Financial Statement Analysis of Tesco: 6AG502 Module Report 2020/2021

VerifiedAdded on 2022/12/29

|13

|3572

|1

Report

AI Summary

This report presents a comprehensive financial statement analysis of Tesco, a multinational retail company. It begins with an introduction to financial statement analysis and its importance, followed by background information on Tesco, including its vision, mission, and SWOT analysis. The main body delves into fundamental analysis, including common size statements, segment analysis, Dupont analysis, and trend analysis. The report then provides a detailed financial analysis and interpretation using various ratios (liquidity, activity, and profitability), examining Tesco's performance from 2018 to 2020. Cash flow analysis and future prospects, considering the impact of COVID-19, are also discussed. The report concludes with recommendations based on the analysis and references supporting the findings. The analysis covers key aspects like strategic planning, competitive landscape, and financial health, offering insights into Tesco's operational efficiency, financial leverage, and overall performance.

Financial

Statement

Analysis

Statement

Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Background information:.............................................................................................................1

Fundamental analysis:..................................................................................................................2

Financial analysis and interpretation:..........................................................................................4

Cash flow analysis:......................................................................................................................7

Future prospects:..........................................................................................................................7

Recommendations:.......................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Background information:.............................................................................................................1

Fundamental analysis:..................................................................................................................2

Financial analysis and interpretation:..........................................................................................4

Cash flow analysis:......................................................................................................................7

Future prospects:..........................................................................................................................7

Recommendations:.......................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION

Financial statement analysis can be defined as a procedure of analysing financial

statement of an organization for the purpose of making decisions. It is used by internal decision

makers of company for formulating effective strategies for expansion and success of business.

This also helps management team of business in the process of monitoring and managing

finances. Apart from this, external stakeholders utilise this approach for understanding financial

health of entity and evaluating its performance as well as business value (Abor, 2017). Basis of

this report is conducting financial statement analysis for Tesco. It is a multinational company

that operates in retailing sector. This report covers industry analysis and description of strategic

planning process. It conducts fundamental analysis of business which involves evaluation of

common size statements as well as segmental analysis. Further, financial statements is analysed

and interpreted along with analysis of cash flow statement. Apart from this, future prospects of

an enterprise is investigated in accordance to effects of Covid 19 and recommendations are

provides as per analysis.

MAIN BODY

Background information:

Background information of Tesco: Tesco is a public limited company that serves in

international market. Company is headquartered in Welwyn Garden city of England, United

Kingdom. It is founded by Jack Cohen in the year 1919. Company operates in retailing industry

and it serves in various areas, that includes, United Kingdom, Slovakia, Ireland, Hungary, Czech

Republic as well as India. Supermarkets, hypermarket, convenience shops and superstore are

products of an organization. Company earned revenue of £63.911 billion in the year 2019 and its

net income is of £1.320 billion in the same year. It is a leading retailer of grocery in UK and

comes among most valuable brands of country. Even in international market, entity is fifteenth

most valuable in context to retail brand in the year 2016. While measuring in terms of revenue,

entity can be stated as night largest around globe and it is third largest in terms of gross revenue.

Number of employees that are working in an organization is about 450,000 in the year 2019

(Dewi Anggadini, 2018).

Vision: To become most valuable business in context to customers that are served, communities

in which it is operated, loyal or committed colleagues as well as shareholders.

1

Financial statement analysis can be defined as a procedure of analysing financial

statement of an organization for the purpose of making decisions. It is used by internal decision

makers of company for formulating effective strategies for expansion and success of business.

This also helps management team of business in the process of monitoring and managing

finances. Apart from this, external stakeholders utilise this approach for understanding financial

health of entity and evaluating its performance as well as business value (Abor, 2017). Basis of

this report is conducting financial statement analysis for Tesco. It is a multinational company

that operates in retailing sector. This report covers industry analysis and description of strategic

planning process. It conducts fundamental analysis of business which involves evaluation of

common size statements as well as segmental analysis. Further, financial statements is analysed

and interpreted along with analysis of cash flow statement. Apart from this, future prospects of

an enterprise is investigated in accordance to effects of Covid 19 and recommendations are

provides as per analysis.

