BABS - Tesco PLC's Financial Reports: Meeting External User Needs

VerifiedAdded on 2023/06/13

|17

|3845

|183

Report

AI Summary

This report examines how Tesco PLC's financial information caters to its non-management external users, including potential investors, trade creditors, lenders, tax authorities, regulatory agencies, and customers. It details how these users leverage annual reports and financial statements to assess the company's financial health, creditworthiness, investment potential, and regulatory compliance. The report analyzes key financial ratios like gross margin, net margin, return on assets, return on equity, and current ratios, demonstrating how these metrics inform stakeholder decisions regarding investment, credit terms, and long-term business relationships. The study highlights the importance of transparent financial reporting in maintaining stakeholder confidence and facilitating informed decision-making.

The non-management External users of

the organisation and the financial

information

the organisation and the financial

information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction:....................................................................................................................................3

The description of the non-management external users..................................................................3

How the financial information is fulfilling the requirement of information of the non

management external users..............................................................................................................5

Conclusion.....................................................................................................................................13

Reference:......................................................................................................................................15

Appendix:......................................................................................................................................16

Latest financial ratios for Tesco PLC (2017-2008)...................................................................16

Introduction:....................................................................................................................................3

The description of the non-management external users..................................................................3

How the financial information is fulfilling the requirement of information of the non

management external users..............................................................................................................5

Conclusion.....................................................................................................................................13

Reference:......................................................................................................................................15

Appendix:......................................................................................................................................16

Latest financial ratios for Tesco PLC (2017-2008)...................................................................16

Introduction:

The chosen organisation Tesco PLC is the leader of the grocery retail super market of the UK

and holds around 28% share of the market .In every year the organisation release an annual

report that represents the major financial statements[income statement, balance sheet cash flow

statement] along with other financial reports[changes in share holder’s equity, fund flow

statement etc] of the organisation so that the external users of the organisation can gather

sufficient information regarding the financial performance as well as the financial position of the

organisation(Kantarworldpanel.com, 2018). The financial report that is used some of the major

non management are the investors, Trade creditors, Institutional as a well as private investors ,

Tax Authorities and Regulatory Agencies, Customers, Employees and the labour Unions. The

chosen organisation complies with the requirements of the International Accounting Standards

(IAS)and the United Kingdom Generally Accepted Accounting Practice[UKGAAP] and the

International Financial Reporting Standards(IFRS) regulated by the International Accounting

Standards Board (IASB)( Wood et al.,2016).

The description of the non-management external users

The major five non-management external users of the organisation that use the annual reports as

well as the finacial statements o f the organisation are as follows:

The potential new Investors are the most important external user of the financial reports of Tesco

PLC as they may not be the part of the management but they are very much interested in past

financial performance of the business or better to say the historical financial performance of the

business. This inference regarding the future will help the investors to regulate the investment

decisions with respect to the organisation in terms of duration of investment and the ,amount of

investment to be made so that maximum return can be generated. The investors study the

financial statements that are presented in the accounting reports released by the organisation for

the purpose of studying the summary of the performance of the different fund generating

activities of the organisation. This study will help the organisation to assess the efficiency of the

The chosen organisation Tesco PLC is the leader of the grocery retail super market of the UK

and holds around 28% share of the market .In every year the organisation release an annual

report that represents the major financial statements[income statement, balance sheet cash flow

statement] along with other financial reports[changes in share holder’s equity, fund flow

statement etc] of the organisation so that the external users of the organisation can gather

sufficient information regarding the financial performance as well as the financial position of the

organisation(Kantarworldpanel.com, 2018). The financial report that is used some of the major

non management are the investors, Trade creditors, Institutional as a well as private investors ,

Tax Authorities and Regulatory Agencies, Customers, Employees and the labour Unions. The

chosen organisation complies with the requirements of the International Accounting Standards

(IAS)and the United Kingdom Generally Accepted Accounting Practice[UKGAAP] and the

International Financial Reporting Standards(IFRS) regulated by the International Accounting

Standards Board (IASB)( Wood et al.,2016).

The description of the non-management external users

The major five non-management external users of the organisation that use the annual reports as

well as the finacial statements o f the organisation are as follows:

The potential new Investors are the most important external user of the financial reports of Tesco

PLC as they may not be the part of the management but they are very much interested in past

financial performance of the business or better to say the historical financial performance of the

business. This inference regarding the future will help the investors to regulate the investment

decisions with respect to the organisation in terms of duration of investment and the ,amount of

investment to be made so that maximum return can be generated. The investors study the

financial statements that are presented in the accounting reports released by the organisation for

the purpose of studying the summary of the performance of the different fund generating

activities of the organisation. This study will help the organisation to assess the efficiency of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

different revenue generating activities of the organisation. The existing investors on the other

hand study the financial report to decide where to hold the investment (which to a large extent

depends upon the financial position of the organisation) or it is better to withdraw the

investments made for the maximization of the returns(Booth and Hamer, 2009)

Trade Creditors or Suppliers are other non-management external users of the financial statement

of the organisation who study the financial report for gathering information regarding the

financial situation as well as liquidity position of the organisation to assess the credit repayment

capability of the organisation. These are the persons who supplies goods and services and raw

material to the chosen organisation TESCO PLC for credit and it is essential for them to

understand the credit repayment capability of the organisation to determine the duration of the

credit period and the possibility of the credit period and to determine also the volume of goods

and services that will be supplied on credit to the organisation. These external users mainly study

the liquidity position of the company, the income statement that describes the profit earned by

the organisation (in a particular period under consideration) and also the cash flow statement to

study the liquidity position of the organisation

Banks and Other private Lenders will study the financial report of the organisation to assess the

debt repayment capability of the organisation. The debt repayment capability of the business to

great extent depends upon the sustainability or stability of the organisation that are reflected

either a stable cash generation capacity or steadily rising cash generation capacity of the

organisation that will gradually strengthen the liquidity position of the organisation by enhancing

the volume of free reserves within the organisation that will strengthen the debt repayment

capacity of the organisation. Apart from the study of the liquidity position the lenders also look

for the different historical ratios that will describe the debt repayment pattern of the organisation

and such ratios are the debt equity ratios, debt asset ratio, interest coverage ratio all that describes

the importance of debt in the capital structure of the borrowing company and how the debt is

managed by the organisation. Beside, the debt equity ratio is specifically studied by the lenders

to understand the purpose of borrowing. That is, a lender who is going to lend certain amount to

