Analysis of Management Accounting Systems at Tesco: A Detailed Report

VerifiedAdded on 2020/12/09

|21

|5323

|106

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems, focusing on their application within Tesco. It begins by defining management accounting and exploring different types of systems, such as cost accounting, inventory management, job costing, and price optimization. The report then details various management accounting reporting methods used by Tesco, including accounts receivable aging, job cost reports, inventory and manufacturing reports, cash flow analysis, budgetary control, revaluation accounting, and statistical techniques. Furthermore, the report includes the production of income statements using both absorption costing and marginal costing techniques, providing a comparative analysis of the two methods. The report also discusses different planning tools and their advantages and disadvantages. Finally, it addresses adapting management accounting systems to respond to financial problems, offering practical insights and recommendations for Tesco's financial management.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK ..............................................................................................................................................1

P.1 Defining management accounting and different types of MA systems that could be used

by Tesco..................................................................................................................................1

P.2 Different methods used by Tesco for management accounting reporting.......................4

TASK 2............................................................................................................................................5

P.3 Production of income statements showing absorption costing and marginal costing

techniques...............................................................................................................................5

TASK 3..........................................................................................................................................10

P.4 Explaining advantages and disadvantages of different types of planning tool..............10

TASK 4..........................................................................................................................................13

P5. Adapting management accounting systems to respond to financial problems..............13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK ..............................................................................................................................................1

P.1 Defining management accounting and different types of MA systems that could be used

by Tesco..................................................................................................................................1

P.2 Different methods used by Tesco for management accounting reporting.......................4

TASK 2............................................................................................................................................5

P.3 Production of income statements showing absorption costing and marginal costing

techniques...............................................................................................................................5

TASK 3..........................................................................................................................................10

P.4 Explaining advantages and disadvantages of different types of planning tool..............10

TASK 4..........................................................................................................................................13

P5. Adapting management accounting systems to respond to financial problems..............13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

The performance of a business is reflected through accounting. There are two branches of

accountancy, fiscal and management. Financial division deals with fiscal data and transactions.

Management Accounting (MA) have wider scope, as it considers both monetary and

administrative information of business and aids the governance in significant decision making. In

presented report a detailed analysis is done of management accounting systems, its relevance and

applications in the organisation and it is carried out on the basis of Tesco, a leading retail chain

in retail sector in economy of UK. With these various reporting methods which can be used in

enterprise is presented, income statements are prepared on marginal and absorption accounting

technique. Different planning tools considerable in governance of firm, their advantages and

disadvantages are reported as well.

TASK

P.1 Defining management accounting and different types of MA systems that could be used by

Tesco.

Management accounting:

Management accounting is designed to produce financial data information for an

enterprises and to supply the same to those who need it. It requires utilization of qualified

information and skills for preparing accounting statements. This is done in such a manner that

can assist management of Tesco for development of policies and in planning and controlling of

operation of organisation.

“Management accounting system are deployed for providing information that can be used by

managements of an organisation for making quality decision.”

“The term management accounting, observes, Board and Carmichael, covers all those services

which can assist management and other departments in formation of policies and effective

control of operations of the organisation.”

This can be defined as a process of identification, measurement, summarization, analysis

and communication of financial information along with significant data related with operation

and administration of Tesco. All this information is critically evaluated by the management of

organisation in process of decision making so that proper steps and decision can be made for

growth and administration of firm (Ward, 2012). This is also referred as cost accounting system.

The main difference between financial and management accounting is that, the former one

1

The performance of a business is reflected through accounting. There are two branches of

accountancy, fiscal and management. Financial division deals with fiscal data and transactions.

Management Accounting (MA) have wider scope, as it considers both monetary and

administrative information of business and aids the governance in significant decision making. In

presented report a detailed analysis is done of management accounting systems, its relevance and

applications in the organisation and it is carried out on the basis of Tesco, a leading retail chain

in retail sector in economy of UK. With these various reporting methods which can be used in

enterprise is presented, income statements are prepared on marginal and absorption accounting

technique. Different planning tools considerable in governance of firm, their advantages and

disadvantages are reported as well.

TASK

P.1 Defining management accounting and different types of MA systems that could be used by

Tesco.

Management accounting:

Management accounting is designed to produce financial data information for an

enterprises and to supply the same to those who need it. It requires utilization of qualified

information and skills for preparing accounting statements. This is done in such a manner that

can assist management of Tesco for development of policies and in planning and controlling of

operation of organisation.

“Management accounting system are deployed for providing information that can be used by

managements of an organisation for making quality decision.”

“The term management accounting, observes, Board and Carmichael, covers all those services

which can assist management and other departments in formation of policies and effective

control of operations of the organisation.”

This can be defined as a process of identification, measurement, summarization, analysis

and communication of financial information along with significant data related with operation

and administration of Tesco. All this information is critically evaluated by the management of

organisation in process of decision making so that proper steps and decision can be made for

growth and administration of firm (Ward, 2012). This is also referred as cost accounting system.

The main difference between financial and management accounting is that, the former one

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

provides information that assist decision of outsider stakeholder, while later one focus on

providing data and information for aiding mangers in decision making process.

Functions of management accounting system: Provide data: data relevant for past progress and for making future forecast are provided

by management accounting. Analysis and interpretation of data: meaningfully analyses data is done for effective

planning and decision making. Means of communication: forwarding plans upward, downward outwards through

organisation.

Facilitates control: helps in translation of given objectives into strategies and plans for

effective achievement of goals.

Difference between management and financial accounting

Basis Financial accounting Management accounting

Period of Data evaluation After a definite time period At regular interval's

Objective Supply information in form of

P&L account, income

statements etc. for outside

stakeholders.

It is designed to provide

accounting information for

internal use of management

Precision Higher Lower

Legal compulsion Compulsory for every

business.

