Financial Management: Tesco vs. Sainsbury Ratio Analysis Report

VerifiedAdded on 2020/02/12

|17

|3284

|417

Report

AI Summary

This report provides a financial ratio analysis of Tesco and Sainsbury, two leading UK retail organizations, over a five-year period (2012-2016). The analysis focuses on profitability ratios (gross profit, operating profit, and net profit margins), liquidity ratios (current and quick ratios), solvency ratios (debt-equity ratio), and efficiency ratios (inventory and debtor turnover ratios). The report compares the financial performance of the two companies, highlighting trends and key differences. The analysis reveals that Sainsbury generally maintained a better financial position in terms of profitability and solvency compared to Tesco during the evaluated period. The report concludes with recommendations for Tesco to improve its financial performance, including focusing on product quality and inventory management. The report uses financial statements and ratio analysis to assess the financial health and efficiency of both firms, providing insights into their performance and competitive positions within the retail sector. The analysis underscores the importance of effective financial management in achieving organizational objectives and navigating market competition.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Financial ratio analysis of Tesco and Sainsbury for the period of Five years ‘...........................3

CONCLUSION................................................................................................................................7

RECOMMENDATIONS.................................................................................................................7

REFERENCES................................................................................................................................9

APPENDIX ].................................................................................................................................10

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Financial ratio analysis of Tesco and Sainsbury for the period of Five years ‘...........................3

CONCLUSION................................................................................................................................7

RECOMMENDATIONS.................................................................................................................7

REFERENCES................................................................................................................................9

APPENDIX ].................................................................................................................................10

INTRODUCTION

Financial management is highly concerned with making suitable decision by making

evaluation of the monetary health and performance. In the present times, effectual management

of fund is highly required to attain organizational aims and objectives. Hence, by using ratio

analysis tool business unit can assess the extent to which it has made optimum use of funds over

the time frame and as compared to the competitors. This project report is based on Tesco and

Sainsbury which are the leading retail organizations of UK. Both the firms are competing with

each other in terms of customer base and market position.Hence, in this, report will shed light on

the financial health and performance ofTesco over the period of five years. Besides this, it also

entails the extent to which Tesco has generated enough profitability in against to the rival firm.

MAIN BODY

Financial ratio analysis of Tesco and Sainsbury for the period of Five years ‘

Profitability ratios

Enclosed in Appendix 2

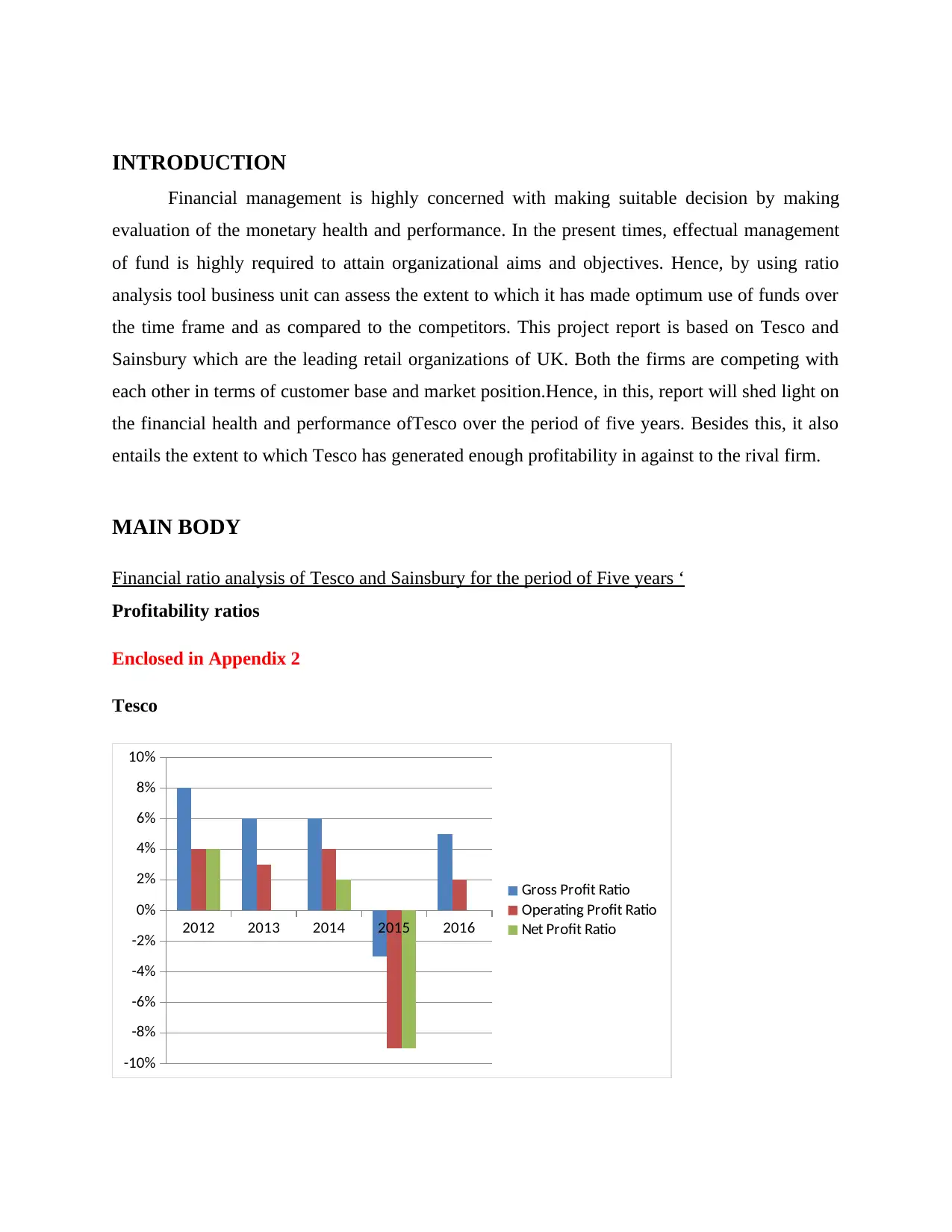

Tesco

2012 2013 2014 2015 2016

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Gross Profit Ratio

Operating Profit Ratio

Net Profit Ratio

Financial management is highly concerned with making suitable decision by making

evaluation of the monetary health and performance. In the present times, effectual management

of fund is highly required to attain organizational aims and objectives. Hence, by using ratio

analysis tool business unit can assess the extent to which it has made optimum use of funds over

the time frame and as compared to the competitors. This project report is based on Tesco and

Sainsbury which are the leading retail organizations of UK. Both the firms are competing with

each other in terms of customer base and market position.Hence, in this, report will shed light on

the financial health and performance ofTesco over the period of five years. Besides this, it also

entails the extent to which Tesco has generated enough profitability in against to the rival firm.

