Financial Analysis: Tesco Liquidity, Investment Appraisal, and LMU PLC

VerifiedAdded on 2020/02/05

|8

|985

|57

Report

AI Summary

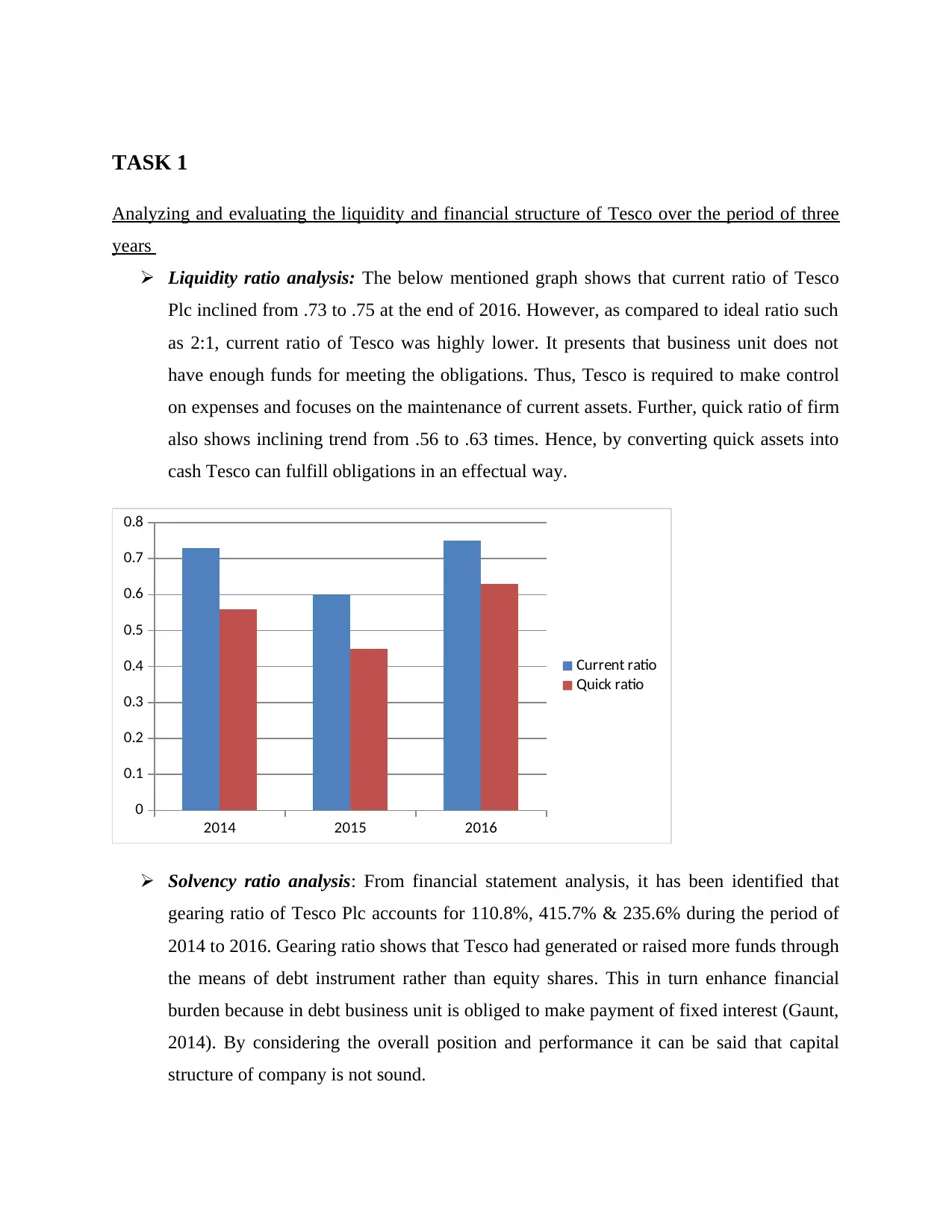

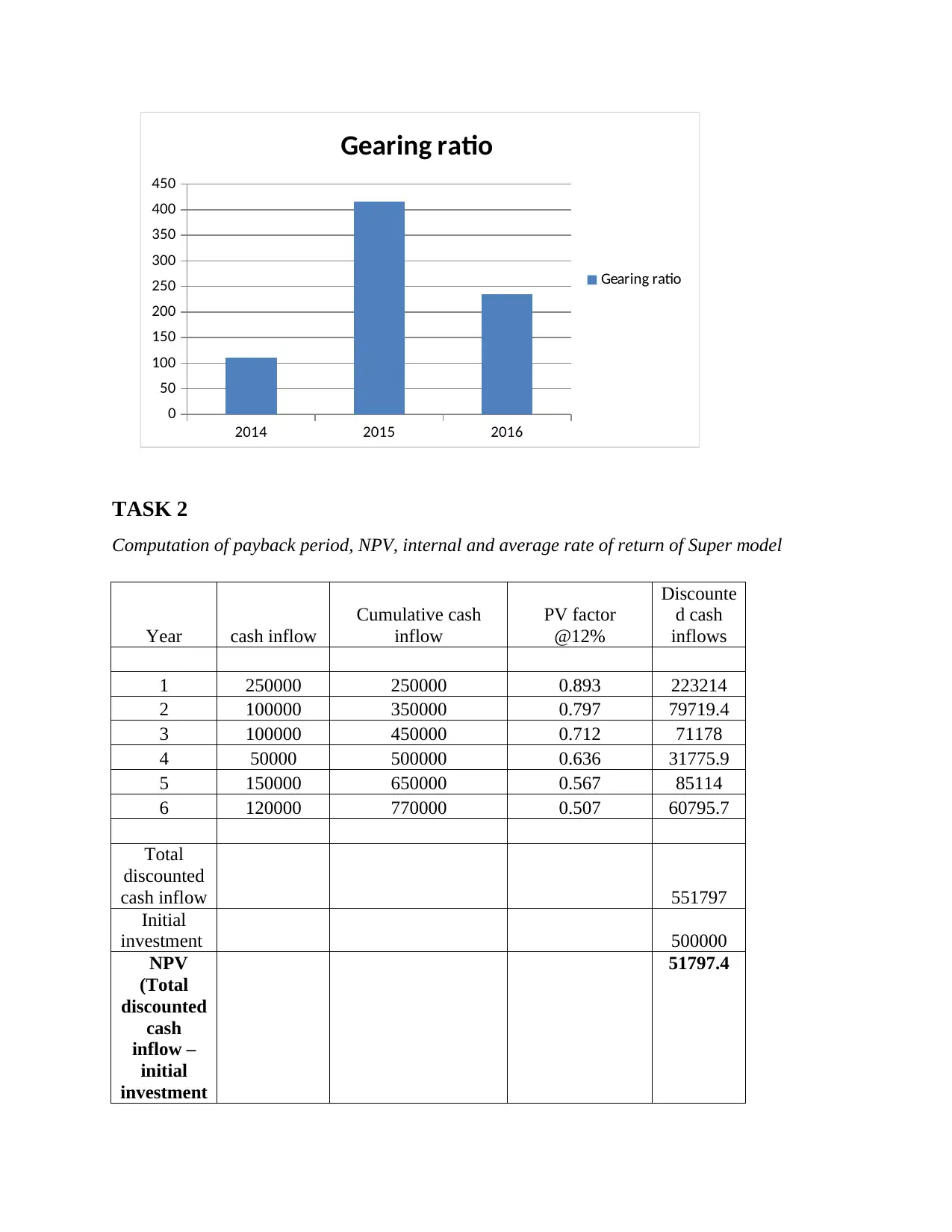

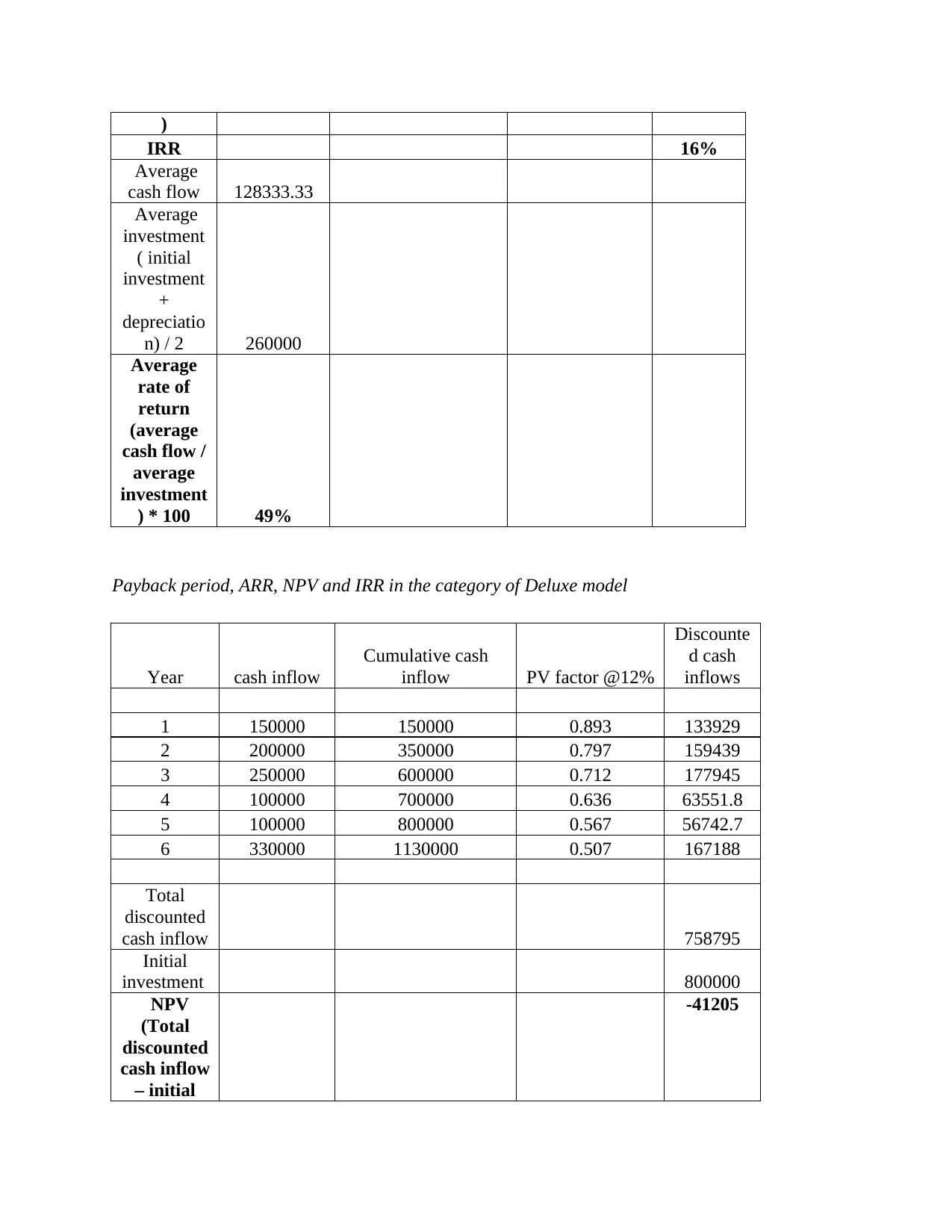

