Management Accounting Report: Tesco's Financial Performance Analysis

VerifiedAdded on 2023/01/06

|14

|3884

|29

Report

AI Summary

This report provides a comprehensive analysis of management accounting, using Tesco as a case study. It begins with an introduction to management accounting, its essential requirements, and different accounting systems, including price optimization, inventory management, cost accounting, and job costing. The report then explores various methods used for management accounting reporting, such as budget reports, account receivable aging reports, job cost reports, and inventory and manufacturing reports. Furthermore, it delves into calculating costs using marginal and absorption costing to create income statements. The report also discusses the benefits and disadvantages of different planning tools, comparing how organizations manage management accounting to deal with financial problems and issues. The report concludes with a summary of findings and references.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................3

MAIN BODY.............................................................................................................................3

TASK1.......................................................................................................................................3

P1 Management accounting and its essential requirements of different types of

management accounting systems...........................................................................................3

P2 Methods used for management accounting reporting.......................................................5

TASK2.......................................................................................................................................7

P3 Calculating costs using suitable methods of cost examination to make an income

statement using marginal and absorption costs................................................................7

TASK 3......................................................................................................................................9

P4: Benefits and disadvantage of various tools of planning..................................................9

TASK 4....................................................................................................................................11

P5: Compare how organisations are managing the function of management accounting to

deal with different financial problems & issues...................................................................11

CONCLUSION........................................................................................................................12

REFERNCES...........................................................................................................................13

INTRODUCTION......................................................................................................................3

MAIN BODY.............................................................................................................................3

TASK1.......................................................................................................................................3

P1 Management accounting and its essential requirements of different types of

management accounting systems...........................................................................................3

P2 Methods used for management accounting reporting.......................................................5

TASK2.......................................................................................................................................7

P3 Calculating costs using suitable methods of cost examination to make an income

statement using marginal and absorption costs................................................................7

TASK 3......................................................................................................................................9

P4: Benefits and disadvantage of various tools of planning..................................................9

TASK 4....................................................................................................................................11

P5: Compare how organisations are managing the function of management accounting to

deal with different financial problems & issues...................................................................11

CONCLUSION........................................................................................................................12

REFERNCES...........................................................................................................................13

INTRODUCTION

Management accounting can be defined as in that part of organisation which is

directly related to managing the provisions of the accounting information system and help the

stakeholders in identifying the current financial position of the organisation by managing

different kind of accounts. In relation to the current report, Tesco is the chosen organisation.

It is a British multinational retail organisation which is selling products used in the global

world. Tesco is operating in more than 13 countries within the retail industry since 1919.

Under the current report, there is a discussion about the management accounting and the

requirements of different kind of management accounting system within the organisation

where the explanation related to method used for management accounting will also be

considered (Gibassier, 2017). There is also use of practical illustrations to define the

absorption and fixed cost implemented by the organisation. In the end of the report, there is a

discussion about the advantages and disadvantages of various budgetary control tools as well

as comparison between management systems to respond different financial problems by

using two organisations.

MAIN BODY

TASK1

P1 Management accounting and its essential requirements of different types of management

accounting systems

Management accounting can be defined as a process within organization which is

related to identification and valuation of different accounts to determine the financial position

of the company as well as use the information for management of finance. In relation to the

organization, management accounting can be defining as system which provides a particular

process to the organization for recording its different accounts to identify its current position

for achieving the goals and objectives.

According to institute of management accounting "Management accounting is that

field of management which is related to Management of financial and cost accounts of the

organization which help the management in taking different decisions related to planning and

increasing the performance of the organization (Armitage, , Webb, and Glynn,, 201). This

system is directly associated with the current position of the organization because it provide

the analysis of financial accounting system of the firm which are prime standard for

determining the financial position of the organization in the current market. Management

Management accounting can be defined as in that part of organisation which is

directly related to managing the provisions of the accounting information system and help the

stakeholders in identifying the current financial position of the organisation by managing

different kind of accounts. In relation to the current report, Tesco is the chosen organisation.

