Financial Management Report: Financial Analysis of Tesco (HND)

VerifiedAdded on 2023/01/11

|22

|6081

|43

Report

AI Summary

This report analyzes the financial management practices of Tesco, a UK-based supermarket. It is divided into two scenarios, exploring various approaches, techniques, and factors contributing to effective decision-making within the organization. Scenario A evaluates stakeholder management, conflicting objectives, the value of management accounting in cost control and maximizing shareholder value, and techniques for fraud detection and ethical decision-making. Scenario B focuses on data informing operational and strategic decisions, investment appraisal techniques, the value of these techniques in decision-making, and the role of financial decision-making in supporting long-term sustainability, concluding with recommendations for management accounting support for financial sustainability. The report examines financial planning, cost accounting, fund flow analysis, and marginal costing techniques used by Tesco to inform decisions, increase efficiency, and ensure long-term growth. The analysis includes ratio calculations and financial statement analysis to effectively present the business operations.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................4

SCENARIO A.............................................................................................................................................4

1. Evaluation range of approaches, techniques and factors contribute to effective decision making.......4

2. Stakeholder management and the management of conflicting objectives of various stakeholder

groups......................................................................................................................................................6

3. Value of management accountings in cost control and maximizing shareholder value.......................7

4. Techniques for fraud detection and prevention approach for ethical decision making.........................8

5. Reflection on understanding................................................................................................................9

SCENARIO B...........................................................................................................................................10

1. Data obtained that help to inform operational and strategic decisions...............................................10

2. Compare and contrast of three investment appraisal techniques that helps in maximize return on

investment.............................................................................................................................................12

3. Value of techniques helps in decision making procedure..................................................................17

4. Financial decision making supports long term sustainability.............................................................18

5. Make recommendations for management accountant supports for financial sustainability................18

CONCLUSION.........................................................................................................................................19

REFRENCES............................................................................................................................................20

INTRODUCTION.......................................................................................................................................4

SCENARIO A.............................................................................................................................................4

1. Evaluation range of approaches, techniques and factors contribute to effective decision making.......4

2. Stakeholder management and the management of conflicting objectives of various stakeholder

groups......................................................................................................................................................6

3. Value of management accountings in cost control and maximizing shareholder value.......................7

4. Techniques for fraud detection and prevention approach for ethical decision making.........................8

5. Reflection on understanding................................................................................................................9

SCENARIO B...........................................................................................................................................10

1. Data obtained that help to inform operational and strategic decisions...............................................10

2. Compare and contrast of three investment appraisal techniques that helps in maximize return on

investment.............................................................................................................................................12

3. Value of techniques helps in decision making procedure..................................................................17

4. Financial decision making supports long term sustainability.............................................................18

5. Make recommendations for management accountant supports for financial sustainability................18

CONCLUSION.........................................................................................................................................19

REFRENCES............................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial management relates to appropriate and productive corporate finance (cash) to

meet the organizational mission. It is the unique role which is closely connected with upper

executives. The sense of this role is not only in the 'section' but is also in use in the total use of

the corporation's 'workers.' The distinct researchers in the field describe this separately. It leads

to strategic planning, organization, preparing and development of source of collecting within an

entity or institution. It also involves the application of management concepts to an organization's

financial assets, even while taking a huge portion in economic management (Albring, Elder and

Xu, 2018). The explanation is that even with good use of the resources, a corporation cannot

operate. It could even be suffering stunted growth. To recognize and implement the best business

strategies in the managing and utilization of funds, one needs to recognize how important a

company is in financial management. This report is based on the Tesco organisation that is

established in UK and conduct own supermarket. This report is mainly based on the value of

management accounting and their techniques in informing decision, increasing efficiency and

helping to assure for the long term sustainability and growth. This report contains two parts in

which analysis of various techniques that are useful for the business. Moreover, to analysis the

actual business situation calculate ratio of the company and analysis all the financial statements

that presents all the business operations effectively.

SCENARIO A

1. Evaluation range of approaches, techniques and factors contribute to effective decision making

Management think evolution is a phase that began in guy's initial periods. It started from

the time frame when man have seen the need for group living. The important people were able to

coordinate the people, to divide them into different classes. The exchange was undertaken in

keeping with the power, mental ability, and intellect of the people. To make the decision in any

business require to focusing on different aspects that are related with the business in direct as

well as indirect manner. For this require to focus on every activities and how useful it in the

business. There are identifying different approaches, techniques and factors of management that

Financial management relates to appropriate and productive corporate finance (cash) to

meet the organizational mission. It is the unique role which is closely connected with upper

executives. The sense of this role is not only in the 'section' but is also in use in the total use of

the corporation's 'workers.' The distinct researchers in the field describe this separately. It leads

to strategic planning, organization, preparing and development of source of collecting within an

entity or institution. It also involves the application of management concepts to an organization's

financial assets, even while taking a huge portion in economic management (Albring, Elder and