No need for every business to

install this system.

Different types of management accounting systems that can be applied in Tesco:

management accounting system is a frame work in which various objectives, functions

and elements are incorporated and evaluated for decision making. These are referred as

standardized system which aims at analysis, identifying and communication of information.

2

providing data and information for aiding mangers in decision making process.

Functions of management accounting system: Provide data: data relevant for past progress and for making future forecast are provided

by management accounting. Analysis and interpretation of data: meaningfully analyses data is done for effective

planning and decision making. Means of communication: forwarding plans upward, downward outwards through

organisation.

Facilitates control: helps in translation of given objectives into strategies and plans for

effective achievement of goals.

Difference between management and financial accounting

Basis Financial accounting Management accounting

Period of Data evaluation After a definite time period At regular interval's

Objective Supply information in form of

P&L account, income

statements etc. for outside

stakeholders.

It is designed to provide

accounting information for

internal use of management

Precision Higher Lower

Legal compulsion Compulsory for every

business.

No need for every business to

install this system.

Different types of management accounting systems that can be applied in Tesco:

management accounting system is a frame work in which various objectives, functions

and elements are incorporated and evaluated for decision making. These are referred as

standardized system which aims at analysis, identifying and communication of information.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

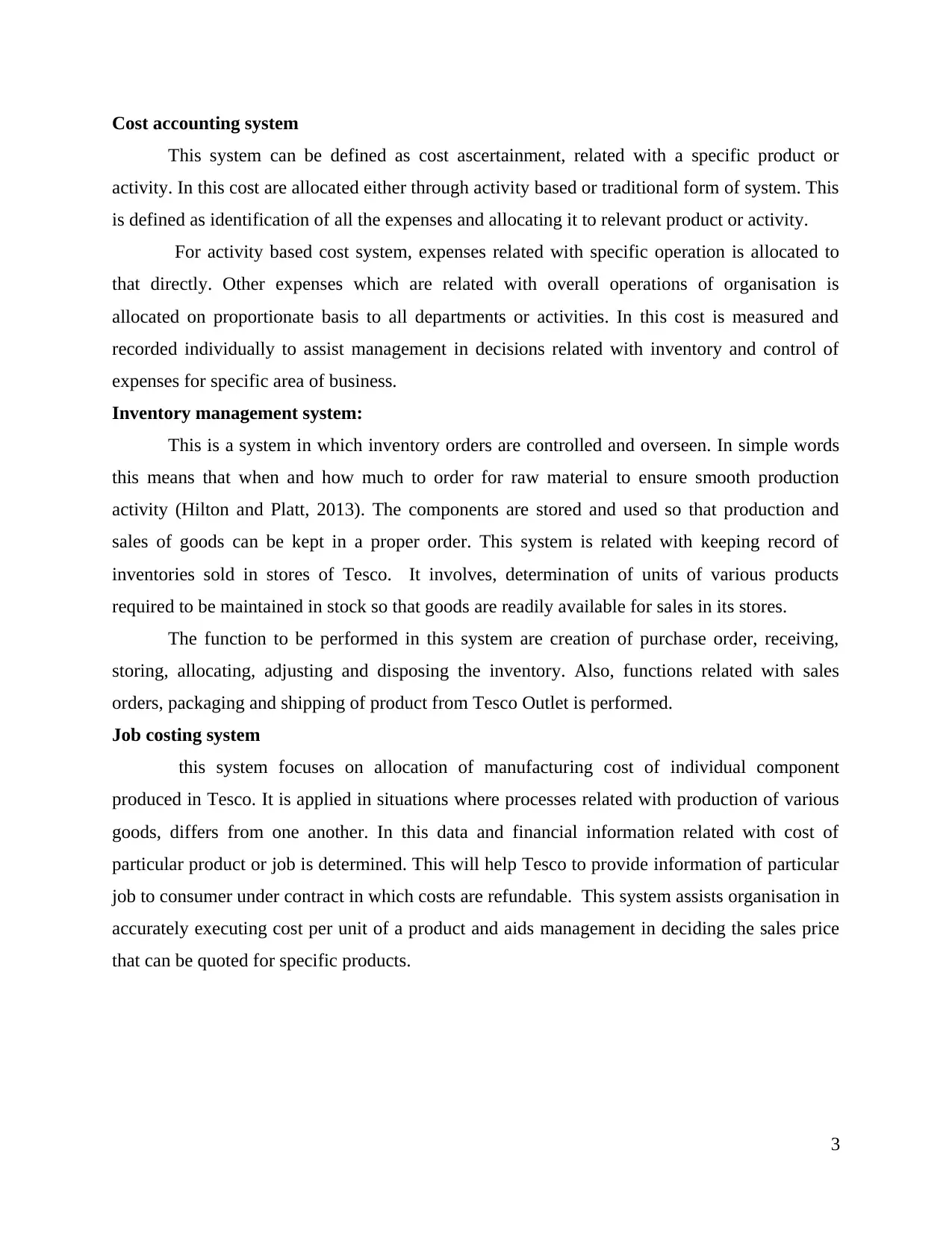

Cost accounting system

This system can be defined as cost ascertainment, related with a specific product or

activity. In this cost are allocated either through activity based or traditional form of system. This

is defined as identification of all the expenses and allocating it to relevant product or activity.

For activity based cost system, expenses related with specific operation is allocated to

that directly. Other expenses which are related with overall operations of organisation is

allocated on proportionate basis to all departments or activities. In this cost is measured and

recorded individually to assist management in decisions related with inventory and control of

expenses for specific area of business.

Inventory management system:

This is a system in which inventory orders are controlled and overseen. In simple words

this means that when and how much to order for raw material to ensure smooth production

activity (Hilton and Platt, 2013). The components are stored and used so that production and

sales of goods can be kept in a proper order. This system is related with keeping record of

inventories sold in stores of Tesco. It involves, determination of units of various products

required to be maintained in stock so that goods are readily available for sales in its stores.

