Managerial Finance Report: Comparative Analysis of Tesco and Sainsbury

VerifiedAdded on 2022/12/30

|16

|3852

|27

Report

AI Summary

This report offers a comprehensive financial analysis of two major retail companies, Tesco and Sainsbury. It begins with an introduction to managerial finance, outlining its importance in planning, organizing, and controlling financial activities. The report then delves into a detailed ratio analysis of both companies for the years 2018 and 2019, covering key financial ratios such as current ratio, liquidity ratio, gross profit margin, price-earning ratio, net profit margin, earnings per share, dividend payout ratio, inventory turnover ratio, capital gearing ratio, and return on capital employed. Each ratio is explained, calculated, and interpreted, with comparisons made between the two companies to assess their relative financial performance and identify strengths and weaknesses. The analysis includes graphical representations of key ratios. The report concludes with recommendations based on the findings and discusses the limitations of ratio analysis. Furthermore, it explores investment appraisal techniques and their limitations, providing a well-rounded view of the financial health and strategic considerations for both companies.

MANAGERIAL

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PORTFOLIO 1.................................................................................................................................1

Ratio analysis of both company for the year 2018 and 2019 ......................................................1

Recommendation.........................................................................................................................9

Limitation of the ratio analysis ...................................................................................................9

PORTFOLIO 2...............................................................................................................................10

Investment appraisal techniques ...............................................................................................10

Limitations of investment appraisal techniques:........................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION...........................................................................................................................1

PORTFOLIO 1.................................................................................................................................1

Ratio analysis of both company for the year 2018 and 2019 ......................................................1

Recommendation.........................................................................................................................9

Limitation of the ratio analysis ...................................................................................................9

PORTFOLIO 2...............................................................................................................................10

Investment appraisal techniques ...............................................................................................10

Limitations of investment appraisal techniques:........................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION

Managerial finance means the method use for the collecting the funds and managing

them according to the day to day activities which is used in other department for carry the

regular activities in the finance activity. It is about planning, organising, analysing, monitoring

and controlling the financial techniques for the better utilization of the resources. In simple terms

there is the use of the manager for manage the activities of the entity to accomplishment of the

business objectives and goal. In this report there is two company is selected which are Tesco and

Sinsburry. Tesco is the largest British Multinational retail based company which is found in

1919, their headquarter is located in UK. And second one is Sainsbury which has largest number

of the market chain in the retail sector (Atanasova, Gatev and Shapiro, 2016). It was founded in

1922, in which headquarter is located in London. In this report there are various topics are

covered such as ratio analysis of both company and limitation of the ratio analysis. Apart from

these limitations of the investment appraisal techniques for the given project.

PORTFOLIO 1

Ratio analysis of both company for the year 2018 and 2019

In context to Sainsbury

Basic Formulas Results for 2018 Results for 2019

Current ratio

Current assets / current

liabilities

7857/10302

=0.73:1

7550 /11849

=0.63:1

Liquid / quick ratio

Quick assets / current

liabilities

1933/10302

=0.19

1283 /11849

=0.19

Gross profit Ratio Gross profit / total sales

518/28456

=0.018%

601 /29007

=0.02%

P/E ratio

Market value per share /

Earnings per share

238.80/0.22

=10.85

213.40/46

=4.64

Net profit Ratio Net profit / total sales

309/28456

=0.11%

186/29007

=0.006%

Earnings per share Income available / total 22 46

1

Managerial finance means the method use for the collecting the funds and managing

them according to the day to day activities which is used in other department for carry the

regular activities in the finance activity. It is about planning, organising, analysing, monitoring

and controlling the financial techniques for the better utilization of the resources. In simple terms

there is the use of the manager for manage the activities of the entity to accomplishment of the

business objectives and goal. In this report there is two company is selected which are Tesco and

Sinsburry. Tesco is the largest British Multinational retail based company which is found in

1919, their headquarter is located in UK. And second one is Sainsbury which has largest number

of the market chain in the retail sector (Atanasova, Gatev and Shapiro, 2016). It was founded in

1922, in which headquarter is located in London. In this report there are various topics are

covered such as ratio analysis of both company and limitation of the ratio analysis. Apart from

these limitations of the investment appraisal techniques for the given project.

