TESLA INC 18 ANALYSING POSITION AND PERFORMANCE – WHERE TO NOW

VerifiedAdded on 2021/05/31

|13

|4163

|78

Report

AI Summary

This report provides a comprehensive financial analysis of Tesla Inc., examining its financial position and performance for the years 2016 and 2017. The analysis utilizes various financial ratios, including liquidity, leverage, and efficiency ratios, to assess the company's financial health. The report delves into key metrics such as the current ratio, quick ratio, working capital, debt ratio, debt-to-equity ratio, and equity ratio to evaluate Tesla's ability to manage its short-term and long-term obligations, as well as its overall solvency. The report also considers the company's business nature, focusing on electric vehicle manufacturing, energy storage, and solar panel production. The analysis aims to provide insights into Tesla's financial standing, identify potential risks, and offer recommendations regarding investment considerations. The report concludes with an overview of the company's financial position and performance, drawing conclusions from the calculated financial ratios and data analysis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................2

NAME OF COMPANY AND NATURE OF BUSINESS.......................................................................................3

ANALYSING THE POSITION OF THE COMPANY............................................................................................3

ANALYZING THE PERFORMANCE OF THE COMPANY...................................................................................7

CONCLUSION AND RECOMMENDATION.....................................................................................................9

REFERENCES................................................................................................................................................9

APPENDIX..................................................................................................................................................10

EXECUTIVE SUMMARY

The financial statement plays the significant role in assessing the results of the company. The

title of the report is analyzing the financial position and financial performance from the last two

years and as of now where the Tesla stands. As the title suggests, there are three major aims of

the report. The first major aim of the report is to analyze the financial position of the company

using the data from the annual report of the company. The second aim is to analyze the financial

performance of the company using the data from annual report of the company. Along with this

primary data, the report has used the secondary data sources. The last aim is to use the financial

ratios to understand the financial position and the financial performance of the company. With

these considerations the report has been prepared and divided into different sections.

INTRODUCTION

Financial position and the financial performance of the company can be judged only through the

financial statements of the company. The financial statements are embedded in the annual report

of the company. These financial statements are prepared for the users of the financial statements

so that they can have the meaningful and effective decision. In this report, the data of the

company – Tesla Inc has been obtained and the analyses have been done accordingly. The

company is listed in United States Stock Exchange. At first the name of company and the nature

of business of the company along with the background of the company have been detailed. After

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................2

NAME OF COMPANY AND NATURE OF BUSINESS.......................................................................................3

ANALYSING THE POSITION OF THE COMPANY............................................................................................3

ANALYZING THE PERFORMANCE OF THE COMPANY...................................................................................7

CONCLUSION AND RECOMMENDATION.....................................................................................................9

REFERENCES................................................................................................................................................9

APPENDIX..................................................................................................................................................10

EXECUTIVE SUMMARY

The financial statement plays the significant role in assessing the results of the company. The

title of the report is analyzing the financial position and financial performance from the last two

years and as of now where the Tesla stands. As the title suggests, there are three major aims of

the report. The first major aim of the report is to analyze the financial position of the company

using the data from the annual report of the company. The second aim is to analyze the financial

performance of the company using the data from annual report of the company. Along with this

primary data, the report has used the secondary data sources. The last aim is to use the financial

ratios to understand the financial position and the financial performance of the company. With

these considerations the report has been prepared and divided into different sections.

INTRODUCTION

Financial position and the financial performance of the company can be judged only through the

financial statements of the company. The financial statements are embedded in the annual report

of the company. These financial statements are prepared for the users of the financial statements

so that they can have the meaningful and effective decision. In this report, the data of the

company – Tesla Inc has been obtained and the analyses have been done accordingly. The

company is listed in United States Stock Exchange. At first the name of company and the nature

of business of the company along with the background of the company have been detailed. After

that through the annual report of the company the financial position of the company has been

analysed. For the purpose of the analyses, the annual report of the company for the year ending

31st of December 2017 and 31st of December 2016 has been considered. Two years have been

considered for the same company only because of the fact of having more clear and precise

comparison with earlier year as base for computation. Then the financial performance of the

company has been analysed as to whether the company is making profits or not and whether the

company is generating the higher earnings to their investors. There are three methods for

analyses – one is vertical, other one is horizontal and the last one is ratio analysis. In the given

report, the ratio analyses have been considered. The analyses have been made with reference to

the accounting ratios for profitability as well as liquidity. After the analyses, the appropriate

conclusion and the recommendation has been suggested as to whether the investors shall invest

in this company or not keeping in consideration all the analyses made from the financial

statements.

NAME OF COMPANY AND NATURE OF BUSINESS

For the purpose of conducting the analyses, the financial data of company – Tesla Inc has been

taken. Tesla Inc formed in the year of two thousand and thirteen in Delaware, United States of

America. Its headquarters are located in Palo Alto, California, United States of America. The

company is engaged in the manufacturing of the all types of electric vehicles, storage devices for

energy and solar panel. The company has the production facilities and plants for assembly at

different locations. Since the year of its operations, the company has been earning profits and

good reputation in the market. The company uses the calendar year as the financial year and ends

the financial statements by 31st of December of each year. Therefore the form 10K has been

considered for obtaining the data and figures.

ANALYSING THE POSITION OF THE COMPANY

Position is related to the standing as on particular date. In the common parlance if the personnel

working in an organization has been promoted from Manager to Director of the company then

the position of that personnel earlier was Manager and now he is working ad Director of the

company (Anastasia, 2015). The position is identified at the particular point of time. Similarly in

case of company the financial position of the company can obtained only at the particular date

analysed. For the purpose of the analyses, the annual report of the company for the year ending

31st of December 2017 and 31st of December 2016 has been considered. Two years have been

considered for the same company only because of the fact of having more clear and precise

comparison with earlier year as base for computation. Then the financial performance of the

company has been analysed as to whether the company is making profits or not and whether the

company is generating the higher earnings to their investors. There are three methods for

analyses – one is vertical, other one is horizontal and the last one is ratio analysis. In the given

report, the ratio analyses have been considered. The analyses have been made with reference to

the accounting ratios for profitability as well as liquidity. After the analyses, the appropriate

conclusion and the recommendation has been suggested as to whether the investors shall invest

in this company or not keeping in consideration all the analyses made from the financial

statements.

