% to 11.55% thereby giving the positive outlook of the company (Gitman, Juchau and

Flanagan, 2015).

PROFITABILITY 2018 2019

Net Profit Net income 2.07% 2.10%

Net sales

Return on Equity Net income 8.90% 11.55%

Net Equity

Solvency

Solvency ratios are the ratios which defines the method in which the funds have been acquired

by the business and in different means. For example Tesco has acquired funds in the combination

of the debt and the equity. As per the current scenario, the debt to equity ratio as increased from

0.38 times to 0.68 times as the company is focusing more towards the long term debt to improve

Running Head: TESCO PLC ANALYSIS

the liquidity ratios (Robinson, Henry, Pirie and Broihahn, 2015). This also implies the company

wishes to claim the advantage arising from debt financing and at the same time this will also

increase the personal savings of the company. Times interest coverage ratio on the other hand is

another metric that is used to determine the ability of the company to pay back the costs arising

from the financial expenses such as interest. At present the company’s ability has declined a bit

from 4.02 times to 3.07 times and this also implies that too much debt will burden will burden

the company and reduce the pay ratio. Hence, long term debts shall be acquired but on limited

basis (Edwards, Schwab and Shevlin, 2015).

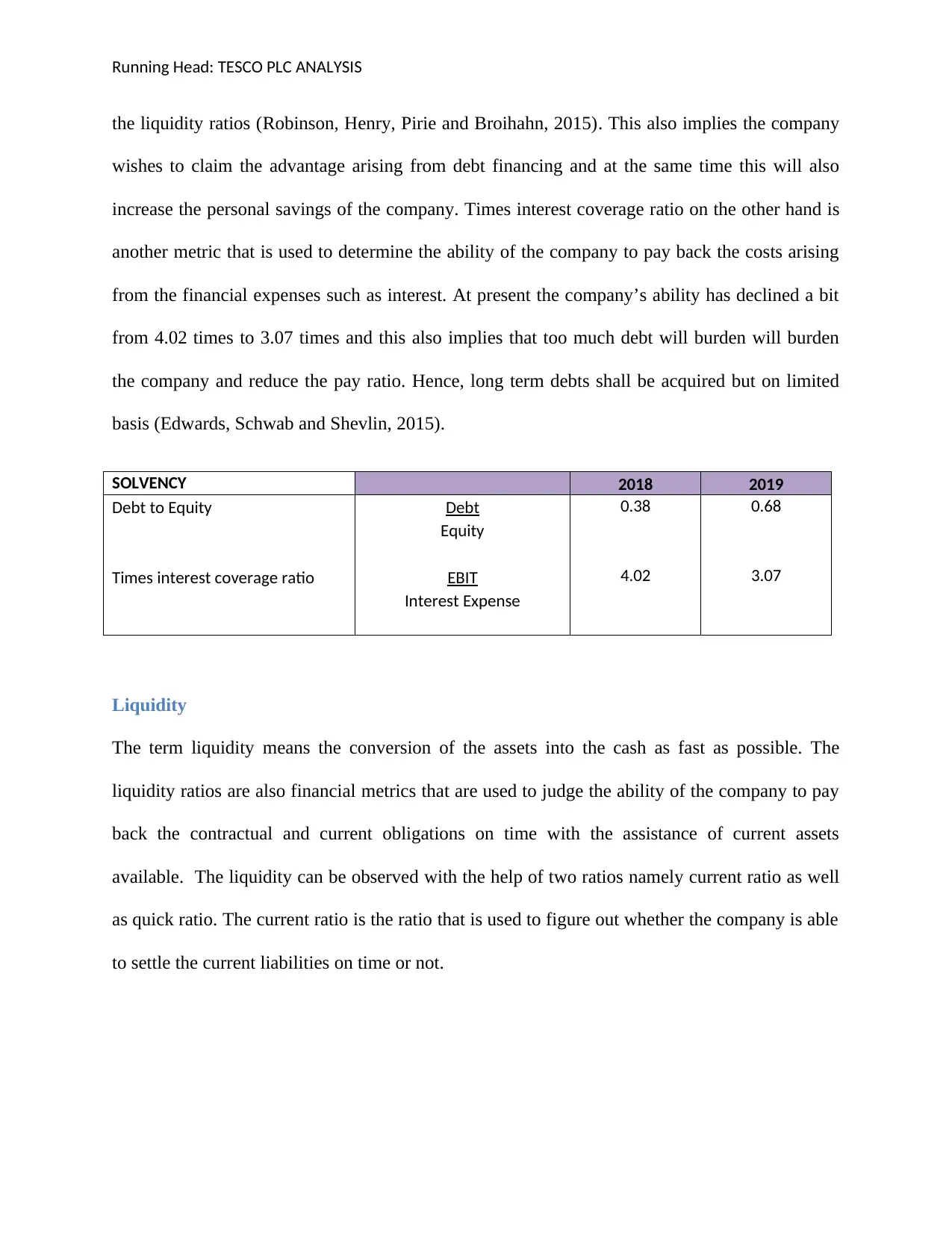

SOLVENCY 2018 2019

Debt to Equity Debt 0.38 0.68

Equity

Times interest coverage ratio EBIT 4.02 3.07

Interest Expense

Liquidity

The term liquidity means the conversion of the assets into the cash as fast as possible. The

liquidity ratios are also financial metrics that are used to judge the ability of the company to pay