Xu, 2018). The explanation is that even with good use of the resources, a corporation cannot

operate. It could even be suffering stunted growth. To recognize and implement the best business

strategies in the managing and utilization of funds, one needs to recognize how important a

company is in financial management. This report is based on the Tesco organisation that is

established in UK and conduct own supermarket. This report is mainly based on the value of

management accounting and their techniques in informing decision, increasing efficiency and

helping to assure for the long term sustainability and growth. This report contains two parts in

which analysis of various techniques that are useful for the business. Moreover, to analysis the

actual business situation calculate ratio of the company and analysis all the financial statements

that presents all the business operations effectively.

SCENARIO A

1. Evaluation range of approaches, techniques and factors contribute to effective decision making

Management think evolution is a phase that began in guy's initial periods. It started from

the time frame when man have seen the need for group living. The important people were able to

coordinate the people, to divide them into different classes. The exchange was undertaken in

keeping with the power, mental ability, and intellect of the people. To make the decision in any

business require to focusing on different aspects that are related with the business in direct as

well as indirect manner. For this require to focus on every activities and how useful it in the

business. There are identifying different approaches, techniques and factors of management that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

utilize by the Tesco organisation to make decision in regard of any project investment (Junkus

and Berry, 2015). There are discussed various approaches such as:

Operational approach: This approach considers administration as an operation that is

focused on some specific managerial functions. Development is seen as a mechanism for doing

things by preparing, coordinating, and hiring, guiding and managing functions. It involves the

human and technological resource management cooperation (Blums and Weigand, 2017).

Communication center approach: This approach focus on management as a center that

receives, processes, and disseminates information, thereby underlining the importance of

communication in business administration.

Decision theory approach: The approach focuses on manager's decision-making role.

Accordingly, administrators’ primary emphasis is on decision-making. The significant

difficulties a manager faces are deciding what to accomplish, as well as how to actually

accomplish it. It concerns not just decision taking so everything that precedes a decision because

everything that accompanies it.

System approach: This approach treats a program as an organization. A system consists

of connected, interrelated components which form a unifying entire. Growing device is

composed of many subsystems. Likewise an institution is also considered in the form of agencies

as a scheme consisting of multiple sections although each dept is autonomous and achieves

particular predefined objectives, all are organized by upper executives.

Make and buy decision: A decision to make or purchase is a process of showing

between fabricating a product in-house or ordering it from an outsourced service. A make-or -

buy decision, also alluded to as an evaluation process, contrasts the costs and benefits with

manufacturing a desired product or service domestically with the health advantages related with

finding an external manufacturer for the systems needed. This approach helps to decision to take

right decision in regard of the business.

Limiting factor: Limiting variables contribute to limitations on the provision of

manufacturing services (e.g. labor requirements, labor hours or equipment) that prohibit a

company from optimizing its profits. If an company produces upwards of one item and

and Berry, 2015). There are discussed various approaches such as:

Operational approach: This approach considers administration as an operation that is

focused on some specific managerial functions. Development is seen as a mechanism for doing

things by preparing, coordinating, and hiring, guiding and managing functions. It involves the

human and technological resource management cooperation (Blums and Weigand, 2017).

Communication center approach: This approach focus on management as a center that

receives, processes, and disseminates information, thereby underlining the importance of

communication in business administration.

Decision theory approach: The approach focuses on manager's decision-making role.

Accordingly, administrators’ primary emphasis is on decision-making. The significant

difficulties a manager faces are deciding what to accomplish, as well as how to actually

accomplish it. It concerns not just decision taking so everything that precedes a decision because

everything that accompanies it.

System approach: This approach treats a program as an organization. A system consists

of connected, interrelated components which form a unifying entire. Growing device is

composed of many subsystems. Likewise an institution is also considered in the form of agencies

as a scheme consisting of multiple sections although each dept is autonomous and achieves

particular predefined objectives, all are organized by upper executives.

Make and buy decision: A decision to make or purchase is a process of showing

between fabricating a product in-house or ordering it from an outsourced service. A make-or -

buy decision, also alluded to as an evaluation process, contrasts the costs and benefits with

manufacturing a desired product or service domestically with the health advantages related with

finding an external manufacturer for the systems needed. This approach helps to decision to take

right decision in regard of the business.

Limiting factor: Limiting variables contribute to limitations on the provision of

manufacturing services (e.g. labor requirements, labor hours or equipment) that prohibit a

company from optimizing its profits. If an company produces upwards of one item and

experiences a shortfall in the availability of a specific asset (e.g. work hours, manufacturing

overhead or a components) needed to produce its helps determine, what amounts of its multiple

brands should be manufactured to boost revenue. On the basis of these factors an organization

take right decision in regard of business activities.