NAME OF COMPANY AND NATURE OF BUSINESS

For the purpose of conducting the analyses, the financial data of company – Tesla Inc has been

taken. Tesla Inc formed in the year of two thousand and thirteen in Delaware, United States of

America. Its headquarters are located in Palo Alto, California, United States of America. The

company is engaged in the manufacturing of the all types of electric vehicles, storage devices for

energy and solar panel. The company has the production facilities and plants for assembly at

different locations. Since the year of its operations, the company has been earning profits and

good reputation in the market. The company uses the calendar year as the financial year and ends

the financial statements by 31st of December of each year. Therefore the form 10K has been

considered for obtaining the data and figures.

ANALYSING THE POSITION OF THE COMPANY

Position is related to the standing as on particular date. In the common parlance if the personnel

working in an organization has been promoted from Manager to Director of the company then

the position of that personnel earlier was Manager and now he is working ad Director of the

company (Anastasia, 2015). The position is identified at the particular point of time. Similarly in

case of company the financial position of the company can obtained only at the particular date

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and point of time. For instance, the company provides the financial statements on 31st of

December 2017 then the financial position can be judged only on that day itself.

The position of the company is analysed through the statement of the affairs or the balance sheet

of the company as the case may be. Financial position will not only help in assessing the net

worth of the company but also helps in the knowing of the fact as to whether the company has

enough liquid funds, whether the assets have been correctly valued or not, whether the company

is able to achieve its short term liabilities as and when it becomes due and whether the

company’s long term liabilities as stated in the balance sheet is at par or it has exceeded the

limits and so on (Taylor, 2011). For making analyses the financial ratios have been calculated

and then analyses have been made. Ratio has been calculated under the four major headings. One

is profitability ratios, second is Liquidity ratio, third is Leverage Ratio and the last is the

efficiency ratio. The ratios have been calculated for two years ending the 31st of December 2017

and 31st of December 2016. It is because the benchmark as 2016 figures has been considered for

the purpose of the analyses. The financial ratios have been calculated and identified and

accordingly the analyses have been made.

Liquidity Ratio – Liquidity ratio is one of the best measure through which the manager of the

company can judge or assess the ability of the company to repay the short term liabilities

including the liabilities towards the expenses. If the company is not maintaining its liquidity ratio

at good level there will be chances that the company will go bankrupt or insolvent. Directors of

the company are separately more concerned when the company fails to serve the interest and

principal obligations when it falls due (Delen, 2013). It is because the liability of the directors of

the company will be personal if the deposit of liabilities has not been maintained.

