Comprehensive Financial Ratio Analysis Report on Tesco PLC

VerifiedAdded on 2023/06/14

|16

|2660

|120

Report

AI Summary

This report provides a comprehensive financial ratio analysis of Tesco PLC from 2019 to 2021, evaluating the company's liquidity, profitability, leverage, and working capital. The analysis includes calculations and interpretations of key ratios such as current ratio, quick ratio, cash ratio, gross margin, operating margin, pre-tax margin, net profit margin, return on equity, return on assets, debt-to-equity ratio, debt-to-capital ratio, equity multiplier, and accounts receivable days. The report identifies areas of strength and weakness in Tesco's financial performance, noting the stability of gross profitability and the fluctuations in other key metrics. Based on the analysis, recommendations are provided for improving budgetary control mechanisms and overall financial management.

Introduction to Managing

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

EXECUTIVE SUMMARY.................................................................................................................................3

INTRODUCTION...........................................................................................................................................4

MAIN BODY.................................................................................................................................................4

Ratio Analysis...........................................................................................................................................4

Results of Ratio Analysis..........................................................................................................................6

Recommendations.................................................................................................................................12

CONCLUSION.............................................................................................................................................12

REFERENCES..............................................................................................................................................13

APPENDIX..................................................................................................................................................14

EXECUTIVE SUMMARY.................................................................................................................................3

INTRODUCTION...........................................................................................................................................4

MAIN BODY.................................................................................................................................................4

Ratio Analysis...........................................................................................................................................4

Results of Ratio Analysis..........................................................................................................................6

Recommendations.................................................................................................................................12

CONCLUSION.............................................................................................................................................12

REFERENCES..............................................................................................................................................13

APPENDIX..................................................................................................................................................14

EXECUTIVE SUMMARY

Trading, banking, trading, spending, investing, and anticipating are all examples of financial

management. Financial management is the act of overseeing business earnings in such a manner

that it remains lucrative and adhering to all relevant legislation. This first need a high-level plan

as well as on execution. Any company wishing to expand must employ cash in such a way that

the dividend payments surpass the cost of borrowing. This report based on the Tesco plc which is

leading organisation of retail sector in United Kingdom. In this report analysis the ratio of the

company in order to know the actual financial situation in proper manner and get better results in

regard investments. This ratio analysis present company effective position in effective manner.

Trading, banking, trading, spending, investing, and anticipating are all examples of financial

management. Financial management is the act of overseeing business earnings in such a manner

that it remains lucrative and adhering to all relevant legislation. This first need a high-level plan

as well as on execution. Any company wishing to expand must employ cash in such a way that

the dividend payments surpass the cost of borrowing. This report based on the Tesco plc which is

leading organisation of retail sector in United Kingdom. In this report analysis the ratio of the

company in order to know the actual financial situation in proper manner and get better results in

regard investments. This ratio analysis present company effective position in effective manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Tesco plc, based in Welwyn Garden City, England, is a British - based grocery and

consumer products store. It is the third largest retail in terms of revenues earnings and indeed the

ninth-largest in terms of revenue growth. Jack Cohen created Tesco PLC in 1919 in London,

England. Cohen started selling food from a modest booth after coming from the war, making a

profit of £1 on sales revenue of £4. Tesco has been one of the nation's biggest supermarkets,

working approximately 530,000 employees and supplying millions of consumers every week

across 14 countries. Tesco's Core Aim is to work with each other to improve what important. It's

loyal to their origins, but it's much more applicable to present era and the type of firm they like

being. The main objective to analysis financial performance of company in 2019 to 2021 by the

ratio analysis. Along with present all the data information in regard of ratio analysis with charts

and identify the problems by the ratio. At the end of the report provide appropriate

recommendations for the effective changes in business.

MAIN BODY

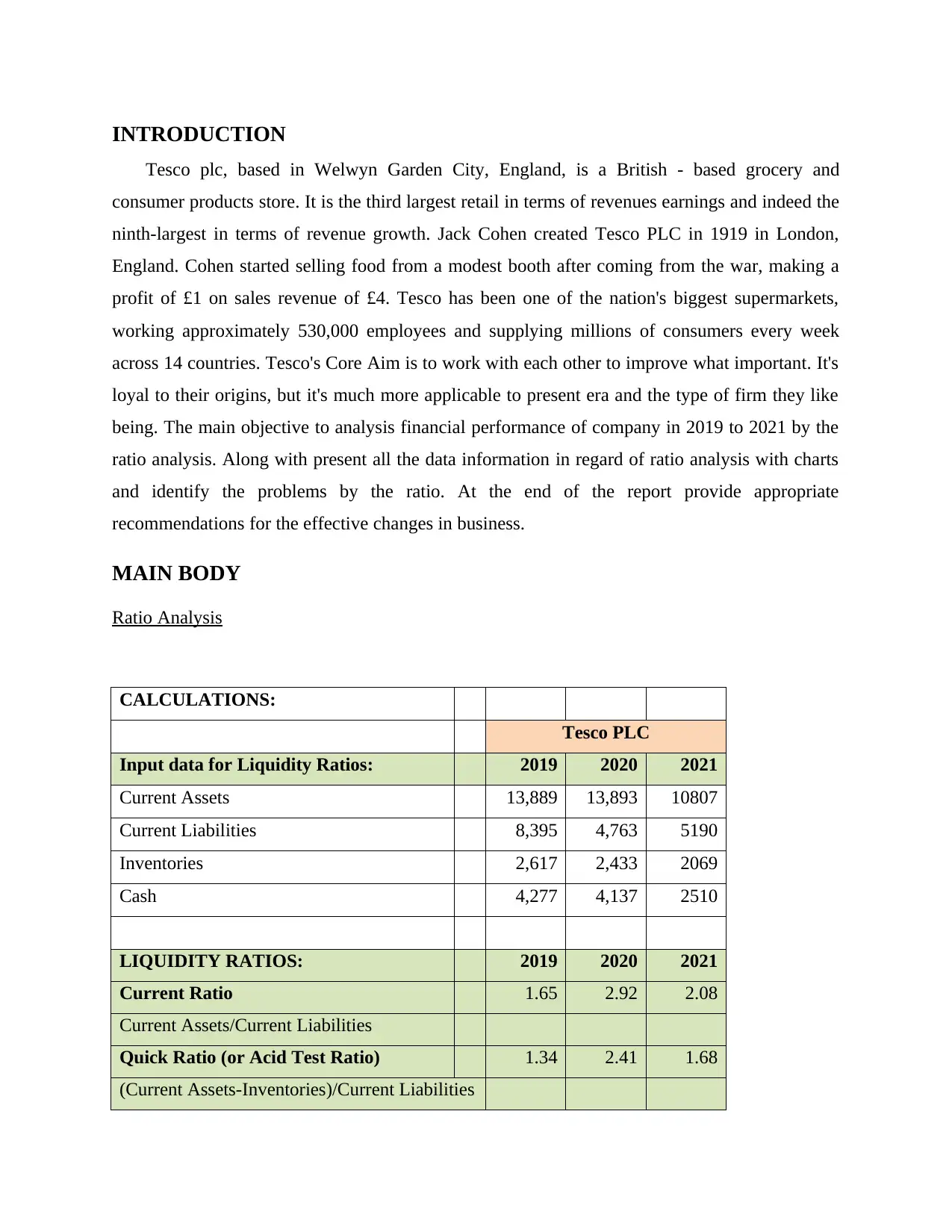

Ratio Analysis

CALCULATIONS:

Tesco PLC

Input data for Liquidity Ratios: 2019 2020 2021

Current Assets 13,889 13,893 10807

Current Liabilities 8,395 4,763 5190

Inventories 2,617 2,433 2069

Cash 4,277 4,137 2510

LIQUIDITY RATIOS: 2019 2020 2021

Current Ratio 1.65 2.92 2.08

Current Assets/Current Liabilities

Quick Ratio (or Acid Test Ratio) 1.34 2.41 1.68

(Current Assets-Inventories)/Current Liabilities

Tesco plc, based in Welwyn Garden City, England, is a British - based grocery and

consumer products store. It is the third largest retail in terms of revenues earnings and indeed the

ninth-largest in terms of revenue growth. Jack Cohen created Tesco PLC in 1919 in London,

England. Cohen started selling food from a modest booth after coming from the war, making a

profit of £1 on sales revenue of £4. Tesco has been one of the nation's biggest supermarkets,

working approximately 530,000 employees and supplying millions of consumers every week

across 14 countries. Tesco's Core Aim is to work with each other to improve what important. It's

loyal to their origins, but it's much more applicable to present era and the type of firm they like

being. The main objective to analysis financial performance of company in 2019 to 2021 by the

ratio analysis. Along with present all the data information in regard of ratio analysis with charts

and identify the problems by the ratio. At the end of the report provide appropriate

recommendations for the effective changes in business.

MAIN BODY

Ratio Analysis

CALCULATIONS:

Tesco PLC

Input data for Liquidity Ratios: 2019 2020 2021

Current Assets 13,889 13,893 10807

Current Liabilities 8,395 4,763 5190

Inventories 2,617 2,433 2069

Cash 4,277 4,137 2510

LIQUIDITY RATIOS: 2019 2020 2021

Current Ratio 1.65 2.92 2.08

Current Assets/Current Liabilities

Quick Ratio (or Acid Test Ratio) 1.34 2.41 1.68

(Current Assets-Inventories)/Current Liabilities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash Ratio 0.51 0.87 0.48

