Comparative Analysis Report: Risk and Return of Portfolio Stocks

VerifiedAdded on 2021/05/30

|9

|1845

|228

Report

AI Summary

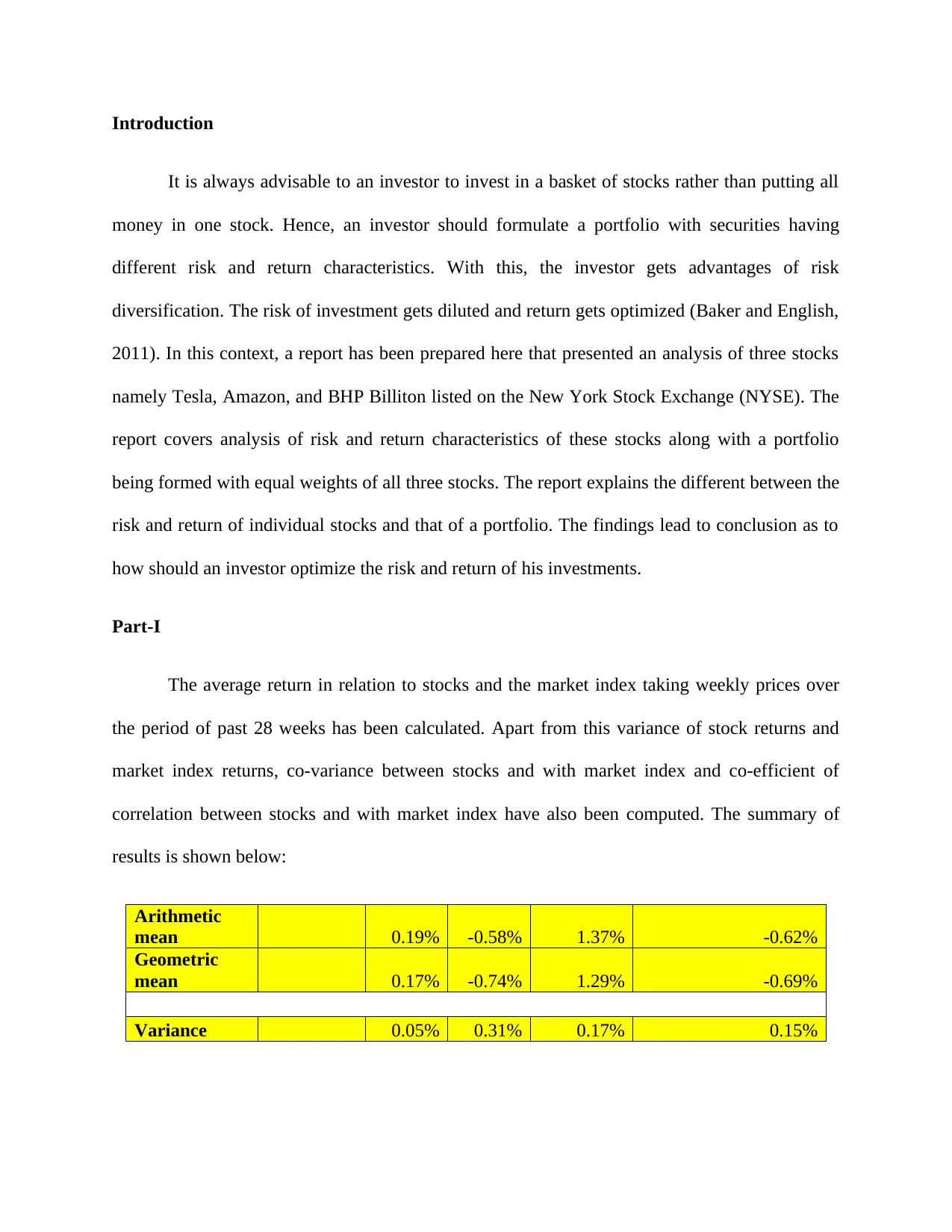

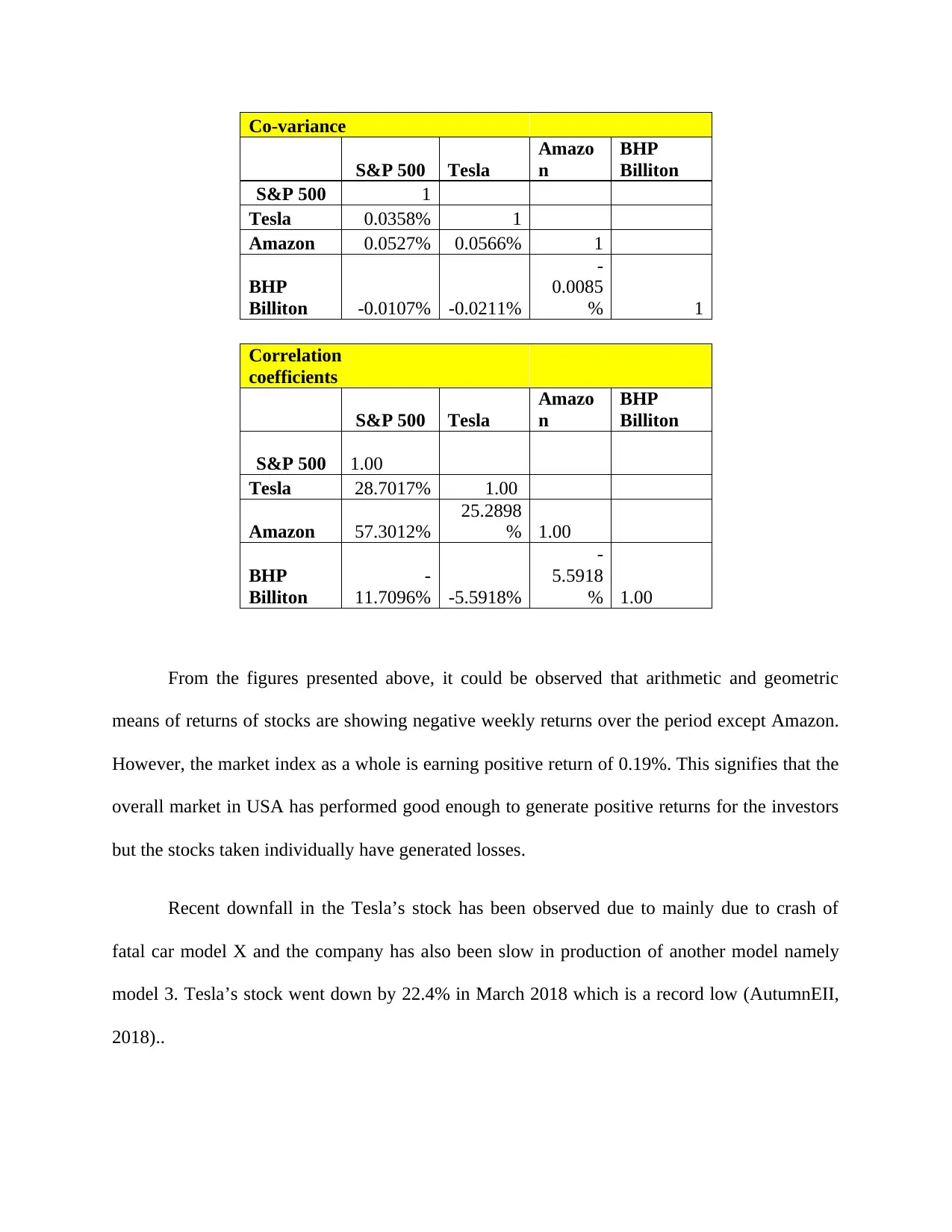

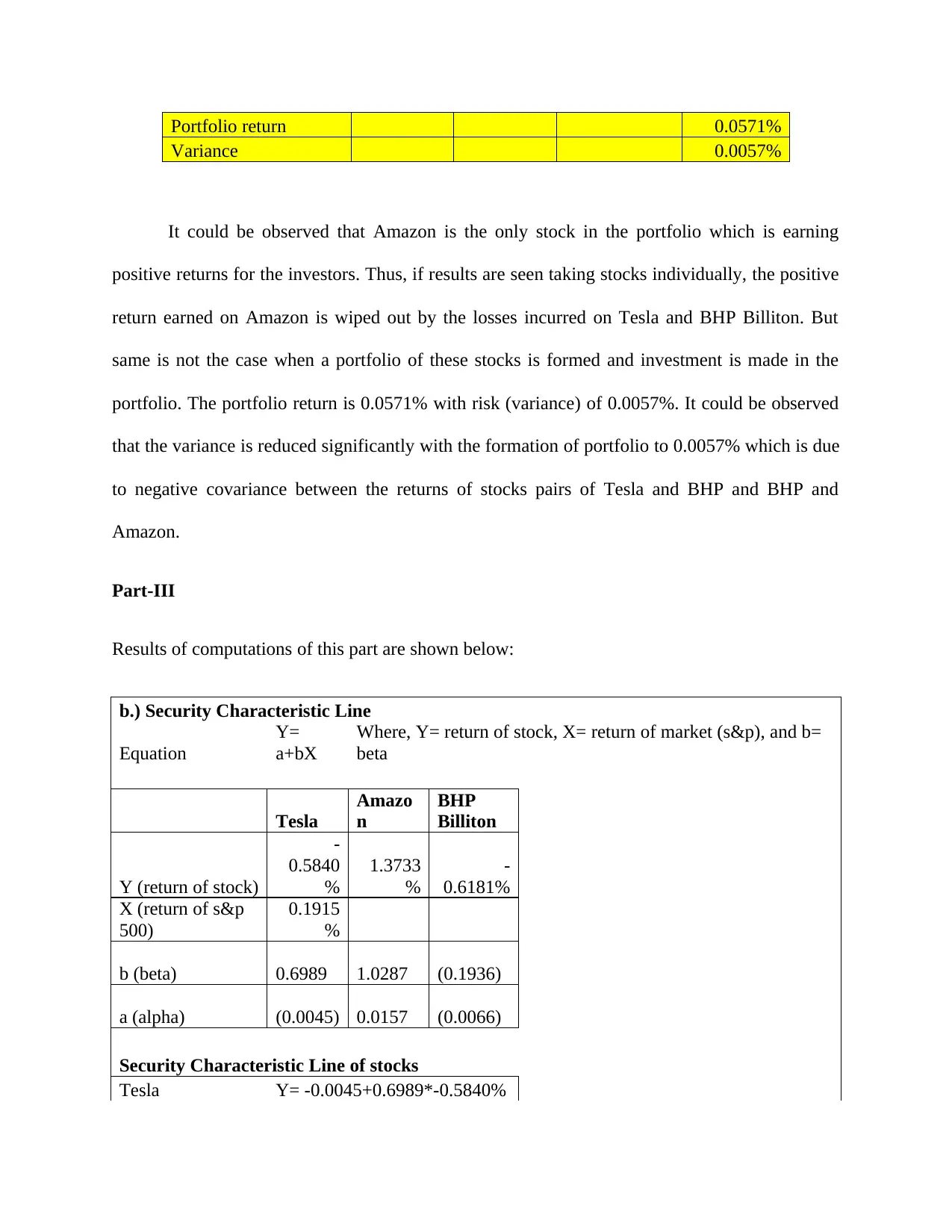

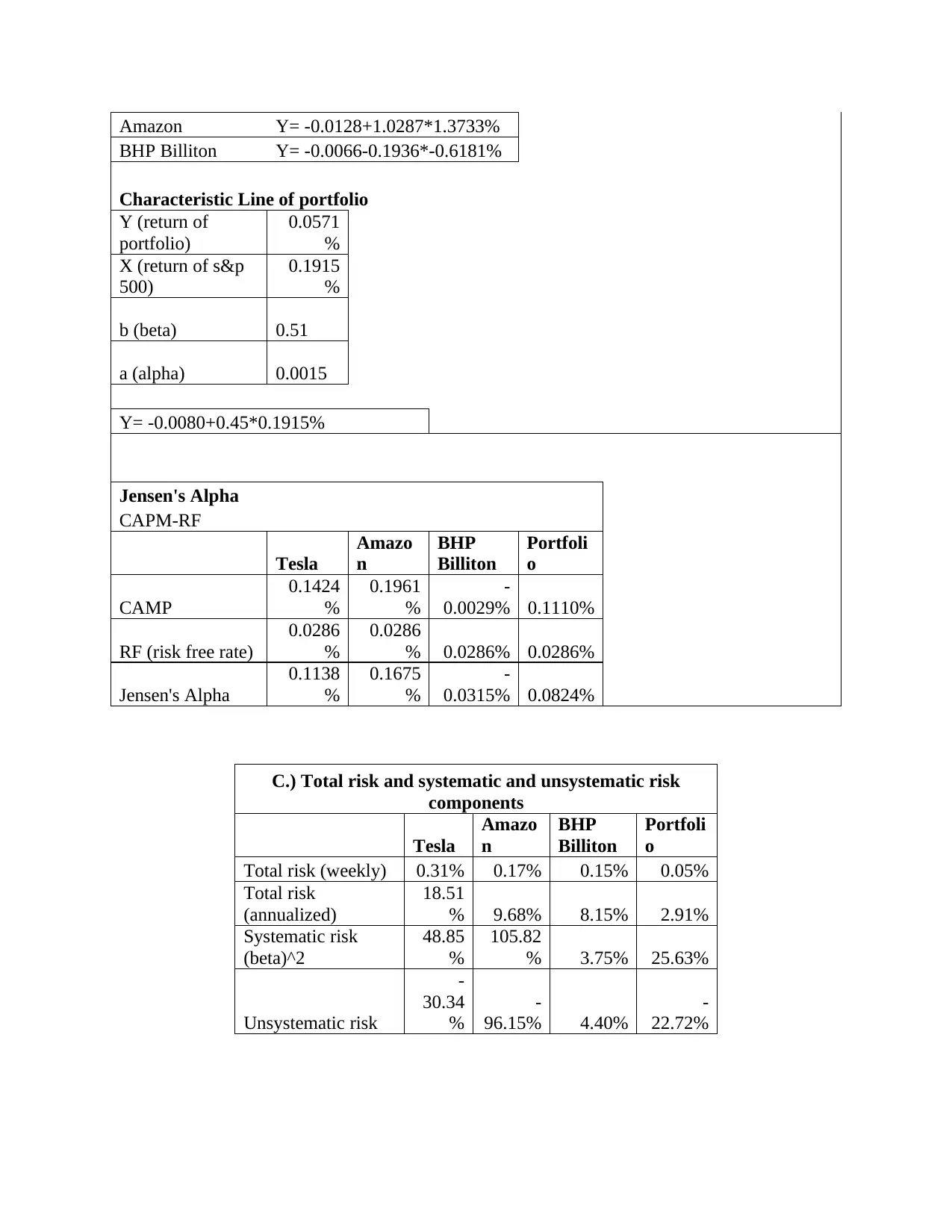

This report presents an analysis of portfolio management, focusing on the stocks of Tesla, Amazon, and BHP Billiton. It evaluates the risk and return characteristics of each stock, along with a portfolio constructed with equal weights of all three. The report examines weekly average returns, variances, covariances, and correlation coefficients, comparing individual stock performance to the portfolio's overall performance. The analysis includes calculations of beta, alpha, and systematic/unsystematic risk to assess the performance of each stock and the portfolio. Findings indicate that while individual stocks may exhibit losses, portfolio diversification can mitigate risk and optimize returns, as shown by the comparison of individual stock returns with portfolio returns and the reduction in variance. The report concludes with insights for investors seeking to optimize their investment strategies, considering both the benefits of diversification and the limitations of historical data-based analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.