PORTFOLIO 1

Ratio analysis of both company for the year 2018 and 2019

In context to Sainsbury

Basic Formulas Results for 2018 Results for 2019

Current ratio

Current assets / current

liabilities

7857/10302

=0.73:1

7550 /11849

=0.63:1

Liquid / quick ratio

Quick assets / current

liabilities

1933/10302

=0.19

1283 /11849

=0.19

Gross profit Ratio Gross profit / total sales

518/28456

=0.018%

601 /29007

=0.02%

P/E ratio

Market value per share /

Earnings per share

238.80/0.22

=10.85

213.40/46

=4.64

Net profit Ratio Net profit / total sales

309/28456

=0.11%

186/29007

=0.006%

Earnings per share Income available / total 22 46

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

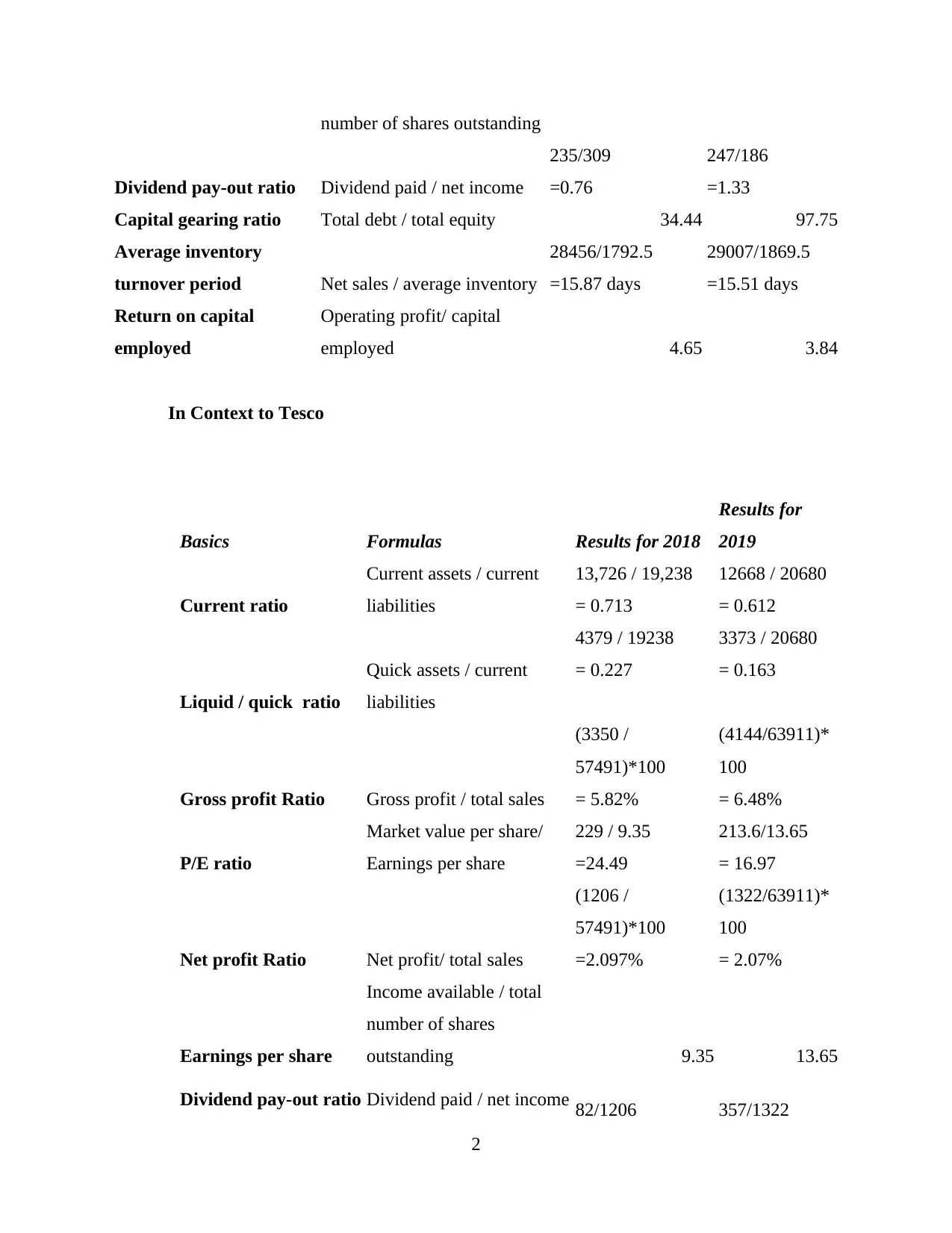

number of shares outstanding

Dividend pay-out ratio Dividend paid / net income

235/309

=0.76

247/186

=1.33

Capital gearing ratio Total debt / total equity 34.44 97.75

Average inventory

turnover period Net sales / average inventory

28456/1792.5

=15.87 days

29007/1869.5

=15.51 days

Return on capital

employed

Operating profit/ capital

employed 4.65 3.84

In Context to Tesco

Basics Formulas Results for 2018

Results for

2019

Current ratio

Current assets / current

liabilities

13,726 / 19,238

= 0.713

12668 / 20680

= 0.612

Liquid / quick ratio

Quick assets / current

liabilities

4379 / 19238

= 0.227

3373 / 20680

= 0.163

Gross profit Ratio Gross profit / total sales

(3350 /

57491)*100

= 5.82%

(4144/63911)*

100

= 6.48%

P/E ratio

Market value per share/

Earnings per share

229 / 9.35

=24.49

213.6/13.65

= 16.97

Net profit Ratio Net profit/ total sales

(1206 /

57491)*100

=2.097%

(1322/63911)*

100

= 2.07%

Earnings per share

Income available / total

number of shares

outstanding 9.35 13.65

Dividend pay-out ratio Dividend paid / net income 82/1206 357/1322

2

Dividend pay-out ratio Dividend paid / net income

235/309

=0.76

247/186

=1.33

Capital gearing ratio Total debt / total equity 34.44 97.75

Average inventory

turnover period Net sales / average inventory

28456/1792.5

=15.87 days

29007/1869.5

=15.51 days

Return on capital

employed

Operating profit/ capital

employed 4.65 3.84

In Context to Tesco

Basics Formulas Results for 2018

Results for

2019

Current ratio

Current assets / current

liabilities

13,726 / 19,238

= 0.713

12668 / 20680

= 0.612

Liquid / quick ratio

Quick assets / current

liabilities

4379 / 19238

= 0.227

3373 / 20680

= 0.163

Gross profit Ratio Gross profit / total sales

(3350 /

57491)*100

= 5.82%

(4144/63911)*

100

= 6.48%

P/E ratio

Market value per share/

Earnings per share

229 / 9.35

=24.49

213.6/13.65

= 16.97

Net profit Ratio Net profit/ total sales

(1206 /

57491)*100

=2.097%

(1322/63911)*

100

= 2.07%

Earnings per share

Income available / total

number of shares

outstanding 9.35 13.65

Dividend pay-out ratio Dividend paid / net income 82/1206 357/1322

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 0.68 = 0.27

Average inventory

turnover period

Net sales / average

inventory

57491/2282.5

= 25.91 days

63911/2240.5

= 28.52 days

Capital gearing ratio Total debt / total equity

44862/10480

= 4.280%

49047 / 14858

= 3.301%

Return on capital

employed

Operating profit/ capital

employed 5.13 6.86

Ratio interpretation

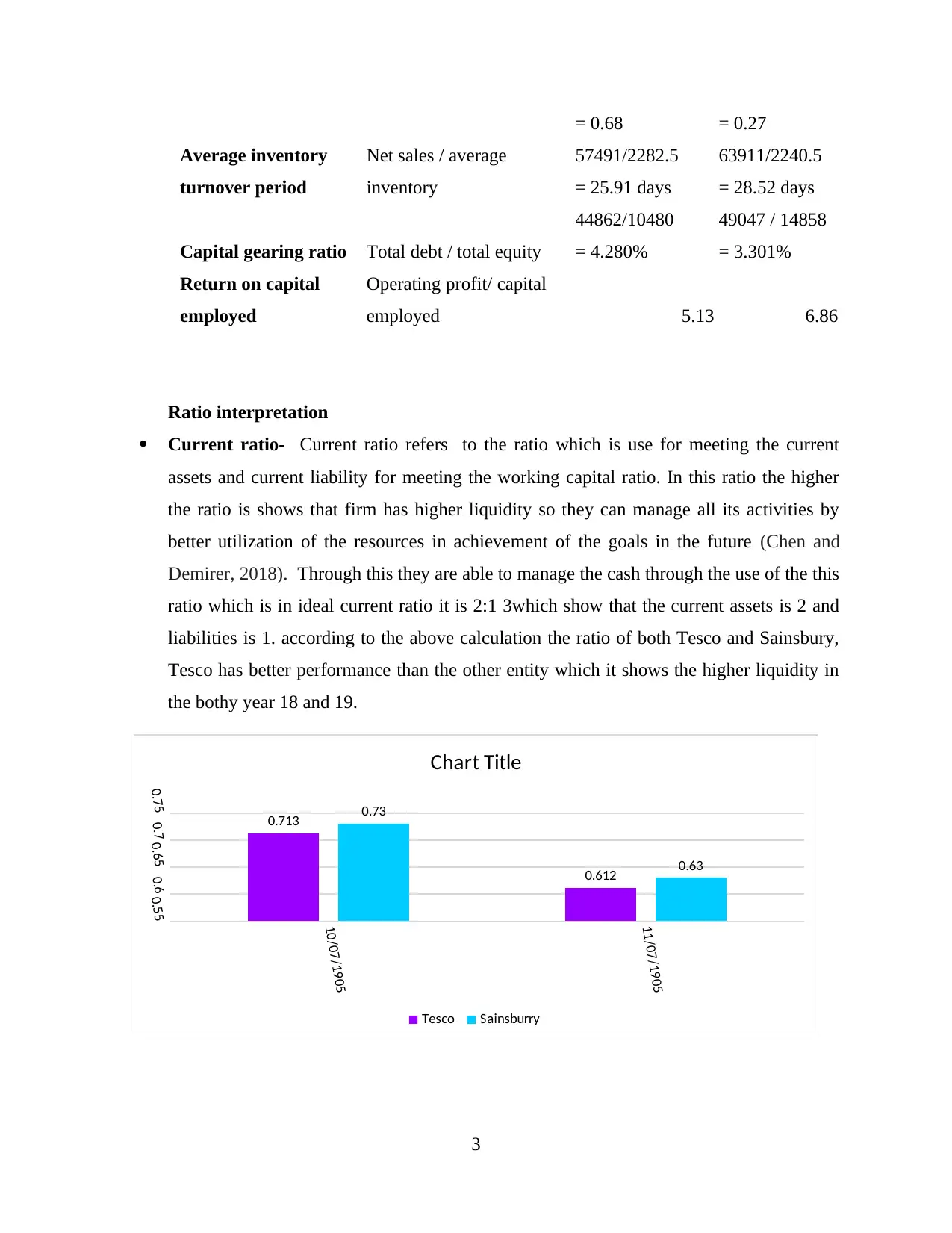

Current ratio- Current ratio refers to the ratio which is use for meeting the current

assets and current liability for meeting the working capital ratio. In this ratio the higher

the ratio is shows that firm has higher liquidity so they can manage all its activities by

better utilization of the resources in achievement of the goals in the future (Chen and

Demirer, 2018). Through this they are able to manage the cash through the use of the this

ratio which is in ideal current ratio it is 2:1 3which show that the current assets is 2 and

liabilities is 1. according to the above calculation the ratio of both Tesco and Sainsbury,

Tesco has better performance than the other entity which it shows the higher liquidity in

the bothy year 18 and 19.