Cash/Current Liabilities

Tesco PLC

Input data for Profitability Ratios: 2019 2020 2021

Gross Profit 4,696 4,098 3965

Operating Income 2,649 2,206 1736

Pre Tax Income 1,617 1,028 825

Net Income 1,270 973 6147

Sales 63,911 58,091 57887

Total Equity 13,548 13,369 12325

Total Assets 58,325 53,147 45,778

PROFITABILITY RATIOS: 2019 2020 2021

Gross Margin 0.07 0.07 0.07

Gross Profit/Sales

Operating Margin 0.04 0.04 0.03

Operating Income/Sales

PreTax Margin 0.03 0.02 0.01

PreTax Income/Sales

Net Profit Margin 0.02 0.02 0.11

Net Income/Sales

Return on Equity (ROE) 0.09 0.07 0.50

Net Income/Tot.Equity

Return on Assets (ROA) 0.02 0.02 0.13

Net Income/Tot.Assets

LEVERAGE RATIOS Input: 2019 2020 2021

Total Debt 44,777 39,778 33,453

Total Equity 13,548 13,369 12325

Total Assets 58,325 53,147 45,778

Cash/Current Liabilities

Tesco PLC

Input data for Profitability Ratios: 2019 2020 2021

Gross Profit 4,696 4,098 3965

Operating Income 2,649 2,206 1736

Pre Tax Income 1,617 1,028 825

Net Income 1,270 973 6147

Sales 63,911 58,091 57887

Total Equity 13,548 13,369 12325

Total Assets 58,325 53,147 45,778

PROFITABILITY RATIOS: 2019 2020 2021

Gross Margin 0.07 0.07 0.07

Gross Profit/Sales

Operating Margin 0.04 0.04 0.03

Operating Income/Sales

PreTax Margin 0.03 0.02 0.01

PreTax Income/Sales

Net Profit Margin 0.02 0.02 0.11

Net Income/Sales

Return on Equity (ROE) 0.09 0.07 0.50

Net Income/Tot.Equity

Return on Assets (ROA) 0.02 0.02 0.13

Net Income/Tot.Assets

LEVERAGE RATIOS Input: 2019 2020 2021

Total Debt 44,777 39,778 33,453

Total Equity 13,548 13,369 12325

Total Assets 58,325 53,147 45,778

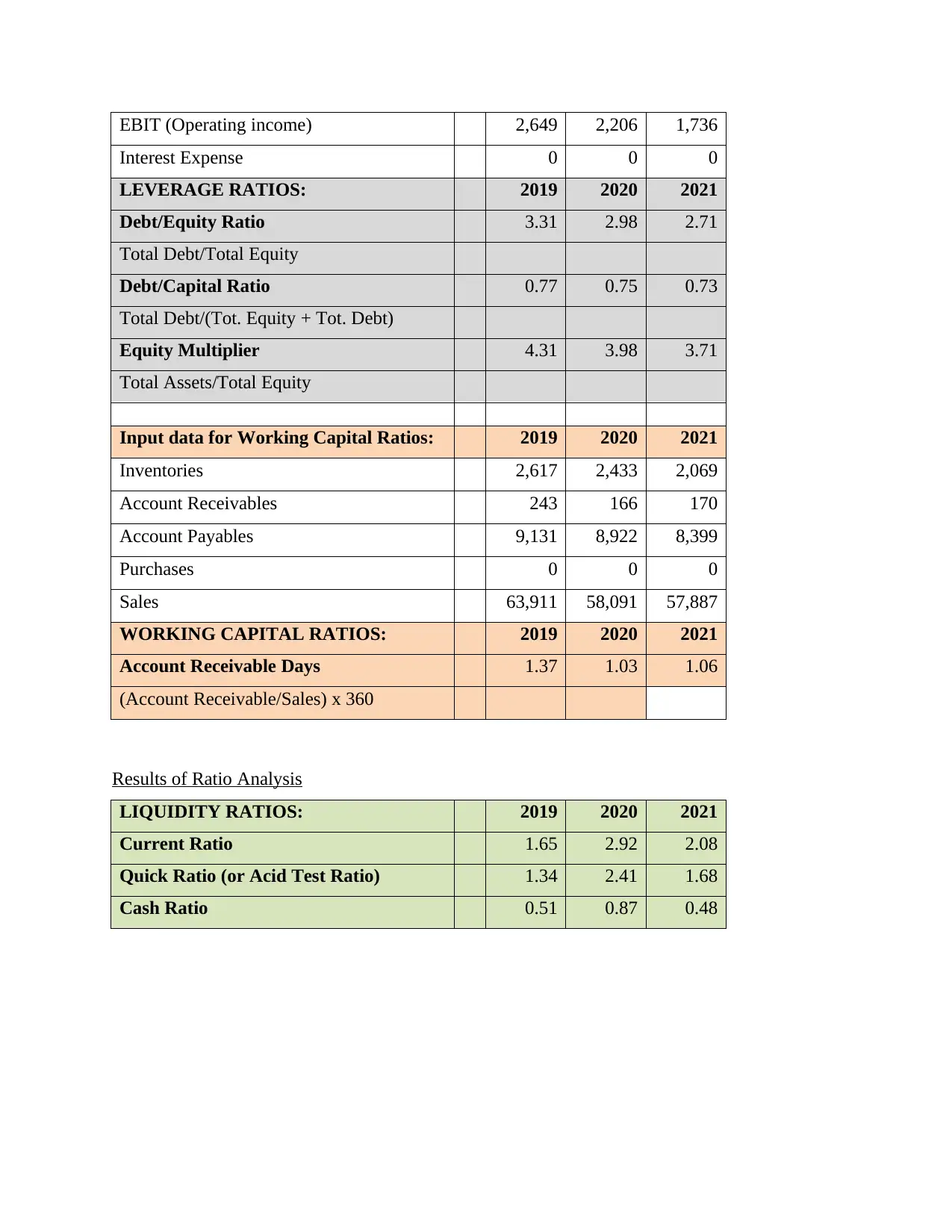

EBIT (Operating income) 2,649 2,206 1,736

Interest Expense 0 0 0

LEVERAGE RATIOS: 2019 2020 2021

Debt/Equity Ratio 3.31 2.98 2.71

Total Debt/Total Equity

Debt/Capital Ratio 0.77 0.75 0.73

Total Debt/(Tot. Equity + Tot. Debt)

Equity Multiplier 4.31 3.98 3.71

Total Assets/Total Equity

Input data for Working Capital Ratios: 2019 2020 2021

Inventories 2,617 2,433 2,069

Account Receivables 243 166 170

Account Payables 9,131 8,922 8,399

Purchases 0 0 0

Sales 63,911 58,091 57,887

WORKING CAPITAL RATIOS: 2019 2020 2021

Account Receivable Days 1.37 1.03 1.06

(Account Receivable/Sales) x 360

Results of Ratio Analysis

LIQUIDITY RATIOS: 2019 2020 2021

Current Ratio 1.65 2.92 2.08

Quick Ratio (or Acid Test Ratio) 1.34 2.41 1.68

Cash Ratio 0.51 0.87 0.48

Interest Expense 0 0 0

LEVERAGE RATIOS: 2019 2020 2021

Debt/Equity Ratio 3.31 2.98 2.71

Total Debt/Total Equity

Debt/Capital Ratio 0.77 0.75 0.73

Total Debt/(Tot. Equity + Tot. Debt)

Equity Multiplier 4.31 3.98 3.71

Total Assets/Total Equity

Input data for Working Capital Ratios: 2019 2020 2021

Inventories 2,617 2,433 2,069

Account Receivables 243 166 170

Account Payables 9,131 8,922 8,399

Purchases 0 0 0

Sales 63,911 58,091 57,887

WORKING CAPITAL RATIOS: 2019 2020 2021

Account Receivable Days 1.37 1.03 1.06

(Account Receivable/Sales) x 360

Results of Ratio Analysis

LIQUIDITY RATIOS: 2019 2020 2021

Current Ratio 1.65 2.92 2.08

Quick Ratio (or Acid Test Ratio) 1.34 2.41 1.68

Cash Ratio 0.51 0.87 0.48

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2019 2020 2021

0

0.5

1

1.5

2

2.5

3

1.65

2.92

2.08

1.34

2.41

1.68

0.51

0.87

0.48

Current Ratio

Quick Ratio (or Acid Test

Ratio)

