Financial Management Report: Evaluating Decision-Making at Tesco Plc

VerifiedAdded on 2023/01/10

|15

|4991

|20

Report

AI Summary

This financial management report provides a detailed analysis of financial strategies and decision-making processes within Tesco Plc. The report is divided into two sections, A and B. Section A explores techniques, approaches, and factors contributing to effective decision-making, stakeholder management, cost control through management accounting, fraud detection, and ethical considerations. Section B delves into the role of data in informing operational and strategic decisions, investment appraisal techniques, financial decision-making values, and long-term sustainability. The report evaluates various financial management aspects, including make-or-buy decisions, formal and information approaches, stakeholder conflicts, and the application of financial ratios. It also examines the value of management accounting in cost control and maximizing shareholder value, along with fraud detection methods and ethical decision-making processes. The analysis includes recommendations and a conclusion summarizing the key findings and insights into Tesco Plc's financial management practices.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Section A.........................................................................................................................................1

1. Evaluate the range of techniques, approaches and factors which contribute in effective

decision making...........................................................................................................................1

2. Stakeholder management and conflicting objectives of different stakeholders group............2

3. Value of management accounting techniques in controlling cost and maximising

shareholders value.......................................................................................................................3

4. Fraud detection technique and approaches to ethical decisions making.................................4

5. Reflection on the basis of your learning..................................................................................5

Section B..........................................................................................................................................5

1. Evaluate that how data obtaining help to inform operational and strategic decisions.............5

2. Compare and contrast three investment appraisal techniques and evaluate its effectiveness. 8

3. Evaluate the values of techniques which helps in financial decision making process..........10

4. Analyse how financial decision making support long term sustainability............................11

5. Recommendations..................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

MAIN BODY..................................................................................................................................1

Section A.........................................................................................................................................1

1. Evaluate the range of techniques, approaches and factors which contribute in effective

decision making...........................................................................................................................1

2. Stakeholder management and conflicting objectives of different stakeholders group............2

3. Value of management accounting techniques in controlling cost and maximising

shareholders value.......................................................................................................................3

4. Fraud detection technique and approaches to ethical decisions making.................................4

5. Reflection on the basis of your learning..................................................................................5

Section B..........................................................................................................................................5

1. Evaluate that how data obtaining help to inform operational and strategic decisions.............5

2. Compare and contrast three investment appraisal techniques and evaluate its effectiveness. 8

3. Evaluate the values of techniques which helps in financial decision making process..........10

4. Analyse how financial decision making support long term sustainability............................11

5. Recommendations..................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial management aims to understand the company's overall financial responsibility

which causes trouble being planned for financial purposes. Financial analysis is an integral part

of the particular business which leads to the growth of a company. Data on the accounts helps

companies to determine the profitability (Abrahamsen And et.al., 2018). For the better

understanding of this concept, Tesco Plc is selected. Section A is derived from various topics,

such as approaches, techniques or aspects to financial management that leads to successful

decision making processes. It also covers stakeholder involvement, management shareholder

conflict, financial management value, etc. Furthermore, this section discusses the various forms

of theft, ethics in decision-making processes or the expression of this principle that the author

has learned. Section B of this study covers the value of the business with the assistance of

investment appraisal strategies, financial ratios and how strategies assist in financial decision-

making. It also addresses how financial judgment promotes stability in the long run along with

several suggestions.

MAIN BODY

Section A

1. Evaluate the range of techniques, approaches and factors which contribute in effective

decision making

Approaches:

Make or buy decision: The decision to make or buy is the part of creating a rational choice

between designing an object directly (in-house) or purchasing it commercially (to an outside

distributor). The purchases side of the judgment is also called outsourcing. Make-or - buy

options typically occur when a business that has produced a unit of product or drastically

updated a product or component has issues with existing vendors, or has lost capability or

increased demand.

Formal and information approach: It is used to generate a credible plan for the firm's

decision-making process. This approach eliminates the unbiased decision and gave

justification of the reasons make appropriate decisions. This helps in increasing the

opportunity to pick approaches that satisfy the power of different stakeholder as per

their needs. There are logical viable alternatives which eliminate waste of the tasks involved.

1

Financial management aims to understand the company's overall financial responsibility

which causes trouble being planned for financial purposes. Financial analysis is an integral part

of the particular business which leads to the growth of a company. Data on the accounts helps

companies to determine the profitability (Abrahamsen And et.al., 2018). For the better

understanding of this concept, Tesco Plc is selected. Section A is derived from various topics,

such as approaches, techniques or aspects to financial management that leads to successful

decision making processes. It also covers stakeholder involvement, management shareholder

conflict, financial management value, etc. Furthermore, this section discusses the various forms

of theft, ethics in decision-making processes or the expression of this principle that the author

has learned. Section B of this study covers the value of the business with the assistance of

investment appraisal strategies, financial ratios and how strategies assist in financial decision-

making. It also addresses how financial judgment promotes stability in the long run along with

several suggestions.

MAIN BODY

Section A

1. Evaluate the range of techniques, approaches and factors which contribute in effective

decision making

Approaches:

Make or buy decision: The decision to make or buy is the part of creating a rational choice

between designing an object directly (in-house) or purchasing it commercially (to an outside

distributor). The purchases side of the judgment is also called outsourcing. Make-or - buy

options typically occur when a business that has produced a unit of product or drastically

updated a product or component has issues with existing vendors, or has lost capability or

increased demand.

Formal and information approach: It is used to generate a credible plan for the firm's

decision-making process. This approach eliminates the unbiased decision and gave

justification of the reasons make appropriate decisions. This helps in increasing the

opportunity to pick approaches that satisfy the power of different stakeholder as per

their needs. There are logical viable alternatives which eliminate waste of the tasks involved.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The approach allows for a more urgent re-evaluation of the partners' circumstances,

priorities or aim changes. It allows Tesco Plc to consider making more business decisions in

every respect.