Tesco PLC will deeply study the historical debt-equity ratio of the organisation to study to what

extent the debt is taken to utilize the advantage of financial leverage and top whit extent the debt

has been taken to finance some investment projects as the organisation has reached to a

hand study the financial report to decide where to hold the investment (which to a large extent

depends upon the financial position of the organisation) or it is better to withdraw the

investments made for the maximization of the returns(Booth and Hamer, 2009)

Trade Creditors or Suppliers are other non-management external users of the financial statement

of the organisation who study the financial report for gathering information regarding the

financial situation as well as liquidity position of the organisation to assess the credit repayment

capability of the organisation. These are the persons who supplies goods and services and raw

material to the chosen organisation TESCO PLC for credit and it is essential for them to

understand the credit repayment capability of the organisation to determine the duration of the

credit period and the possibility of the credit period and to determine also the volume of goods

and services that will be supplied on credit to the organisation. These external users mainly study

the liquidity position of the company, the income statement that describes the profit earned by

the organisation (in a particular period under consideration) and also the cash flow statement to

study the liquidity position of the organisation

Banks and Other private Lenders will study the financial report of the organisation to assess the

debt repayment capability of the organisation. The debt repayment capability of the business to

great extent depends upon the sustainability or stability of the organisation that are reflected

either a stable cash generation capacity or steadily rising cash generation capacity of the

organisation that will gradually strengthen the liquidity position of the organisation by enhancing

the volume of free reserves within the organisation that will strengthen the debt repayment

capacity of the organisation. Apart from the study of the liquidity position the lenders also look

for the different historical ratios that will describe the debt repayment pattern of the organisation

and such ratios are the debt equity ratios, debt asset ratio, interest coverage ratio all that describes

the importance of debt in the capital structure of the borrowing company and how the debt is

managed by the organisation. Beside, the debt equity ratio is specifically studied by the lenders

to understand the purpose of borrowing. That is, a lender who is going to lend certain amount to

Tesco PLC will deeply study the historical debt-equity ratio of the organisation to study to what

extent the debt is taken to utilize the advantage of financial leverage and top whit extent the debt

has been taken to finance some investment projects as the organisation has reached to a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

saturation position with respect to the raising of capital by the issue of shares for a particular

period under consideration.

Tax Authorities and Regulatory organization always keep a tap on the financial reporting of the

organization Tesco PLC to Understand that to what extent the organization is complying with the

regulatory requirements of report presentation and in the method of accounting as per the IFRS

so that the correct profit amount is presented as the tax rate will be charged on the profit amount

and if the calculation or accounting of the profit amount is not done as per the accounting

standard then the tax calculated on the basis of the profit will be wrong and this wrong amount

will be paid to the required authority. The regulatory agencies also looks after over the annual

report deceleration to track whether the organization has submitted all the required report to the

different regulatory agencies and has made all the required disclosure of the financial

information as per the accounting standard or not. These regulatory agencies always monitor the

activities of the organization in order to protect the interest of the share holders, creditors as well

as investors of the company so that everybody can get access on the required information before

making any vital decisions regarding the organization.

Customers or the clients often study the financial report of an organisation specifically in case

where the customer is a business and is engaged in a Business –to –Business relation with the

organisation. The main reason of studying the annual report for a customer to understand the

capability as well as efficiency of the organisation with respect to the delivery of a particular raw

material or a finished goods that the customer really need to carry on its own operation. For

instance, if a cake making agency buys huge amount of floor from nearby TESCO outlets then

the organisation may be interested to study the financial report to understand that how long

Tesco will be interested to carry on its outlet in the nearby location where the cake maker owns

the shop as the business of the cake maker who is a micro business owner and is very much

dependent over the flour that the micro business owner buys from the only available big retail

grocery outlet of Tesco.

period under consideration.

Tax Authorities and Regulatory organization always keep a tap on the financial reporting of the

organization Tesco PLC to Understand that to what extent the organization is complying with the

regulatory requirements of report presentation and in the method of accounting as per the IFRS

so that the correct profit amount is presented as the tax rate will be charged on the profit amount

and if the calculation or accounting of the profit amount is not done as per the accounting

standard then the tax calculated on the basis of the profit will be wrong and this wrong amount

will be paid to the required authority. The regulatory agencies also looks after over the annual

report deceleration to track whether the organization has submitted all the required report to the

different regulatory agencies and has made all the required disclosure of the financial

information as per the accounting standard or not. These regulatory agencies always monitor the

activities of the organization in order to protect the interest of the share holders, creditors as well

as investors of the company so that everybody can get access on the required information before

making any vital decisions regarding the organization.

Customers or the clients often study the financial report of an organisation specifically in case

where the customer is a business and is engaged in a Business –to –Business relation with the

organisation. The main reason of studying the annual report for a customer to understand the

capability as well as efficiency of the organisation with respect to the delivery of a particular raw

material or a finished goods that the customer really need to carry on its own operation. For

instance, if a cake making agency buys huge amount of floor from nearby TESCO outlets then

the organisation may be interested to study the financial report to understand that how long

Tesco will be interested to carry on its outlet in the nearby location where the cake maker owns

the shop as the business of the cake maker who is a micro business owner and is very much

dependent over the flour that the micro business owner buys from the only available big retail

grocery outlet of Tesco.

How the financial information is fulfilling the requirement of

information of the non management external users

The external users that has been discussed here are not part of the management and therefore

they are not involved in the decision making process of the organisation but still they are

important stake holders of the organisation and makes an in-depth study the financial reports of

the organisation(Seaton and Waterson,2013).

