MBA 606: Financial Management, Decision Making, Tesco PLC Analysis

VerifiedAdded on 2023/04/20

|13

|2819

|481

Report

AI Summary

This report delves into the critical role of financial management in business decision-making, using Tesco PLC as a case study. It explores how financial statements are used to project future cash flows and provides an in-depth evaluation of Tesco's financial performance for the years 2017 and 2018 using ratio analysis. The analysis covers liquidity, profitability, turnover, and financial leverage ratios, highlighting areas of improvement and concern for Tesco PLC. The report concludes with recommendations based on the financial analysis, emphasizing the importance of effective financial management for the company's long-term sustainability and growth. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

Running head: FINANCIAL MANAGEMENT

Financial management

Name of the student

Name of the university

Student ID

Author note

Financial management

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Table of Contents

Introduction................................................................................................................................2

Role of the financial Management in context of decision making.............................................2

Projecting future cash flows using financial statements............................................................4

Importance of financial statements............................................................................................5

Evaluation of financial statements.............................................................................................6

Interpretation..............................................................................................................................7

Conclusion and recommendation...............................................................................................9

Reference..................................................................................................................................11

Table of Contents

Introduction................................................................................................................................2

Role of the financial Management in context of decision making.............................................2

Projecting future cash flows using financial statements............................................................4

Importance of financial statements............................................................................................5

Evaluation of financial statements.............................................................................................6

Interpretation..............................................................................................................................7

Conclusion and recommendation...............................................................................................9

Reference..................................................................................................................................11

2FINANCIAL MANAGEMENT

Introduction

Financial management is considered as an important activity for any firm. It is the

procedure for organizing, planning, monitoring and controlling the financial resources with

the aim of achieving the overall objectives and goals of the firm. It is the ultimate approach

for controlling the organization’s financial activities including funds procurement, fund

utilization, risk assessment, payments and other things associated with money. Proper

financial management of a firm enables it to function efficiently. If the finances are not

managed appropriately it will face different barriers that may have severe impact on its

development and growth (Bekaert & Hodrick, 2017). Tesco PLC is the retail company that is

engaged in retails business and associated activities related to retail. 2 segments of the entity

are ROI (Republic of Ireland) and UK (United Kingdom). The entity was established by John

Edward in the year 1919 and it has it’s headquarter in Welwyn Garden, UK. The entity holds

the leading position among the food retailers of Great Britain with the market share of more

than 15% (Tesco plc, 2019).

Role of the financial Management in context of decision making

Proper usage and distribution of the funds results into improvement in operational

efficiency of business concern that is possible through proper financial management. While

the finance manager properly uses the funds, cost of capital can be reduced which in turn will

enhance the firm’s value. It further helps in taking sound financial decision regarding the

business concern. Financial decision making have impact on entire business as direct

relationship is there among different departmental functions including production personnel

and marketing (Finkler, Smith & Calabrese, 2019). Major decision making areas in the

business through financial management are as follows –

Introduction

Financial management is considered as an important activity for any firm. It is the

procedure for organizing, planning, monitoring and controlling the financial resources with

the aim of achieving the overall objectives and goals of the firm. It is the ultimate approach

for controlling the organization’s financial activities including funds procurement, fund

utilization, risk assessment, payments and other things associated with money. Proper

financial management of a firm enables it to function efficiently. If the finances are not

managed appropriately it will face different barriers that may have severe impact on its

development and growth (Bekaert & Hodrick, 2017). Tesco PLC is the retail company that is

engaged in retails business and associated activities related to retail. 2 segments of the entity

are ROI (Republic of Ireland) and UK (United Kingdom). The entity was established by John

Edward in the year 1919 and it has it’s headquarter in Welwyn Garden, UK. The entity holds

the leading position among the food retailers of Great Britain with the market share of more

than 15% (Tesco plc, 2019).