MAIN BODY

Background information:

Background information of Tesco: Tesco is a public limited company that serves in

international market. Company is headquartered in Welwyn Garden city of England, United

Kingdom. It is founded by Jack Cohen in the year 1919. Company operates in retailing industry

and it serves in various areas, that includes, United Kingdom, Slovakia, Ireland, Hungary, Czech

Republic as well as India. Supermarkets, hypermarket, convenience shops and superstore are

products of an organization. Company earned revenue of £63.911 billion in the year 2019 and its

net income is of £1.320 billion in the same year. It is a leading retailer of grocery in UK and

comes among most valuable brands of country. Even in international market, entity is fifteenth

most valuable in context to retail brand in the year 2016. While measuring in terms of revenue,

entity can be stated as night largest around globe and it is third largest in terms of gross revenue.

Number of employees that are working in an organization is about 450,000 in the year 2019

(Dewi Anggadini, 2018).

Vision: To become most valuable business in context to customers that are served, communities

in which it is operated, loyal or committed colleagues as well as shareholders.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Mission: To become champions for the customers and help them in enjoying better standard of

life.

SWOT Analysis of Tesco:

Strengths Weaknesses

Tesco is the market leader in retail

sector hence, enjoys long term

sustainability and high profitability.

Supply chain network of an

organization is highly efficient and

pertains effective policies for waste

management which leads to reduction

in costs that incurs in business.

Low cost strategy of Tesco leads to

reduction in profit margin.

Strategies of business for entering in

markets of United states and markets of

Japan comes up as a failure.

Opportunities Threats

Firm pertains an opportunity in

expanding its operations in various

untapped markets.

Tesco can further grow its operations

by enhancing its activities of online

sales.

Increasing number of competitors in the

market comes up as a threat for

business.

No deal Brexit leads towards

suspension of free trade agreement

along with EU.

Strategic planning process: It refers to a organizational procedure that includes strategic

defining, direction, and making of decisions for allocation of resources for the purpose of

pursuing strategies. It is a control mechanism that guides implementation of strategies. It is an

essential aspect of strategic management and is executed by internal decision makers. It involves

various steps such as, determination of strategic position of business, identification or

prioritization of goals or objectives, development of strategic plan, mobilization of resources,

execution of decided action plan and lastly, management and monitoring of performance of

business activities (Doron, 2016). Strategic plan of Tesco is to divide organizational activities in

three different types of levels as per its priorities, corporate level strategy is applied fr highest

level, business level strategy is for middle level and operational strategy for activities that require

lower level of management. Adoption of this strategy enables an organization to gain

2

life.

SWOT Analysis of Tesco:

Strengths Weaknesses

Tesco is the market leader in retail

sector hence, enjoys long term

sustainability and high profitability.

Supply chain network of an

organization is highly efficient and

pertains effective policies for waste

management which leads to reduction

in costs that incurs in business.

Low cost strategy of Tesco leads to

reduction in profit margin.

Strategies of business for entering in

markets of United states and markets of

Japan comes up as a failure.

Opportunities Threats

Firm pertains an opportunity in

expanding its operations in various

untapped markets.

Tesco can further grow its operations

by enhancing its activities of online

sales.

Increasing number of competitors in the

market comes up as a threat for

business.

No deal Brexit leads towards

suspension of free trade agreement

along with EU.

Strategic planning process: It refers to a organizational procedure that includes strategic

defining, direction, and making of decisions for allocation of resources for the purpose of

pursuing strategies. It is a control mechanism that guides implementation of strategies. It is an

essential aspect of strategic management and is executed by internal decision makers. It involves

various steps such as, determination of strategic position of business, identification or

prioritization of goals or objectives, development of strategic plan, mobilization of resources,

execution of decided action plan and lastly, management and monitoring of performance of

business activities (Doron, 2016). Strategic plan of Tesco is to divide organizational activities in

three different types of levels as per its priorities, corporate level strategy is applied fr highest

level, business level strategy is for middle level and operational strategy for activities that require

lower level of management. Adoption of this strategy enables an organization to gain

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

competitive advantage in an international market and enhance its efficiency as well as

productivity. Apart from this, entity is focused towards providing superior quality products at

low piece which improvises long term sustainability of business and ensures enhancement of

customer loyalty. It increases profitability of an enterprise. Main competitors of Tesco are Asda,

Sainsbury's as well as Morrison's. Apart from this, Aldi, Lidl, and Wait rose are also competitors

of an organization. Tesco is evaluated as third largest in context to retail industries in word,

Walmart and Asda are top two player globally, while, in relevance to United Kingdom company

is top player in retail sector.