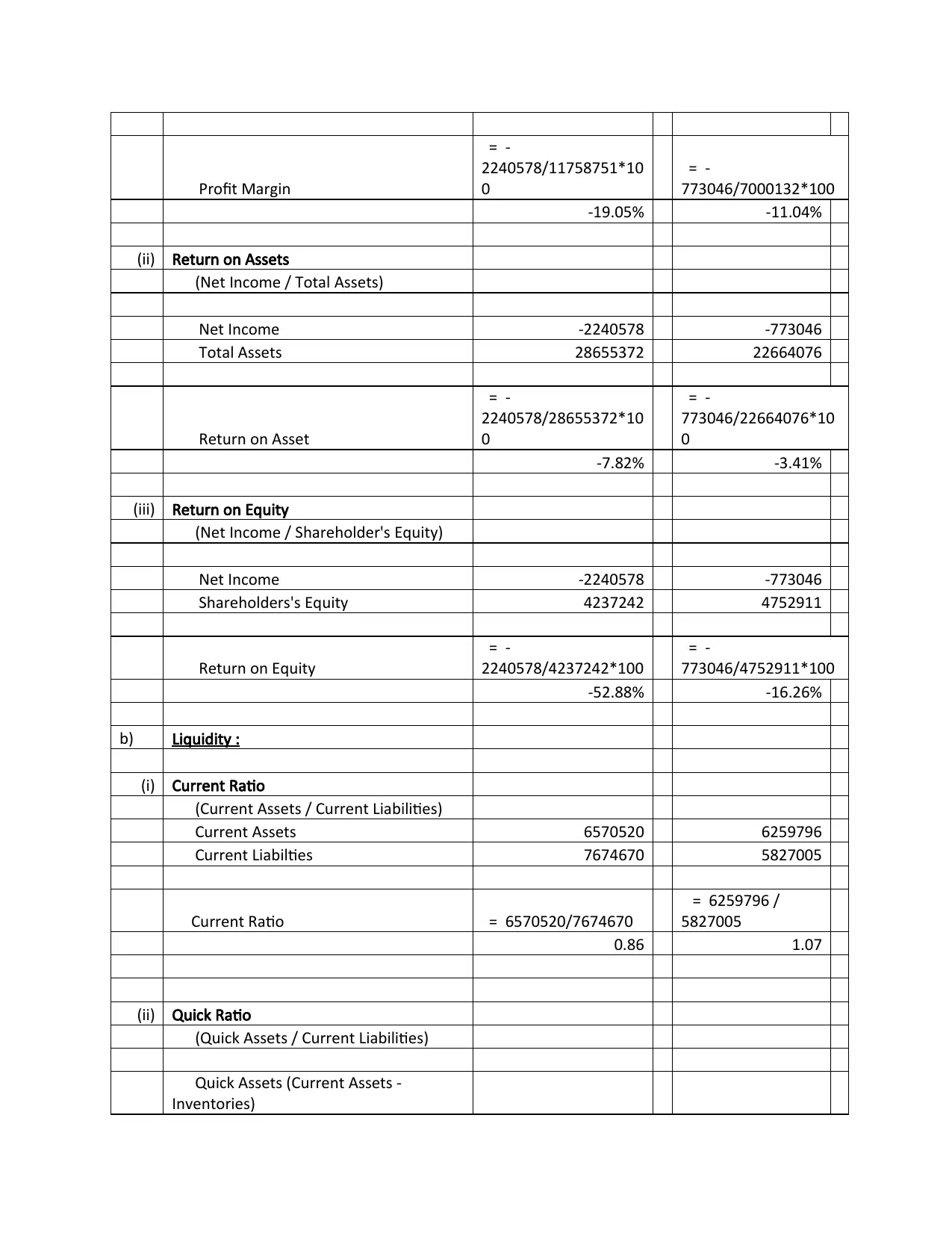

- Current Ratio – It is one of the basic ratios which every company considers before

finalizing the financial statements of the company. At first the current ratio is the

financial ratio which helps in comparing the current assets and current liabilities. It

compares as to whether the company will be able to make the payment of the liabilities

that is due in the near future and that too shall be paid within the period of one year. In

the given case of Tesla Inc, the current ratio for the year 2016 was 1.07 and for the year

2017 it was 0.86. The decrease in current ratio is the tremendous one. It means that the

current ratio has fallen down and it has been fallen by 80 cents. There are the chances

December 2017 then the financial position can be judged only on that day itself.

The position of the company is analysed through the statement of the affairs or the balance sheet

of the company as the case may be. Financial position will not only help in assessing the net

worth of the company but also helps in the knowing of the fact as to whether the company has

enough liquid funds, whether the assets have been correctly valued or not, whether the company

is able to achieve its short term liabilities as and when it becomes due and whether the

company’s long term liabilities as stated in the balance sheet is at par or it has exceeded the

limits and so on (Taylor, 2011). For making analyses the financial ratios have been calculated

and then analyses have been made. Ratio has been calculated under the four major headings. One

is profitability ratios, second is Liquidity ratio, third is Leverage Ratio and the last is the

efficiency ratio. The ratios have been calculated for two years ending the 31st of December 2017

and 31st of December 2016. It is because the benchmark as 2016 figures has been considered for

the purpose of the analyses. The financial ratios have been calculated and identified and

accordingly the analyses have been made.

Liquidity Ratio – Liquidity ratio is one of the best measure through which the manager of the

company can judge or assess the ability of the company to repay the short term liabilities

including the liabilities towards the expenses. If the company is not maintaining its liquidity ratio

at good level there will be chances that the company will go bankrupt or insolvent. Directors of

the company are separately more concerned when the company fails to serve the interest and

principal obligations when it falls due (Delen, 2013). It is because the liability of the directors of

the company will be personal if the deposit of liabilities has not been maintained.

- Current Ratio – It is one of the basic ratios which every company considers before

finalizing the financial statements of the company. At first the current ratio is the

financial ratio which helps in comparing the current assets and current liabilities. It

compares as to whether the company will be able to make the payment of the liabilities

that is due in the near future and that too shall be paid within the period of one year. In

the given case of Tesla Inc, the current ratio for the year 2016 was 1.07 and for the year

2017 it was 0.86. The decrease in current ratio is the tremendous one. It means that the

current ratio has fallen down and it has been fallen by 80 cents. There are the chances

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

from the side of the company that there will be inability to pay off the short term

liabilities in near future. If the situation still persist then the there is high probability of

having the company insolvent. Therefore, the current ratio shall be worked out. .

- Quick Ratio – The quick ratio deals with the ability of the company to generate the cash

and its equivalent to pay off the liabilities. The deciding factor of the quick ratio is that

higher the quick ratio, higher are the chances for the company to pay off its debts as the

company will be able to meet off the liabilities very fast. For calculation of the quick

ratio the amount of inventory is reduced from the current assets. In the given case the

quick ratio for the year ending 31st of December 2017 is 0.56 and for the year ending 31st

of December 2016 as 0.72. There has also seen the decrease in percentage due to which

there are the high probability that the company might get itself as insolvent.

- Working Capital – Working capital is the capital which every company requires to

generate and operate the working capital cycle or the operating cycle. Without

mentioning the operating cycle and working capital required, no company can perform its

function very well. In simpler words working capital is the safety which is required to be

kept so as to meet the expenses in the near future. In the given case, the company has the

negative working capital of $1104150 thousands in 2017 and in 2016; the company has

positive working capital as $432791. It means that the working capital condition of the

company is not good in this year as compared to the earlier year. Due to negative

working capital neither any of the financial institutions will provide the finance to the

company nor would the company have the enough capital to fund their own leading to the

situation of short term insolvent.

Leverage Ratio / Solvency Ratio – The liquidity is related to the short term obligations and

related payments and the solvency ratio is related to future obligations for more than one year

and related payments. The leverage ratio helps in understanding what should be the structure of

the capital of the company so as to enable the company to obtain the debt financing so as to

maximize the return to the shareholders of the company (Drake, 2010). These ratios are very

important for every company in assessing the risk profile of the company. The leverage /

solvency ratios are mentioned below:

liabilities in near future. If the situation still persist then the there is high probability of

having the company insolvent. Therefore, the current ratio shall be worked out. .

- Quick Ratio – The quick ratio deals with the ability of the company to generate the cash

and its equivalent to pay off the liabilities. The deciding factor of the quick ratio is that

higher the quick ratio, higher are the chances for the company to pay off its debts as the

company will be able to meet off the liabilities very fast. For calculation of the quick

ratio the amount of inventory is reduced from the current assets. In the given case the

quick ratio for the year ending 31st of December 2017 is 0.56 and for the year ending 31st

of December 2016 as 0.72. There has also seen the decrease in percentage due to which

there are the high probability that the company might get itself as insolvent.

