Management Accounting Report: Tesco's Financial Strategies

VerifiedAdded on 2020/12/09

|16

|3509

|245

Report

AI Summary

This report provides a comprehensive analysis of management accounting within Tesco, a multinational supermarket retailer. It delves into the core principles of management accounting, its role in decision-making, and the application of various tools and techniques. The report examines planning tools like cash flow statements, CVP analysis, and cash forecasting budgets, evaluating their advantages and disadvantages. Furthermore, it explores how Tesco responds to financial problems through inventory management, pricing strategies, and cash flow forecasting. Financial statement analysis, including profitability ratios, is used to assess Tesco's financial performance and provide insights into its effectiveness in addressing financial challenges. The report highlights the importance of management accounting in formulating strategies to enhance productivity, profitability, and stability within the organization.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO1 and LO2...................................................................................................................................1

LO3 and LO4...................................................................................................................................1

SCENARIO 2: PART A..................................................................................................................1

Evaluation of different planning tools.........................................................................................1

PART B............................................................................................................................................4

Comparing how organisation is responding towards financial problems...................................4

Financial statements analysis .....................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

LO1 and LO2...................................................................................................................................1

LO3 and LO4...................................................................................................................................1

SCENARIO 2: PART A..................................................................................................................1

Evaluation of different planning tools.........................................................................................1

PART B............................................................................................................................................4

Comparing how organisation is responding towards financial problems...................................4

Financial statements analysis .....................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Management accounting is the process of presenting the financial data into useful information

which helps the managers in their decision making procedure. It involves a detailed analysis of

cost related and finance related data of an organization for drawing a meaningful information

that could used by management in formulating rationale decisions regarding policies and

strategies for enhancing their productivity, profitability and stability. The management

accountant prepares a comprehensive reports meant for the internal purpose in which complete

analysis of entire organization is provided related to the costs, expenses and it also highlights the

responsibility centres which are over consuming the company's resources in relation to their

productivity.

The present project report is going to cover the management accounting in Tesco, a

multinational supermarket retailer based in the United Kingdom . It mainly deals in groceries and

general merchandise. The company is headquartered in Welwyn Garden City, UK. It is a public

limited company and is listed on the London Stock Exchange and FTSE 100 component. The

study is going to highlight an explanation of management accounting, its role and its principles.

It will also cover different management accounting system and their roles along with the tools

and techniques of management accounting for presenting calculation from income statement and

balance sheet. Further, it will show the benefits of integrated management accounting system in

Tesco. The other segment of report will cover different planning tools used in management

accounting that could effectively be used for facing the financial problems in the organization.

LO1 and LO2

Covered in PPT.

LO3 and LO4

SCENARIO 2: PART A

Evaluation of different planning tools

Management accounting is is used for the internal purpose of organisation. It includes the

management accounts which are used for making decision in organisation. Planning tools are

those which are used for improving the performance of organisation by making the various

statements and budgets. The planning tools are used to provide understanding to the organisation

about the variation in the budgeted figures and actual to improve the performance accordingly.

1

Management accounting is the process of presenting the financial data into useful information

which helps the managers in their decision making procedure. It involves a detailed analysis of

cost related and finance related data of an organization for drawing a meaningful information

that could used by management in formulating rationale decisions regarding policies and

strategies for enhancing their productivity, profitability and stability. The management

accountant prepares a comprehensive reports meant for the internal purpose in which complete

analysis of entire organization is provided related to the costs, expenses and it also highlights the

responsibility centres which are over consuming the company's resources in relation to their

productivity.

The present project report is going to cover the management accounting in Tesco, a

multinational supermarket retailer based in the United Kingdom . It mainly deals in groceries and

general merchandise. The company is headquartered in Welwyn Garden City, UK. It is a public

limited company and is listed on the London Stock Exchange and FTSE 100 component. The

study is going to highlight an explanation of management accounting, its role and its principles.

It will also cover different management accounting system and their roles along with the tools

and techniques of management accounting for presenting calculation from income statement and

balance sheet. Further, it will show the benefits of integrated management accounting system in

Tesco. The other segment of report will cover different planning tools used in management

accounting that could effectively be used for facing the financial problems in the organization.

LO1 and LO2

Covered in PPT.

LO3 and LO4

SCENARIO 2: PART A

Evaluation of different planning tools

Management accounting is is used for the internal purpose of organisation. It includes the

management accounts which are used for making decision in organisation. Planning tools are

those which are used for improving the performance of organisation by making the various

statements and budgets. The planning tools are used to provide understanding to the organisation

about the variation in the budgeted figures and actual to improve the performance accordingly.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash flow statement

The cash flow statement provides clarity regarding the inflows and outflows of cash in

effectual manner for a particular time period. The cash flow statement is useful as it helps

company to plan its income and expenses to be incurred in a better manner. The cash flow

statement is quite useful for business as it provides with inflows and outflows in effective

manner.

Advantages

It is helpful as it helps to make cash forecast and cash position is planned by the

company's management in a better manner.