It is a British multinational retail organisation which is selling products used in the global

world. Tesco is operating in more than 13 countries within the retail industry since 1919.

Under the current report, there is a discussion about the management accounting and the

requirements of different kind of management accounting system within the organisation

where the explanation related to method used for management accounting will also be

considered (Gibassier, 2017). There is also use of practical illustrations to define the

absorption and fixed cost implemented by the organisation. In the end of the report, there is a

discussion about the advantages and disadvantages of various budgetary control tools as well

as comparison between management systems to respond different financial problems by

using two organisations.

MAIN BODY

TASK1

P1 Management accounting and its essential requirements of different types of management

accounting systems

Management accounting can be defined as a process within organization which is

related to identification and valuation of different accounts to determine the financial position

of the company as well as use the information for management of finance. In relation to the

organization, management accounting can be defining as system which provides a particular

process to the organization for recording its different accounts to identify its current position

for achieving the goals and objectives.

According to institute of management accounting "Management accounting is that

field of management which is related to Management of financial and cost accounts of the

organization which help the management in taking different decisions related to planning and

increasing the performance of the organization (Armitage, , Webb, and Glynn,, 201). This

system is directly associated with the current position of the organization because it provide

the analysis of financial accounting system of the firm which are prime standard for

determining the financial position of the organization in the current market. Management

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting can also use and system which is related to controlling and monitoring the cost of

different products and services offered by the organization and various activities which are

involved in process of business”.

In relation to Tesco, there are ample of benefits to organization by using the management

function which are discussed below:

Profit maximization: management accounting is helpful to the organization in

maximizing the profits because it is related to management of cost the organization which it

implements on different kind of activities. With help of management of cost organization

and easily identify with actual amount of profit as a financial position of the company within

market.

Efficiency booster: Management accounting also acts as a tool to increase the

efficiency of employees within the organization as well as other resources of the firm. This is

because management accounting helps in identification of various cost involved which

directly related to evaluation of the performance of different individuals and their roles. This

will increase the efficiency of individuals while working on a job because they can identify

their performance and can use the tools of management accounting in management of cost

(Kihn. and Näsi, , 2017).

Various systems that are used in management accounting

Price optimization system: under the system of management accounting or

organization use a calculation instrument which is directly related to managing the

performance of accounting system within the organization to identify the response of

customer behavior and use this customer behavior for managing the prices of the product

offered by organization (Sugahara, , Daidj and Ushio, 2017). It is the best suitable method for

the organization like Tesco, because It helped the firm in determining the price of the product

identification of their actual cost and expenditure which is involved while producing the

products and services. Major objective behind this system is to increase the profitability of

the organization by using appropriate pricing strategies and structure for the products and

services offered by the firm within the market.

Inventory management system: Inventory management system is also important

part in the marketing accounting system which is related to focusing on the organization

product by managing inventory and classifying the inventory in finished, unfinished and

different products and services offered by the organization and various activities which are

involved in process of business”.

In relation to Tesco, there are ample of benefits to organization by using the management

function which are discussed below:

Profit maximization: management accounting is helpful to the organization in

maximizing the profits because it is related to management of cost the organization which it

implements on different kind of activities. With help of management of cost organization

and easily identify with actual amount of profit as a financial position of the company within

market.

Efficiency booster: Management accounting also acts as a tool to increase the

efficiency of employees within the organization as well as other resources of the firm. This is

because management accounting helps in identification of various cost involved which

directly related to evaluation of the performance of different individuals and their roles. This

will increase the efficiency of individuals while working on a job because they can identify

their performance and can use the tools of management accounting in management of cost

(Kihn. and Näsi, , 2017).

Various systems that are used in management accounting

Price optimization system: under the system of management accounting or

organization use a calculation instrument which is directly related to managing the

performance of accounting system within the organization to identify the response of

customer behavior and use this customer behavior for managing the prices of the product

offered by organization (Sugahara, , Daidj and Ushio, 2017). It is the best suitable method for

the organization like Tesco, because It helped the firm in determining the price of the product

identification of their actual cost and expenditure which is involved while producing the

products and services. Major objective behind this system is to increase the profitability of

the organization by using appropriate pricing strategies and structure for the products and

services offered by the firm within the market.