Fundamental analysis:

Common size statement: It can be explained as a form of interpretation or analysis of

financial statements of business. It is also termed as vertical analysis. This method enables

evaluation of financial statements by considering each line items as base amount percentage for a

particular period of accounting. Common size statement simplifies analysis of financial

information of an enterprise and is always expressed in percentage form. There are mainly two

types of financial statement, that is, income statement and balance sheet (Dut, 2016). Former is a

statement in which every item is expressed as percentage of revenue. It is utilised for the purpose

of vertically analysing financial statement and evaluating performance of Tesco. It shows

profitability position of an entity. While on the other hand, later, displays numeric value as well

as relative percentage of liabilities, assets and equity of Tesco. In balance sheet of common size

items of single asset line is compared with total asset value, similarly, value of total liabilities

and equity is compared with total liability and total equity, respectively.

Segment analysis: Segment refers to a component of an organization or business that

generates revenue or reacts product line. In other words, segments can be defined as a unit of

business which is self sufficient. Hence, it can be noted that segment are those part of an

organization that pertains separate information regarding finance and separate strategy for

management. Segment analysis or reporting is a procedure of breaking of financial data of

company into different divisions or segments. It provides clear picture of financial performance

of an organization to its stakeholders. Hence, it is used by management team of Tesco for

evaluation of incomes, expenditures, assets as well as liabilities in context to each segment or

division of business. Accounting standards are set for segment analysis which states that

statement analysis should align with reporting structure of an enterprise (Duţescu, 2019).

3

productivity. Apart from this, entity is focused towards providing superior quality products at

low piece which improvises long term sustainability of business and ensures enhancement of

customer loyalty. It increases profitability of an enterprise. Main competitors of Tesco are Asda,

Sainsbury's as well as Morrison's. Apart from this, Aldi, Lidl, and Wait rose are also competitors

of an organization. Tesco is evaluated as third largest in context to retail industries in word,

Walmart and Asda are top two player globally, while, in relevance to United Kingdom company

is top player in retail sector.

Fundamental analysis:

Common size statement: It can be explained as a form of interpretation or analysis of

financial statements of business. It is also termed as vertical analysis. This method enables

evaluation of financial statements by considering each line items as base amount percentage for a

particular period of accounting. Common size statement simplifies analysis of financial

information of an enterprise and is always expressed in percentage form. There are mainly two

types of financial statement, that is, income statement and balance sheet (Dut, 2016). Former is a

statement in which every item is expressed as percentage of revenue. It is utilised for the purpose

of vertically analysing financial statement and evaluating performance of Tesco. It shows

profitability position of an entity. While on the other hand, later, displays numeric value as well

as relative percentage of liabilities, assets and equity of Tesco. In balance sheet of common size

items of single asset line is compared with total asset value, similarly, value of total liabilities

and equity is compared with total liability and total equity, respectively.

Segment analysis: Segment refers to a component of an organization or business that

generates revenue or reacts product line. In other words, segments can be defined as a unit of

business which is self sufficient. Hence, it can be noted that segment are those part of an

organization that pertains separate information regarding finance and separate strategy for

management. Segment analysis or reporting is a procedure of breaking of financial data of

company into different divisions or segments. It provides clear picture of financial performance

of an organization to its stakeholders. Hence, it is used by management team of Tesco for

evaluation of incomes, expenditures, assets as well as liabilities in context to each segment or

division of business. Accounting standards are set for segment analysis which states that

statement analysis should align with reporting structure of an enterprise (Duţescu, 2019).

3

Dupont analysis: It is a framework that is utilised for evaluating fundamental

performance of an organization. This techniques is applied for the purpose of decomposing

different drivers for return on equity. It allows investors of business to focus on key metrics

regarding financial performance and helps in identifying its strengths and weaknesses. It mainly

focuses on three financial metrics, that are, operational efficiency, efficiency regarding usage of

assets as well as financial leverage. Net profit margin represents operational efficiency,

efficiency of asset use is measured with asset turnover ratio and equity multiplier helps in

measuring leverage (Elsayed, 2017).