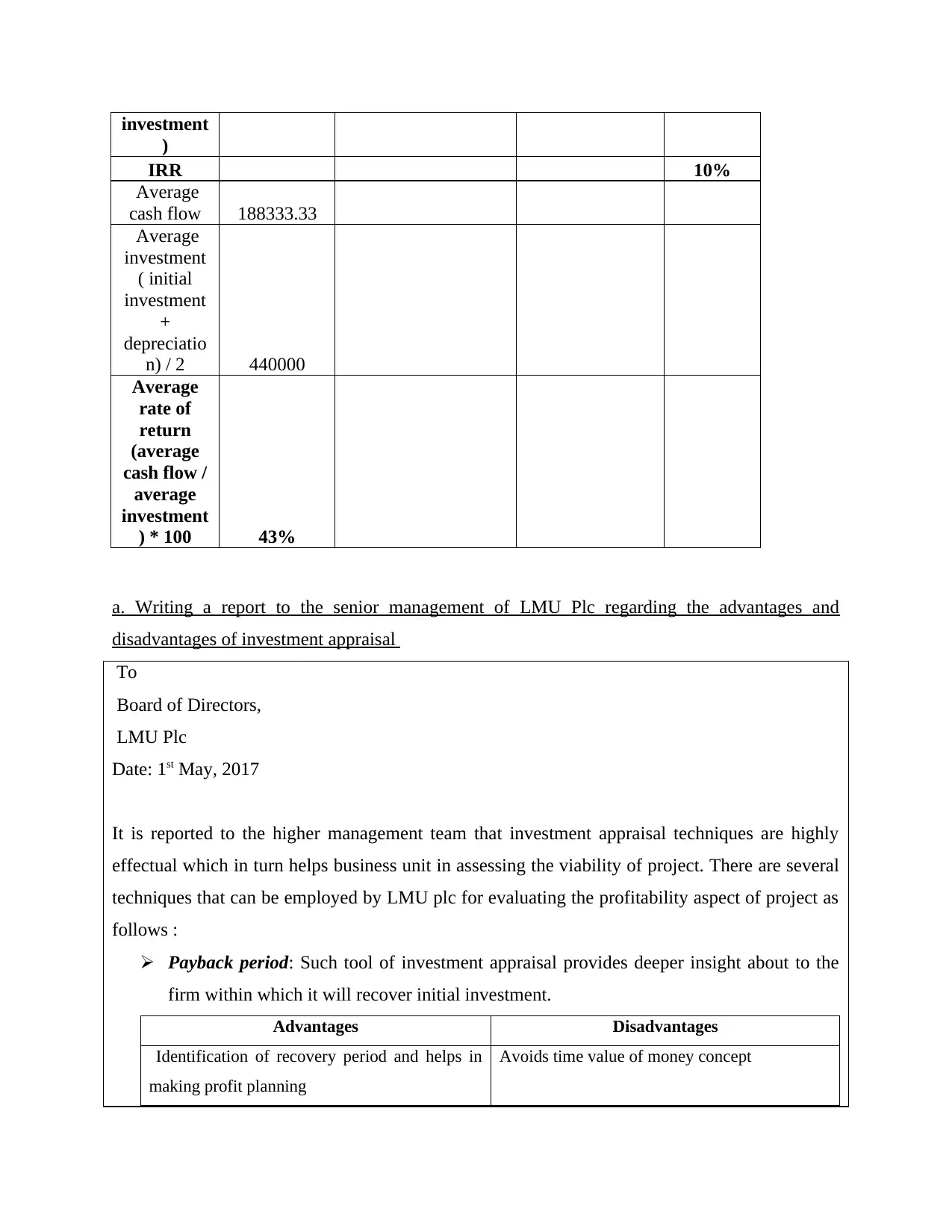

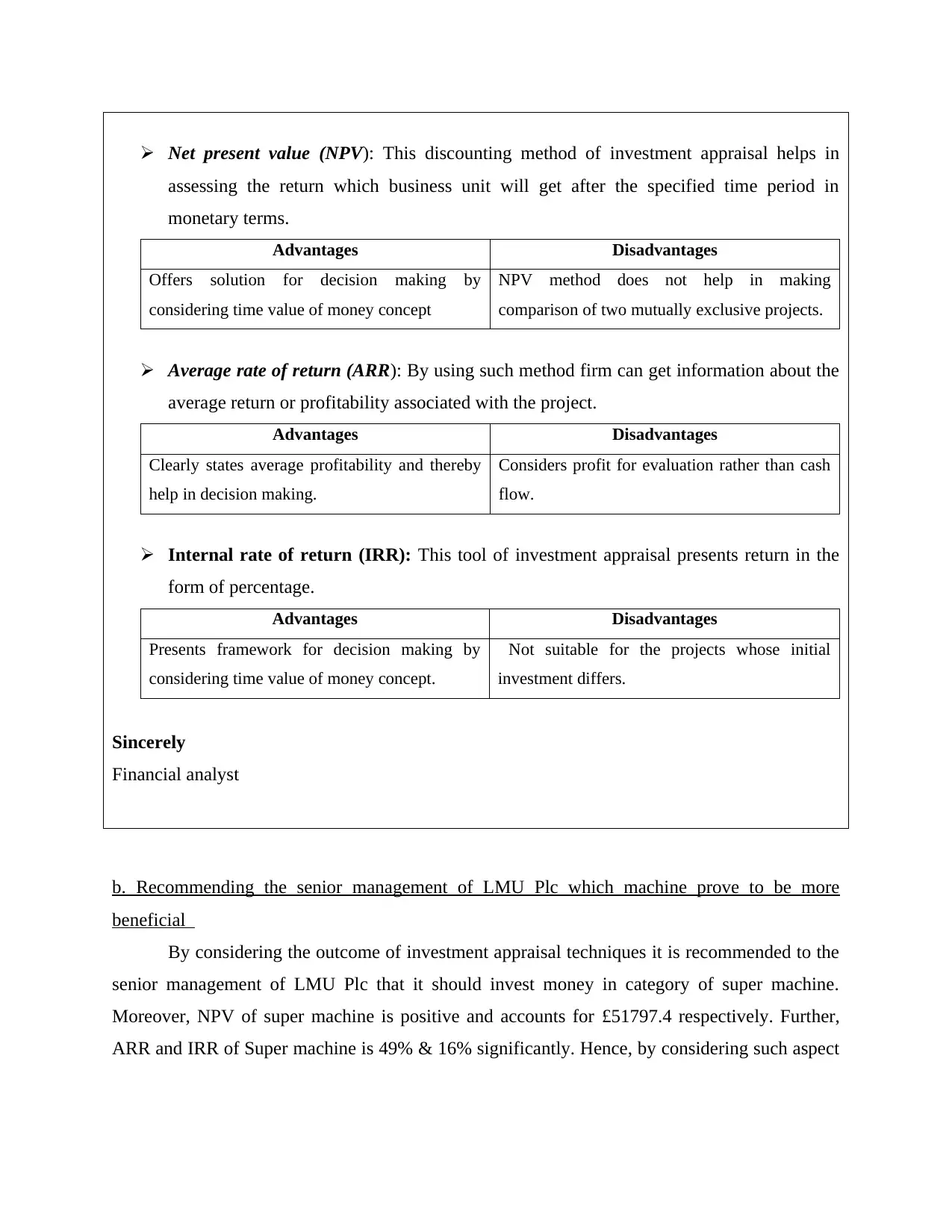

This report provides a detailed financial analysis of Tesco's performance over a three-year period, focusing on liquidity and solvency ratios. It evaluates Tesco's financial structure, highlighting the company's current and quick ratios, as well as its gearing ratio, to assess its ability to meet short-term obligations and manage its debt. The report also delves into investment appraisal techniques, including payback period, net present value (NPV), internal rate of return (IRR), and average rate of return (ARR), applied to two machine models (Super and Deluxe). It includes a report to LMU PLC's senior management, discussing the advantages and disadvantages of each appraisal method and recommending the 'Super' machine based on its superior financial metrics (positive NPV, higher IRR, and ARR). The analysis is supported by financial data, calculations, and references to relevant accounting and finance literature.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.