Tesco PLC Financial Analysis - Corporate Finance Report, 2019

VerifiedAdded on 2023/04/23

|12

|3267

|80

Report

AI Summary

This report provides a comprehensive financial analysis of Tesco PLC, a British multinational grocery and merchandise retailer. It examines the pros and cons of the company being listed on the stock exchange, calculates the cost of equity using the CAPM model, and determines the intrinsic value of the share using the DCF model, comparing it with the current market value. The analysis includes a discussion of the weighted average cost of capital (WACC) and an overview of Tesco's capital structure over the past three years, highlighting the company's shift towards equity financing. The report concludes by comparing the intrinsic value derived from the DCF model with the current market share price, offering insights into the company's valuation and potential investment opportunities. Desklib provides access to similar reports and solved assignments for students.

Running Head: FINANCIAL ANALYSIS 0

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 1

Introduction

Tesco PLC is the British multinational company dealing in the groceries and general

merchandise leader having its headquarters in Welwyn Garden City, Hertfordshire. The company

was founded in the year 1919 almost around 100 years ago. The key person that founded this

company was Jack Cohen. The company is listed on the London Stock Exchange and is currently

operating in United Kingdom, Ireland, India, Malaysia, Thailand, Czech Republic and Hungary.

A total of 6569 shops are there in the year 2018. Also currently the company is operating at the

revenue of 57491 million and earing the operating income of 1644 million. This will not only

provide the investors the future earnings but also the greater opportunities. Further this report

also determines the calculation of cost of equity using the CAPM model and using the DCF

model to calculate the intrinsic value of share and further compare it with the market value of

share at the current levels. Also the pros and cons of the company being listed on the stock

exchange is also analyzed as to whether there is a necessity to list the company on the stock

exchange or not (Frank and Shen, 2016).

Pros and cons of listing on stock exchange

Stock exchange listing procedure is the procedure where a privately owned organization is

transitioned into the publically owned company whose shares can be traded on stock exchange.

There are certain benefits of listing on stock exchange and the same are outlined below (Baker,

and Wurgler, 2015).

Advantages

The main benefit of the company being listed on the stock exchange is that it assists the firm in

enhancing the brand name and thereby adding the value to the company. As well as it can add

Introduction

Tesco PLC is the British multinational company dealing in the groceries and general

merchandise leader having its headquarters in Welwyn Garden City, Hertfordshire. The company

was founded in the year 1919 almost around 100 years ago. The key person that founded this

company was Jack Cohen. The company is listed on the London Stock Exchange and is currently

operating in United Kingdom, Ireland, India, Malaysia, Thailand, Czech Republic and Hungary.

A total of 6569 shops are there in the year 2018. Also currently the company is operating at the

revenue of 57491 million and earing the operating income of 1644 million. This will not only

provide the investors the future earnings but also the greater opportunities. Further this report

also determines the calculation of cost of equity using the CAPM model and using the DCF

model to calculate the intrinsic value of share and further compare it with the market value of

share at the current levels. Also the pros and cons of the company being listed on the stock

exchange is also analyzed as to whether there is a necessity to list the company on the stock

exchange or not (Frank and Shen, 2016).

Pros and cons of listing on stock exchange

Stock exchange listing procedure is the procedure where a privately owned organization is

transitioned into the publically owned company whose shares can be traded on stock exchange.

There are certain benefits of listing on stock exchange and the same are outlined below (Baker,

and Wurgler, 2015).

Advantages

The main benefit of the company being listed on the stock exchange is that it assists the firm in

enhancing the brand name and thereby adding the value to the company. As well as it can add

FINANCIAL ANALYSIS 2

the value by implementing the scheme of the option. A listing on the stock market acts as a key

driver in opening the doors for the company Tesco with ample amount of opportunities (Pham,

and Alenikov, 2018).

Potential capital Growth

The secondary benefit of the listing the company on the stock exchange is the procurement of the

additional resources to finance the business activities and its expansion plans. For instance, if the

company wants to fund the department of the research and development the new machinery must

be purchased and the new offices must be set up. Since the company is of the public nature the

extra feature is that the company can also issue the new shares to build the extra capital (Berger,

Chen and Li, 2018.

Institutional investment

In case of the public limited company the hassle of the negotiations are not carried together as a

burden to attract the institutional investment. Through listing on the stock exchange the exposure

is enlarged in terms of the market coverage. The network gets widened including the market

makers, buyers and the sellers, institutional traders and the mutual funds (Huizinga, Voget and

Wagner, 2018).