- Working Capital – Working capital is the capital which every company requires to

generate and operate the working capital cycle or the operating cycle. Without

mentioning the operating cycle and working capital required, no company can perform its

function very well. In simpler words working capital is the safety which is required to be

kept so as to meet the expenses in the near future. In the given case, the company has the

negative working capital of $1104150 thousands in 2017 and in 2016; the company has

positive working capital as $432791. It means that the working capital condition of the

company is not good in this year as compared to the earlier year. Due to negative

working capital neither any of the financial institutions will provide the finance to the

company nor would the company have the enough capital to fund their own leading to the

situation of short term insolvent.

Leverage Ratio / Solvency Ratio – The liquidity is related to the short term obligations and

related payments and the solvency ratio is related to future obligations for more than one year

and related payments. The leverage ratio helps in understanding what should be the structure of

the capital of the company so as to enable the company to obtain the debt financing so as to

maximize the return to the shareholders of the company (Drake, 2010). These ratios are very

important for every company in assessing the risk profile of the company. The leverage /

solvency ratios are mentioned below:

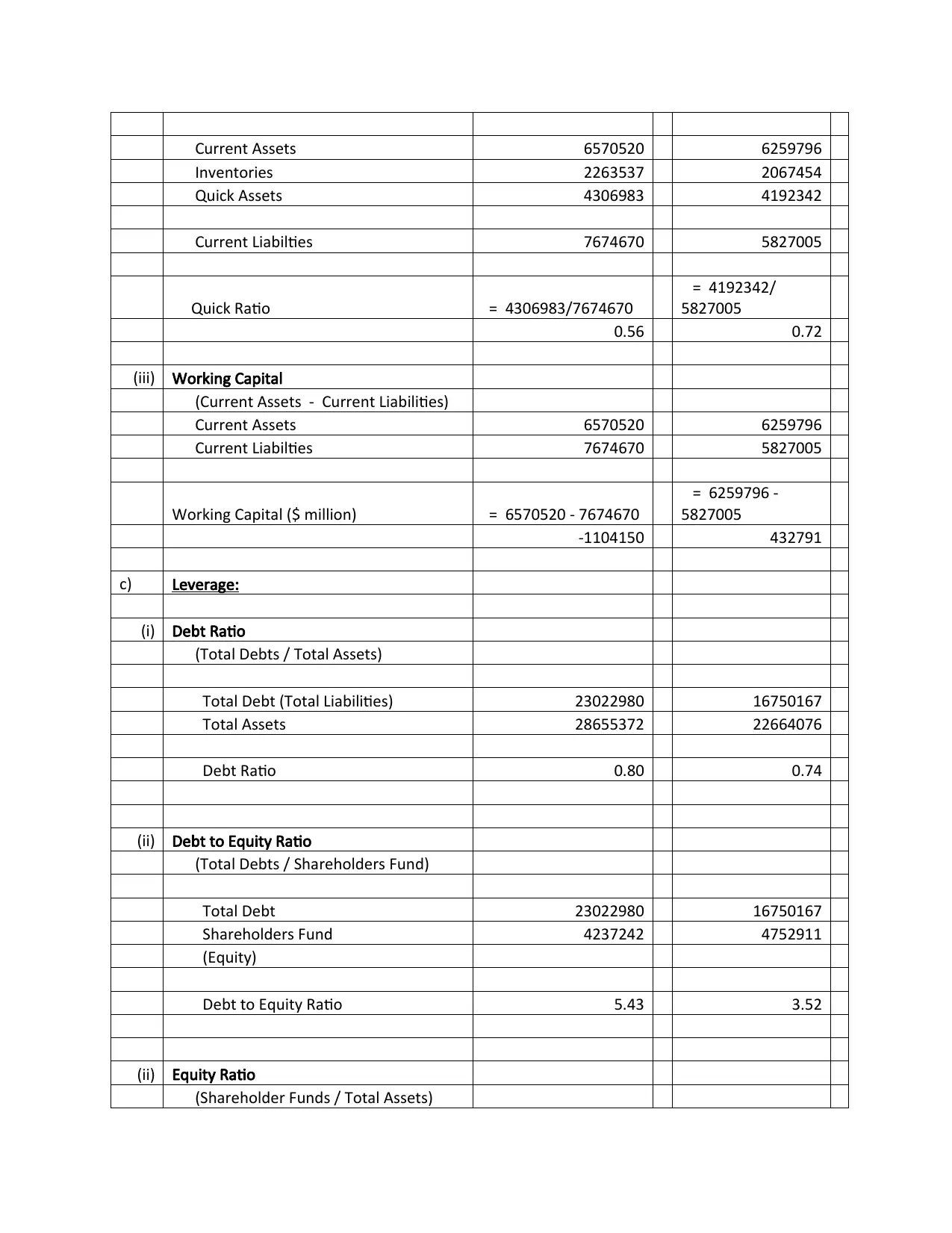

- Debt Ratio – It compares the total liabilities to the total assets of the company. It details

as to how much assets are there in paying the debt of the company. If the ratio is

decreasing then the capital structure of the company shall be regarded as less risky one

and in case the ratio is increasing then the capital structure of the company shall be

regarded as more risky one. In the given case, debt ratio has been increased from 0.74 in

the year 2016 to 0.80 in the year 2017. It means that the company has employed the high

risk capital structure which can any time prove as fatal to the organization.

- Debt to Equity Ratio – This ratio helps in making the comparison between the total

liabilities of the company and the total equity of the company including shareholders

funds and reserves and surplus. In the given case, Debt to equity ratio has been increased

from 3.52 in the year 2016 to 5.43 in the year 2017. The higher ratio is the alarming

situation for the company as higher the debt to equity ratio higher will be the chances that

company is at the risk of insolvency. Therefore, capital structure shall be maintained in

such a manner so as to avoid the situation of insolvency.