Inventory management system: Inventory management system is also important

part in the marketing accounting system which is related to focusing on the organization

product by managing inventory and classifying the inventory in finished, unfinished and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

processing goods. Under this system, organization used to manage the inventory by the help

of software and hardware. This software involved pre-determined processes for managing the

inventory where various kind of methods like FIFO, LIFO and many more used by the

organization to manage the inventory with inventory management system.

Cost accounting system: Cost accounting system can be defined as in that part of

management accounting which is directly related to identification of the overall cost of the

product identification of various factors and cost involved within the manufacturing of the

product (Maas, , Schaltegger and Crutzen, 2016). It is mandatory part for the organization to

adopt a cost accounting system within the firm so that it can identify the overall

manufacturing cost by using different kind of cost like operating cost, absorption cost,

variable cost, fixed cost and many more. Management accounting style includes different

kind of diagram charts. It includes sales chart marginal cost chart and other which help in

identification of cost related to the product and manage the performance by identification of

cost involved.

Job costing system: It is that type of costing system which include identification of

the overall cost and expenses which are incurred by the organization on a particular job.

These expenses are related to development of products and services in relation to a particular

activity. These activities include sales of product, purchase of products and many other

operations within the organization. It act as an important system within the management

accounting of organization because there are various industries like manufacturing in process

which are highly dependent on the job costing system. In relation to the system of job

costing, organization used to identify the cost involved in a particular activity so that it can

decide the pricing of the product by managing the compensation to labors and other factors

involved in the activity. This method can be used by the Tesco in identification of actual

profits by determination of revenues and expenses on products and services offered by the

organization according to the particular job (Quattrone, 2016). It can be analyzed from

above mentioned information there are different kind of functions performed under the

management accounting system. It can also see that management accounting is a great impact

on the organization show a firm must use a proper system within the management accounting

to manage its accounts and identify the actual position within the market.

P2 Methods used for management accounting reporting

Management accounting reporting

of software and hardware. This software involved pre-determined processes for managing the

inventory where various kind of methods like FIFO, LIFO and many more used by the

organization to manage the inventory with inventory management system.

Cost accounting system: Cost accounting system can be defined as in that part of

management accounting which is directly related to identification of the overall cost of the

product identification of various factors and cost involved within the manufacturing of the

product (Maas, , Schaltegger and Crutzen, 2016). It is mandatory part for the organization to

adopt a cost accounting system within the firm so that it can identify the overall

manufacturing cost by using different kind of cost like operating cost, absorption cost,

variable cost, fixed cost and many more. Management accounting style includes different

kind of diagram charts. It includes sales chart marginal cost chart and other which help in

identification of cost related to the product and manage the performance by identification of

cost involved.

Job costing system: It is that type of costing system which include identification of

the overall cost and expenses which are incurred by the organization on a particular job.

These expenses are related to development of products and services in relation to a particular

activity. These activities include sales of product, purchase of products and many other

operations within the organization. It act as an important system within the management

accounting of organization because there are various industries like manufacturing in process

which are highly dependent on the job costing system. In relation to the system of job

costing, organization used to identify the cost involved in a particular activity so that it can

decide the pricing of the product by managing the compensation to labors and other factors

involved in the activity. This method can be used by the Tesco in identification of actual

profits by determination of revenues and expenses on products and services offered by the

organization according to the particular job (Quattrone, 2016). It can be analyzed from

above mentioned information there are different kind of functions performed under the

management accounting system. It can also see that management accounting is a great impact

on the organization show a firm must use a proper system within the management accounting

to manage its accounts and identify the actual position within the market.