The internal management is benefited as company will be able to make financial policy to

be adopted in future as it applies all information to funds (Lean, Ang and Smyth, 2015).

The cash position is effectively revealed with the help of cash flow statement. It helps to

see whether there is increase or decrease in cash. This helps management to plan out

things (Cash Flow Statement: Features, Importance and Advantages, 2017).

Disadvantages

Major disadvantage of cash flow statement is that only movement of cash flow can be

ascertained. However, it does not provide reason behind change in cash position.

The cash flow statement only records items which either decreases cash or increase the

same (Lean, Ang and Smyth, 2015). It ignores all other items which are important to be

noted for analysing financial position.

It is made only at the end of accounting period and as a result, major items which are

changed in between year are not accounted for (Ioannou and Serafeim, 2015).

CVP Analysis

CVP (Cost Volume Profit) analysis is one of the important technique and planning tool as

it provides clarity regarding volume of production required by company to accomplish breakeven

point (Alawattage and Wickramasinghe, 2018). The costs and volume and profit are analysed

which provides whether company may be able to attain break even sales or not. By meeting

breakeven point, company makes no profit no loss. Hence, above breakeven point, profits start to

float in.

Advantages

2

The cash flow statement provides clarity regarding the inflows and outflows of cash in

effectual manner for a particular time period. The cash flow statement is useful as it helps

company to plan its income and expenses to be incurred in a better manner. The cash flow

statement is quite useful for business as it provides with inflows and outflows in effective

manner.

Advantages

It is helpful as it helps to make cash forecast and cash position is planned by the

company's management in a better manner.

The internal management is benefited as company will be able to make financial policy to

be adopted in future as it applies all information to funds (Lean, Ang and Smyth, 2015).

The cash position is effectively revealed with the help of cash flow statement. It helps to

see whether there is increase or decrease in cash. This helps management to plan out

things (Cash Flow Statement: Features, Importance and Advantages, 2017).

Disadvantages

Major disadvantage of cash flow statement is that only movement of cash flow can be

ascertained. However, it does not provide reason behind change in cash position.

The cash flow statement only records items which either decreases cash or increase the

same (Lean, Ang and Smyth, 2015). It ignores all other items which are important to be

noted for analysing financial position.

It is made only at the end of accounting period and as a result, major items which are

changed in between year are not accounted for (Ioannou and Serafeim, 2015).

CVP Analysis

CVP (Cost Volume Profit) analysis is one of the important technique and planning tool as

it provides clarity regarding volume of production required by company to accomplish breakeven

point (Alawattage and Wickramasinghe, 2018). The costs and volume and profit are analysed

which provides whether company may be able to attain break even sales or not. By meeting

breakeven point, company makes no profit no loss. Hence, above breakeven point, profits start to

float in.

Advantages

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It helps to analyse as to which products are beneficial and how organisation can be

effectively use the same for meeting out maximum amount of revenue.

It also provides what sales volume will be needed by company for accomplishing fixed

level of profits in the best manner possible (Ioannou and Serafeim, 2015).

It also effectively helps for calculating fixed and variable for measuring risk associated

with investment in effectual manner.

Disadvantages

It is assumed that total sales and total costs are tended to be linear and can be represented

by straight lines (Agarwal. 2018). However, in event of firm selling more units, variable

costs per unit decreases for operating more efficiencies in production.

It is performed within stipulated range of operating activity and assumes that productivity

and efficiencies are constant. However, it is not valid.

Another assumption is that costs can be divided into fixed and variable costs which are at

times seems to be invalid.

Cash forecasting budget

The cash forecasting budget is quite useful for business as it provides forecast regarding

cash receipts and cash payments for upcoming period. It is quite useful for business as it

provides forecast of future cash inflows and outflows (Hayes and Newell, 2011). Thus, by

forecasting the cash outflows and inflows, firm is able to make proper assumptions regarding the

same.

Advantages

The main advantage of cash forecasting budget is that resources of organisation can be

effectively planned and full utilisation may be possible.

It helps to identify potential deficits in the system and as a result, quick determination of

cash obligations may be assessed in a better manner (ANAECHE and ALIO, 2018).

The financial position can be determined in comfortable manner as it becomes much

easier for ascertaining future cash flow position of firm by looking at present financials.

Disadvantages

The main demerit of cash forecasting budget as a planning tool is that management

makes estimate regarding budget and real facts does not prevail (Mclntosh. 2017). Hence,

use of estimates is not fruitful.

3

effectively use the same for meeting out maximum amount of revenue.

It also provides what sales volume will be needed by company for accomplishing fixed

level of profits in the best manner possible (Ioannou and Serafeim, 2015).

It also effectively helps for calculating fixed and variable for measuring risk associated

with investment in effectual manner.

Disadvantages

It is assumed that total sales and total costs are tended to be linear and can be represented

by straight lines (Agarwal. 2018). However, in event of firm selling more units, variable

costs per unit decreases for operating more efficiencies in production.