Trend analysis: It refers to a technique of technical analysis that is utilised for studying

financial data of an organization over a time period. It mainly focuses on change factor within

balance sheet as well as income statement of an organization. While conducting trend analysis of

Tesco, in context to its income statement in 2015 and 2016 it is interpreted that cost of sales of

an organization reduced from 95.3 percent of revenue to 94.9 percent. Gross profit of entity

enhanced from 4.7% to 5.1% which is a positive indicator as income earning capacity of from

core operations of business increased. Apart from this, administration expenses of Tesco

increased from 3.1% in 2015 to 3.4% in the year 2016. In relation to operating profit of an

organization, it increased from 1.6 percent to 1.7 percent from 2015 to 2016 which indicates that

ability of entity regarding management of operating expenses is improvising. Interest expenses

of company is 1percent in 2015 while it increased to 1.2 percent in 2016. profit before and after

tax reduced by 0.1 percent from 2015 to 2016 which states that overall profitability of business

declined over a period of time.

Financial analysis and interpretation:

Financial analysis and interpretation is an attempt for determining evaluation and

significance of financial information for the purpose of estimating position of funds in an

organization. Apart from it, this approach helps in forecasting future earning prospects of

business and determines ability of Tesco in context to payment of short term or long term

obligations. Main function of conducting financial analysis enabling effective management of

fund in business (Erdoğan and Erdoğan, 2020). Ratio analysis of Tesco is computed below for

determining financial performance of an enterprise. This framework is used for comparing

performance of business with other entity or its own past performance. It also helps in evaluating

trend line of company for formulating adequate strategies.

4

performance of an organization. This techniques is applied for the purpose of decomposing

different drivers for return on equity. It allows investors of business to focus on key metrics

regarding financial performance and helps in identifying its strengths and weaknesses. It mainly

focuses on three financial metrics, that are, operational efficiency, efficiency regarding usage of

assets as well as financial leverage. Net profit margin represents operational efficiency,

efficiency of asset use is measured with asset turnover ratio and equity multiplier helps in

measuring leverage (Elsayed, 2017).

Trend analysis: It refers to a technique of technical analysis that is utilised for studying

financial data of an organization over a time period. It mainly focuses on change factor within

balance sheet as well as income statement of an organization. While conducting trend analysis of

Tesco, in context to its income statement in 2015 and 2016 it is interpreted that cost of sales of

an organization reduced from 95.3 percent of revenue to 94.9 percent. Gross profit of entity

enhanced from 4.7% to 5.1% which is a positive indicator as income earning capacity of from

core operations of business increased. Apart from this, administration expenses of Tesco

increased from 3.1% in 2015 to 3.4% in the year 2016. In relation to operating profit of an

organization, it increased from 1.6 percent to 1.7 percent from 2015 to 2016 which indicates that

ability of entity regarding management of operating expenses is improvising. Interest expenses

of company is 1percent in 2015 while it increased to 1.2 percent in 2016. profit before and after

tax reduced by 0.1 percent from 2015 to 2016 which states that overall profitability of business

declined over a period of time.

Financial analysis and interpretation:

Financial analysis and interpretation is an attempt for determining evaluation and

significance of financial information for the purpose of estimating position of funds in an

organization. Apart from it, this approach helps in forecasting future earning prospects of

business and determines ability of Tesco in context to payment of short term or long term

obligations. Main function of conducting financial analysis enabling effective management of

fund in business (Erdoğan and Erdoğan, 2020). Ratio analysis of Tesco is computed below for

determining financial performance of an enterprise. This framework is used for comparing

performance of business with other entity or its own past performance. It also helps in evaluating

trend line of company for formulating adequate strategies.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