back the contractual and current obligations on time with the assistance of current assets

available. The liquidity can be observed with the help of two ratios namely current ratio as well

as quick ratio. The current ratio is the ratio that is used to figure out whether the company is able

to settle the current liabilities on time or not.

the liquidity ratios (Robinson, Henry, Pirie and Broihahn, 2015). This also implies the company

wishes to claim the advantage arising from debt financing and at the same time this will also

increase the personal savings of the company. Times interest coverage ratio on the other hand is

another metric that is used to determine the ability of the company to pay back the costs arising

from the financial expenses such as interest. At present the company’s ability has declined a bit

from 4.02 times to 3.07 times and this also implies that too much debt will burden will burden

the company and reduce the pay ratio. Hence, long term debts shall be acquired but on limited

basis (Edwards, Schwab and Shevlin, 2015).

SOLVENCY 2018 2019

Debt to Equity Debt 0.38 0.68

Equity

Times interest coverage ratio EBIT 4.02 3.07

Interest Expense

Liquidity

The term liquidity means the conversion of the assets into the cash as fast as possible. The

liquidity ratios are also financial metrics that are used to judge the ability of the company to pay

back the contractual and current obligations on time with the assistance of current assets

available. The liquidity can be observed with the help of two ratios namely current ratio as well

as quick ratio. The current ratio is the ratio that is used to figure out whether the company is able

to settle the current liabilities on time or not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: TESCO PLC ANALYSIS