It is performed within stipulated range of operating activity and assumes that productivity

and efficiencies are constant. However, it is not valid.

Another assumption is that costs can be divided into fixed and variable costs which are at

times seems to be invalid.

Cash forecasting budget

The cash forecasting budget is quite useful for business as it provides forecast regarding

cash receipts and cash payments for upcoming period. It is quite useful for business as it

provides forecast of future cash inflows and outflows (Hayes and Newell, 2011). Thus, by

forecasting the cash outflows and inflows, firm is able to make proper assumptions regarding the

same.

Advantages

The main advantage of cash forecasting budget is that resources of organisation can be

effectively planned and full utilisation may be possible.

It helps to identify potential deficits in the system and as a result, quick determination of

cash obligations may be assessed in a better manner (ANAECHE and ALIO, 2018).

The financial position can be determined in comfortable manner as it becomes much

easier for ascertaining future cash flow position of firm by looking at present financials.

Disadvantages

The main demerit of cash forecasting budget as a planning tool is that management

makes estimate regarding budget and real facts does not prevail (Mclntosh. 2017). Hence,

use of estimates is not fruitful.

3

The flexibility issue consists in cash forecasting budget. This is because when budget is

submitted having published with budget numbers, it is submitted to management (Gomes,

Carnegie and Rodrigues, 2014).

Manipulation can take place as there may be underestimate of cash budget regarding

expenses. However, disbursements are too low and as a result, variance exists.

PART B

Comparing how organisation is responding towards financial problems

Every business has its ups and downs , faces the time of profitability and financial crisis.

It is only those organisations which makes reserves for the future contingencies and plan

accordingly their operations, survives. Various kinds of financial problems such as declining

sales, excessive cash outflow, unnecessary wastage in the production processes etc. Tools and

techniques of management accounting plays a crucial role in dealing with the financial problems

in the business in the following ways :

Inventory management accounting system : It is a process of keeping a track of

company's stock for facilitating smooth flow in the production process. It helps the managers in

managing the inventory in such a way that reduces the overall cost of handling and carrying the

raw materials and other components of inventory. There are different ways of inventory

management such as :

Just in time

ABC Inventory management

Contingencies theory

Pricing system : Pricing of the products and services plays a great role in the success of

the company. There are different pricing strategies which could help the company in dealing

with its financial crisis :

Price skimming : It is strategy wherein the company sets a higher price at the initial stage

and then lowers it down as the time passes.

Premium pricing : It is often called as prestige pricing wherein the company sets the

prices of its product relatively higher than the market price for satisfying the esteem of

the buyers who prefers products which enhances their social status.

Cash Flow Forecasting budget :

4

submitted having published with budget numbers, it is submitted to management (Gomes,

Carnegie and Rodrigues, 2014).

Manipulation can take place as there may be underestimate of cash budget regarding

expenses. However, disbursements are too low and as a result, variance exists.

PART B

Comparing how organisation is responding towards financial problems

Every business has its ups and downs , faces the time of profitability and financial crisis.

It is only those organisations which makes reserves for the future contingencies and plan

accordingly their operations, survives. Various kinds of financial problems such as declining

sales, excessive cash outflow, unnecessary wastage in the production processes etc. Tools and

techniques of management accounting plays a crucial role in dealing with the financial problems

in the business in the following ways :

Inventory management accounting system : It is a process of keeping a track of

company's stock for facilitating smooth flow in the production process. It helps the managers in

managing the inventory in such a way that reduces the overall cost of handling and carrying the

raw materials and other components of inventory. There are different ways of inventory

management such as :

Just in time

ABC Inventory management

Contingencies theory

Pricing system : Pricing of the products and services plays a great role in the success of

the company. There are different pricing strategies which could help the company in dealing

with its financial crisis :

Price skimming : It is strategy wherein the company sets a higher price at the initial stage

and then lowers it down as the time passes.

Premium pricing : It is often called as prestige pricing wherein the company sets the

prices of its product relatively higher than the market price for satisfying the esteem of

the buyers who prefers products which enhances their social status.

Cash Flow Forecasting budget :

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is a procedure which is concerned with the prediction of inflow and outflow of cash

from the business. The objective behind forecasting cash is to obtain a balance of cash reserve

which depicts neither insufficient cash nor too much ideal cash in the business. This is because

ideal cash is just the like a liability for the company as no income is generating from such cash

while inadequate funds creates a problem of meeting short term liabilities and contingent

liabilities of the business. If facilitates the manager of the company in planning regarding how

much cash and liquidity they require for the next 12 months. Forecasting of the cash also aids the

managers in maintaining the solvency which is needed for surviving peacefully in the market

(Cash Budgeting, Forecasting Cash Flow and Account Analysis , 2019).

If any financial crisis arises, cash budget provides a guideline and framework regarding

the expenditure. This acts as a controlling tool through with company is able to reduce and

control its operational costs and which ultimately helps in dealing with financial problems in the

business.

