Financial Analysis Report: Comparing Tesco and M&S Plc Performance

VerifiedAdded on 2020/07/22

|9

|1328

|38

Report

AI Summary

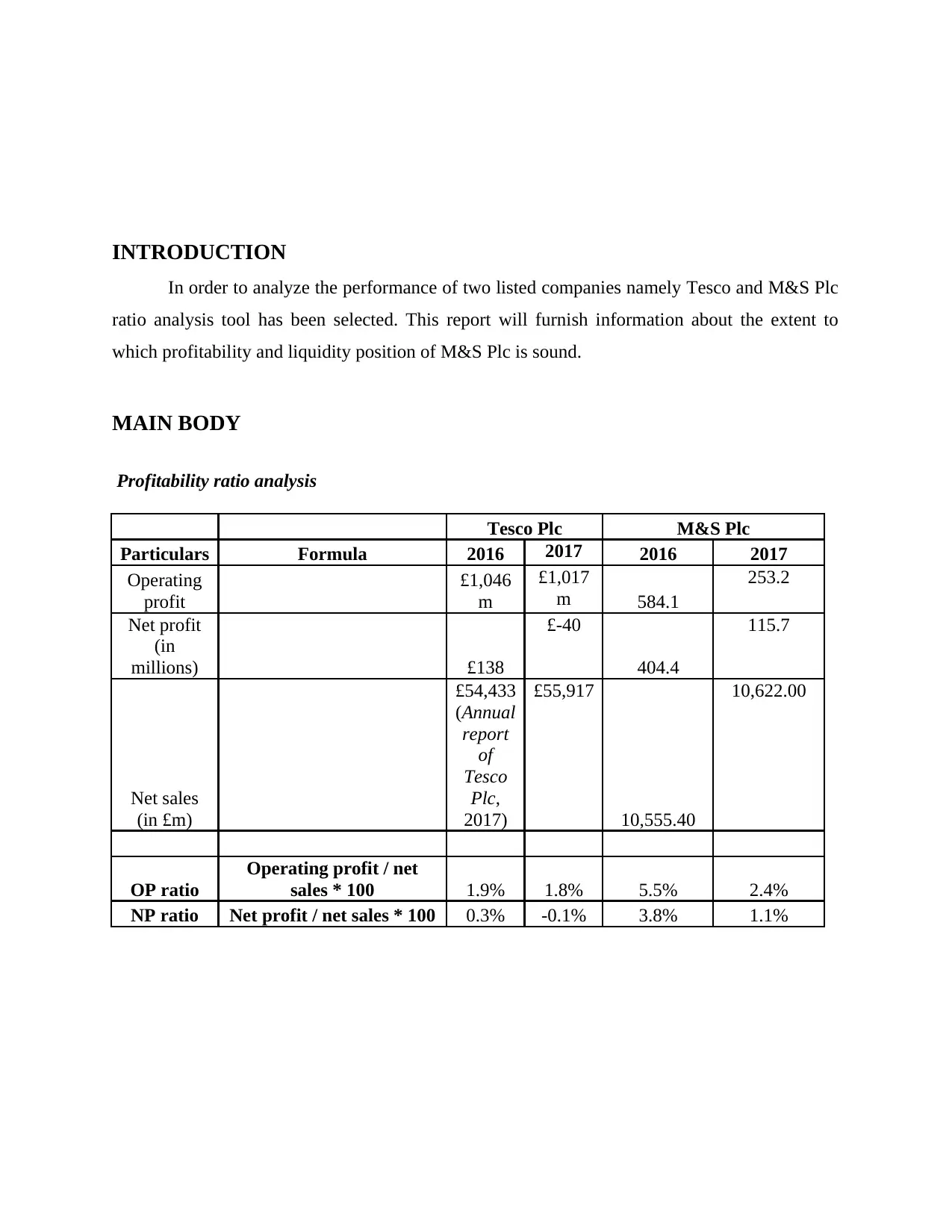

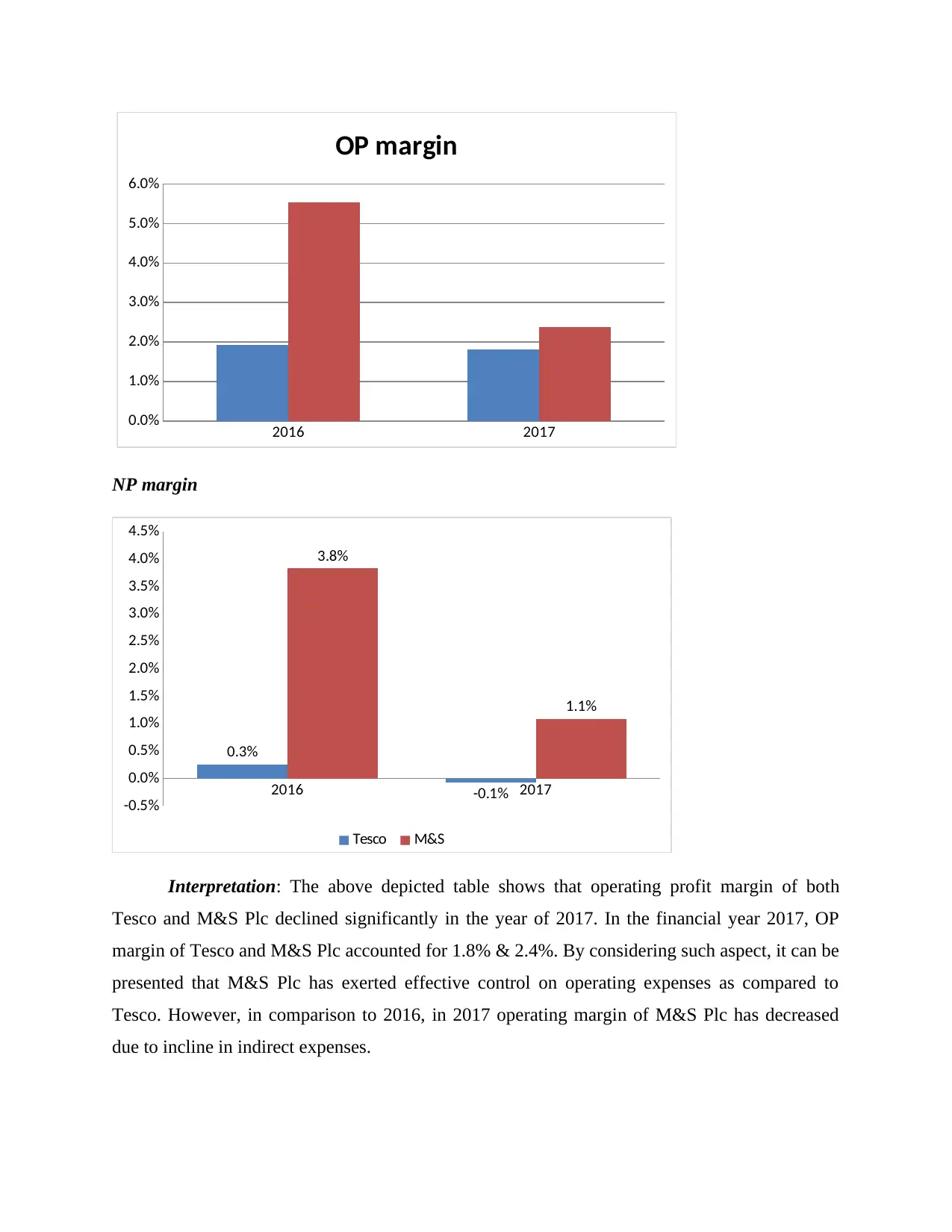

This report provides a detailed financial analysis of Tesco and M&S Plc, two prominent UK companies, using ratio analysis to assess their performance. The analysis covers profitability, liquidity, and working capital ratios for the years 2016 and 2017, comparing the two companies across various metrics. Key ratios such as operating profit margin, net profit margin, current ratio, quick ratio, inventory turnover, and debtor/creditor settlement periods are examined. The report interprets the financial data, highlighting the strengths and weaknesses of each company, and discusses the limitations of ratio analysis. The conclusion states that M&S Plc had a better profitability and liquidity position compared to Tesco Plc. The report also offers recommendations for both companies, such as employing budgeting and budgetary control, and strategic planning for maintaining current assets. Finally, the report includes a list of references used for the analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.