2018

2019

0.00 0.10 0.20 0.30 0.40 0.50 0.60 0.70 0.80

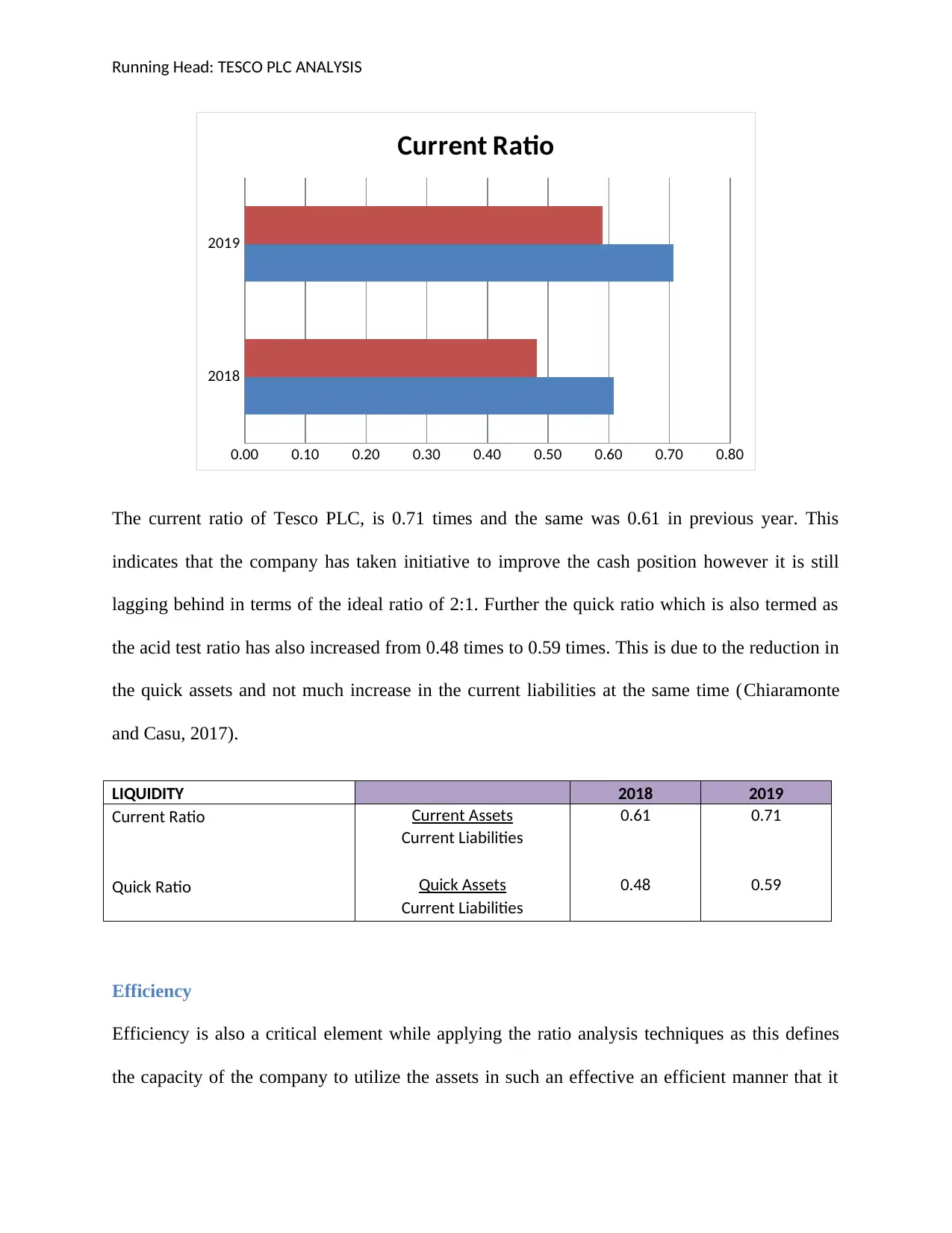

Current Ratio

The current ratio of Tesco PLC, is 0.71 times and the same was 0.61 in previous year. This

indicates that the company has taken initiative to improve the cash position however it is still

lagging behind in terms of the ideal ratio of 2:1. Further the quick ratio which is also termed as

the acid test ratio has also increased from 0.48 times to 0.59 times. This is due to the reduction in

the quick assets and not much increase in the current liabilities at the same time (Chiaramonte

and Casu, 2017).

LIQUIDITY 2018 2019

Current Ratio Current Assets 0.61 0.71

Current Liabilities

Quick Ratio Quick Assets 0.48 0.59

Current Liabilities

Efficiency

Efficiency is also a critical element while applying the ratio analysis techniques as this defines

the capacity of the company to utilize the assets in such an effective an efficient manner that it

2018

2019

0.00 0.10 0.20 0.30 0.40 0.50 0.60 0.70 0.80

Current Ratio

The current ratio of Tesco PLC, is 0.71 times and the same was 0.61 in previous year. This

indicates that the company has taken initiative to improve the cash position however it is still

lagging behind in terms of the ideal ratio of 2:1. Further the quick ratio which is also termed as

the acid test ratio has also increased from 0.48 times to 0.59 times. This is due to the reduction in

the quick assets and not much increase in the current liabilities at the same time (Chiaramonte

and Casu, 2017).