P2 Methods used for management accounting reporting

Management accounting reporting

Accounting reports can be defined as a crucial part of the organisation which healthy

form in framing a complete picture of the business performance. In relation to the

organisation, it is mandatory for the organisation to produce valid accounting reports in every

quarter so that it can identify the current position of the business. Accounting reports can be

defined as a financial status of the business which is directly related to presentation of the

data over a specific period of time (Holopainen, Niskanen and Rissanen, 2019). These

reports are based on financial information from the accounting records which can be used by

the organisation and filled with the data related to transactions operational cost product

profitability and regional sales. these reports are essential for the organisation as well as

manager so that they can take business decisions in an effective way by identifying the

current position of the business. There are different kind of accounting reports which are

discussed below:

Budget report: Budget report can be defined as in most fundamental report within

the organisation which is included under the managerial accounting system. Reports are

essential for the business owners to understand and control the cost on the overall enterprises.

This is because these reports provide the data related to unified organisation or several

departments in an appropriate manner where the decision-making can be facilitated. Under

budget reports, there is evaluation of expenses in prior years so that it can become possible to

estimate t yearhe overall budget for particular year. This is also useful to the organisation in

cutting the cost the placing a proper budget to a particular department and identification of

each and every aspect of a department by evaluation of their cost.

Account receivable aging report: These are also essential accounting reports to the

organisation specially deals in credit (Abernethy, and Wallis, 2019). This type of report is

generally useful to the organisation in identification of the credit customers where it provide

the overview of the balance according to the age. This report helps organisation in dividing

with credit customer in separate categories which are classified as 30, 60 and 90 day’s credit

period. Organisation to manage the credit policies so that it can manage account receivable

ageing report in an appropriate we identify the late payment from the customers and charged

interest according to the requirements and period of late payment.

Job cost report: It include that kind of reports which are directly related to providing

the side by side view of total cost implemented in a single project compared to the total

expected revenue from the project. it is important report in relation to the organisation

form in framing a complete picture of the business performance. In relation to the

organisation, it is mandatory for the organisation to produce valid accounting reports in every

quarter so that it can identify the current position of the business. Accounting reports can be

defined as a financial status of the business which is directly related to presentation of the

data over a specific period of time (Holopainen, Niskanen and Rissanen, 2019). These

reports are based on financial information from the accounting records which can be used by

the organisation and filled with the data related to transactions operational cost product

profitability and regional sales. these reports are essential for the organisation as well as

manager so that they can take business decisions in an effective way by identifying the

current position of the business. There are different kind of accounting reports which are

discussed below:

Budget report: Budget report can be defined as in most fundamental report within

the organisation which is included under the managerial accounting system. Reports are

essential for the business owners to understand and control the cost on the overall enterprises.

This is because these reports provide the data related to unified organisation or several

departments in an appropriate manner where the decision-making can be facilitated. Under

budget reports, there is evaluation of expenses in prior years so that it can become possible to

estimate t yearhe overall budget for particular year. This is also useful to the organisation in

cutting the cost the placing a proper budget to a particular department and identification of

each and every aspect of a department by evaluation of their cost.

Account receivable aging report: These are also essential accounting reports to the

organisation specially deals in credit (Abernethy, and Wallis, 2019). This type of report is

generally useful to the organisation in identification of the credit customers where it provide

the overview of the balance according to the age. This report helps organisation in dividing

with credit customer in separate categories which are classified as 30, 60 and 90 day’s credit

period. Organisation to manage the credit policies so that it can manage account receivable

ageing report in an appropriate we identify the late payment from the customers and charged

interest according to the requirements and period of late payment.

Job cost report: It include that kind of reports which are directly related to providing

the side by side view of total cost implemented in a single project compared to the total

expected revenue from the project. it is important report in relation to the organisation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performing within the retail industry because It helped the leaders in evaluating the

profitability of a particular project and taking decision according to it. It help in optimising

the resources by identification of the the profitability within the operation where organisation

can take decisions related to continuation or closure of the operation on the basis of job cost

reports (Hutaibat, and Alhatabat,, 2019).

Inventory and manufacturing report: In relation to these reports get include

physical product specially those manufactured with no fault tolerance. These reports are

important to the organisation in identification of inventory and manufacturing process where

it helps in centralising the data of inventory cost labour and other forms of overheads which

are involved with the process of production. It helps the organisation in identification of

production processes for providing raw data as well as manage the assembly of machineries

so that management can get knowledge about different aspects of a process related to

inventory and manufacturing of products and services (Joshiand Li, 2016).