Role of the financial Management in context of decision making

Proper usage and distribution of the funds results into improvement in operational

efficiency of business concern that is possible through proper financial management. While

the finance manager properly uses the funds, cost of capital can be reduced which in turn will

enhance the firm’s value. It further helps in taking sound financial decision regarding the

business concern. Financial decision making have impact on entire business as direct

relationship is there among different departmental functions including production personnel

and marketing (Finkler, Smith & Calabrese, 2019). Major decision making areas in the

business through financial management are as follows –

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

Investment decision – investment decision involves generation of assets for earning

incomes. Assets selection for making investment is the decision in context of

investment. The management must decide how realized funds shall be used for

different investments. Generally, the company’s assets include 2 types of assets –

assets those are convertible into cash quickly and assets those yield earnings

spreading over the year. 1st category of investment decision falls under capital

budgeting and the next type falls under working capital management. Capital

budgeting is distribution of the funds on new assets or re-distribution of the capital

when any old asset is replaced. Worthiness of various investment proposals are

crucial part under the exercise of capital budgeting. As the investment is exposed to

different risks, the management is required to consider this with sufficient prudence

and caution (Zietlow et al., 2018). Decision of capital budgeting is considered as

another crucial aspect of financial management. The management must determine the

standards or norms for judging the benefits. This is called as the hurdle rate,

minimum return rate and the rate of cut-off. On the other hand, management of

working capital is associated with the management of shirt-term assets. The entity

requires sufficient working capital for meeting its short term obligations that is

known as liquidity. If the management is not able to estimate the requirement of

working capital properly the company may face liquidity crisis or may have under

utilisation of revenues (Zietlow et al., 2018).

Dividend decision – profit of the entity can be dealt in 2 ways – retain the profit for

business purpose or distribute the profits to the shareholders as dividend.

Shareholders will be unsatisfied if they do not receive dividend as per their

expectations. This in turn, will drop the share’s market value and will lead to

financial crisis. Conversely, if the profits are distributed as dividend to maximum

Investment decision – investment decision involves generation of assets for earning

incomes. Assets selection for making investment is the decision in context of

investment. The management must decide how realized funds shall be used for

different investments. Generally, the company’s assets include 2 types of assets –

assets those are convertible into cash quickly and assets those yield earnings

spreading over the year. 1st category of investment decision falls under capital

budgeting and the next type falls under working capital management. Capital

budgeting is distribution of the funds on new assets or re-distribution of the capital

when any old asset is replaced. Worthiness of various investment proposals are

crucial part under the exercise of capital budgeting. As the investment is exposed to

different risks, the management is required to consider this with sufficient prudence

and caution (Zietlow et al., 2018). Decision of capital budgeting is considered as

another crucial aspect of financial management. The management must determine the

standards or norms for judging the benefits. This is called as the hurdle rate,

minimum return rate and the rate of cut-off. On the other hand, management of

working capital is associated with the management of shirt-term assets. The entity

requires sufficient working capital for meeting its short term obligations that is

known as liquidity. If the management is not able to estimate the requirement of

working capital properly the company may face liquidity crisis or may have under

utilisation of revenues (Zietlow et al., 2018).

Dividend decision – profit of the entity can be dealt in 2 ways – retain the profit for

business purpose or distribute the profits to the shareholders as dividend.

Shareholders will be unsatisfied if they do not receive dividend as per their

expectations. This in turn, will drop the share’s market value and will lead to

financial crisis. Conversely, if the profits are distributed as dividend to maximum

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

extent it will lose the self financing. Hence, the management shall make a sensible

decision that is good combination of retention and distribution. Dividend decision

determines the proportion of net profits to be distributed as dividend to the

shareholders. Management here shall consider 2 crucial facts – investment

opportunity available to the entity and shareholder’s preferences (Andreou, Louca &

Panayides, 2014).