Enhanced corporate evaluation and profile

Listing on the stock exchange helps in elevating the position of the company in terms of the

competition and garners a great amount of the publicity and the goodwill of the firm. An

elevated profile of the company will almost enlarge and create more than the existing

opportunities. This adds the element of the trust and the credibility from the successful listing.

the value by implementing the scheme of the option. A listing on the stock market acts as a key

driver in opening the doors for the company Tesco with ample amount of opportunities (Pham,

and Alenikov, 2018).

Potential capital Growth

The secondary benefit of the listing the company on the stock exchange is the procurement of the

additional resources to finance the business activities and its expansion plans. For instance, if the

company wants to fund the department of the research and development the new machinery must

be purchased and the new offices must be set up. Since the company is of the public nature the

extra feature is that the company can also issue the new shares to build the extra capital (Berger,

Chen and Li, 2018.

Institutional investment

In case of the public limited company the hassle of the negotiations are not carried together as a

burden to attract the institutional investment. Through listing on the stock exchange the exposure

is enlarged in terms of the market coverage. The network gets widened including the market

makers, buyers and the sellers, institutional traders and the mutual funds (Huizinga, Voget and

Wagner, 2018).

Enhanced corporate evaluation and profile

Listing on the stock exchange helps in elevating the position of the company in terms of the

competition and garners a great amount of the publicity and the goodwill of the firm. An

elevated profile of the company will almost enlarge and create more than the existing

opportunities. This adds the element of the trust and the credibility from the successful listing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS 3

In addition to this the company amplifies the awareness of the brands and the products and

makes the company smoother with regards to the liquidity and valuation of the company. This

projects the performance and the market perception of the said firm (Dutta and Nezlobin, 2017).

Profitable exit strategy

Going public is one of the many exit strategies for business owners as it delivers a set

mechanism for the companies to nurture themselves and expand the business. This strategy also

helps in improving the share price of the listed company and performance and selling of the same

(El Ghoul, Guedhami, Kim and Park, 2018).

Disadvantages

In response to the pros of the listing on the stock exchange there are certain drawbacks which the

company must be aware of.

Loss of control and exposed to takeovers

One of the critical demerits of the listing is that the business owners will have to have a share

with the investors and also the shareholder as well as the investors raises their voice in the

policies that are directly related with the operations of the company. The situation is such that the

CEO is also responsible to ensure the correct system of the check and balance (Eades and Eades,

2017).

Higher reporting requirements

If the company is becoming public the obligations and the reporting requirements have to be in

alignment of regulatory requirements in order to be somewhere near to corporate governance.

Since the listed companies are required to prepare the financial statements and publish reports

In addition to this the company amplifies the awareness of the brands and the products and

makes the company smoother with regards to the liquidity and valuation of the company. This

projects the performance and the market perception of the said firm (Dutta and Nezlobin, 2017).

Profitable exit strategy

Going public is one of the many exit strategies for business owners as it delivers a set

mechanism for the companies to nurture themselves and expand the business. This strategy also

helps in improving the share price of the listed company and performance and selling of the same

(El Ghoul, Guedhami, Kim and Park, 2018).

Disadvantages

In response to the pros of the listing on the stock exchange there are certain drawbacks which the

company must be aware of.

Loss of control and exposed to takeovers

One of the critical demerits of the listing is that the business owners will have to have a share

with the investors and also the shareholder as well as the investors raises their voice in the

policies that are directly related with the operations of the company. The situation is such that the

CEO is also responsible to ensure the correct system of the check and balance (Eades and Eades,

2017).

Higher reporting requirements

If the company is becoming public the obligations and the reporting requirements have to be in

alignment of regulatory requirements in order to be somewhere near to corporate governance.

Since the listed companies are required to prepare the financial statements and publish reports

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 4

consequently. The higher the level of reporting the higher will be the costs (Dhaliwal, Judd,

Serfling and Shaikh, 2016).

Accountability to public shareholders

The dilemma for the company arises when the actual trading results are not suitable as per the

expectations of the shareholders. The possibilities can be that the objectives of the company are

different from interests off the shareholders. The listing could make the business to the new

summits and providing the new path for the opportunities for future growth. Therefore at times

the accountability to public shareholders becomes critical and crucial from the point of view of

the company (Gambacorta, and Shin, 2018).