These approaches are using by the management of Tesco to make crucial decision of

business. Along with also use of some techniques of management such as:

Break even analysis: This tool allows a decision-maker to assess the possible alternatives due to

price, total price, and variable cost. Break-even analysis is a metric by which you can assess the

amount of revenue forced to support all operating expenses (Bratten, Causholli and Omer, 2019).

Linear programming: Linear programming is a quantitative approach used when making a

decision. This requires creating an optimal distribution of an institution's limited or insufficient

resources to accomplish a specified target. The term 'linear' shows the results between the

various variables are roughly proportional.

Financial analysis: This decision-making method is utilizing to measure an investment manager

feasibility, to determine the cash flows (the average time for the money gains to compensate for

an investor's actual amount), and to evaluate net income and financing activities.

Ratio analysis: It is an administrative method for understanding knowledge related to

accounting. The correlation between the two parameters is defined by ratios. For a given period,

the rudimentary financial ratios try comparing costs and revenues. The aim of carrying out

accounting ratios is to analyze financial information to assess a firm's positives and negatives, as

well as its family history and existing fiscal status.

Many factors impact an employee or the management. Via boundaries stretching,

customers can monitor these considerations/climates a method of collecting knowledge about

changes that could affect the organization’s strategy (Choudhary, Merkley and Schipper, 2019).

2. Stakeholder management and the management of conflicting objectives of various stakeholder

groups

Stakeholder management requires share holder recognition, review of their preferences

and causes, implementation of improved approaches to collaborate with investors, and

overhead or a components) needed to produce its helps determine, what amounts of its multiple

brands should be manufactured to boost revenue. On the basis of these factors an organization

take right decision in regard of business activities.

These approaches are using by the management of Tesco to make crucial decision of

business. Along with also use of some techniques of management such as:

Break even analysis: This tool allows a decision-maker to assess the possible alternatives due to

price, total price, and variable cost. Break-even analysis is a metric by which you can assess the

amount of revenue forced to support all operating expenses (Bratten, Causholli and Omer, 2019).

Linear programming: Linear programming is a quantitative approach used when making a

decision. This requires creating an optimal distribution of an institution's limited or insufficient

resources to accomplish a specified target. The term 'linear' shows the results between the

various variables are roughly proportional.

Financial analysis: This decision-making method is utilizing to measure an investment manager

feasibility, to determine the cash flows (the average time for the money gains to compensate for

an investor's actual amount), and to evaluate net income and financing activities.

Ratio analysis: It is an administrative method for understanding knowledge related to

accounting. The correlation between the two parameters is defined by ratios. For a given period,

the rudimentary financial ratios try comparing costs and revenues. The aim of carrying out

accounting ratios is to analyze financial information to assess a firm's positives and negatives, as

well as its family history and existing fiscal status.

Many factors impact an employee or the management. Via boundaries stretching,

customers can monitor these considerations/climates a method of collecting knowledge about

changes that could affect the organization’s strategy (Choudhary, Merkley and Schipper, 2019).

2. Stakeholder management and the management of conflicting objectives of various stakeholder

groups

Stakeholder management requires share holder recognition, review of their preferences

and causes, implementation of improved approaches to collaborate with investors, and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

implementation of the method. Repeated contact with the participants is necessary. The

Shareholders' desires and aspirations to be recognized. Often important is the management of

competing priorities and participation of stakeholders in project team actions and decisions.

These are all part of implementation process. The project manager is supposed to have the

capacity to spot stakeholders’ expectations and pressures to efficiently handle them. With

distinct expectations and objectives, companies have different types of internal and external

stakeholders. Occasionally these may conflict with that best interest. One of the implications of

managing projects involves tackling potential conflicts among both relevant parties. The first

industry that falls into this category by interested parties is that of the stockholders, for whom the

aspirations have always been considered primarily by company norms and values (Uchide and

Imanishi, 2016).

Therefore nowadays, project managers must be mindful of the existing views held by

business leaders on shareholder returns, taking into consideration the principle of contradiction.

It is worth noting that the outcomes of their chosen organization have been checked and can

testify to the validity of those opinions. Different parties have different goals. Distinct entities

may have conflicting priorities. For instance:

Companies typically want enormous revenues, and so can be hesitant to see the company

pay workers high wages.

A desire to start jobs to other countries can lower the amount of staffing. Hence, it will

help owners but operate to against rights of current workers who will lose their insurance.

Often, consumers struggle if they get better service.