- Equity Ratio – Equity ratio details as to how much assets are related to the equity of the

company. Higher the ratio, lesser will be the chances of insolvency and lower the ratio,

higher will be the chances of insolvency. In the given case, Equity ratio has been

decreased from 0.21 in the year 2016 to 0.15 in the year 2017. Thus, the company has the

high risk of insolvency.

Efficiency Ratio – The efficiency ratio informs about the company as to how far the particular

assets or finance has been contributing towards the growth of the company. In other words, these

ratios helps in establishing the relationship between two items of the balance sheet and then the

contribution of one item towards the development of second item has been considered.

- Asset Turnover Ratio – This ratio helps in establishing the relationship between assets

and the turnover. It states that in what ratio the assets contribute towards the increase in

revenue. Higher the ratio, higher will be the efficiency of assets in generating revenue

and lower the ratio, lower will be the efficiency of assets and hence turnover will be less.

In the given case, asset turnover ratio has been decreased from 0.56 in the year 2016 to

0.46 in the year 2017. Therefore, the efficiency level is less.

as to how much assets are there in paying the debt of the company. If the ratio is

decreasing then the capital structure of the company shall be regarded as less risky one

and in case the ratio is increasing then the capital structure of the company shall be

regarded as more risky one. In the given case, debt ratio has been increased from 0.74 in

the year 2016 to 0.80 in the year 2017. It means that the company has employed the high

risk capital structure which can any time prove as fatal to the organization.

- Debt to Equity Ratio – This ratio helps in making the comparison between the total

liabilities of the company and the total equity of the company including shareholders

funds and reserves and surplus. In the given case, Debt to equity ratio has been increased

from 3.52 in the year 2016 to 5.43 in the year 2017. The higher ratio is the alarming

situation for the company as higher the debt to equity ratio higher will be the chances that

company is at the risk of insolvency. Therefore, capital structure shall be maintained in

such a manner so as to avoid the situation of insolvency.

- Equity Ratio – Equity ratio details as to how much assets are related to the equity of the

company. Higher the ratio, lesser will be the chances of insolvency and lower the ratio,

higher will be the chances of insolvency. In the given case, Equity ratio has been

decreased from 0.21 in the year 2016 to 0.15 in the year 2017. Thus, the company has the

high risk of insolvency.

Efficiency Ratio – The efficiency ratio informs about the company as to how far the particular

assets or finance has been contributing towards the growth of the company. In other words, these

ratios helps in establishing the relationship between two items of the balance sheet and then the

contribution of one item towards the development of second item has been considered.

- Asset Turnover Ratio – This ratio helps in establishing the relationship between assets

and the turnover. It states that in what ratio the assets contribute towards the increase in

revenue. Higher the ratio, higher will be the efficiency of assets in generating revenue

and lower the ratio, lower will be the efficiency of assets and hence turnover will be less.

In the given case, asset turnover ratio has been decreased from 0.56 in the year 2016 to

0.46 in the year 2017. Therefore, the efficiency level is less.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Thus, in this manner, the analysis of the financial position of the company has been analyzed and

the overall opinion is that the financial position of the company is at high risk.

ANALYZING THE PERFORMANCE OF THE COMPANY

Extending the previous example, in case the appraisal of the same manager is required to be done

then it will be done on the basis of his or her performance over the concerned period. In the same

way as the financial position is judged by the balance sheet of the company, the financial

performance of the company is judged by the statement of the profit and loss of the company.

The balance sheet of the company is prepared at the end of the reporting period at the particular

date whereas the statement of the profit and loss has been prepared for the period ending

reporting period. It covers the whole period of twelve months from January 2017 to December

2017.

Financial performance will not help the users of the financial statements in assessing the growth

of the company but also help them to compare the same with previous year results so as to know

whether the company has made any growth from the past year to the current year or not. The

analysis of the financial performance of the company will be measured through the accounting

ratios under the heading of profitability and account observations under heading observations

and analysis of values (White, 2015). It wills details as to whether the company is in the

profitable situation or loss situation.

Observations - The profit and loss account of Tesla has shown the increase in revenue from

2016 to 2017 by $ 4758619. On the other hand, the cost of revenues that has been incurred to

have high revenue will also increase by $ 4135389. This will lead to increase in Gross Margin

which is $ 2222487 in 2017 as compared to $ 1599257 in 2016. The research and development

expense which is 12 % of revenue has been increased from $ 543665 in 2017 as compared to

2016. Interest expense for the year ended 31st December, 2017 has been increased by $ 272.4

million. In comparison to this other income which is generated from foreign exchange

transaction has shown a decrease of $ 236.7 in 2017. This leads to increase in net loss of $

2240578 in 2017 as against $ 773046 in 2016.

Analysis of Values in Profit and Loss - The revenue of the company has been increased due to

more automation in sales procedures by the company which is considered as positive step along

the overall opinion is that the financial position of the company is at high risk.

ANALYZING THE PERFORMANCE OF THE COMPANY

Extending the previous example, in case the appraisal of the same manager is required to be done

then it will be done on the basis of his or her performance over the concerned period. In the same

way as the financial position is judged by the balance sheet of the company, the financial

performance of the company is judged by the statement of the profit and loss of the company.

The balance sheet of the company is prepared at the end of the reporting period at the particular

date whereas the statement of the profit and loss has been prepared for the period ending

reporting period. It covers the whole period of twelve months from January 2017 to December

2017.

Financial performance will not help the users of the financial statements in assessing the growth

of the company but also help them to compare the same with previous year results so as to know

whether the company has made any growth from the past year to the current year or not. The

analysis of the financial performance of the company will be measured through the accounting

ratios under the heading of profitability and account observations under heading observations

and analysis of values (White, 2015). It wills details as to whether the company is in the

profitable situation or loss situation.