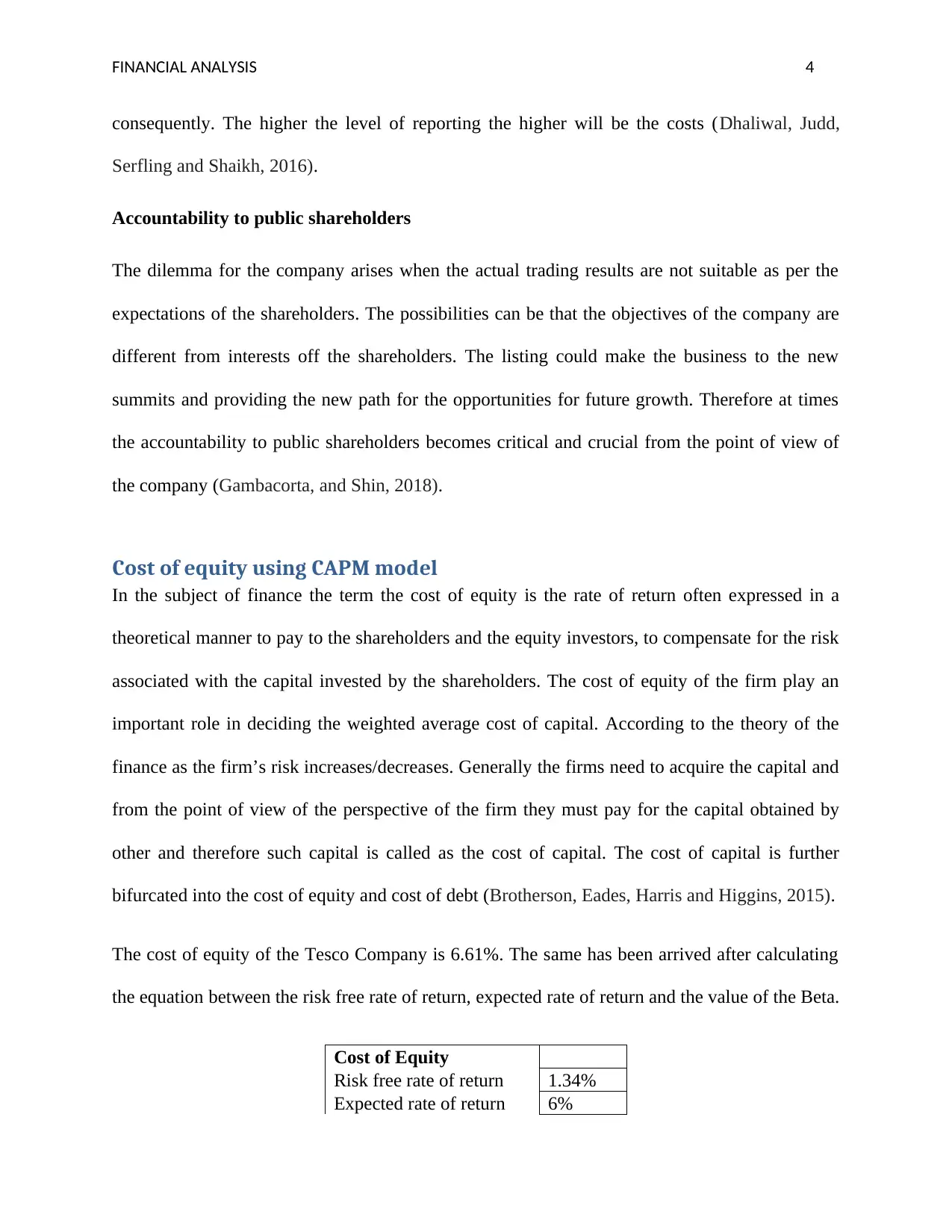

Cost of equity using CAPM model

In the subject of finance the term the cost of equity is the rate of return often expressed in a

theoretical manner to pay to the shareholders and the equity investors, to compensate for the risk

associated with the capital invested by the shareholders. The cost of equity of the firm play an

important role in deciding the weighted average cost of capital. According to the theory of the

finance as the firm’s risk increases/decreases. Generally the firms need to acquire the capital and

from the point of view of the perspective of the firm they must pay for the capital obtained by

other and therefore such capital is called as the cost of capital. The cost of capital is further

bifurcated into the cost of equity and cost of debt (Brotherson, Eades, Harris and Higgins, 2015).