The function to be performed in this system are creation of purchase order, receiving,

storing, allocating, adjusting and disposing the inventory. Also, functions related with sales

orders, packaging and shipping of product from Tesco Outlet is performed.

Job costing system

this system focuses on allocation of manufacturing cost of individual component

produced in Tesco. It is applied in situations where processes related with production of various

goods, differs from one another. In this data and financial information related with cost of

particular product or job is determined. This will help Tesco to provide information of particular

job to consumer under contract in which costs are refundable. This system assists organisation in

accurately executing cost per unit of a product and aids management in deciding the sales price

that can be quoted for specific products.

3

This system can be defined as cost ascertainment, related with a specific product or

activity. In this cost are allocated either through activity based or traditional form of system. This

is defined as identification of all the expenses and allocating it to relevant product or activity.

For activity based cost system, expenses related with specific operation is allocated to

that directly. Other expenses which are related with overall operations of organisation is

allocated on proportionate basis to all departments or activities. In this cost is measured and

recorded individually to assist management in decisions related with inventory and control of

expenses for specific area of business.

Inventory management system:

This is a system in which inventory orders are controlled and overseen. In simple words

this means that when and how much to order for raw material to ensure smooth production

activity (Hilton and Platt, 2013). The components are stored and used so that production and

sales of goods can be kept in a proper order. This system is related with keeping record of

inventories sold in stores of Tesco. It involves, determination of units of various products

required to be maintained in stock so that goods are readily available for sales in its stores.

The function to be performed in this system are creation of purchase order, receiving,

storing, allocating, adjusting and disposing the inventory. Also, functions related with sales

orders, packaging and shipping of product from Tesco Outlet is performed.

Job costing system

this system focuses on allocation of manufacturing cost of individual component

produced in Tesco. It is applied in situations where processes related with production of various

goods, differs from one another. In this data and financial information related with cost of

particular product or job is determined. This will help Tesco to provide information of particular

job to consumer under contract in which costs are refundable. This system assists organisation in

accurately executing cost per unit of a product and aids management in deciding the sales price

that can be quoted for specific products.

3

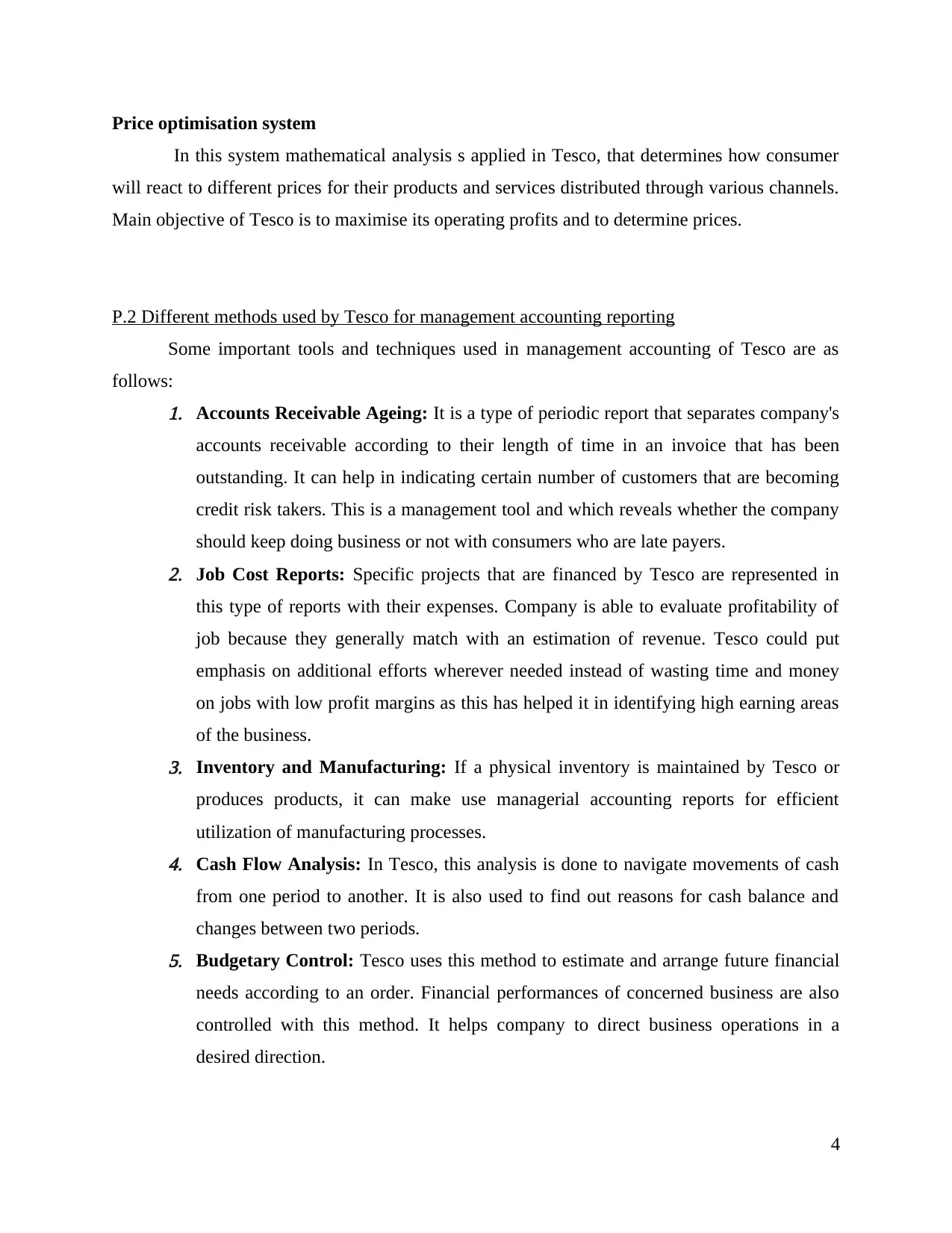

Price optimisation system

In this system mathematical analysis s applied in Tesco, that determines how consumer

will react to different prices for their products and services distributed through various channels.