3

10/07/1905

11/07/1905

0.550.60.650.70.75 0.713

0.612

0.73

0.63

Chart Title

Tesco Sainsburry

Average inventory

turnover period

Net sales / average

inventory

57491/2282.5

= 25.91 days

63911/2240.5

= 28.52 days

Capital gearing ratio Total debt / total equity

44862/10480

= 4.280%

49047 / 14858

= 3.301%

Return on capital

employed

Operating profit/ capital

employed 5.13 6.86

Ratio interpretation

Current ratio- Current ratio refers to the ratio which is use for meeting the current

assets and current liability for meeting the working capital ratio. In this ratio the higher

the ratio is shows that firm has higher liquidity so they can manage all its activities by

better utilization of the resources in achievement of the goals in the future (Chen and

Demirer, 2018). Through this they are able to manage the cash through the use of the this

ratio which is in ideal current ratio it is 2:1 3which show that the current assets is 2 and

liabilities is 1. according to the above calculation the ratio of both Tesco and Sainsbury,

Tesco has better performance than the other entity which it shows the higher liquidity in

the bothy year 18 and 19.

3

10/07/1905

11/07/1905

0.550.60.650.70.75 0.713

0.612

0.73

0.63

Chart Title

Tesco Sainsburry

Liquidity ratio- Liquid ratio is known as Acid ratio which means cash and bank balances

of the entity, in this ratio there is the use of the formula in which there is the use of the

current assets minus stock and divided by the current liability. It give the efficiency of the

company in the market. The higher the liquidity ratio is there is more chances to pay its

short term debts (Harbi and Toumia, 2020). From the above calculations it has been

analysed that Tesco and Sainsbury have different liquidity in the year 2018 and 2019. In

2018 Tesco maintain their liquidity which is higher than Sainsbury in both year there is

the management of the assets in both year 2018 and 2019, Tesco declines their liquid

assets which is not managed properly for use the resources efficiently.

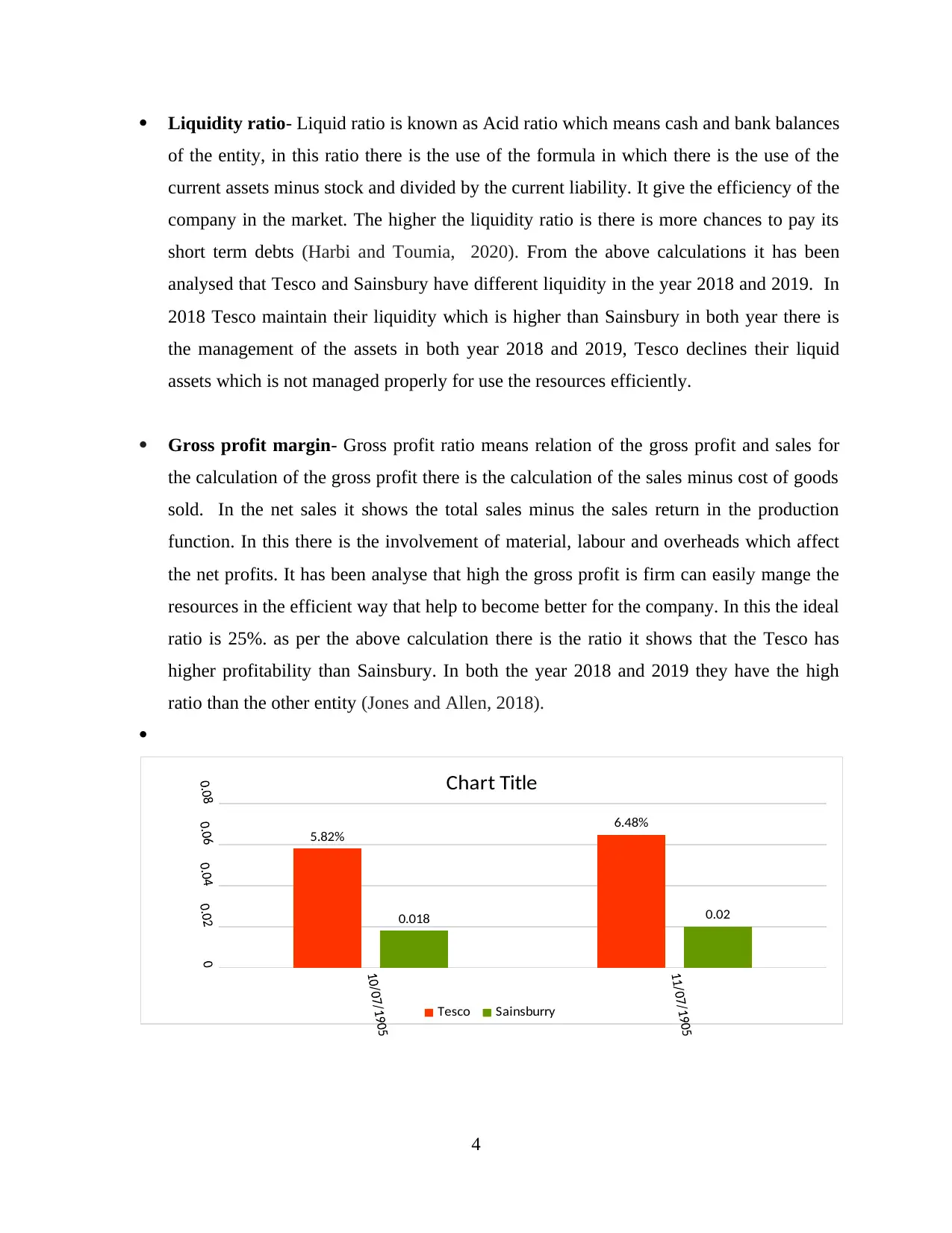

Gross profit margin- Gross profit ratio means relation of the gross profit and sales for

the calculation of the gross profit there is the calculation of the sales minus cost of goods

sold. In the net sales it shows the total sales minus the sales return in the production

function. In this there is the involvement of material, labour and overheads which affect

the net profits. It has been analyse that high the gross profit is firm can easily mange the

resources in the efficient way that help to become better for the company. In this the ideal

ratio is 25%. as per the above calculation there is the ratio it shows that the Tesco has

higher profitability than Sainsbury. In both the year 2018 and 2019 they have the high

ratio than the other entity (Jones and Allen, 2018).

5.82%

6.48%

0.018 0.02

Chart Title

Tesco Sainsburry

4

of the entity, in this ratio there is the use of the formula in which there is the use of the

current assets minus stock and divided by the current liability. It give the efficiency of the

company in the market. The higher the liquidity ratio is there is more chances to pay its

short term debts (Harbi and Toumia, 2020). From the above calculations it has been

analysed that Tesco and Sainsbury have different liquidity in the year 2018 and 2019. In

2018 Tesco maintain their liquidity which is higher than Sainsbury in both year there is

the management of the assets in both year 2018 and 2019, Tesco declines their liquid

assets which is not managed properly for use the resources efficiently.