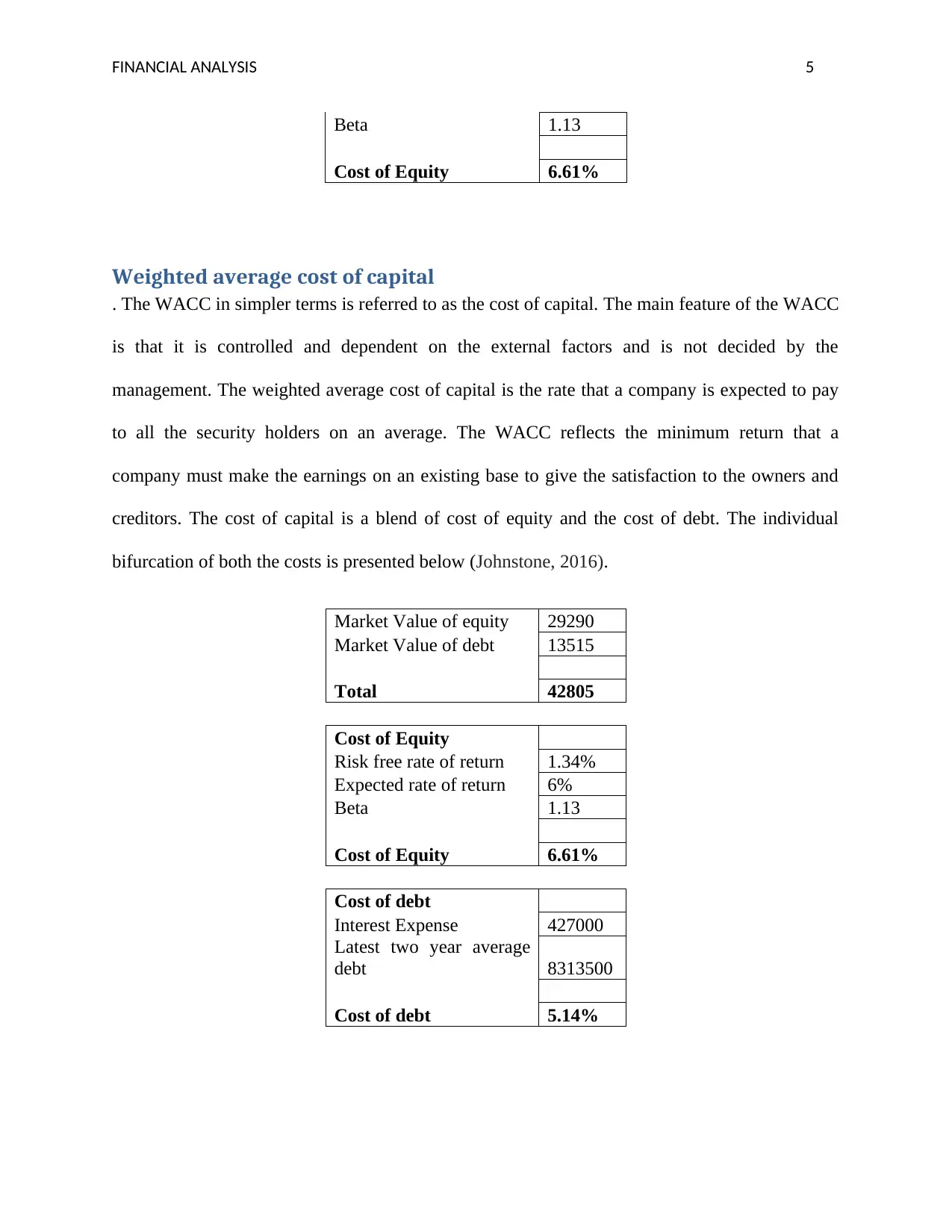

The cost of equity of the Tesco Company is 6.61%. The same has been arrived after calculating

the equation between the risk free rate of return, expected rate of return and the value of the Beta.

Cost of Equity

Risk free rate of return 1.34%

Expected rate of return 6%

consequently. The higher the level of reporting the higher will be the costs (Dhaliwal, Judd,

Serfling and Shaikh, 2016).

Accountability to public shareholders

The dilemma for the company arises when the actual trading results are not suitable as per the

expectations of the shareholders. The possibilities can be that the objectives of the company are

different from interests off the shareholders. The listing could make the business to the new

summits and providing the new path for the opportunities for future growth. Therefore at times

the accountability to public shareholders becomes critical and crucial from the point of view of

the company (Gambacorta, and Shin, 2018).

Cost of equity using CAPM model

In the subject of finance the term the cost of equity is the rate of return often expressed in a

theoretical manner to pay to the shareholders and the equity investors, to compensate for the risk

associated with the capital invested by the shareholders. The cost of equity of the firm play an

important role in deciding the weighted average cost of capital. According to the theory of the

finance as the firm’s risk increases/decreases. Generally the firms need to acquire the capital and

from the point of view of the perspective of the firm they must pay for the capital obtained by

other and therefore such capital is called as the cost of capital. The cost of capital is further

bifurcated into the cost of equity and cost of debt (Brotherson, Eades, Harris and Higgins, 2015).