Main objective of Tesco is to maximise its operating profits and to determine prices.

P.2 Different methods used by Tesco for management accounting reporting

Some important tools and techniques used in management accounting of Tesco are as

follows:

1. Accounts Receivable Ageing: It is a type of periodic report that separates company's

accounts receivable according to their length of time in an invoice that has been

outstanding. It can help in indicating certain number of customers that are becoming

credit risk takers. This is a management tool and which reveals whether the company

should keep doing business or not with consumers who are late payers.

2. Job Cost Reports: Specific projects that are financed by Tesco are represented in

this type of reports with their expenses. Company is able to evaluate profitability of

job because they generally match with an estimation of revenue. Tesco could put

emphasis on additional efforts wherever needed instead of wasting time and money

on jobs with low profit margins as this has helped it in identifying high earning areas

of the business.

3. Inventory and Manufacturing: If a physical inventory is maintained by Tesco or

produces products, it can make use managerial accounting reports for efficient

utilization of manufacturing processes.

4. Cash Flow Analysis: In Tesco, this analysis is done to navigate movements of cash

from one period to another. It is also used to find out reasons for cash balance and

changes between two periods.

5. Budgetary Control: Tesco uses this method to estimate and arrange future financial

needs according to an order. Financial performances of concerned business are also

controlled with this method. It helps company to direct business operations in a

desired direction.

4

In this system mathematical analysis s applied in Tesco, that determines how consumer

will react to different prices for their products and services distributed through various channels.

Main objective of Tesco is to maximise its operating profits and to determine prices.

P.2 Different methods used by Tesco for management accounting reporting

Some important tools and techniques used in management accounting of Tesco are as

follows:

1. Accounts Receivable Ageing: It is a type of periodic report that separates company's

accounts receivable according to their length of time in an invoice that has been

outstanding. It can help in indicating certain number of customers that are becoming

credit risk takers. This is a management tool and which reveals whether the company

should keep doing business or not with consumers who are late payers.

2. Job Cost Reports: Specific projects that are financed by Tesco are represented in

this type of reports with their expenses. Company is able to evaluate profitability of

job because they generally match with an estimation of revenue. Tesco could put

emphasis on additional efforts wherever needed instead of wasting time and money

on jobs with low profit margins as this has helped it in identifying high earning areas

of the business.

3. Inventory and Manufacturing: If a physical inventory is maintained by Tesco or

produces products, it can make use managerial accounting reports for efficient

utilization of manufacturing processes.

4. Cash Flow Analysis: In Tesco, this analysis is done to navigate movements of cash

from one period to another. It is also used to find out reasons for cash balance and

changes between two periods.

5. Budgetary Control: Tesco uses this method to estimate and arrange future financial

needs according to an order. Financial performances of concerned business are also