3. Value of management accountings in cost control and maximizing shareholder value

Management accounting techniques are about "the procedure of determining, assessing

and transmitting financial data to facilitate users to make informed decisions and judgments

about the details. Accounting management strategies provide corporate executives with the

means to calculate and increasing income margins while reducing operating costs. The variety of

analytical methods is broad enough to fill classrooms for college students, and the international

accounting standards board provides widely esteemed accreditations from the accounting

industry. By extremely cautious of accounting management practices, groups are encouraged to

steer their institutions in the appropriate path and improve their cash flow (Harris, 2017). These

Shareholders' desires and aspirations to be recognized. Often important is the management of

competing priorities and participation of stakeholders in project team actions and decisions.

These are all part of implementation process. The project manager is supposed to have the

capacity to spot stakeholders’ expectations and pressures to efficiently handle them. With

distinct expectations and objectives, companies have different types of internal and external

stakeholders. Occasionally these may conflict with that best interest. One of the implications of

managing projects involves tackling potential conflicts among both relevant parties. The first

industry that falls into this category by interested parties is that of the stockholders, for whom the

aspirations have always been considered primarily by company norms and values (Uchide and

Imanishi, 2016).

Therefore nowadays, project managers must be mindful of the existing views held by

business leaders on shareholder returns, taking into consideration the principle of contradiction.

It is worth noting that the outcomes of their chosen organization have been checked and can

testify to the validity of those opinions. Different parties have different goals. Distinct entities

may have conflicting priorities. For instance:

Companies typically want enormous revenues, and so can be hesitant to see the company

pay workers high wages.

A desire to start jobs to other countries can lower the amount of staffing. Hence, it will

help owners but operate to against rights of current workers who will lose their insurance.

Often, consumers struggle if they get better service.

3. Value of management accountings in cost control and maximizing shareholder value

Management accounting techniques are about "the procedure of determining, assessing

and transmitting financial data to facilitate users to make informed decisions and judgments

about the details. Accounting management strategies provide corporate executives with the

means to calculate and increasing income margins while reducing operating costs. The variety of

analytical methods is broad enough to fill classrooms for college students, and the international

accounting standards board provides widely esteemed accreditations from the accounting

industry. By extremely cautious of accounting management practices, groups are encouraged to

steer their institutions in the appropriate path and improve their cash flow (Harris, 2017). These

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

techniques are valuable for business that helps in control the cost and maximizing the

shareholder value. There are discussed various types of techniques that are used by the Tesco in

their business activities such as:

Financial planning: Any business organization’s main goal is to increase profits. The

accomplishment of this goal is through reasonable or reasonable financial planning.

Consequently, financial planning is seen as the strongest approach for accomplishing company

goals.

Cost accounting: Cost accounting describes cost data in the manner of an item, method

wise, company wise, division wise, etc. Such expense results are processed to default one. A

two-cost analysis helps managers to assess the factors that are responsible for the disparity

between those prices (Duvanskaya, 2016).

Fund flow analysis: This study points out how the investment transfers from one time to

the next. In fact, this measure is also helpful when determining whether or not the fund is being

correctly spent in a year relative to the previous period. The shifts in capital expenditures and

operating resources are also discovered through such a research (Cao, Han and Zhu, 2018).

Marginal costing: Marginal costing methodology is used to set the sales price, pick best

selling mix, allow efficient use of resources input products or services, inventory level, approve

or reject bulk orders and international orders and such like. This is limited to a fixed, changeable,

and participation costs.

Decision making accounting: The option of some of the strongest and perhaps most

competitive alternatives can address a marketing problem. The related results are contrasted for

selecting such an alternative. Management accounting is therefore often used remedy the

company issue that arises from the growing difficulty of the business operations (Alkaraan,

2015).

4. Techniques for fraud detection and prevention approach for ethical decision making

Fraud has become a continuous, harmful and extraordinarily expensive issue for

companies and governmental organizations. Fraudulent strategies are more advanced and the

massive amount of criminal activities being committed has become tougher to maintain too. Yet

shareholder value. There are discussed various types of techniques that are used by the Tesco in

their business activities such as:

Financial planning: Any business organization’s main goal is to increase profits. The

accomplishment of this goal is through reasonable or reasonable financial planning.

Consequently, financial planning is seen as the strongest approach for accomplishing company

goals.

Cost accounting: Cost accounting describes cost data in the manner of an item, method

wise, company wise, division wise, etc. Such expense results are processed to default one. A

two-cost analysis helps managers to assess the factors that are responsible for the disparity

between those prices (Duvanskaya, 2016).

Fund flow analysis: This study points out how the investment transfers from one time to

the next. In fact, this measure is also helpful when determining whether or not the fund is being

correctly spent in a year relative to the previous period. The shifts in capital expenditures and

operating resources are also discovered through such a research (Cao, Han and Zhu, 2018).