The cost of equity of the Tesco Company is 6.61%. The same has been arrived after calculating

the equation between the risk free rate of return, expected rate of return and the value of the Beta.

Cost of Equity

Risk free rate of return 1.34%

Expected rate of return 6%

FINANCIAL ANALYSIS 5

Beta 1.13

Cost of Equity 6.61%

Weighted average cost of capital

. The WACC in simpler terms is referred to as the cost of capital. The main feature of the WACC

is that it is controlled and dependent on the external factors and is not decided by the

management. The weighted average cost of capital is the rate that a company is expected to pay

to all the security holders on an average. The WACC reflects the minimum return that a

company must make the earnings on an existing base to give the satisfaction to the owners and

creditors. The cost of capital is a blend of cost of equity and the cost of debt. The individual

bifurcation of both the costs is presented below (Johnstone, 2016).

Market Value of equity 29290

Market Value of debt 13515

Total 42805

Cost of Equity

Risk free rate of return 1.34%

Expected rate of return 6%

Beta 1.13

Cost of Equity 6.61%

Cost of debt

Interest Expense 427000

Latest two year average

debt 8313500

Cost of debt 5.14%

Beta 1.13

Cost of Equity 6.61%

Weighted average cost of capital

. The WACC in simpler terms is referred to as the cost of capital. The main feature of the WACC

is that it is controlled and dependent on the external factors and is not decided by the

management. The weighted average cost of capital is the rate that a company is expected to pay

to all the security holders on an average. The WACC reflects the minimum return that a

company must make the earnings on an existing base to give the satisfaction to the owners and

creditors. The cost of capital is a blend of cost of equity and the cost of debt. The individual

bifurcation of both the costs is presented below (Johnstone, 2016).

Market Value of equity 29290

Market Value of debt 13515

Total 42805

Cost of Equity

Risk free rate of return 1.34%

Expected rate of return 6%

Beta 1.13

Cost of Equity 6.61%

Cost of debt

Interest Expense 427000

Latest two year average

debt 8313500

Cost of debt 5.14%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS 6

The cost of equity is 6.16% and the cost of debt is 5.14%. In order to reduce the cost of capital

the company must reduce the debt financing. In terms of the debt financing the company must

focus on reducing the interest rate and in terms of the equity financing the Tesco can offer the

stock which are having low beta as it is less risky to the investors and can offer a less risk

premium. The other elements the risk free premium and the market risk of general nature are

beyond the control of the company (Brusov, Filatova, Orekhova and Eskindarov, 2018).

Capital structure

The capital structure over the past three years of the Tesco Company can be observed form the

table. The capital structure of the Tesco Company reflects that the company has the mixed

choices of the debt as well as the equity. Earlier in the year 2016 the debt component was 55%

whereas the equity component was 45% of the total cost capital. The same increased to 60% in

the successive year in terms of the debt and the in terms of the equity it turned out to be 40%.

Thereafter the company realized that the debt financing has increased which in results into

increase in the cost of capital hence the Tesco followed the new strategy of financing more

towards the equity rather than the debt. Thereafter the ratio of the debt to the equity became 41%

and 59% respectively (Hirth and Steckel, 2016).

The cost of equity is 6.16% and the cost of debt is 5.14%. In order to reduce the cost of capital

the company must reduce the debt financing. In terms of the debt financing the company must

focus on reducing the interest rate and in terms of the equity financing the Tesco can offer the

stock which are having low beta as it is less risky to the investors and can offer a less risk

premium. The other elements the risk free premium and the market risk of general nature are

beyond the control of the company (Brusov, Filatova, Orekhova and Eskindarov, 2018).

Capital structure

The capital structure over the past three years of the Tesco Company can be observed form the

table. The capital structure of the Tesco Company reflects that the company has the mixed

choices of the debt as well as the equity. Earlier in the year 2016 the debt component was 55%

whereas the equity component was 45% of the total cost capital. The same increased to 60% in

the successive year in terms of the debt and the in terms of the equity it turned out to be 40%.