controlled with this method. It helps company to direct business operations in a

desired direction.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

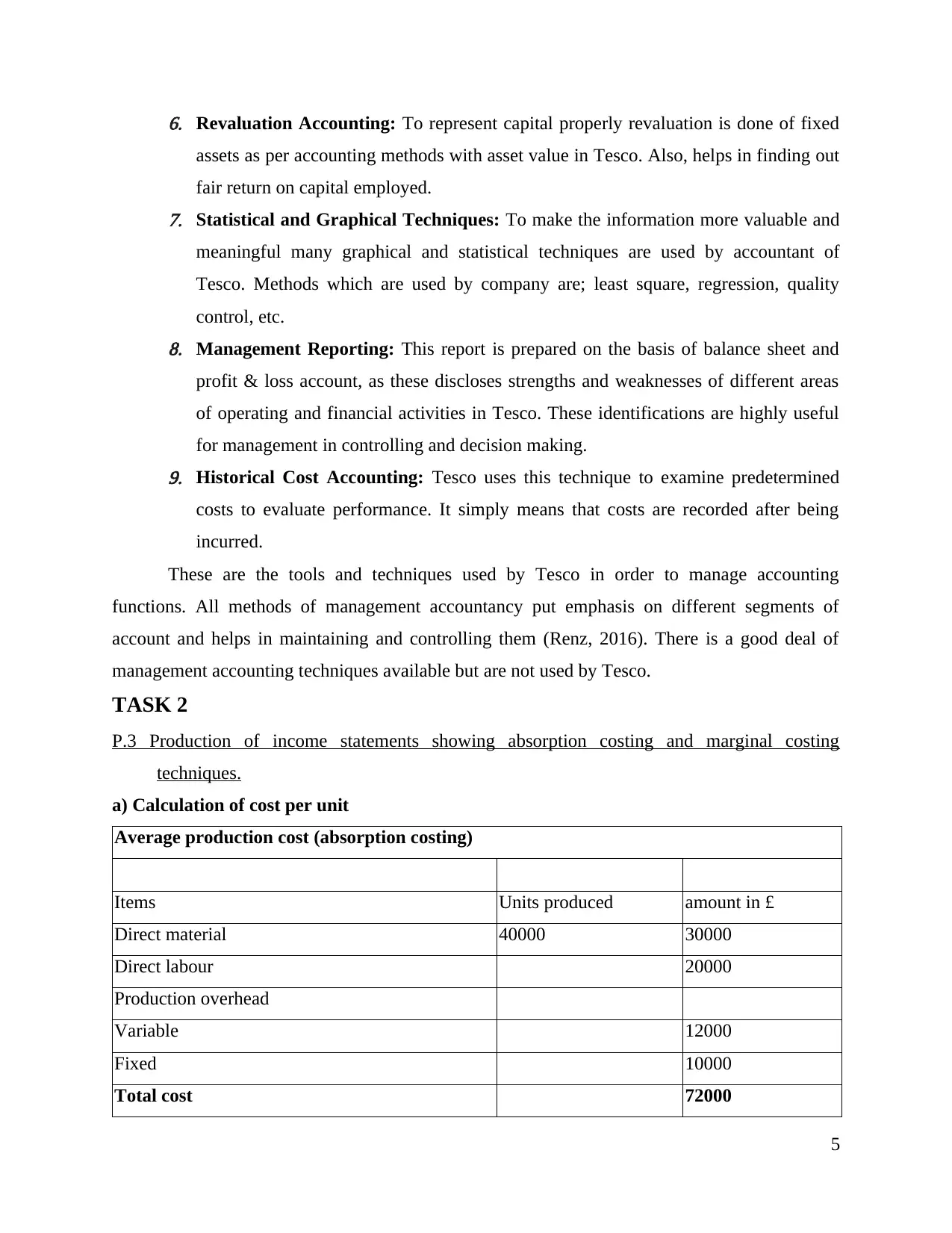

6. Revaluation Accounting: To represent capital properly revaluation is done of fixed

assets as per accounting methods with asset value in Tesco. Also, helps in finding out

fair return on capital employed.

7. Statistical and Graphical Techniques: To make the information more valuable and

meaningful many graphical and statistical techniques are used by accountant of

Tesco. Methods which are used by company are; least square, regression, quality

control, etc.

8. Management Reporting: This report is prepared on the basis of balance sheet and

profit & loss account, as these discloses strengths and weaknesses of different areas

of operating and financial activities in Tesco. These identifications are highly useful

for management in controlling and decision making.

9. Historical Cost Accounting: Tesco uses this technique to examine predetermined

costs to evaluate performance. It simply means that costs are recorded after being

incurred.

These are the tools and techniques used by Tesco in order to manage accounting

functions. All methods of management accountancy put emphasis on different segments of

account and helps in maintaining and controlling them (Renz, 2016). There is a good deal of

management accounting techniques available but are not used by Tesco.

TASK 2

P.3 Production of income statements showing absorption costing and marginal costing

techniques.

a) Calculation of cost per unit

Average production cost (absorption costing)

Items Units produced amount in £

Direct material 40000 30000

Direct labour 20000

Production overhead

Variable 12000

Fixed 10000

Total cost 72000

5

assets as per accounting methods with asset value in Tesco. Also, helps in finding out

fair return on capital employed.

7. Statistical and Graphical Techniques: To make the information more valuable and

meaningful many graphical and statistical techniques are used by accountant of

Tesco. Methods which are used by company are; least square, regression, quality

control, etc.

8. Management Reporting: This report is prepared on the basis of balance sheet and

profit & loss account, as these discloses strengths and weaknesses of different areas

of operating and financial activities in Tesco. These identifications are highly useful

for management in controlling and decision making.

9. Historical Cost Accounting: Tesco uses this technique to examine predetermined

costs to evaluate performance. It simply means that costs are recorded after being

incurred.

These are the tools and techniques used by Tesco in order to manage accounting

functions. All methods of management accountancy put emphasis on different segments of

account and helps in maintaining and controlling them (Renz, 2016). There is a good deal of

management accounting techniques available but are not used by Tesco.

TASK 2

P.3 Production of income statements showing absorption costing and marginal costing

techniques.

a) Calculation of cost per unit

Average production cost (absorption costing)

Items Units produced amount in £

Direct material 40000 30000

Direct labour 20000

Production overhead

Variable 12000

Fixed 10000

Total cost 72000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost per unit 1.8