Techniques:

T-Chart: This diagram is designed to display the options with maximum and minimum

points. That means both negative and positive aspects are taken into account when choosing

critical decisions

Decision Matrix: Management teams should assess the strategy at the time of requirement.

Within this matrix, all of the possibilities are placed first in the bar counter, and the things

that influenced the first segment decisions (Agrawal, 2018). This includes ranking and

weighing parameters based on their relevance and picking the very best options.

Factors Contributes in effective decision making:

Social factors: Tesco Plc interactions with newly formed companies, trustworthy alliance

with the customer and their company have a full effect on the product lifecycle in the

enterprise. To develop public confidence with managers is essential to take publicly

supportive acts. Social factors must acknowledge preserving the interests of the public at the

course of creating strategic decisions to optimize their participation.

Financial factors: The formation of a strategic move refers to the financial resources of a

organization. The capital and the long term opportunity to make assumptions on their

investment of these construction cost is therefore easy to transport out. Tesco’s management

determine certain financial considerations that influence decision-making processes and then

further impact both economic advantage and performance. That process relates to effective

decision-making for managers.

2. Stakeholder management and conflicting objectives of different stakeholders group

Stakeholders are those people who can significantly affect or influence a strategy. They

may also involve people who have a particular interest in social, intellectual, or political

objectives in the project, although it does not specifically affect them personally and their family,

friends and colleagues (BLŠTÁKOVÁ And et.al., 2019). By general, owners tend to be paying

interest in a campaign or collective of activists on how it will influence or harm them. The

further they go on profiting from it, or ending up having lost it, and the likelihood of everyone’s

interest. The bigger the effort or group they are participating in, the increasing their purpose as

2

priorities or aim changes. It allows Tesco Plc to consider making more business decisions in

every respect.

Techniques:

T-Chart: This diagram is designed to display the options with maximum and minimum

points. That means both negative and positive aspects are taken into account when choosing

critical decisions

Decision Matrix: Management teams should assess the strategy at the time of requirement.

Within this matrix, all of the possibilities are placed first in the bar counter, and the things

that influenced the first segment decisions (Agrawal, 2018). This includes ranking and

weighing parameters based on their relevance and picking the very best options.

Factors Contributes in effective decision making:

Social factors: Tesco Plc interactions with newly formed companies, trustworthy alliance

with the customer and their company have a full effect on the product lifecycle in the

enterprise. To develop public confidence with managers is essential to take publicly

supportive acts. Social factors must acknowledge preserving the interests of the public at the

course of creating strategic decisions to optimize their participation.

Financial factors: The formation of a strategic move refers to the financial resources of a

organization. The capital and the long term opportunity to make assumptions on their

investment of these construction cost is therefore easy to transport out. Tesco’s management

determine certain financial considerations that influence decision-making processes and then

further impact both economic advantage and performance. That process relates to effective

decision-making for managers.

2. Stakeholder management and conflicting objectives of different stakeholders group

Stakeholders are those people who can significantly affect or influence a strategy. They

may also involve people who have a particular interest in social, intellectual, or political

objectives in the project, although it does not specifically affect them personally and their family,

friends and colleagues (BLŠTÁKOVÁ And et.al., 2019). By general, owners tend to be paying

interest in a campaign or collective of activists on how it will influence or harm them. The

further they go on profiting from it, or ending up having lost it, and the likelihood of everyone’s

interest. The bigger the effort or group they are participating in, the increasing their purpose as

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

well. Stakeholders' high interest puts more suggestions on the negotiation table, includes

different perspectives, moral boost and also strengthens their organizational position.

Conflicts in the organization affect two different parties but also the participants are

actively involved in coercion, victimization, and escape. But once two parties are engaged in

conflicts that includes transaction as both parties. Both users decide what happens, each effect

others and it is influenced by the other, almost often including a third party to cause a negative

triangle. It appears to enhance the pressure and make things worse. Tesco Plc's managers tackle

the dispute between management and creditors by using Agency Concept. In addition, there are

also some other disputes between management with interested parties, such as conflicts among

receivables and payables parties.

3. Value of management accounting techniques in controlling cost and maximising shareholders

value

Management accounting must be used for short term as well as for long-term decisions

in regards to the financial performance of a company (Chand, 2019). Tesco Plc's financial

managers are assisted by management accounting to develop a strategic plan which focuses on

helping to improve the organization’s operational profitability while still helping to make

potential investment choices. Efficiency forecasting, management and monitoring are a key

function of accounting treatment to ensure that the total results are consistent with the earnings

and expenses identified at the beginning.

The role of management accounting professionals is to concentrate on delivering crucial

perspectives that help a company’s senior management to make all of its decisions. Management

accounting support decision-making processes within a firm by providing data for financial

reporting purpose, which is often endorsed by appropriate accounting system. Accountant's play

multiple roles, such as providing product review, marketing plan, recruitment and retention,

organizational program evaluation, funds and resources etc. Such roles help the Tesco Plc’s

accountants to attain their corporate objectives & goals. It helps the managers to maximise the

value of shareholders as well as helps in controlling cost to increase the profit margin.

Tesco's Finance Managers are the representatives of the company and their job is to look

after shareholder’s interests. The goal of a certain shareholder or investor would be a good rate

on the capital of all, and the security of all the capital. Each one of these targets is quite well

suited as a pure wealth maximization indicator of business decision. There are so many forms of

3

different perspectives, moral boost and also strengthens their organizational position.