Thereafter the company realized that the debt financing has increased which in results into

increase in the cost of capital hence the Tesco followed the new strategy of financing more

towards the equity rather than the debt. Thereafter the ratio of the debt to the equity became 41%

and 59% respectively (Hirth and Steckel, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 7

Capital Structure of Tesco

2016 Weights 2017

Weight

s 2018 Weights

Debt 10711 55% 9433 60% 7142 41%

Equity 8616 45% 6414 40% 10458 59%

19327 100% 15847 100% 17600 100%

Discounted cash flow model

The valuation technique which is used to estimate the value of an investment based on the future

cash flows. A present value estimate is then used to evaluate a potential investment. If after the

calculation the value that is arrived is greater than the cost of investment, the opportunity shall be

considered wisely. The main purpose of calculation through the DCF model is to estimate the

money an investor would receive from the funds invested by him. The major feature associated

with the DCF valuation is the consideration of the concept of the time value of money (Othieno

and Biekpe, 2019). According to the theory of the time value of money the worth of the dollar at

present is more than the worth of the dollar in future. Though there are certain benefits to the

Tesco as it truly captures the underlying fundamental drivers of the business. Unlike the other

valuation methods used to calculate the intrinsic price of the shares the DCF model makes use of

the free cash flows. Since the cash flows are used the possibility of the window dressing and the

elimination of the subjective accounting policies are considered as the reliable measures (Hafner

and Berlin, 2017).

Apart from this the DCF model is explicitly considers the key challenges and the business

strategies in the valuation of the price which otherwise are not considered in the other models.

Also when the entire sector is overvalued or undervalued the credibility as well as well as the

reliability of the other methods reduces. Instead of estimating the fair intrinsic value, the current

share price of the company can be plugged into the model and working backwards, DCF model

Capital Structure of Tesco

2016 Weights 2017

Weight

s 2018 Weights

Debt 10711 55% 9433 60% 7142 41%

Equity 8616 45% 6414 40% 10458 59%

19327 100% 15847 100% 17600 100%

Discounted cash flow model

The valuation technique which is used to estimate the value of an investment based on the future

cash flows. A present value estimate is then used to evaluate a potential investment. If after the

calculation the value that is arrived is greater than the cost of investment, the opportunity shall be

considered wisely. The main purpose of calculation through the DCF model is to estimate the

money an investor would receive from the funds invested by him. The major feature associated

with the DCF valuation is the consideration of the concept of the time value of money (Othieno

and Biekpe, 2019). According to the theory of the time value of money the worth of the dollar at

present is more than the worth of the dollar in future. Though there are certain benefits to the

Tesco as it truly captures the underlying fundamental drivers of the business. Unlike the other

valuation methods used to calculate the intrinsic price of the shares the DCF model makes use of

the free cash flows. Since the cash flows are used the possibility of the window dressing and the

elimination of the subjective accounting policies are considered as the reliable measures (Hafner

and Berlin, 2017).

Apart from this the DCF model is explicitly considers the key challenges and the business

strategies in the valuation of the price which otherwise are not considered in the other models.

Also when the entire sector is overvalued or undervalued the credibility as well as well as the

reliability of the other methods reduces. Instead of estimating the fair intrinsic value, the current

share price of the company can be plugged into the model and working backwards, DCF model

FINANCIAL ANALYSIS 8

will tell how much the stock moves and in what direction. In contrast to the advantages there are

certain disadvantages that can hamper the performance of the Tesco while using such model for

valuation. The major demerit of this method is it works best only when there is a greater degree

of confidence of cash flows (Alshomaly, Masa’deh and AqabaBranch, 2018). Thus, DCF

strategy is defenseless to mistake and is prone to the errors if the accounting is not done in the

proper manner (Lie, Meng, Qian and Zhou, 2017).

Comparison

The share price of the Tesco at the current levels is 228.80, whereas in comparison to the DCF

model the share price of the Tesco is 192.33. If the intrinsic value of the company is lower than

the share price of the company than it indicates that the share is overvalued. The strategy of the

investors is that they tend to buy the less stock of the same company. However the other factors

are also taken into consideration. It does not necessarily means that the stock must be avoided.

The disparity between the intrinsic value and the current market price allows the company to

examine the price to book value ratio (Larocque, Lawrence and Veenstra, 2018). The goal of any

investor is to purchase low and sell high amount of the stocks and if an investor considers the

analysis and reaches to the conclusion that the stock will have the future benefits and will have

higher market price in comparison to the current value than the investors are advised to hold the

shares. For the purpose of the long term and the after analyzing the movements of the stock price

over the period of the regular years than the investors are advised to keep a check on the regular

basis. Since the stock is overvalued it and the trends suggest that Tesco will share future earnings

the investors must take care and hold the shares until the grand opportunity knocks their doors.