MAIN BODY

Financial ratio analysis of Tesco and Sainsbury for the period of Five years ‘

Profitability ratios

Enclosed in Appendix 2

Tesco

2012 2013 2014 2015 2016

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Gross Profit Ratio

Operating Profit Ratio

Net Profit Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

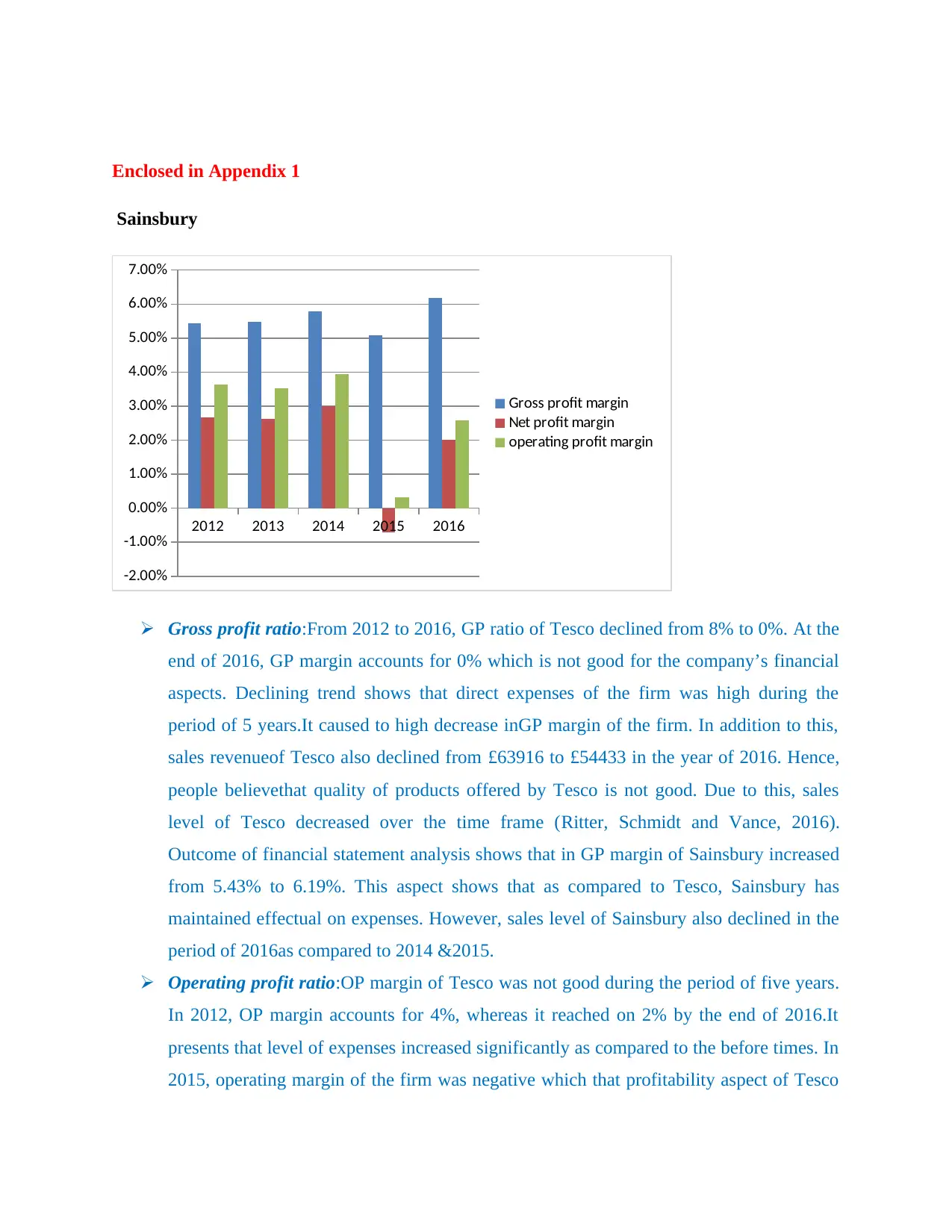

Enclosed in Appendix 1

Sainsbury

2012 2013 2014 2015 2016

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

Gross profit margin

Net profit margin

operating profit margin

Gross profit ratio:From 2012 to 2016, GP ratio of Tesco declined from 8% to 0%. At the

end of 2016, GP margin accounts for 0% which is not good for the company’s financial

aspects. Declining trend shows that direct expenses of the firm was high during the

period of 5 years.It caused to high decrease inGP margin of the firm. In addition to this,

sales revenueof Tesco also declined from £63916 to £54433 in the year of 2016. Hence,

people believethat quality of products offered by Tesco is not good. Due to this, sales

level of Tesco decreased over the time frame (Ritter, Schmidt and Vance, 2016).

Outcome of financial statement analysis shows that in GP margin of Sainsbury increased

from 5.43% to 6.19%. This aspect shows that as compared to Tesco, Sainsbury has

maintained effectual on expenses. However, sales level of Sainsbury also declined in the

period of 2016as compared to 2014 &2015.

Operating profit ratio:OP margin of Tesco was not good during the period of five years.

In 2012, OP margin accounts for 4%, whereas it reached on 2% by the end of 2016.It

presents that level of expenses increased significantly as compared to the before times. In

2015, operating margin of the firm was negative which that profitability aspect of Tesco

Sainsbury

2012 2013 2014 2015 2016

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

Gross profit margin

Net profit margin

operating profit margin

Gross profit ratio:From 2012 to 2016, GP ratio of Tesco declined from 8% to 0%. At the

end of 2016, GP margin accounts for 0% which is not good for the company’s financial

aspects. Declining trend shows that direct expenses of the firm was high during the

period of 5 years.It caused to high decrease inGP margin of the firm. In addition to this,

sales revenueof Tesco also declined from £63916 to £54433 in the year of 2016. Hence,

people believethat quality of products offered by Tesco is not good. Due to this, sales

level of Tesco decreased over the time frame (Ritter, Schmidt and Vance, 2016).

