Strategic Financial Management Report: Tesco PLC 2018-2019

VerifiedAdded on 2022/12/19

|15

|3290

|447

Report

AI Summary

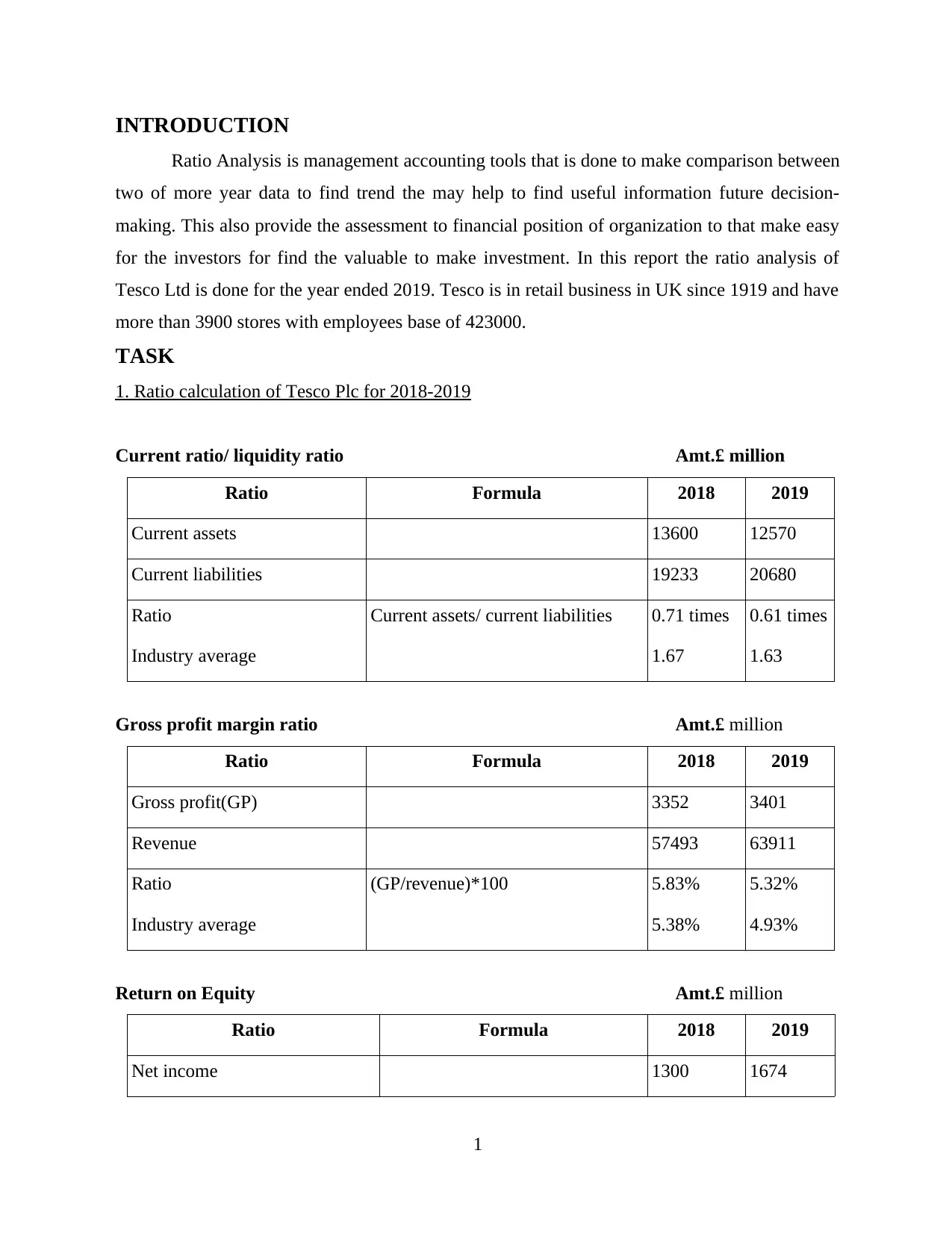

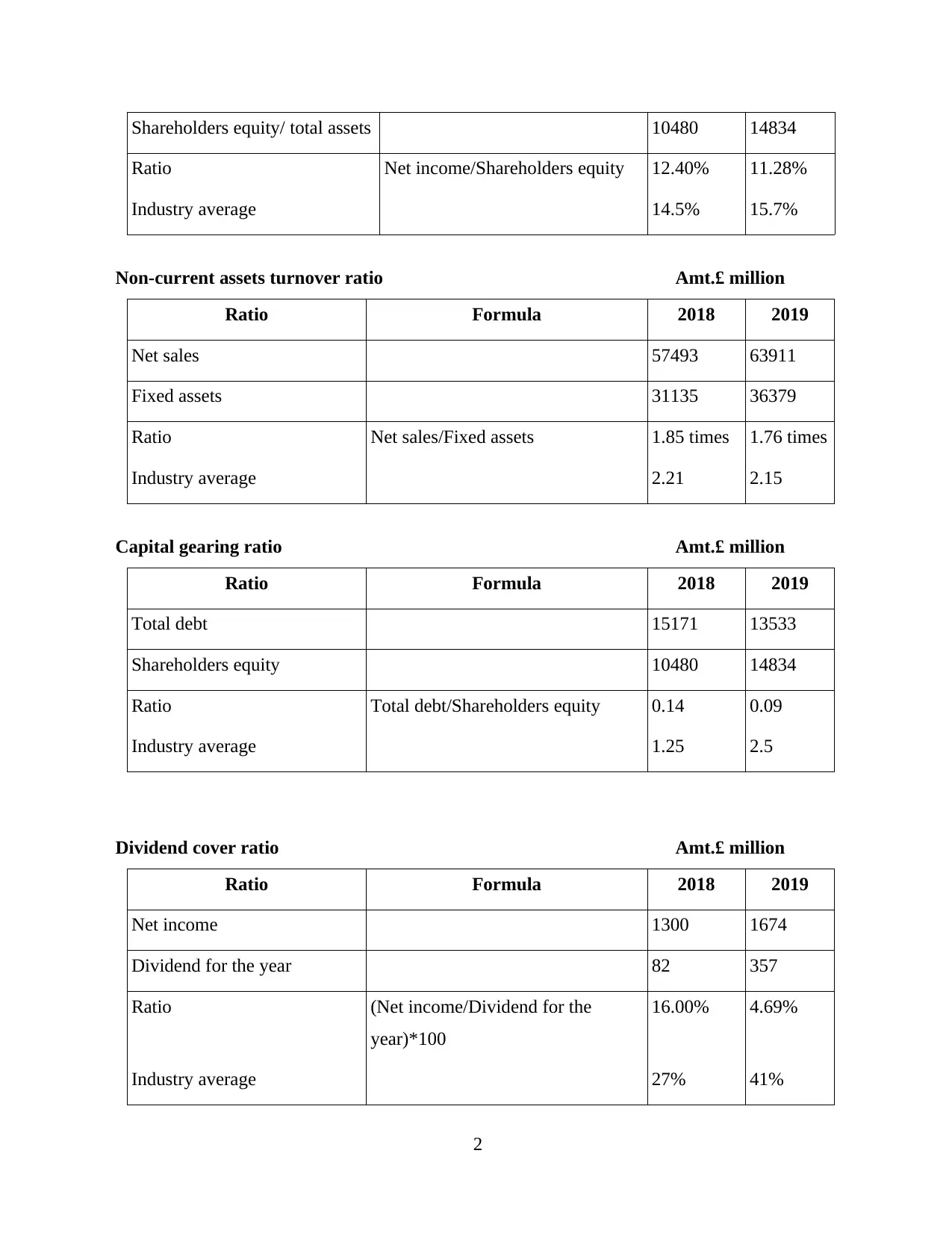