Also the fact is such that this mind set will allow the company to perform in a better manner

(Sorensen and Jagannathan, 2015).

will tell how much the stock moves and in what direction. In contrast to the advantages there are

certain disadvantages that can hamper the performance of the Tesco while using such model for

valuation. The major demerit of this method is it works best only when there is a greater degree

of confidence of cash flows (Alshomaly, Masa’deh and AqabaBranch, 2018). Thus, DCF

strategy is defenseless to mistake and is prone to the errors if the accounting is not done in the

proper manner (Lie, Meng, Qian and Zhou, 2017).

Comparison

The share price of the Tesco at the current levels is 228.80, whereas in comparison to the DCF

model the share price of the Tesco is 192.33. If the intrinsic value of the company is lower than

the share price of the company than it indicates that the share is overvalued. The strategy of the

investors is that they tend to buy the less stock of the same company. However the other factors

are also taken into consideration. It does not necessarily means that the stock must be avoided.

The disparity between the intrinsic value and the current market price allows the company to

examine the price to book value ratio (Larocque, Lawrence and Veenstra, 2018). The goal of any

investor is to purchase low and sell high amount of the stocks and if an investor considers the

analysis and reaches to the conclusion that the stock will have the future benefits and will have

higher market price in comparison to the current value than the investors are advised to hold the

shares. For the purpose of the long term and the after analyzing the movements of the stock price

over the period of the regular years than the investors are advised to keep a check on the regular

basis. Since the stock is overvalued it and the trends suggest that Tesco will share future earnings

the investors must take care and hold the shares until the grand opportunity knocks their doors.

Also the fact is such that this mind set will allow the company to perform in a better manner

(Sorensen and Jagannathan, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS 9

Conclusion

From the above analysis it can be concluded that the WACC and the cost of capital are the core

factors in taking the decision from the point of view of the investors. Since the investors invest

their funds in the market it becomes a necessity to deliver the best returns to the company.

Moreover the valuation of the stock was done on the basis of the DCF model and hence the

investors are recommended to keep the stocks on hold. Further the concept of the WACC is the

as described above is the concept of the two categories and hence the Tesco is required to create

a balance between debt and equity according to the existing capital structure and strategies.

Conclusion

From the above analysis it can be concluded that the WACC and the cost of capital are the core

factors in taking the decision from the point of view of the investors. Since the investors invest

their funds in the market it becomes a necessity to deliver the best returns to the company.

Moreover the valuation of the stock was done on the basis of the DCF model and hence the

investors are recommended to keep the stocks on hold. Further the concept of the WACC is the

as described above is the concept of the two categories and hence the Tesco is required to create

a balance between debt and equity according to the existing capital structure and strategies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 10

References

Alshomaly, I., Masa’deh, R.E. and AqabaBranch, J., 2018. The Capital Assets Pricing Model &

Arbitrage Pricing Theory: Properties and Applications in Jordan. Modern Applied

Science, 12(11).

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic Review, 105(5),

pp.315-20.

Berger, P.G., Chen, H.J. and Li, F., 2018. Firm specific information and the cost of equity

capital. Feng, Firm Specific Information and the Cost of Equity Capital (April 2, 2018).

Brotherson, W.T., Eades, K.M., Harris, R.S. and Higgins, R.C., 2015. 'Best Practices' in

Estimating the Cost of Capital: An Update.

Brusov, P., Filatova, T., Orekhova, N. and Eskindarov, M., 2018. New meaningful effects in

modern capital structure theory. In Modern Corporate Finance, Investments, Taxation and

Ratings (pp. 537-568). Springer, Cham.

Dhaliwal, D., Judd, J.S., Serfling, M. and Shaikh, S., 2016. Customer concentration risk and the

cost of equity capital. Journal of Accounting and Economics, 61(1), pp.23-48.

Dutta, S. and Nezlobin, A., 2017. Information disclosure, firm growth, and the cost of

capital. Journal of Financial Economics, 123(2), pp.415-431.

Eades, K.M. and Eades, K.M., 2017. Procter and Gamble: Cost of Capital. Darden Business

Publishing Cases, pp.1-16.

El Ghoul, S., Guedhami, O., Kim, H. and Park, K., 2018. Corporate environmental responsibility

and the cost of capital: International evidence. Journal of Business Ethics, 149(2), pp.335-361.

Frank, M.Z. and Shen, T., 2016. Investment and the weighted average cost of capital. Journal of

Financial Economics, 119(2), pp.300-315.

Gambacorta, L. and Shin, H.S., 2018. Why bank capital matters for monetary policy. Journal of

Financial Intermediation, 35, pp.17-29.

