Managerial Finance Report

VerifiedAdded on 2019/12/18

|19

|3560

|162

Report

AI Summary

This report analyzes the financial performance of Tesco and Sainsbury, two major UK supermarket chains, for the 2014/15 financial period. It uses ratio analysis to compare profitability (ROCE, net profit margin, gross profit margin), liquidity (current ratio, acid test ratio), efficiency (inventory turnover, asset turnover), and gearing (interest cover, earnings per share). The report finds that Sainsbury's generally outperforms Tesco across most ratios, particularly in profitability and liquidity. It also discusses the limitations of using financial ratios for interpreting firm performance, such as historical data limitations, inflation effects, and accounting policy differences. The second part of the report involves capital investment appraisal, specifically comparing two projects (A and B) using Net Present Value (NPV). Project A is recommended due to its higher positive NPV. The report concludes by highlighting the limitations of NPV, including sensitivity to the discount rate, exclusion of real options, and assumptions about future cash flows.

Managerial Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................2

Ratio Analysis..................................................................................................................................2

Profitability ratios........................................................................................................................2

The Return on Capital Employed (ROCE)..............................................................................3

Net Profit Margin.....................................................................................................................4

Gross Profit Margin.................................................................................................................4

Liquidity Ratio.............................................................................................................................5

Current Ratio...........................................................................................................................5

Acid Test Ratio........................................................................................................................6

Efficiency Ratio...........................................................................................................................6

Inventories turnover.................................................................................................................7

Assets Turnover.......................................................................................................................7

Gearing Ratio...............................................................................................................................8

Interest Cover...........................................................................................................................8

Earnings per share....................................................................................................................9

Introduction......................................................................................................................................2

Ratio Analysis..................................................................................................................................2

Profitability ratios........................................................................................................................2

The Return on Capital Employed (ROCE)..............................................................................3

Net Profit Margin.....................................................................................................................4

Gross Profit Margin.................................................................................................................4

Liquidity Ratio.............................................................................................................................5

Current Ratio...........................................................................................................................5

Acid Test Ratio........................................................................................................................6

Efficiency Ratio...........................................................................................................................6

Inventories turnover.................................................................................................................7

Assets Turnover.......................................................................................................................7

Gearing Ratio...............................................................................................................................8

Interest Cover...........................................................................................................................8

Earnings per share....................................................................................................................9

Recommendations of how the financial performance of the poorly performing business can be

improved..........................................................................................................................................9

Liquidity ratios...........................................................................................................................10

Efficiency ratios.........................................................................................................................10

Profitability ratios......................................................................................................................10

Leverage ratios...........................................................................................................................11

The limitations of relying on financial ratios to interpret firm performance.................................11

Portfolio 2; Capital Investment Appraisal.....................................................................................13

The limitations of using investment appraisal techniques to aid long term decision-making.......14

Bibliography..................................................................................................................................16

improved..........................................................................................................................................9

Liquidity ratios...........................................................................................................................10

Efficiency ratios.........................................................................................................................10

Profitability ratios......................................................................................................................10

Leverage ratios...........................................................................................................................11

The limitations of relying on financial ratios to interpret firm performance.................................11

Portfolio 2; Capital Investment Appraisal.....................................................................................13

The limitations of using investment appraisal techniques to aid long term decision-making.......14

Bibliography..................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Portfolio 1

Comparative analysis between Tesco limited and Sainsbury limited

Introduction

The report focus on examine the financial performance for two famous company (Sainsbury and

Tesco) in the retail market in UK. The report permits the comparison of the ratio analysis, in

which the profitability, liquidity, efficiency and gearing ratio is examined and recommendation

provided for the best companies from the examination of the ratio analysis for the financial

period 2014/15. Tesco is the global third largest retail company after Wal-Mart and Carrefour as

evaluated in term of income (2015). The company is the UK leading home supermarket chain.

The company has 2306 stores with more than 31% shareholding in UK market. Sainsbury is the

3rd biggest retail firm in the UK supermarket industry with it holding of more than 17% of UK

market shares.

Ratio Analysis

Profitability ratios

Profitability ratio indicates the profitability of the firm. The ratio covers the return on capital

employed, the net profit margin, and the gross profit margin as depicted in the table below.

TESCO Sainsbury's

PROFITABILTY RATIOS 2014 2015 2014 2015

Return on Capital Employed

(%) 4.65 -23.54 9.3 -1

Net Profit Margin (%) 1.53 -9.22 2.99 -0.7

Comparative analysis between Tesco limited and Sainsbury limited

Introduction

The report focus on examine the financial performance for two famous company (Sainsbury and

Tesco) in the retail market in UK. The report permits the comparison of the ratio analysis, in

which the profitability, liquidity, efficiency and gearing ratio is examined and recommendation

provided for the best companies from the examination of the ratio analysis for the financial

period 2014/15. Tesco is the global third largest retail company after Wal-Mart and Carrefour as

evaluated in term of income (2015). The company is the UK leading home supermarket chain.