Marginal costing: Marginal costing methodology is used to set the sales price, pick best

selling mix, allow efficient use of resources input products or services, inventory level, approve

or reject bulk orders and international orders and such like. This is limited to a fixed, changeable,

and participation costs.

Decision making accounting: The option of some of the strongest and perhaps most

competitive alternatives can address a marketing problem. The related results are contrasted for

selecting such an alternative. Management accounting is therefore often used remedy the

company issue that arises from the growing difficulty of the business operations (Alkaraan,

2015).

4. Techniques for fraud detection and prevention approach for ethical decision making

Fraud has become a continuous, harmful and extraordinarily expensive issue for

companies and governmental organizations. Fraudulent strategies are more advanced and the

massive amount of criminal activities being committed has become tougher to maintain too. Yet

still, even before strategic partnerships or over smart phones, customers and residents even now

request a satisfying transition. The secret is combating fraud with early detection and diagnosis

at the outset. Detection of fraud implies the recognition of real or suspected fraud inside an

institution. A company needs to incorporate appropriate processes and protocols to identify fraud

at or just before it happens at an advanced stage. Fraud analysis is carried out using the following

strategies (Edwards, 2018). The technique of fraudulent activities is critical for an enterprise to

figure out new types of corruption and so some conventional fraud. Even a professional fraudster

can overcome the most powerful detecting fraud methodology. The institution should therefore

be very intelligent in improving those very methodologies for detecting fraud. There are

discussed various techniques which are used for the fraud detection and prevention such as:

Proactive and Reactive approach: Proactive Techniques are methods that are

continually used in an effort to minimize the risk of the problematic behavior happening.

Reactive approaches are methods which can only be used after the activity takes place. They're

behavioral effects (or responses). A proactive approach aims to eliminate difficulties already

when they occur and a reactive approach is premised on reacting to events after they occur. The

primary difference between the two is the perspective that each gives when evaluating situations

and interactions. The distinction between a constructive approach being implemented and a

reactive approach is essentially one of planning and transparency (Ewert and Wagenhofer, 2016).

Where a new client requests for reviews from a building inspector, the plasterer will respond by

going over his list of previous clients and contacting them one at a to find out whether they will

be able to even provide feedback. A stronger approach would be to appoint one worker to

establish a customer service registry that has already demonstrated their desire to do just that.

The one who can supply high-quality references quickly would form a good benefit in a rivalry

in between contractor with a responsive comparison approach and one with a positive reference

strategy.

Manual and automated approach: While manual testing is performed by hand, system

software is based on the specific software packages that can be used. Application development

tools are used to perform tests, compare back, and start comparing runs today with original ones.

Such a method needs less government input, having various study new episodes at any given

time. In unit process (as the title implies) new tests are implemented manual process (by a human

request a satisfying transition. The secret is combating fraud with early detection and diagnosis

at the outset. Detection of fraud implies the recognition of real or suspected fraud inside an

institution. A company needs to incorporate appropriate processes and protocols to identify fraud

at or just before it happens at an advanced stage. Fraud analysis is carried out using the following

strategies (Edwards, 2018). The technique of fraudulent activities is critical for an enterprise to

figure out new types of corruption and so some conventional fraud. Even a professional fraudster

can overcome the most powerful detecting fraud methodology. The institution should therefore

be very intelligent in improving those very methodologies for detecting fraud. There are

discussed various techniques which are used for the fraud detection and prevention such as:

Proactive and Reactive approach: Proactive Techniques are methods that are

continually used in an effort to minimize the risk of the problematic behavior happening.

Reactive approaches are methods which can only be used after the activity takes place. They're

behavioral effects (or responses). A proactive approach aims to eliminate difficulties already

when they occur and a reactive approach is premised on reacting to events after they occur. The

primary difference between the two is the perspective that each gives when evaluating situations

and interactions. The distinction between a constructive approach being implemented and a

reactive approach is essentially one of planning and transparency (Ewert and Wagenhofer, 2016).

Where a new client requests for reviews from a building inspector, the plasterer will respond by

going over his list of previous clients and contacting them one at a to find out whether they will

be able to even provide feedback. A stronger approach would be to appoint one worker to

establish a customer service registry that has already demonstrated their desire to do just that.

The one who can supply high-quality references quickly would form a good benefit in a rivalry

in between contractor with a responsive comparison approach and one with a positive reference

strategy.

Manual and automated approach: While manual testing is performed by hand, system

software is based on the specific software packages that can be used. Application development

tools are used to perform tests, compare back, and start comparing runs today with original ones.

Such a method needs less government input, having various study new episodes at any given

time. In unit process (as the title implies) new tests are implemented manual process (by a human

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

being that is) with little weapon or screenplay assistance. But testing phase is conducted with the

aid of tools, scripts, and applications, with test automation. Evaluation is an essential part of any

worthwhile venture with the apps (Chyzhmar, Farynnyk and Stupnyk, 2017).