In the context of business unit, monetary problems are recognized as an essential part with

which every manager has to deal. Hence, there are several techniques which can be undertaken

by Tesco’s manager for dealing with financial problems or issues. Such techniques mainly

include benchmarking, key performance indicator (KPI), variance analysis, financial governance,

balance scorecard etc.

Benchmarking

On the basis of such technique by setting benchmarks with regards to monetary aspects

such as sale, profit etc company can evaluate monetary performance. It offers opportunity to the

firm in relation to the identification of deficiencies take place in departmental performance.

Key performance indicator (KPI)

By setting KPI’s in relation to sales, profit, market share etc company can make

evaluation of its performance and thereby would become able to assess areas where

improvement needed.

Variance analysis

In accordance with this technique, by doing comparison of actual output or figures in

against to the standards business unit can identify variance. This technique lays emphasis on

determining causes due to which deviations are occurred. Accordingly, by taking corrective

5

from the business. The objective behind forecasting cash is to obtain a balance of cash reserve

which depicts neither insufficient cash nor too much ideal cash in the business. This is because

ideal cash is just the like a liability for the company as no income is generating from such cash

while inadequate funds creates a problem of meeting short term liabilities and contingent

liabilities of the business. If facilitates the manager of the company in planning regarding how

much cash and liquidity they require for the next 12 months. Forecasting of the cash also aids the

managers in maintaining the solvency which is needed for surviving peacefully in the market

(Cash Budgeting, Forecasting Cash Flow and Account Analysis , 2019).

If any financial crisis arises, cash budget provides a guideline and framework regarding

the expenditure. This acts as a controlling tool through with company is able to reduce and

control its operational costs and which ultimately helps in dealing with financial problems in the

business.

In the context of business unit, monetary problems are recognized as an essential part with

which every manager has to deal. Hence, there are several techniques which can be undertaken

by Tesco’s manager for dealing with financial problems or issues. Such techniques mainly

include benchmarking, key performance indicator (KPI), variance analysis, financial governance,

balance scorecard etc.

Benchmarking

On the basis of such technique by setting benchmarks with regards to monetary aspects

such as sale, profit etc company can evaluate monetary performance. It offers opportunity to the

firm in relation to the identification of deficiencies take place in departmental performance.

Key performance indicator (KPI)

By setting KPI’s in relation to sales, profit, market share etc company can make

evaluation of its performance and thereby would become able to assess areas where

improvement needed.

Variance analysis

In accordance with this technique, by doing comparison of actual output or figures in

against to the standards business unit can identify variance. This technique lays emphasis on

determining causes due to which deviations are occurred. Accordingly, by taking corrective

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

measures for improvement within the4 suitable time period firm can respond monetary problems

effectually.

Balance scorecard

This tool of management accounting assists in measuring performance from both

financial and non-financial perspectives. Such aspects mainly include learning & growth,

business processes, customer perspectives and financial data set. Hence, by evaluating

performance in against to such elements need pertaining to improvement can be identified.

By doing assessment, it has identified that Tesco undertakes KPI’s with the motive to

evaluate current performance. This in turn helps company in assessing the extent to which goals

are met. Thus, by comparing performance in against to KPI’s firm can take significant action for

future growth or improvement. On the other side, leading hospitality firm namely Hilton focuses

on undertaking variance analysis to deal with monetary problems. As, it gives clear indication

regarding the aspects due to which firm failed to meet predetermined goals. However, on the

critical note, if business unit fails to set appropriate standards then it may result into

inappropriate framework for decision making. Thus, it can be stated that technique undertaken

by Tesco for meeting financial problem is highly effectual over others.