The company has 2306 stores with more than 31% shareholding in UK market. Sainsbury is the

3rd biggest retail firm in the UK supermarket industry with it holding of more than 17% of UK

market shares.

Ratio Analysis

Profitability ratios

Profitability ratio indicates the profitability of the firm. The ratio covers the return on capital

employed, the net profit margin, and the gross profit margin as depicted in the table below.

TESCO Sainsbury's

PROFITABILTY RATIOS 2014 2015 2014 2015

Return on Capital Employed

(%) 4.65 -23.54 9.3 -1

Net Profit Margin (%) 1.53 -9.22 2.99 -0.7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

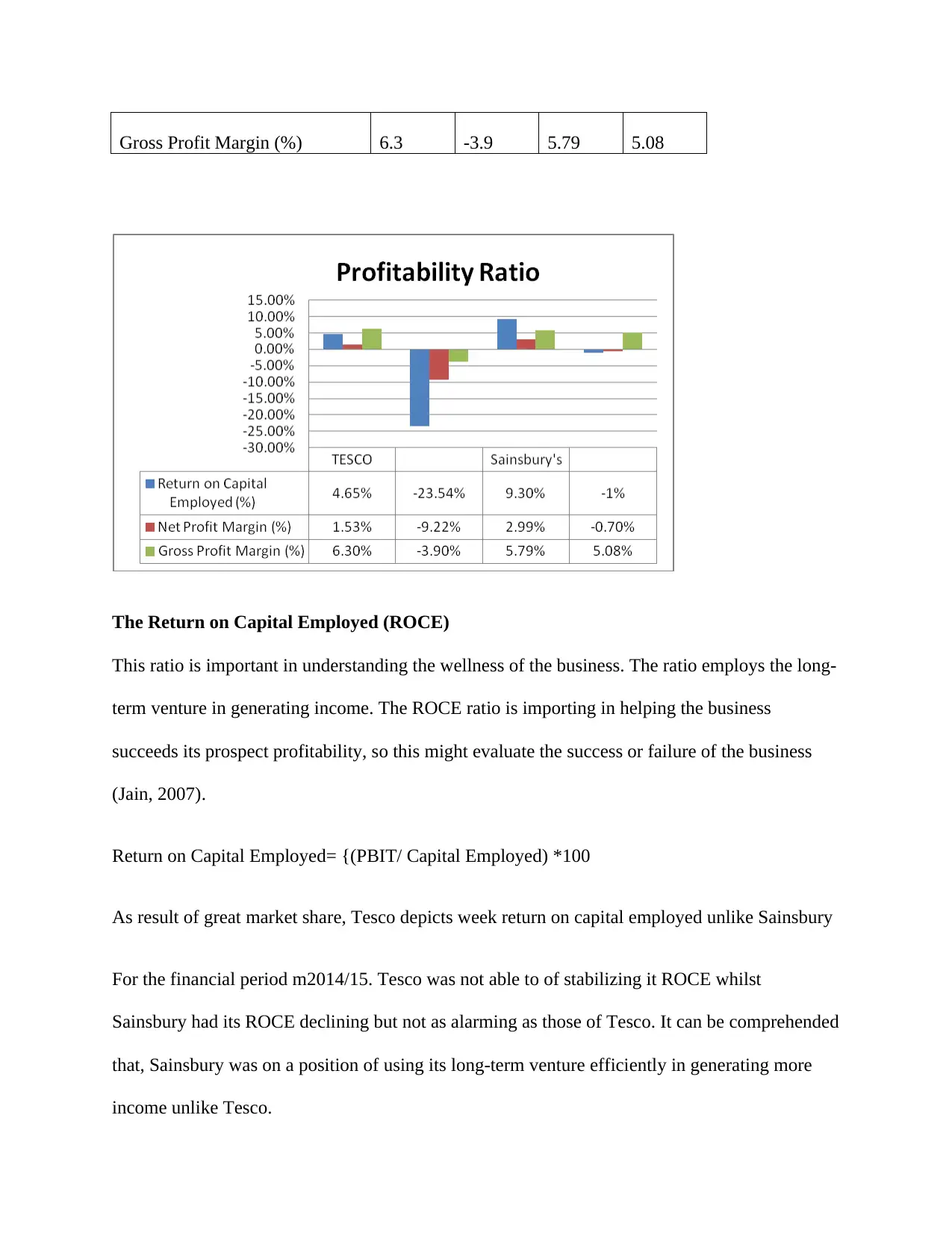

Gross Profit Margin (%) 6.3 -3.9 5.79 5.08

The Return on Capital Employed (ROCE)

This ratio is important in understanding the wellness of the business. The ratio employs the long-

term venture in generating income. The ROCE ratio is importing in helping the business

succeeds its prospect profitability, so this might evaluate the success or failure of the business

(Jain, 2007).