Outcome of financial statement analysis shows that in GP margin of Sainsbury increased

from 5.43% to 6.19%. This aspect shows that as compared to Tesco, Sainsbury has

maintained effectual on expenses. However, sales level of Sainsbury also declined in the

period of 2016as compared to 2014 &2015.

Operating profit ratio:OP margin of Tesco was not good during the period of five years.

In 2012, OP margin accounts for 4%, whereas it reached on 2% by the end of 2016.It

presents that level of expenses increased significantly as compared to the before times. In

2015, operating margin of the firm was negative which that profitability aspect of Tesco

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is worst.On the other side, operating profit margin of Sainsburydeclined over the time

frame (Jami and Bahar, 2016). However, operating profit ratio of Sainsbury was .32%

and 2.58%. Hence, it can be stated that operating margin of Sainsbury was good in

against to Tesco.

Net profit ratio: By applying the tools and techniques of ratio analysis, it has been

assessed that NP margin of Tesco wasNIL in the year of 2013 and 2016. On the other

hand, NP margin of Tesco was negative such -9% in period of2015. By considering this,

it can be stated that as compared to sales revenue, indirect expense level of business unit

was high. Hence, due to the high expense level NP margin of Tesco decreased

significantly. Along with this, due to the existence of high competition during the period

of 2015 Sainsbury also placed more emphasis on the promotional aspect. Hence, due to

this, NP margin of the firm accounts for negative -0.70. In comparison to Tesco,

Sainsbury generated positive profit margin of 2%. It is still lowerbut from the perspective

of existence of competition and competitors Sainsbury’s profitability aspectgood

(Goldmann, 2017). Hence, from overall evaluation, it can be stated that profitability

position of Sainsbury was sound in comparison to Tesco.

Liquidity ratios

Enclosed in Appendix 2

Tesco

frame (Jami and Bahar, 2016). However, operating profit ratio of Sainsbury was .32%

and 2.58%. Hence, it can be stated that operating margin of Sainsbury was good in

against to Tesco.

Net profit ratio: By applying the tools and techniques of ratio analysis, it has been

assessed that NP margin of Tesco wasNIL in the year of 2013 and 2016. On the other

hand, NP margin of Tesco was negative such -9% in period of2015. By considering this,

it can be stated that as compared to sales revenue, indirect expense level of business unit

was high. Hence, due to the high expense level NP margin of Tesco decreased

significantly. Along with this, due to the existence of high competition during the period

of 2015 Sainsbury also placed more emphasis on the promotional aspect. Hence, due to

this, NP margin of the firm accounts for negative -0.70. In comparison to Tesco,

Sainsbury generated positive profit margin of 2%. It is still lowerbut from the perspective

of existence of competition and competitors Sainsbury’s profitability aspectgood

(Goldmann, 2017). Hence, from overall evaluation, it can be stated that profitability

position of Sainsbury was sound in comparison to Tesco.

Liquidity ratios

Enclosed in Appendix 2

Tesco

2012 2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Current Ratio

Quick Ratio

Enclosed in Appendix 1

Sainsbury

2012 2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Current ratio

Quick ratio/acid test ratio

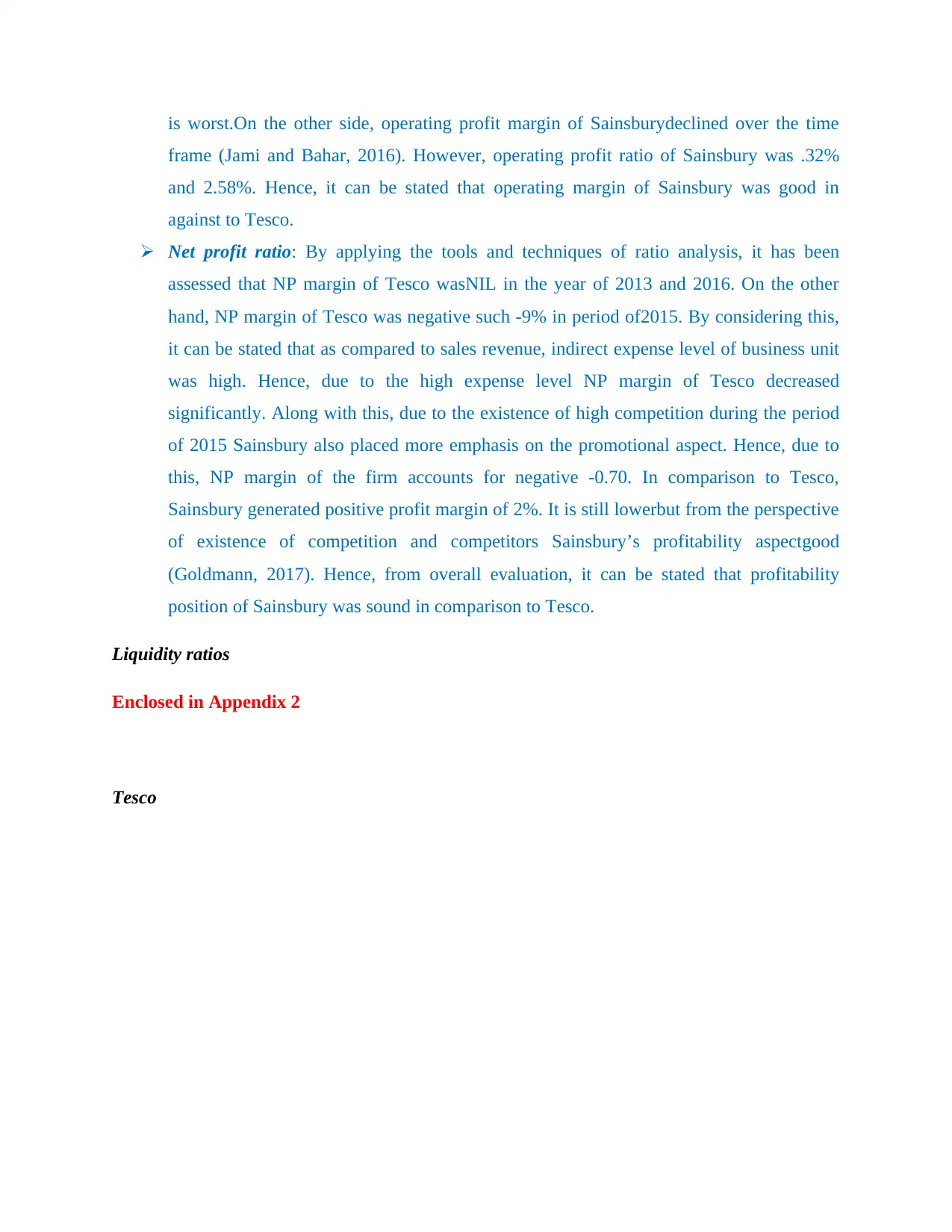

Current ratio:From ratio analysis, it has been assessed that current ratio of Tesco was

fluctuated within the period of 5 years. However, as compared to previous years current

ratio of Tesco inclined from .67 times to.75 times at the end ofaccounting year 2016. It