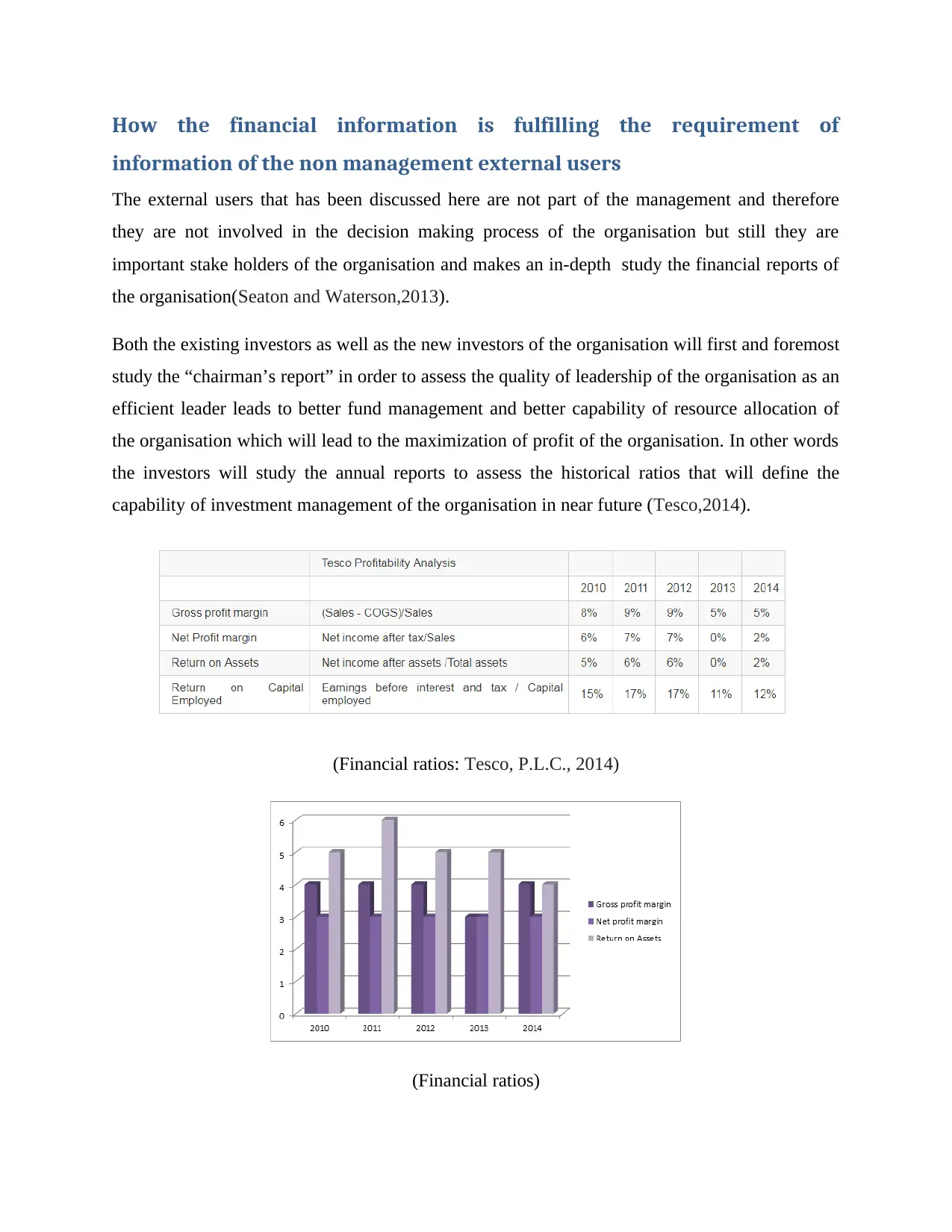

Both the existing investors as well as the new investors of the organisation will first and foremost

study the “chairman’s report” in order to assess the quality of leadership of the organisation as an

efficient leader leads to better fund management and better capability of resource allocation of

the organisation which will lead to the maximization of profit of the organisation. In other words

the investors will study the annual reports to assess the historical ratios that will define the

capability of investment management of the organisation in near future (Tesco,2014).

(Financial ratios: Tesco, P.L.C., 2014)

(Financial ratios)

information of the non management external users

The external users that has been discussed here are not part of the management and therefore

they are not involved in the decision making process of the organisation but still they are

important stake holders of the organisation and makes an in-depth study the financial reports of

the organisation(Seaton and Waterson,2013).

Both the existing investors as well as the new investors of the organisation will first and foremost

study the “chairman’s report” in order to assess the quality of leadership of the organisation as an

efficient leader leads to better fund management and better capability of resource allocation of

the organisation which will lead to the maximization of profit of the organisation. In other words

the investors will study the annual reports to assess the historical ratios that will define the

capability of investment management of the organisation in near future (Tesco,2014).

(Financial ratios: Tesco, P.L.C., 2014)

(Financial ratios)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Source: Tesco, P.L.C., 2014)

2017-02 2016-02 2015-02 2014-02

-5

0

5

10

5.2 5.3

-3.9

6.3

Gross Margin %

Gross Margin %

(Source: Financials.morningstar.com, 2018)

2017-02 2016-02 2015-02 2014-02

-10

-8

-6

-4

-2

0

2

4 -0.07 0.25

-9.22

1.53

Net Margin %

Net Margin %

(Source: Financials.morningstar.com, 2018)