It can be evaluated from the above that there are various kind of accounting reports

which can be used by the organisation for managing its functions as well as identification of

opportunities within the market. It can be seen that budget reports account receivable aging

reports and job costing reports can be used in identification of appropriate cost and using the

tools and techniques for achievement of objectives.

TASK2

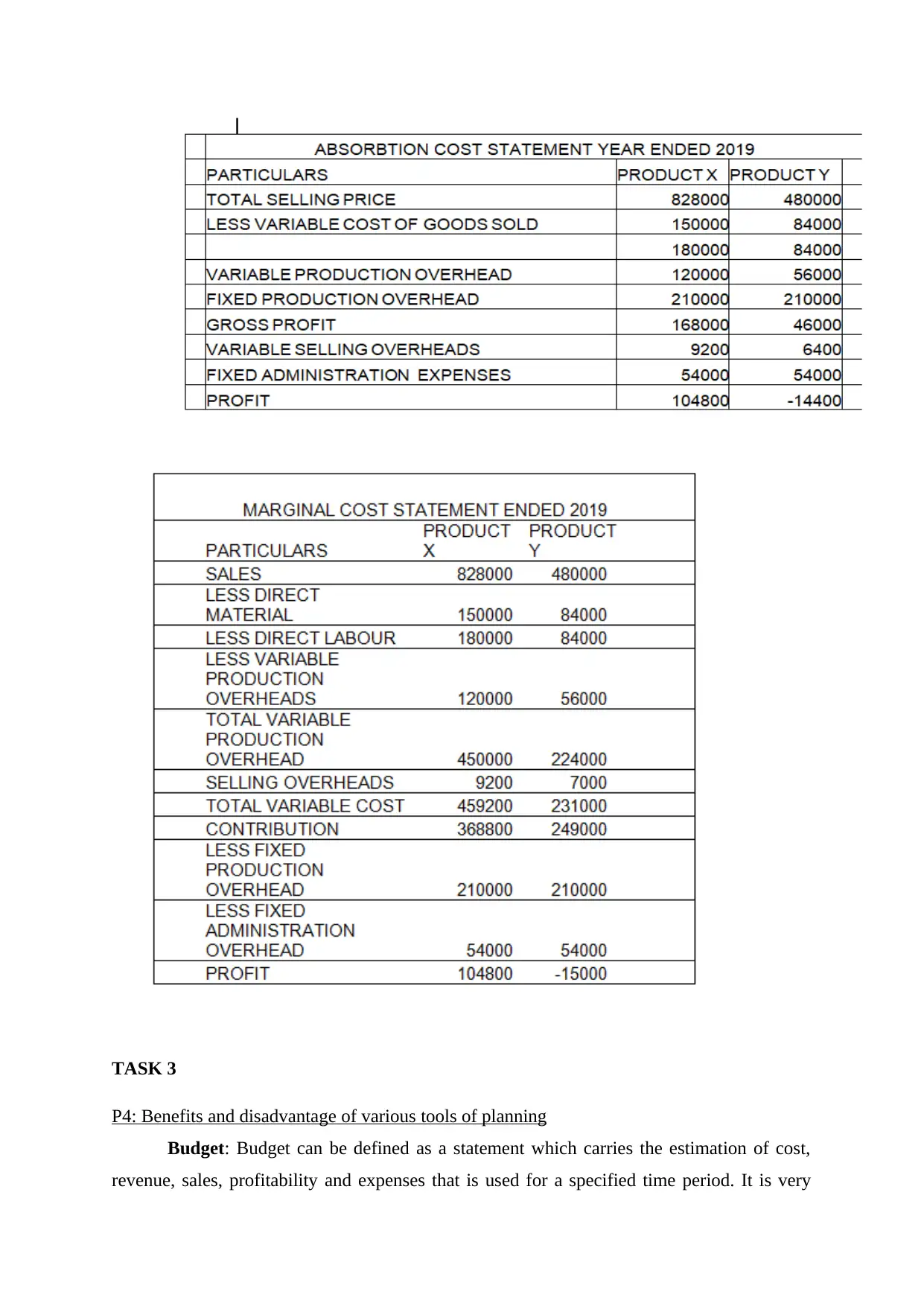

P3 Calculating costs using suitable methods of cost examination to make an income statement