LIQUIDITY 2018 2019

Current Ratio Current Assets 0.61 0.71

Current Liabilities

Quick Ratio Quick Assets 0.48 0.59

Current Liabilities

Efficiency

Efficiency is also a critical element while applying the ratio analysis techniques as this defines

the capacity of the company to utilize the assets in such an effective an efficient manner that it

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: TESCO PLC ANALYSIS

can generate higher income and thereby resulting in improvement of the overall performance. the

efficiency of the company can be analyzed on the basis of net assets turnover ratio and the days

receivable ratios (Schroeder, Clark and Cathey, 2019). The asset turnover ratio is the metric

measures how well the company can generate the revenue with the help of the assets. As per

analysis of Tesco PLC, the net sales have increased at the minimal increase of the assets thereby

resulting in total asset turnover ratio of 4.42 times which declined from 4.84 times. This also

states that the performance of the company will see down times if the situation continues to be

the same. The receivables turnover ratio is the metric that mentions how effective the company is

in providing the credit facility to the customers and in how much time it is able to collect the

cash. The days receivable outstanding on the contrary have increased from 9.16 days to 9.55

days, stating the company is taking longer time to convert the credit sales into cash form. Overall

the efficiency of the company is not so smooth as it shall have been (Monistrics, 2017).

EFFICIENCY 2018 2019

Total Asset turnover Net Sales 4.84 4.42

Average total Assets

Receivable turnover ratio Accounts receivable * 365 9.16 9.55

Credit sales

Good investment or not

Any good investment is based on certain factors such as high profitability, returns and the stable

performance of the company. From the overall analysis it can be stated that Tesco PLC has a

progressive liquidity position and also works satisfactory in giving the returns to its investors and

shareholders. This does not tales away the fact that it needs to improve in area of solvency and

efficiency to have the better possibility of generation of more income. The net profit can be

can generate higher income and thereby resulting in improvement of the overall performance. the

efficiency of the company can be analyzed on the basis of net assets turnover ratio and the days

receivable ratios (Schroeder, Clark and Cathey, 2019). The asset turnover ratio is the metric

measures how well the company can generate the revenue with the help of the assets. As per

analysis of Tesco PLC, the net sales have increased at the minimal increase of the assets thereby

resulting in total asset turnover ratio of 4.42 times which declined from 4.84 times. This also

states that the performance of the company will see down times if the situation continues to be

the same. The receivables turnover ratio is the metric that mentions how effective the company is

in providing the credit facility to the customers and in how much time it is able to collect the

cash. The days receivable outstanding on the contrary have increased from 9.16 days to 9.55

days, stating the company is taking longer time to convert the credit sales into cash form. Overall

the efficiency of the company is not so smooth as it shall have been (Monistrics, 2017).

EFFICIENCY 2018 2019

Total Asset turnover Net Sales 4.84 4.42

Average total Assets

Receivable turnover ratio Accounts receivable * 365 9.16 9.55

Credit sales

Good investment or not

Any good investment is based on certain factors such as high profitability, returns and the stable

performance of the company. From the overall analysis it can be stated that Tesco PLC has a

progressive liquidity position and also works satisfactory in giving the returns to its investors and

shareholders. This does not tales away the fact that it needs to improve in area of solvency and

efficiency to have the better possibility of generation of more income. The net profit can be

Running Head: TESCO PLC ANALYSIS

improved by developing a new price scheme and reducing the credit sales and focusing more

towards the cash sales. Also the efficiency can be revamped by reducing the time period of the

credit sales and provide discounts on early payment from the customers. An investor can invest

in the business for long term, analyzing the two major prospects and monitoring the performance

on monthly basis to get ideas and news. Overall the company can improve in near future and can

provide greater return to the shareholders and investors. Henceforth it can be said that it is a good

investment if the shares are hold for longer time period.

Limitations of Analysis

While undertaking the analysis of Tesco PLC, it has been seen that the only limitation that have

been came across is that the future value cannot be ascertained with proper accuracy. Only

assumptions can be taken on the basis of the past performance. The figures can also be changed

at the year end to improve the ratios and showcase the positive performance even when the

company is making losses. Also if the company has changed its accounting policies and

procedures, this could significantly change the overall performance of the business. In this

scenario, key financial measurements used in proportion investigation are adjusted and the

budgetary outcomes recorded after the change are not equivalent to the outcomes recorded

preceding the change. Changes can be presented in the notes to the budget summaries area.