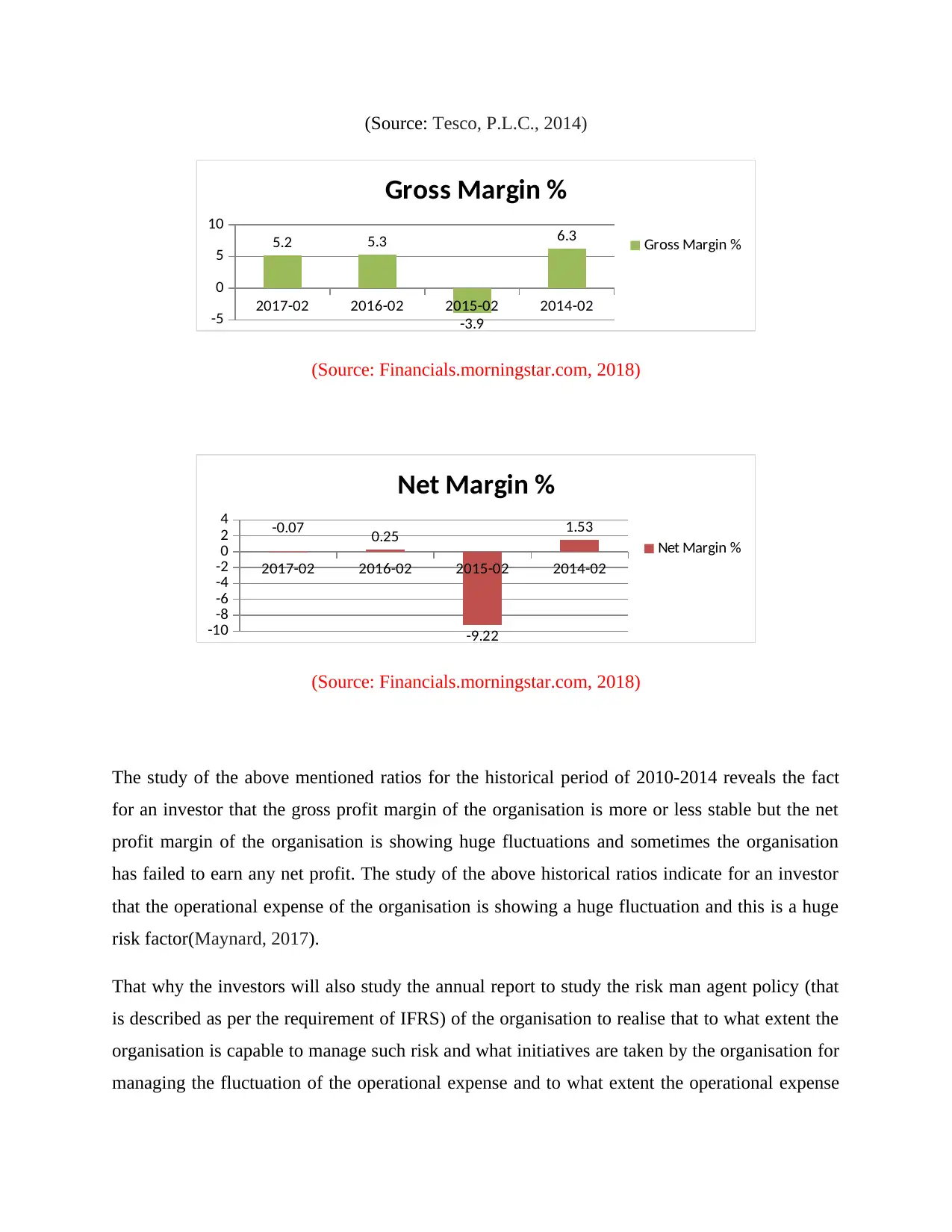

The study of the above mentioned ratios for the historical period of 2010-2014 reveals the fact

for an investor that the gross profit margin of the organisation is more or less stable but the net

profit margin of the organisation is showing huge fluctuations and sometimes the organisation

has failed to earn any net profit. The study of the above historical ratios indicate for an investor

that the operational expense of the organisation is showing a huge fluctuation and this is a huge

risk factor(Maynard, 2017).

That why the investors will also study the annual report to study the risk man agent policy (that

is described as per the requirement of IFRS) of the organisation to realise that to what extent the

organisation is capable to manage such risk and what initiatives are taken by the organisation for

managing the fluctuation of the operational expense and to what extent the operational expense

2017-02 2016-02 2015-02 2014-02

-5

0

5

10

5.2 5.3

-3.9

6.3

Gross Margin %

Gross Margin %

(Source: Financials.morningstar.com, 2018)

2017-02 2016-02 2015-02 2014-02

-10

-8

-6

-4

-2

0

2

4 -0.07 0.25

-9.22

1.53

Net Margin %

Net Margin %

(Source: Financials.morningstar.com, 2018)

The study of the above mentioned ratios for the historical period of 2010-2014 reveals the fact

for an investor that the gross profit margin of the organisation is more or less stable but the net

profit margin of the organisation is showing huge fluctuations and sometimes the organisation

has failed to earn any net profit. The study of the above historical ratios indicate for an investor

that the operational expense of the organisation is showing a huge fluctuation and this is a huge

risk factor(Maynard, 2017).

That why the investors will also study the annual report to study the risk man agent policy (that

is described as per the requirement of IFRS) of the organisation to realise that to what extent the

organisation is capable to manage such risk and what initiatives are taken by the organisation for

managing the fluctuation of the operational expense and to what extent the operational expense