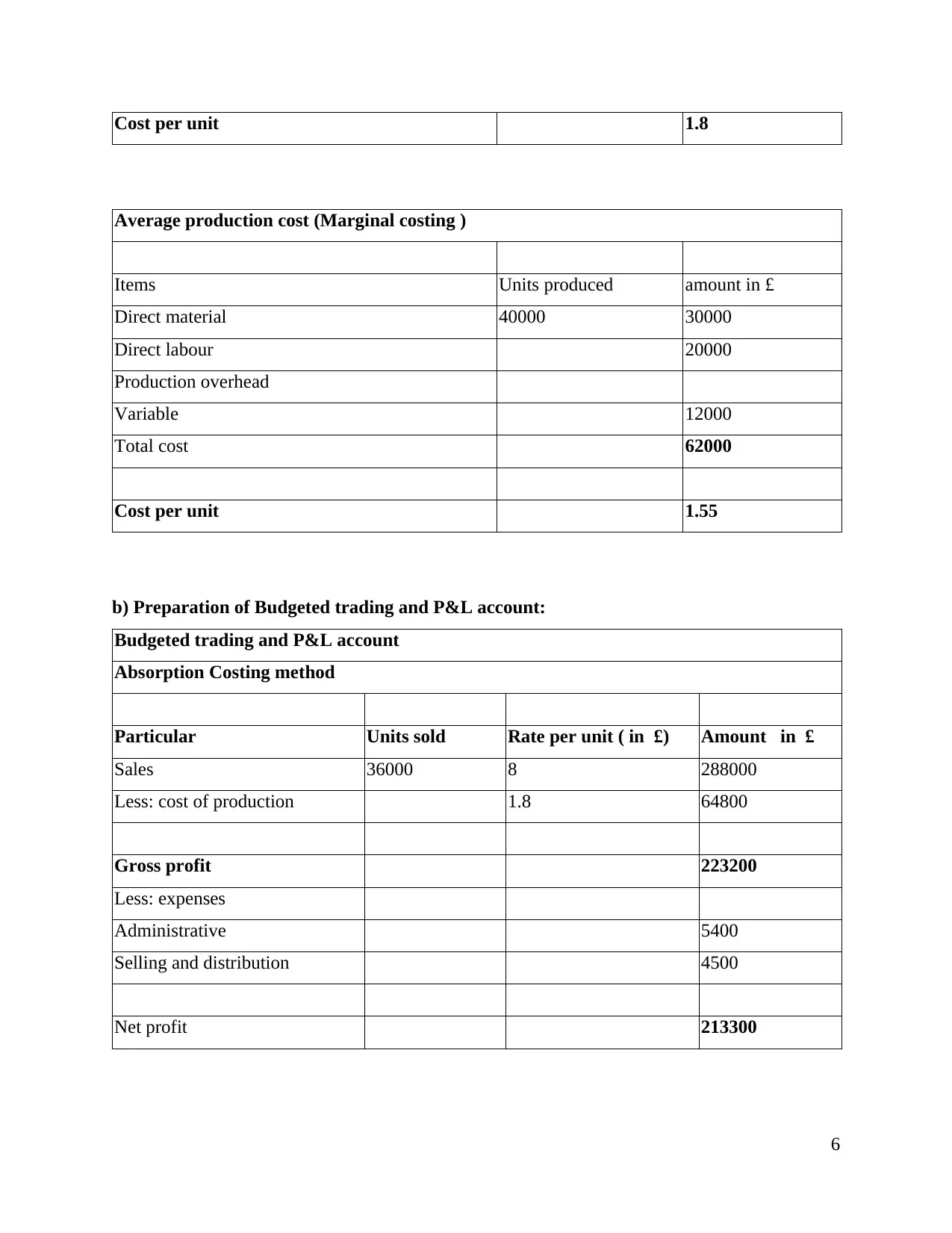

Average production cost (Marginal costing )

Items Units produced amount in £

Direct material 40000 30000

Direct labour 20000

Production overhead

Variable 12000

Total cost 62000

Cost per unit 1.55

b) Preparation of Budgeted trading and P&L account:

Budgeted trading and P&L account

Absorption Costing method

Particular Units sold Rate per unit ( in £) Amount in £

Sales 36000 8 288000

Less: cost of production 1.8 64800

Gross profit 223200

Less: expenses

Administrative 5400

Selling and distribution 4500

Net profit 213300

6

Average production cost (Marginal costing )

Items Units produced amount in £

Direct material 40000 30000

Direct labour 20000

Production overhead

Variable 12000

Total cost 62000

Cost per unit 1.55

b) Preparation of Budgeted trading and P&L account:

Budgeted trading and P&L account

Absorption Costing method

Particular Units sold Rate per unit ( in £) Amount in £

Sales 36000 8 288000

Less: cost of production 1.8 64800

Gross profit 223200

Less: expenses

Administrative 5400

Selling and distribution 4500

Net profit 213300

6

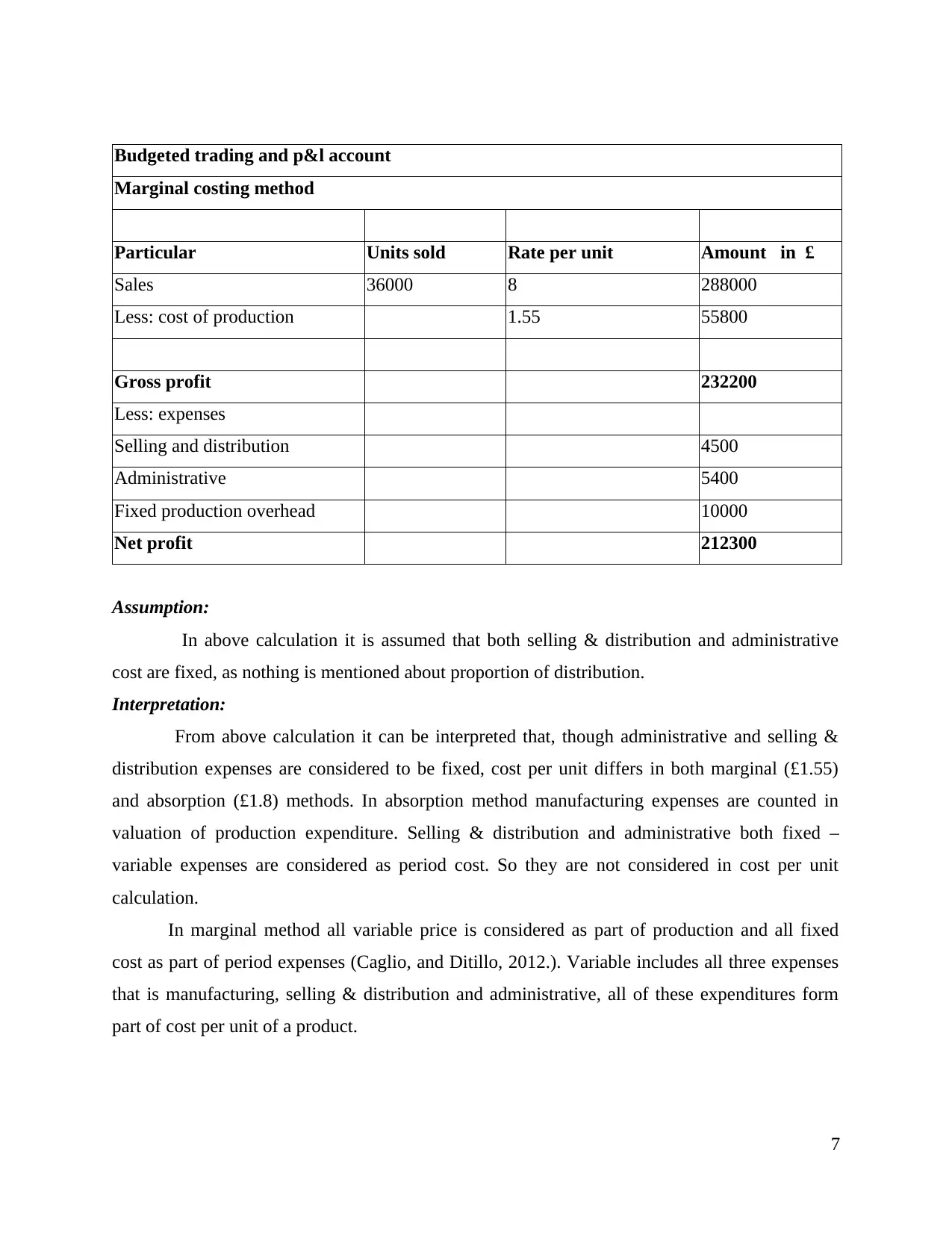

Budgeted trading and p&l account

Marginal costing method

Particular Units sold Rate per unit Amount in £

Sales 36000 8 288000

Less: cost of production 1.55 55800

Gross profit 232200

Less: expenses

Selling and distribution 4500

Administrative 5400

Fixed production overhead 10000

Net profit 212300

Assumption:

In above calculation it is assumed that both selling & distribution and administrative

cost are fixed, as nothing is mentioned about proportion of distribution.

Interpretation:

From above calculation it can be interpreted that, though administrative and selling &

distribution expenses are considered to be fixed, cost per unit differs in both marginal (£1.55)

and absorption (£1.8) methods. In absorption method manufacturing expenses are counted in

valuation of production expenditure. Selling & distribution and administrative both fixed –

variable expenses are considered as period cost. So they are not considered in cost per unit

calculation.

In marginal method all variable price is considered as part of production and all fixed

cost as part of period expenses (Caglio, and Ditillo, 2012.). Variable includes all three expenses

that is manufacturing, selling & distribution and administrative, all of these expenditures form

part of cost per unit of a product.

7

Marginal costing method

Particular Units sold Rate per unit Amount in £

Sales 36000 8 288000

Less: cost of production 1.55 55800

Gross profit 232200

Less: expenses

Selling and distribution 4500

Administrative 5400

Fixed production overhead 10000

Net profit 212300

Assumption:

In above calculation it is assumed that both selling & distribution and administrative

cost are fixed, as nothing is mentioned about proportion of distribution.

Interpretation:

From above calculation it can be interpreted that, though administrative and selling &

distribution expenses are considered to be fixed, cost per unit differs in both marginal (£1.55)

and absorption (£1.8) methods. In absorption method manufacturing expenses are counted in

valuation of production expenditure. Selling & distribution and administrative both fixed –

variable expenses are considered as period cost. So they are not considered in cost per unit

calculation.

In marginal method all variable price is considered as part of production and all fixed

cost as part of period expenses (Caglio, and Ditillo, 2012.). Variable includes all three expenses

that is manufacturing, selling & distribution and administrative, all of these expenditures form

part of cost per unit of a product.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

C) Advice to Heinz

Form the above calculation it can be concluded that in both the method company will

earn good profits. Cost of production is very low and sales prices are set high. Though price per

unit in absorption costing is high at £1.88 but it considers fixed manufacturing expenditure as

part of per product price giving a net profit of £213300. In marginal costing method value per

unit is £1.55 only but it considered fixed factory expenses of £10000 as part period expenditure

not as per unit value. Hence, giving a profit of £212300.

This is suggested to Heinz that, it can proceed with production plan as both methods are

giving good profits and in order to earn maximum profitability. Company can adopt absorption

method as it will generate higher profits of 10000 as compared to marginal costing technique.

Absorption Costing

This type of costing is also known as full cost accounting and is an accepted technique of

determining cost. In this method value is made up of direct plus overhead costs absorbed on

some suitable basis. In this techniques cost per unit remains same but when each unit fluctuates it

also changes level of output because of fixed cost which remains constant. In case of one product

and no inventory it is very useful. This method is also used in GAAP principles of accounting in

UK. In Tesco while considering absorption cost, all manufacturing costs are treated as product

costs. The COGS (cost of goods sold) would include direct materials, direct labour and overhead.

Advantages of Absorption Costing:

8

Illustration 1: Absorption Costing Income Statement.

(Source: Absorption Costing, 2018)

Form the above calculation it can be concluded that in both the method company will

earn good profits. Cost of production is very low and sales prices are set high. Though price per

unit in absorption costing is high at £1.88 but it considers fixed manufacturing expenditure as

part of per product price giving a net profit of £213300. In marginal costing method value per

unit is £1.55 only but it considered fixed factory expenses of £10000 as part period expenditure

not as per unit value. Hence, giving a profit of £212300.

This is suggested to Heinz that, it can proceed with production plan as both methods are

giving good profits and in order to earn maximum profitability. Company can adopt absorption

method as it will generate higher profits of 10000 as compared to marginal costing technique.

Absorption Costing

This type of costing is also known as full cost accounting and is an accepted technique of

determining cost. In this method value is made up of direct plus overhead costs absorbed on

some suitable basis. In this techniques cost per unit remains same but when each unit fluctuates it

also changes level of output because of fixed cost which remains constant. In case of one product

and no inventory it is very useful. This method is also used in GAAP principles of accounting in

UK. In Tesco while considering absorption cost, all manufacturing costs are treated as product

costs. The COGS (cost of goods sold) would include direct materials, direct labour and overhead.

Advantages of Absorption Costing:

8

Illustration 1: Absorption Costing Income Statement.

(Source: Absorption Costing, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Consideration of fixed costs: Importance of including fixed production costs in

determining suitable pricing policy is recognised correctly by absorption costing in

Tesco.