Cash Ratio

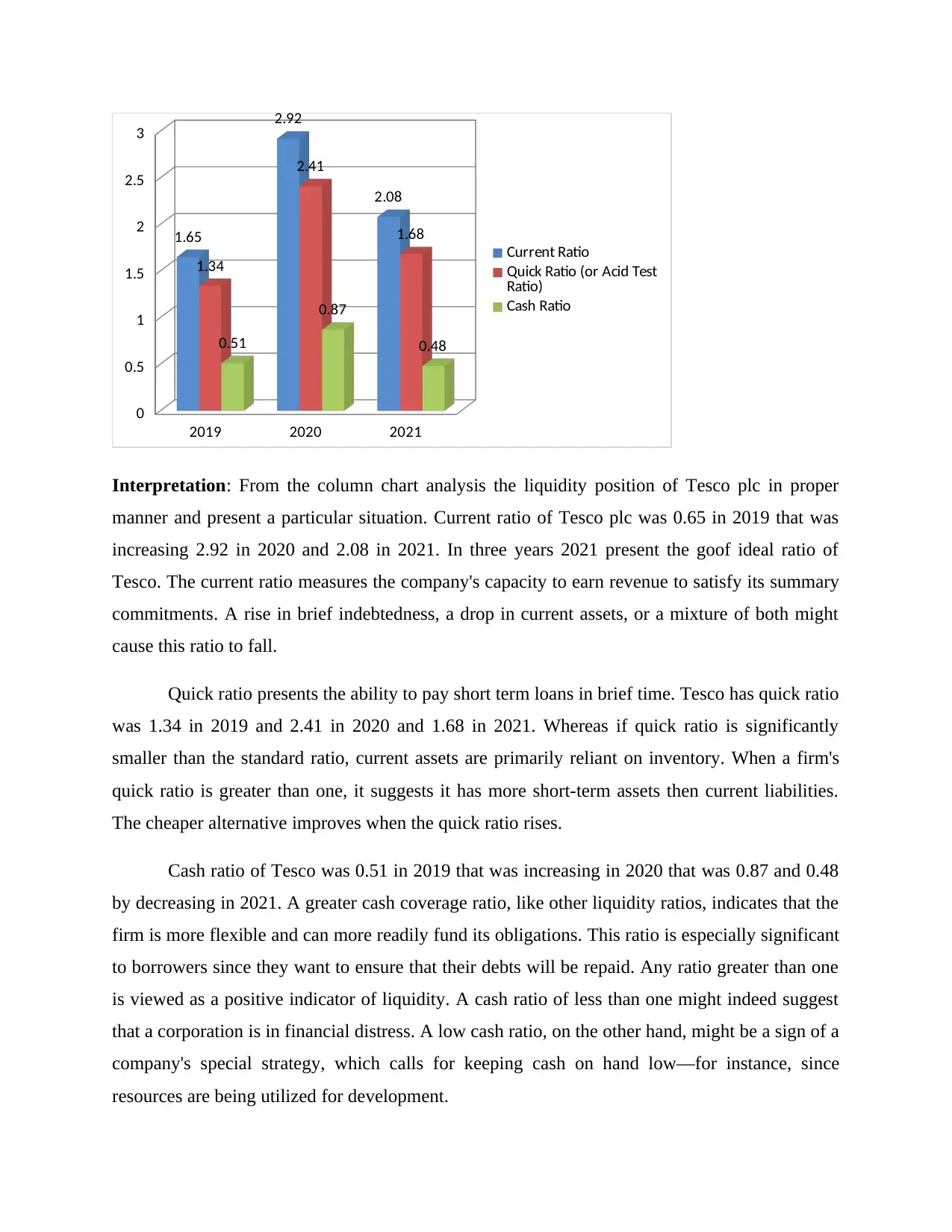

Interpretation: From the column chart analysis the liquidity position of Tesco plc in proper

manner and present a particular situation. Current ratio of Tesco plc was 0.65 in 2019 that was

increasing 2.92 in 2020 and 2.08 in 2021. In three years 2021 present the goof ideal ratio of

Tesco. The current ratio measures the company's capacity to earn revenue to satisfy its summary

commitments. A rise in brief indebtedness, a drop in current assets, or a mixture of both might

cause this ratio to fall.

Quick ratio presents the ability to pay short term loans in brief time. Tesco has quick ratio

was 1.34 in 2019 and 2.41 in 2020 and 1.68 in 2021. Whereas if quick ratio is significantly

smaller than the standard ratio, current assets are primarily reliant on inventory. When a firm's

quick ratio is greater than one, it suggests it has more short-term assets then current liabilities.

The cheaper alternative improves when the quick ratio rises.

Cash ratio of Tesco was 0.51 in 2019 that was increasing in 2020 that was 0.87 and 0.48

by decreasing in 2021. A greater cash coverage ratio, like other liquidity ratios, indicates that the

firm is more flexible and can more readily fund its obligations. This ratio is especially significant

to borrowers since they want to ensure that their debts will be repaid. Any ratio greater than one

is viewed as a positive indicator of liquidity. A cash ratio of less than one might indeed suggest

that a corporation is in financial distress. A low cash ratio, on the other hand, might be a sign of a

company's special strategy, which calls for keeping cash on hand low—for instance, since

resources are being utilized for development.

0

0.5

1

1.5

2

2.5

3

1.65

2.92

2.08

1.34

2.41

1.68

0.51

0.87

0.48

Current Ratio

Quick Ratio (or Acid Test

Ratio)

Cash Ratio

Interpretation: From the column chart analysis the liquidity position of Tesco plc in proper

manner and present a particular situation. Current ratio of Tesco plc was 0.65 in 2019 that was

increasing 2.92 in 2020 and 2.08 in 2021. In three years 2021 present the goof ideal ratio of

Tesco. The current ratio measures the company's capacity to earn revenue to satisfy its summary

commitments. A rise in brief indebtedness, a drop in current assets, or a mixture of both might

cause this ratio to fall.

Quick ratio presents the ability to pay short term loans in brief time. Tesco has quick ratio

was 1.34 in 2019 and 2.41 in 2020 and 1.68 in 2021. Whereas if quick ratio is significantly

smaller than the standard ratio, current assets are primarily reliant on inventory. When a firm's

quick ratio is greater than one, it suggests it has more short-term assets then current liabilities.

The cheaper alternative improves when the quick ratio rises.

Cash ratio of Tesco was 0.51 in 2019 that was increasing in 2020 that was 0.87 and 0.48

by decreasing in 2021. A greater cash coverage ratio, like other liquidity ratios, indicates that the

firm is more flexible and can more readily fund its obligations. This ratio is especially significant

to borrowers since they want to ensure that their debts will be repaid. Any ratio greater than one

is viewed as a positive indicator of liquidity. A cash ratio of less than one might indeed suggest

that a corporation is in financial distress. A low cash ratio, on the other hand, might be a sign of a

company's special strategy, which calls for keeping cash on hand low—for instance, since

resources are being utilized for development.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