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

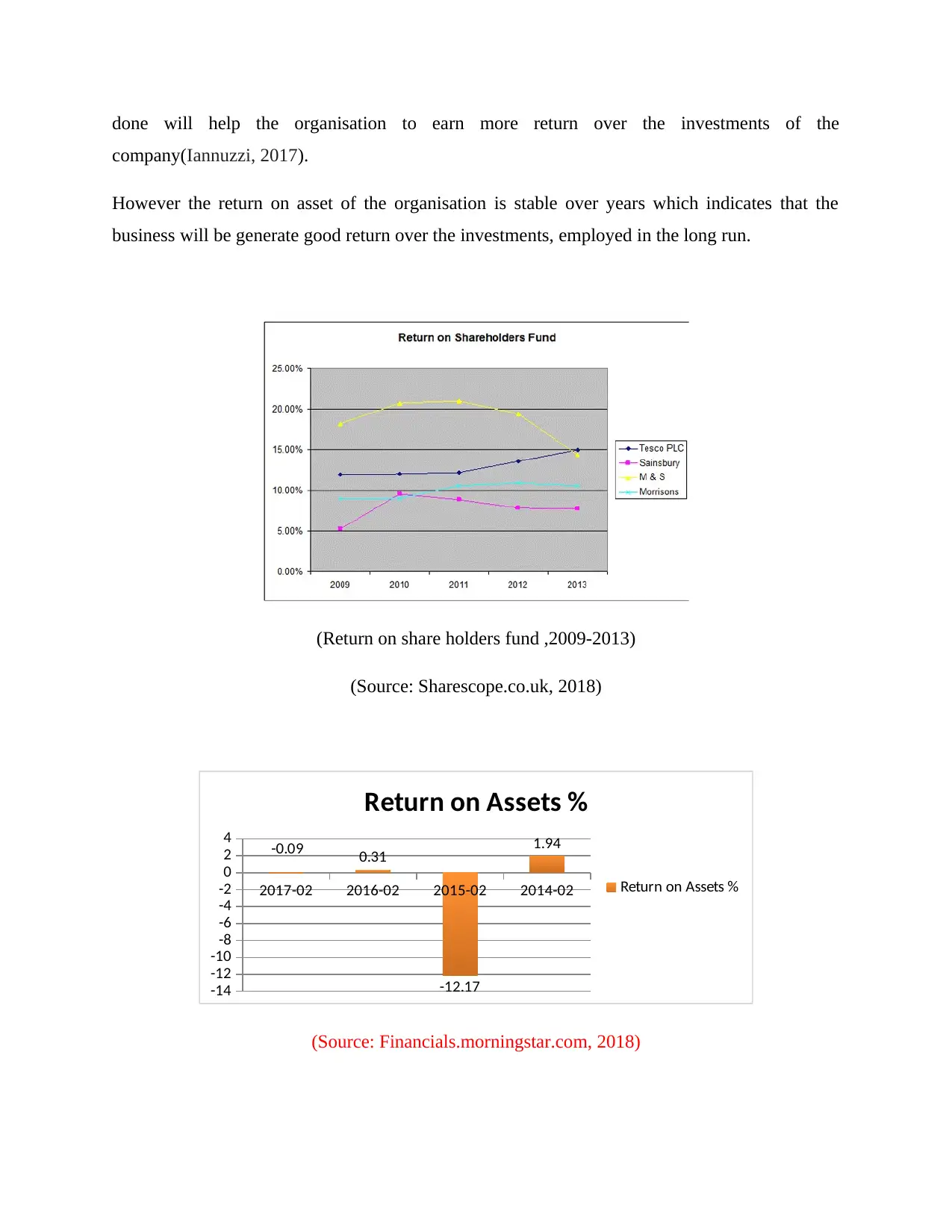

done will help the organisation to earn more return over the investments of the

company(Iannuzzi, 2017).

However the return on asset of the organisation is stable over years which indicates that the

business will be generate good return over the investments, employed in the long run.

(Return on share holders fund ,2009-2013)

(Source: Sharescope.co.uk, 2018)

2017-02 2016-02 2015-02 2014-02

-14

-12

-10

-8

-6

-4

-2

0

2

4 -0.09 0.31

-12.17

1.94

Return on Assets %

Return on Assets %

(Source: Financials.morningstar.com, 2018)

company(Iannuzzi, 2017).

However the return on asset of the organisation is stable over years which indicates that the

business will be generate good return over the investments, employed in the long run.

(Return on share holders fund ,2009-2013)

(Source: Sharescope.co.uk, 2018)

2017-02 2016-02 2015-02 2014-02

-14

-12

-10

-8

-6

-4

-2

0

2

4 -0.09 0.31

-12.17

1.94

Return on Assets %

Return on Assets %

(Source: Financials.morningstar.com, 2018)

2017-02 2016-02 2015-02 2014-02

-60

-50

-40

-30

-20

-10

0

10 -0.53

1.76

-52.7

6.21

Return on Equity %

Return on Equity %

(Source:Financials.morningstar.com, 2018)

(Source: Financials.morningstar.com, 2018)