using marginal and absorption costs

Income statement: Income statement can we define a document which is related to financial

position of the organization in a particular period of time. it shows how the revenues of the

organization are transformed in the net income and net profit by adjusting overall expenses.

Main purpose of income statement within the organization is to show the manager and the

investors about the financial position of the organization in relation to profit and loss during

particular period. it is necessary for the organization to perform separate income statement

which credit ability of the firm within the market and its financial position to attract the

investor (Collis, and Hussey, 2017)

Absorption cost: Absorption cost can be defined as in that kind of cost which includes

the full cost of manufacturing for a particular service within the organization. It is not only

profitability of a particular project and taking decision according to it. It help in optimising

the resources by identification of the the profitability within the operation where organisation

can take decisions related to continuation or closure of the operation on the basis of job cost

reports (Hutaibat, and Alhatabat,, 2019).

Inventory and manufacturing report: In relation to these reports get include

physical product specially those manufactured with no fault tolerance. These reports are

important to the organisation in identification of inventory and manufacturing process where

it helps in centralising the data of inventory cost labour and other forms of overheads which

are involved with the process of production. It helps the organisation in identification of

production processes for providing raw data as well as manage the assembly of machineries

so that management can get knowledge about different aspects of a process related to

inventory and manufacturing of products and services (Joshiand Li, 2016).

It can be evaluated from the above that there are various kind of accounting reports

which can be used by the organisation for managing its functions as well as identification of

opportunities within the market. It can be seen that budget reports account receivable aging

reports and job costing reports can be used in identification of appropriate cost and using the

tools and techniques for achievement of objectives.

TASK2

P3 Calculating costs using suitable methods of cost examination to make an income statement

using marginal and absorption costs

Income statement: Income statement can we define a document which is related to financial

position of the organization in a particular period of time. it shows how the revenues of the

organization are transformed in the net income and net profit by adjusting overall expenses.

Main purpose of income statement within the organization is to show the manager and the

investors about the financial position of the organization in relation to profit and loss during

particular period. it is necessary for the organization to perform separate income statement

which credit ability of the firm within the market and its financial position to attract the

investor (Collis, and Hussey, 2017)

Absorption cost: Absorption cost can be defined as in that kind of cost which includes

the full cost of manufacturing for a particular service within the organization. It is not only

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the cost of materials and Labor but also include the manufacturing overhead whether the

fixed or variable (Van der Stede, 2017). The cost of each cost center can be direct or indirect

where the direct costs can be easily identified within the individual cost centers but indirect

cost cannot be identified easily within a cost center. This is the reason behind using the

concept of absorption cause which distributes the overhead among the departments in an

appropriate way for identification of a particular cost which is absorbed by a particular

department.

fixed or variable (Van der Stede, 2017). The cost of each cost center can be direct or indirect

where the direct costs can be easily identified within the individual cost centers but indirect

cost cannot be identified easily within a cost center. This is the reason behind using the

concept of absorption cause which distributes the overhead among the departments in an

appropriate way for identification of a particular cost which is absorbed by a particular

department.

TASK 3

P4: Benefits and disadvantage of various tools of planning

Budget: Budget can be defined as a statement which carries the estimation of cost,

revenue, sales, profitability and expenses that is used for a specified time period. It is very

P4: Benefits and disadvantage of various tools of planning

Budget: Budget can be defined as a statement which carries the estimation of cost,

revenue, sales, profitability and expenses that is used for a specified time period. It is very

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

helpful for a organisation to ensure its timely internal management and to measure the

performance according to set standards (Cuzdriorean, 2017). Budgetary control is a

technique that can be used for the purpose of determination of sales accordance to some

budgeted figures but the time period is specified. After which the actual calculation is made

to understand these figures in context of a organisation.