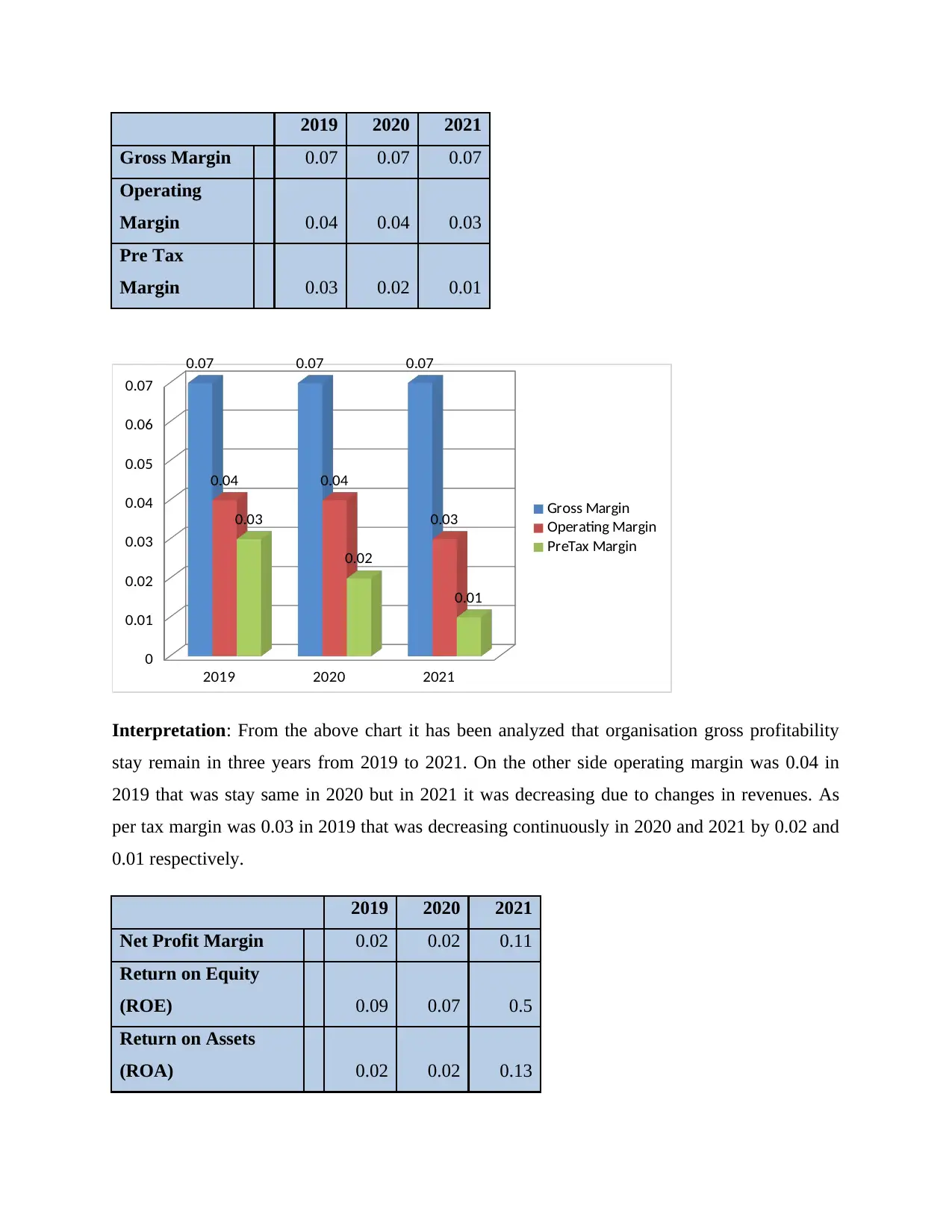

2019 2020 2021

Gross Margin 0.07 0.07 0.07

Operating

Margin 0.04 0.04 0.03

Pre Tax

Margin 0.03 0.02 0.01

2019 2020 2021

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.07 0.07 0.07

0.04 0.04

0.030.03

0.02

0.01

Gross Margin

Operating Margin

PreTax Margin

Interpretation: From the above chart it has been analyzed that organisation gross profitability

stay remain in three years from 2019 to 2021. On the other side operating margin was 0.04 in

2019 that was stay same in 2020 but in 2021 it was decreasing due to changes in revenues. As

per tax margin was 0.03 in 2019 that was decreasing continuously in 2020 and 2021 by 0.02 and

0.01 respectively.

2019 2020 2021

Net Profit Margin 0.02 0.02 0.11

Return on Equity

(ROE) 0.09 0.07 0.5

Return on Assets

(ROA) 0.02 0.02 0.13

Gross Margin 0.07 0.07 0.07

Operating

Margin 0.04 0.04 0.03

Pre Tax

Margin 0.03 0.02 0.01

2019 2020 2021

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.07 0.07 0.07

0.04 0.04

0.030.03

0.02

0.01

Gross Margin

Operating Margin

PreTax Margin

Interpretation: From the above chart it has been analyzed that organisation gross profitability

stay remain in three years from 2019 to 2021. On the other side operating margin was 0.04 in

2019 that was stay same in 2020 but in 2021 it was decreasing due to changes in revenues. As

per tax margin was 0.03 in 2019 that was decreasing continuously in 2020 and 2021 by 0.02 and

0.01 respectively.

2019 2020 2021

Net Profit Margin 0.02 0.02 0.11

Return on Equity

(ROE) 0.09 0.07 0.5

Return on Assets

(ROA) 0.02 0.02 0.13

2019 2020 2021

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

0.02 0.02

0.11

0.09 0.07

0.5

0.02 0.02

0.13

Net Profit Margin

Return on Equity (ROE)

Return on Assets (ROA)