Financing decisions – this decision involves where and when funds shall be raised for

meeting investment requirements. It is associated with financial leverage or capital

structure. If higher proportion of capital is raised through debt, risk of shareholder’s

are reduced and at the same time chances of receiving dividend on their holdings

reduced. Hence, under financial decision important point is trading off among risk

and return. Further, unlike the investment decision the financing decision is related to

the determination of capital structure that is proper balance among equity and debt.

Financing decision has 2 major dimensions – to find out whether capital structure is

optimum and proportion of fund to be raised for maximizing return to shareholders

(Cornwall, Vang & Hartman, 2016).

Projecting future cash flows using financial statements

Under financial statements, the cash flow statement reveals how the changes in the

income and balance sheet have an impact on the cash flows of the entity and accordingly the

management makes the operational analysis. Generally, the cash flow statement is concerned

regarding the inflow and outflow of business cash. It involves both current operating results

as well as the changes in the accompanying balance sheet. Hence, the financial statements

are used in financial management as an analytical tool to determine the entity’s short-term

viability and and its ability to meet the obligations. For projecting the cash flows for the

extent it will lose the self financing. Hence, the management shall make a sensible

decision that is good combination of retention and distribution. Dividend decision

determines the proportion of net profits to be distributed as dividend to the

shareholders. Management here shall consider 2 crucial facts – investment

opportunity available to the entity and shareholder’s preferences (Andreou, Louca &

Panayides, 2014).

Financing decisions – this decision involves where and when funds shall be raised for

meeting investment requirements. It is associated with financial leverage or capital

structure. If higher proportion of capital is raised through debt, risk of shareholder’s

are reduced and at the same time chances of receiving dividend on their holdings

reduced. Hence, under financial decision important point is trading off among risk

and return. Further, unlike the investment decision the financing decision is related to

the determination of capital structure that is proper balance among equity and debt.

Financing decision has 2 major dimensions – to find out whether capital structure is

optimum and proportion of fund to be raised for maximizing return to shareholders

(Cornwall, Vang & Hartman, 2016).

Projecting future cash flows using financial statements

Under financial statements, the cash flow statement reveals how the changes in the

income and balance sheet have an impact on the cash flows of the entity and accordingly the

management makes the operational analysis. Generally, the cash flow statement is concerned

regarding the inflow and outflow of business cash. It involves both current operating results

as well as the changes in the accompanying balance sheet. Hence, the financial statements

are used in financial management as an analytical tool to determine the entity’s short-term

viability and and its ability to meet the obligations. For projecting the cash flows for the

5FINANCIAL MANAGEMENT

future period management may perform the common size analysis of the income statement

and balance sheet (Baños-Caballero, García-Teruel & Martínez-Solano, 2014). It will enable

to analyse the composition of liabilities and assets, weightage of expenses to total cost and

revenues. This in turn helps to predict the future cash flows.

Importance of financial statements

The main purpose of the financial statement is delivering information regarding the

financial performances, position and variation in the firm’s financial position during the

specific period. Financial statements includes 4 major statements as follows –

Income statement that represents the earnings and expenses of the firm for the

particular period

Balance sheet that represents the items and amount of assets, liabilities and

shareholder’s equity.

Cash flow statement that represents the cash inflows and cash outflows taken place

during the particular period (Wang, 2014)

Statement of changes in equity that represents the owner’s equity in the business.

Financial statements are useful as it delivers wide range of useful information to the

users as follows –

Managers use the financial statements for managing company’s affairs and analysing

the financial position and performance

Investors use the financial statements for analysing the return and risks associated

with the investment and taking investment related decisions based on that.

Employees use the financial statements for analysing the profitability status of the

entity and its impact on their remuneration and security of the job

future period management may perform the common size analysis of the income statement

and balance sheet (Baños-Caballero, García-Teruel & Martínez-Solano, 2014). It will enable

to analyse the composition of liabilities and assets, weightage of expenses to total cost and

revenues. This in turn helps to predict the future cash flows.