Hence, these were the certain limitations which are occurred when this type of technique is

implemented for evaluating the overall financial performance (The Accounting Tools, 2018).

improved by developing a new price scheme and reducing the credit sales and focusing more

towards the cash sales. Also the efficiency can be revamped by reducing the time period of the

credit sales and provide discounts on early payment from the customers. An investor can invest

in the business for long term, analyzing the two major prospects and monitoring the performance

on monthly basis to get ideas and news. Overall the company can improve in near future and can

provide greater return to the shareholders and investors. Henceforth it can be said that it is a good

investment if the shares are hold for longer time period.

Limitations of Analysis

While undertaking the analysis of Tesco PLC, it has been seen that the only limitation that have

been came across is that the future value cannot be ascertained with proper accuracy. Only

assumptions can be taken on the basis of the past performance. The figures can also be changed

at the year end to improve the ratios and showcase the positive performance even when the

company is making losses. Also if the company has changed its accounting policies and

procedures, this could significantly change the overall performance of the business. In this

scenario, key financial measurements used in proportion investigation are adjusted and the

budgetary outcomes recorded after the change are not equivalent to the outcomes recorded

preceding the change. Changes can be presented in the notes to the budget summaries area.

Hence, these were the certain limitations which are occurred when this type of technique is

implemented for evaluating the overall financial performance (The Accounting Tools, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: TESCO PLC ANALYSIS

References

Chiaramonte, L. and Casu, B., (2017) Capital and liquidity ratios and financial distress. Evidence

from the European banking industry. The British Accounting Review, 49(2), pp.138-161.

Edwards, A., Schwab, C., and Shevlin, T. (2015) Financial constraints and cash tax savings. The

Accounting Review, 91(3), pp 859-881.

Gitman, L.J., Juchau, R. and Flanagan, J., (2015) Principles of managerial finance. Pearson

Higher Education AU.

Goldmann, K., (2017) Financial liquidity and profitability management in practice of polish

business. In Financial Environment and Business Development (pp. 103-112). Springer, Cham.

Monistrics, (2017) The Advantages and Disadvantages of Corporate Financial Reporting.

[Online] Available from http://www.monistrics.ga/2018/01/the-advantages-and-disadvantages-

of-corporate-financial-reporting.html [Accessed on 17th March 2020]

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., (2015) International financial

statement analysis. John Wiley & Sons.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., (2019) Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Tesco PLC, (2019) Annual Report [Online] Available from

https://www.tescoplc.com/media/476422/tesco_ara2019_full_report_web.pdf [Accessed on 17th

March 2020]

References

Chiaramonte, L. and Casu, B., (2017) Capital and liquidity ratios and financial distress. Evidence

from the European banking industry. The British Accounting Review, 49(2), pp.138-161.

Edwards, A., Schwab, C., and Shevlin, T. (2015) Financial constraints and cash tax savings. The

Accounting Review, 91(3), pp 859-881.

Gitman, L.J., Juchau, R. and Flanagan, J., (2015) Principles of managerial finance. Pearson

Higher Education AU.

Goldmann, K., (2017) Financial liquidity and profitability management in practice of polish

business. In Financial Environment and Business Development (pp. 103-112). Springer, Cham.

Monistrics, (2017) The Advantages and Disadvantages of Corporate Financial Reporting.

[Online] Available from http://www.monistrics.ga/2018/01/the-advantages-and-disadvantages-

of-corporate-financial-reporting.html [Accessed on 17th March 2020]

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., (2015) International financial

statement analysis. John Wiley & Sons.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., (2019) Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Tesco PLC, (2019) Annual Report [Online] Available from

https://www.tescoplc.com/media/476422/tesco_ara2019_full_report_web.pdf [Accessed on 17th

March 2020]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: TESCO PLC ANALYSIS

The Accounting Tools, (2018) Limitations of ratios analysis. [Online] Available from

https://www.accountingtools.com/articles/what-are-the-limitations-of-ratio-analysis.html

[Accessed on 17th March 2020]

The Accounting Tools, (2018) Limitations of ratios analysis. [Online] Available from

https://www.accountingtools.com/articles/what-are-the-limitations-of-ratio-analysis.html

[Accessed on 17th March 2020]

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.