Return on Capital Employed= {(PBIT/ Capital Employed) *100

As result of great market share, Tesco depicts week return on capital employed unlike Sainsbury

For the financial period m2014/15. Tesco was not able to of stabilizing it ROCE whilst

Sainsbury had its ROCE declining but not as alarming as those of Tesco. It can be comprehended

that, Sainsbury was on a position of using its long-term venture efficiently in generating more

income unlike Tesco.

The Return on Capital Employed (ROCE)

This ratio is important in understanding the wellness of the business. The ratio employs the long-

term venture in generating income. The ROCE ratio is importing in helping the business

succeeds its prospect profitability, so this might evaluate the success or failure of the business

(Jain, 2007).

Return on Capital Employed= {(PBIT/ Capital Employed) *100

As result of great market share, Tesco depicts week return on capital employed unlike Sainsbury

For the financial period m2014/15. Tesco was not able to of stabilizing it ROCE whilst

Sainsbury had its ROCE declining but not as alarming as those of Tesco. It can be comprehended

that, Sainsbury was on a position of using its long-term venture efficiently in generating more

income unlike Tesco.

Net Profit Margin

The net profit margin appraises the amount of every pounds of income for the business keeps

earning which implies that a 5% net margin signifies that the business depict a net income of

0.05 pounds.

Net profit Margin= {Net income/sales)*100}

Specifically, the table above depict that Tesco’s profit margin was low unlike those of Sainsbury

for the financial period 2014/15, there was substantial plunge of Tesco’s profit margin from

1.53% to -9.22%. Sainsbury depict a decline in profit margin from 2.99% to -0.70%. In this

regards, it might be concluded that Sainsbury depict an ideal performance in terms of creating

income unlike Tesco for the financial period 2014/15.

Gross Profit Margin

The gross profit margin depicts the earning of the company after taking into consideration the

expense incurred by the business in producing the goods/service (Shi, 2001).

Gross Profit Margin = {Gross profit/ Sale Revenue}*100

From the table above, it can be observed that the gross profit margin for Sainsbury is much better

unlike for Tesco. Although Tesco depict a high portion of gross profit margin, there is a big

declining trend. Nevertheless, Sainsbury’s portion of gross profit margin is not as good as those

of Tesco limited.

The net profit margin appraises the amount of every pounds of income for the business keeps

earning which implies that a 5% net margin signifies that the business depict a net income of

0.05 pounds.

Net profit Margin= {Net income/sales)*100}

Specifically, the table above depict that Tesco’s profit margin was low unlike those of Sainsbury

for the financial period 2014/15, there was substantial plunge of Tesco’s profit margin from

1.53% to -9.22%. Sainsbury depict a decline in profit margin from 2.99% to -0.70%. In this

regards, it might be concluded that Sainsbury depict an ideal performance in terms of creating

income unlike Tesco for the financial period 2014/15.

Gross Profit Margin

The gross profit margin depicts the earning of the company after taking into consideration the

expense incurred by the business in producing the goods/service (Shi, 2001).

Gross Profit Margin = {Gross profit/ Sale Revenue}*100

From the table above, it can be observed that the gross profit margin for Sainsbury is much better

unlike for Tesco. Although Tesco depict a high portion of gross profit margin, there is a big

declining trend. Nevertheless, Sainsbury’s portion of gross profit margin is not as good as those

of Tesco limited.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Concerning the gross profit margin, it can be appraised from the table above that Sainsbury

depict better performance. Although Tesco depict a high portion of gross profit margin, this

shows that the profit margin is decline very fast unlike those of Sainsbury. Nevertheless,

Sainsbury portion of gross profit is not as good as those of Tesco but it might be depicted that

Sainsbury had slight decline in gross profit for the financial period 2014/15. In this regards, as

much as Sainsbury depicted a slight decline in gross profit, the company overall, depicted an

improvement.

