Detailed Financial Analysis Case Study: TESCO PLC Performance

VerifiedAdded on 2020/10/22

|10

|1720

|78

Case Study

AI Summary

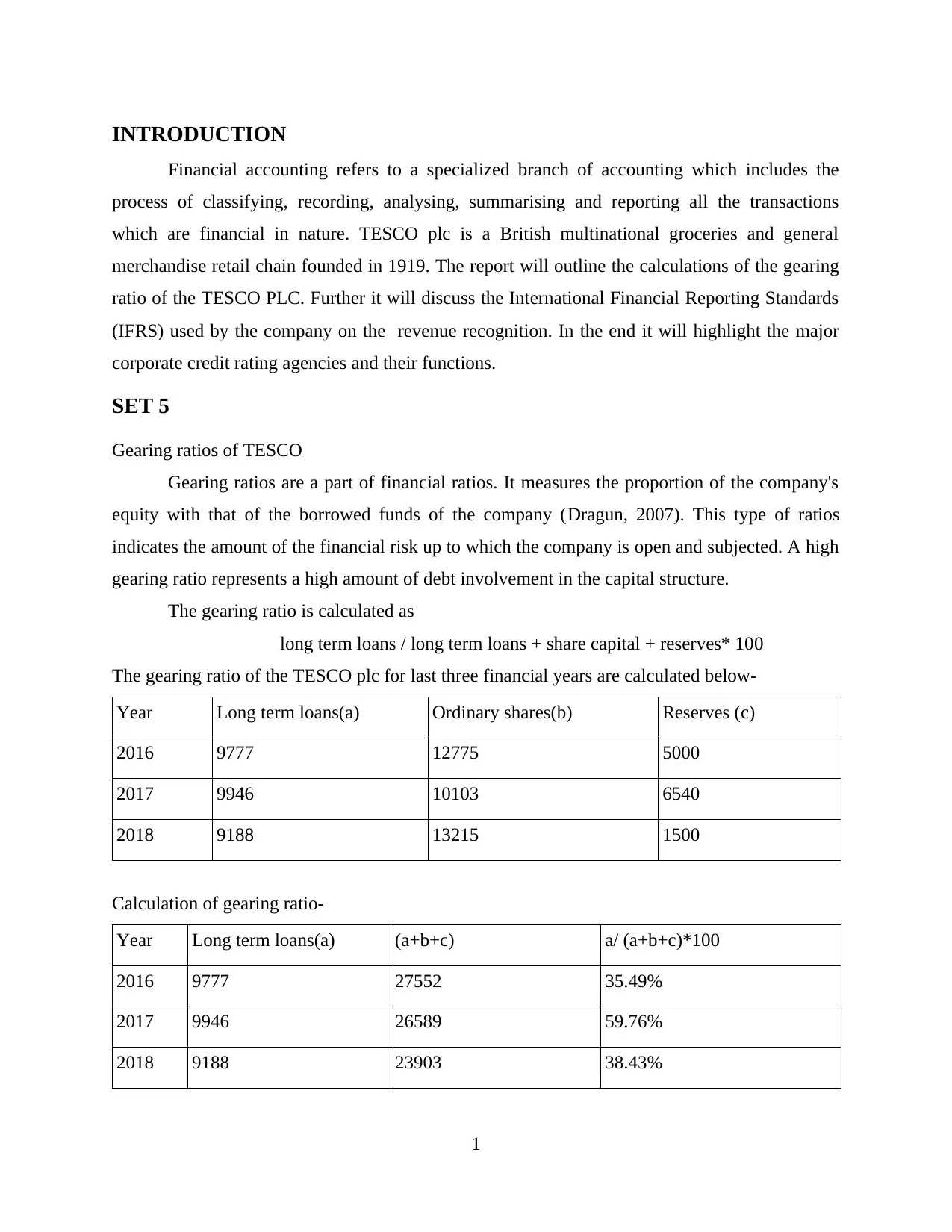

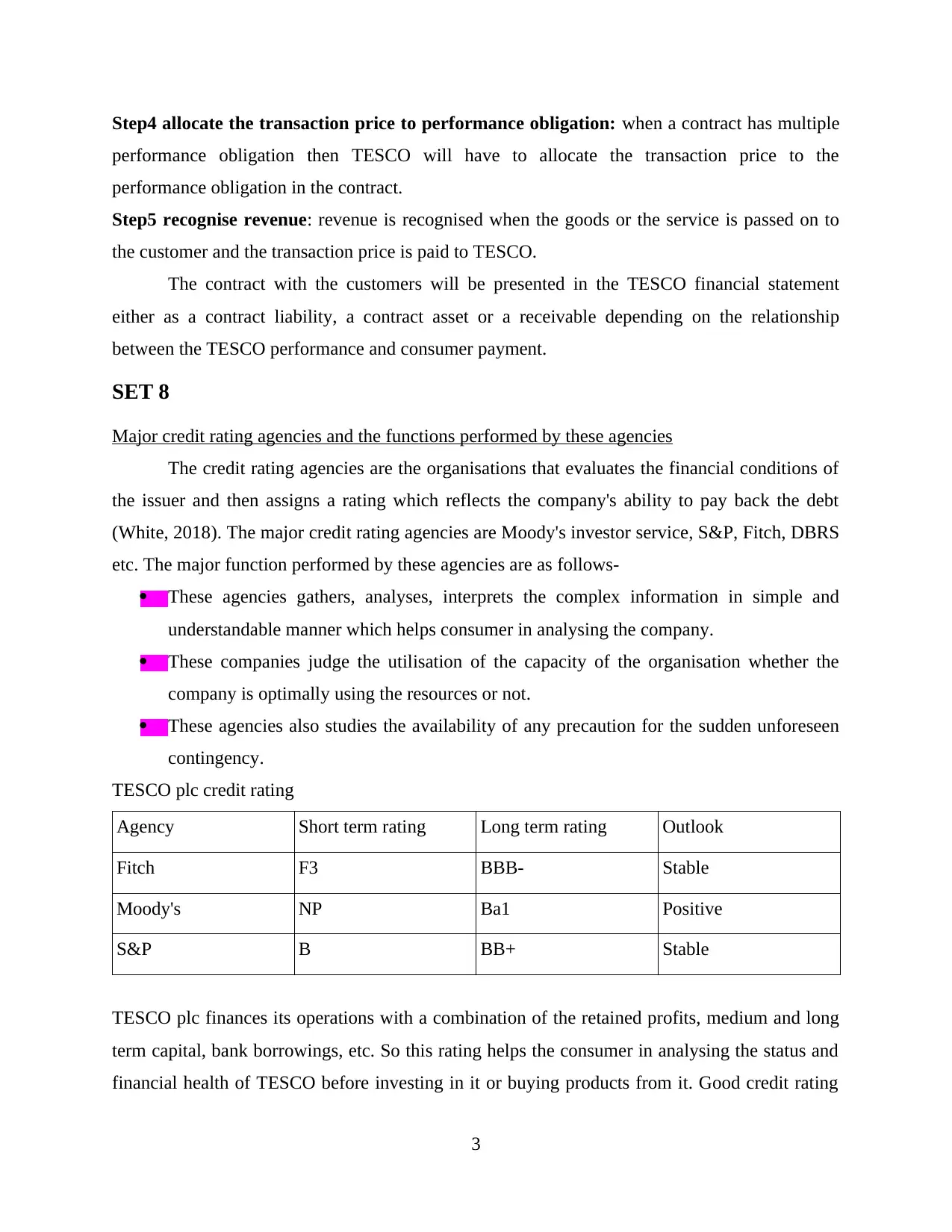

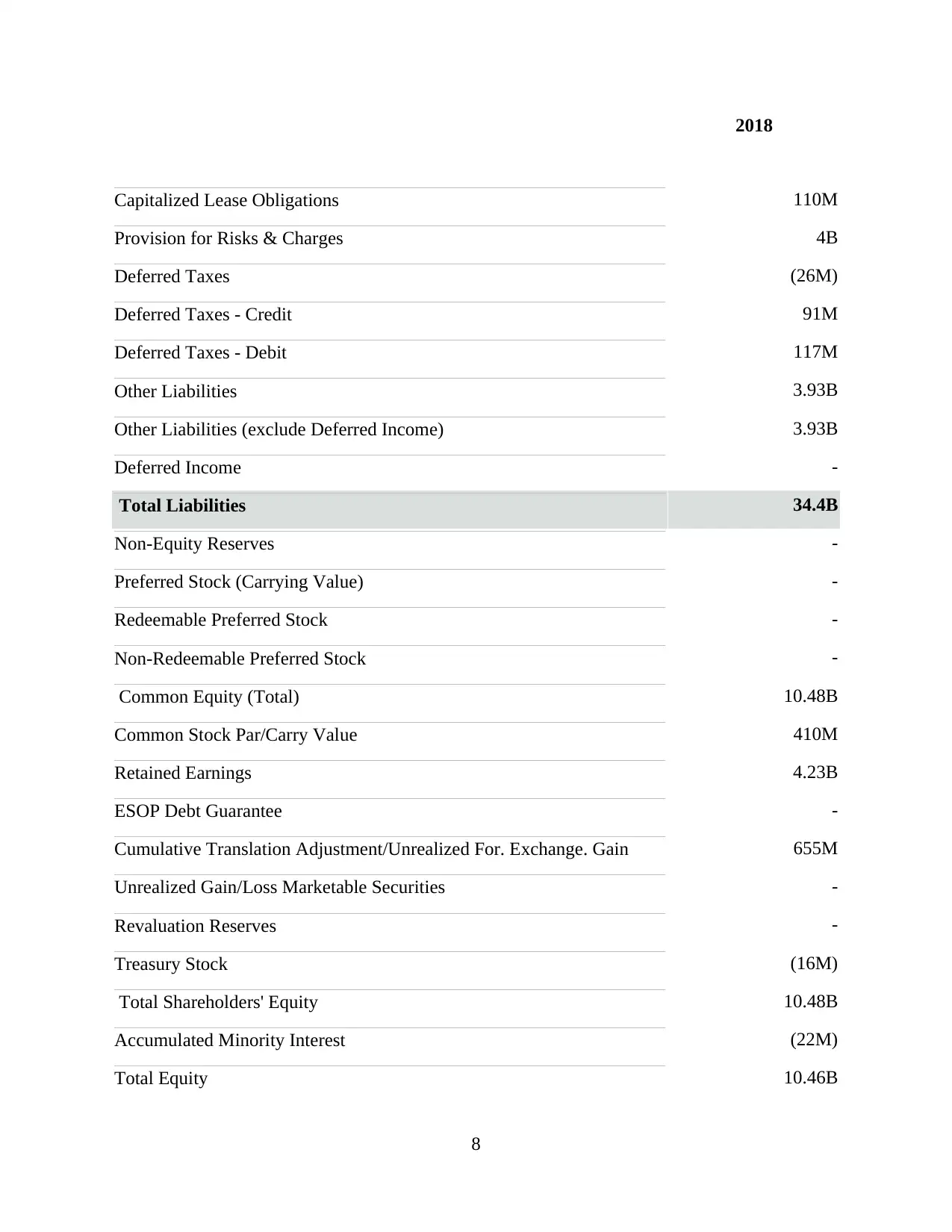

This case study provides a financial analysis of TESCO PLC, a major British multinational retailer. It begins by calculating and interpreting the gearing ratios for TESCO over three financial years (2016-2018), offering insights into the company's debt levels. The study then delves into the International Financial Reporting Standards (IFRS) used by TESCO, specifically focusing on IFRS 15 and its application to revenue recognition, highlighting the five-step model employed by the company. Finally, the case study examines major credit rating agencies, such as Moody's, S&P, and Fitch, and their functions in assessing TESCO's financial health, including a summary of the company's credit ratings from these agencies. The analysis includes the interpretation of the financial statements and ratios, and the study concludes with a summary of the key findings regarding TESCO's financial performance, emphasizing the importance of financial accounting principles and credit ratings in understanding the company's financial position.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.