5. Reflection on understanding

As per the above four question I can understand various things that impact on the

professional skills. When an organisation wants to take decision in regard of profitability so that

time focus on various range, method and approaches. These are based on the financial

accounting and this time I can understand the various approaches use by entity in decision

making procedure.

To manage the business activities require t mange stakeholder which is new concept and

learn during to my research and communicate various types of stakeholders of particular

organization. As a result it helps to increase my knowledge effectively.

To increase the shareholder value and cost control based on the management accounting

techniques. Before research I know few techniques but at the time research I can learn various

techniques that use by the business entity with various purposes.

I can rely that in the business face the problem of data fraud so for this apply different

techniques to overcome this. At the time of research I can face various problem that impact on

the skills but I can learn many things and use different methods of learning as well as research.

SCENARIO B

1. Data obtained that help to inform operational and strategic decisions

Ratio Analysis: Ratio analysis can be characterized as the method of evaluating the

financial metrics used only to indicate a company's long - term economic health using only a few

types of methods, including such liquidity, productivity, operation, debt, business, and liquidity,

capacity and distribution percentages (Throsby, 2016). There are presenting some calculations of

Tesco plc such as:

Calculation of Ratio

aid of tools, scripts, and applications, with test automation. Evaluation is an essential part of any

worthwhile venture with the apps (Chyzhmar, Farynnyk and Stupnyk, 2017).

5. Reflection on understanding

As per the above four question I can understand various things that impact on the

professional skills. When an organisation wants to take decision in regard of profitability so that

time focus on various range, method and approaches. These are based on the financial

accounting and this time I can understand the various approaches use by entity in decision

making procedure.

To manage the business activities require t mange stakeholder which is new concept and

learn during to my research and communicate various types of stakeholders of particular

organization. As a result it helps to increase my knowledge effectively.

To increase the shareholder value and cost control based on the management accounting

techniques. Before research I know few techniques but at the time research I can learn various

techniques that use by the business entity with various purposes.

I can rely that in the business face the problem of data fraud so for this apply different

techniques to overcome this. At the time of research I can face various problem that impact on

the skills but I can learn many things and use different methods of learning as well as research.

SCENARIO B

1. Data obtained that help to inform operational and strategic decisions

Ratio Analysis: Ratio analysis can be characterized as the method of evaluating the

financial metrics used only to indicate a company's long - term economic health using only a few

types of methods, including such liquidity, productivity, operation, debt, business, and liquidity,

capacity and distribution percentages (Throsby, 2016). There are presenting some calculations of

Tesco plc such as:

Calculation of Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

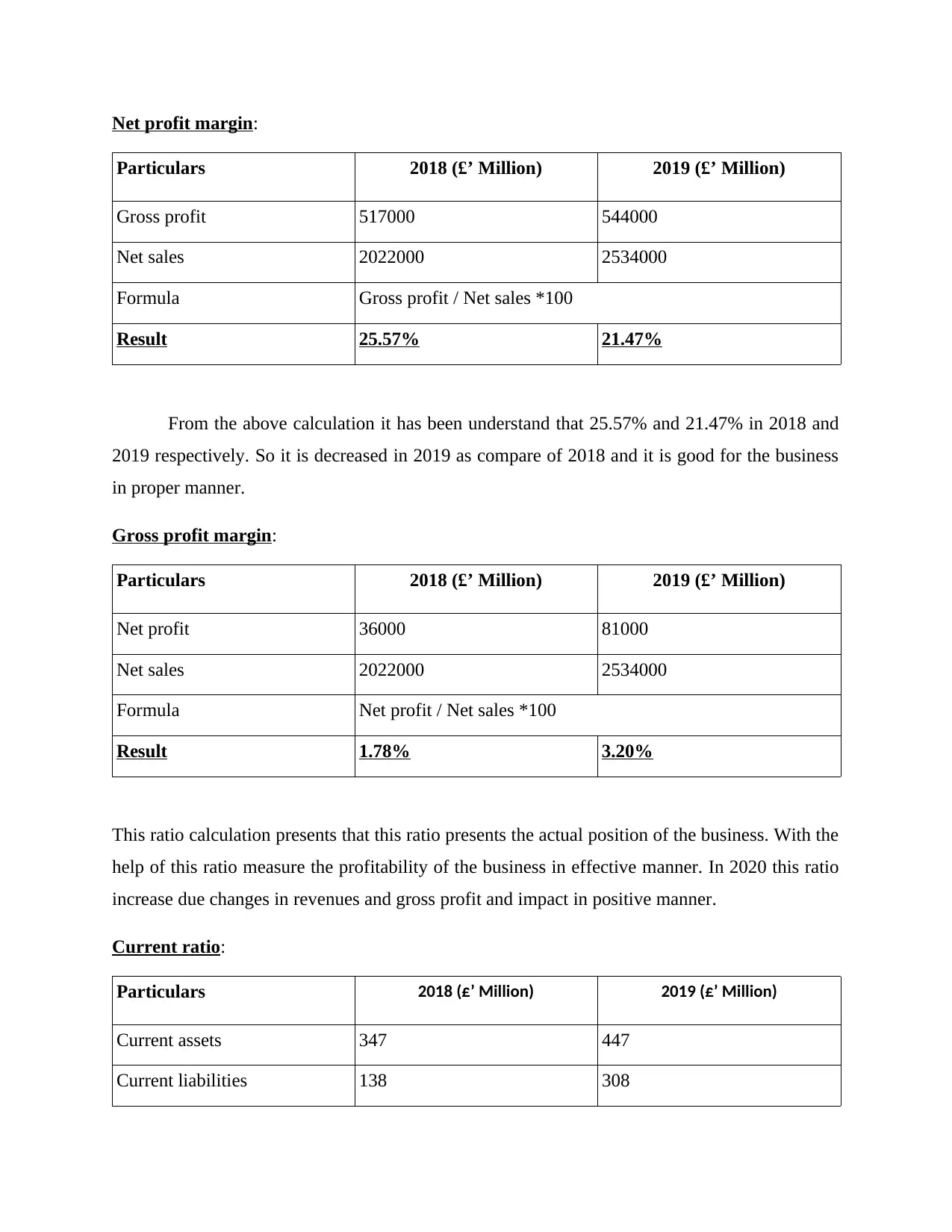

Net profit margin:

Particulars 2018 (£’ Million) 2019 (£’ Million)

Gross profit 517000 544000

Net sales 2022000 2534000

Formula Gross profit / Net sales *100

Result 25.57% 21.47%

From the above calculation it has been understand that 25.57% and 21.47% in 2018 and

2019 respectively. So it is decreased in 2019 as compare of 2018 and it is good for the business

in proper manner.

Gross profit margin:

Particulars 2018 (£’ Million) 2019 (£’ Million)

Net profit 36000 81000

Net sales 2022000 2534000

Formula Net profit / Net sales *100

Result 1.78% 3.20%

This ratio calculation presents that this ratio presents the actual position of the business. With the

help of this ratio measure the profitability of the business in effective manner. In 2020 this ratio

increase due changes in revenues and gross profit and impact in positive manner.

Current ratio:

Particulars 2018 (£’ Million) 2019 (£’ Million)

Current assets 347 447

Current liabilities 138 308

Particulars 2018 (£’ Million) 2019 (£’ Million)

Gross profit 517000 544000

Net sales 2022000 2534000

Formula Gross profit / Net sales *100

Result 25.57% 21.47%

From the above calculation it has been understand that 25.57% and 21.47% in 2018 and

2019 respectively. So it is decreased in 2019 as compare of 2018 and it is good for the business

in proper manner.

Gross profit margin:

Particulars 2018 (£’ Million) 2019 (£’ Million)

Net profit 36000 81000

Net sales 2022000 2534000

Formula Net profit / Net sales *100

Result 1.78% 3.20%

This ratio calculation presents that this ratio presents the actual position of the business. With the

help of this ratio measure the profitability of the business in effective manner. In 2020 this ratio

increase due changes in revenues and gross profit and impact in positive manner.

Current ratio:

Particulars 2018 (£’ Million) 2019 (£’ Million)