Importance of financial statements

The main purpose of the financial statement is delivering information regarding the

financial performances, position and variation in the firm’s financial position during the

specific period. Financial statements includes 4 major statements as follows –

Income statement that represents the earnings and expenses of the firm for the

particular period

Balance sheet that represents the items and amount of assets, liabilities and

shareholder’s equity.

Cash flow statement that represents the cash inflows and cash outflows taken place

during the particular period (Wang, 2014)

Statement of changes in equity that represents the owner’s equity in the business.

Financial statements are useful as it delivers wide range of useful information to the

users as follows –

Managers use the financial statements for managing company’s affairs and analysing

the financial position and performance

Investors use the financial statements for analysing the return and risks associated

with the investment and taking investment related decisions based on that.

Employees use the financial statements for analysing the profitability status of the

entity and its impact on their remuneration and security of the job

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

Competitors can compare the performance through analysing the financial statement

and can develop their plan and strategies accordingly (Wahlen, Baginski & Bradshaw,

2014).

Evaluation of financial statements

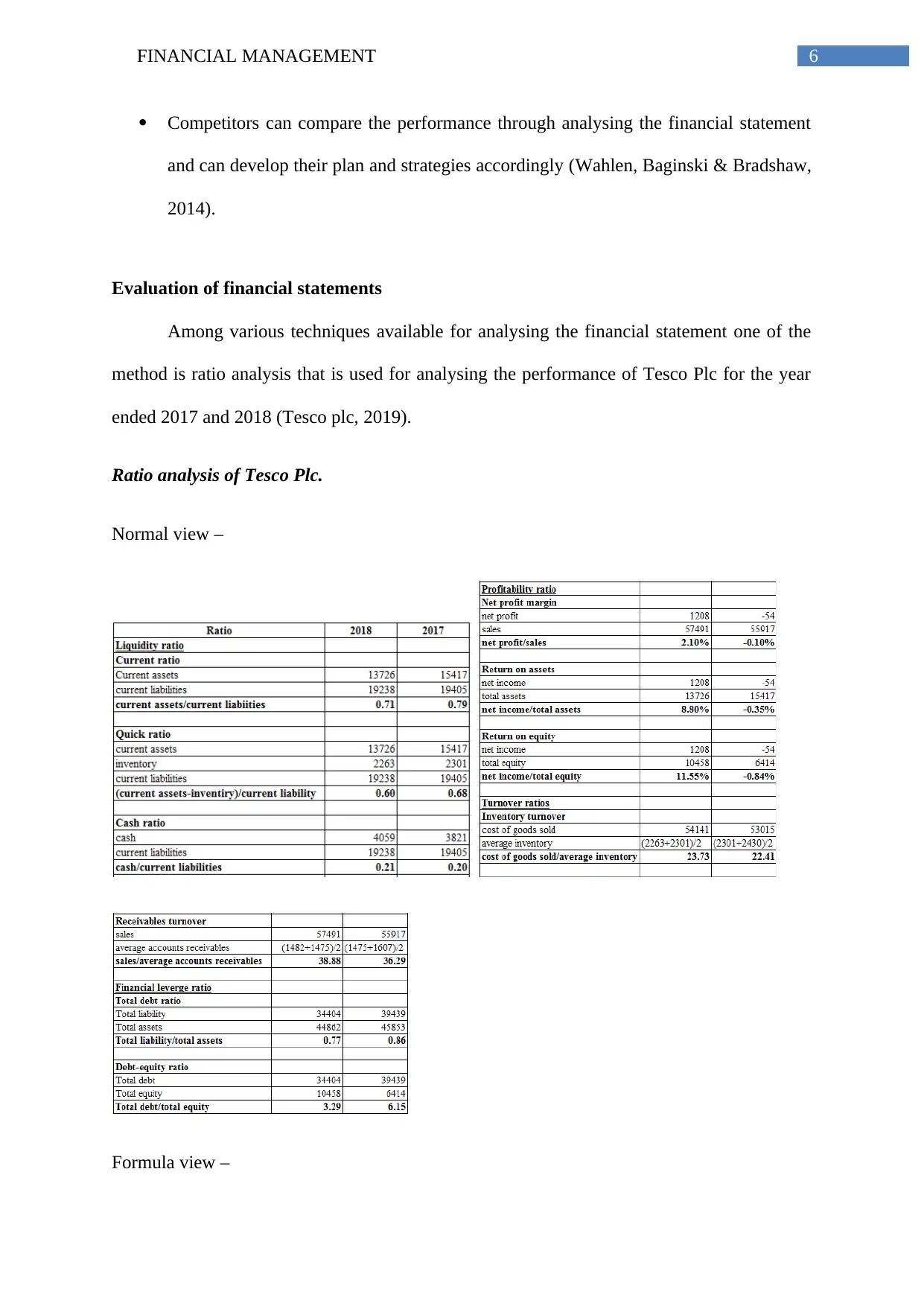

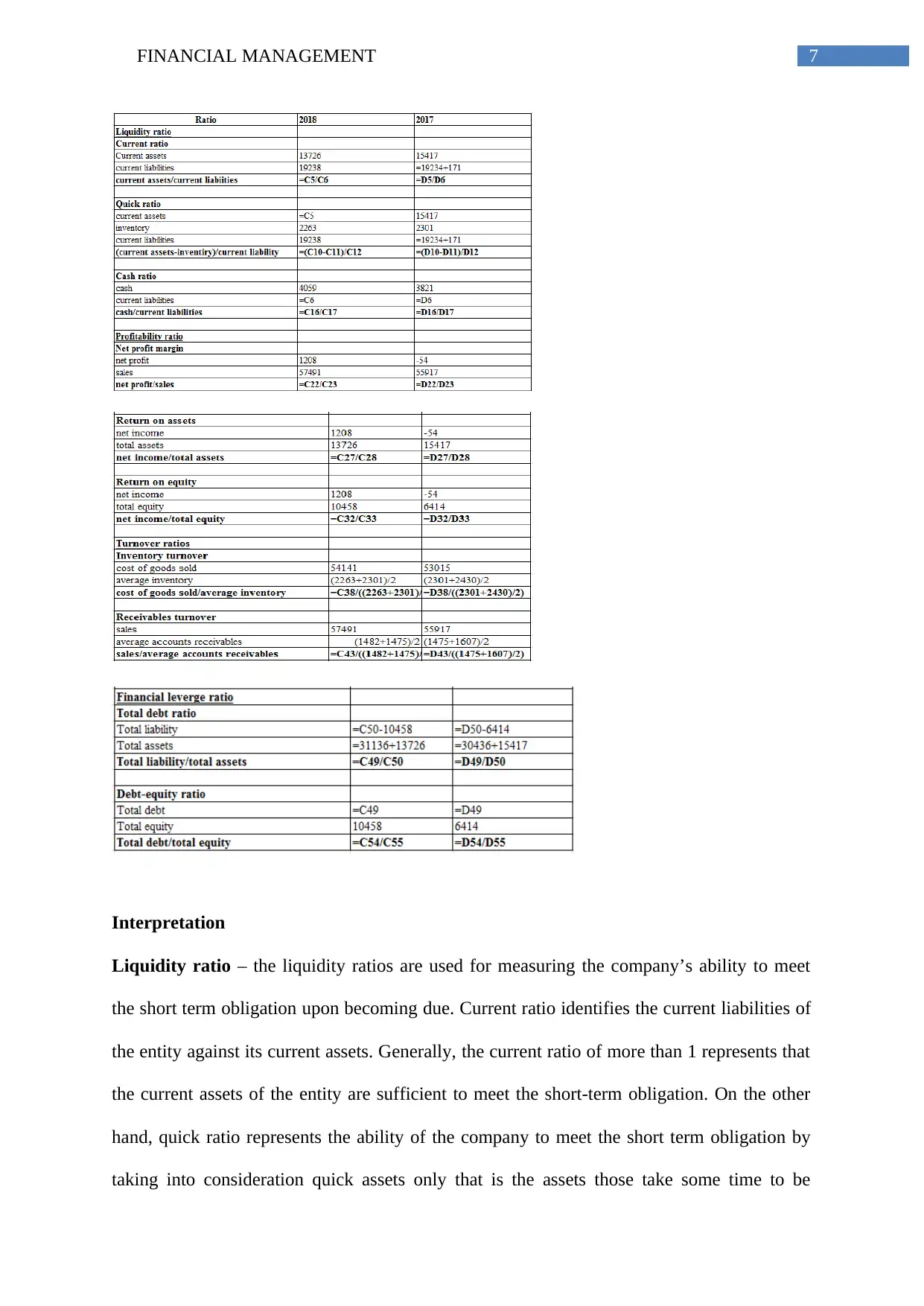

Among various techniques available for analysing the financial statement one of the