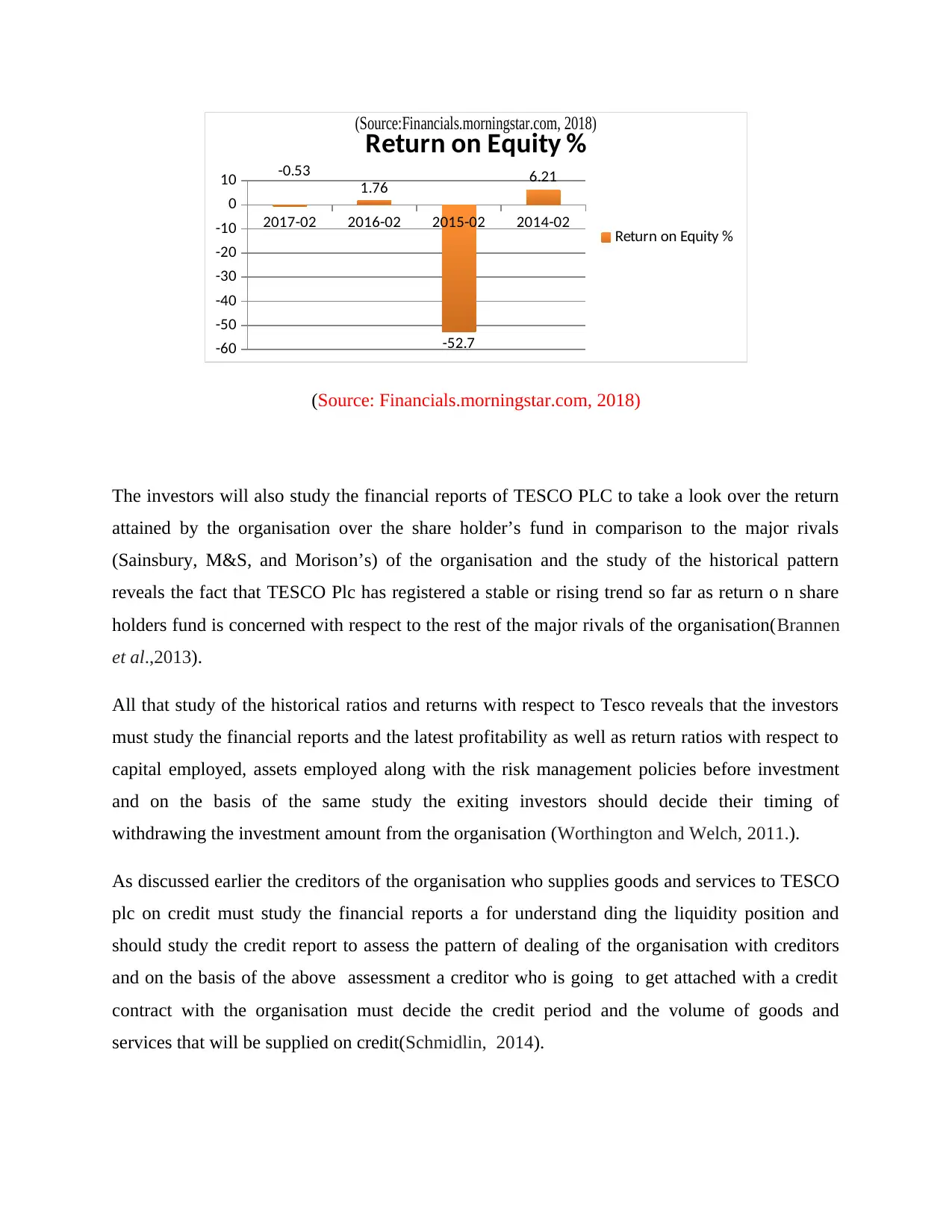

The investors will also study the financial reports of TESCO PLC to take a look over the return

attained by the organisation over the share holder’s fund in comparison to the major rivals

(Sainsbury, M&S, and Morison’s) of the organisation and the study of the historical pattern

reveals the fact that TESCO Plc has registered a stable or rising trend so far as return o n share

holders fund is concerned with respect to the rest of the major rivals of the organisation(Brannen

et al.,2013).

All that study of the historical ratios and returns with respect to Tesco reveals that the investors

must study the financial reports and the latest profitability as well as return ratios with respect to

capital employed, assets employed along with the risk management policies before investment

and on the basis of the same study the exiting investors should decide their timing of

withdrawing the investment amount from the organisation (Worthington and Welch, 2011.).

As discussed earlier the creditors of the organisation who supplies goods and services to TESCO

plc on credit must study the financial reports a for understand ding the liquidity position and

should study the credit report to assess the pattern of dealing of the organisation with creditors

and on the basis of the above assessment a creditor who is going to get attached with a credit

contract with the organisation must decide the credit period and the volume of goods and

services that will be supplied on credit(Schmidlin, 2014).

-60

-50

-40

-30

-20

-10

0

10 -0.53

1.76

-52.7

6.21

Return on Equity %

Return on Equity %

(Source:Financials.morningstar.com, 2018)

(Source: Financials.morningstar.com, 2018)

The investors will also study the financial reports of TESCO PLC to take a look over the return

attained by the organisation over the share holder’s fund in comparison to the major rivals

(Sainsbury, M&S, and Morison’s) of the organisation and the study of the historical pattern

reveals the fact that TESCO Plc has registered a stable or rising trend so far as return o n share

holders fund is concerned with respect to the rest of the major rivals of the organisation(Brannen

et al.,2013).

All that study of the historical ratios and returns with respect to Tesco reveals that the investors

must study the financial reports and the latest profitability as well as return ratios with respect to

capital employed, assets employed along with the risk management policies before investment

and on the basis of the same study the exiting investors should decide their timing of

withdrawing the investment amount from the organisation (Worthington and Welch, 2011.).

As discussed earlier the creditors of the organisation who supplies goods and services to TESCO

plc on credit must study the financial reports a for understand ding the liquidity position and

should study the credit report to assess the pattern of dealing of the organisation with creditors

and on the basis of the above assessment a creditor who is going to get attached with a credit

contract with the organisation must decide the credit period and the volume of goods and

services that will be supplied on credit(Schmidlin, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