Observations - The profit and loss account of Tesla has shown the increase in revenue from

2016 to 2017 by $ 4758619. On the other hand, the cost of revenues that has been incurred to

have high revenue will also increase by $ 4135389. This will lead to increase in Gross Margin

which is $ 2222487 in 2017 as compared to $ 1599257 in 2016. The research and development

expense which is 12 % of revenue has been increased from $ 543665 in 2017 as compared to

2016. Interest expense for the year ended 31st December, 2017 has been increased by $ 272.4

million. In comparison to this other income which is generated from foreign exchange

transaction has shown a decrease of $ 236.7 in 2017. This leads to increase in net loss of $

2240578 in 2017 as against $ 773046 in 2016.

Analysis of Values in Profit and Loss - The revenue of the company has been increased due to

more automation in sales procedures by the company which is considered as positive step along

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

with increase in no of deliverable in vehicles by the company. The company cost to revenue in

comparison to revenue has also enhanced due to increase in volume of sales and also increase in

cost of maintenance services provided by the company. As the result, the gross margin has been

increased but has only to increased to cover up the variable costs of the company. The margin is

not contributing to net margin due to enhance of expenses for research and development and

interest expense which in turn helps in development of new products with enhanced volume but

ultimately not fulfilling the goal of stakeholder of profit maximization.

Profitability Ratio: To earn profit is the only motive of all the organization and is very

important for the survival of the company. It tells about the efficiency and effectiveness of the

operations of the company. The shareholders are interested in profit so as to know the increase in

return over the investment made, the creditors will be interested in knowing the ability of the

company to make the payment of the interest and the principal and even the managers of the

company are interested in knowing the profit as it is directly linked to their incentive and reward

plans. Following ratios have been detailed:

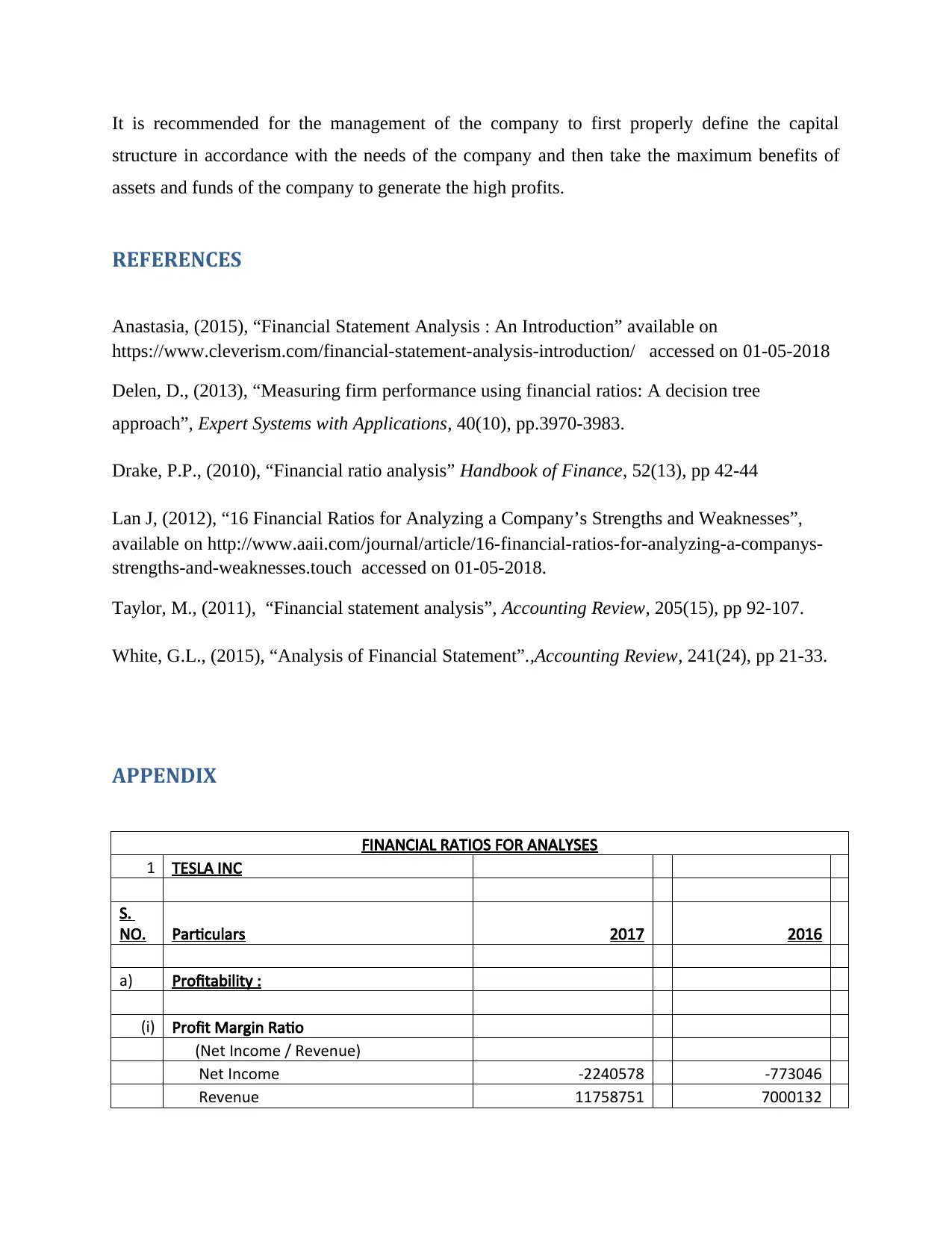

- Net Profit Margin – The net profit margin ratio helps in ascertaining the ability of the

company to generate profits from the sales made during the year. In the given case, the

net profit margin ratio has been decreased from negative 11.04% to negative 19.05%

from the year ending 2016 to 2017 respectively. It exhibits that the company has been

generating net loss at the end of the year and it further shows that company is not able to

generate the profits from the sales so as to set off the expenditure if any pending in this

regard. Thus, the company is working at loss from the last year.