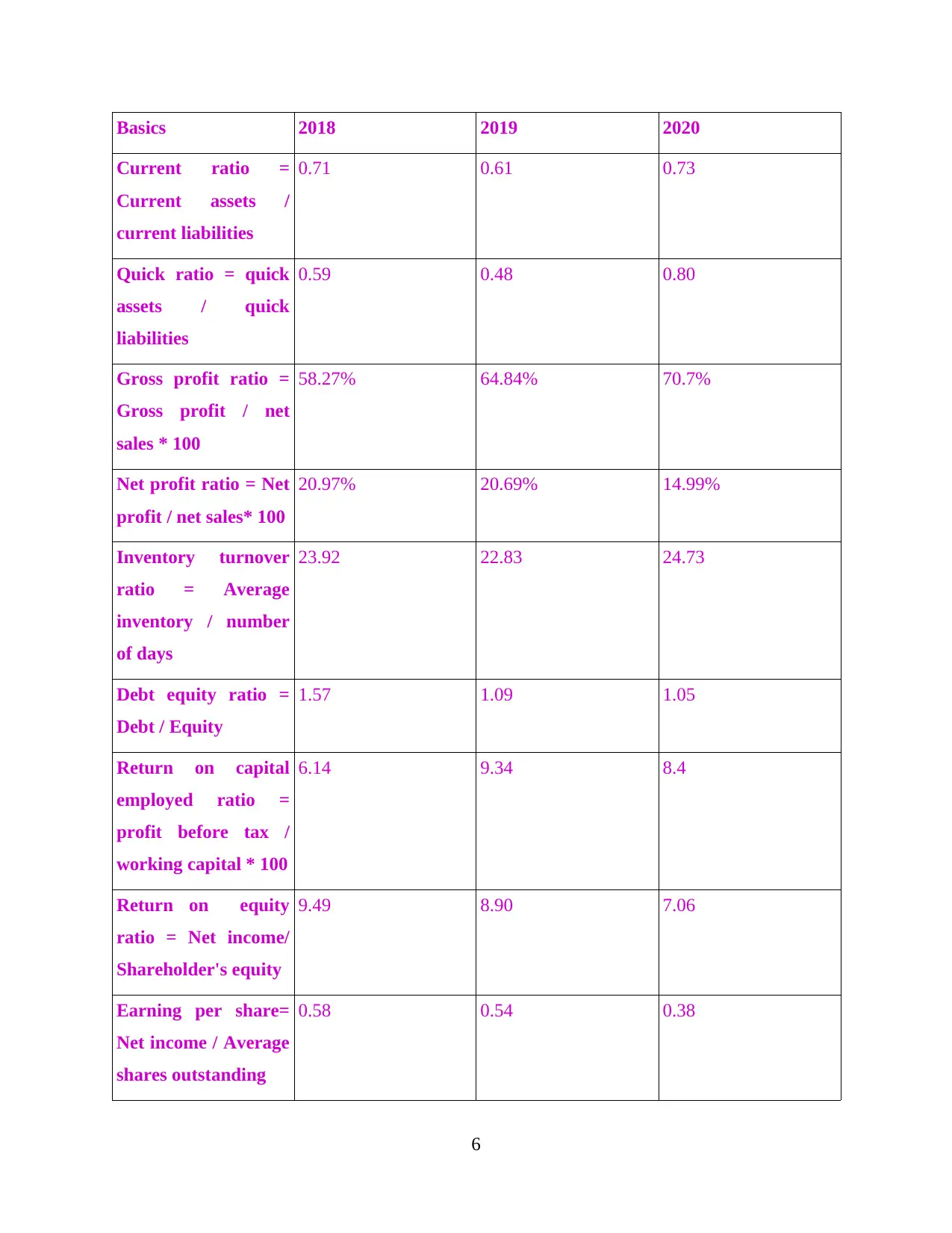

Ratio analysis of Tesco:

5

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Basics 2018 2019 2020

Current ratio =

Current assets /

current liabilities

0.71 0.61 0.73

Quick ratio = quick

assets / quick

liabilities

0.59 0.48 0.80

Gross profit ratio =

Gross profit / net

sales * 100

58.27% 64.84% 70.7%

Net profit ratio = Net

profit / net sales* 100

20.97% 20.69% 14.99%

Inventory turnover

ratio = Average

inventory / number

of days

23.92 22.83 24.73

Debt equity ratio =

Debt / Equity

1.57 1.09 1.05

Return on capital

employed ratio =

profit before tax /

working capital * 100

6.14 9.34 8.4

Return on equity

ratio = Net income/

Shareholder's equity

9.49 8.90 7.06

Earning per share=

Net income / Average

shares outstanding

0.58 0.54 0.38

6

Current ratio =

Current assets /

current liabilities

0.71 0.61 0.73

Quick ratio = quick

assets / quick

liabilities

0.59 0.48 0.80

Gross profit ratio =

Gross profit / net

sales * 100

58.27% 64.84% 70.7%

Net profit ratio = Net

profit / net sales* 100

20.97% 20.69% 14.99%

Inventory turnover

ratio = Average

inventory / number

of days

23.92 22.83 24.73

Debt equity ratio =

Debt / Equity

1.57 1.09 1.05

Return on capital

employed ratio =

profit before tax /

working capital * 100

6.14 9.34 8.4

Return on equity

ratio = Net income/

Shareholder's equity

9.49 8.90 7.06

Earning per share=

Net income / Average

shares outstanding

0.58 0.54 0.38

6

Liquidity ratio: This financial metric helps in determining ability of an enterprise in