There are some specific tools that are used for the purpose of budgetary planning:

Flexible budget: This is a tool that is used in case of budgetary control so that

activities can be easily managed according to the requirement of organisation. Innovation

drinks can also use this for the purpose of monitoring their sales as compared to the standard

sales that is desired by the organisation for a specific time period.

Benefits: It is used for determining the required level of production. According to sales of a

specific period future prediction can be done. Organisation has a motive to minimise the

inventory cost.

Limitation: There is need of highly trained staff so that there can be proper management of

work according to future requirements (Kumarasiri, and Jubb, 2016). Flexible budget is not

financially viable to organisations as there is need of high monetary compensation that has to

be paid to trained staff.

Master budget: It consist lower level of budget, in this divisional budget is summed

in one budget that is combined in one single department. This consists of financial planning,

cash flow forecasting, budgeted statements. In innocent drinks this type of budget has to be

prepared for a time of one financial year.

Benefits: This budget is the summary of management information. It is reflecting the whole

expense and associated revenue of each department. It summarises all the budgets together so

there is no need to maintain separate budgets.

Limitation: It is difficult to upgrade to budget so there comes a need to make timely changes

that can help in meeting the overall budget requirements. There is need to timely make

Changes as the requirement are changing very fast this can affect the overall procurer of

financial management in a organisation like innocent drinks.

performance according to set standards (Cuzdriorean, 2017). Budgetary control is a

technique that can be used for the purpose of determination of sales accordance to some

budgeted figures but the time period is specified. After which the actual calculation is made

to understand these figures in context of a organisation.

There are some specific tools that are used for the purpose of budgetary planning:

Flexible budget: This is a tool that is used in case of budgetary control so that

activities can be easily managed according to the requirement of organisation. Innovation

drinks can also use this for the purpose of monitoring their sales as compared to the standard

sales that is desired by the organisation for a specific time period.

Benefits: It is used for determining the required level of production. According to sales of a

specific period future prediction can be done. Organisation has a motive to minimise the

inventory cost.

Limitation: There is need of highly trained staff so that there can be proper management of

work according to future requirements (Kumarasiri, and Jubb, 2016). Flexible budget is not

financially viable to organisations as there is need of high monetary compensation that has to

be paid to trained staff.

Master budget: It consist lower level of budget, in this divisional budget is summed

in one budget that is combined in one single department. This consists of financial planning,

cash flow forecasting, budgeted statements. In innocent drinks this type of budget has to be

prepared for a time of one financial year.

Benefits: This budget is the summary of management information. It is reflecting the whole

expense and associated revenue of each department. It summarises all the budgets together so

there is no need to maintain separate budgets.

Limitation: It is difficult to upgrade to budget so there comes a need to make timely changes

that can help in meeting the overall budget requirements. There is need to timely make

Changes as the requirement are changing very fast this can affect the overall procurer of

financial management in a organisation like innocent drinks.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

P5: Compare how organisations are managing the function of management accounting to

deal with different financial problems & issues

Financial issues are related to limited supply of financial resources. There are issues

that can happen because of misrepresentation, default of financial managers or sometimes

financial departments. Some of the financial issues are mentioned below:

High expense: There are some situations where Innocent drinks have to make lot of

promotion while they are launching some new products (Alsharari, and Youssef, 2017). They

have to distribute their free samples so that people can realise its taste and then purchase.

Financial governance: This is a method that can be adopted by organisations for the purpose

of gathering of the necessary information. It helps in enhancing the authenticity of financial

information so that further decision can be made on this basis. This helps in fast decision

making so that no opportunity can be lost.

Benchmarking: It is a approach that can be adopted by organisation to work according to

certain specified standards. This is a very effective tool that can help in setting benchmarks

and then working according to such pre set benchmarks.

For the Purpose of analysing two organisations on based below discussed is the

differentiation table that will help in analysing some of the aspect that are different in two

organisations who are operating at similar level and are part of same industry.