Hafner, R. and Berlin, H.T.W., 2017. Implied Equity Risk Premium for Germany in January

2017. Hochschule für Technik und Wirtschaft Berlin.

Hirth, L. and Steckel, J.C., 2016. The role of capital costs in decarbonizing the electricity

sector. Environmental Research Letters, 11(11), p.114010.

References

Alshomaly, I., Masa’deh, R.E. and AqabaBranch, J., 2018. The Capital Assets Pricing Model &

Arbitrage Pricing Theory: Properties and Applications in Jordan. Modern Applied

Science, 12(11).

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic Review, 105(5),

pp.315-20.

Berger, P.G., Chen, H.J. and Li, F., 2018. Firm specific information and the cost of equity

capital. Feng, Firm Specific Information and the Cost of Equity Capital (April 2, 2018).

Brotherson, W.T., Eades, K.M., Harris, R.S. and Higgins, R.C., 2015. 'Best Practices' in

Estimating the Cost of Capital: An Update.

Brusov, P., Filatova, T., Orekhova, N. and Eskindarov, M., 2018. New meaningful effects in

modern capital structure theory. In Modern Corporate Finance, Investments, Taxation and

Ratings (pp. 537-568). Springer, Cham.

Dhaliwal, D., Judd, J.S., Serfling, M. and Shaikh, S., 2016. Customer concentration risk and the

cost of equity capital. Journal of Accounting and Economics, 61(1), pp.23-48.

Dutta, S. and Nezlobin, A., 2017. Information disclosure, firm growth, and the cost of

capital. Journal of Financial Economics, 123(2), pp.415-431.

Eades, K.M. and Eades, K.M., 2017. Procter and Gamble: Cost of Capital. Darden Business

Publishing Cases, pp.1-16.

El Ghoul, S., Guedhami, O., Kim, H. and Park, K., 2018. Corporate environmental responsibility

and the cost of capital: International evidence. Journal of Business Ethics, 149(2), pp.335-361.

Frank, M.Z. and Shen, T., 2016. Investment and the weighted average cost of capital. Journal of

Financial Economics, 119(2), pp.300-315.

Gambacorta, L. and Shin, H.S., 2018. Why bank capital matters for monetary policy. Journal of

Financial Intermediation, 35, pp.17-29.

Hafner, R. and Berlin, H.T.W., 2017. Implied Equity Risk Premium for Germany in January

2017. Hochschule für Technik und Wirtschaft Berlin.

Hirth, L. and Steckel, J.C., 2016. The role of capital costs in decarbonizing the electricity

sector. Environmental Research Letters, 11(11), p.114010.

FINANCIAL ANALYSIS 11

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

Johnstone, D., 2016. The effect of information on uncertainty and the cost of

capital. Contemporary Accounting Research, 33(2), pp.752-774.

Larocque, S., Lawrence, A. and Veenstra, K., 2018. Managers’ cost of equity capital estimates:

empirical evidence. Journal of Accounting, Auditing & Finance, 33(3), pp.382-401.

Lie, E., Meng, B., Qian, Y. and Zhou, G., 2017. Corporate activities and the market risk

premium.

Othieno, F. and Biekpe, N., 2019. Estimating the conditional equity risk premium in African

frontier markets. Research in International Business and Finance, 47, pp.538-551.

Pham, T.N.B. and Alenikov, T., 2018. The importance of Weighted Average Cost of Capital in

investment decision-making for investors of corporations in the healthcare industry.

Sorensen, M. and Jagannathan, R., 2015. The public market equivalent and private equity

performance. Financial Analysts Journal, 71(4), pp.43-50.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

Johnstone, D., 2016. The effect of information on uncertainty and the cost of

capital. Contemporary Accounting Research, 33(2), pp.752-774.

Larocque, S., Lawrence, A. and Veenstra, K., 2018. Managers’ cost of equity capital estimates:

empirical evidence. Journal of Accounting, Auditing & Finance, 33(3), pp.382-401.

Lie, E., Meng, B., Qian, Y. and Zhou, G., 2017. Corporate activities and the market risk

premium.

Othieno, F. and Biekpe, N., 2019. Estimating the conditional equity risk premium in African

frontier markets. Research in International Business and Finance, 47, pp.538-551.

Pham, T.N.B. and Alenikov, T., 2018. The importance of Weighted Average Cost of Capital in

investment decision-making for investors of corporations in the healthcare industry.

Sorensen, M. and Jagannathan, R., 2015. The public market equivalent and private equity

performance. Financial Analysts Journal, 71(4), pp.43-50.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.