method is ratio analysis that is used for analysing the performance of Tesco Plc for the year

ended 2017 and 2018 (Tesco plc, 2019).

Ratio analysis of Tesco Plc.

Normal view –

Formula view –

Competitors can compare the performance through analysing the financial statement

and can develop their plan and strategies accordingly (Wahlen, Baginski & Bradshaw,

2014).

Evaluation of financial statements

Among various techniques available for analysing the financial statement one of the

method is ratio analysis that is used for analysing the performance of Tesco Plc for the year

ended 2017 and 2018 (Tesco plc, 2019).

Ratio analysis of Tesco Plc.

Normal view –

Formula view –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

Interpretation

Liquidity ratio – the liquidity ratios are used for measuring the company’s ability to meet

the short term obligation upon becoming due. Current ratio identifies the current liabilities of

the entity against its current assets. Generally, the current ratio of more than 1 represents that

the current assets of the entity are sufficient to meet the short-term obligation. On the other

hand, quick ratio represents the ability of the company to meet the short term obligation by

taking into consideration quick assets only that is the assets those take some time to be

Interpretation

Liquidity ratio – the liquidity ratios are used for measuring the company’s ability to meet

the short term obligation upon becoming due. Current ratio identifies the current liabilities of

the entity against its current assets. Generally, the current ratio of more than 1 represents that

the current assets of the entity are sufficient to meet the short-term obligation. On the other