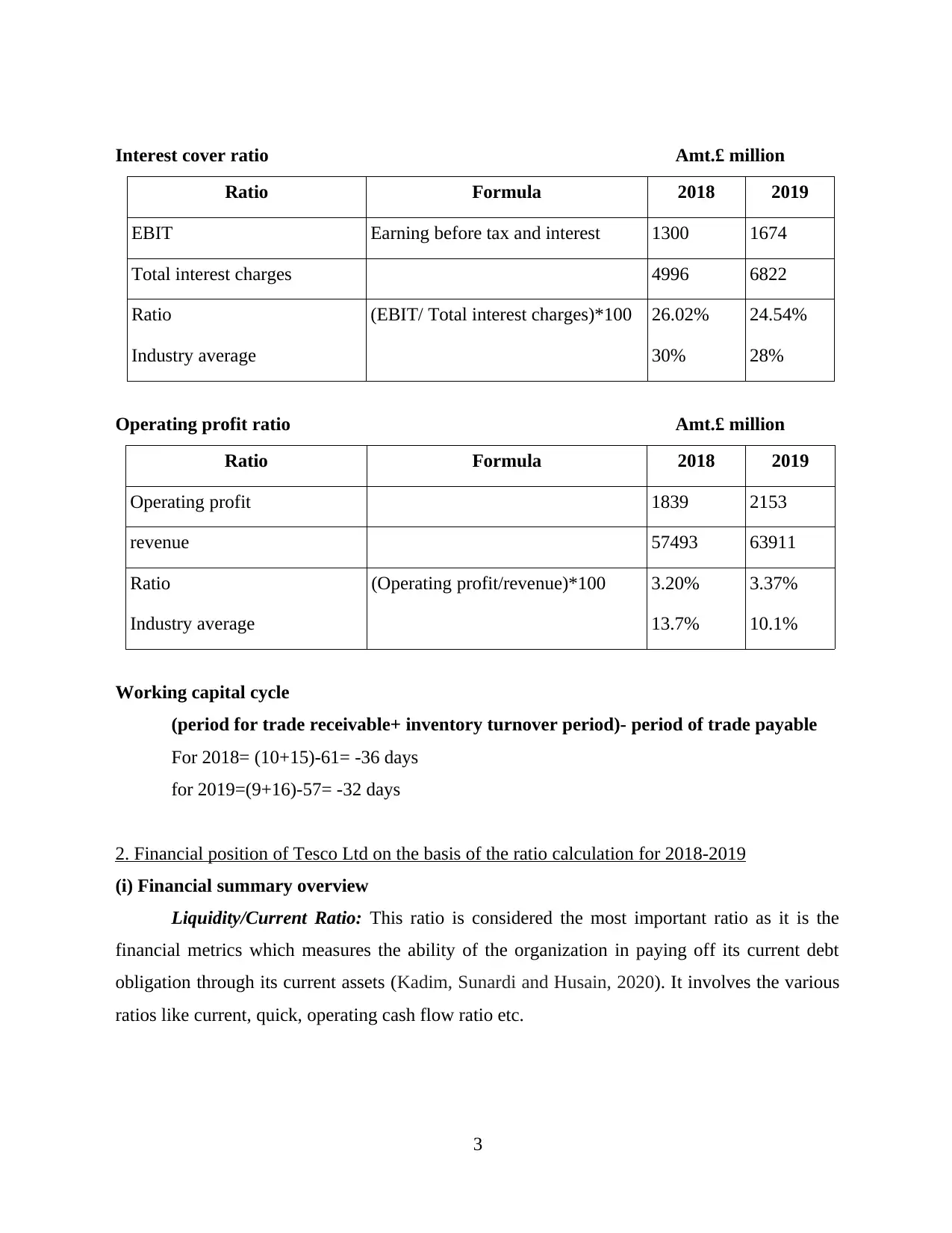

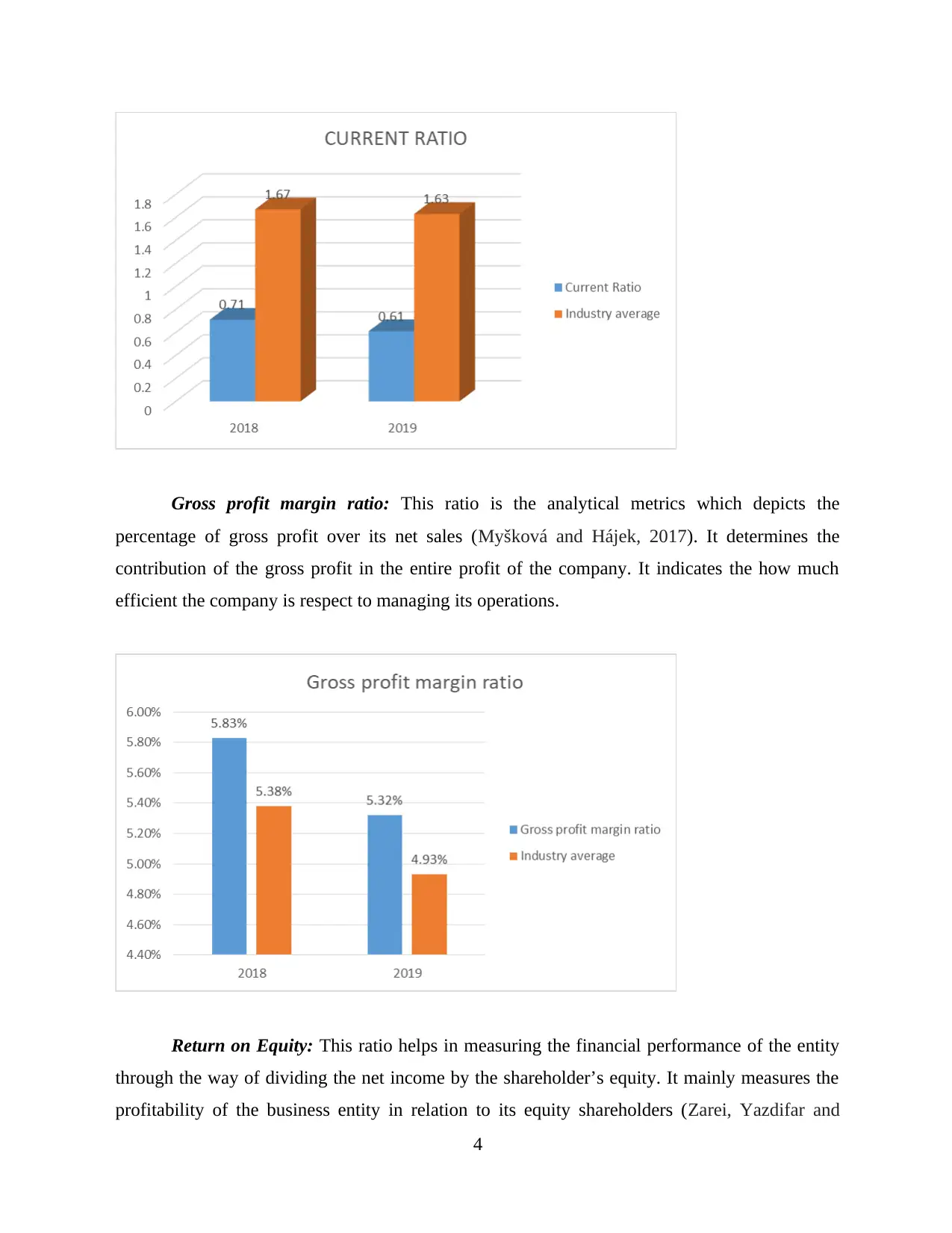

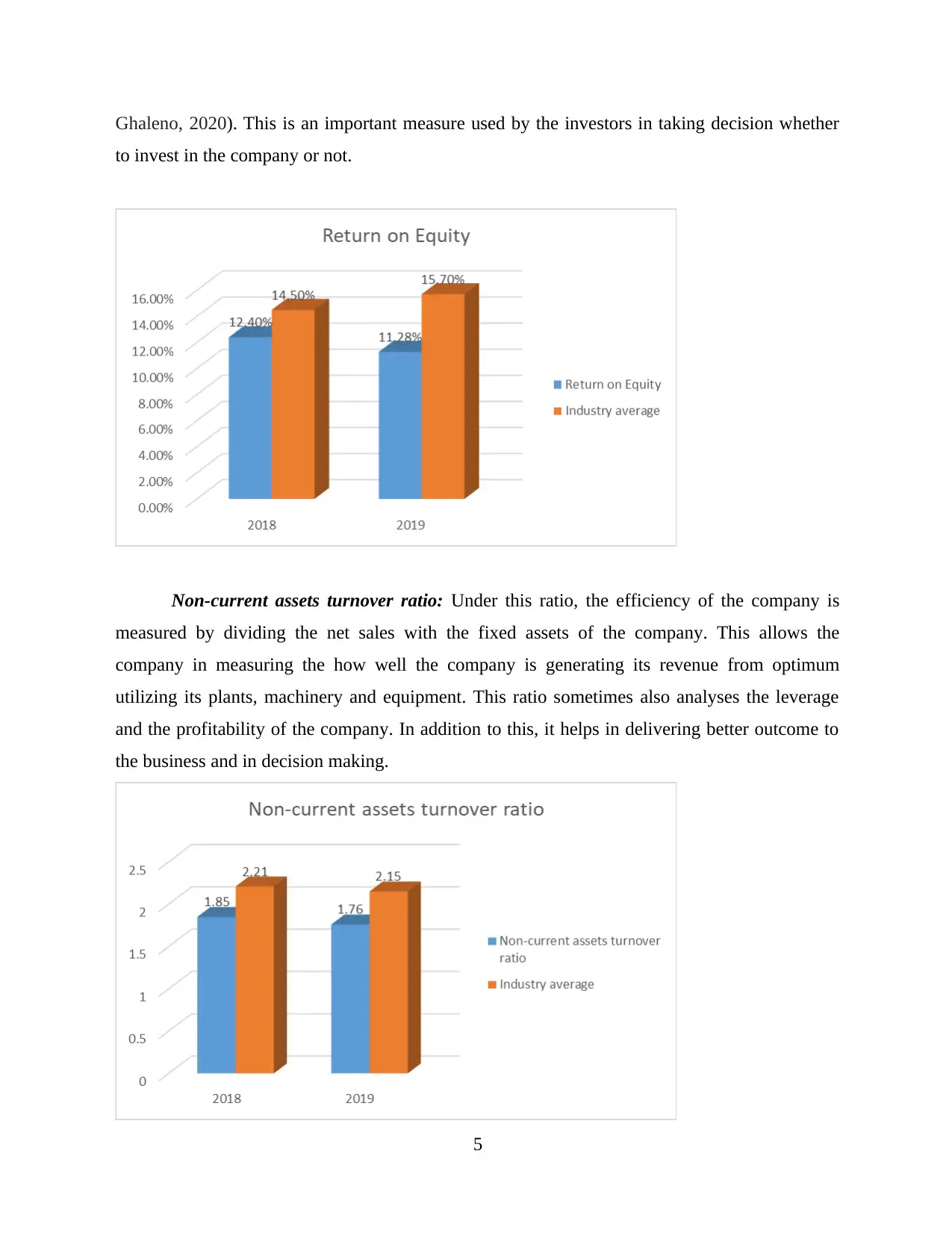

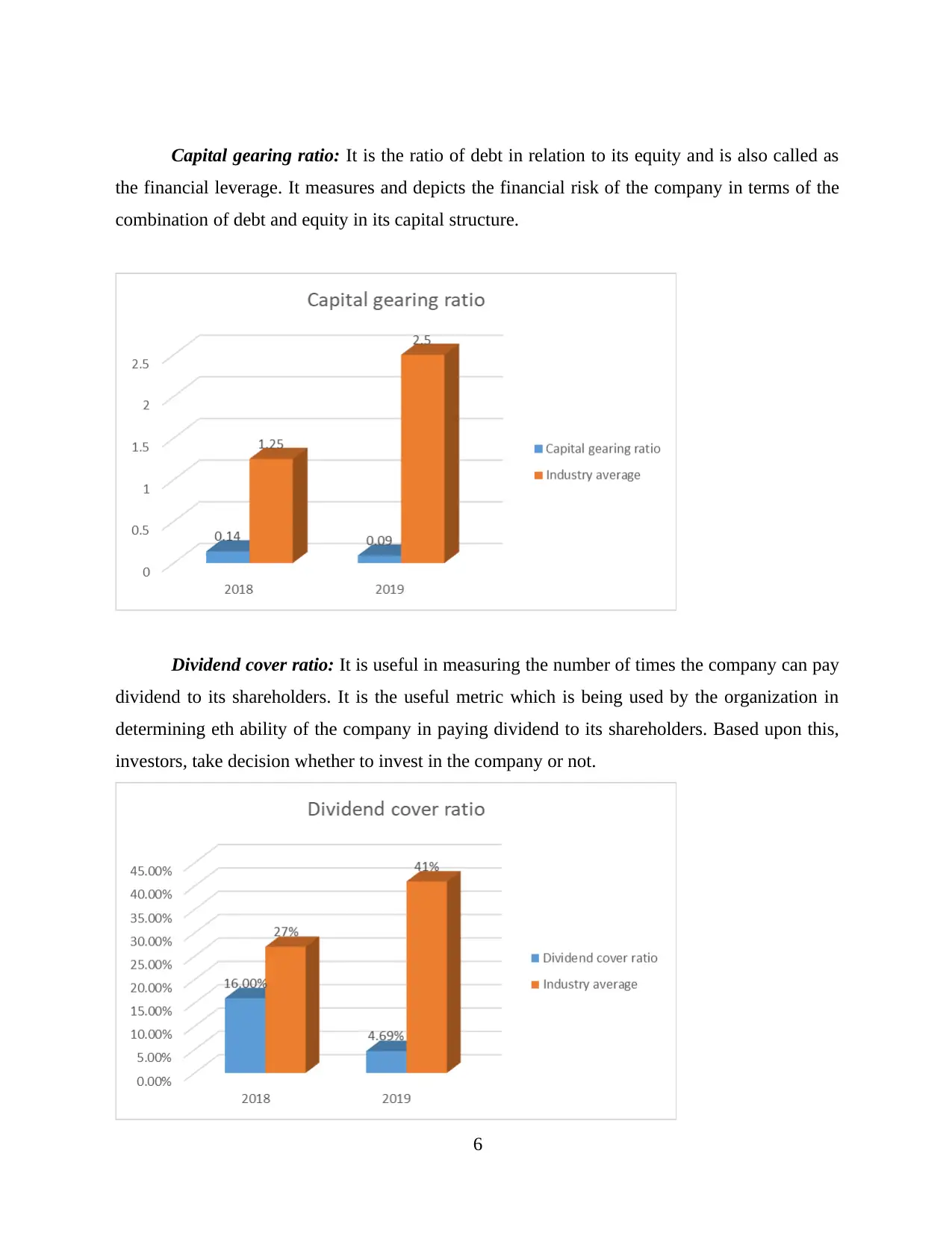

