Analysis and Interpretation of Financial Ratios: Tesco PLC Performance

VerifiedAdded on 2023/06/08

|9

|2180

|280

Report

AI Summary

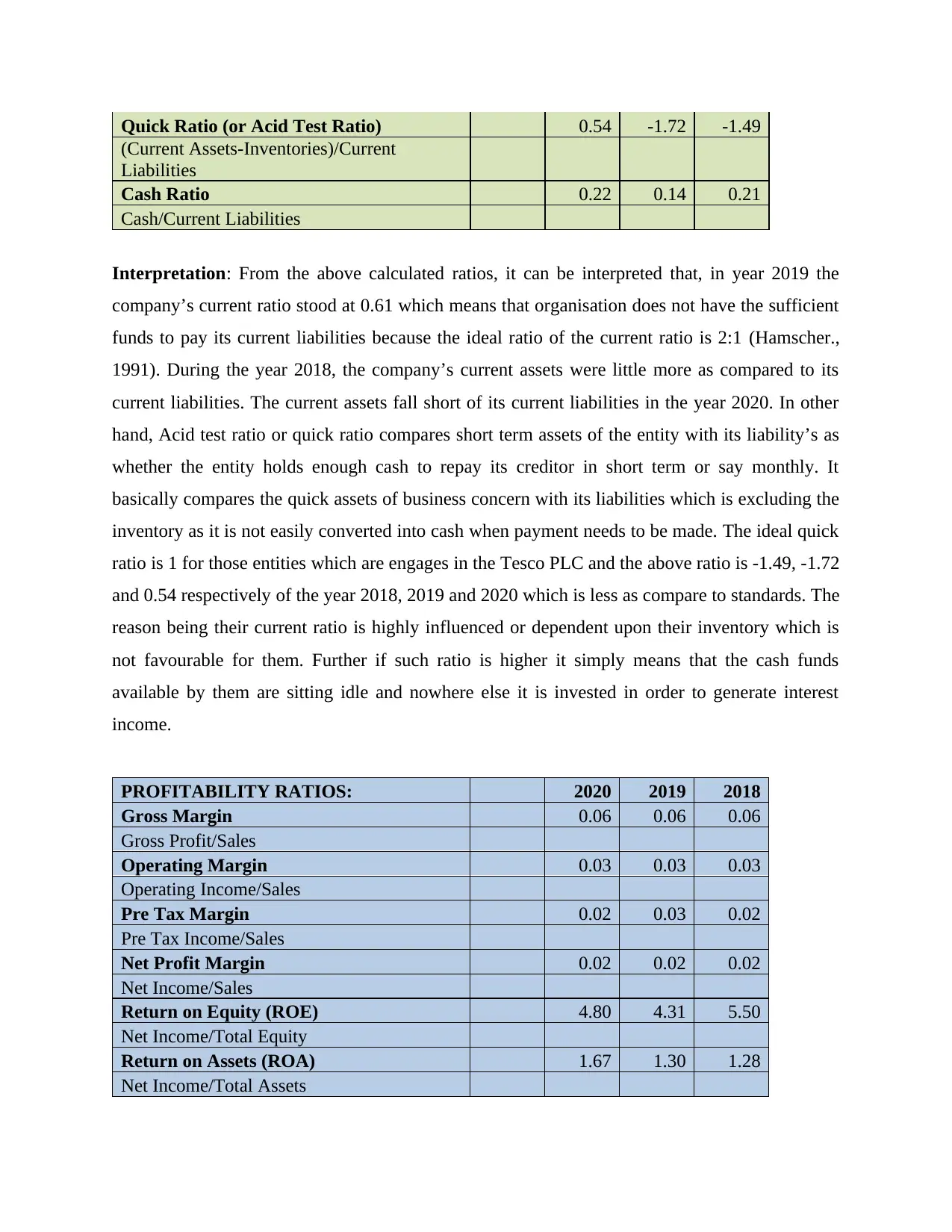

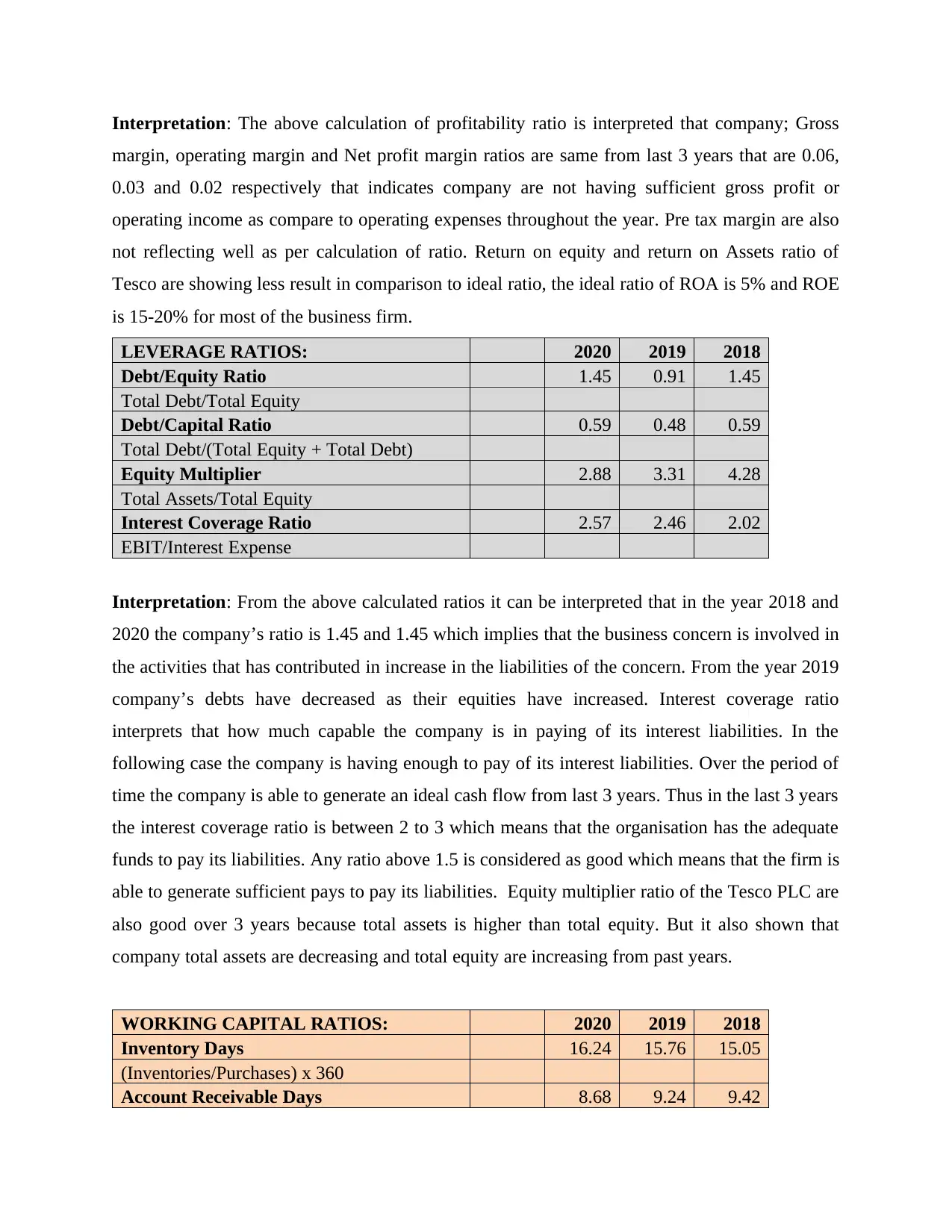

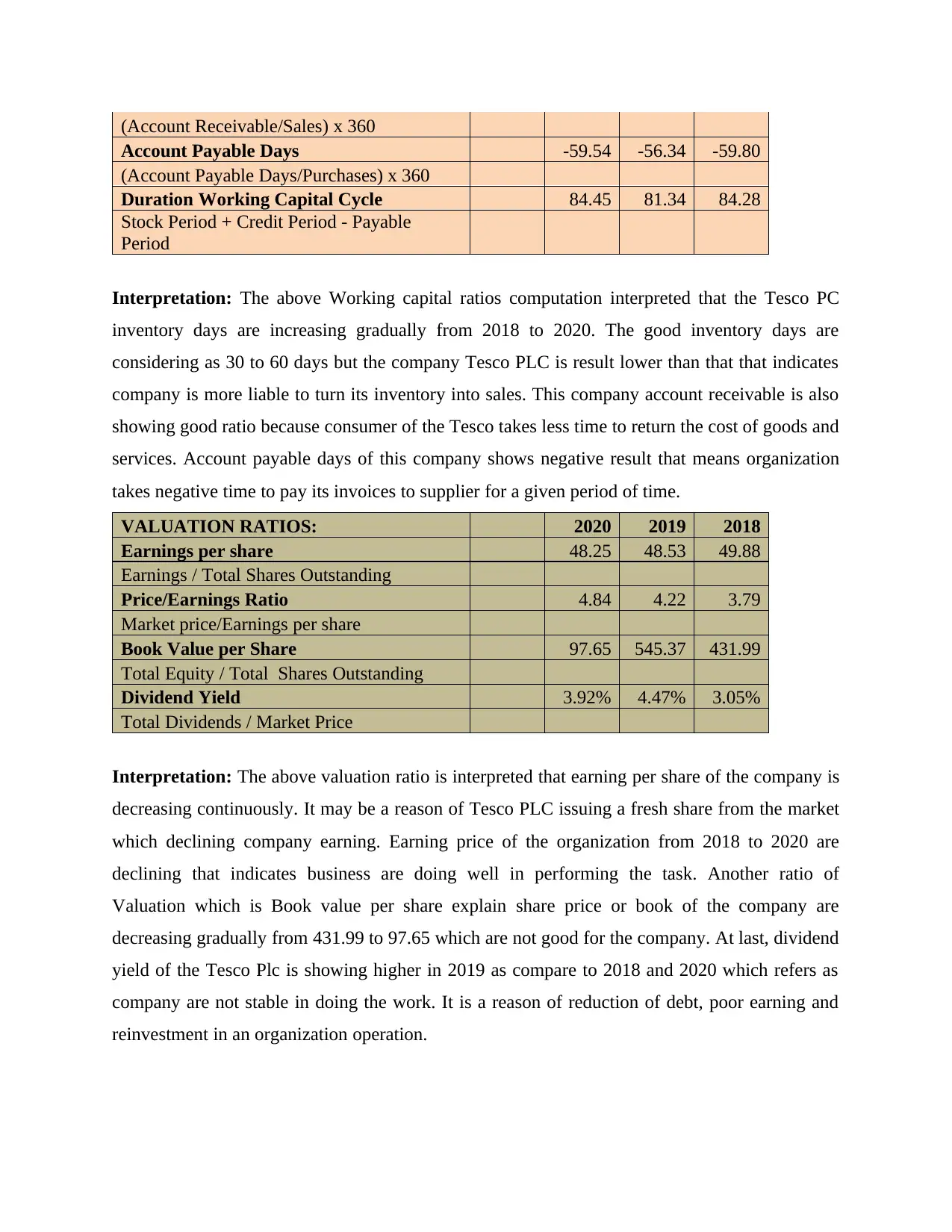

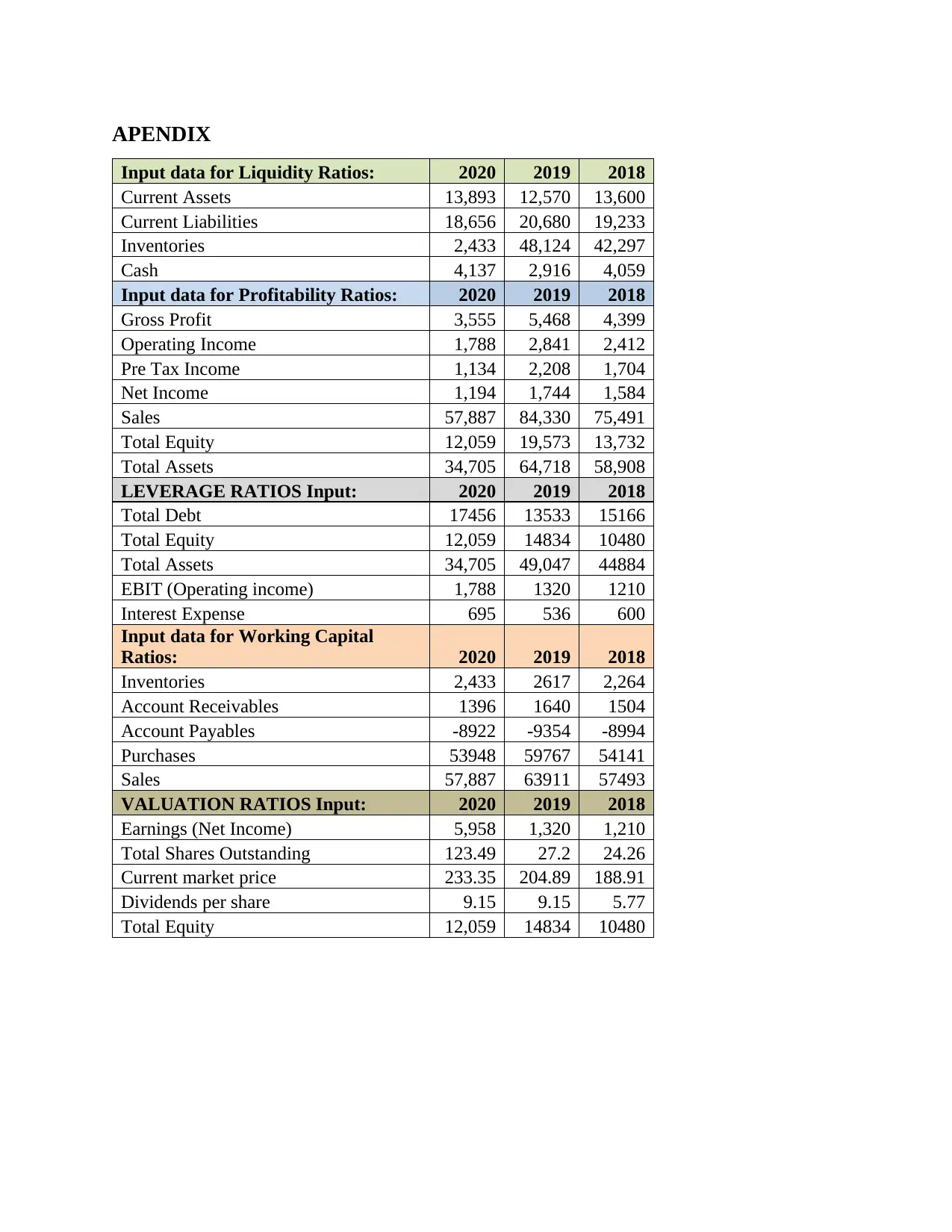

This report presents a comprehensive financial analysis of Tesco PLC, examining its performance from 2018 to 2020. The analysis encompasses various financial ratios, categorized into liquidity, profitability, leverage, working capital, and valuation ratios. The report begins with an introduction to Tesco PLC, followed by the calculation and interpretation of each ratio category. Liquidity ratios, such as the current and quick ratios, are assessed to determine the company's ability to meet short-term obligations. Profitability ratios, including gross margin and net profit margin, are analyzed to evaluate the company's efficiency in generating profits. Leverage ratios, like the debt-to-equity ratio, are used to assess the company's financial risk. Working capital ratios, such as inventory days and account receivable days, are reviewed to understand the company's operational efficiency. Valuation ratios, including earnings per share and dividend yield, are used to assess the company's market value. The report concludes with recommendations based on the findings and highlights areas for improvement, such as maintaining liquidity and efficiency. The report utilizes financial data from the years 2018, 2019, and 2020 to provide a comparative analysis of Tesco PLC's financial performance over the specified period. The analysis provides insight into the financial health of the company.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.