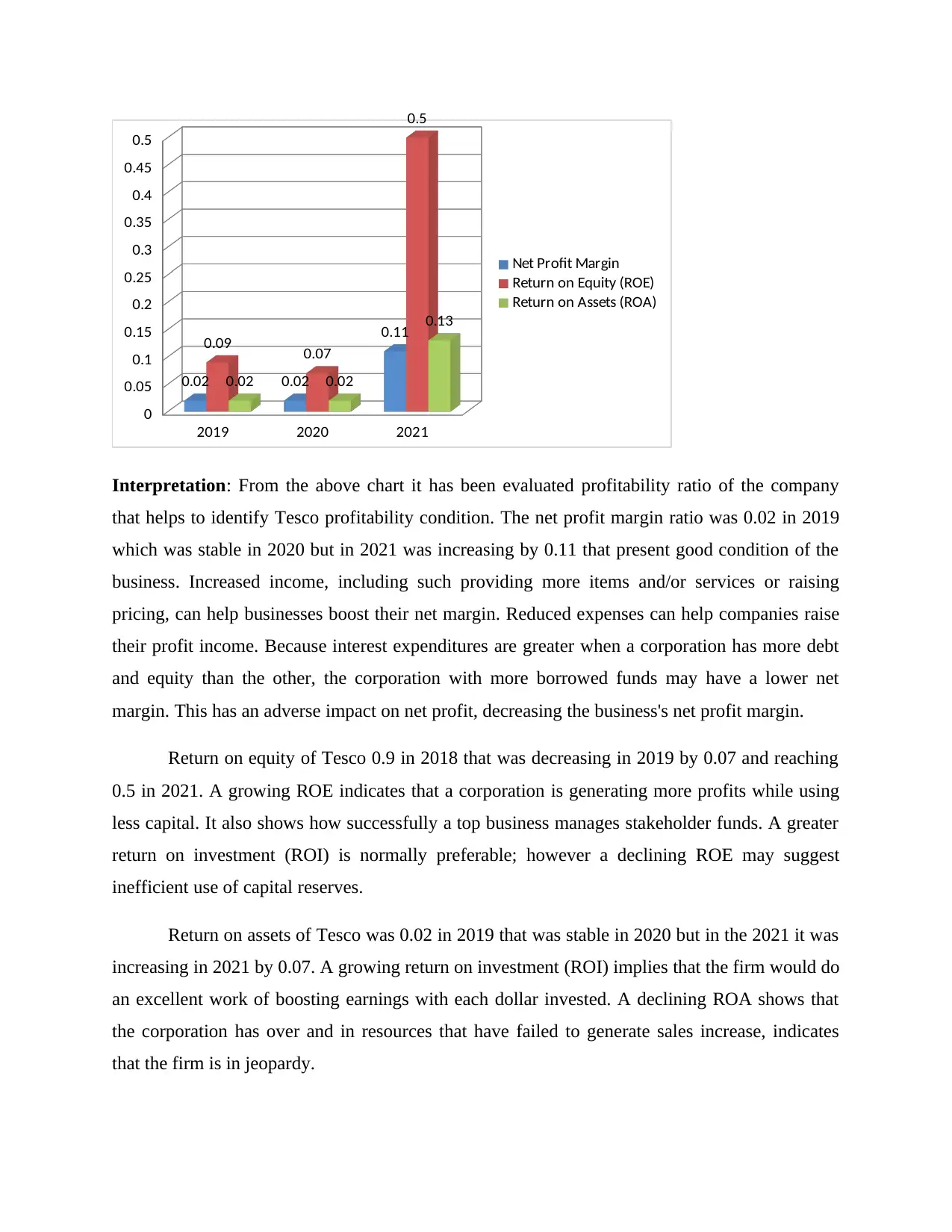

Interpretation: From the above chart it has been evaluated profitability ratio of the company

that helps to identify Tesco profitability condition. The net profit margin ratio was 0.02 in 2019

which was stable in 2020 but in 2021 was increasing by 0.11 that present good condition of the

business. Increased income, including such providing more items and/or services or raising

pricing, can help businesses boost their net margin. Reduced expenses can help companies raise

their profit income. Because interest expenditures are greater when a corporation has more debt

and equity than the other, the corporation with more borrowed funds may have a lower net

margin. This has an adverse impact on net profit, decreasing the business's net profit margin.

Return on equity of Tesco 0.9 in 2018 that was decreasing in 2019 by 0.07 and reaching

0.5 in 2021. A growing ROE indicates that a corporation is generating more profits while using

less capital. It also shows how successfully a top business manages stakeholder funds. A greater

return on investment (ROI) is normally preferable; however a declining ROE may suggest

inefficient use of capital reserves.

Return on assets of Tesco was 0.02 in 2019 that was stable in 2020 but in the 2021 it was

increasing in 2021 by 0.07. A growing return on investment (ROI) implies that the firm would do

an excellent work of boosting earnings with each dollar invested. A declining ROA shows that

the corporation has over and in resources that have failed to generate sales increase, indicates

that the firm is in jeopardy.

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

0.02 0.02

0.11

0.09 0.07

0.5

0.02 0.02

0.13

Net Profit Margin

Return on Equity (ROE)

Return on Assets (ROA)

Interpretation: From the above chart it has been evaluated profitability ratio of the company

that helps to identify Tesco profitability condition. The net profit margin ratio was 0.02 in 2019

which was stable in 2020 but in 2021 was increasing by 0.11 that present good condition of the

business. Increased income, including such providing more items and/or services or raising

pricing, can help businesses boost their net margin. Reduced expenses can help companies raise

their profit income. Because interest expenditures are greater when a corporation has more debt

and equity than the other, the corporation with more borrowed funds may have a lower net

margin. This has an adverse impact on net profit, decreasing the business's net profit margin.

Return on equity of Tesco 0.9 in 2018 that was decreasing in 2019 by 0.07 and reaching

0.5 in 2021. A growing ROE indicates that a corporation is generating more profits while using

less capital. It also shows how successfully a top business manages stakeholder funds. A greater

return on investment (ROI) is normally preferable; however a declining ROE may suggest

inefficient use of capital reserves.

Return on assets of Tesco was 0.02 in 2019 that was stable in 2020 but in the 2021 it was

increasing in 2021 by 0.07. A growing return on investment (ROI) implies that the firm would do

an excellent work of boosting earnings with each dollar invested. A declining ROA shows that

the corporation has over and in resources that have failed to generate sales increase, indicates

that the firm is in jeopardy.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