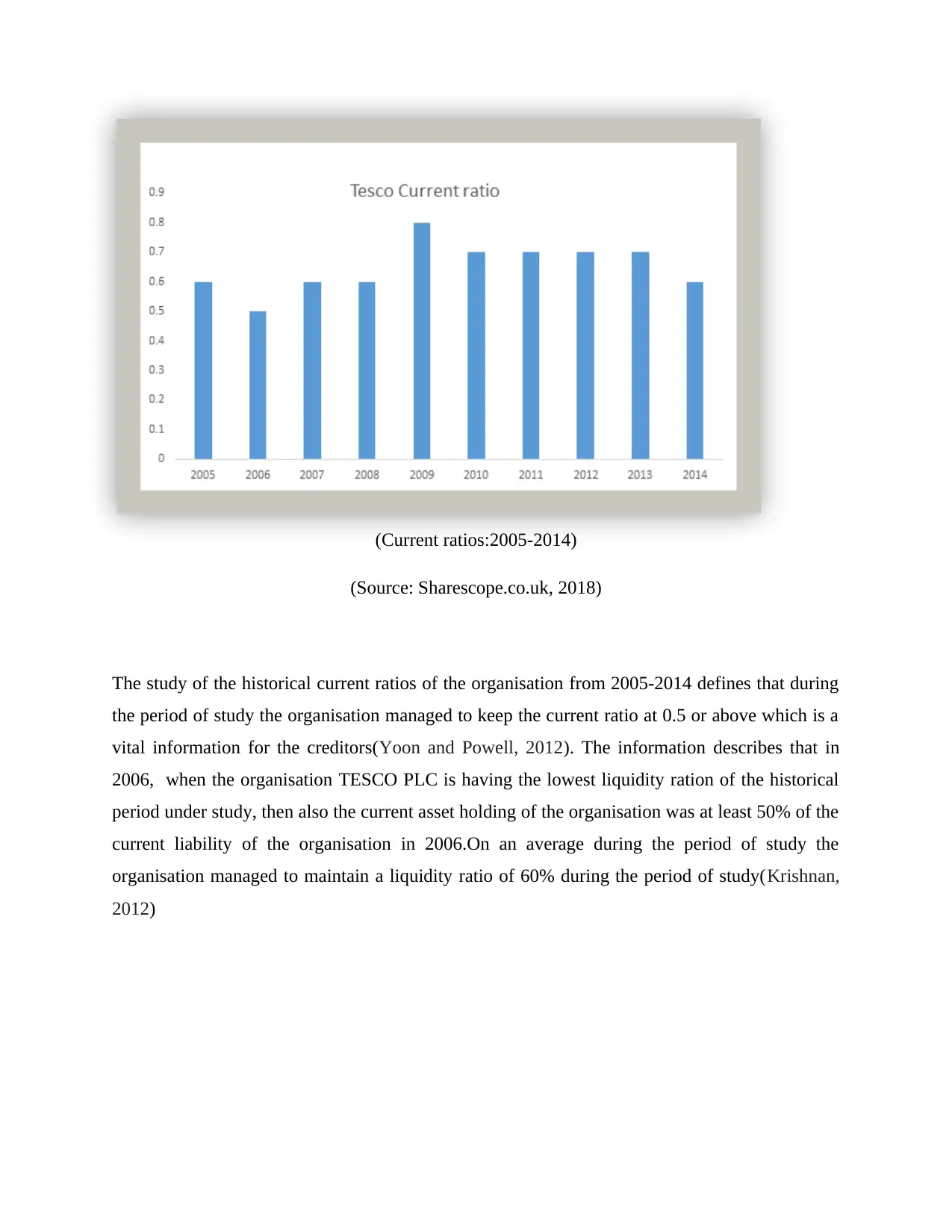

(Current ratios:2005-2014)

(Source: Sharescope.co.uk, 2018)

The study of the historical current ratios of the organisation from 2005-2014 defines that during

the period of study the organisation managed to keep the current ratio at 0.5 or above which is a

vital information for the creditors(Yoon and Powell, 2012). The information describes that in

2006, when the organisation TESCO PLC is having the lowest liquidity ration of the historical

period under study, then also the current asset holding of the organisation was at least 50% of the

current liability of the organisation in 2006.On an average during the period of study the

organisation managed to maintain a liquidity ratio of 60% during the period of study(Krishnan,

2012)

(Source: Sharescope.co.uk, 2018)

The study of the historical current ratios of the organisation from 2005-2014 defines that during

the period of study the organisation managed to keep the current ratio at 0.5 or above which is a

vital information for the creditors(Yoon and Powell, 2012). The information describes that in

2006, when the organisation TESCO PLC is having the lowest liquidity ration of the historical

period under study, then also the current asset holding of the organisation was at least 50% of the

current liability of the organisation in 2006.On an average during the period of study the

organisation managed to maintain a liquidity ratio of 60% during the period of study(Krishnan,

2012)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

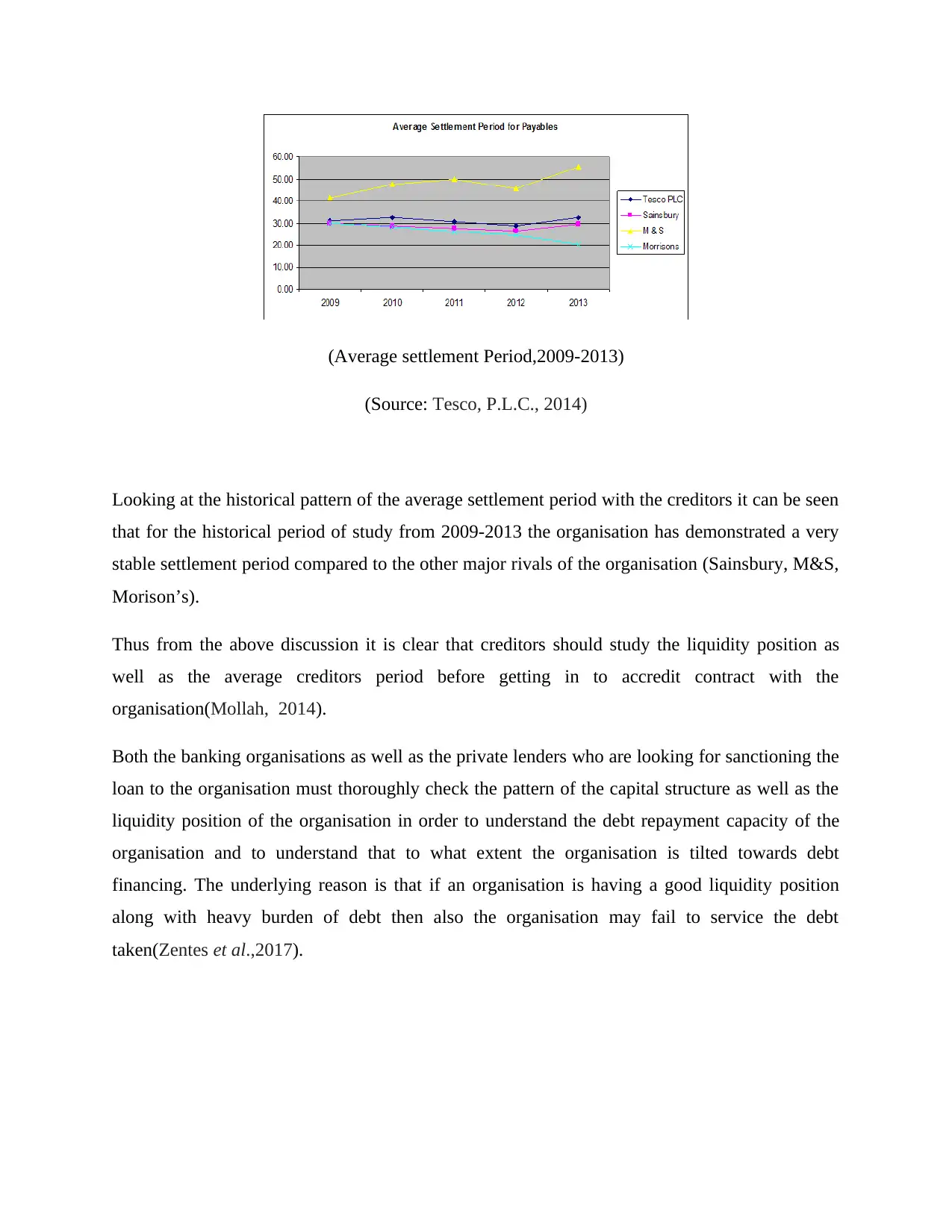

(Average settlement Period,2009-2013)

(Source: Tesco, P.L.C., 2014)

Looking at the historical pattern of the average settlement period with the creditors it can be seen

that for the historical period of study from 2009-2013 the organisation has demonstrated a very

stable settlement period compared to the other major rivals of the organisation (Sainsbury, M&S,

Morison’s).