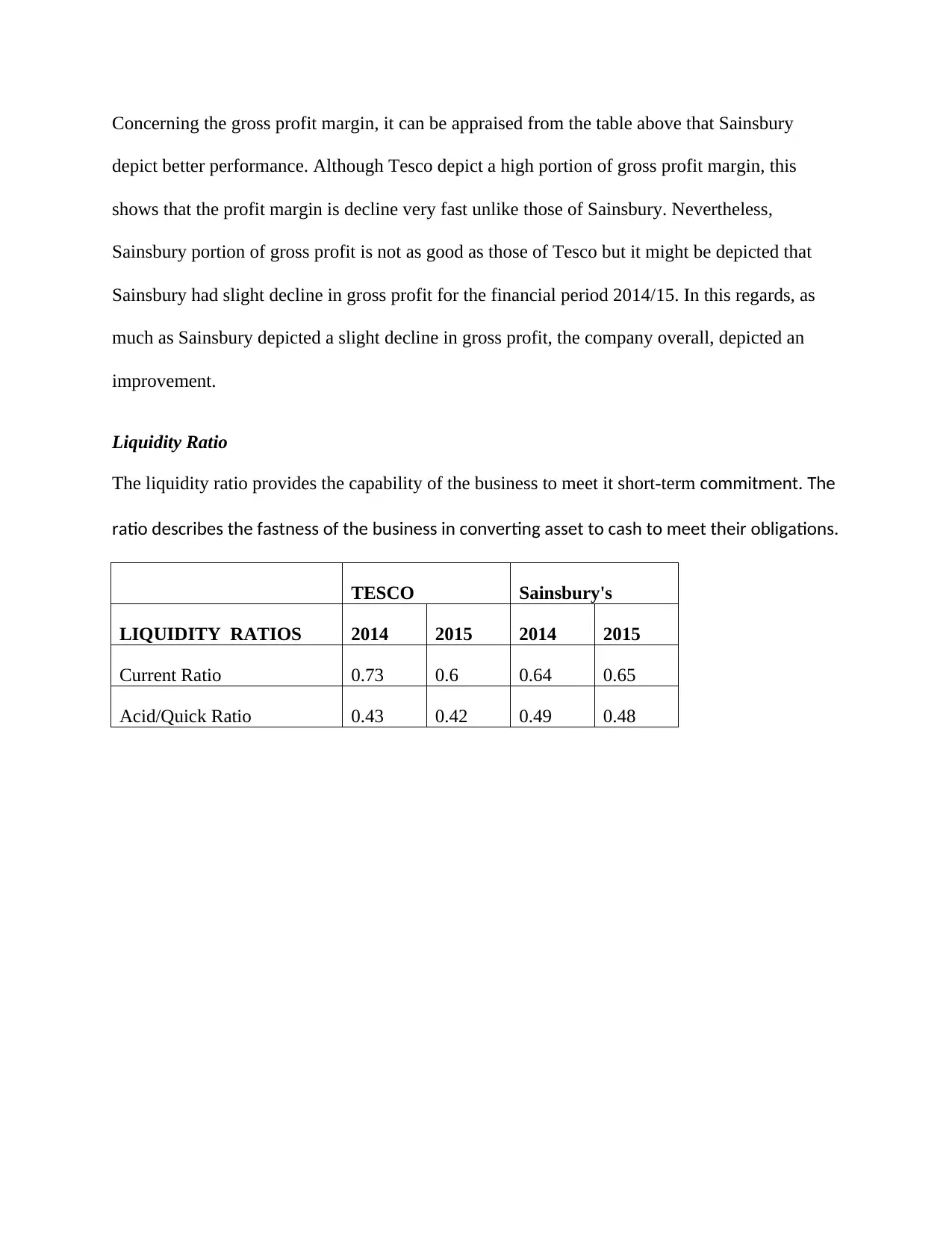

Liquidity Ratio

The liquidity ratio provides the capability of the business to meet it short-term commitment. The

ratio describes the fastness of the business in converting asset to cash to meet their obligations.

TESCO Sainsbury's

LIQUIDITY RATIOS 2014 2015 2014 2015

Current Ratio 0.73 0.6 0.64 0.65

Acid/Quick Ratio 0.43 0.42 0.49 0.48

depict better performance. Although Tesco depict a high portion of gross profit margin, this

shows that the profit margin is decline very fast unlike those of Sainsbury. Nevertheless,

Sainsbury portion of gross profit is not as good as those of Tesco but it might be depicted that

Sainsbury had slight decline in gross profit for the financial period 2014/15. In this regards, as

much as Sainsbury depicted a slight decline in gross profit, the company overall, depicted an

improvement.

Liquidity Ratio

The liquidity ratio provides the capability of the business to meet it short-term commitment. The

ratio describes the fastness of the business in converting asset to cash to meet their obligations.