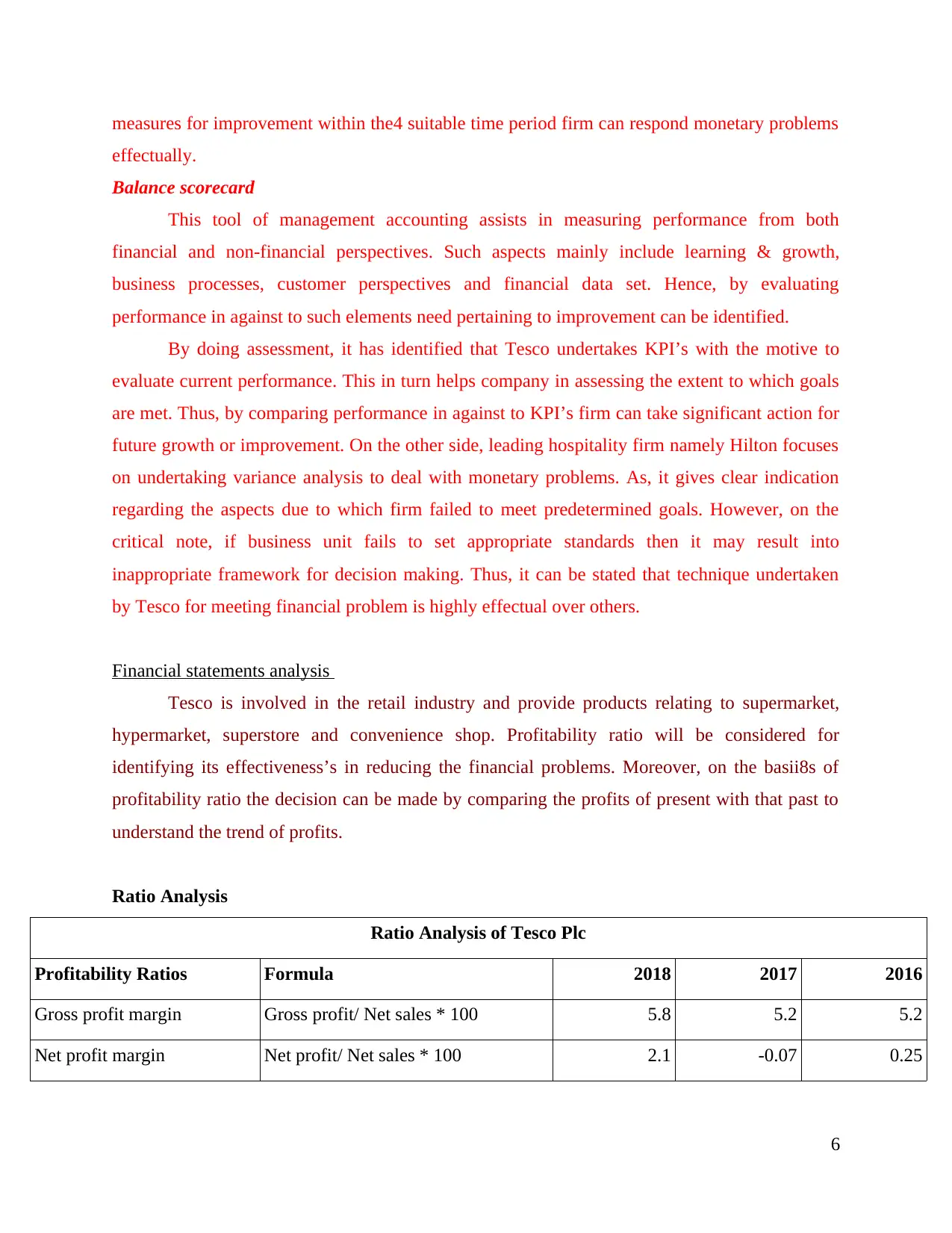

Financial statements analysis

Tesco is involved in the retail industry and provide products relating to supermarket,

hypermarket, superstore and convenience shop. Profitability ratio will be considered for

identifying its effectiveness’s in reducing the financial problems. Moreover, on the basii8s of

profitability ratio the decision can be made by comparing the profits of present with that past to

understand the trend of profits.