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Current Ratio

Quick Ratio

Enclosed in Appendix 1

Sainsbury

2012 2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Current ratio

Quick ratio/acid test ratio

Current ratio:From ratio analysis, it has been assessed that current ratio of Tesco was

fluctuated within the period of 5 years. However, as compared to previous years current

ratio of Tesco inclined from .67 times to.75 times at the end ofaccounting year 2016. It

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

shows that company’s ability in relation to fulfilling the obligationsincreased over the

years. Nevertheless current ratio of Tesco is very far from the ideal ratio which is 2:1

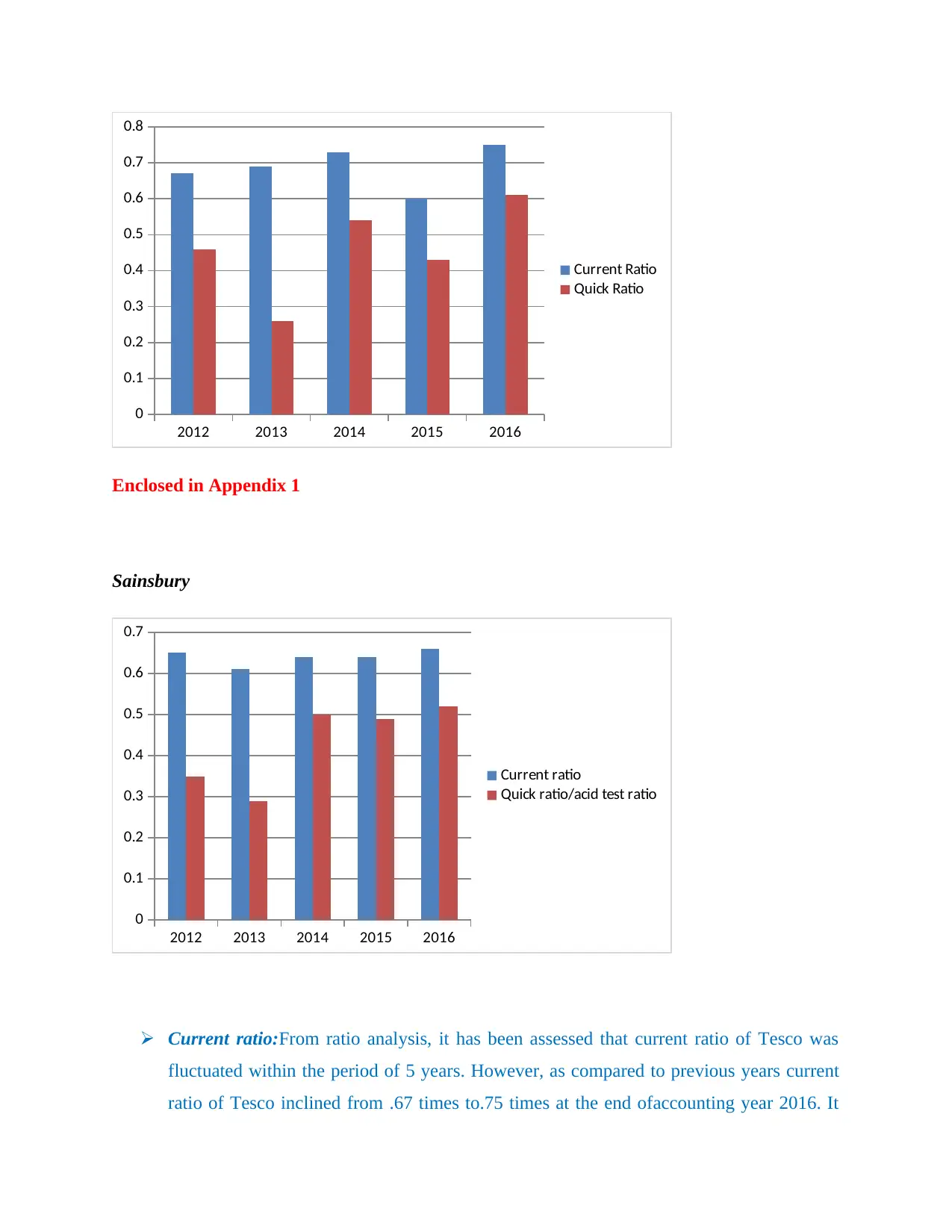

(MATTHEW, FADA and UKONU, 2016).On the other side,current ratio of Sainsbury

was .65, .61and .64 from the period of 2012 to 2014. In contrast to this, current ratio

accounts for .64 &.66 during the year 2015 and 2016.With the motive to enhance

customer base and market share both the companies are placing high level of emphasis on

promotional aspects and discounting strategies (Dopson and Hayes, 2016). It is one of the

main reasons due to which both the companies failed to maintain enough current assets.

Hence, liquidity position of both these companies wasnot goodfrom the period of 2012 to

2016.

Quick ratio:During the period of five yearsTesco succeed in attaining ideal ratio in 2014

and 2016. Hence, from 2014 to 2016 Tesco has maintainedenough current assets other

than inventory and prepaid expensesthat can easily be convertible into cash (Arkan and

et.al., 2016). Further,quick ratio of Sainsbury also inclined from .35 to .52 times in the

year of 2016. Thus,it can be stated that both the companies were able to meet their

monetary obligations.