Conflicts in the organization affect two different parties but also the participants are

actively involved in coercion, victimization, and escape. But once two parties are engaged in

conflicts that includes transaction as both parties. Both users decide what happens, each effect

others and it is influenced by the other, almost often including a third party to cause a negative

triangle. It appears to enhance the pressure and make things worse. Tesco Plc's managers tackle

the dispute between management and creditors by using Agency Concept. In addition, there are

also some other disputes between management with interested parties, such as conflicts among

receivables and payables parties.

3. Value of management accounting techniques in controlling cost and maximising shareholders

value

Management accounting must be used for short term as well as for long-term decisions

in regards to the financial performance of a company (Chand, 2019). Tesco Plc's financial

managers are assisted by management accounting to develop a strategic plan which focuses on

helping to improve the organization’s operational profitability while still helping to make

potential investment choices. Efficiency forecasting, management and monitoring are a key

function of accounting treatment to ensure that the total results are consistent with the earnings

and expenses identified at the beginning.

The role of management accounting professionals is to concentrate on delivering crucial

perspectives that help a company’s senior management to make all of its decisions. Management

accounting support decision-making processes within a firm by providing data for financial

reporting purpose, which is often endorsed by appropriate accounting system. Accountant's play

multiple roles, such as providing product review, marketing plan, recruitment and retention,

organizational program evaluation, funds and resources etc. Such roles help the Tesco Plc’s

accountants to attain their corporate objectives & goals. It helps the managers to maximise the

value of shareholders as well as helps in controlling cost to increase the profit margin.

Tesco's Finance Managers are the representatives of the company and their job is to look

after shareholder’s interests. The goal of a certain shareholder or investor would be a good rate

on the capital of all, and the security of all the capital. Each one of these targets is quite well

suited as a pure wealth maximization indicator of business decision. There are so many forms of

3

capital budgeting that are used by Tesco's financial team to optimize shareholder equity such as

present value, accounting rate of return, payback time etc.

Management accountants continue pursuing the shareholders maximizing profit goal which

might represent on the organization's communication with shareholders and the resulting

decision-making behaviour (Famulska and Rogowska-Rajda, 2018). Management Accountant

carries out a variety of roles to make sure monetary sustainability by administering all of firm’s

financial aspects. It enables the business to force forward its plans and practices. The executive

branch Accountant ensures that all processes and operational activities are effectively carried out

after keeping the costs under control or maximise shareholders wealth.

Profitable business tends to make the use financial reporting to reduce fraud and the

morally wrong problems generated within the Tesco Plc. Management system tries to find fair

tools and approaches. It will provide an accrual accounting which focused to controlling

investment asset-related tasks and making intelligent business decisions on numerous economic

consequences. People use distinct forms of financial strategies which were employed by Tesco

Plc Business to reduce running costs. Cost management approach is managerial accounting

technique which used to mitigate manufacturing costs and optimize profit margin.

4. Fraud detection technique and approaches to ethical decisions making

Several methodologies are often used to track or avoid the fraud. Build a portfolio of

potential fraud that often involves risk management, identifying the areas where fraud is

probable to appear in the company, and the potential types of fraud within the operations. Then

assess the risk which also based on the firm's total accessibility. Focused on risk, those are very

likely to decrease value for shareholders. Systems influencing the several aspects such

as extended supply chain, reliability, efficiency, product quality and operations.

Strengthen payment regulations over time, and using regular inspection and review to

check the efficacy of compliance (Finkler, Smith and Calabrese, 2018). Repeated or unwilling to

compromise is the appraisals of fraud prevention which involve implementing scripts to run to

enormous amounts of information to recognize the abnormalities that occur in the process. This

method would substantially enhance the general effectiveness, safety and precision of the

detecting fraud processes. That wasn't the only processes, there was much more to identify fraud.

Ethics:

4

present value, accounting rate of return, payback time etc.

Management accountants continue pursuing the shareholders maximizing profit goal which

might represent on the organization's communication with shareholders and the resulting

decision-making behaviour (Famulska and Rogowska-Rajda, 2018). Management Accountant

carries out a variety of roles to make sure monetary sustainability by administering all of firm’s

financial aspects. It enables the business to force forward its plans and practices. The executive

branch Accountant ensures that all processes and operational activities are effectively carried out

after keeping the costs under control or maximise shareholders wealth.

Profitable business tends to make the use financial reporting to reduce fraud and the

morally wrong problems generated within the Tesco Plc. Management system tries to find fair

tools and approaches. It will provide an accrual accounting which focused to controlling

investment asset-related tasks and making intelligent business decisions on numerous economic

consequences. People use distinct forms of financial strategies which were employed by Tesco

Plc Business to reduce running costs. Cost management approach is managerial accounting

technique which used to mitigate manufacturing costs and optimize profit margin.

4. Fraud detection technique and approaches to ethical decisions making

Several methodologies are often used to track or avoid the fraud. Build a portfolio of

potential fraud that often involves risk management, identifying the areas where fraud is

probable to appear in the company, and the potential types of fraud within the operations. Then

assess the risk which also based on the firm's total accessibility. Focused on risk, those are very

likely to decrease value for shareholders. Systems influencing the several aspects such

as extended supply chain, reliability, efficiency, product quality and operations.

Strengthen payment regulations over time, and using regular inspection and review to

check the efficacy of compliance (Finkler, Smith and Calabrese, 2018). Repeated or unwilling to

compromise is the appraisals of fraud prevention which involve implementing scripts to run to

enormous amounts of information to recognize the abnormalities that occur in the process. This

method would substantially enhance the general effectiveness, safety and precision of the

detecting fraud processes. That wasn't the only processes, there was much more to identify fraud.

Ethics:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ethics is a collection of standard values which influence how a person makes choices and

how they enjoy their lives. Ethics must consider what is right for culture and people, as well as

ideology. Ethical decision making refers to the process by which alternatives are decided and

evaluated in a manner that complies with ethical principles. The detection and elimination of

unethical options in ethical decision-making is critical and the selection of the correct moral

option. Ethical decision-making demands commitment, understanding and skill.