paying off its current obligations without raising any external capital (Haskins, 2017). Current

ratio and quick ratio are calculated for analysing liquidity position of Tesco.

Current ratio measures that whether enterprise have enough resources for the purpose of

meeting its short term debts. Hence, it compares current assets of business with its current

liabilities. On interpretation of current assets of Tesco it can be noted that it decreased from 0.71

in 2018 to 0.61 in 2019 which states decrement in paying capacity of short term, while in 2020

current ratio of company again improved to 0.73. Hence, short term debt paying capacity of

Tesco has increased over a period of time.

Quick ratio evaluates liquidity position of an organization for analysing capacity of

company in paying its current debts by available liquid assets. It is also known as acid test ratio.

Higher acid test ratio indicates better liquidity position of business, while on the contrary lower

acid test ratio indicates negative results. Interpretation of quick ratio of Tesco states that quick

ratio of company was 0.59 in 2018 and it decreased to 0.48 in 2019. But, quick ratio of an

organization enhanced to 0.80 in the year 2020. Hence, liquidity position of business has

enhanced over time which indicates improvisation in liquidity position of enterprise.

Activity ratios: This financial metrics helps in analysing operational efficiency of an

enterprise. Hence, it is also termed as efficiency ratio (Kim, Kang and Park, 2019).

Inventory turnover ratio highlights efficiency of company in context to selling or

replacing inventory over a time period. On computation of inventory turnover ratio of Tesco it

can be noted that inventory turnover of company reduced from 23.92 times in the year 2018 to

22.83 times in the year 2019. It indicates decrement in sales of an organization. While, in the

year 2020, inventory turnover ratio of Tesco improvised to 24.73 times which states that

efficiency of company regarding management of inventory is increasing.

Financing ratio: It can be described as a magnitude which compares statistical values of

financial statement of an enterprise (Mitchell, Nørreklit and Nørreklit, 2017).

Debt equity ratio is a technique that helps in analysing capital structure of business and

it measures financial risk associated with an organization. Dent equity ratio of Tesco indicates

that it reduced from 1.57 in 2018 to 1.09 in the year 2019. Further, in 2020 its debt equity ratio

7

paying off its current obligations without raising any external capital (Haskins, 2017). Current

ratio and quick ratio are calculated for analysing liquidity position of Tesco.

Current ratio measures that whether enterprise have enough resources for the purpose of

meeting its short term debts. Hence, it compares current assets of business with its current

liabilities. On interpretation of current assets of Tesco it can be noted that it decreased from 0.71

in 2018 to 0.61 in 2019 which states decrement in paying capacity of short term, while in 2020

current ratio of company again improved to 0.73. Hence, short term debt paying capacity of

Tesco has increased over a period of time.

Quick ratio evaluates liquidity position of an organization for analysing capacity of

company in paying its current debts by available liquid assets. It is also known as acid test ratio.

Higher acid test ratio indicates better liquidity position of business, while on the contrary lower

acid test ratio indicates negative results. Interpretation of quick ratio of Tesco states that quick

ratio of company was 0.59 in 2018 and it decreased to 0.48 in 2019. But, quick ratio of an

organization enhanced to 0.80 in the year 2020. Hence, liquidity position of business has

enhanced over time which indicates improvisation in liquidity position of enterprise.

Activity ratios: This financial metrics helps in analysing operational efficiency of an

enterprise. Hence, it is also termed as efficiency ratio (Kim, Kang and Park, 2019).

Inventory turnover ratio highlights efficiency of company in context to selling or

replacing inventory over a time period. On computation of inventory turnover ratio of Tesco it

can be noted that inventory turnover of company reduced from 23.92 times in the year 2018 to

22.83 times in the year 2019. It indicates decrement in sales of an organization. While, in the

year 2020, inventory turnover ratio of Tesco improvised to 24.73 times which states that

efficiency of company regarding management of inventory is increasing.