Current assets 347 447

Current liabilities 138 308

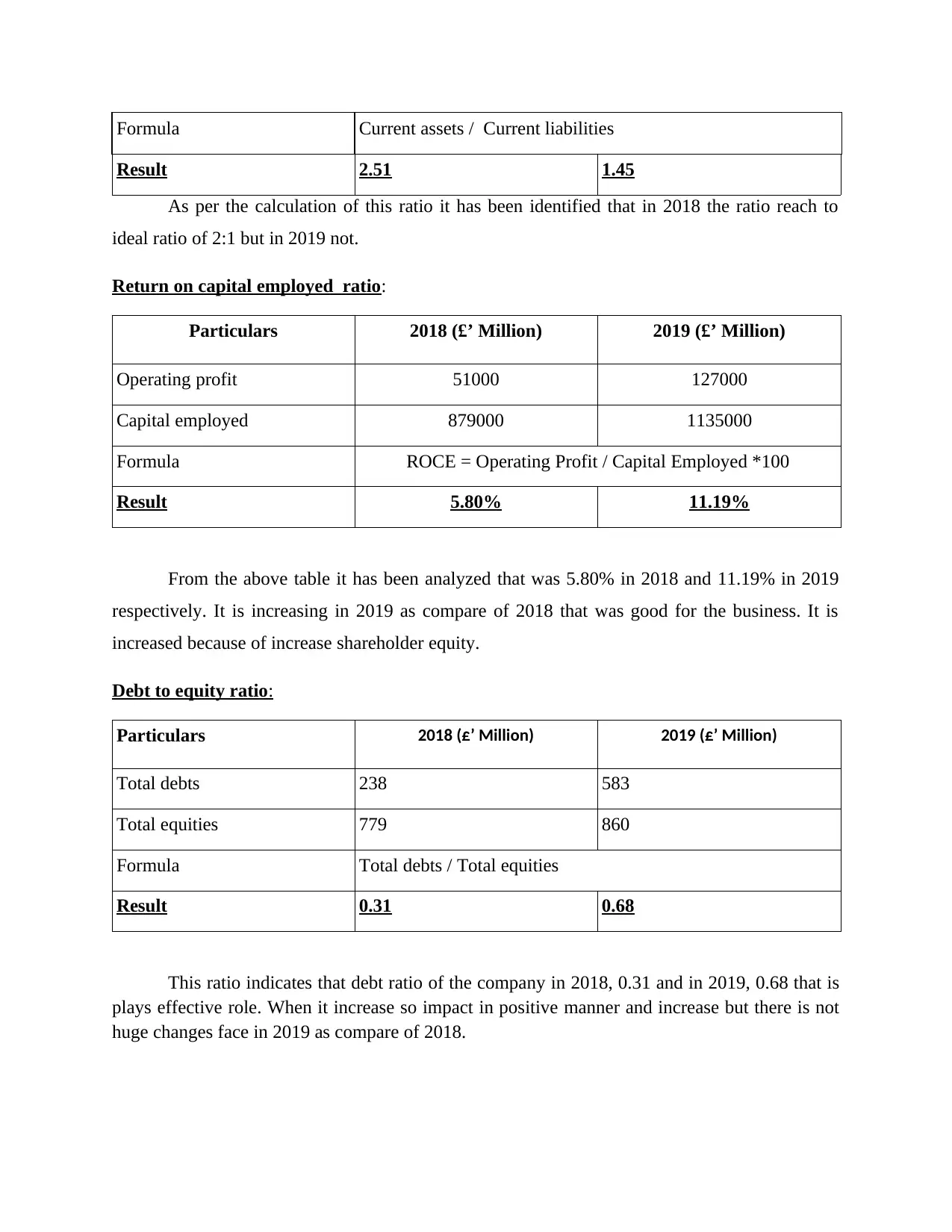

Formula Current assets / Current liabilities

Result 2.51 1.45

As per the calculation of this ratio it has been identified that in 2018 the ratio reach to

ideal ratio of 2:1 but in 2019 not.

Return on capital employed ratio:

Particulars 2018 (£’ Million) 2019 (£’ Million)

Operating profit 51000 127000

Capital employed 879000 1135000

Formula ROCE = Operating Profit / Capital Employed *100

Result 5.80% 11.19%

From the above table it has been analyzed that was 5.80% in 2018 and 11.19% in 2019

respectively. It is increasing in 2019 as compare of 2018 that was good for the business. It is

increased because of increase shareholder equity.

Debt to equity ratio:

Particulars 2018 (£’ Million) 2019 (£’ Million)

Total debts 238 583

Total equities 779 860

Formula Total debts / Total equities

Result 0.31 0.68

This ratio indicates that debt ratio of the company in 2018, 0.31 and in 2019, 0.68 that is

plays effective role. When it increase so impact in positive manner and increase but there is not

huge changes face in 2019 as compare of 2018.

Result 2.51 1.45

As per the calculation of this ratio it has been identified that in 2018 the ratio reach to

ideal ratio of 2:1 but in 2019 not.

Return on capital employed ratio:

Particulars 2018 (£’ Million) 2019 (£’ Million)

Operating profit 51000 127000

Capital employed 879000 1135000

Formula ROCE = Operating Profit / Capital Employed *100

Result 5.80% 11.19%

From the above table it has been analyzed that was 5.80% in 2018 and 11.19% in 2019

respectively. It is increasing in 2019 as compare of 2018 that was good for the business. It is

increased because of increase shareholder equity.

Debt to equity ratio:

Particulars 2018 (£’ Million) 2019 (£’ Million)

Total debts 238 583

Total equities 779 860

Formula Total debts / Total equities

Result 0.31 0.68

This ratio indicates that debt ratio of the company in 2018, 0.31 and in 2019, 0.68 that is

plays effective role. When it increase so impact in positive manner and increase but there is not

huge changes face in 2019 as compare of 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.