Ratio Analysis

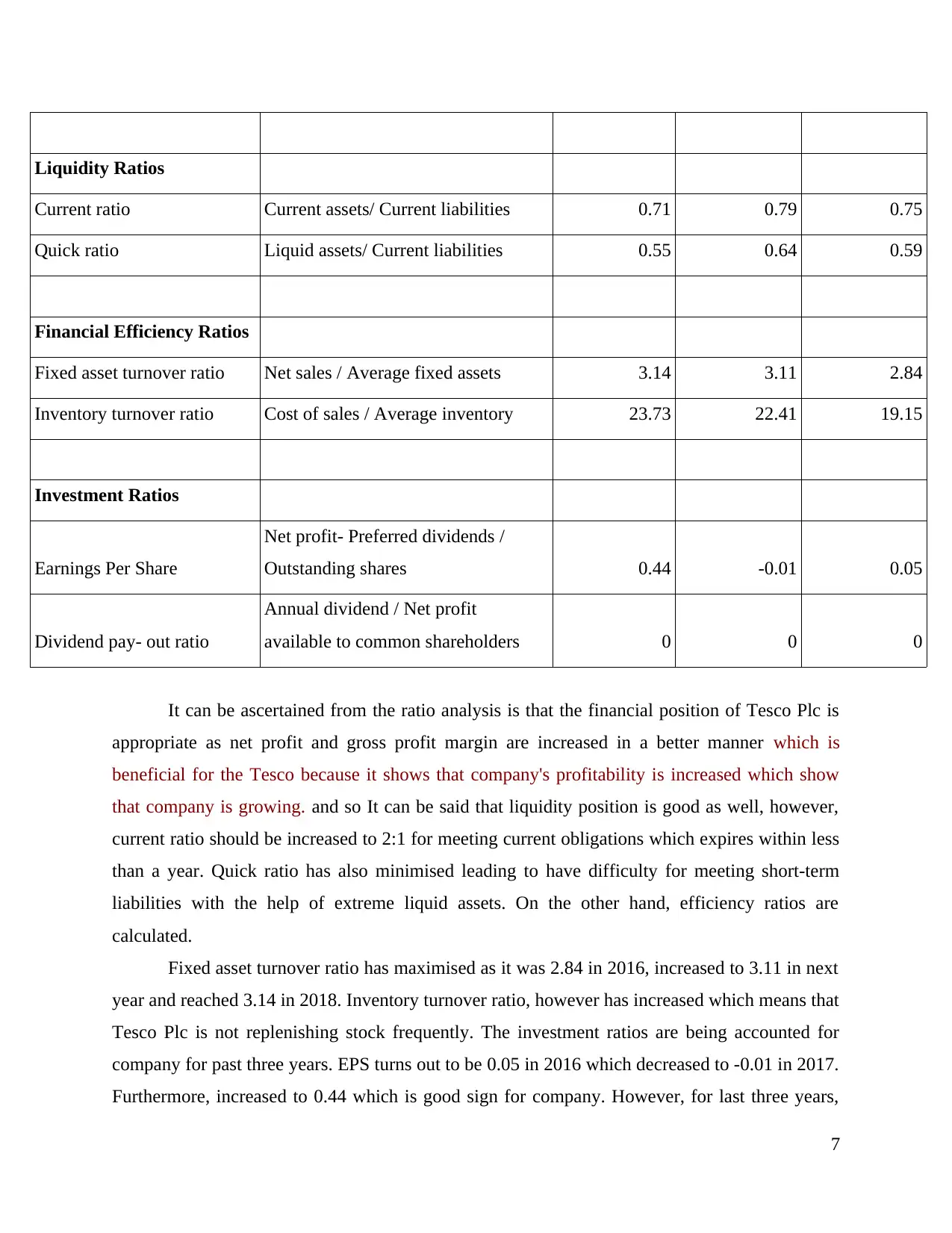

Ratio Analysis of Tesco Plc

Profitability Ratios Formula 2018 2017 2016

Gross profit margin Gross profit/ Net sales * 100 5.8 5.2 5.2

Net profit margin Net profit/ Net sales * 100 2.1 -0.07 0.25

6

effectually.

Balance scorecard

This tool of management accounting assists in measuring performance from both

financial and non-financial perspectives. Such aspects mainly include learning & growth,

business processes, customer perspectives and financial data set. Hence, by evaluating

performance in against to such elements need pertaining to improvement can be identified.

By doing assessment, it has identified that Tesco undertakes KPI’s with the motive to

evaluate current performance. This in turn helps company in assessing the extent to which goals

are met. Thus, by comparing performance in against to KPI’s firm can take significant action for

future growth or improvement. On the other side, leading hospitality firm namely Hilton focuses

on undertaking variance analysis to deal with monetary problems. As, it gives clear indication

regarding the aspects due to which firm failed to meet predetermined goals. However, on the

critical note, if business unit fails to set appropriate standards then it may result into

inappropriate framework for decision making. Thus, it can be stated that technique undertaken

by Tesco for meeting financial problem is highly effectual over others.

Financial statements analysis

Tesco is involved in the retail industry and provide products relating to supermarket,

hypermarket, superstore and convenience shop. Profitability ratio will be considered for

identifying its effectiveness’s in reducing the financial problems. Moreover, on the basii8s of

profitability ratio the decision can be made by comparing the profits of present with that past to

understand the trend of profits.

Ratio Analysis

Ratio Analysis of Tesco Plc

Profitability Ratios Formula 2018 2017 2016

Gross profit margin Gross profit/ Net sales * 100 5.8 5.2 5.2

Net profit margin Net profit/ Net sales * 100 2.1 -0.07 0.25

6

Liquidity Ratios

Current ratio Current assets/ Current liabilities 0.71 0.79 0.75

Quick ratio Liquid assets/ Current liabilities 0.55 0.64 0.59

Financial Efficiency Ratios

Fixed asset turnover ratio Net sales / Average fixed assets 3.14 3.11 2.84

Inventory turnover ratio Cost of sales / Average inventory 23.73 22.41 19.15

Investment Ratios

Earnings Per Share

Net profit- Preferred dividends /

Outstanding shares 0.44 -0.01 0.05

Dividend pay- out ratio

Annual dividend / Net profit

available to common shareholders 0 0 0

It can be ascertained from the ratio analysis is that the financial position of Tesco Plc is

appropriate as net profit and gross profit margin are increased in a better manner which is

beneficial for the Tesco because it shows that company's profitability is increased which show

that company is growing. and so It can be said that liquidity position is good as well, however,

current ratio should be increased to 2:1 for meeting current obligations which expires within less

than a year. Quick ratio has also minimised leading to have difficulty for meeting short-term

liabilities with the help of extreme liquid assets. On the other hand, efficiency ratios are

calculated.

Fixed asset turnover ratio has maximised as it was 2.84 in 2016, increased to 3.11 in next

year and reached 3.14 in 2018. Inventory turnover ratio, however has increased which means that

Tesco Plc is not replenishing stock frequently. The investment ratios are being accounted for

company for past three years. EPS turns out to be 0.05 in 2016 which decreased to -0.01 in 2017.