Gross profit margin- Gross profit ratio means relation of the gross profit and sales for

the calculation of the gross profit there is the calculation of the sales minus cost of goods

sold. In the net sales it shows the total sales minus the sales return in the production

function. In this there is the involvement of material, labour and overheads which affect

the net profits. It has been analyse that high the gross profit is firm can easily mange the

resources in the efficient way that help to become better for the company. In this the ideal

ratio is 25%. as per the above calculation there is the ratio it shows that the Tesco has

higher profitability than Sainsbury. In both the year 2018 and 2019 they have the high

ratio than the other entity (Jones and Allen, 2018).

5.82%

6.48%

0.018 0.02

Chart Title

Tesco Sainsburry

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

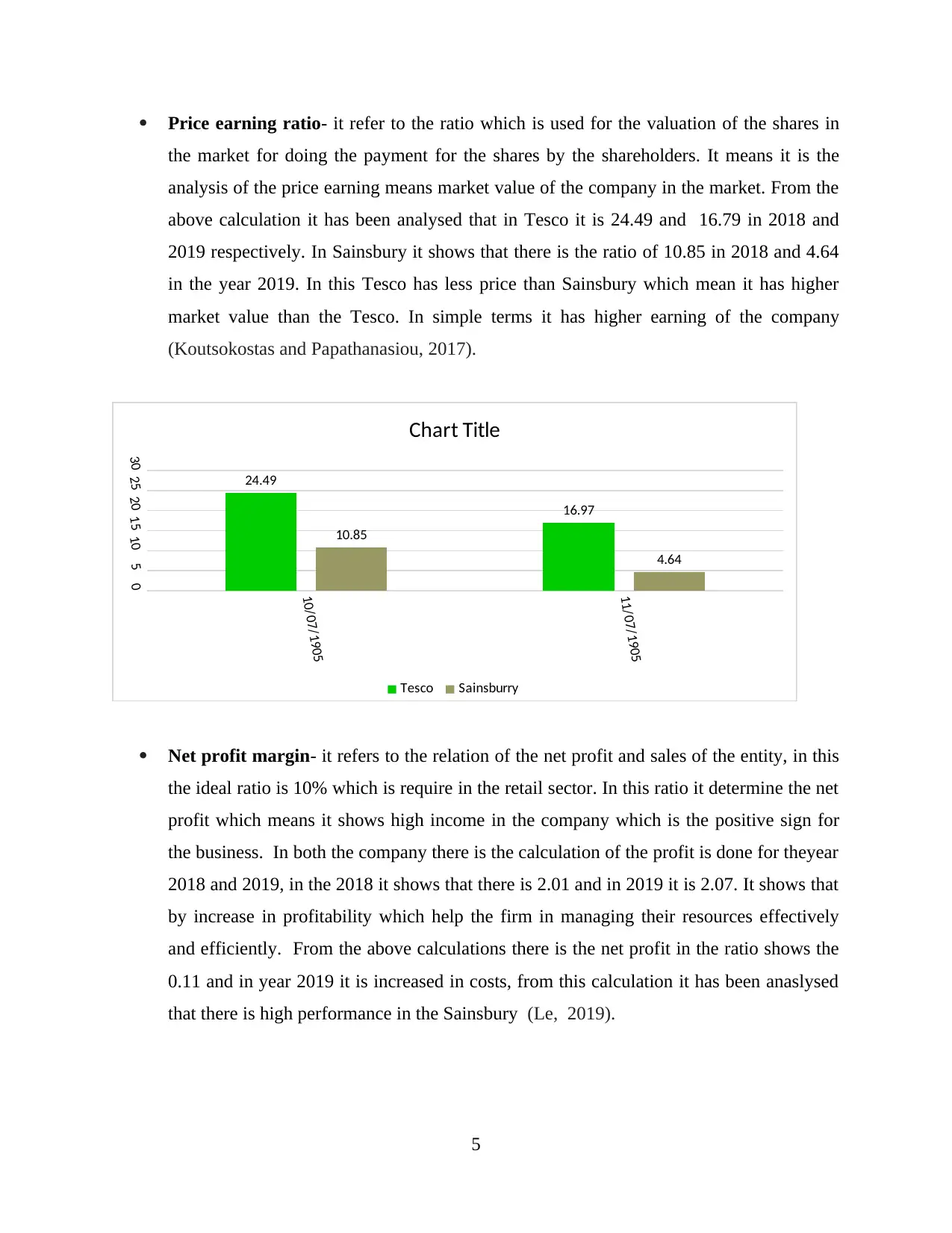

Price earning ratio- it refer to the ratio which is used for the valuation of the shares in

the market for doing the payment for the shares by the shareholders. It means it is the

analysis of the price earning means market value of the company in the market. From the

above calculation it has been analysed that in Tesco it is 24.49 and 16.79 in 2018 and

2019 respectively. In Sainsbury it shows that there is the ratio of 10.85 in 2018 and 4.64

in the year 2019. In this Tesco has less price than Sainsbury which mean it has higher

market value than the Tesco. In simple terms it has higher earning of the company

(Koutsokostas and Papathanasiou, 2017).

10/07/1905

11/07/1905

051015202530 24.49

16.97

10.85

4.64

Chart Title

Tesco Sainsburry

Net profit margin- it refers to the relation of the net profit and sales of the entity, in this

the ideal ratio is 10% which is require in the retail sector. In this ratio it determine the net

profit which means it shows high income in the company which is the positive sign for

the business. In both the company there is the calculation of the profit is done for theyear

2018 and 2019, in the 2018 it shows that there is 2.01 and in 2019 it is 2.07. It shows that

by increase in profitability which help the firm in managing their resources effectively

and efficiently. From the above calculations there is the net profit in the ratio shows the

0.11 and in year 2019 it is increased in costs, from this calculation it has been anaslysed

that there is high performance in the Sainsbury (Le, 2019).

5

the market for doing the payment for the shares by the shareholders. It means it is the

analysis of the price earning means market value of the company in the market. From the

above calculation it has been analysed that in Tesco it is 24.49 and 16.79 in 2018 and

2019 respectively. In Sainsbury it shows that there is the ratio of 10.85 in 2018 and 4.64

in the year 2019. In this Tesco has less price than Sainsbury which mean it has higher

market value than the Tesco. In simple terms it has higher earning of the company

(Koutsokostas and Papathanasiou, 2017).