Basis Innocent drinks Mars drinks

Innocent drinks are dealing in

juices, smoothies that are sold

in coffee shops, supermarkets.

All its functions are managed

by brands such as Coca cola.

Marks is having speciality in

coffee beverage. They are

having presence in France,

UK, Canada, America.

Issues There has been a Huge decline

in revenue since quarter

ending in march 2020 because

of the situations of COVID-19

as people are not preferring

There is no meeting up of the

set sales targets.

P5: Compare how organisations are managing the function of management accounting to

deal with different financial problems & issues

Financial issues are related to limited supply of financial resources. There are issues

that can happen because of misrepresentation, default of financial managers or sometimes

financial departments. Some of the financial issues are mentioned below:

High expense: There are some situations where Innocent drinks have to make lot of

promotion while they are launching some new products (Alsharari, and Youssef, 2017). They

have to distribute their free samples so that people can realise its taste and then purchase.

Financial governance: This is a method that can be adopted by organisations for the purpose

of gathering of the necessary information. It helps in enhancing the authenticity of financial

information so that further decision can be made on this basis. This helps in fast decision

making so that no opportunity can be lost.

Benchmarking: It is a approach that can be adopted by organisation to work according to

certain specified standards. This is a very effective tool that can help in setting benchmarks

and then working according to such pre set benchmarks.

For the Purpose of analysing two organisations on based below discussed is the

differentiation table that will help in analysing some of the aspect that are different in two

organisations who are operating at similar level and are part of same industry.

Basis Innocent drinks Mars drinks

Innocent drinks are dealing in

juices, smoothies that are sold

in coffee shops, supermarkets.

All its functions are managed

by brands such as Coca cola.

Marks is having speciality in

coffee beverage. They are

having presence in France,

UK, Canada, America.

Issues There has been a Huge decline

in revenue since quarter

ending in march 2020 because

of the situations of COVID-19

as people are not preferring

There is no meeting up of the

set sales targets.

outside eatables

(McLaren, Appleyard and

Mitchell, 2016).

Management accounting It is a branch of cost

accounting which is used for

cost ascertainment like fixed

cost calculation. This help in

taking benefits of economies

of scale as when fixed cost is

spread overall large quantities

of production then it leads to

reduction in its elements and

taking benefits of variable

cost.

The financial department of

Mars drinks has adopted the

inventory management system

to maintain the cost of

inventory.

CONCLUSION

It can be concluded from the above-mentioned report that management accounting is an

essential part of the organisation because it was elected in identification of different kind of

cost which is involved by the organisation in production services. It can be seen that Tesco

can use different kind of management accounting which help form in profit maximization as

well as increasing the efficiency. There are different kind of systems like price optimisation

system, inventory management system, cost accounting system and job costing system which

is mandatory for the firm to achieve a separate image within the market by using proper

costing techniques. It is also analysed that management accounting reporting is also essential

for the firm which include different kind of reports for increasing efficiency and working

within the firm in an appropriate manner

(McLaren, Appleyard and

Mitchell, 2016).

Management accounting It is a branch of cost

accounting which is used for

cost ascertainment like fixed

cost calculation. This help in

taking benefits of economies

of scale as when fixed cost is

spread overall large quantities

of production then it leads to

reduction in its elements and

taking benefits of variable

cost.

The financial department of

Mars drinks has adopted the

inventory management system

to maintain the cost of

inventory.

CONCLUSION

It can be concluded from the above-mentioned report that management accounting is an

essential part of the organisation because it was elected in identification of different kind of

cost which is involved by the organisation in production services. It can be seen that Tesco

can use different kind of management accounting which help form in profit maximization as

well as increasing the efficiency. There are different kind of systems like price optimisation

system, inventory management system, cost accounting system and job costing system which

is mandatory for the firm to achieve a separate image within the market by using proper

costing techniques. It is also analysed that management accounting reporting is also essential

for the firm which include different kind of reports for increasing efficiency and working

within the firm in an appropriate manner

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.