Thus from the above discussion it is clear that creditors should study the liquidity position as

well as the average creditors period before getting in to accredit contract with the

organisation(Mollah, 2014).

Both the banking organisations as well as the private lenders who are looking for sanctioning the

loan to the organisation must thoroughly check the pattern of the capital structure as well as the

liquidity position of the organisation in order to understand the debt repayment capacity of the

organisation and to understand that to what extent the organisation is tilted towards debt

financing. The underlying reason is that if an organisation is having a good liquidity position

along with heavy burden of debt then also the organisation may fail to service the debt

taken(Zentes et al.,2017).

(Source: Tesco, P.L.C., 2014)

Looking at the historical pattern of the average settlement period with the creditors it can be seen

that for the historical period of study from 2009-2013 the organisation has demonstrated a very

stable settlement period compared to the other major rivals of the organisation (Sainsbury, M&S,

Morison’s).

Thus from the above discussion it is clear that creditors should study the liquidity position as

well as the average creditors period before getting in to accredit contract with the

organisation(Mollah, 2014).

Both the banking organisations as well as the private lenders who are looking for sanctioning the

loan to the organisation must thoroughly check the pattern of the capital structure as well as the

liquidity position of the organisation in order to understand the debt repayment capacity of the

organisation and to understand that to what extent the organisation is tilted towards debt

financing. The underlying reason is that if an organisation is having a good liquidity position

along with heavy burden of debt then also the organisation may fail to service the debt

taken(Zentes et al.,2017).

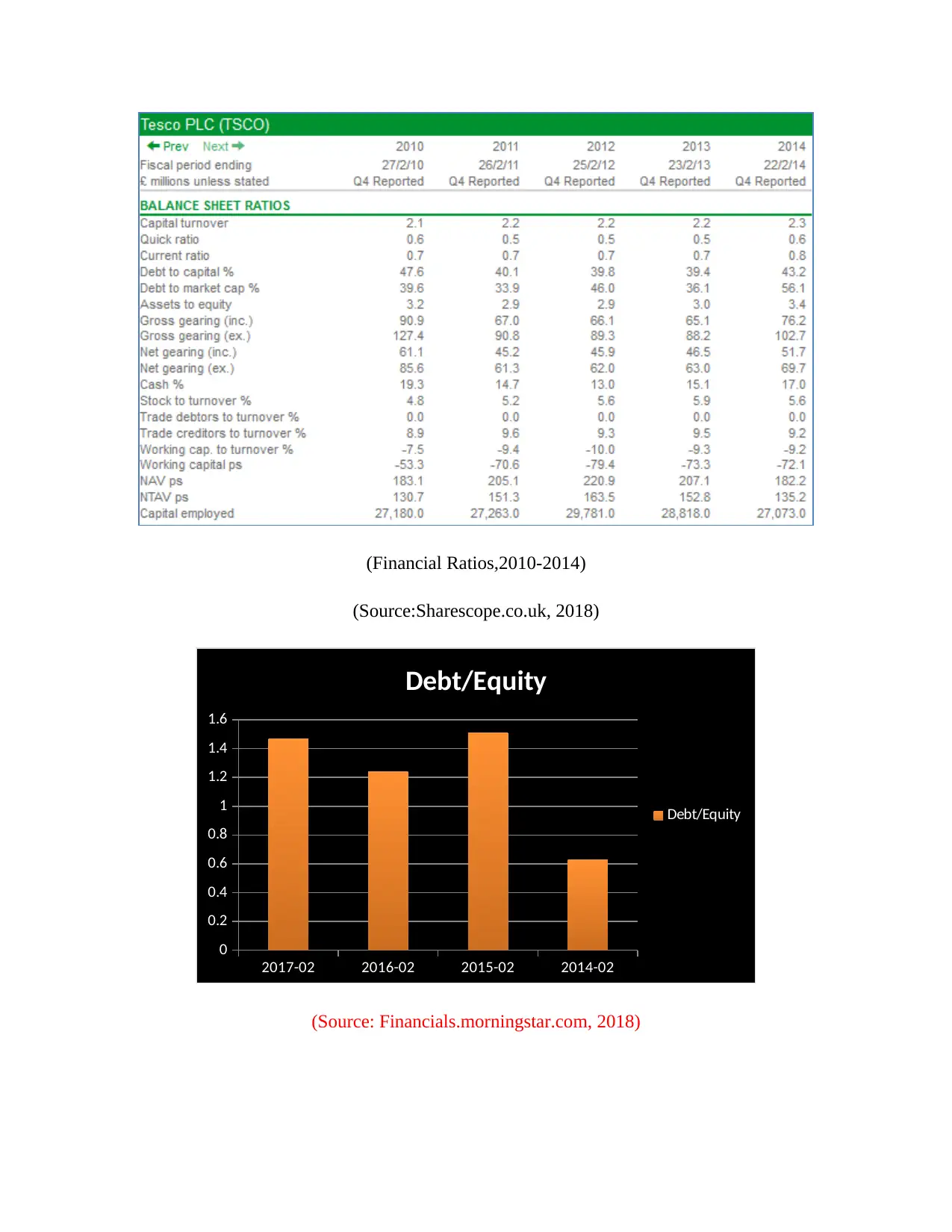

(Financial Ratios,2010-2014)

(Source:Sharescope.co.uk, 2018)

2017-02 2016-02 2015-02 2014-02

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Debt/Equity

Debt/Equity

(Source: Financials.morningstar.com, 2018)

(Source:Sharescope.co.uk, 2018)

2017-02 2016-02 2015-02 2014-02

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Debt/Equity

Debt/Equity

(Source: Financials.morningstar.com, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.