10/07/1905

11/07/1905

051015202530 24.49

16.97

10.85

4.64

Chart Title

Tesco Sainsburry

Net profit margin- it refers to the relation of the net profit and sales of the entity, in this

the ideal ratio is 10% which is require in the retail sector. In this ratio it determine the net

profit which means it shows high income in the company which is the positive sign for

the business. In both the company there is the calculation of the profit is done for theyear

2018 and 2019, in the 2018 it shows that there is 2.01 and in 2019 it is 2.07. It shows that

by increase in profitability which help the firm in managing their resources effectively

and efficiently. From the above calculations there is the net profit in the ratio shows the

0.11 and in year 2019 it is increased in costs, from this calculation it has been anaslysed

that there is high performance in the Sainsbury (Le, 2019).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10/07/1905

11/07/1905

00.511.522.5 2.097 2.07

0.11 0.006

Chart Title

Tesco Sainsburry

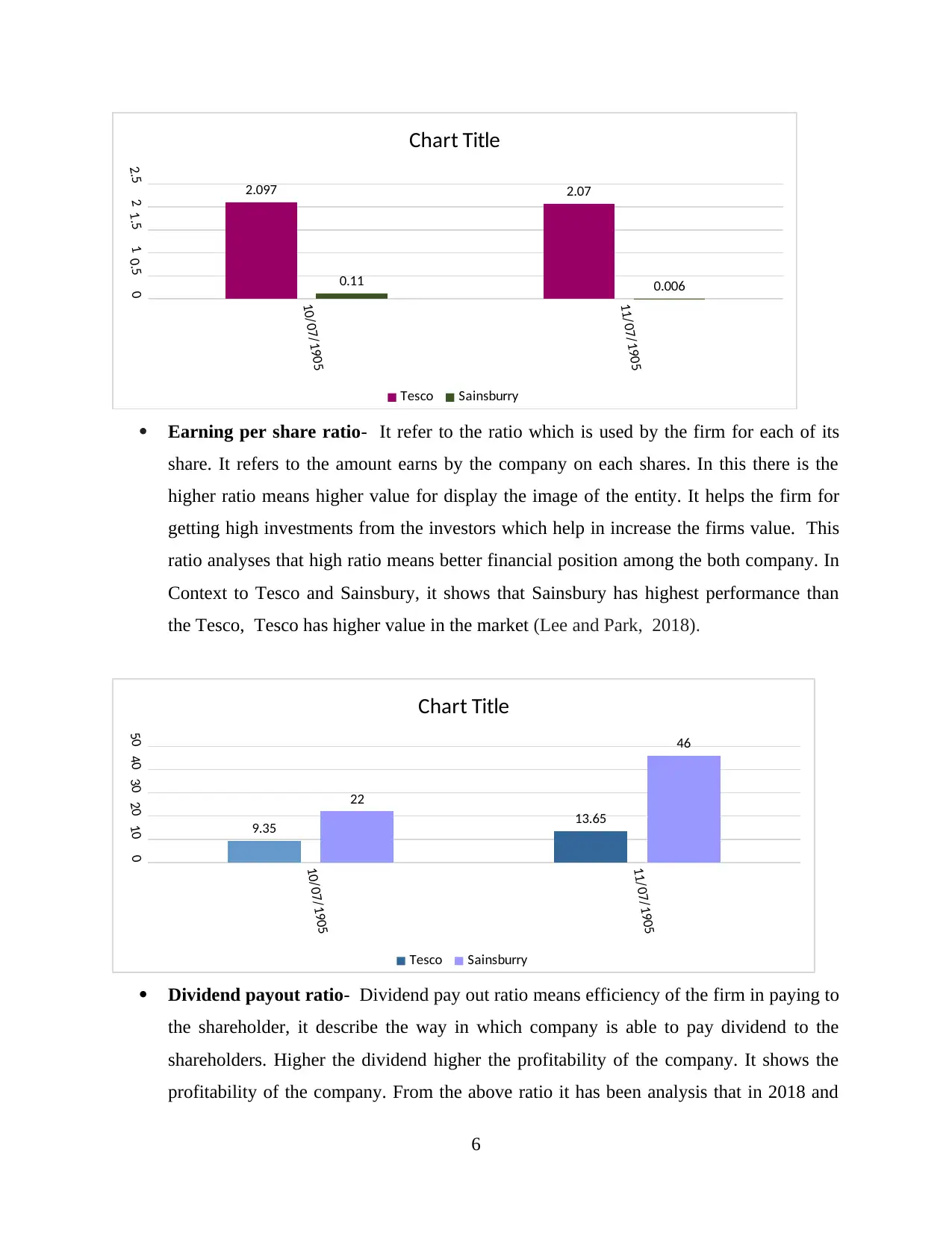

Earning per share ratio- It refer to the ratio which is used by the firm for each of its

share. It refers to the amount earns by the company on each shares. In this there is the

higher ratio means higher value for display the image of the entity. It helps the firm for

getting high investments from the investors which help in increase the firms value. This

ratio analyses that high ratio means better financial position among the both company. In

Context to Tesco and Sainsbury, it shows that Sainsbury has highest performance than

the Tesco, Tesco has higher value in the market (Lee and Park, 2018).

10/07/1905

11/07/1905

01020304050

9.35 13.65

22

46

Chart Title

Tesco Sainsburry

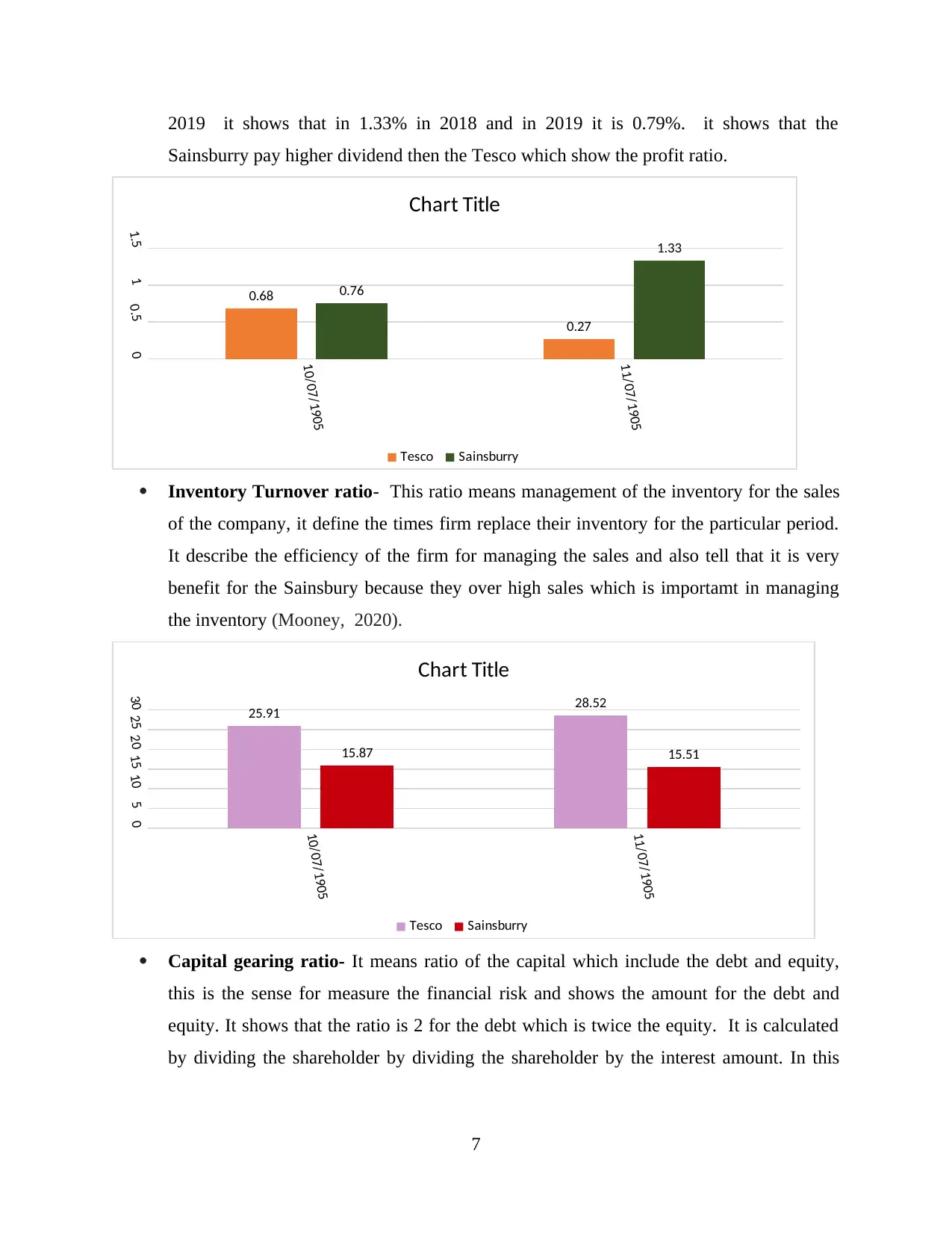

Dividend payout ratio- Dividend pay out ratio means efficiency of the firm in paying to

the shareholder, it describe the way in which company is able to pay dividend to the

shareholders. Higher the dividend higher the profitability of the company. It shows the

profitability of the company. From the above ratio it has been analysis that in 2018 and