There are so many ethical decision-making techniques such as right or equality approach,

humanistic approach, general welfare or virtual approach. Using such strategies, the managers

are able to take ethical action with regards to the organization. This also allows demand be

created by stakeholders (Hilkens, Reid, Klerkx and Gray, 2018). Tesco Plc will adopt a practical

approach for successful decision-making by assessing action which is based on its intended

outcome. Before making final judgments, it is essential to consider the benefits and

disadvantages. This technique aims to achieve the greatest profit to the highest number although

the least level of damage or trying to avoid the biggest suffering is actually occurring at the very

same advancements.

5. Reflection on the basis of your learning

Multiple learning’s have been included at the time evaluating my performances while

completing this report. During this research, I encountered many challenges but still learned to

understand how to tackle several issues. The crucial problem I encountered during this task is

that process of researching data on the specific topics and other activities. I used browsers to find

useful data but there are still a number of choices that have made it more complicated. That is

because the time needed to finish the project was too restricted. I also found it on top problem, as

well as a shortage in websites providing appropriate or reliable information.

Section B

1. Evaluate that how data obtaining help to inform operational and strategic decisions

It has revealed that managers generally work to complete their daily operations.

Management teams will have all the information on the company's overall greatest recent

discount rate (Jayaprawira, 2019). It is not as simple as anything more profitable or cost-effective

operations. Knowledge acquisition is often a large exercise which can have a significant impact

5

how they enjoy their lives. Ethics must consider what is right for culture and people, as well as

ideology. Ethical decision making refers to the process by which alternatives are decided and

evaluated in a manner that complies with ethical principles. The detection and elimination of

unethical options in ethical decision-making is critical and the selection of the correct moral

option. Ethical decision-making demands commitment, understanding and skill.

There are so many ethical decision-making techniques such as right or equality approach,

humanistic approach, general welfare or virtual approach. Using such strategies, the managers

are able to take ethical action with regards to the organization. This also allows demand be

created by stakeholders (Hilkens, Reid, Klerkx and Gray, 2018). Tesco Plc will adopt a practical

approach for successful decision-making by assessing action which is based on its intended

outcome. Before making final judgments, it is essential to consider the benefits and

disadvantages. This technique aims to achieve the greatest profit to the highest number although

the least level of damage or trying to avoid the biggest suffering is actually occurring at the very

same advancements.

5. Reflection on the basis of your learning

Multiple learning’s have been included at the time evaluating my performances while

completing this report. During this research, I encountered many challenges but still learned to

understand how to tackle several issues. The crucial problem I encountered during this task is

that process of researching data on the specific topics and other activities. I used browsers to find

useful data but there are still a number of choices that have made it more complicated. That is

because the time needed to finish the project was too restricted. I also found it on top problem, as

well as a shortage in websites providing appropriate or reliable information.

Section B

1. Evaluate that how data obtaining help to inform operational and strategic decisions

It has revealed that managers generally work to complete their daily operations.

Management teams will have all the information on the company's overall greatest recent

discount rate (Jayaprawira, 2019). It is not as simple as anything more profitable or cost-effective

operations. Knowledge acquisition is often a large exercise which can have a significant impact

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

on firms over the period. There is a great deal of structural data that managers regularly collect.

All the applicable decision-making relies on the organisation's aspect and position (Khitrin and

Pachkova, 2016). This endorses managers and many other people who relate their routine

decision for the requirement of information which further helps in taking managerial or strategic

decisions. Using Tesco's financial report is important for assessing their current position. The

below is the corporate combination analysis using data from the organization's annual statements

that will aid Tesco Plc in taking strategic and operational decisions. Calculation of ratios

mentioned below:

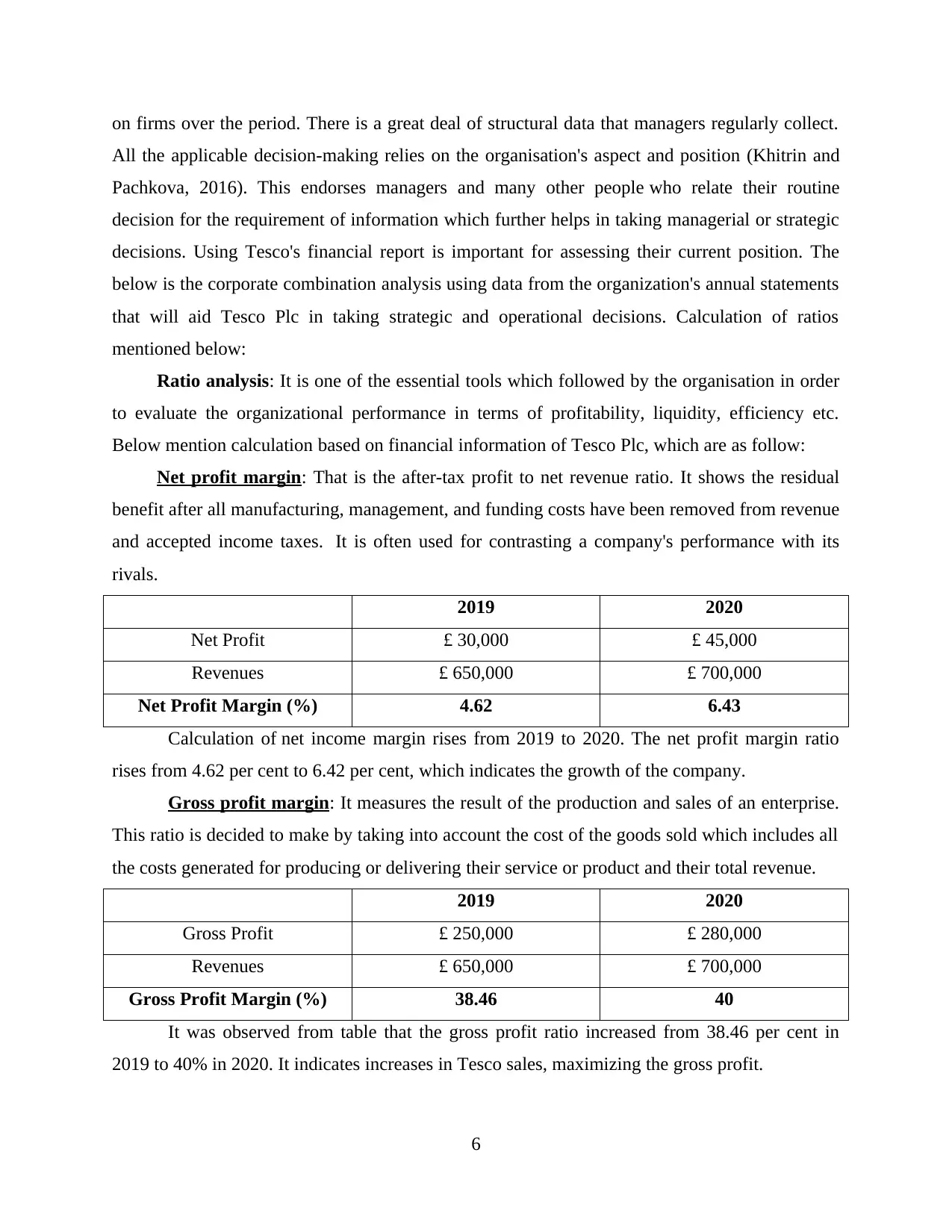

Ratio analysis: It is one of the essential tools which followed by the organisation in order

to evaluate the organizational performance in terms of profitability, liquidity, efficiency etc.

Below mention calculation based on financial information of Tesco Plc, which are as follow:

Net profit margin: That is the after-tax profit to net revenue ratio. It shows the residual

benefit after all manufacturing, management, and funding costs have been removed from revenue

and accepted income taxes. It is often used for contrasting a company's performance with its

rivals.

2019 2020

Net Profit £ 30,000 £ 45,000

Revenues £ 650,000 £ 700,000

Net Profit Margin (%) 4.62 6.43

Calculation of net income margin rises from 2019 to 2020. The net profit margin ratio

rises from 4.62 per cent to 6.42 per cent, which indicates the growth of the company.

Gross profit margin: It measures the result of the production and sales of an enterprise.

This ratio is decided to make by taking into account the cost of the goods sold which includes all

the costs generated for producing or delivering their service or product and their total revenue.

2019 2020

Gross Profit £ 250,000 £ 280,000

Revenues £ 650,000 £ 700,000

Gross Profit Margin (%) 38.46 40

It was observed from table that the gross profit ratio increased from 38.46 per cent in

2019 to 40% in 2020. It indicates increases in Tesco sales, maximizing the gross profit.

6

All the applicable decision-making relies on the organisation's aspect and position (Khitrin and

Pachkova, 2016). This endorses managers and many other people who relate their routine

decision for the requirement of information which further helps in taking managerial or strategic

decisions. Using Tesco's financial report is important for assessing their current position. The

below is the corporate combination analysis using data from the organization's annual statements

that will aid Tesco Plc in taking strategic and operational decisions. Calculation of ratios

mentioned below:

Ratio analysis: It is one of the essential tools which followed by the organisation in order

to evaluate the organizational performance in terms of profitability, liquidity, efficiency etc.

Below mention calculation based on financial information of Tesco Plc, which are as follow:

Net profit margin: That is the after-tax profit to net revenue ratio. It shows the residual

benefit after all manufacturing, management, and funding costs have been removed from revenue

and accepted income taxes. It is often used for contrasting a company's performance with its

rivals.

2019 2020

Net Profit £ 30,000 £ 45,000

Revenues £ 650,000 £ 700,000

Net Profit Margin (%) 4.62 6.43

Calculation of net income margin rises from 2019 to 2020. The net profit margin ratio

rises from 4.62 per cent to 6.42 per cent, which indicates the growth of the company.

Gross profit margin: It measures the result of the production and sales of an enterprise.

This ratio is decided to make by taking into account the cost of the goods sold which includes all

the costs generated for producing or delivering their service or product and their total revenue.

2019 2020

Gross Profit £ 250,000 £ 280,000

Revenues £ 650,000 £ 700,000

Gross Profit Margin (%) 38.46 40

It was observed from table that the gross profit ratio increased from 38.46 per cent in

2019 to 40% in 2020. It indicates increases in Tesco sales, maximizing the gross profit.