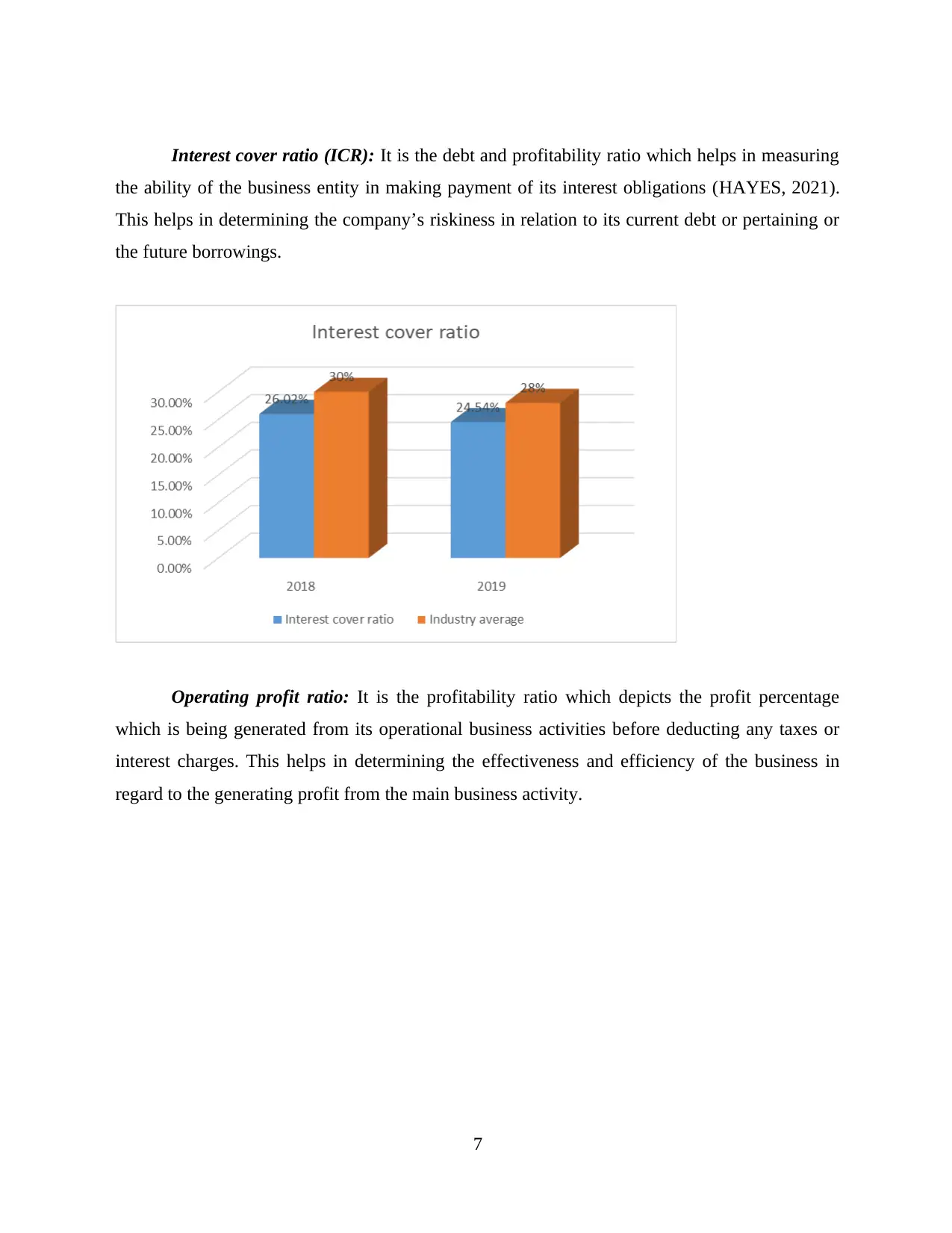

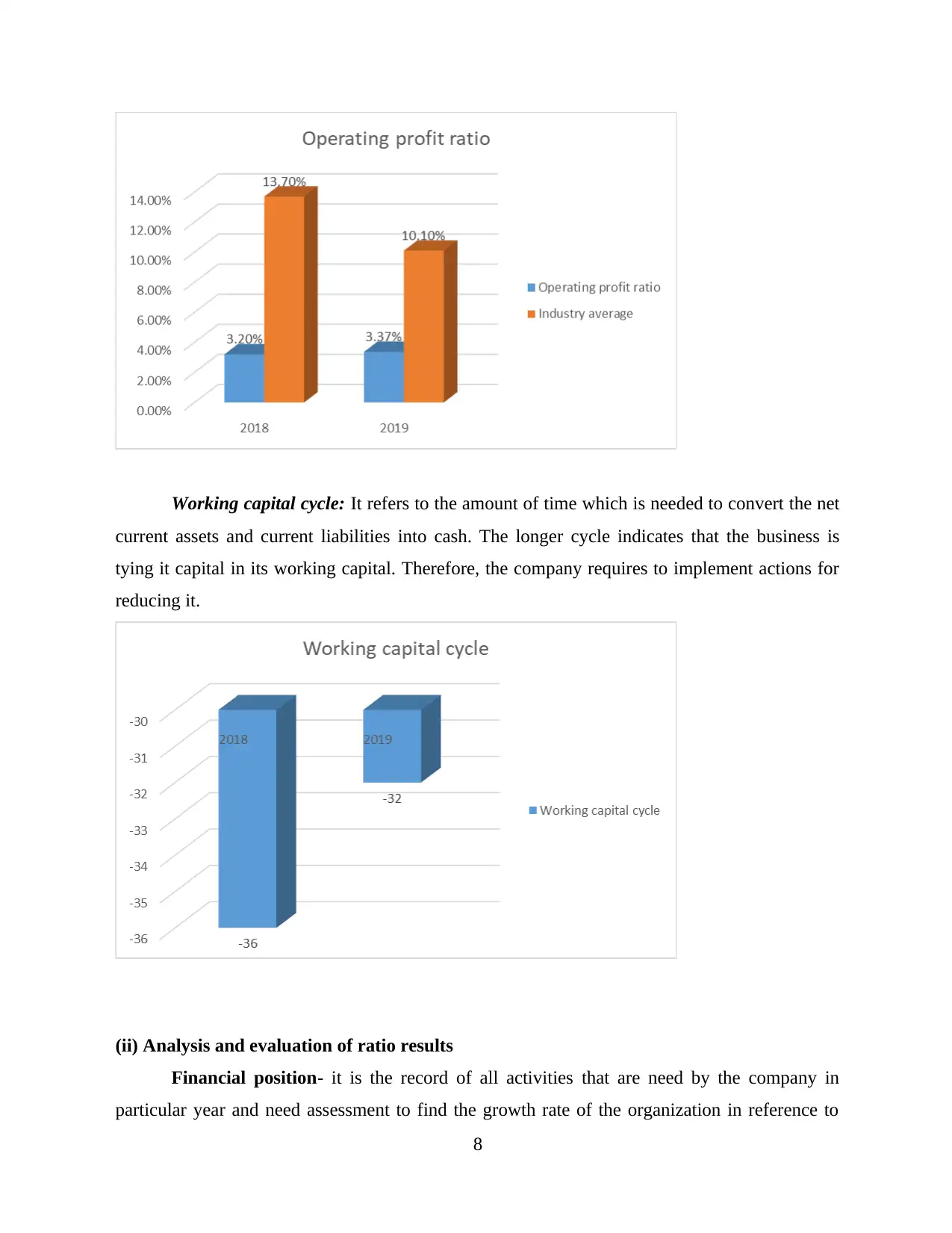

This report presents a strategic financial management analysis of Tesco PLC, focusing on the financial years 2018 and 2019. The analysis employs a variety of financial ratios, including current ratio, gross profit margin, return on equity, non-current assets turnover ratio, capital gearing ratio, dividend cover ratio, interest cover ratio, operating profit ratio, and working capital cycle. The report calculates and interprets these ratios, comparing them to industry averages and assessing Tesco's financial position, liquidity, profitability, and solvency. The findings highlight Tesco's strengths and weaknesses, offering insights into its operational efficiency, financial risk, and ability to meet its financial obligations. The report concludes with an overview of Tesco's financial health and provides recommendations for improvement. This report provides a comprehensive overview of Tesco's financial standing during the specified period, offering valuable insights into its performance and financial stability, supported by relevant calculations and comparisons.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.