2. Seasonal Sales: This costing method is more reliable in case where production is

done to incur sales in future as it shows correct calculation of profits as compared to

variable costing. All fixed costs will be represented as an expense in the same

accounting period where variable costing might be zero in such cases.

3. Conformity with Accrual and Matching Concepts: Accounting concepts are

matched and accrual with help of absorption costing which involves revenue with

matching costs for a specific accounting period.

Disadvantages:

1. Difficulty in comparison and control of cost: Different costs are obtained from

diverse extents in Tesco as this type of costing depends upon level of output. An

increase in the volume of output normally results in reduction of unit costs and

decrease in output effects in an increased cost per unit because of existence of fixed

expenses.

2. Not Helpful in Managerial Decisions: This type of costing is not very much helpful

in making management decisions like; selection of suitable product mix, etc.

3. Cost Vitiated because of Fixed Cost included in Inventory: A part of fixed cost is

carried forward to the next accounting period as closing stock which is valued at cost

of production.

4. Fixed Cost Inclusion in cost not justified: These costs do not provide future

benefits as selling over heads, administration and fixed manufacturing are period

costs. Tesco also argued about the same.

Marginal Costing

It is a technique in which variable costing is charged to units of cost, while fixed cost is

completely written off against the contribution.

Marginal Cost = Direct Material + Direct Labour + Direct Expenses + Variable Overheads

9

determining suitable pricing policy is recognised correctly by absorption costing in

Tesco.

2. Seasonal Sales: This costing method is more reliable in case where production is

done to incur sales in future as it shows correct calculation of profits as compared to

variable costing. All fixed costs will be represented as an expense in the same

accounting period where variable costing might be zero in such cases.

3. Conformity with Accrual and Matching Concepts: Accounting concepts are

matched and accrual with help of absorption costing which involves revenue with

matching costs for a specific accounting period.

Disadvantages:

1. Difficulty in comparison and control of cost: Different costs are obtained from

diverse extents in Tesco as this type of costing depends upon level of output. An

increase in the volume of output normally results in reduction of unit costs and

decrease in output effects in an increased cost per unit because of existence of fixed

expenses.

2. Not Helpful in Managerial Decisions: This type of costing is not very much helpful

in making management decisions like; selection of suitable product mix, etc.

3. Cost Vitiated because of Fixed Cost included in Inventory: A part of fixed cost is

carried forward to the next accounting period as closing stock which is valued at cost

of production.

4. Fixed Cost Inclusion in cost not justified: These costs do not provide future

benefits as selling over heads, administration and fixed manufacturing are period

costs. Tesco also argued about the same.

Marginal Costing

It is a technique in which variable costing is charged to units of cost, while fixed cost is

completely written off against the contribution.

Marginal Cost = Direct Material + Direct Labour + Direct Expenses + Variable Overheads

9

Advantages of Marginal Costing:

1. Cost Control: Marginal costing had made it easy to determine and control costs of

production. Management could be able to concentrate on achieving and maintaining a

consistent marginal cost by avoiding the arbitrary allocation of fixed overhead costs.

2. Simplicity: This type of costing is easy to understand and operate and have capability to

combine with other forms of costing without having much difficulty.

3. Maximum return to the business: The effects of alternative sales or production policies

are easily accepted, appreciated and assessed with help of marginal costing to ensure that

decisions taken will yield the maximum return to business.

Disadvantages:

1. Classifying Costs: Since all costs are variable in a long run, it becomes hard to

separate fixed and variable costs clearly. Such classifications may give misleading

results.

2. Recovery of Overheads: There is often the problem of under or over recovery of

overheads as variable costs are implemented on the basis of estimation not on actual

value.

TASK 3

P.4 Explaining advantages and disadvantages of different types of planning tool

Following are some types of planning tools which are used by Tesco in budgetary

control: Zero Based Budgeting- ZBB: All the expenses for each new period must be justified in

this method. This process starts with zero base and every function is analysed according

to its cost and needs within an organization (Zimmerman and Yahya-Zadeh, 2011). It

allows top level strategic goals to implement into the budgeting process.

Advantages:

1. It provides a systematic way to evaluate operations and programmes of activity to the

organization.

2. It allows management to allocate resources according to the priority of programme.

3. It enables departmental budgets to be proved on the basis of cost benefit comparison.

(Zero Base Budgeting: Advantages and Limitations, 2018)

Disadvantages:

10

1. Cost Control: Marginal costing had made it easy to determine and control costs of

production. Management could be able to concentrate on achieving and maintaining a

consistent marginal cost by avoiding the arbitrary allocation of fixed overhead costs.

2. Simplicity: This type of costing is easy to understand and operate and have capability to

combine with other forms of costing without having much difficulty.

3. Maximum return to the business: The effects of alternative sales or production policies

are easily accepted, appreciated and assessed with help of marginal costing to ensure that

decisions taken will yield the maximum return to business.

Disadvantages:

1. Classifying Costs: Since all costs are variable in a long run, it becomes hard to

separate fixed and variable costs clearly. Such classifications may give misleading

results.

2. Recovery of Overheads: There is often the problem of under or over recovery of

overheads as variable costs are implemented on the basis of estimation not on actual

value.

TASK 3

P.4 Explaining advantages and disadvantages of different types of planning tool

Following are some types of planning tools which are used by Tesco in budgetary

control: Zero Based Budgeting- ZBB: All the expenses for each new period must be justified in

this method. This process starts with zero base and every function is analysed according

to its cost and needs within an organization (Zimmerman and Yahya-Zadeh, 2011). It

allows top level strategic goals to implement into the budgeting process.

Advantages:

1. It provides a systematic way to evaluate operations and programmes of activity to the

organization.

2. It allows management to allocate resources according to the priority of programme.

3. It enables departmental budgets to be proved on the basis of cost benefit comparison.

(Zero Base Budgeting: Advantages and Limitations, 2018)

Disadvantages:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.