6

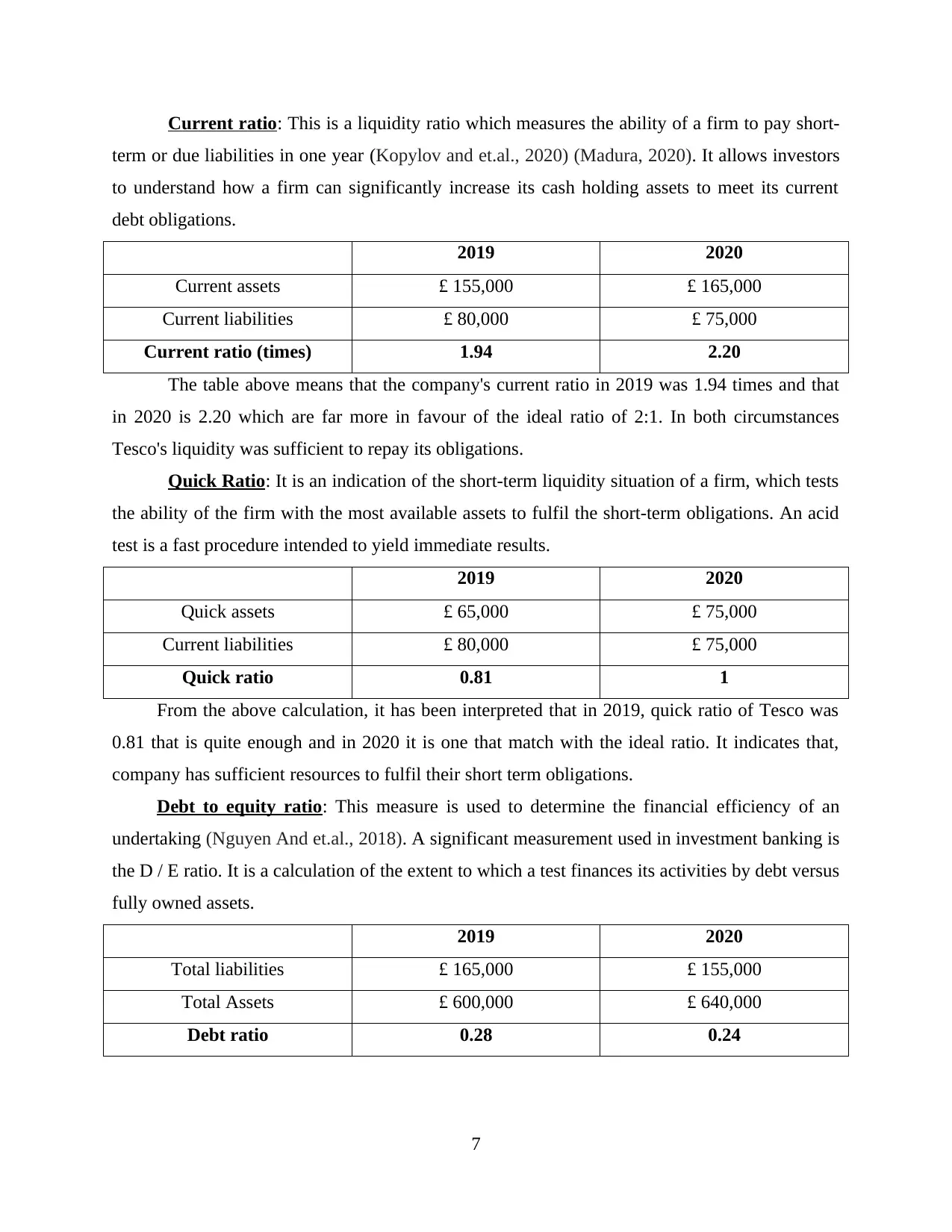

Current ratio: This is a liquidity ratio which measures the ability of a firm to pay short-

term or due liabilities in one year (Kopylov and et.al., 2020) (Madura, 2020). It allows investors

to understand how a firm can significantly increase its cash holding assets to meet its current

debt obligations.

2019 2020

Current assets £ 155,000 £ 165,000

Current liabilities £ 80,000 £ 75,000

Current ratio (times) 1.94 2.20

The table above means that the company's current ratio in 2019 was 1.94 times and that

in 2020 is 2.20 which are far more in favour of the ideal ratio of 2:1. In both circumstances

Tesco's liquidity was sufficient to repay its obligations.

Quick Ratio: It is an indication of the short-term liquidity situation of a firm, which tests

the ability of the firm with the most available assets to fulfil the short-term obligations. An acid

test is a fast procedure intended to yield immediate results.

2019 2020

Quick assets £ 65,000 £ 75,000

Current liabilities £ 80,000 £ 75,000

Quick ratio 0.81 1

From the above calculation, it has been interpreted that in 2019, quick ratio of Tesco was

0.81 that is quite enough and in 2020 it is one that match with the ideal ratio. It indicates that,

company has sufficient resources to fulfil their short term obligations.

Debt to equity ratio: This measure is used to determine the financial efficiency of an

undertaking (Nguyen And et.al., 2018). A significant measurement used in investment banking is

the D / E ratio. It is a calculation of the extent to which a test finances its activities by debt versus

fully owned assets.

2019 2020

Total liabilities £ 165,000 £ 155,000

Total Assets £ 600,000 £ 640,000

Debt ratio 0.28 0.24

7

term or due liabilities in one year (Kopylov and et.al., 2020) (Madura, 2020). It allows investors

to understand how a firm can significantly increase its cash holding assets to meet its current

debt obligations.

2019 2020

Current assets £ 155,000 £ 165,000

Current liabilities £ 80,000 £ 75,000

Current ratio (times) 1.94 2.20

The table above means that the company's current ratio in 2019 was 1.94 times and that

in 2020 is 2.20 which are far more in favour of the ideal ratio of 2:1. In both circumstances

Tesco's liquidity was sufficient to repay its obligations.

Quick Ratio: It is an indication of the short-term liquidity situation of a firm, which tests

the ability of the firm with the most available assets to fulfil the short-term obligations. An acid

test is a fast procedure intended to yield immediate results.

2019 2020

Quick assets £ 65,000 £ 75,000

Current liabilities £ 80,000 £ 75,000

Quick ratio 0.81 1

From the above calculation, it has been interpreted that in 2019, quick ratio of Tesco was

0.81 that is quite enough and in 2020 it is one that match with the ideal ratio. It indicates that,

company has sufficient resources to fulfil their short term obligations.

Debt to equity ratio: This measure is used to determine the financial efficiency of an

undertaking (Nguyen And et.al., 2018). A significant measurement used in investment banking is

the D / E ratio. It is a calculation of the extent to which a test finances its activities by debt versus

fully owned assets.