TESCO Sainsbury's

LIQUIDITY RATIOS 2014 2015 2014 2015

Current Ratio 0.73 0.6 0.64 0.65

Acid/Quick Ratio 0.43 0.42 0.49 0.48

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

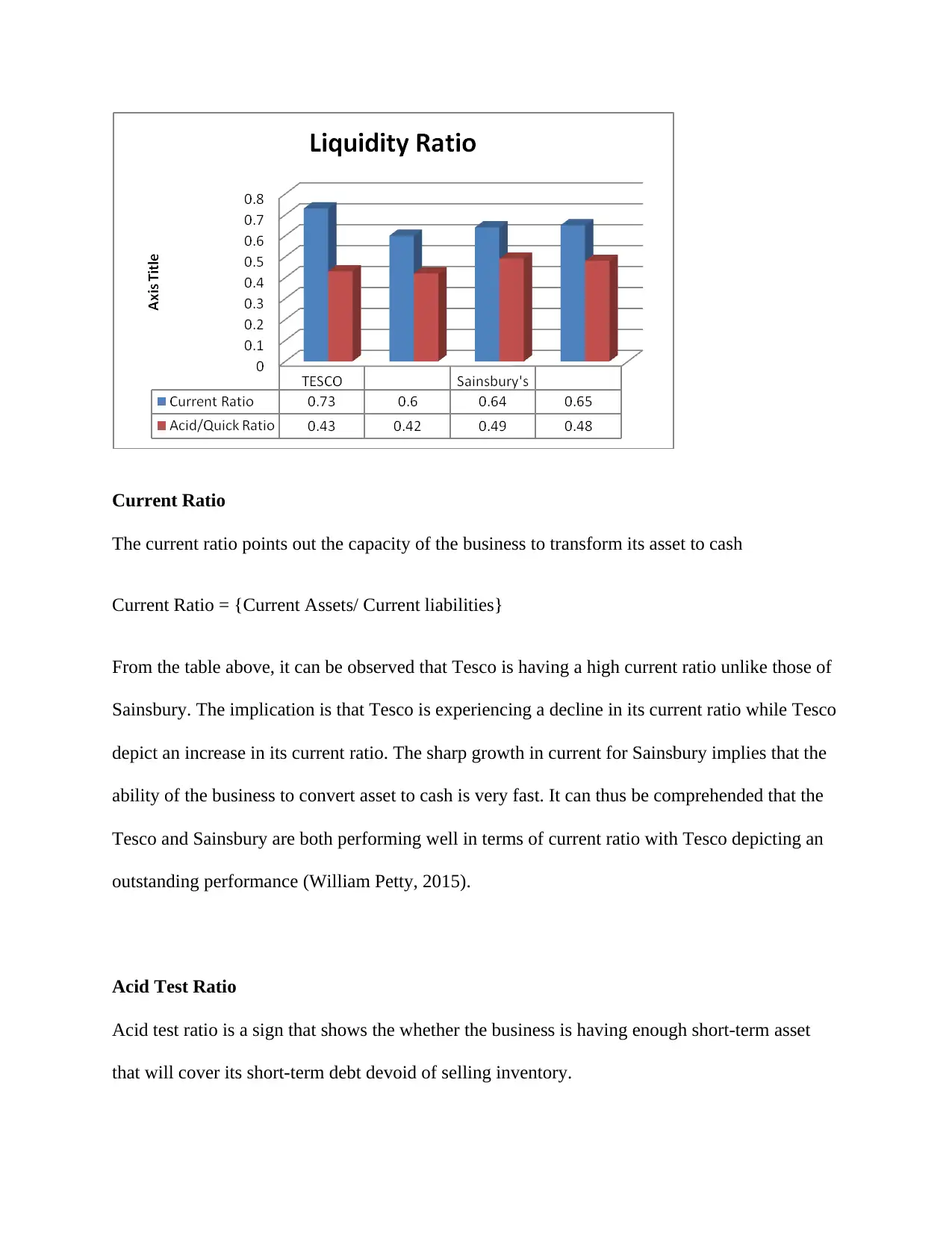

Current Ratio

The current ratio points out the capacity of the business to transform its asset to cash

Current Ratio = {Current Assets/ Current liabilities}

From the table above, it can be observed that Tesco is having a high current ratio unlike those of

Sainsbury. The implication is that Tesco is experiencing a decline in its current ratio while Tesco

depict an increase in its current ratio. The sharp growth in current for Sainsbury implies that the

ability of the business to convert asset to cash is very fast. It can thus be comprehended that the

Tesco and Sainsbury are both performing well in terms of current ratio with Tesco depicting an

outstanding performance (William Petty, 2015).

Acid Test Ratio

Acid test ratio is a sign that shows the whether the business is having enough short-term asset

that will cover its short-term debt devoid of selling inventory.

The current ratio points out the capacity of the business to transform its asset to cash

Current Ratio = {Current Assets/ Current liabilities}

From the table above, it can be observed that Tesco is having a high current ratio unlike those of

Sainsbury. The implication is that Tesco is experiencing a decline in its current ratio while Tesco

depict an increase in its current ratio. The sharp growth in current for Sainsbury implies that the

ability of the business to convert asset to cash is very fast. It can thus be comprehended that the

Tesco and Sainsbury are both performing well in terms of current ratio with Tesco depicting an

outstanding performance (William Petty, 2015).

Acid Test Ratio

Acid test ratio is a sign that shows the whether the business is having enough short-term asset

that will cover its short-term debt devoid of selling inventory.

Acid test ratio = {Current assets – Inventories} / Current liabilities

From the table above, it is evident that Sainsbury was better unlike Tesco limited implying that

Sainsbury depict sufficient short-term asset and the company does not need to sell its inventory

to meet its short-term debt (Peter, 2015).