Furthermore, increased to 0.44 which is good sign for company. However, for last three years,

7

Current ratio Current assets/ Current liabilities 0.71 0.79 0.75

Quick ratio Liquid assets/ Current liabilities 0.55 0.64 0.59

Financial Efficiency Ratios

Fixed asset turnover ratio Net sales / Average fixed assets 3.14 3.11 2.84

Inventory turnover ratio Cost of sales / Average inventory 23.73 22.41 19.15

Investment Ratios

Earnings Per Share

Net profit- Preferred dividends /

Outstanding shares 0.44 -0.01 0.05

Dividend pay- out ratio

Annual dividend / Net profit

available to common shareholders 0 0 0

It can be ascertained from the ratio analysis is that the financial position of Tesco Plc is

appropriate as net profit and gross profit margin are increased in a better manner which is

beneficial for the Tesco because it shows that company's profitability is increased which show

that company is growing. and so It can be said that liquidity position is good as well, however,

current ratio should be increased to 2:1 for meeting current obligations which expires within less

than a year. Quick ratio has also minimised leading to have difficulty for meeting short-term

liabilities with the help of extreme liquid assets. On the other hand, efficiency ratios are

calculated.

Fixed asset turnover ratio has maximised as it was 2.84 in 2016, increased to 3.11 in next

year and reached 3.14 in 2018. Inventory turnover ratio, however has increased which means that

Tesco Plc is not replenishing stock frequently. The investment ratios are being accounted for

company for past three years. EPS turns out to be 0.05 in 2016 which decreased to -0.01 in 2017.

Furthermore, increased to 0.44 which is good sign for company. However, for last three years,

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

dividend payout ratio has not been paid highlighting that shareholders are not provided return on

their investments in form of dividend.

CONCLUSION

From the above project report, it can be summarised that management accounting is one

of the most important tool for the management of TESCO while making decisions for the

company. The study covered different management accounting system such as cost accounting

system, price optimization, job costing and inventory management accounting system. Cost

management accounting system is concerned with proper allocation of costs of each activity of

business organization to the relevant department. Such optimum allocation of costs to the

relevant overheads helps the managers in finding out the productivity and profitability of each

operating department in the company. By this way, strategies and decisions are taken regarding

to fund allocation like the responsibility centre that is highly profitable are granted with more

resources as compared to less productive responsibility centre.

Further, the report concluded that proper integration of the different management

accounting systems helps the company in managing its resources every effectively through

which operational costs could be controlled. It ultimately helps it in achieving its organisational

objective of being cost effective firm in the market. Different planning tools such as budgets,

zero based budgeting etc., helps the organisation in creating a spending or expenditure plan

based on the previous trends and current market trends. This plan guides expenditure actions of

the different departments in the entity. Budgetary control tools are crucial to the firm because it

helps it in controlling its cost. Expenses set are compared against the actual ones and variances

are identified which later are analysed. This analysis helps the management in forming more cost

effective policies and strategies for the company that assist it dealing with the various financial

problems such as lack of funds for conducting routine operations or loss making phase of

company. Thus, management accounting helps TESCO in maintaining its stability and

profitability in the global market.

8

their investments in form of dividend.

CONCLUSION

From the above project report, it can be summarised that management accounting is one

of the most important tool for the management of TESCO while making decisions for the

company. The study covered different management accounting system such as cost accounting

system, price optimization, job costing and inventory management accounting system. Cost

management accounting system is concerned with proper allocation of costs of each activity of

business organization to the relevant department. Such optimum allocation of costs to the

relevant overheads helps the managers in finding out the productivity and profitability of each

operating department in the company. By this way, strategies and decisions are taken regarding

to fund allocation like the responsibility centre that is highly profitable are granted with more

resources as compared to less productive responsibility centre.

Further, the report concluded that proper integration of the different management

accounting systems helps the company in managing its resources every effectively through

which operational costs could be controlled. It ultimately helps it in achieving its organisational

objective of being cost effective firm in the market. Different planning tools such as budgets,

zero based budgeting etc., helps the organisation in creating a spending or expenditure plan

based on the previous trends and current market trends. This plan guides expenditure actions of

the different departments in the entity. Budgetary control tools are crucial to the firm because it

helps it in controlling its cost. Expenses set are compared against the actual ones and variances

are identified which later are analysed. This analysis helps the management in forming more cost

effective policies and strategies for the company that assist it dealing with the various financial

problems such as lack of funds for conducting routine operations or loss making phase of

company. Thus, management accounting helps TESCO in maintaining its stability and

profitability in the global market.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Alawattage, C. and Wickramasinghe, D., 2018. Strategizing Management Accounting: Liberal

Origins and Neoliberal Trends. Routledge.

ANAECHE, K. and ALIO, B., 2018. REDUCING UNEMPLOYMENT AND POVERTY

LEVEL THROUGH MATHEMATICS EDUCATION IN NIGERIA. Journal of Science

and Computer Education. 2(1). pp.309-321.