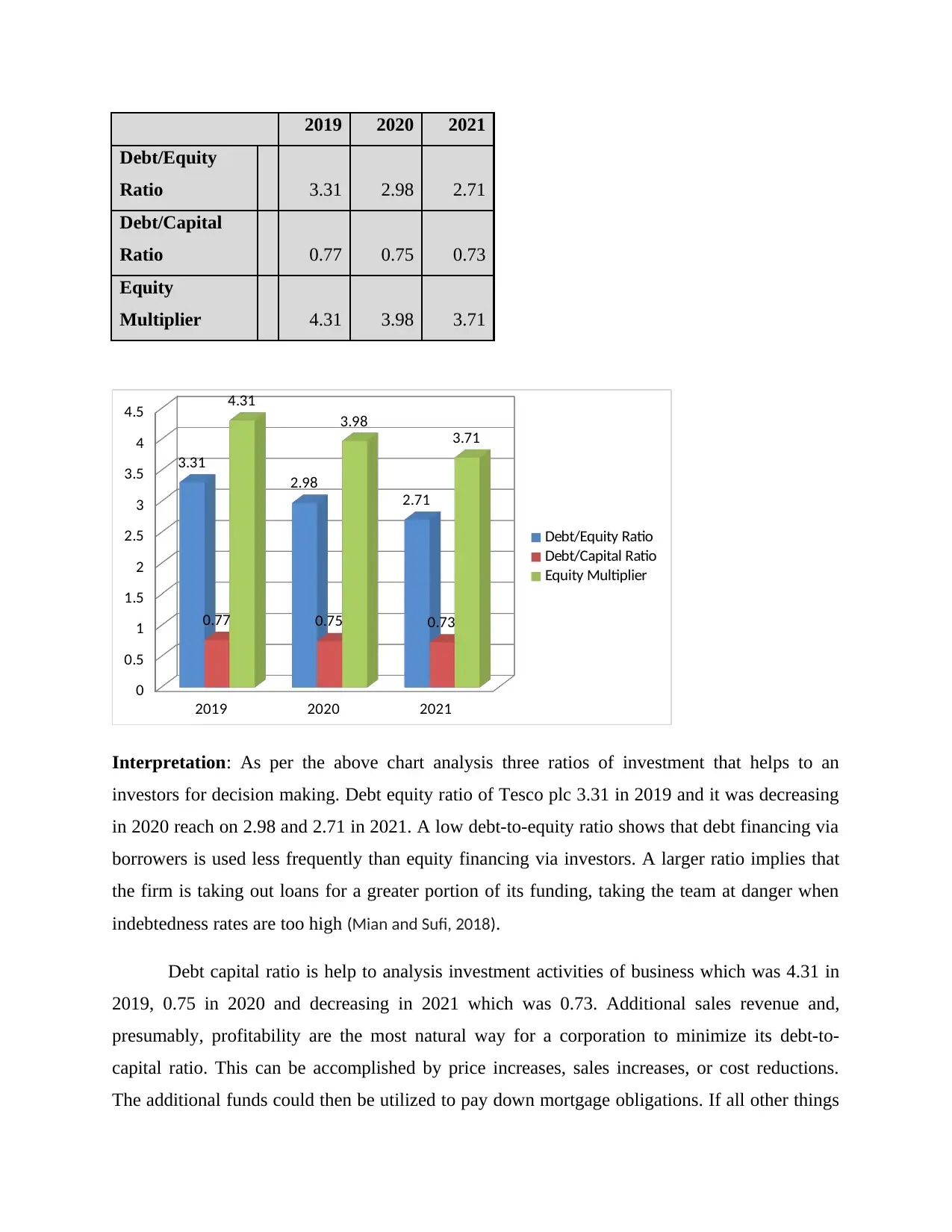

2019 2020 2021

Debt/Equity

Ratio 3.31 2.98 2.71

Debt/Capital

Ratio 0.77 0.75 0.73

Equity

Multiplier 4.31 3.98 3.71

2019 2020 2021

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

3.31

2.98

2.71

0.77 0.75 0.73

4.31

3.98

3.71

Debt/Equity Ratio

Debt/Capital Ratio

Equity Multiplier

Interpretation: As per the above chart analysis three ratios of investment that helps to an

investors for decision making. Debt equity ratio of Tesco plc 3.31 in 2019 and it was decreasing

in 2020 reach on 2.98 and 2.71 in 2021. A low debt-to-equity ratio shows that debt financing via

borrowers is used less frequently than equity financing via investors. A larger ratio implies that

the firm is taking out loans for a greater portion of its funding, taking the team at danger when

indebtedness rates are too high (Mian and Sufi, 2018).

Debt capital ratio is help to analysis investment activities of business which was 4.31 in

2019, 0.75 in 2020 and decreasing in 2021 which was 0.73. Additional sales revenue and,

presumably, profitability are the most natural way for a corporation to minimize its debt-to-

capital ratio. This can be accomplished by price increases, sales increases, or cost reductions.

The additional funds could then be utilized to pay down mortgage obligations. If all other things

Debt/Equity

Ratio 3.31 2.98 2.71

Debt/Capital

Ratio 0.77 0.75 0.73

Equity

Multiplier 4.31 3.98 3.71

2019 2020 2021

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

3.31

2.98

2.71

0.77 0.75 0.73

4.31

3.98

3.71

Debt/Equity Ratio

Debt/Capital Ratio

Equity Multiplier

Interpretation: As per the above chart analysis three ratios of investment that helps to an

investors for decision making. Debt equity ratio of Tesco plc 3.31 in 2019 and it was decreasing

in 2020 reach on 2.98 and 2.71 in 2021. A low debt-to-equity ratio shows that debt financing via

borrowers is used less frequently than equity financing via investors. A larger ratio implies that

the firm is taking out loans for a greater portion of its funding, taking the team at danger when

indebtedness rates are too high (Mian and Sufi, 2018).

Debt capital ratio is help to analysis investment activities of business which was 4.31 in

2019, 0.75 in 2020 and decreasing in 2021 which was 0.73. Additional sales revenue and,

presumably, profitability are the most natural way for a corporation to minimize its debt-to-

capital ratio. This can be accomplished by price increases, sales increases, or cost reductions.

The additional funds could then be utilized to pay down mortgage obligations. If all other things

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are considered, a corporation with a greater debt-to-capital ratio is hazardous. It's because the

greater the debt-to-equity ratio, the further the firm is supported by debt rather than equity,

implying a higher obligation to pay back the debt and an increased risk of loan disgorgement

whereas if loan is not compensated.

Equity multiplier ratio was 4.31 in 2019 which was decreasing in 2020 by 3.98 and it was

decreasing by 3.71 in 2021. The equity multiplier is a metric that indicates how much of a firm's

profits are funded through shares instead of borrowing. A large equity multiplier usually suggests

that a corporation has a lot of debt. A smaller equity multiplier is preferable since it shows that

the corporation is borrowing less to purchase shares. Corporation DEF is favored over company

ABC in this situation since it owes less revenue and hence bears less hazard.