Solvency ratios:Outcome ofratio shows that debt-equity ratio of Tesco was in line with the

ideal ratio in the year of2012 and2014. Moreover, during such perioddebt-equity ratio of the firm

was .56 & .62 respectively. On the contraryto this, such ratio of Tescowas exceeded ideal ratio to

in the year of 2015 and 2016. It shows that, in 2015 and 2016business unit raised more of its

fund from debt sources rather than equity. Hence, it is not good for the company because debt

instruments impose fix burden in front of company (Anwar and et.al., 2016). Moreover, in this,

company has to make paymentof interestwhichin turn closely affects monetary position and

performance of firm. Thus, for enhancing financial position and performance Tesco should keep

in mind ideal ratio such as .5:1 while determining the capital structure (Chiaramonte and Casu,

2016).Ratio analysis of Sainsbury shows that debt-equity ratio of the firm lies within the range of

.5:1. Moreover, from the period of 2012 to 2015,debt-equity ratio accounts within the category of

.32 to .46. Hence, it can be stated that solvency position or performance of Sainsbury was good

during such period as compared toTesco.

Efficiency ratios

years. Nevertheless current ratio of Tesco is very far from the ideal ratio which is 2:1

(MATTHEW, FADA and UKONU, 2016).On the other side,current ratio of Sainsbury

was .65, .61and .64 from the period of 2012 to 2014. In contrast to this, current ratio

accounts for .64 &.66 during the year 2015 and 2016.With the motive to enhance

customer base and market share both the companies are placing high level of emphasis on

promotional aspects and discounting strategies (Dopson and Hayes, 2016). It is one of the

main reasons due to which both the companies failed to maintain enough current assets.

Hence, liquidity position of both these companies wasnot goodfrom the period of 2012 to

2016.

Quick ratio:During the period of five yearsTesco succeed in attaining ideal ratio in 2014

and 2016. Hence, from 2014 to 2016 Tesco has maintainedenough current assets other

than inventory and prepaid expensesthat can easily be convertible into cash (Arkan and

et.al., 2016). Further,quick ratio of Sainsbury also inclined from .35 to .52 times in the

year of 2016. Thus,it can be stated that both the companies were able to meet their

monetary obligations.

Solvency ratios:Outcome ofratio shows that debt-equity ratio of Tesco was in line with the

ideal ratio in the year of2012 and2014. Moreover, during such perioddebt-equity ratio of the firm

was .56 & .62 respectively. On the contraryto this, such ratio of Tescowas exceeded ideal ratio to

in the year of 2015 and 2016. It shows that, in 2015 and 2016business unit raised more of its

fund from debt sources rather than equity. Hence, it is not good for the company because debt

instruments impose fix burden in front of company (Anwar and et.al., 2016). Moreover, in this,

company has to make paymentof interestwhichin turn closely affects monetary position and

performance of firm. Thus, for enhancing financial position and performance Tesco should keep

in mind ideal ratio such as .5:1 while determining the capital structure (Chiaramonte and Casu,

2016).Ratio analysis of Sainsbury shows that debt-equity ratio of the firm lies within the range of

.5:1. Moreover, from the period of 2012 to 2015,debt-equity ratio accounts within the category of

.32 to .46. Hence, it can be stated that solvency position or performance of Sainsbury was good

during such period as compared toTesco.

Efficiency ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Debtor’s turnover ratio is the one of the main elements of working capital management.

Moreover, company’s ability in relation to meeting the financial obligation is highly influenced

from the time period within which it will receive or collect money from debtors (Ahmad, 2016).

Hence, credit which is provided by the business organization to the customer has high level of

impact on working capital management. Moreover, in the absence of having enough funds it is

not possible for Tesco to carry out day to day activities more effectively and efficiently

(Inventory to Working Capital Analysis, 2016). Moreover, business organization itself purchases

material on a credit basis from suppliers. In this, if firm receives payment from debtors after long

time then it will find difficulty in making payment to creditors. Hence, by considering such

aspect it can be stated that debtor’s turnover ratio has significant impact on the aspects of

working capital management.

Along with this, high and low inventory turnover ratio also closely influences the aspects

of effective working capital management (Rakićević and et.al., 2016). Moreover, high inventory

turnover ratio presents that company is able to convert inventory into sales or cash more quickly.

Hence, such aspect has significant impact on company’s ability in relation to meeting of

monetary obligations (Bergo and et.al., 2016). Moreover, in the case of low inventory turnover

ratio, company is not in position to generate cash quickly by selling assets. Hence, both these are

the main two elements which in turn closely influences theworking capital management or

aspects of business organization.