Financing ratio: It can be described as a magnitude which compares statistical values of

financial statement of an enterprise (Mitchell, Nørreklit and Nørreklit, 2017).

Debt equity ratio is a technique that helps in analysing capital structure of business and

it measures financial risk associated with an organization. Dent equity ratio of Tesco indicates

that it reduced from 1.57 in 2018 to 1.09 in the year 2019. Further, in 2020 its debt equity ratio

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

further decreased to 1.05. Hence, it can be pinpointed that financial risk of Tesco is declining as

its debt component is reducing over a period of time.

Return on equity: It is calculated to measure financial performance of an organization

by dividing net income earned by business from shareholder's equity. From above calculated

return on equity of Tesco it can be identified that it reduced from 9.49 in 2018 to 8.90 in 2019

and 7.06 in 2020 which pinpoint decrement financial performance of an organization.

Earning per share: It refers earning that is generated by common shares of business. In

context to Tesco, its EPS decreased from 0.58 to 0.38 from 2018 to 2020. It indicates drcrement

in value of earnings in context to per outstanding shares.

Profitability ratio: This ratio is applied by managers of business and investors for the

purpose of analysing earning or profit generation capacity of an enterprise. It reveals about most

profitable sectors of business (Othman, 2020). There are several types of profitability ratios, such

as, gross profit ratio, net profit ratio etc.

Gross profit ratio indicates relationship among gross profit and net revenue of business.

In other words, this ratio is calculated for evaluating operational performance of an entity. Gross

profit of Tesco interprets that gross profit earned by company enhanced from 58.27 percent in

the year 2018 to 64.84 percent in the year 2017. while, in the year 2020 it further enhanced to

70.7 percentage. Hence, profit generation capacity of Tesco from its core operations increased in

during this time period which indicates increasing efficiency of business.

Net profit margin reveal actual profit that is earned by company after deducting all types

of expenses. Hence, net profit ratio states percentage of income that is generated by company. By

interpreting net profit margin of Tesco it can be stated that net profit margin of an organization

reduced from 20.97% to 14.99% from 2018 to 2020. hence, profitability factor of business is

decreasing.

Return on capital employed: It measures profitability of an enterprise in terms of

capital that is employed in business. It is utilised for analysing for analysing profitability of

company by investigating its capacity for earning profit from capital. From this ratio analysis it

can be interpreted that return on capital employed of Tesco was low in 2018, that is , 6.14 while

it increased at high level and showcased 78.4 return on capital employed in the year 2020. hence,

efficiency of an entity have improvising and company is gaining comparatively high level of

return from capital that is employed in it.

8

its debt component is reducing over a period of time.

Return on equity: It is calculated to measure financial performance of an organization

by dividing net income earned by business from shareholder's equity. From above calculated

return on equity of Tesco it can be identified that it reduced from 9.49 in 2018 to 8.90 in 2019

and 7.06 in 2020 which pinpoint decrement financial performance of an organization.

Earning per share: It refers earning that is generated by common shares of business. In

context to Tesco, its EPS decreased from 0.58 to 0.38 from 2018 to 2020. It indicates drcrement

in value of earnings in context to per outstanding shares.

Profitability ratio: This ratio is applied by managers of business and investors for the

purpose of analysing earning or profit generation capacity of an enterprise. It reveals about most

profitable sectors of business (Othman, 2020). There are several types of profitability ratios, such

as, gross profit ratio, net profit ratio etc.

Gross profit ratio indicates relationship among gross profit and net revenue of business.

In other words, this ratio is calculated for evaluating operational performance of an entity. Gross

profit of Tesco interprets that gross profit earned by company enhanced from 58.27 percent in

the year 2018 to 64.84 percent in the year 2017. while, in the year 2020 it further enhanced to

70.7 percentage. Hence, profit generation capacity of Tesco from its core operations increased in

during this time period which indicates increasing efficiency of business.

Net profit margin reveal actual profit that is earned by company after deducting all types

of expenses. Hence, net profit ratio states percentage of income that is generated by company. By

interpreting net profit margin of Tesco it can be stated that net profit margin of an organization

reduced from 20.97% to 14.99% from 2018 to 2020. hence, profitability factor of business is

decreasing.