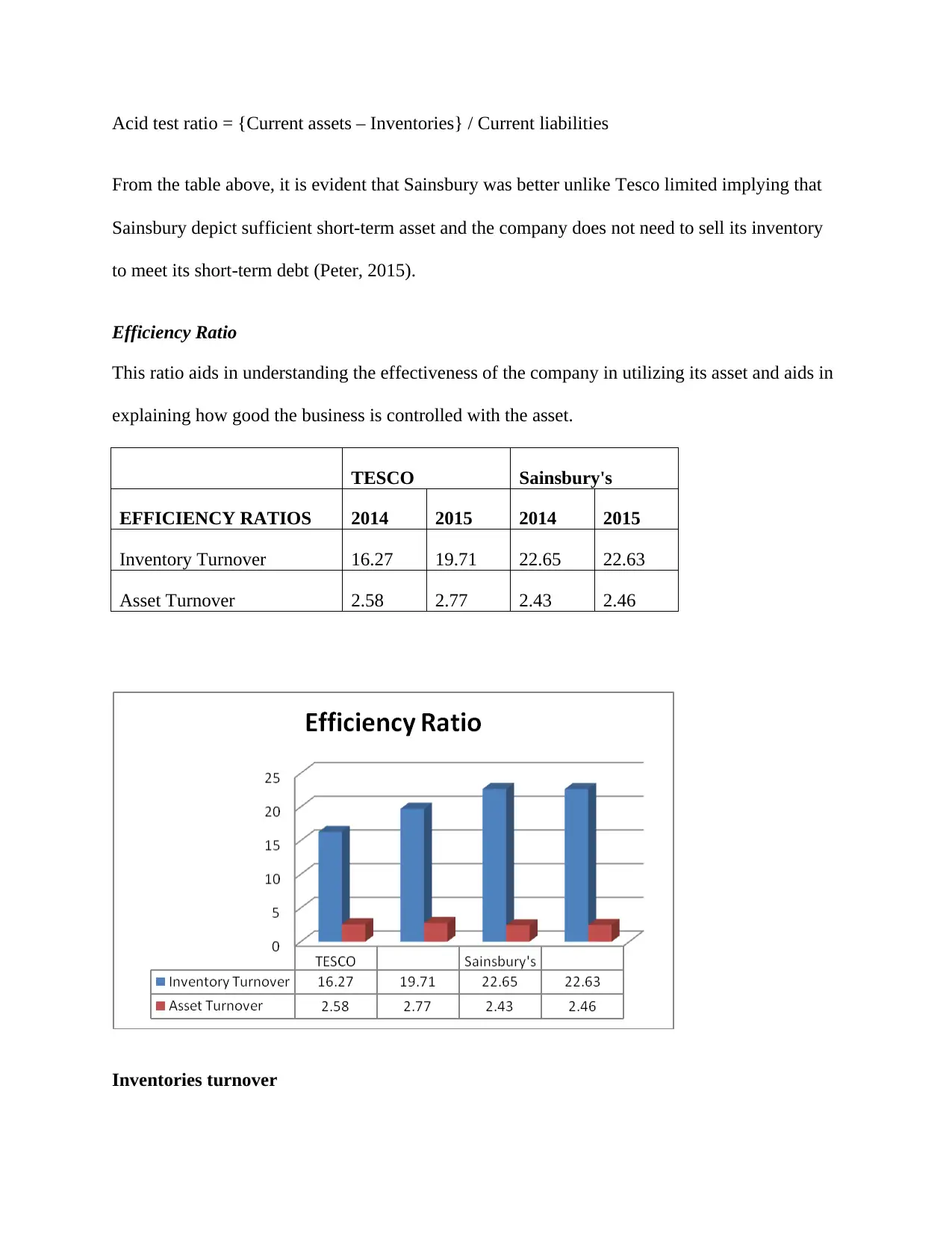

Efficiency Ratio

This ratio aids in understanding the effectiveness of the company in utilizing its asset and aids in

explaining how good the business is controlled with the asset.

TESCO Sainsbury's

EFFICIENCY RATIOS 2014 2015 2014 2015

Inventory Turnover 16.27 19.71 22.65 22.63

Asset Turnover 2.58 2.77 2.43 2.46

Inventories turnover

From the table above, it is evident that Sainsbury was better unlike Tesco limited implying that

Sainsbury depict sufficient short-term asset and the company does not need to sell its inventory

to meet its short-term debt (Peter, 2015).

Efficiency Ratio

This ratio aids in understanding the effectiveness of the company in utilizing its asset and aids in

explaining how good the business is controlled with the asset.

TESCO Sainsbury's

EFFICIENCY RATIOS 2014 2015 2014 2015

Inventory Turnover 16.27 19.71 22.65 22.63

Asset Turnover 2.58 2.77 2.43 2.46

Inventories turnover

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The inventory turnover is evaluated by days implying that the duration that is required to change

inventory to sales. As a result, the less the number of days, the better the performance of the

company.

Inventory Turnover (days) = {Inventory / Cost of sales} * 365

In specific, the table above depicts that the inventory turnover for Tesco will be able to transform

its inventories to cash within 16 to 19 days. On the other Hand, the inventory turnover for

Sainsbury is 22.65 to 22.63 for the financial period ending 2014/15 respectively. In this regards,

Tesco performed well in term of inventory turnover as compared to Sainsbury.