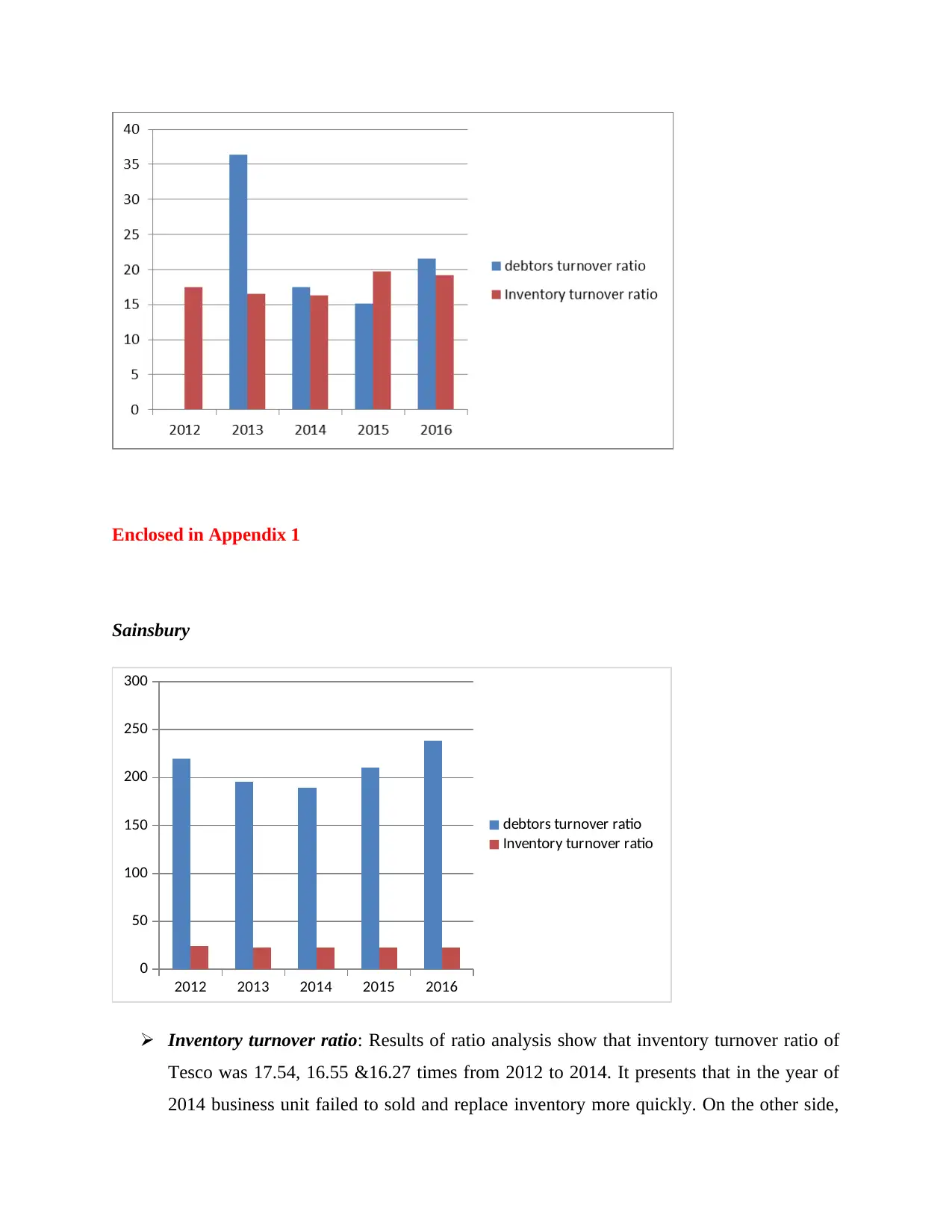

Enclosed in Appendix 2

Tesco

Moreover, company’s ability in relation to meeting the financial obligation is highly influenced

from the time period within which it will receive or collect money from debtors (Ahmad, 2016).

Hence, credit which is provided by the business organization to the customer has high level of

impact on working capital management. Moreover, in the absence of having enough funds it is

not possible for Tesco to carry out day to day activities more effectively and efficiently

(Inventory to Working Capital Analysis, 2016). Moreover, business organization itself purchases

material on a credit basis from suppliers. In this, if firm receives payment from debtors after long

time then it will find difficulty in making payment to creditors. Hence, by considering such

aspect it can be stated that debtor’s turnover ratio has significant impact on the aspects of

working capital management.

Along with this, high and low inventory turnover ratio also closely influences the aspects

of effective working capital management (Rakićević and et.al., 2016). Moreover, high inventory

turnover ratio presents that company is able to convert inventory into sales or cash more quickly.

Hence, such aspect has significant impact on company’s ability in relation to meeting of

monetary obligations (Bergo and et.al., 2016). Moreover, in the case of low inventory turnover

ratio, company is not in position to generate cash quickly by selling assets. Hence, both these are

the main two elements which in turn closely influences theworking capital management or

aspects of business organization.