Bedford, D. S. and Speklé, R. F., 2018. Construct validity in survey-based management

accounting and control research. Journal of Management Accounting Research. 30(2).

pp.23-58.

Booth, P., 2018. Management control in a voluntary organization: accounting and accountants

in organizational context. Routledge.

Gomes, D., Carnegie, G. D. and Rodrigues, L. L., 2014. Accounting as a technology of

government in the Portuguese empire: The development, application and enforcement of

accounting rules during the Pombaline era (1761–1777). European Accounting

Review. 23(1). pp.87-115.

Hayes, B. K. and Newell, B. R., 2011. The uncertain status of Bayesian accounts of

reasoning. Behavioral and Brain Sciences. 34(4). pp.201-202.

Horton, K. E. and de Araujo Wanderley, C., 2018. Identity conflict and the paradox of embedded

agency in the management accounting profession: adding a new piece to the theoretical

jigsaw. Management Accounting Research. 38. pp.39-50.

Ioannou, I. and Serafeim, G. 2015. The impact of corporate social responsibility on investment

recommendations: Analysts' perceptions and shifting institutional logics. Strategic

Management Journal. 36(7). 1053-1081.

Latan, H. and et.al., 2018. Effects of environmental strategy, environmental uncertainty and top

management's commitment on corporate environmental performance: The role of

environmental management accounting. Journal of cleaner production. 180. pp.297-306.

Lean, H. H., Ang, W. R. and Smyth, R. 2015. Performance and performance persistence of

socially responsible investment funds in Europe and North America. The North American

Journal of Economics and Finance. 34. 254-266.

Malina, M. A. ed., 2018. Advances in management accounting. Emerald Publishing Limited.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Online

Mclntosh. 2017 The Disadvantages of a Cash Budget. [Online]. Available Through:

<https://bizfluent.com/info-7762104-disadvantages-cash-budget.html>.

9

Books and Journals

Alawattage, C. and Wickramasinghe, D., 2018. Strategizing Management Accounting: Liberal

Origins and Neoliberal Trends. Routledge.

ANAECHE, K. and ALIO, B., 2018. REDUCING UNEMPLOYMENT AND POVERTY

LEVEL THROUGH MATHEMATICS EDUCATION IN NIGERIA. Journal of Science

and Computer Education. 2(1). pp.309-321.

Bedford, D. S. and Speklé, R. F., 2018. Construct validity in survey-based management

accounting and control research. Journal of Management Accounting Research. 30(2).

pp.23-58.

Booth, P., 2018. Management control in a voluntary organization: accounting and accountants

in organizational context. Routledge.

Gomes, D., Carnegie, G. D. and Rodrigues, L. L., 2014. Accounting as a technology of

government in the Portuguese empire: The development, application and enforcement of

accounting rules during the Pombaline era (1761–1777). European Accounting

Review. 23(1). pp.87-115.

Hayes, B. K. and Newell, B. R., 2011. The uncertain status of Bayesian accounts of

reasoning. Behavioral and Brain Sciences. 34(4). pp.201-202.

Horton, K. E. and de Araujo Wanderley, C., 2018. Identity conflict and the paradox of embedded

agency in the management accounting profession: adding a new piece to the theoretical

jigsaw. Management Accounting Research. 38. pp.39-50.

Ioannou, I. and Serafeim, G. 2015. The impact of corporate social responsibility on investment

recommendations: Analysts' perceptions and shifting institutional logics. Strategic

Management Journal. 36(7). 1053-1081.

Latan, H. and et.al., 2018. Effects of environmental strategy, environmental uncertainty and top

management's commitment on corporate environmental performance: The role of

environmental management accounting. Journal of cleaner production. 180. pp.297-306.

Lean, H. H., Ang, W. R. and Smyth, R. 2015. Performance and performance persistence of

socially responsible investment funds in Europe and North America. The North American

Journal of Economics and Finance. 34. 254-266.

Malina, M. A. ed., 2018. Advances in management accounting. Emerald Publishing Limited.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Online

Mclntosh. 2017 The Disadvantages of a Cash Budget. [Online]. Available Through:

<https://bizfluent.com/info-7762104-disadvantages-cash-budget.html>.

9

Agarwal. 2018 Cost-Volume Profit (CVP): Definition and Limitations [Online]. Available

Through: <http://www.yourarticlelibrary.com/accounting/costing/cost-volume-profit-cvp-

definition-and-limitations/52670>.

Cash Flow Statement: Features, Importance and Advantages. 2017.[Online]. Available

through :<http://www.yourarticlelibrary.com/accounting/cash-flow/cash-flow-statement-

features-importance-and-advantages/59517>

10

Through: <http://www.yourarticlelibrary.com/accounting/costing/cost-volume-profit-cvp-

definition-and-limitations/52670>.

Cash Flow Statement: Features, Importance and Advantages. 2017.[Online]. Available

through :<http://www.yourarticlelibrary.com/accounting/cash-flow/cash-flow-statement-

features-importance-and-advantages/59517>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.