2019 2020

Total liabilities £ 165,000 £ 155,000

Total Assets £ 600,000 £ 640,000

Debt ratio 0.28 0.24

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It has been observed that, debt ratio in 2020 is 0.24 and in 2019 it was 0.28 which shows

the decline around 0.04. Manager’s of Tesco Plc need to improve their operational strategy

which further helps in improving their efficiency.

2. Compare and contrast three investment appraisal techniques and evaluate its effectiveness

Payback Period: It is the essential strategy that shows recovery period through an initial

investment of a specific project. High the recovery period rejected and lower period is more

profitable as well as beneficial for the organization. Its formula and calculations are as follow:

Initial Investment: £ 100,000

Year Cash flow Cumulative cash flow

Year 1 £ 30,000 £ 30,000

Year 2 £ 40,000 £ 70,000

Year 3 £ 90,000 £ 160,000

Year 4 £ 120,000 £ 280,000

Year 5 £ 150,000 £ 430,000

Formula:

Payback period= Year before full recovery + amount remained to be recover/ next year cash flow

= 2 + 30,000/90,000

= 2.33 years

Above calculation shows that, Tesco should adopt this project because it has low

recovery period that is 2.33 years.

Net Present Value (NPV): It is one of most usable method that illustrates the advantages

of the existing values in a given project or program (Njenga and Jagongo, 2019). This measure

will receive the benefits from such a capital expenditure the different equity gains that the

business gains.

Discount rate = 10%

Initial Investment = 100,000

Year Cash flow PV factor Discounted cash flow

1 £ 30,000 0.909 27,270

2 £ 40,000 0.826 33,040

8

the decline around 0.04. Manager’s of Tesco Plc need to improve their operational strategy

which further helps in improving their efficiency.

2. Compare and contrast three investment appraisal techniques and evaluate its effectiveness

Payback Period: It is the essential strategy that shows recovery period through an initial

investment of a specific project. High the recovery period rejected and lower period is more

profitable as well as beneficial for the organization. Its formula and calculations are as follow:

Initial Investment: £ 100,000

Year Cash flow Cumulative cash flow

Year 1 £ 30,000 £ 30,000

Year 2 £ 40,000 £ 70,000

Year 3 £ 90,000 £ 160,000

Year 4 £ 120,000 £ 280,000

Year 5 £ 150,000 £ 430,000

Formula:

Payback period= Year before full recovery + amount remained to be recover/ next year cash flow

= 2 + 30,000/90,000

= 2.33 years

Above calculation shows that, Tesco should adopt this project because it has low

recovery period that is 2.33 years.

Net Present Value (NPV): It is one of most usable method that illustrates the advantages

of the existing values in a given project or program (Njenga and Jagongo, 2019). This measure

will receive the benefits from such a capital expenditure the different equity gains that the

business gains.

Discount rate = 10%

Initial Investment = 100,000

Year Cash flow PV factor Discounted cash flow

1 £ 30,000 0.909 27,270

2 £ 40,000 0.826 33,040

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3 £ 90,000 0.751 67,590

4 £ 120,000 0.683 81,960

5 £ 150,000 0.621 93,150

303,010

NPV= Discounted cash flow-investment

= 303,010 - 100,000

= 203,010

Managers of Tesco should select this project because it value of NPV is positive and it

indicate that project is beneficial as well as profitable for the organizations.