Enclosed in Appendix 2

Tesco

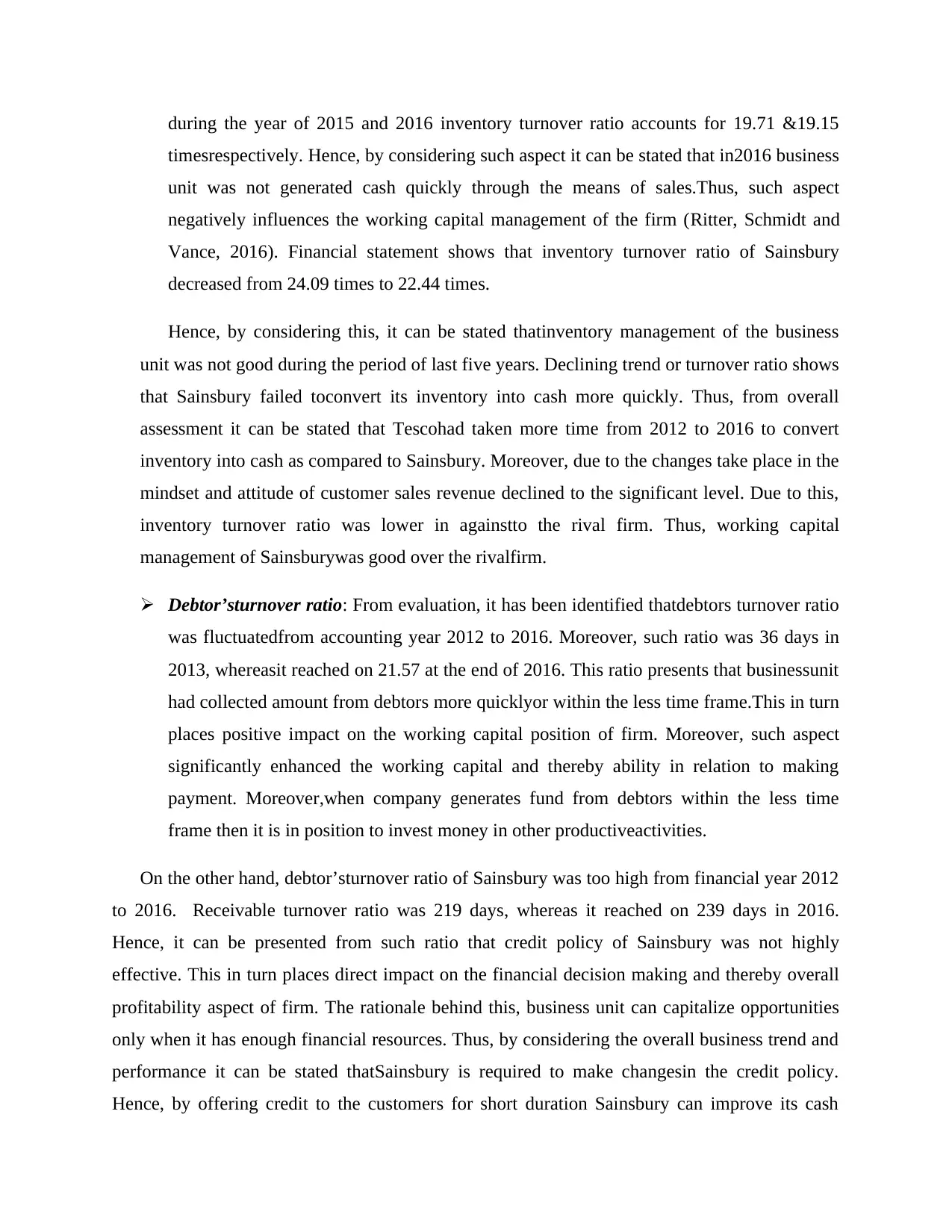

Enclosed in Appendix 1

Sainsbury

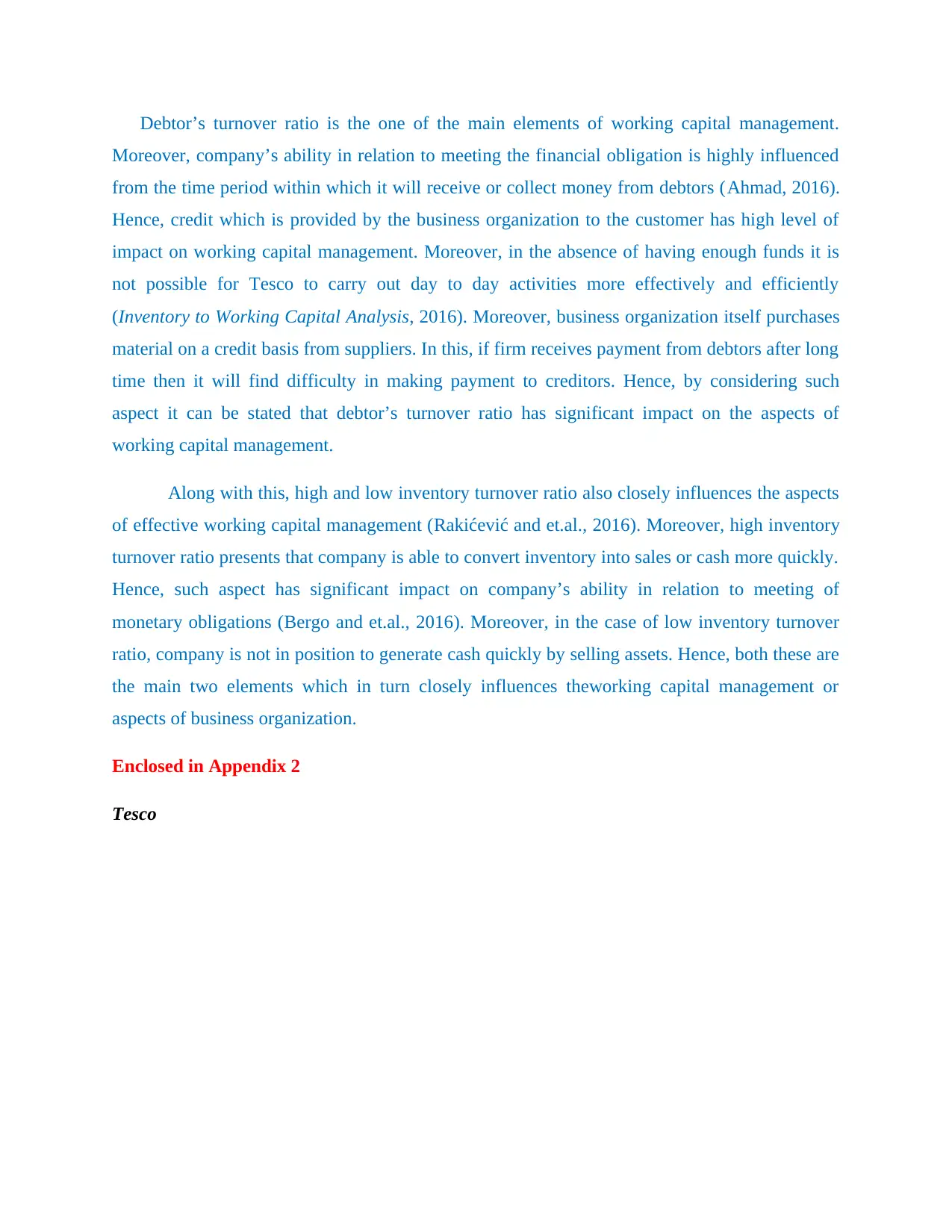

2012 2013 2014 2015 2016

0

50

100

150

200

250

300

debtors turnover ratio

Inventory turnover ratio

Inventory turnover ratio: Results of ratio analysis show that inventory turnover ratio of

Tesco was 17.54, 16.55 &16.27 times from 2012 to 2014. It presents that in the year of

2014 business unit failed to sold and replace inventory more quickly. On the other side,

Sainsbury

2012 2013 2014 2015 2016

0

50

100

150

200

250

300

debtors turnover ratio

Inventory turnover ratio

Inventory turnover ratio: Results of ratio analysis show that inventory turnover ratio of

Tesco was 17.54, 16.55 &16.27 times from 2012 to 2014. It presents that in the year of

2014 business unit failed to sold and replace inventory more quickly. On the other side,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

during the year of 2015 and 2016 inventory turnover ratio accounts for 19.71 &19.15

timesrespectively. Hence, by considering such aspect it can be stated that in2016 business

unit was not generated cash quickly through the means of sales.Thus, such aspect

negatively influences the working capital management of the firm (Ritter, Schmidt and

Vance, 2016). Financial statement shows that inventory turnover ratio of Sainsbury

decreased from 24.09 times to 22.44 times.

Hence, by considering this, it can be stated thatinventory management of the business

unit was not good during the period of last five years. Declining trend or turnover ratio shows

that Sainsbury failed toconvert its inventory into cash more quickly. Thus, from overall

assessment it can be stated that Tescohad taken more time from 2012 to 2016 to convert

inventory into cash as compared to Sainsbury. Moreover, due to the changes take place in the

mindset and attitude of customer sales revenue declined to the significant level. Due to this,

inventory turnover ratio was lower in againstto the rival firm. Thus, working capital

management of Sainsburywas good over the rivalfirm.

Debtor’sturnover ratio: From evaluation, it has been identified thatdebtors turnover ratio

was fluctuatedfrom accounting year 2012 to 2016. Moreover, such ratio was 36 days in

2013, whereasit reached on 21.57 at the end of 2016. This ratio presents that businessunit

had collected amount from debtors more quicklyor within the less time frame.This in turn

places positive impact on the working capital position of firm. Moreover, such aspect

significantly enhanced the working capital and thereby ability in relation to making

payment. Moreover,when company generates fund from debtors within the less time

frame then it is in position to invest money in other productiveactivities.

On the other hand, debtor’sturnover ratio of Sainsbury was too high from financial year 2012

to 2016. Receivable turnover ratio was 219 days, whereas it reached on 239 days in 2016.