6

11/07/1905

00.511.522.5 2.097 2.07

0.11 0.006

Chart Title

Tesco Sainsburry

Earning per share ratio- It refer to the ratio which is used by the firm for each of its

share. It refers to the amount earns by the company on each shares. In this there is the

higher ratio means higher value for display the image of the entity. It helps the firm for

getting high investments from the investors which help in increase the firms value. This

ratio analyses that high ratio means better financial position among the both company. In

Context to Tesco and Sainsbury, it shows that Sainsbury has highest performance than

the Tesco, Tesco has higher value in the market (Lee and Park, 2018).

10/07/1905

11/07/1905

01020304050

9.35 13.65

22

46

Chart Title

Tesco Sainsburry

Dividend payout ratio- Dividend pay out ratio means efficiency of the firm in paying to

the shareholder, it describe the way in which company is able to pay dividend to the

shareholders. Higher the dividend higher the profitability of the company. It shows the

profitability of the company. From the above ratio it has been analysis that in 2018 and

6

2019 it shows that in 1.33% in 2018 and in 2019 it is 0.79%. it shows that the

Sainsburry pay higher dividend then the Tesco which show the profit ratio.

10/07/1905

11/07/1905

00.511.5

0.68

0.27

0.76

1.33

Chart Title

Tesco Sainsburry

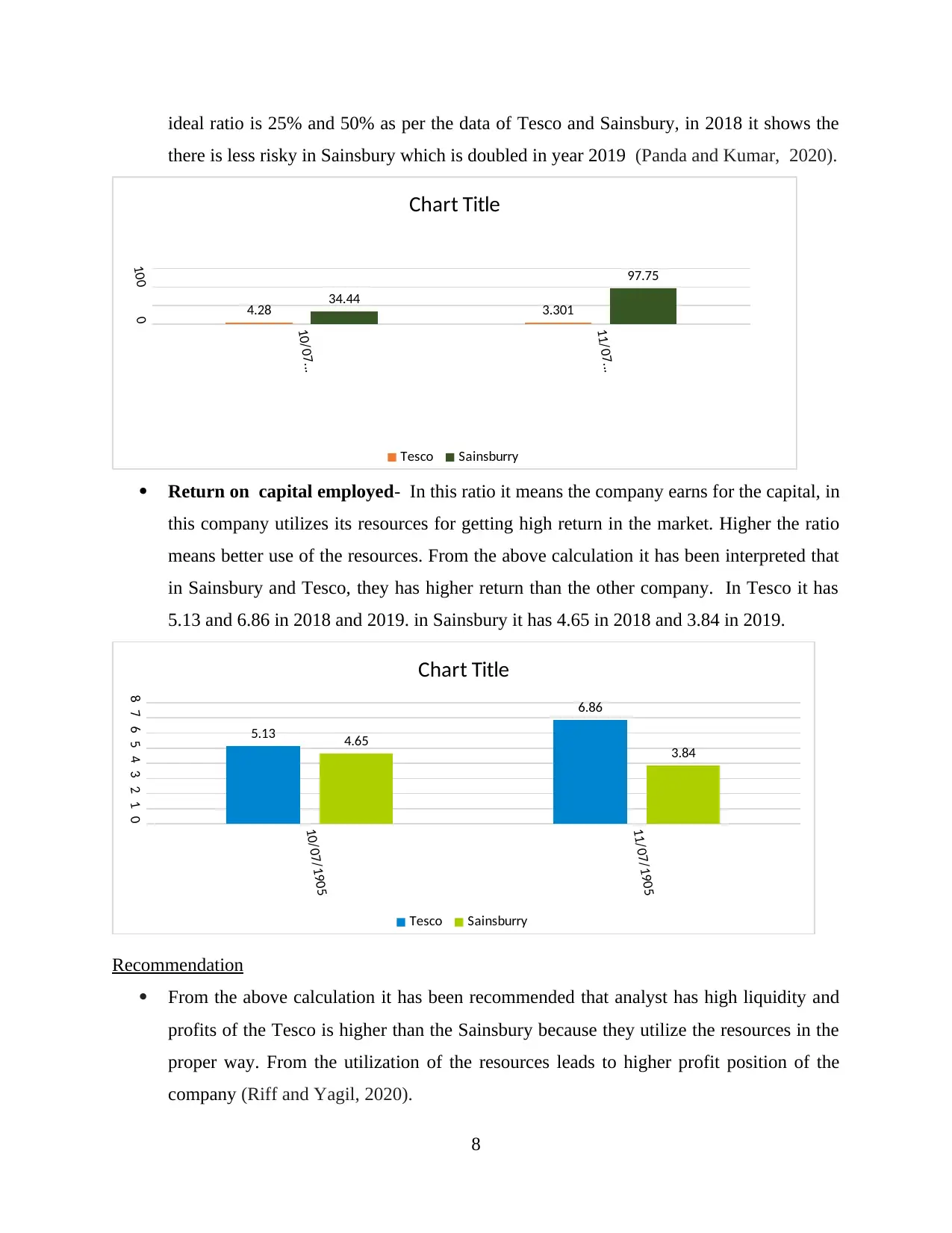

Inventory Turnover ratio- This ratio means management of the inventory for the sales

of the company, it define the times firm replace their inventory for the particular period.

It describe the efficiency of the firm for managing the sales and also tell that it is very

benefit for the Sainsbury because they over high sales which is importamt in managing

the inventory (Mooney, 2020).

10/07/1905

11/07/1905

051015202530 25.91 28.52

15.87 15.51

Chart Title

Tesco Sainsburry

Capital gearing ratio- It means ratio of the capital which include the debt and equity,

this is the sense for measure the financial risk and shows the amount for the debt and

equity. It shows that the ratio is 2 for the debt which is twice the equity. It is calculated

by dividing the shareholder by dividing the shareholder by the interest amount. In this

7

Sainsburry pay higher dividend then the Tesco which show the profit ratio.

10/07/1905

11/07/1905

00.511.5

0.68

0.27

0.76

1.33

Chart Title

Tesco Sainsburry

Inventory Turnover ratio- This ratio means management of the inventory for the sales

of the company, it define the times firm replace their inventory for the particular period.

It describe the efficiency of the firm for managing the sales and also tell that it is very

benefit for the Sainsbury because they over high sales which is importamt in managing

the inventory (Mooney, 2020).