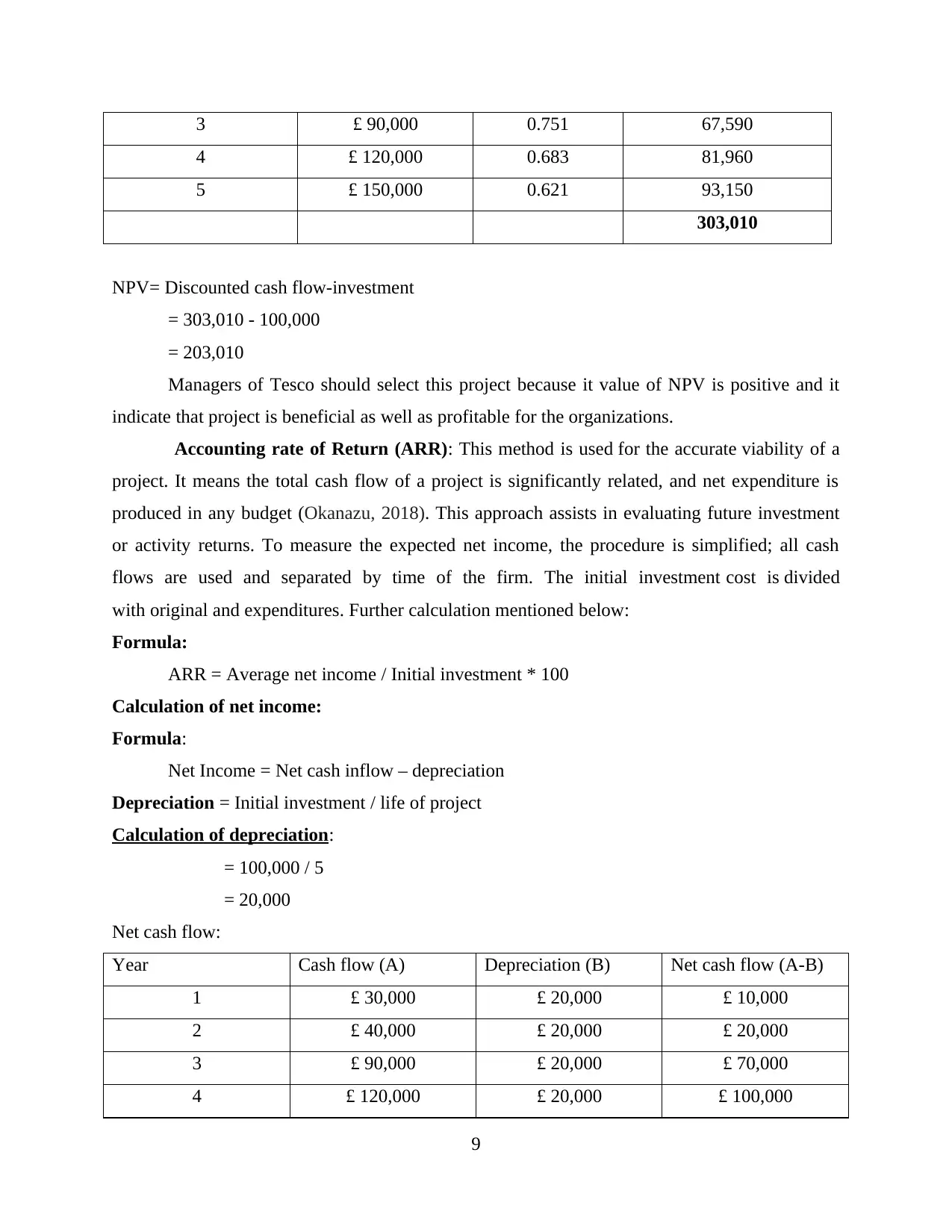

Accounting rate of Return (ARR): This method is used for the accurate viability of a

project. It means the total cash flow of a project is significantly related, and net expenditure is

produced in any budget (Okanazu, 2018). This approach assists in evaluating future investment

or activity returns. To measure the expected net income, the procedure is simplified; all cash

flows are used and separated by time of the firm. The initial investment cost is divided

with original and expenditures. Further calculation mentioned below:

Formula:

ARR = Average net income / Initial investment * 100

Calculation of net income:

Formula:

Net Income = Net cash inflow – depreciation

Depreciation = Initial investment / life of project

Calculation of depreciation:

= 100,000 / 5

= 20,000

Net cash flow:

Year Cash flow (A) Depreciation (B) Net cash flow (A-B)

1 £ 30,000 £ 20,000 £ 10,000

2 £ 40,000 £ 20,000 £ 20,000

3 £ 90,000 £ 20,000 £ 70,000

4 £ 120,000 £ 20,000 £ 100,000

9

4 £ 120,000 0.683 81,960

5 £ 150,000 0.621 93,150

303,010

NPV= Discounted cash flow-investment

= 303,010 - 100,000

= 203,010

Managers of Tesco should select this project because it value of NPV is positive and it

indicate that project is beneficial as well as profitable for the organizations.

Accounting rate of Return (ARR): This method is used for the accurate viability of a

project. It means the total cash flow of a project is significantly related, and net expenditure is

produced in any budget (Okanazu, 2018). This approach assists in evaluating future investment

or activity returns. To measure the expected net income, the procedure is simplified; all cash

flows are used and separated by time of the firm. The initial investment cost is divided

with original and expenditures. Further calculation mentioned below:

Formula:

ARR = Average net income / Initial investment * 100

Calculation of net income:

Formula:

Net Income = Net cash inflow – depreciation

Depreciation = Initial investment / life of project

Calculation of depreciation:

= 100,000 / 5

= 20,000

Net cash flow:

Year Cash flow (A) Depreciation (B) Net cash flow (A-B)

1 £ 30,000 £ 20,000 £ 10,000

2 £ 40,000 £ 20,000 £ 20,000

3 £ 90,000 £ 20,000 £ 70,000

4 £ 120,000 £ 20,000 £ 100,000

9

5 £ 150,000 £ 20,000 £ 130,000

£ 330,000

Average net income:

Year Net cash flow (A-B)

1 £ 10,000

2 £ 20,000

3 £ 70,000

4 £ 100,000

5 £ 130,000

Total £ 330,000

Average net income = 330,000 / 5

= 66,000

So,

ARR = 66,000 / 100,000 * 100

= 66%

The value of Accounting Rate of Return is of 66% which indicates that project is beneficial

for Tesco plc.

3. Evaluate the values of techniques which helps in financial decision making process

There are several values of techniques which help the managers of Tesco in the financial

decision making process. Some of them are as follow:

Determining profit: financial management techniques typically involve in cash flow,

break-even analysis, procedures for capital budgeting, etc. These strategies allow businesses to

predict potential earnings from sales. Through this, Tesco plc company's managers can calculate

their original profit margin portion.

Helps in setting long term goals: These strategies enable managers to evaluate long-term

corporate goals as management teams make a decision on their development objectives by

evaluating their needed to maximize and cash income over a specified period of time.

10

£ 330,000

Average net income:

Year Net cash flow (A-B)

1 £ 10,000

2 £ 20,000

3 £ 70,000

4 £ 100,000

5 £ 130,000

Total £ 330,000

Average net income = 330,000 / 5

= 66,000

So,

ARR = 66,000 / 100,000 * 100

= 66%

The value of Accounting Rate of Return is of 66% which indicates that project is beneficial

for Tesco plc.

3. Evaluate the values of techniques which helps in financial decision making process

There are several values of techniques which help the managers of Tesco in the financial

decision making process. Some of them are as follow:

Determining profit: financial management techniques typically involve in cash flow,

break-even analysis, procedures for capital budgeting, etc. These strategies allow businesses to

predict potential earnings from sales. Through this, Tesco plc company's managers can calculate

their original profit margin portion.

Helps in setting long term goals: These strategies enable managers to evaluate long-term

corporate goals as management teams make a decision on their development objectives by

evaluating their needed to maximize and cash income over a specified period of time.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.