Assets Turnover

The Asset turnover ratio employed to define the wellness of the business in using its assets. The

amount of revenue generated per unit of assets. The higher the ratio, the better it is because it

implies that the business is making more income per unit of asset. The asset turnover for

Sainsbury is low as compared those of Tesco, which implies that the ability of Tesco to utilize its

assets is very effective unlike Sainsbury. Both firms depict an asset turnover that is steady for the

last two years which is good for Tesco and Sainsbury.

Asset Turnover = {Sale revenue / Total assets}

Gearing Ratio

The gearing ratio is a financial ratio that appraises the financial advantage, which signifies the

extent that the firm activities will be financed by owner’s funds versus the creditor’s funds. In

this regards, the higher the firms leverage level, the more the firm is deem to be risk since the

firm should keep on servicing its debt devoid of how bad the income is.

inventory to sales. As a result, the less the number of days, the better the performance of the

company.

Inventory Turnover (days) = {Inventory / Cost of sales} * 365

In specific, the table above depicts that the inventory turnover for Tesco will be able to transform

its inventories to cash within 16 to 19 days. On the other Hand, the inventory turnover for

Sainsbury is 22.65 to 22.63 for the financial period ending 2014/15 respectively. In this regards,

Tesco performed well in term of inventory turnover as compared to Sainsbury.

Assets Turnover

The Asset turnover ratio employed to define the wellness of the business in using its assets. The

amount of revenue generated per unit of assets. The higher the ratio, the better it is because it

implies that the business is making more income per unit of asset. The asset turnover for

Sainsbury is low as compared those of Tesco, which implies that the ability of Tesco to utilize its

assets is very effective unlike Sainsbury. Both firms depict an asset turnover that is steady for the

last two years which is good for Tesco and Sainsbury.

Asset Turnover = {Sale revenue / Total assets}

Gearing Ratio

The gearing ratio is a financial ratio that appraises the financial advantage, which signifies the

extent that the firm activities will be financed by owner’s funds versus the creditor’s funds. In

this regards, the higher the firms leverage level, the more the firm is deem to be risk since the

firm should keep on servicing its debt devoid of how bad the income is.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