hand, quick ratio represents the ability of the company to meet the short term obligation by

taking into consideration quick assets only that is the assets those take some time to be

8FINANCIAL MANAGEMENT

converted into cash are not considered (Ehiedu, 2014). Generally, the quick ratio of more

than 1 represents that the quick assets of the entity are sufficient to meet the short-term

obligation. Further, the cash ratio that compares the cash and cash equivalent of the entity

with current liabilities is considered good if it is more than 1. However, both the current ratio

and quick ratio and cash ratio of the entity for 2017 as well as 2018 are considerably lower

than 1. Hence, the liquidity position of the entity is not good (Tesco plc, 2019).

Profitability ratio – it represents the profit earning capability of the entity from the revenues

after meeting all the expenses. Net profit margin represents the percentage of earning

available with the firm after paying all the expenses of the business. Return on assets

indicates the percentage of profit generated by the entity from the assets. Return on equity

represents the earnings received by the shareholders on their holdings (Growe et al., 2014). It

is found that as the company was not able to earn any positive earnings in the year 2017 all

the profitability ratios are in negative. However, the position in the year 2018 has been

improved and the company was able to generate positive return on shareholder’s holdings

and generate income from the assets (Tesco plc, 2019).

Turnover ratios – these are also known as the efficiency ratios used for measuring the

efficiency of the entity with regard to collection of its dues and replacement of its inventories.