- Return on Assets – This ratio helps in establishing the relationship by comparing the net

profit earned by the company during the year with the total assets of the company. It

basically represents the ability of the company to generate profits from the own assets of

the company. The deciding factor under this ratio is that higher the return on assets higher

will be the contribution of the assets in generating the net profit of the company and

lower the return on assets lower will be the contribution of the assets in generating the net

profit of the company (Lan, 2012). In the given case, the return on assets has been

decreased from negative 3.41% in the year ending 31st of December 2016 to negative

7.82% in the year ending 31st of December 2017. It exhibits that the company’s assets

comparison to revenue has also enhanced due to increase in volume of sales and also increase in

cost of maintenance services provided by the company. As the result, the gross margin has been

increased but has only to increased to cover up the variable costs of the company. The margin is

not contributing to net margin due to enhance of expenses for research and development and

interest expense which in turn helps in development of new products with enhanced volume but

ultimately not fulfilling the goal of stakeholder of profit maximization.

Profitability Ratio: To earn profit is the only motive of all the organization and is very

important for the survival of the company. It tells about the efficiency and effectiveness of the

operations of the company. The shareholders are interested in profit so as to know the increase in

return over the investment made, the creditors will be interested in knowing the ability of the

company to make the payment of the interest and the principal and even the managers of the

company are interested in knowing the profit as it is directly linked to their incentive and reward

plans. Following ratios have been detailed:

- Net Profit Margin – The net profit margin ratio helps in ascertaining the ability of the

company to generate profits from the sales made during the year. In the given case, the

net profit margin ratio has been decreased from negative 11.04% to negative 19.05%

from the year ending 2016 to 2017 respectively. It exhibits that the company has been

generating net loss at the end of the year and it further shows that company is not able to

generate the profits from the sales so as to set off the expenditure if any pending in this

regard. Thus, the company is working at loss from the last year.

- Return on Assets – This ratio helps in establishing the relationship by comparing the net

profit earned by the company during the year with the total assets of the company. It

basically represents the ability of the company to generate profits from the own assets of

the company. The deciding factor under this ratio is that higher the return on assets higher

will be the contribution of the assets in generating the net profit of the company and

lower the return on assets lower will be the contribution of the assets in generating the net

profit of the company (Lan, 2012). In the given case, the return on assets has been

decreased from negative 3.41% in the year ending 31st of December 2016 to negative

7.82% in the year ending 31st of December 2017. It exhibits that the company’s assets

are not being utilized in the effective and efficient manner through which the return on

assets have been decreased.

- Return on Equity - This ratio helps in establishing the relationship by comparing the net

profit earned by the company during the year with the shareholders equity of the

company. It basically represents the ability of the company to generate profits from the

funds provided by the shareholders of the company. The deciding factor under this ratio

is that higher the return on equity higher will be the contribution of the assets in

generating the net profit of the company and lower the return on equity lower will be the

contribution of the assets in generating the net profit of the company. In the given case,

the return on equity has been decreased from negative 16.26% in the year ending 31st of

December 2016 to negative 52.88% in the year ending 31st of December 2017. It shows

that the funds as provided by the shareholders of the company are not being utilized and

managed in the proper manner due to which the return on equity has become negative.

Thus, in this manner, the analysis of the financial performance of the company has been

analyzed and the overall opinion is that the financial performance of the company is very bad

and is not being controlled and managed in the defined manner.

CONCLUSION AND RECOMMENDATION

Financial statement forms the part of the annual report of the company. It plays very crucial role

from the eyes of the users of the financial statements. It is because of the fact that all the users of

the financial statements take their decision on the basis of that only. The report has analyzed in

detail the financial position and the financial performance of the company namely Tesla Inc. The

ratios showing the financial position has exhibited very clearly that the company is in higher risk

in relation to the liquidity as well the solvency. It means the company can become the insolvent

at any time. Similarly the negative impact has been seen in the statement of the profit and loss

showing the financial performance of the company. In order to conclude the report, the financial

position and the financial performance of the company is so bad that neither any investors nor

any potential investor will be happy o make an investment in the company.

assets have been decreased.

- Return on Equity - This ratio helps in establishing the relationship by comparing the net

profit earned by the company during the year with the shareholders equity of the

company. It basically represents the ability of the company to generate profits from the

funds provided by the shareholders of the company. The deciding factor under this ratio

is that higher the return on equity higher will be the contribution of the assets in

generating the net profit of the company and lower the return on equity lower will be the

contribution of the assets in generating the net profit of the company. In the given case,

the return on equity has been decreased from negative 16.26% in the year ending 31st of

December 2016 to negative 52.88% in the year ending 31st of December 2017. It shows

that the funds as provided by the shareholders of the company are not being utilized and

managed in the proper manner due to which the return on equity has become negative.

Thus, in this manner, the analysis of the financial performance of the company has been

analyzed and the overall opinion is that the financial performance of the company is very bad

and is not being controlled and managed in the defined manner.

CONCLUSION AND RECOMMENDATION

Financial statement forms the part of the annual report of the company. It plays very crucial role

from the eyes of the users of the financial statements. It is because of the fact that all the users of

the financial statements take their decision on the basis of that only. The report has analyzed in

detail the financial position and the financial performance of the company namely Tesla Inc. The

ratios showing the financial position has exhibited very clearly that the company is in higher risk

in relation to the liquidity as well the solvency. It means the company can become the insolvent

at any time. Similarly the negative impact has been seen in the statement of the profit and loss

showing the financial performance of the company. In order to conclude the report, the financial

position and the financial performance of the company is so bad that neither any investors nor

any potential investor will be happy o make an investment in the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is recommended for the management of the company to first properly define the capital

structure in accordance with the needs of the company and then take the maximum benefits of

assets and funds of the company to generate the high profits.

REFERENCES

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 01-05-2018

Delen, D., (2013), “Measuring firm performance using financial ratios: A decision tree

approach”, Expert Systems with Applications, 40(10), pp.3970-3983.