Return on capital employed: It measures profitability of an enterprise in terms of

capital that is employed in business. It is utilised for analysing for analysing profitability of

company by investigating its capacity for earning profit from capital. From this ratio analysis it

can be interpreted that return on capital employed of Tesco was low in 2018, that is , 6.14 while

it increased at high level and showcased 78.4 return on capital employed in the year 2020. hence,

efficiency of an entity have improvising and company is gaining comparatively high level of

return from capital that is employed in it.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash flow analysis:

Cash flow analysis is a technique which is utilised for evaluating flow cash in an

organization during a predetermined time period (Yesiariani and Rahayu, 2017). Purpose of

analysis cash flow of Tesco is to identify sources of cash generation and areas in which business

incurs high expenditure. It helps in determining liquidity and solvency position of business. In

relevance to Tesco, it can be identified that outflow of cash is increasing due to improved

expenses of administration and interest charges.

Future prospects:

There is no doubt in the fact that pandemic of Covid 19 has hindered operations of

business at huge extent. This outbreak brought various new challenges for organizations in

context to attracting and retaining customers and maintaining long term sustainability.

Profitability of Tesco declined as sales unit reduced due to decrement in buying capacity of

customers. Apart from this, expenditures where high as company have to pay fixed expenses

such as, interest, rent, maintenance cost etc. here, Tesco possess an opportunity to increase

customer engagement by providing high quality services to customers, such as home delivery of

products, offering discounts etc. for the purpose of retaining customer base.

Recommendations:

For the purpose of increasing productivity and sustainability of Tesco, it is recommended

that company should focus on reducing its expenses by eliminating unnecessary expenditures.

Apart from this, company can further increase its operational efficiency by minimizing

operational cost. Risk factor associated with firm should be reduced by properly managing debts

of business.

CONCLUSION

From the above report it can be concluded that financial statement analysis enables

financial manager of an organization for gaining insight of financial situation of business by

evaluating and analysing its financial statements, which are, cash flow statement, income

statement as well as balance sheet. Fundamental analysis can be conducted by evaluating

segment analysis and trend analysis of business for investigating about its financial performance.

Trend analysis of Tesco states that efficiency of company is improving over a period of time.

Apart from this, profit earning capacity of an organization is also enhancing. By focusing on

9

Cash flow analysis is a technique which is utilised for evaluating flow cash in an

organization during a predetermined time period (Yesiariani and Rahayu, 2017). Purpose of

analysis cash flow of Tesco is to identify sources of cash generation and areas in which business

incurs high expenditure. It helps in determining liquidity and solvency position of business. In

relevance to Tesco, it can be identified that outflow of cash is increasing due to improved

expenses of administration and interest charges.

Future prospects:

There is no doubt in the fact that pandemic of Covid 19 has hindered operations of

business at huge extent. This outbreak brought various new challenges for organizations in

context to attracting and retaining customers and maintaining long term sustainability.

Profitability of Tesco declined as sales unit reduced due to decrement in buying capacity of

customers. Apart from this, expenditures where high as company have to pay fixed expenses

such as, interest, rent, maintenance cost etc. here, Tesco possess an opportunity to increase

customer engagement by providing high quality services to customers, such as home delivery of

products, offering discounts etc. for the purpose of retaining customer base.

Recommendations:

For the purpose of increasing productivity and sustainability of Tesco, it is recommended

that company should focus on reducing its expenses by eliminating unnecessary expenditures.

Apart from this, company can further increase its operational efficiency by minimizing

operational cost. Risk factor associated with firm should be reduced by properly managing debts

of business.

CONCLUSION

From the above report it can be concluded that financial statement analysis enables

financial manager of an organization for gaining insight of financial situation of business by

evaluating and analysing its financial statements, which are, cash flow statement, income

statement as well as balance sheet. Fundamental analysis can be conducted by evaluating

segment analysis and trend analysis of business for investigating about its financial performance.

Trend analysis of Tesco states that efficiency of company is improving over a period of time.

Apart from this, profit earning capacity of an organization is also enhancing. By focusing on

9

minimization of expenses and enhancing management activities in business company can further

improvise its profitability.

10

improvise its profitability.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.