Inventory turnover represents the times the entity is able to sale or replace its inventories

during the year (Williams & Dobelman, 2017). It is identified that the efficiency of the

company with regard to inventory has been improved from 22.41 times to 23.73 times.

Receivable turnover ratio represent the times the entity is able to collect its dues during the

year. It is identified that the efficiency of the company with regard to collection has been

improved from 36.29 times to 38.88 times (Tesco plc, 2019).

converted into cash are not considered (Ehiedu, 2014). Generally, the quick ratio of more

than 1 represents that the quick assets of the entity are sufficient to meet the short-term

obligation. Further, the cash ratio that compares the cash and cash equivalent of the entity

with current liabilities is considered good if it is more than 1. However, both the current ratio

and quick ratio and cash ratio of the entity for 2017 as well as 2018 are considerably lower

than 1. Hence, the liquidity position of the entity is not good (Tesco plc, 2019).

Profitability ratio – it represents the profit earning capability of the entity from the revenues

after meeting all the expenses. Net profit margin represents the percentage of earning

available with the firm after paying all the expenses of the business. Return on assets

indicates the percentage of profit generated by the entity from the assets. Return on equity

represents the earnings received by the shareholders on their holdings (Growe et al., 2014). It

is found that as the company was not able to earn any positive earnings in the year 2017 all

the profitability ratios are in negative. However, the position in the year 2018 has been

improved and the company was able to generate positive return on shareholder’s holdings

and generate income from the assets (Tesco plc, 2019).

Turnover ratios – these are also known as the efficiency ratios used for measuring the

efficiency of the entity with regard to collection of its dues and replacement of its inventories.

Inventory turnover represents the times the entity is able to sale or replace its inventories

during the year (Williams & Dobelman, 2017). It is identified that the efficiency of the

company with regard to inventory has been improved from 22.41 times to 23.73 times.

Receivable turnover ratio represent the times the entity is able to collect its dues during the

year. It is identified that the efficiency of the company with regard to collection has been

improved from 36.29 times to 38.88 times (Tesco plc, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

Financial leverage ratio – it represents the leverage position of the company that is the

proportion of debt and equity it its capital structure. Debt ratio represents the proportion of

assets raised through debt financing. Debt ratio of the company has been improved in 2018 as

compared to 2017 as the ratio is reduced from 0.86 to 0.77 (Chen et al., 2014). On the other

hand, debt equity ratio represents the debt and equity portion of the capital structure of the

entity. Generally, the ratio of 0.50 represents that the company is well balanced. Though the

debt equity ratio of the entity has been improved from 6.15 to 3.29, significantly high debt

equity ratio is indicating that the company is highly leveraged (Tesco plc, 2019).

Conclusion and recommendation

Based on the above discussion and interpretation of the financial performance of

Tesco Plc, it can be concluded that financial management is an important aspect in context of

making various major financial decisions. Further, through financial management future cash

flows of the entity can be projected by assessing the financial statements. Financial

statements deliver information regarding the financial performances, position of the entity

and delivers wide range of useful information to the users including management, employees,

government, suppliers and investors. Looking into the financial performance of Tesco Plc for

the year ended 2017 and 2018 it can be stated that the liquidity position of the company is not

good enough to meet its short term obligations. On the other hand, profitability ratios and

turnover ratio has been improved in 2018 as compared to 2017. However, though the

financial leverage ratios have been improved in 2018, very high debt portion is indicating that

the company is highly leveraged. Hence, it is recommended that for improving the liquidity

position the company it shall tight the credit period allowed to its customers and make the

payment of dues within the allowed credit period. Further, to improve the debt position, the

entity shall raise additional fund, if required through equity and not through borrowing.