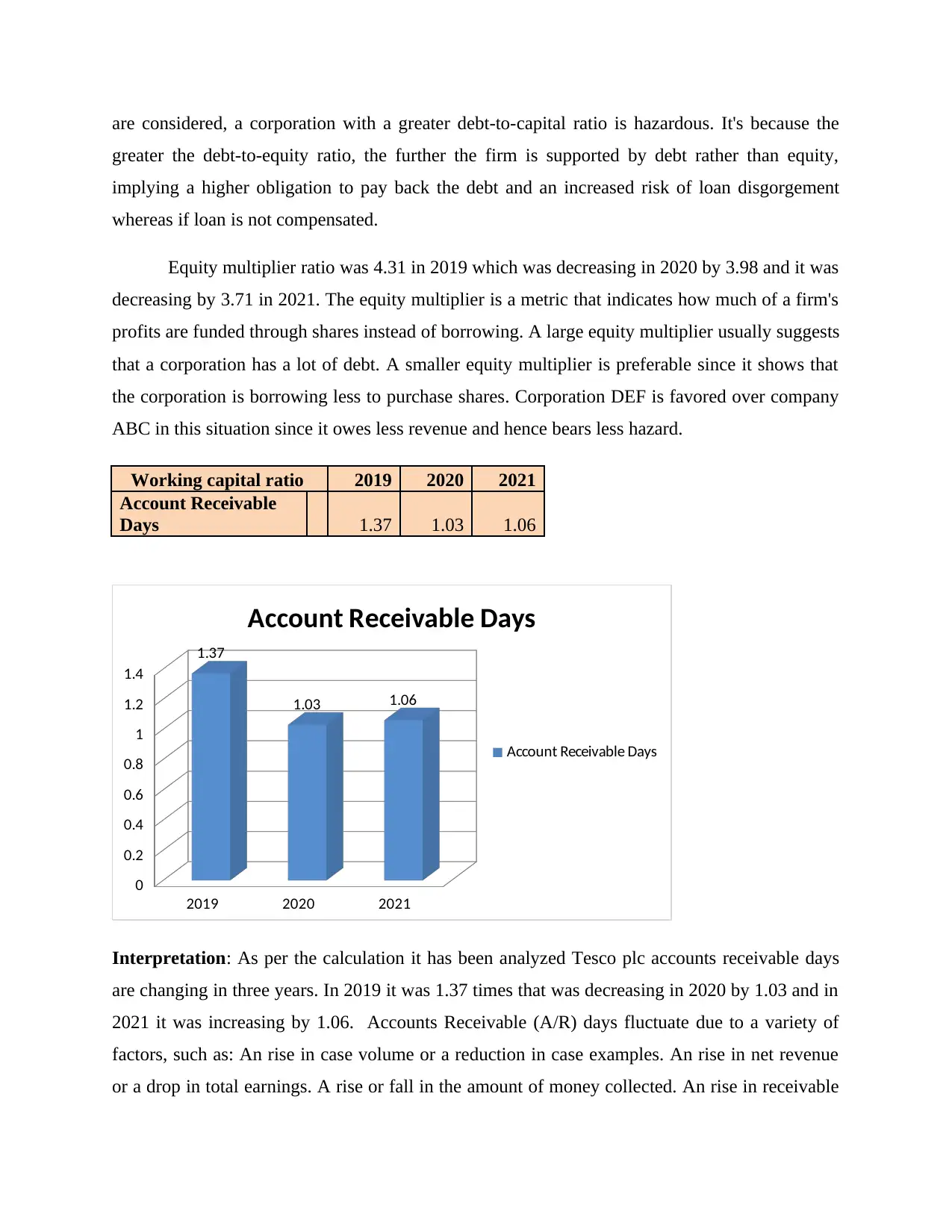

Working capital ratio 2019 2020 2021

Account Receivable

Days 1.37 1.03 1.06

2019 2020 2021

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.37

1.03 1.06

Account Receivable Days

Account Receivable Days

Interpretation: As per the calculation it has been analyzed Tesco plc accounts receivable days

are changing in three years. In 2019 it was 1.37 times that was decreasing in 2020 by 1.03 and in

2021 it was increasing by 1.06. Accounts Receivable (A/R) days fluctuate due to a variety of

factors, such as: An rise in case volume or a reduction in case examples. An rise in net revenue

or a drop in total earnings. A rise or fall in the amount of money collected. An rise in receivable

greater the debt-to-equity ratio, the further the firm is supported by debt rather than equity,

implying a higher obligation to pay back the debt and an increased risk of loan disgorgement

whereas if loan is not compensated.

Equity multiplier ratio was 4.31 in 2019 which was decreasing in 2020 by 3.98 and it was

decreasing by 3.71 in 2021. The equity multiplier is a metric that indicates how much of a firm's

profits are funded through shares instead of borrowing. A large equity multiplier usually suggests

that a corporation has a lot of debt. A smaller equity multiplier is preferable since it shows that

the corporation is borrowing less to purchase shares. Corporation DEF is favored over company

ABC in this situation since it owes less revenue and hence bears less hazard.

Working capital ratio 2019 2020 2021

Account Receivable

Days 1.37 1.03 1.06

2019 2020 2021

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.37

1.03 1.06

Account Receivable Days

Account Receivable Days

Interpretation: As per the calculation it has been analyzed Tesco plc accounts receivable days

are changing in three years. In 2019 it was 1.37 times that was decreasing in 2020 by 1.03 and in

2021 it was increasing by 1.06. Accounts Receivable (A/R) days fluctuate due to a variety of

factors, such as: An rise in case volume or a reduction in case examples. An rise in net revenue

or a drop in total earnings. A rise or fall in the amount of money collected. An rise in receivable

accounts turnover indicates that a firm is executing credits more efficiently. A decline in

accounts receivable rotation indicates that a firm is encountering more overdue customers. When

accounts receivable fell through one year to the next, it means that the firm's previous trade

receivables were recovered (i.e., sales invoices were finally transformed to cash transactions),

resulting in cash inflow (Terry, Macy, Owens and Vinyard, 2020).

Results: From the overall analysis of ratio it is identifying that Debt capital ratio and cash ratio is

lower of Tesco. Profitability ratio present good position of company and make stable position of

company. Liquidity ratio is present that current ratio is near by the deal ratio it means company

maintain their performance in effective manner.

Recommendations

• The organisation is urged to focus on the correct installation of budgetary control mechanisms.

It may enable the company to develop strategic plans for operational activity. To attain business

goals, it is necessary for a company to have an integrated design process that includes the use of

a highly appropriate budget so that data can be gathered that can be used to identify potential

stumbling blocks and opportunities. It helps users to obtain knowledge that is quite useful in

making informed decisions that allow you to achieve excellent results. Coordinating and

conducting the company's operations in a more efficient way gets conceivable.

• The company should work to reduce costs that contribute to higher depreciation and

amortization in the financial plan. As a produce, businesses must seek out options that will result

in the least amount of cash being used. They might choose clientele who are willing to pay a

higher fee for selling property.

CONCLUSION

According to the aforementioned study report, in business, money should be managed

properly since any type of mismanagement in corporate finance can result in poor business

situations. From the above analysis it is saying that Tesco has good position in retail sector and

good for the investment purpose.

accounts receivable rotation indicates that a firm is encountering more overdue customers. When

accounts receivable fell through one year to the next, it means that the firm's previous trade

receivables were recovered (i.e., sales invoices were finally transformed to cash transactions),

resulting in cash inflow (Terry, Macy, Owens and Vinyard, 2020).

Results: From the overall analysis of ratio it is identifying that Debt capital ratio and cash ratio is

lower of Tesco. Profitability ratio present good position of company and make stable position of

company. Liquidity ratio is present that current ratio is near by the deal ratio it means company

maintain their performance in effective manner.

Recommendations

• The organisation is urged to focus on the correct installation of budgetary control mechanisms.

It may enable the company to develop strategic plans for operational activity. To attain business

goals, it is necessary for a company to have an integrated design process that includes the use of

a highly appropriate budget so that data can be gathered that can be used to identify potential

stumbling blocks and opportunities. It helps users to obtain knowledge that is quite useful in

making informed decisions that allow you to achieve excellent results. Coordinating and

conducting the company's operations in a more efficient way gets conceivable.

• The company should work to reduce costs that contribute to higher depreciation and

amortization in the financial plan. As a produce, businesses must seek out options that will result

in the least amount of cash being used. They might choose clientele who are willing to pay a

higher fee for selling property.

CONCLUSION

According to the aforementioned study report, in business, money should be managed

properly since any type of mismanagement in corporate finance can result in poor business

situations. From the above analysis it is saying that Tesco has good position in retail sector and

good for the investment purpose.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.