Hence, it can be presented from such ratio that credit policy of Sainsbury was not highly

effective. This in turn places direct impact on the financial decision making and thereby overall

profitability aspect of firm. The rationale behind this, business unit can capitalize opportunities

only when it has enough financial resources. Thus, by considering the overall business trend and

performance it can be stated thatSainsbury is required to make changesin the credit policy.

Hence, by offering credit to the customers for short duration Sainsbury can improve its cash

timesrespectively. Hence, by considering such aspect it can be stated that in2016 business

unit was not generated cash quickly through the means of sales.Thus, such aspect

negatively influences the working capital management of the firm (Ritter, Schmidt and

Vance, 2016). Financial statement shows that inventory turnover ratio of Sainsbury

decreased from 24.09 times to 22.44 times.

Hence, by considering this, it can be stated thatinventory management of the business

unit was not good during the period of last five years. Declining trend or turnover ratio shows

that Sainsbury failed toconvert its inventory into cash more quickly. Thus, from overall

assessment it can be stated that Tescohad taken more time from 2012 to 2016 to convert

inventory into cash as compared to Sainsbury. Moreover, due to the changes take place in the

mindset and attitude of customer sales revenue declined to the significant level. Due to this,

inventory turnover ratio was lower in againstto the rival firm. Thus, working capital

management of Sainsburywas good over the rivalfirm.

Debtor’sturnover ratio: From evaluation, it has been identified thatdebtors turnover ratio

was fluctuatedfrom accounting year 2012 to 2016. Moreover, such ratio was 36 days in

2013, whereasit reached on 21.57 at the end of 2016. This ratio presents that businessunit

had collected amount from debtors more quicklyor within the less time frame.This in turn

places positive impact on the working capital position of firm. Moreover, such aspect

significantly enhanced the working capital and thereby ability in relation to making

payment. Moreover,when company generates fund from debtors within the less time

frame then it is in position to invest money in other productiveactivities.

On the other hand, debtor’sturnover ratio of Sainsbury was too high from financial year 2012

to 2016. Receivable turnover ratio was 219 days, whereas it reached on 239 days in 2016.

Hence, it can be presented from such ratio that credit policy of Sainsbury was not highly

effective. This in turn places direct impact on the financial decision making and thereby overall

profitability aspect of firm. The rationale behind this, business unit can capitalize opportunities

only when it has enough financial resources. Thus, by considering the overall business trend and

performance it can be stated thatSainsbury is required to make changesin the credit policy.

Hence, by offering credit to the customers for short duration Sainsbury can improve its cash

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

conversion cycle to the significant level. Moreover, less turnover entails that business unit

receives payment from debtors within the fewer time frames.

CONCLUSION

From this report, it has been concluded that profitability aspect or position ofTesco was

not sound in the last 5 years. In comparison to this, rival firm such as Sainsbury has generated

high profit in the highly stiff competitive situation. Besides this, it can be revealed from the

report thatboth the do not have amount of assets for meeting the current financial obligations.

This in turn closely influences the decision making of investors in the negative direction. Further,

it has been articulated that financial structure of Sainsbury wassound from 2012 to 2016 as

compared to rival firm. It can be summarized that Tesco needs to undertake significant action or

measure for making improvementin theinventory turnover ratio. By this, Tesco can enhance

working capital aspect or position and becomes able to meet obligations more quickly.

RECOMMENDATIONS

It is recommendedto Tesco that it should focus on the improvement of product quality

and services. Moreover, now customers consider and make evaluationof both the factors

such as price and quality aspects while making decision about purchase. Hence, by

making focus on such aspects Tesco can improve its productivity and thereby

profitability. Along with this, in the advertisements Tesco should the quality aspectof

product which in turn helps in enticing the decision making of large of customers and

thereby profitability.

Besides this, it is advised to Tesco to undertake either zero base or activity based

budgeting technique. This in turn helps them in making control on expenses to a great

extent. Moreover, such techniques facilitate optimum allocation of funds thereby helps in

reducing the level of expenses.

Further, Tesco needs to make focus onthe maintenance of current assetssuch as cash,

debtors etc. Hence, by maintainingsuch assets unit can improve its liquidity position and

aspects. For this purpose, Tesco needs to make continuous monitoring of expenses.By

doing this, company can maintain high level of liquidity.

receives payment from debtors within the fewer time frames.

CONCLUSION

From this report, it has been concluded that profitability aspect or position ofTesco was

not sound in the last 5 years. In comparison to this, rival firm such as Sainsbury has generated

high profit in the highly stiff competitive situation. Besides this, it can be revealed from the

report thatboth the do not have amount of assets for meeting the current financial obligations.

This in turn closely influences the decision making of investors in the negative direction. Further,

it has been articulated that financial structure of Sainsbury wassound from 2012 to 2016 as

compared to rival firm. It can be summarized that Tesco needs to undertake significant action or

measure for making improvementin theinventory turnover ratio. By this, Tesco can enhance

working capital aspect or position and becomes able to meet obligations more quickly.

RECOMMENDATIONS

It is recommendedto Tesco that it should focus on the improvement of product quality

and services. Moreover, now customers consider and make evaluationof both the factors

such as price and quality aspects while making decision about purchase. Hence, by

making focus on such aspects Tesco can improve its productivity and thereby

profitability. Along with this, in the advertisements Tesco should the quality aspectof

product which in turn helps in enticing the decision making of large of customers and

thereby profitability.

Besides this, it is advised to Tesco to undertake either zero base or activity based

budgeting technique. This in turn helps them in making control on expenses to a great

extent. Moreover, such techniques facilitate optimum allocation of funds thereby helps in

reducing the level of expenses.

Further, Tesco needs to make focus onthe maintenance of current assetssuch as cash,

debtors etc. Hence, by maintainingsuch assets unit can improve its liquidity position and

aspects. For this purpose, Tesco needs to make continuous monitoring of expenses.By

doing this, company can maintain high level of liquidity.

To prepare highly balanced financial Tesco should raise funds from equity sources in the

near future. It enables firm to ensure proper balance in thefinancial structureand thereby

makes improvement in the solvency position or aspects.

Tesco is required to develop positive image in the mind of customers regarding the

quality of products or services offered by it. Through this, business unit would become

ableto generate high cash by selling inventory more quickly.

near future. It enables firm to ensure proper balance in thefinancial structureand thereby

makes improvement in the solvency position or aspects.

Tesco is required to develop positive image in the mind of customers regarding the

quality of products or services offered by it. Through this, business unit would become

ableto generate high cash by selling inventory more quickly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.