10/07/1905

11/07/1905

051015202530 25.91 28.52

15.87 15.51

Chart Title

Tesco Sainsburry

Capital gearing ratio- It means ratio of the capital which include the debt and equity,

this is the sense for measure the financial risk and shows the amount for the debt and

equity. It shows that the ratio is 2 for the debt which is twice the equity. It is calculated

by dividing the shareholder by dividing the shareholder by the interest amount. In this

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

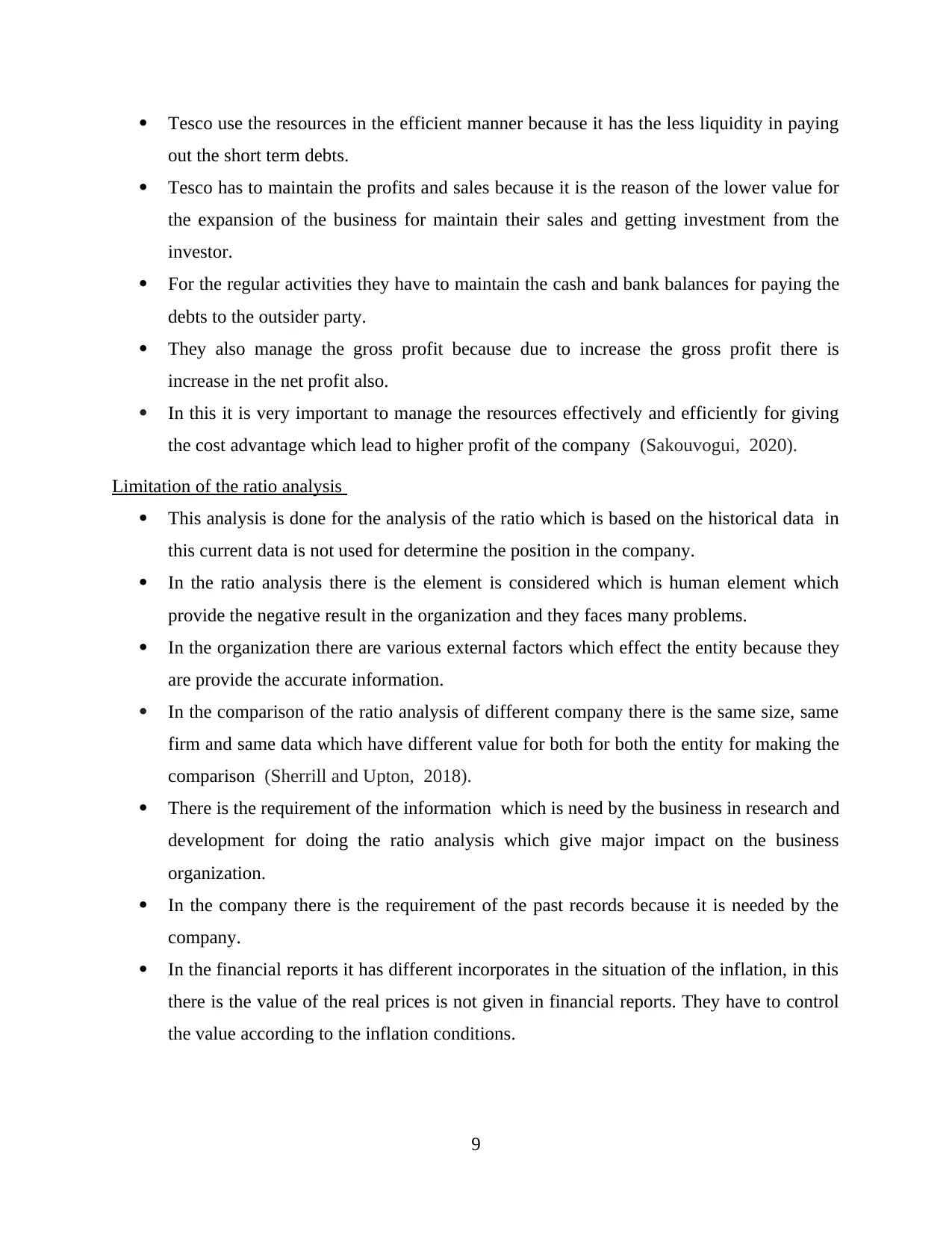

ideal ratio is 25% and 50% as per the data of Tesco and Sainsbury, in 2018 it shows the

there is less risky in Sainsbury which is doubled in year 2019 (Panda and Kumar, 2020).

10/07...

11/07...

0100

4.28 3.301

34.44

97.75

Chart Title

Tesco Sainsburry

Return on capital employed- In this ratio it means the company earns for the capital, in

this company utilizes its resources for getting high return in the market. Higher the ratio

means better use of the resources. From the above calculation it has been interpreted that

in Sainsbury and Tesco, they has higher return than the other company. In Tesco it has

5.13 and 6.86 in 2018 and 2019. in Sainsbury it has 4.65 in 2018 and 3.84 in 2019.

10/07/1905

11/07/1905

012345678

5.13

6.86

4.65 3.84

Chart Title

Tesco Sainsburry

Recommendation

From the above calculation it has been recommended that analyst has high liquidity and

profits of the Tesco is higher than the Sainsbury because they utilize the resources in the

proper way. From the utilization of the resources leads to higher profit position of the

company (Riff and Yagil, 2020).

8

there is less risky in Sainsbury which is doubled in year 2019 (Panda and Kumar, 2020).

10/07...

11/07...

0100

4.28 3.301

34.44

97.75

Chart Title

Tesco Sainsburry

Return on capital employed- In this ratio it means the company earns for the capital, in

this company utilizes its resources for getting high return in the market. Higher the ratio

means better use of the resources. From the above calculation it has been interpreted that

in Sainsbury and Tesco, they has higher return than the other company. In Tesco it has

5.13 and 6.86 in 2018 and 2019. in Sainsbury it has 4.65 in 2018 and 3.84 in 2019.

10/07/1905

11/07/1905

012345678

5.13

6.86

4.65 3.84

Chart Title

Tesco Sainsburry

Recommendation

From the above calculation it has been recommended that analyst has high liquidity and

profits of the Tesco is higher than the Sainsbury because they utilize the resources in the

proper way. From the utilization of the resources leads to higher profit position of the

company (Riff and Yagil, 2020).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tesco use the resources in the efficient manner because it has the less liquidity in paying

out the short term debts.

Tesco has to maintain the profits and sales because it is the reason of the lower value for

the expansion of the business for maintain their sales and getting investment from the

investor.

For the regular activities they have to maintain the cash and bank balances for paying the

debts to the outsider party.

They also manage the gross profit because due to increase the gross profit there is

increase in the net profit also.

In this it is very important to manage the resources effectively and efficiently for giving

the cost advantage which lead to higher profit of the company (Sakouvogui, 2020).

Limitation of the ratio analysis

This analysis is done for the analysis of the ratio which is based on the historical data in

this current data is not used for determine the position in the company.

In the ratio analysis there is the element is considered which is human element which

provide the negative result in the organization and they faces many problems.

In the organization there are various external factors which effect the entity because they

are provide the accurate information.

In the comparison of the ratio analysis of different company there is the same size, same

firm and same data which have different value for both for both the entity for making the

comparison (Sherrill and Upton, 2018).

There is the requirement of the information which is need by the business in research and

development for doing the ratio analysis which give major impact on the business

organization.

In the company there is the requirement of the past records because it is needed by the

company.

In the financial reports it has different incorporates in the situation of the inflation, in this

there is the value of the real prices is not given in financial reports. They have to control

the value according to the inflation conditions.

9

out the short term debts.

Tesco has to maintain the profits and sales because it is the reason of the lower value for

the expansion of the business for maintain their sales and getting investment from the

investor.

For the regular activities they have to maintain the cash and bank balances for paying the

debts to the outsider party.