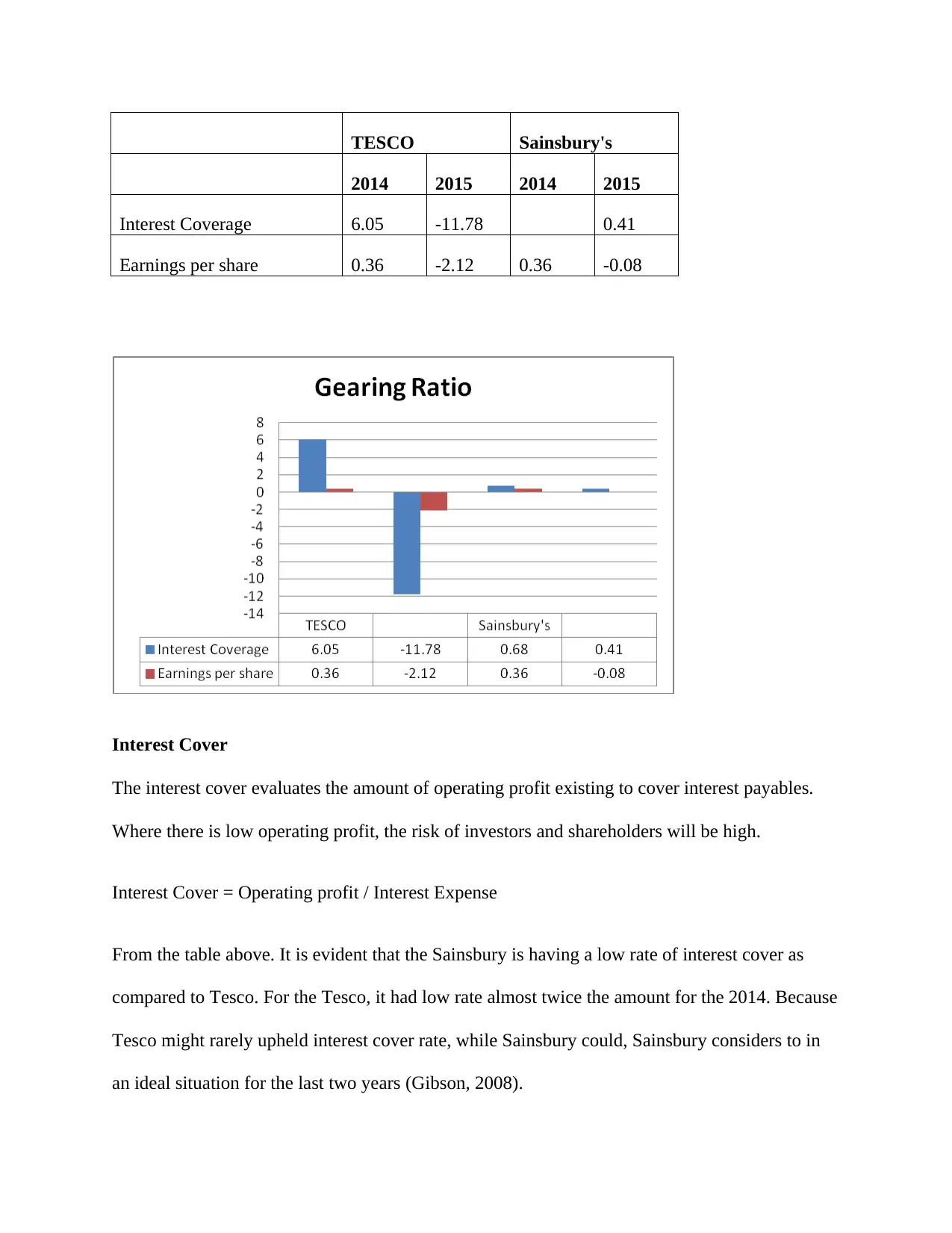

TESCO Sainsbury's

2014 2015 2014 2015

Interest Coverage 6.05 -11.78 0.41

Earnings per share 0.36 -2.12 0.36 -0.08

Interest Cover

The interest cover evaluates the amount of operating profit existing to cover interest payables.

Where there is low operating profit, the risk of investors and shareholders will be high.

Interest Cover = Operating profit / Interest Expense

From the table above. It is evident that the Sainsbury is having a low rate of interest cover as

compared to Tesco. For the Tesco, it had low rate almost twice the amount for the 2014. Because

Tesco might rarely upheld interest cover rate, while Sainsbury could, Sainsbury considers to in

an ideal situation for the last two years (Gibson, 2008).

2014 2015 2014 2015

Interest Coverage 6.05 -11.78 0.41

Earnings per share 0.36 -2.12 0.36 -0.08

Interest Cover

The interest cover evaluates the amount of operating profit existing to cover interest payables.

Where there is low operating profit, the risk of investors and shareholders will be high.

Interest Cover = Operating profit / Interest Expense

From the table above. It is evident that the Sainsbury is having a low rate of interest cover as

compared to Tesco. For the Tesco, it had low rate almost twice the amount for the 2014. Because

Tesco might rarely upheld interest cover rate, while Sainsbury could, Sainsbury considers to in

an ideal situation for the last two years (Gibson, 2008).

Earnings per share

Earnings per share depict the amount shareholder will receive as derived at the end of financial

period. Where the company provides improved earning per share each financial period, depict

that the business is improving in terms of profitability and expansion.

EPS= {Earning attributable to ordinary shareholders/ Number of shareholders}

From the table above, it is evident that both Tesco and Sainsbury depict a decline in EPS with

Tesco depict the worst decline EPS. The general implication is that Sainsbury is having better

business performance unlike Tesco about profit creations and business growth.

Recommendations of how the financial performance of the poorly performing business can

be improved

The best option to examine the financial health of the business and identification of areas for

improvement is observing closely the financial ratios. The ratios employed in making

comparison between diverse aspects of a firm’s performance or how the business is performing

poorly. Ratios must be evaluated monthly in order to ensure that top changing tends in the

business are maintained (Damodaran, 2010). Even though there are diverse terms for diverse

ratios, the ratio falls into four basic classes as explained below.

Liquidity ratios

The ratio evaluates the liquidity of the business that will be available in covering the debts and

providing wide overview of the financial, health of the business. The current ratio evaluates the

ability of the business to create cash to meet its short-term debt while the quick ratio evaluates

the ability of the business to have cash to support its debt requirement. High quick ratio is a sign

Earnings per share depict the amount shareholder will receive as derived at the end of financial

period. Where the company provides improved earning per share each financial period, depict

that the business is improving in terms of profitability and expansion.

EPS= {Earning attributable to ordinary shareholders/ Number of shareholders}

From the table above, it is evident that both Tesco and Sainsbury depict a decline in EPS with

Tesco depict the worst decline EPS. The general implication is that Sainsbury is having better

business performance unlike Tesco about profit creations and business growth.

Recommendations of how the financial performance of the poorly performing business can

be improved

The best option to examine the financial health of the business and identification of areas for

improvement is observing closely the financial ratios. The ratios employed in making

comparison between diverse aspects of a firm’s performance or how the business is performing

poorly. Ratios must be evaluated monthly in order to ensure that top changing tends in the

business are maintained (Damodaran, 2010). Even though there are diverse terms for diverse

ratios, the ratio falls into four basic classes as explained below.

Liquidity ratios

The ratio evaluates the liquidity of the business that will be available in covering the debts and

providing wide overview of the financial, health of the business. The current ratio evaluates the

ability of the business to create cash to meet its short-term debt while the quick ratio evaluates

the ability of the business to have cash to support its debt requirement. High quick ratio is a sign

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.