Financial leverage ratio – it represents the leverage position of the company that is the

proportion of debt and equity it its capital structure. Debt ratio represents the proportion of

assets raised through debt financing. Debt ratio of the company has been improved in 2018 as

compared to 2017 as the ratio is reduced from 0.86 to 0.77 (Chen et al., 2014). On the other

hand, debt equity ratio represents the debt and equity portion of the capital structure of the

entity. Generally, the ratio of 0.50 represents that the company is well balanced. Though the

debt equity ratio of the entity has been improved from 6.15 to 3.29, significantly high debt

equity ratio is indicating that the company is highly leveraged (Tesco plc, 2019).

Conclusion and recommendation

Based on the above discussion and interpretation of the financial performance of

Tesco Plc, it can be concluded that financial management is an important aspect in context of

making various major financial decisions. Further, through financial management future cash

flows of the entity can be projected by assessing the financial statements. Financial

statements deliver information regarding the financial performances, position of the entity

and delivers wide range of useful information to the users including management, employees,

government, suppliers and investors. Looking into the financial performance of Tesco Plc for

the year ended 2017 and 2018 it can be stated that the liquidity position of the company is not

good enough to meet its short term obligations. On the other hand, profitability ratios and

turnover ratio has been improved in 2018 as compared to 2017. However, though the

financial leverage ratios have been improved in 2018, very high debt portion is indicating that

the company is highly leveraged. Hence, it is recommended that for improving the liquidity

position the company it shall tight the credit period allowed to its customers and make the

payment of dues within the allowed credit period. Further, to improve the debt position, the

entity shall raise additional fund, if required through equity and not through borrowing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

11FINANCIAL MANAGEMENT

Reference

Andreou, P. C., Louca, C., & Panayides, P. M. (2014). Corporate governance, financial

management decisions and firm performance: Evidence from the maritime

industry. Transportation Research Part E: Logistics and Transportation Review, 63,

59-78.

Baños-Caballero, S., García-Teruel, P. J., & Martínez-Solano, P. (2014). Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), 332-338.

Bekaert, G., & Hodrick, R. (2017). International financial management. Cambridge

University Press.

Chen, R. R., Chidambaran, N. K., Imerman, M. B., & Sopranzetti, B. J. (2014). Liquidity,

leverage, and Lehman: A structural analysis of financial institutions in crisis. Journal

of Banking & Finance, 45, 117-139.

Cornwall, J. R., Vang, D. O., & Hartman, J. M. (2016). Entrepreneurial financial

management: An applied approach. Routledge.

Dudin, M., Lyasnikov, N., Yahyaev, M., & Kuznecov, A. (2014). The organization

approaches peculiarities of an industrial enterprises financial management. Life

Science Journal, 11(9), 333-336.

Ehiedu, V. C. (2014). The impact of liquidity on profitability of some selected companies: the

financial statement analysis (FSA) approach. Research Journal of Finance and

Accounting, 5(5), 81-90.

Reference

Andreou, P. C., Louca, C., & Panayides, P. M. (2014). Corporate governance, financial

management decisions and firm performance: Evidence from the maritime

industry. Transportation Research Part E: Logistics and Transportation Review, 63,

59-78.

Baños-Caballero, S., García-Teruel, P. J., & Martínez-Solano, P. (2014). Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), 332-338.

Bekaert, G., & Hodrick, R. (2017). International financial management. Cambridge

University Press.

Chen, R. R., Chidambaran, N. K., Imerman, M. B., & Sopranzetti, B. J. (2014). Liquidity,

leverage, and Lehman: A structural analysis of financial institutions in crisis. Journal

of Banking & Finance, 45, 117-139.

Cornwall, J. R., Vang, D. O., & Hartman, J. M. (2016). Entrepreneurial financial

management: An applied approach. Routledge.

Dudin, M., Lyasnikov, N., Yahyaev, M., & Kuznecov, A. (2014). The organization

approaches peculiarities of an industrial enterprises financial management. Life

Science Journal, 11(9), 333-336.

Ehiedu, V. C. (2014). The impact of liquidity on profitability of some selected companies: the

financial statement analysis (FSA) approach. Research Journal of Finance and

Accounting, 5(5), 81-90.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.