Drake, P.P., (2010), “Financial ratio analysis” Handbook of Finance, 52(13), pp 42-44

Lan J, (2012), “16 Financial Ratios for Analyzing a Company’s Strengths and Weaknesses”,

available on http://www.aaii.com/journal/article/16-financial-ratios-for-analyzing-a-companys-

strengths-and-weaknesses.touch accessed on 01-05-2018.

Taylor, M., (2011), “Financial statement analysis”, Accounting Review, 205(15), pp 92-107.

White, G.L., (2015), “Analysis of Financial Statement”.,Accounting Review, 241(24), pp 21-33.

APPENDIX

FINANCIAL RATIOS FOR ANALYSES

1 TESLA INC

S.

NO. Particulars 2017 2016

a) Profitability :

(i) Profit Margin Ratio

(Net Income / Revenue)

Net Income -2240578 -773046

Revenue 11758751 7000132

structure in accordance with the needs of the company and then take the maximum benefits of

assets and funds of the company to generate the high profits.

REFERENCES

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 01-05-2018

Delen, D., (2013), “Measuring firm performance using financial ratios: A decision tree

approach”, Expert Systems with Applications, 40(10), pp.3970-3983.

Drake, P.P., (2010), “Financial ratio analysis” Handbook of Finance, 52(13), pp 42-44

Lan J, (2012), “16 Financial Ratios for Analyzing a Company’s Strengths and Weaknesses”,

available on http://www.aaii.com/journal/article/16-financial-ratios-for-analyzing-a-companys-

strengths-and-weaknesses.touch accessed on 01-05-2018.

Taylor, M., (2011), “Financial statement analysis”, Accounting Review, 205(15), pp 92-107.

White, G.L., (2015), “Analysis of Financial Statement”.,Accounting Review, 241(24), pp 21-33.

APPENDIX

FINANCIAL RATIOS FOR ANALYSES

1 TESLA INC

S.

NO. Particulars 2017 2016

a) Profitability :

(i) Profit Margin Ratio

(Net Income / Revenue)

Net Income -2240578 -773046

Revenue 11758751 7000132

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit Margin

= -

2240578/11758751*10

0

= -

773046/7000132*100

-19.05% -11.04%

(ii) Return on Assets

(Net Income / Total Assets)

Net Income -2240578 -773046

Total Assets 28655372 22664076

Return on Asset

= -

2240578/28655372*10

0

= -

773046/22664076*10

0

-7.82% -3.41%

(iii) Return on Equity

(Net Income / Shareholder's Equity)

Net Income -2240578 -773046

Shareholders's Equity 4237242 4752911

Return on Equity

= -

2240578/4237242*100

= -

773046/4752911*100

-52.88% -16.26%

b) Liquidity :

(i) Current Ratio

(Current Assets / Current Liabilities)

Current Assets 6570520 6259796

Current Liabilties 7674670 5827005

Current Ratio = 6570520/7674670

= 6259796 /

5827005

0.86 1.07

(ii) Quick Ratio

(Quick Assets / Current Liabilities)

Quick Assets (Current Assets -

Inventories)

= -

2240578/11758751*10

0

= -

773046/7000132*100

-19.05% -11.04%

(ii) Return on Assets

(Net Income / Total Assets)

Net Income -2240578 -773046

Total Assets 28655372 22664076

Return on Asset

= -

2240578/28655372*10

0

= -

773046/22664076*10

0

-7.82% -3.41%

(iii) Return on Equity

(Net Income / Shareholder's Equity)

Net Income -2240578 -773046

Shareholders's Equity 4237242 4752911

Return on Equity

= -

2240578/4237242*100

= -

773046/4752911*100

-52.88% -16.26%

b) Liquidity :

(i) Current Ratio

(Current Assets / Current Liabilities)

Current Assets 6570520 6259796

Current Liabilties 7674670 5827005

Current Ratio = 6570520/7674670

= 6259796 /

5827005

0.86 1.07

(ii) Quick Ratio

(Quick Assets / Current Liabilities)

Quick Assets (Current Assets -

Inventories)

Current Assets 6570520 6259796

Inventories 2263537 2067454

Quick Assets 4306983 4192342

Current Liabilties 7674670 5827005

Quick Ratio = 4306983/7674670

= 4192342/

5827005

0.56 0.72

(iii) Working Capital

(Current Assets - Current Liabilities)

Current Assets 6570520 6259796

Current Liabilties 7674670 5827005

Working Capital ($ million) = 6570520 - 7674670

= 6259796 -

5827005

-1104150 432791

c) Leverage:

(i) Debt Ratio

(Total Debts / Total Assets)

Total Debt (Total Liabilities) 23022980 16750167

Total Assets 28655372 22664076

Debt Ratio 0.80 0.74

(ii) Debt to Equity Ratio

(Total Debts / Shareholders Fund)

Total Debt 23022980 16750167

Shareholders Fund 4237242 4752911

(Equity)

Debt to Equity Ratio 5.43 3.52

(ii) Equity Ratio

(Shareholder Funds / Total Assets)

Inventories 2263537 2067454

Quick Assets 4306983 4192342

Current Liabilties 7674670 5827005

Quick Ratio = 4306983/7674670

= 4192342/

5827005

0.56 0.72

(iii) Working Capital

(Current Assets - Current Liabilities)

Current Assets 6570520 6259796

Current Liabilties 7674670 5827005

Working Capital ($ million) = 6570520 - 7674670

= 6259796 -

5827005

-1104150 432791

c) Leverage:

(i) Debt Ratio

(Total Debts / Total Assets)

Total Debt (Total Liabilities) 23022980 16750167

Total Assets 28655372 22664076

Debt Ratio 0.80 0.74

(ii) Debt to Equity Ratio

(Total Debts / Shareholders Fund)

Total Debt 23022980 16750167

Shareholders Fund 4237242 4752911

(Equity)

Debt to Equity Ratio 5.43 3.52

(ii) Equity Ratio

(Shareholder Funds / Total Assets)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.