They also manage the gross profit because due to increase the gross profit there is

increase in the net profit also.

In this it is very important to manage the resources effectively and efficiently for giving

the cost advantage which lead to higher profit of the company (Sakouvogui, 2020).

Limitation of the ratio analysis

This analysis is done for the analysis of the ratio which is based on the historical data in

this current data is not used for determine the position in the company.

In the ratio analysis there is the element is considered which is human element which

provide the negative result in the organization and they faces many problems.

In the organization there are various external factors which effect the entity because they

are provide the accurate information.

In the comparison of the ratio analysis of different company there is the same size, same

firm and same data which have different value for both for both the entity for making the

comparison (Sherrill and Upton, 2018).

There is the requirement of the information which is need by the business in research and

development for doing the ratio analysis which give major impact on the business

organization.

In the company there is the requirement of the past records because it is needed by the

company.

In the financial reports it has different incorporates in the situation of the inflation, in this

there is the value of the real prices is not given in financial reports. They have to control

the value according to the inflation conditions.

9

In ratio analysis they change their operational factor for making changes in the supply

chain for making the strategy during the selling times. It also effect the effective

decisions which is use by the company for managing the management.

In the seasonal factors there are some implications of the ratio analysis it effect the

performance of the business by interpret the financial ability of the ratio in accordance

with the wrong interpretation.

In the ratio analysis there is the understand of the financial information for making

financial statements, which result is comparison of actual result with the expected reason

for removing the conflicts of the finance information.

By making changes in the price level due to the inflation there is use of the historical data

which is based on the historical costs. Price level changes is also use for comparison of

the financial situation of the enterprise (Ashour, Rennie and Santamaria, 2019).

By the unavailability of the ratio analysis there is the use of the formulas which is utilized

by the company for the calculation of current ratio which consider all current liabilities

minus overdraft of bank.

One limitation is use of the application of ratio analysis for incorporating different

strategies for making in appropriate evolution.

According to accounting policies it has been noted that there is the recording of the same

transactions for the accounting which is not provide the appropriate results.

Business can not able to make alterations in the year end of its financial statements which

help in increasing the analysis of the ratio which lead to Window Dressing.

PORTFOLIO 2

Investment appraisal techniques

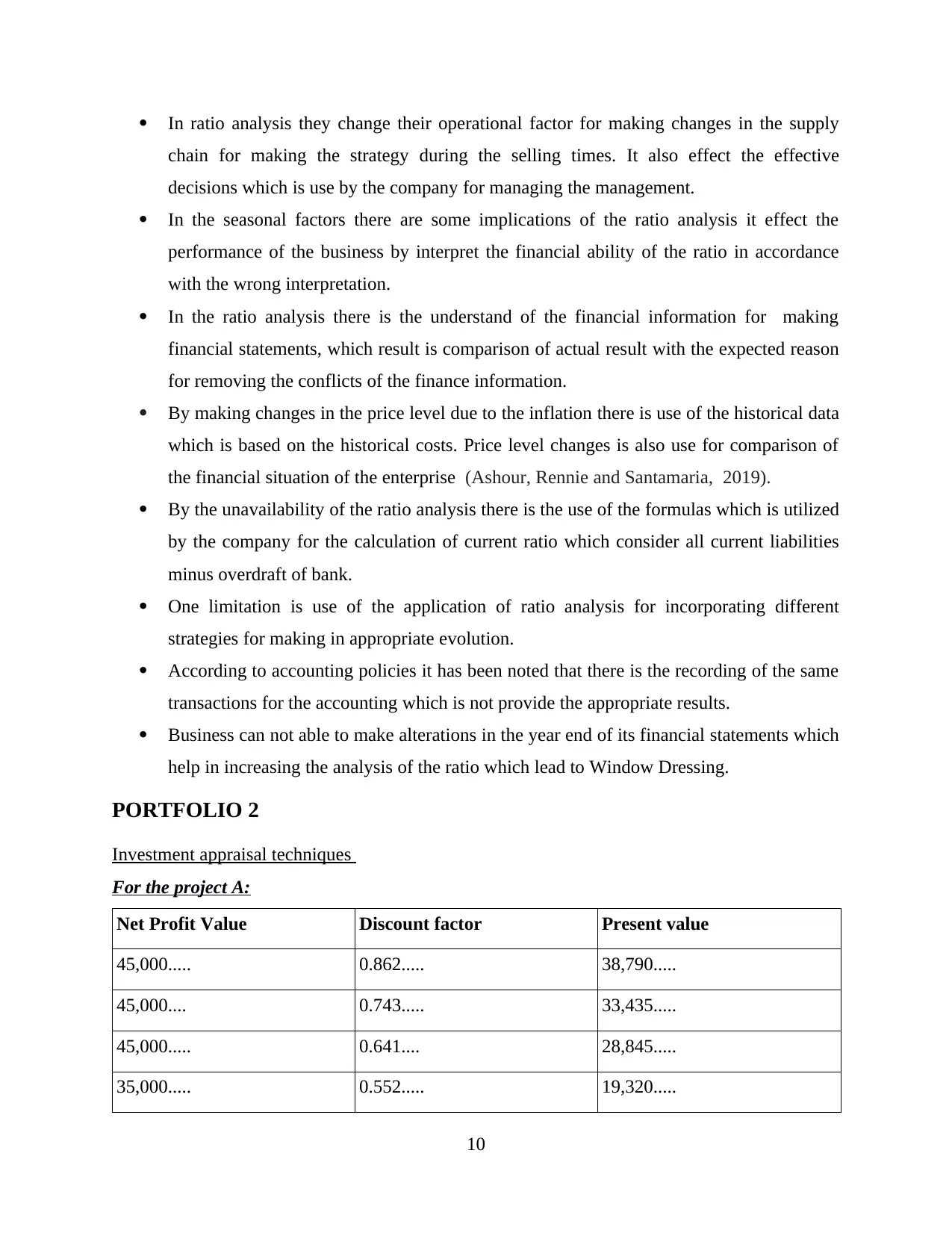

For the project A:

Net Profit Value Discount factor Present value

45,000..... 0.862..... 38,790.....

45,000.... 0.743..... 33,435.....

45,000..... 0.641.... 28,845.....

35,000..... 0.552..... 19,320.....

10

chain for making the strategy during the selling times. It also effect the effective

decisions which is use by the company for managing the management.

In the seasonal factors there are some implications of the ratio analysis it effect the

performance of the business by interpret the financial ability of the ratio in accordance

with the wrong interpretation.

In the ratio analysis there is the understand of the financial information for making

financial statements, which result is comparison of actual result with the expected reason

for removing the conflicts of the finance information.

By making changes in the price level due to the inflation there is use of the historical data

which is based on the historical costs. Price level changes is also use for comparison of

the financial situation of the enterprise (Ashour, Rennie and Santamaria, 2019).

By the unavailability of the ratio analysis there is the use of the formulas which is utilized

by the company for the calculation of current ratio which consider all current liabilities

minus overdraft of bank.

One limitation is use of the application of ratio analysis for incorporating different

strategies for making in appropriate evolution.

According to accounting policies it has been noted that there is the recording of the same

transactions for the accounting which is not provide the appropriate results.

Business can not able to make alterations in the year end of its financial statements which

help in increasing the analysis of the ratio which lead to Window Dressing.

PORTFOLIO 2

Investment appraisal techniques

For the project A:

Net Profit Value Discount factor Present value

45,000..... 0.862..... 38,790.....

45,000.... 0.743..... 33,435.....

45,000..... 0.641.... 28,845.....

35,000..... 0.552..... 19,320.....

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.